Comparative Financial Reporting Analysis of BHP and Rio Tinto (ASX)

VerifiedAdded on 2023/06/07

|15

|3353

|303

Report

AI Summary

This report provides a comparative financial analysis of BHP Billiton Plc and Rio Tinto Plc, two major ASX-listed mining companies, focusing on their financial reporting practices. The analysis covers the owners' equity section, cash flow statements, other comprehensive income statements, and corpora...

FINANCIAL REPORTING ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

Corporate financial reporting plays a major role in assessing the firm's value and financial

capabilities not only in terms of financial strength and health but also in terms of reporting

regulations compliance, disclosure requirements, transparency, and efficient reporting

presentation. The instant report briefly analyses the financial reporting of two ASX listed

companies. Such companies are BHP Billiton Plc (hereinafter may be referred to as “BHP”) and

Rio Tinto Plc (hereinafter may be referred to as “Rio Tinto”). These two companies are chosen

as both the companies are huge in size and occupy a significant position in the overall Australian

mining industry.

The entire report has been divided into four different parts. At the very beginning of the study,

the researcher provides a comparative analysis of the owners' equity section of the annual report

of both the companies. The second section focuses on the comparative analysis of the cash flow

statement. In the subsequent part of the study, the report performs a comparative analysis of

another comprehensive income statement of both the companies and the last sections focuses on

the corporate income tax position for both BJP and Rio Tinto. The researcher finally wraps up

the discussion by way of ending note.

Page 2 of 15

Corporate financial reporting plays a major role in assessing the firm's value and financial

capabilities not only in terms of financial strength and health but also in terms of reporting

regulations compliance, disclosure requirements, transparency, and efficient reporting

presentation. The instant report briefly analyses the financial reporting of two ASX listed

companies. Such companies are BHP Billiton Plc (hereinafter may be referred to as “BHP”) and

Rio Tinto Plc (hereinafter may be referred to as “Rio Tinto”). These two companies are chosen

as both the companies are huge in size and occupy a significant position in the overall Australian

mining industry.

The entire report has been divided into four different parts. At the very beginning of the study,

the researcher provides a comparative analysis of the owners' equity section of the annual report

of both the companies. The second section focuses on the comparative analysis of the cash flow

statement. In the subsequent part of the study, the report performs a comparative analysis of

another comprehensive income statement of both the companies and the last sections focuses on

the corporate income tax position for both BJP and Rio Tinto. The researcher finally wraps up

the discussion by way of ending note.

Page 2 of 15

Table of Contents

1.0 Introduction................................................................................................................................4

2.0 Comparative Analysis of Owners’ Equity.................................................................................5

2.1 Comparative Analysis of Line Items.....................................................................................5

2.2 Comparative Analysis of Debt and Equity Position..............................................................6

3.0 Comparative Analysis of Cash Flow Statement........................................................................7

3.1 Comparative Analysis of Line Items.....................................................................................7

3.2 Comparative Analysis of Cash Position.................................................................................8

4.0 Comparative Analysis of Other Comprehensive Income Statement.........................................9

4.1 Comparative Analysis of Line Items.....................................................................................9

4.2 Comparative Analysis of Comprehensive Income Position................................................10

5.0 Comparative Analysis of Corporate Income Tax....................................................................11

5.1 Tax Expenses.......................................................................................................................11

5.2 Effective Tax Rate...............................................................................................................11

5.3 Deferred Tax Position..........................................................................................................11

5.4 Cash Tax Payment...............................................................................................................12

5.5 Cash Tax Rate......................................................................................................................13

6.0 Conclusion...............................................................................................................................14

References......................................................................................................................................15

Page 3 of 15

1.0 Introduction................................................................................................................................4

2.0 Comparative Analysis of Owners’ Equity.................................................................................5

2.1 Comparative Analysis of Line Items.....................................................................................5

2.2 Comparative Analysis of Debt and Equity Position..............................................................6

3.0 Comparative Analysis of Cash Flow Statement........................................................................7

3.1 Comparative Analysis of Line Items.....................................................................................7

3.2 Comparative Analysis of Cash Position.................................................................................8

4.0 Comparative Analysis of Other Comprehensive Income Statement.........................................9

4.1 Comparative Analysis of Line Items.....................................................................................9

4.2 Comparative Analysis of Comprehensive Income Position................................................10

5.0 Comparative Analysis of Corporate Income Tax....................................................................11

5.1 Tax Expenses.......................................................................................................................11

5.2 Effective Tax Rate...............................................................................................................11

5.3 Deferred Tax Position..........................................................................................................11

5.4 Cash Tax Payment...............................................................................................................12

5.5 Cash Tax Rate......................................................................................................................13

6.0 Conclusion...............................................................................................................................14

References......................................................................................................................................15

Page 3 of 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1.0 Introduction

Analysis of financial reporting may be considered to be one of the most crucial aspects of

business studies as the process of such analysis and evaluation may involve consideration of

different success-critical business matters that are both internal and external to the operations of

the firms. Such analysis shows the comparative position of the financial reporting of two or more

companies belonging to an industry. The report discusses the same in subsequent sections.

