IFRS Goodwill Accounting and Reporting

VerifiedAdded on 2020/05/16

|15

|2989

|37

AI Summary

This assignment delves into the complexities of International Financial Reporting Standards (IFRS) related to goodwill accounting and reporting. It requires an analysis of various aspects, including compliance with disclosure requirements, the effectiveness of impairment testing procedures, and potential challenges faced by companies in applying IFRS guidelines. The analysis should draw upon relevant academic literature and case studies to provide a comprehensive understanding of the topic.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: ADVANCE FINANCE IMPAIRMENT

ADVANCE FINANCE IMPAIRMENT

Name of the student

Name of the university

Author Note

ADVANCE FINANCE IMPAIRMENT

Name of the student

Name of the university

Author Note

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1ADVANCE FINANCE IMPAIRMENT

Table of Contents

Assessment task Part A....................................................................................................................3

(i) Assets tested for impairment.............................................................................................3

(ii) Method of conducting impairment test.............................................................................4

(iii) Impairment expenditures...................................................................................................5

(iv) Assumptions and estimates used by the company for conducting impairment test..........6

(v) Subjectivity involved in the process of impairment testing..............................................7

(vi) Interesting, surprising, difficult or confusing part to understand impairment testing.......7

(vii) New insights regarding conducting the impairment.........................................................8

(viii) Fair value measurement.................................................................................................8

Assessment task Part B....................................................................................................................9

(i) Reason why the former accounting standards does not reflect the economic reality.......9

(ii) Reasons why under the previous accounting standards the lease liabilities of the

reporting entities in the balance sheet were 66 times more than the reported debts under the

balance sheet................................................................................................................................9

(iii) Reasons why the Chairperson of IASB is in the view that under the previous accounting

standard no level playing field was there among some airline entities.....................................10

(iv) Reasons why the Chairperson is in the view that the new standard will not be popular

with everyone.............................................................................................................................10

Table of Contents

Assessment task Part A....................................................................................................................3

(i) Assets tested for impairment.............................................................................................3

(ii) Method of conducting impairment test.............................................................................4

(iii) Impairment expenditures...................................................................................................5

(iv) Assumptions and estimates used by the company for conducting impairment test..........6

(v) Subjectivity involved in the process of impairment testing..............................................7

(vi) Interesting, surprising, difficult or confusing part to understand impairment testing.......7

(vii) New insights regarding conducting the impairment.........................................................8

(viii) Fair value measurement.................................................................................................8

Assessment task Part B....................................................................................................................9

(i) Reason why the former accounting standards does not reflect the economic reality.......9

(ii) Reasons why under the previous accounting standards the lease liabilities of the

reporting entities in the balance sheet were 66 times more than the reported debts under the

balance sheet................................................................................................................................9

(iii) Reasons why the Chairperson of IASB is in the view that under the previous accounting

standard no level playing field was there among some airline entities.....................................10

(iv) Reasons why the Chairperson is in the view that the new standard will not be popular

with everyone.............................................................................................................................10

2ADVANCE FINANCE IMPAIRMENT

(v) Possibilities that the new visibility with regard to all the leases will result into better

informed decision for investment..............................................................................................11

References......................................................................................................................................12

(v) Possibilities that the new visibility with regard to all the leases will result into better

informed decision for investment..............................................................................................11

References......................................................................................................................................12

3ADVANCE FINANCE IMPAIRMENT

Assessment task Part A

The main aim of this report is to focus on the disorder benchmark as well as the

assumptions, which have been implemented by the given company called, Campbell Brothers

Limited. It is a testing service providing company. At first, it was named as Campbell Brothers

and later they changed it to ALS Limited. The company is based in Australia and the company is

a soap and chemical manufacturing company that is listed under the Australian Stock exchange

(Alsglobal.com 2018). The company has its main operations in 4 major divisions, ranging from

the Industrials, Energy, Life Sciences and Minerals. It is one of the largest testing and analytical

groups of companies around the world.

While accounting for a company, the financial asset of a company is assessed at a given

reporting period in order to give evidence in case the asset is impaired. In accounting terms, an

asset is considered impaired or disordered during the time when the evidences that have been

earlier collected expresses that several events that have taken place in the course of business is

negatively influencing the cash flow values for the future. In such cases, definite impairment

charges are required to be taken and the loss needs are to be calculated (AmirALSani, Iatridis

and Pope 2013). An impairment loss is with respect to the financial or non-financial assets that is

measured at an amortized cost. The amortized cost is the contrast in between the present value of

the asset that is reckoned, and the carrying cost. However, there are certain assets that are

impaired individually, and certain assets are impaired in groups.

(i) Assets that are tested for impairment

As witnessed from the annual reports of the company for the year ended as on 31 March

2016.

Assessment task Part A

The main aim of this report is to focus on the disorder benchmark as well as the

assumptions, which have been implemented by the given company called, Campbell Brothers

Limited. It is a testing service providing company. At first, it was named as Campbell Brothers

and later they changed it to ALS Limited. The company is based in Australia and the company is

a soap and chemical manufacturing company that is listed under the Australian Stock exchange

(Alsglobal.com 2018). The company has its main operations in 4 major divisions, ranging from

the Industrials, Energy, Life Sciences and Minerals. It is one of the largest testing and analytical

groups of companies around the world.

