Financial Analysis: IAS 16 & IAS 38 Report - Griffith College Dublin

VerifiedAdded on 2023/06/10

|8

|1383

|464

Report

AI Summary

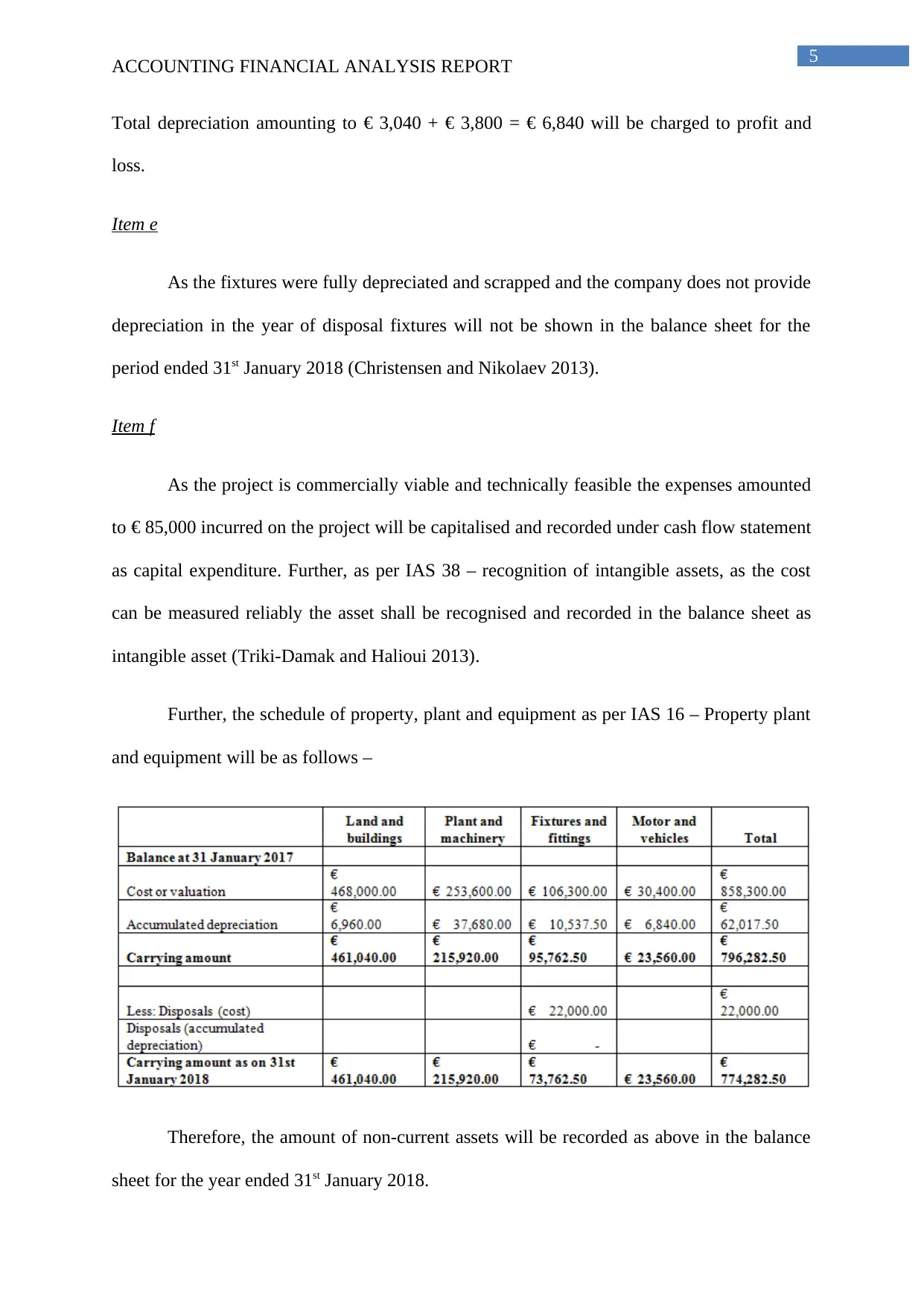

This financial analysis report focuses on International Accounting Standards (IAS) 16 and 38, addressing the accounting treatment of property, plant, equipment, and intangible assets. It explains the objectives, recognition, measurement, and disclosure requirements of IAS 16. The report also details the accounting treatment for research and development costs under IAS 38, differentiating between research expenses (which are expensed) and development costs (which may be capitalized under specific conditions). Furthermore, the report includes specific accounting treatments for various items, such as depreciation on buildings and plants, government grants, vehicle depreciation, and the handling of fully depreciated fixtures, providing a thorough overview of how these assets are reported in financial statements according to international accounting standards. The report adheres to IFRS guidelines.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.