Page 4 of 15

Analysis of financial reporting may be considered to be one of the most crucial aspects of

business studies as the process of such analysis and evaluation may involve consideration of

different success-critical business matters that are both internal and external to the operations of

the firms. Such analysis shows the comparative position of the financial reporting of two or more

companies belonging to an industry. The report discusses the same in subsequent sections.

Page 4 of 15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.0 Comparative Analysis of Owners’ Equity

The comparative analysis of each and every line items of owners’ equity of both the companies

is conducted in the subsequent parts of the report.

2.1 Comparative Analysis of Line Items

BHP:

Owners’ equity of the group may consist of the share capital of BHP Billiton Limited and BHP

Billiton Plc. In addition, there are some treasure shares and reserves which primarily include

share premium account, foreign currency translation reserve, employee share awards reserve,

hedging reserve, financial assets reserve, shares buy-back reserve. In addition, there are retained

earnings which may be construed to be the accumulation of past profits. Since the consideration

is about the owners, the non-controlling interests have not been taken into consideration here

(Bhp.com, 2018).

As far as change is concerned, the total equity has increased in the last three years under review

i.e. 2015 to 2017. In the current year, there has been a rise from $60,071 million in the year 2016

to $62,726 million in the year 2017 (Bhp.com, 2018). Such increase is primarily attributable to

the increase in reserve as the share capital has remained stagnant throughout.

Rio Tinto:

On the other hand, the owners’ equity of Rio Tinto includes almost similar line items that have

appeared in the books of accounts of BHP. The items are primarily shared capital of Rio Tinto

Plc and Rio Tinto Limited, other reserves and retained earnings. It is interesting to note that the

management of Rio Tinto has excluded share premium reserve out of the reserves and shown it

Page 5 of 15

The comparative analysis of each and every line items of owners’ equity of both the companies

is conducted in the subsequent parts of the report.

2.1 Comparative Analysis of Line Items

BHP:

Owners’ equity of the group may consist of the share capital of BHP Billiton Limited and BHP

Billiton Plc. In addition, there are some treasure shares and reserves which primarily include

share premium account, foreign currency translation reserve, employee share awards reserve,

hedging reserve, financial assets reserve, shares buy-back reserve. In addition, there are retained

earnings which may be construed to be the accumulation of past profits. Since the consideration

is about the owners, the non-controlling interests have not been taken into consideration here

(Bhp.com, 2018).

As far as change is concerned, the total equity has increased in the last three years under review

i.e. 2015 to 2017. In the current year, there has been a rise from $60,071 million in the year 2016

to $62,726 million in the year 2017 (Bhp.com, 2018). Such increase is primarily attributable to

the increase in reserve as the share capital has remained stagnant throughout.

Rio Tinto:

On the other hand, the owners’ equity of Rio Tinto includes almost similar line items that have

appeared in the books of accounts of BHP. The items are primarily shared capital of Rio Tinto

Plc and Rio Tinto Limited, other reserves and retained earnings. It is interesting to note that the

management of Rio Tinto has excluded share premium reserve out of the reserves and shown it

Page 5 of 15

separately as separate line items in the Balance Sheet. The other reserves of Rio Tinto have

consisted of capital redemption reserve, hedging reserve, sale revaluation reserve and foreign

currency translation reserve (Riotinto.com, 2018).

The growth story has almost been similar in the case of Rio Tinto as well. However, there has

been a marginal increase in share capital and the lion's portion of growth has been occurring due

to the growth in reserves (Riotinto.com, 2018).

2.2 Comparative Analysis of Debt and Equity Position

Both the firms have largely reliant on debt as may be evident from the last three year’s balance

sheets. The debt part of the entire liabilities bucket has been substantially high and almost equal

to the equity position. In other words, the management has been aggressive to grow on debt

probably because of the leverage benefit as may be derived therefrom. Moreover, the debt, being

the cheaper source of funding than equity, may easily be an easy option for the management to

choose for the purpose of sourcing (Finocchiaro and Mendicino, 2015).