While accounting for a company, the financial asset of a company is assessed at a given

reporting period in order to give evidence in case the asset is impaired. In accounting terms, an

asset is considered impaired or disordered during the time when the evidences that have been

earlier collected expresses that several events that have taken place in the course of business is

negatively influencing the cash flow values for the future. In such cases, definite impairment

charges are required to be taken and the loss needs are to be calculated (AmirALSani, Iatridis

and Pope 2013). An impairment loss is with respect to the financial or non-financial assets that is

measured at an amortized cost. The amortized cost is the contrast in between the present value of

the asset that is reckoned, and the carrying cost. However, there are certain assets that are

impaired individually, and certain assets are impaired in groups.

(i) Assets that are tested for impairment

As witnessed from the annual reports of the company for the year ended as on 31 March

2016.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4ADVANCE FINANCE IMPAIRMENT

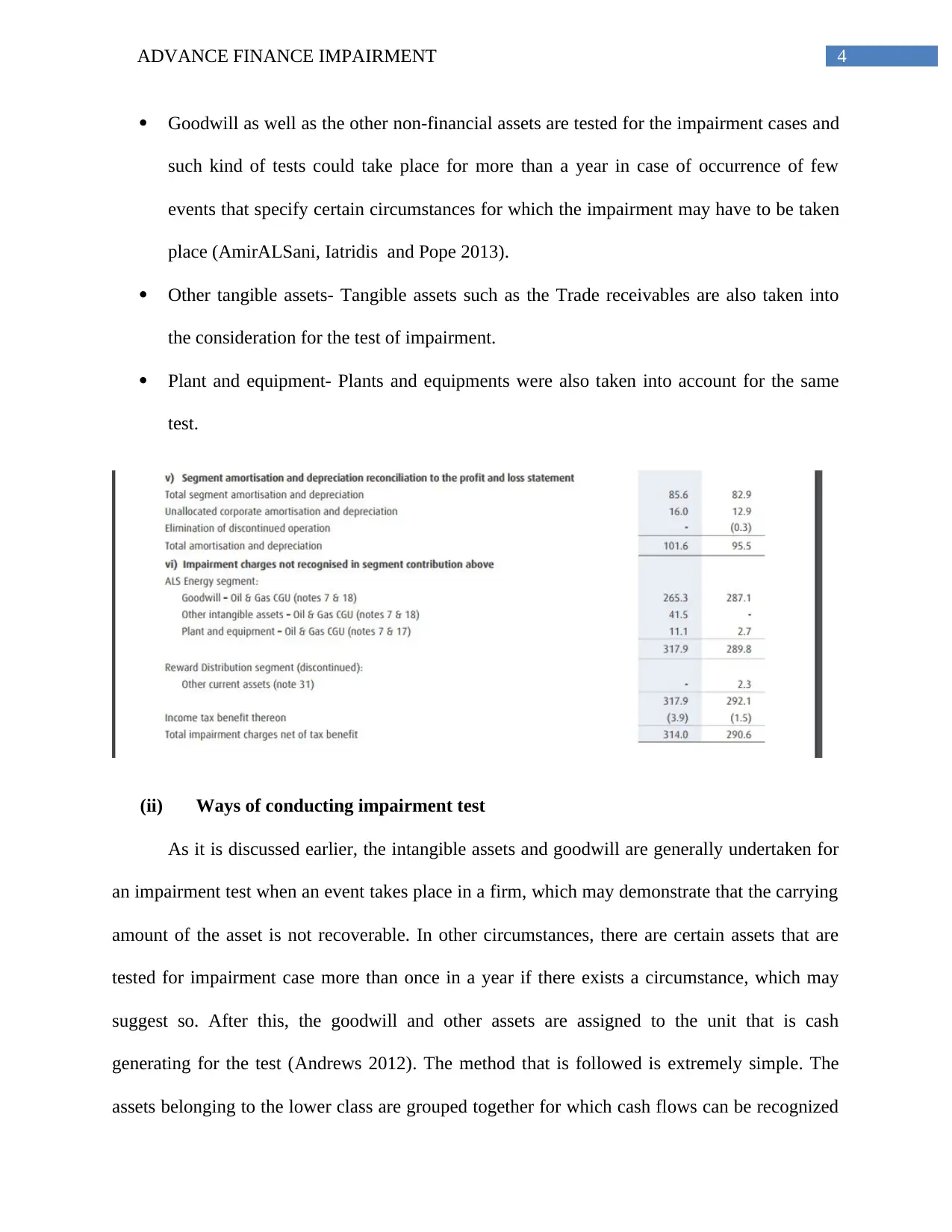

Goodwill as well as the other non-financial assets are tested for the impairment cases and

such kind of tests could take place for more than a year in case of occurrence of few

events that specify certain circumstances for which the impairment may have to be taken

place (AmirALSani, Iatridis and Pope 2013).

Other tangible assets- Tangible assets such as the Trade receivables are also taken into

the consideration for the test of impairment.

Plant and equipment- Plants and equipments were also taken into account for the same

test.

(ii) Ways of conducting impairment test

As it is discussed earlier, the intangible assets and goodwill are generally undertaken for

an impairment test when an event takes place in a firm, which may demonstrate that the carrying

amount of the asset is not recoverable. In other circumstances, there are certain assets that are

tested for impairment case more than once in a year if there exists a circumstance, which may

suggest so. After this, the goodwill and other assets are assigned to the unit that is cash

generating for the test (Andrews 2012). The method that is followed is extremely simple. The

assets belonging to the lower class are grouped together for which cash flows can be recognized

Goodwill as well as the other non-financial assets are tested for the impairment cases and

such kind of tests could take place for more than a year in case of occurrence of few

events that specify certain circumstances for which the impairment may have to be taken

place (AmirALSani, Iatridis and Pope 2013).

Other tangible assets- Tangible assets such as the Trade receivables are also taken into

the consideration for the test of impairment.

Plant and equipment- Plants and equipments were also taken into account for the same

test.

(ii) Ways of conducting impairment test

As it is discussed earlier, the intangible assets and goodwill are generally undertaken for

an impairment test when an event takes place in a firm, which may demonstrate that the carrying

amount of the asset is not recoverable. In other circumstances, there are certain assets that are

tested for impairment case more than once in a year if there exists a circumstance, which may

suggest so. After this, the goodwill and other assets are assigned to the unit that is cash

generating for the test (Andrews 2012). The method that is followed is extremely simple. The

assets belonging to the lower class are grouped together for which cash flows can be recognized

5ADVANCE FINANCE IMPAIRMENT

separately and for the assets, which are not based on these, are grouped different. Except

goodwill, all other assets that have undergone the impairment have the chance of reversal as

according to the date at which the reporting is done.

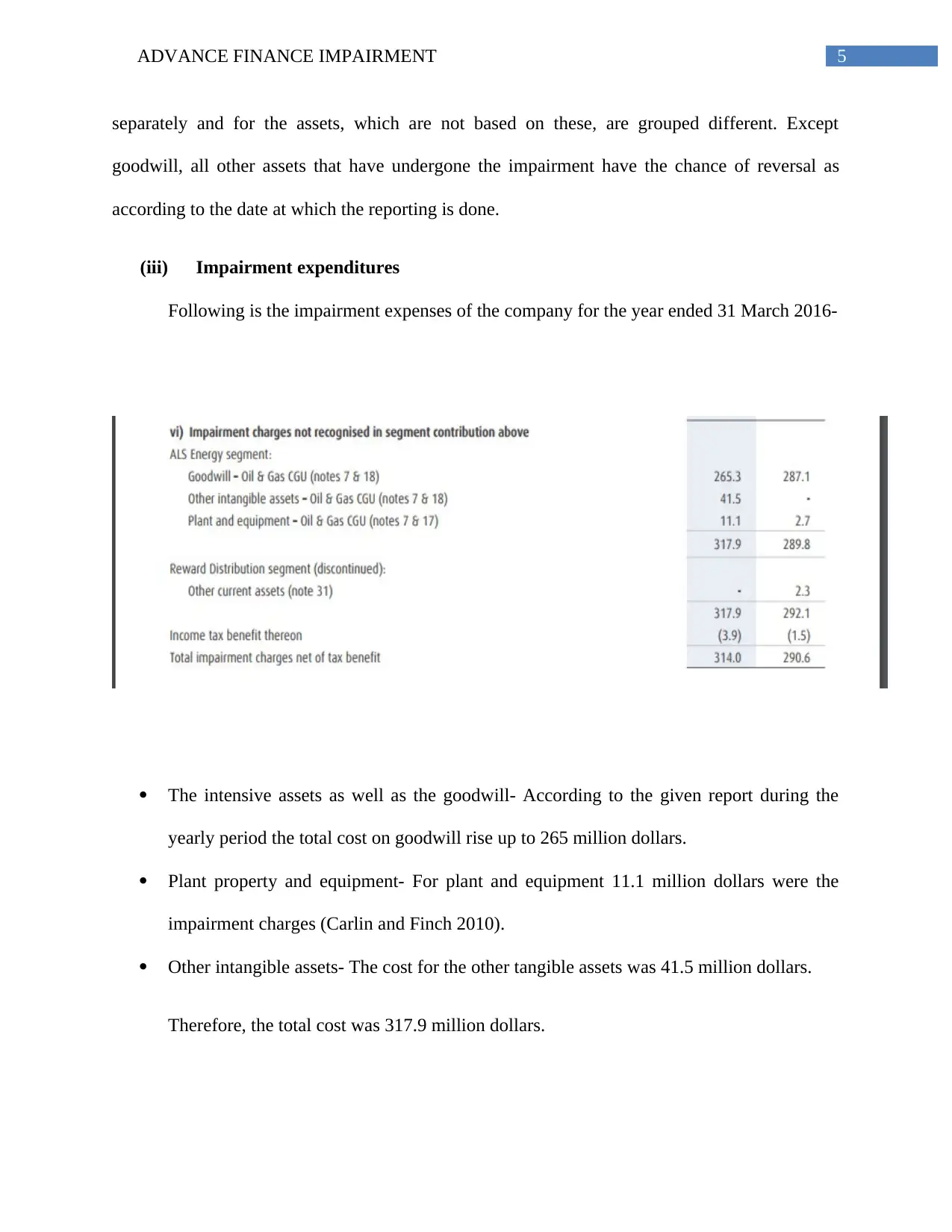

(iii) Impairment expenditures

Following is the impairment expenses of the company for the year ended 31 March 2016-

The intensive assets as well as the goodwill- According to the given report during the

yearly period the total cost on goodwill rise up to 265 million dollars.

Plant property and equipment- For plant and equipment 11.1 million dollars were the

impairment charges (Carlin and Finch 2010).

Other intangible assets- The cost for the other tangible assets was 41.5 million dollars.

Therefore, the total cost was 317.9 million dollars.

separately and for the assets, which are not based on these, are grouped different. Except

goodwill, all other assets that have undergone the impairment have the chance of reversal as

according to the date at which the reporting is done.

(iii) Impairment expenditures

Following is the impairment expenses of the company for the year ended 31 March 2016-

The intensive assets as well as the goodwill- According to the given report during the

yearly period the total cost on goodwill rise up to 265 million dollars.

Plant property and equipment- For plant and equipment 11.1 million dollars were the

impairment charges (Carlin and Finch 2010).

Other intangible assets- The cost for the other tangible assets was 41.5 million dollars.

Therefore, the total cost was 317.9 million dollars.

6ADVANCE FINANCE IMPAIRMENT

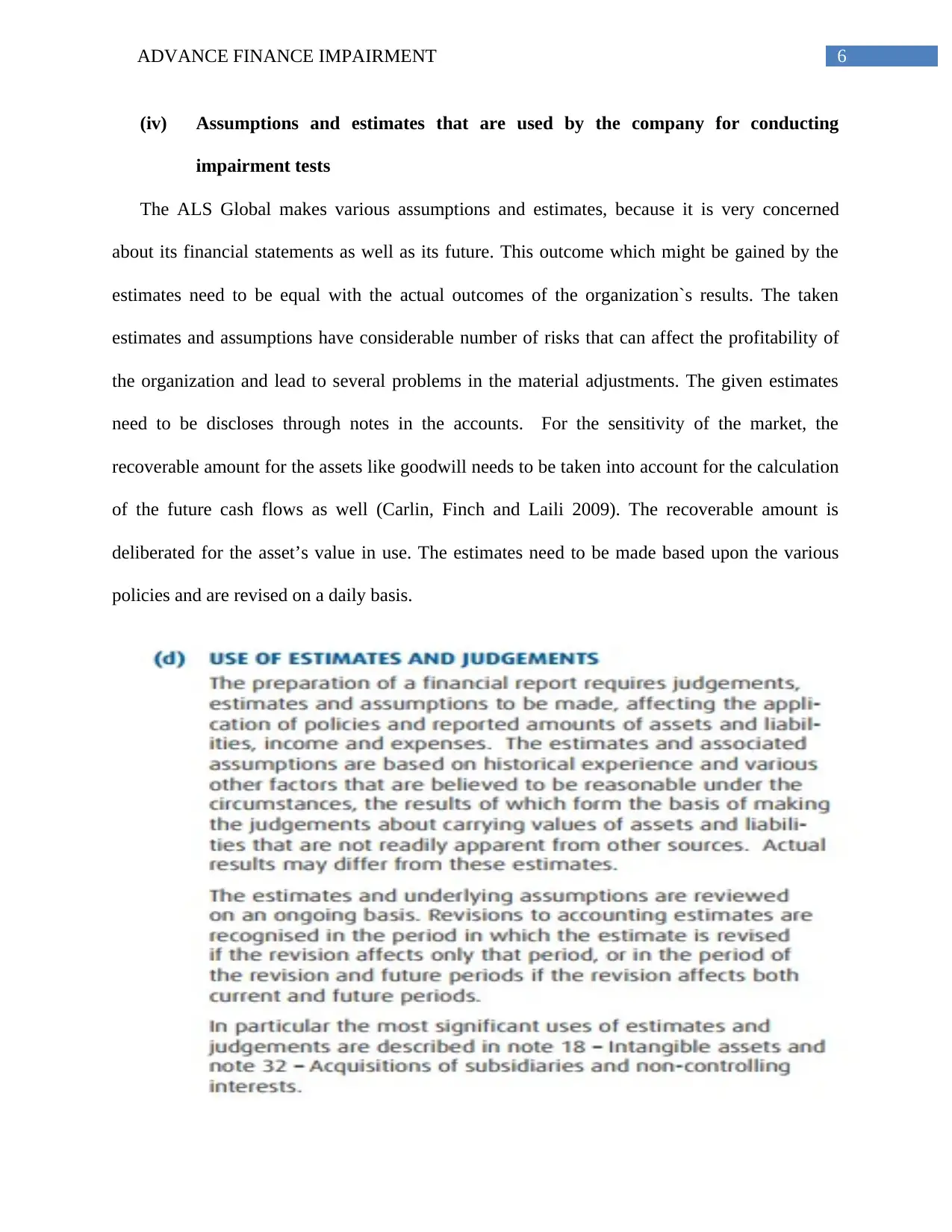

(iv) Assumptions and estimates that are used by the company for conducting

impairment tests

The ALS Global makes various assumptions and estimates, because it is very concerned

about its financial statements as well as its future. This outcome which might be gained by the

estimates need to be equal with the actual outcomes of the organization`s results. The taken

estimates and assumptions have considerable number of risks that can affect the profitability of

the organization and lead to several problems in the material adjustments. The given estimates

need to be discloses through notes in the accounts. For the sensitivity of the market, the

recoverable amount for the assets like goodwill needs to be taken into account for the calculation

of the future cash flows as well (Carlin, Finch and Laili 2009). The recoverable amount is

deliberated for the asset’s value in use. The estimates need to be made based upon the various

policies and are revised on a daily basis.

(iv) Assumptions and estimates that are used by the company for conducting

impairment tests

The ALS Global makes various assumptions and estimates, because it is very concerned

about its financial statements as well as its future. This outcome which might be gained by the

estimates need to be equal with the actual outcomes of the organization`s results. The taken

estimates and assumptions have considerable number of risks that can affect the profitability of

the organization and lead to several problems in the material adjustments. The given estimates

need to be discloses through notes in the accounts. For the sensitivity of the market, the

recoverable amount for the assets like goodwill needs to be taken into account for the calculation

of the future cash flows as well (Carlin, Finch and Laili 2009). The recoverable amount is

deliberated for the asset’s value in use. The estimates need to be made based upon the various

policies and are revised on a daily basis.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7ADVANCE FINANCE IMPAIRMENT

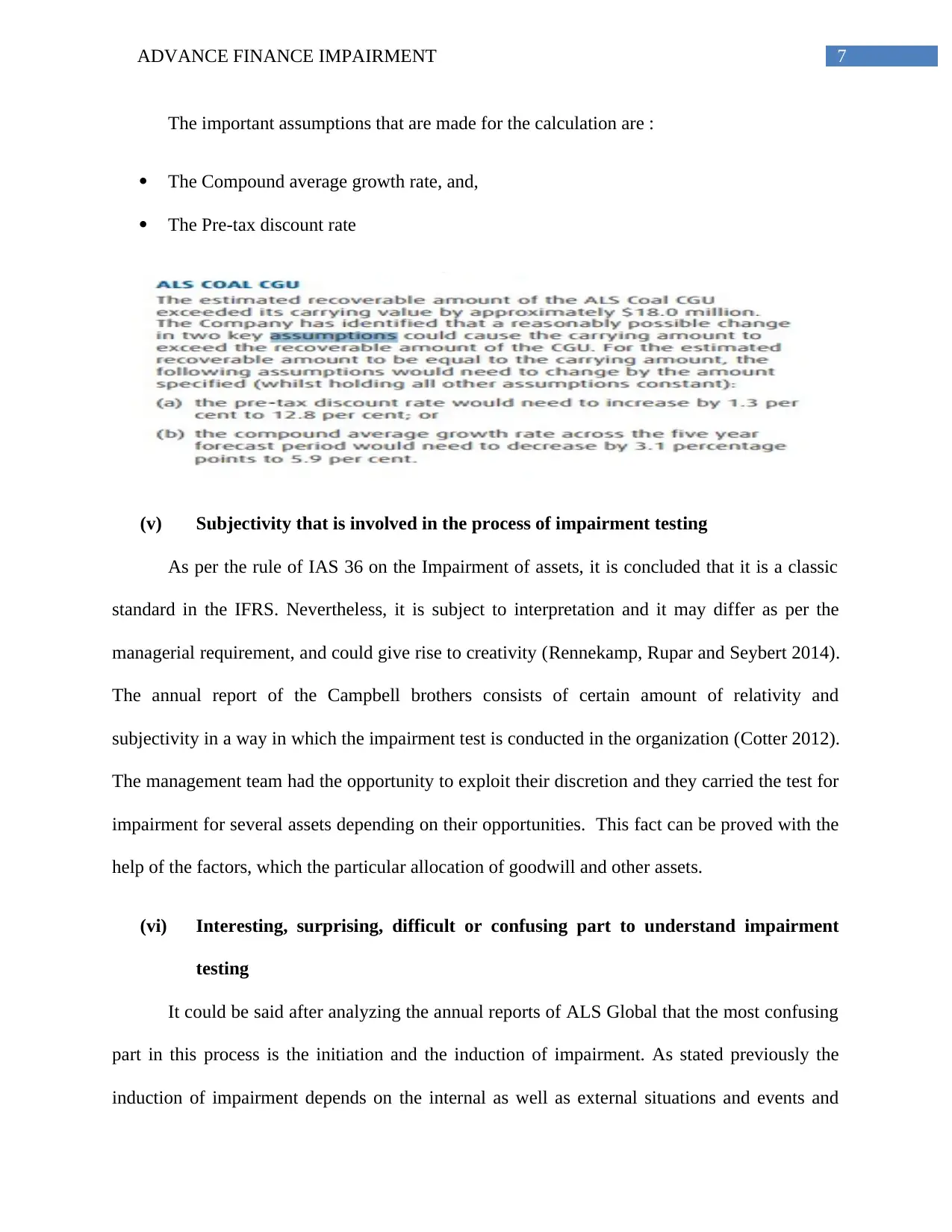

The important assumptions that are made for the calculation are :

The Compound average growth rate, and,

The Pre-tax discount rate

(v) Subjectivity that is involved in the process of impairment testing

As per the rule of IAS 36 on the Impairment of assets, it is concluded that it is a classic

standard in the IFRS. Nevertheless, it is subject to interpretation and it may differ as per the

managerial requirement, and could give rise to creativity (Rennekamp, Rupar and Seybert 2014).

The annual report of the Campbell brothers consists of certain amount of relativity and

subjectivity in a way in which the impairment test is conducted in the organization (Cotter 2012).

The management team had the opportunity to exploit their discretion and they carried the test for

impairment for several assets depending on their opportunities. This fact can be proved with the

help of the factors, which the particular allocation of goodwill and other assets.

(vi) Interesting, surprising, difficult or confusing part to understand impairment

testing

It could be said after analyzing the annual reports of ALS Global that the most confusing

part in this process is the initiation and the induction of impairment. As stated previously the

induction of impairment depends on the internal as well as external situations and events and

The important assumptions that are made for the calculation are :

The Compound average growth rate, and,

The Pre-tax discount rate

(v) Subjectivity that is involved in the process of impairment testing

As per the rule of IAS 36 on the Impairment of assets, it is concluded that it is a classic

standard in the IFRS. Nevertheless, it is subject to interpretation and it may differ as per the

managerial requirement, and could give rise to creativity (Rennekamp, Rupar and Seybert 2014).

The annual report of the Campbell brothers consists of certain amount of relativity and

subjectivity in a way in which the impairment test is conducted in the organization (Cotter 2012).

The management team had the opportunity to exploit their discretion and they carried the test for

impairment for several assets depending on their opportunities. This fact can be proved with the

help of the factors, which the particular allocation of goodwill and other assets.

(vi) Interesting, surprising, difficult or confusing part to understand impairment

testing

It could be said after analyzing the annual reports of ALS Global that the most confusing

part in this process is the initiation and the induction of impairment. As stated previously the

induction of impairment depends on the internal as well as external situations and events and

8ADVANCE FINANCE IMPAIRMENT

with the same, on the frequency of the test is depending completely on the discretion of the

management (Fitó, Moya and Orgaz 2013). Due to this fact, in the discretion of the management,

there might be the chances that the impairment that are generally undertaken, is either subjective

or many depend on the choice of the management. Hence, as stated above there exists chances

that the management might carry out the test depending on these opportunities that are available

and utilized the impairment option when there is a slump in the value of the given asset.

(vii) New insights concerning conducting of the impairment tests

The impairment loss can be referred to as the difference between carrying amount of the

given asset and recoverable amount of the asset. When the recoverable amount of the asset in

cases where the value in use comes into picture, is higher than it may be in the case where the

value of the asset is decreased to the disposable cost (Lee and Hooy 2013). The fair value of an

asset is determined through the sales agreement or the value of the asset that has been taken from

the market where the particular asset is usual, traded. In other cases, the value as per the rule of

IAS 36, can be described as the present value of the cash flows that might take place in future

from the asset.

(viii) Fair value measurement

According to the new IFRS 13, the fair value of an asset is determined through-

The sales agreement.

The value of the asset in the market where it is traded (Ifrs.org. 2018).

with the same, on the frequency of the test is depending completely on the discretion of the

management (Fitó, Moya and Orgaz 2013). Due to this fact, in the discretion of the management,

there might be the chances that the impairment that are generally undertaken, is either subjective

or many depend on the choice of the management. Hence, as stated above there exists chances

that the management might carry out the test depending on these opportunities that are available

and utilized the impairment option when there is a slump in the value of the given asset.

(vii) New insights concerning conducting of the impairment tests

The impairment loss can be referred to as the difference between carrying amount of the

given asset and recoverable amount of the asset. When the recoverable amount of the asset in

cases where the value in use comes into picture, is higher than it may be in the case where the

value of the asset is decreased to the disposable cost (Lee and Hooy 2013). The fair value of an

asset is determined through the sales agreement or the value of the asset that has been taken from

the market where the particular asset is usual, traded. In other cases, the value as per the rule of

IAS 36, can be described as the present value of the cash flows that might take place in future

from the asset.

(viii) Fair value measurement

According to the new IFRS 13, the fair value of an asset is determined through-

The sales agreement.

The value of the asset in the market where it is traded (Ifrs.org. 2018).

9ADVANCE FINANCE IMPAIRMENT

Assessment task Part B

(i) The reason why the former accounting standards does not reflect the economic

reality

It is believed that about every one out of two companies that make the use of US GAAP

or IFRS in its business have been affected by the various different changes and alterations, which

have taken place in a given year. According to today’s scenario, the companies who are

registered under US GAAP or IFRS have near about 3.3 trillion dollars worth leased assets and

other commitments. Out of these, near about two-third of the total data is not reported in the

balance sheet. This is due to the fact that, they are often treated as operating leases ( Jennings and

Marques 2013). In order to compensate such loss the investors normally include those estimates

that are just a prediction. These are incomparable and inaccurate computations. Therefore, it is

often reflected that the accounting standards that were used before, did not reflect the economic

reality.

(ii) Reasons why under the previous accounting standards the lease liabilities of the

reporting entities in the balance sheet were 66 times more than the reported

debts under the balance sheet

When the previous accounting standard was in use nearly 85 percent of the companies put

their leases amount under the operating leases instead of balance sheet. While these operating

leases were not recorded under the given balance sheet, they were able to create liabilities, which

were true (loans, retirement and education 2018). Hence, when financial crises will occur, there

were certain companies that were not able to adapt to the new systems and hence they went on a

Assessment task Part B

(i) The reason why the former accounting standards does not reflect the economic

reality

It is believed that about every one out of two companies that make the use of US GAAP

or IFRS in its business have been affected by the various different changes and alterations, which

have taken place in a given year. According to today’s scenario, the companies who are

registered under US GAAP or IFRS have near about 3.3 trillion dollars worth leased assets and

other commitments. Out of these, near about two-third of the total data is not reported in the

balance sheet. This is due to the fact that, they are often treated as operating leases ( Jennings and

Marques 2013). In order to compensate such loss the investors normally include those estimates

that are just a prediction. These are incomparable and inaccurate computations. Therefore, it is

often reflected that the accounting standards that were used before, did not reflect the economic

reality.

(ii) Reasons why under the previous accounting standards the lease liabilities of the

reporting entities in the balance sheet were 66 times more than the reported

debts under the balance sheet

When the previous accounting standard was in use nearly 85 percent of the companies put

their leases amount under the operating leases instead of balance sheet. While these operating

leases were not recorded under the given balance sheet, they were able to create liabilities, which

were true (loans, retirement and education 2018). Hence, when financial crises will occur, there

were certain companies that were not able to adapt to the new systems and hence they went on a

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10ADVANCE FINANCE IMPAIRMENT

bankrupt. For this reason, the lease liabilities of the reporting entities in the balance sheet were

66 times greater than the reported debts that are under the balance sheet

(iii) Reasons behind why the Chairperson of IASB is in the view that under the

previous accounting standard no level playing field was there among some

airline entities

The main problem with the earlier accounting systems was related to comparability. For

the airline industries, most of the leases are treated as the operating leases and therefore they are

not recorded in the balance sheet. Hence, due to this reason, it is often said that the level of

playing field does not exist among the given airline companies. When the new given standards

will be introduced, it is supposed that such types of problems will not be there as all the given

eases will be taken as assets and the given leases will account as the liabilities.

(iv) Reasons why the Chairperson is in the view that the new standard will not be

popular with everyone

Any new change that takes place in the firm has an impact on the overall business of the

company. Hence, the given companies need to be careful enough and be prepared to make the

given accounting changes in their given income statement and also to the balance sheets. Apart

from the visible impacts, it is also believed that there will be certain contractual arrangements as

well as banking policies associated with the statements of the country (Md Khokan , Rahman

and Mollik 2014). These are normally related with the aspects of human resource and may

change the overall structure of the bonus payment and the other relevant ratios.

bankrupt. For this reason, the lease liabilities of the reporting entities in the balance sheet were

66 times greater than the reported debts that are under the balance sheet

(iii) Reasons behind why the Chairperson of IASB is in the view that under the

previous accounting standard no level playing field was there among some

airline entities

The main problem with the earlier accounting systems was related to comparability. For

the airline industries, most of the leases are treated as the operating leases and therefore they are

not recorded in the balance sheet. Hence, due to this reason, it is often said that the level of

playing field does not exist among the given airline companies. When the new given standards

will be introduced, it is supposed that such types of problems will not be there as all the given

eases will be taken as assets and the given leases will account as the liabilities.

(iv) Reasons why the Chairperson is in the view that the new standard will not be

popular with everyone

Any new change that takes place in the firm has an impact on the overall business of the

company. Hence, the given companies need to be careful enough and be prepared to make the

given accounting changes in their given income statement and also to the balance sheets. Apart

from the visible impacts, it is also believed that there will be certain contractual arrangements as

well as banking policies associated with the statements of the country (Md Khokan , Rahman

and Mollik 2014). These are normally related with the aspects of human resource and may

change the overall structure of the bonus payment and the other relevant ratios.

11ADVANCE FINANCE IMPAIRMENT

(v) Possibilities that the new visibility with regard to all the leases will result into

better informed decision for investment as well as the company

The blessing in disguise in terms of the new accounting standard is that the companies all

over the world will provide more transparency in their accounting statements after this

implementation. This transparency shall result in better information for the investors who plan to

invest their savings in the different shares of the company (Ramanna and Watts 2012). With the

earlier accounting standard that are in use, the companies used to keep their operating leases

under their income statement and this has made it impossible for the investors to compare.

Therefore, when the new standard will upgrade to the rule of IFRS 16, the investors will then be

able to take better decisions for their respective company.

(v) Possibilities that the new visibility with regard to all the leases will result into

better informed decision for investment as well as the company

The blessing in disguise in terms of the new accounting standard is that the companies all

over the world will provide more transparency in their accounting statements after this

implementation. This transparency shall result in better information for the investors who plan to

invest their savings in the different shares of the company (Ramanna and Watts 2012). With the

earlier accounting standard that are in use, the companies used to keep their operating leases

under their income statement and this has made it impossible for the investors to compare.

Therefore, when the new standard will upgrade to the rule of IFRS 16, the investors will then be

able to take better decisions for their respective company.

12ADVANCE FINANCE IMPAIRMENT

References

Alsglobal.com ,2018. ALS. [online] Alsglobal.com. Available at:

https://www.alsglobal.com/-/media/als/resources/myals/.../2016-annual-report.pdf [Accessed 25

Jan. 2018].

AmirALSani, H., Iatridis, G.E. and Pope, P.F. ,2013. Accounting for asset impairment. London:

Cass Business School.

AmirALSani, H., Iatridis, G.E. and Pope, P.F. ,2013. Accounting for asset impairment: a test for

IFRS compliance across Europe. Centre for Financial Analysis and Reporting Research

(CeFARR).

Andrews, R. ,2012. Fair Value, earnings management and asset impairment: The impact of a

change in the regulatory environment. Procedia Economics and Finance, 2, pp.16-25.

Carlin, T.M. and Finch, N. ,2010. Resisting compliance with IFRS goodwill accounting and

reporting disclosures evidence from Australia, Journal of Accounting and Organizational

Change, Vol. 6 No. 2, pp. 260-280. [Google Scholar] [Link] [Infotrieve]

Carlin, T.M. and Finch, N. ,2011. Goodwill impairment testing under IFRS: a false impossible

shore?, Pacific Accounting Review, Vol. 23 No. 3, pp. 368-392. [Google Scholar] [Link]

[Infotrieve]

Carlin, T.M., Finch, N. and Laili, N.H. ,2009. Goodwill accounting in Malaysia and the

transition to IFRS – a compliance assessment of large first year adopters, Journal of Financial

Reporting and Accounting, Vol. 7 No. 1, pp. 75-104. [Google Scholar] [Link] [Infotrieve]

References

Alsglobal.com ,2018. ALS. [online] Alsglobal.com. Available at:

https://www.alsglobal.com/-/media/als/resources/myals/.../2016-annual-report.pdf [Accessed 25

Jan. 2018].

AmirALSani, H., Iatridis, G.E. and Pope, P.F. ,2013. Accounting for asset impairment. London:

Cass Business School.

AmirALSani, H., Iatridis, G.E. and Pope, P.F. ,2013. Accounting for asset impairment: a test for

IFRS compliance across Europe. Centre for Financial Analysis and Reporting Research

(CeFARR).

Andrews, R. ,2012. Fair Value, earnings management and asset impairment: The impact of a

change in the regulatory environment. Procedia Economics and Finance, 2, pp.16-25.

Carlin, T.M. and Finch, N. ,2010. Resisting compliance with IFRS goodwill accounting and

reporting disclosures evidence from Australia, Journal of Accounting and Organizational

Change, Vol. 6 No. 2, pp. 260-280. [Google Scholar] [Link] [Infotrieve]

Carlin, T.M. and Finch, N. ,2011. Goodwill impairment testing under IFRS: a false impossible

shore?, Pacific Accounting Review, Vol. 23 No. 3, pp. 368-392. [Google Scholar] [Link]

[Infotrieve]

Carlin, T.M., Finch, N. and Laili, N.H. ,2009. Goodwill accounting in Malaysia and the

transition to IFRS – a compliance assessment of large first year adopters, Journal of Financial

Reporting and Accounting, Vol. 7 No. 1, pp. 75-104. [Google Scholar] [Link] [Infotrieve]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13ADVANCE FINANCE IMPAIRMENT

Cotter, D. ,2012. Advanced financial reporting: A complete guide to IFRS. Financial

Times/Prentice Hall.

Fitó, M.À., Moya, S. and Orgaz, N. ,2013. Considering the effects of operating lease

capitalization on key financial ratios. Spanish Journal of Finance and Accounting/Revista

Española de Financiación y Contabilidad, 42(159), pp.341-369.

Ifrs.org. ,2018. IFRS. [online] Available at: http://www.ifrs.org/ [Accessed 25 Jan. 2018].

Jennings, R. and Marques, A. ,2013. Amortized cost for operating lease assets. Accounting

Horizons, 27(1), pp.51-74.

Lee, C.H. and Hooy, C.W. ,2013. Determinants of systematic financial risk exposures of airlines

in North America, Europe and Asia. Journal of Air Transport Management, 24, pp.31-35.

loans, H., retirement, S., and education, N. ,2018. Bank Accounts, Super, Insurance and Home

Loans - AMP. Amp.com.au. Retrieved 25 January 2018, from https://www.amp.com.au/

Marshall, D. ,2016. Accounting: What the numbers mean. McGraw-Hill Higher Education.

Md Khokan Bepari, Sheikh F. Rahman and Abu Taher Mollik. ,2014 .Firms' compliance with

the disclosure requirements of IFRS for goodwill impairment testing: Effect of the global

financial crisis and other firm characteristics, Journal of Accounting and Organizational

Change, Vol. 10 Issue: 1, pp.116149, https://doi.org/10.1108/JAOC-02-2011-0008

Ramanna, K. and Watts, R.L. ,2012. Evidence on the use of unverifiable estimates in required

goodwill impairment. Review of Accounting Studies, 17(4), pp.749-780.

Cotter, D. ,2012. Advanced financial reporting: A complete guide to IFRS. Financial

Times/Prentice Hall.

Fitó, M.À., Moya, S. and Orgaz, N. ,2013. Considering the effects of operating lease

capitalization on key financial ratios. Spanish Journal of Finance and Accounting/Revista

Española de Financiación y Contabilidad, 42(159), pp.341-369.

Ifrs.org. ,2018. IFRS. [online] Available at: http://www.ifrs.org/ [Accessed 25 Jan. 2018].

Jennings, R. and Marques, A. ,2013. Amortized cost for operating lease assets. Accounting

Horizons, 27(1), pp.51-74.

Lee, C.H. and Hooy, C.W. ,2013. Determinants of systematic financial risk exposures of airlines

in North America, Europe and Asia. Journal of Air Transport Management, 24, pp.31-35.

loans, H., retirement, S., and education, N. ,2018. Bank Accounts, Super, Insurance and Home

Loans - AMP. Amp.com.au. Retrieved 25 January 2018, from https://www.amp.com.au/

Marshall, D. ,2016. Accounting: What the numbers mean. McGraw-Hill Higher Education.

Md Khokan Bepari, Sheikh F. Rahman and Abu Taher Mollik. ,2014 .Firms' compliance with

the disclosure requirements of IFRS for goodwill impairment testing: Effect of the global

financial crisis and other firm characteristics, Journal of Accounting and Organizational

Change, Vol. 10 Issue: 1, pp.116149, https://doi.org/10.1108/JAOC-02-2011-0008

Ramanna, K. and Watts, R.L. ,2012. Evidence on the use of unverifiable estimates in required

goodwill impairment. Review of Accounting Studies, 17(4), pp.749-780.

14ADVANCE FINANCE IMPAIRMENT

Rennekamp, K., Rupar, K.K. and Seybert, N. ,2014. Impaired judgment: The effects of asset

impairment reversibility and cognitive dissonance on future investment. The Accounting

Review, 90(2), pp.739-759.

Rennekamp, K., Rupar, K.K. and Seybert, N. ,2014. Impaired judgment: The effects of asset

impairment reversibility and cognitive dissonance on future investment. The Accounting

Review, 90(2), pp.739-759.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.