However, the comparative position may show that Rio Tinto has more debt burden in its capital

structure than that of BHP in the year 2016. However, the figure for 2017 depicts the almost the

same proportion of debt-equity mix for both the firms.

Page 6 of 15

consisted of capital redemption reserve, hedging reserve, sale revaluation reserve and foreign

currency translation reserve (Riotinto.com, 2018).

The growth story has almost been similar in the case of Rio Tinto as well. However, there has

been a marginal increase in share capital and the lion's portion of growth has been occurring due

to the growth in reserves (Riotinto.com, 2018).

2.2 Comparative Analysis of Debt and Equity Position

Both the firms have largely reliant on debt as may be evident from the last three year’s balance

sheets. The debt part of the entire liabilities bucket has been substantially high and almost equal

to the equity position. In other words, the management has been aggressive to grow on debt

probably because of the leverage benefit as may be derived therefrom. Moreover, the debt, being

the cheaper source of funding than equity, may easily be an easy option for the management to

choose for the purpose of sourcing (Finocchiaro and Mendicino, 2015).

However, the comparative position may show that Rio Tinto has more debt burden in its capital

structure than that of BHP in the year 2016. However, the figure for 2017 depicts the almost the

same proportion of debt-equity mix for both the firms.

Page 6 of 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3.0 Comparative Analysis of Cash Flow Statement

Cash flow statement is a critical financial statement which reflects the net cash flow position of

the business and the comparative analysis of cash flow statement establishes the mutual

comparison between two firms with respect to their respective liquidity stand point. The

discussion has been briefly performed as below.

3.1 Comparative Analysis of Line Items

BHP:

Cash generated from operations (CGO) for the company in last three years has been declining

from $21,620 million in the year 2015 to $12,671 million in 2016 and finally revived to $19,377

million in 2017 (Bhp.com, 2018). There has been a sharp fall in cash generation in the last year,

because of loss booked by the group. Investment in PP&E has been declining continuously in the

last three years from $11,947 million (2015) to $4,252 million (2017). In addition, the repayment

of loan has also been a substantially huge line item of the company and the same has been

fluctuating showing an overall increasing trend during the period under review (from $4 billion

in 2015 to $7 billion in 2017 approximately). However, the dividend payments to the

stockholders have also shown a downward trend in the last three years to the extent of 50%

decline ( from $6.5 billion to less than $3 billion).

Rio Tinto:

On the other hand, the company has been able to increase the cash generated from operations

substantially from the last two years - almost 50% increase from the figure of 2015. The

purchase of PP&E has also been fairly stable throughout the period. In the current year, there has

Page 7 of 15

Cash flow statement is a critical financial statement which reflects the net cash flow position of

the business and the comparative analysis of cash flow statement establishes the mutual

comparison between two firms with respect to their respective liquidity stand point. The

discussion has been briefly performed as below.

3.1 Comparative Analysis of Line Items

BHP:

Cash generated from operations (CGO) for the company in last three years has been declining

from $21,620 million in the year 2015 to $12,671 million in 2016 and finally revived to $19,377

million in 2017 (Bhp.com, 2018). There has been a sharp fall in cash generation in the last year,

because of loss booked by the group. Investment in PP&E has been declining continuously in the

last three years from $11,947 million (2015) to $4,252 million (2017). In addition, the repayment

of loan has also been a substantially huge line item of the company and the same has been

fluctuating showing an overall increasing trend during the period under review (from $4 billion

in 2015 to $7 billion in 2017 approximately). However, the dividend payments to the

stockholders have also shown a downward trend in the last three years to the extent of 50%

decline ( from $6.5 billion to less than $3 billion).

Rio Tinto:

On the other hand, the company has been able to increase the cash generated from operations

substantially from the last two years - almost 50% increase from the figure of 2015. The

purchase of PP&E has also been fairly stable throughout the period. In the current year, there has

Page 7 of 15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

been significant inflow from the disposal of subsidiaries, joint ventures, and associates to the

extent of $2,675 million (Riotinto.com, 2018). Dividend payment has also been fluctuating with

an overall stable rate as far as figures of 2015 and 2017 are concerned. Repayment of borrowing

is another critical item in the cash flow statement which is also very much fluctuating with

movement from $3 billion to $9 billion in 2016 and again less than $3 billion in 2017

(Riotinto.com, 2018).

3.2 Comparative Analysis of Cash Position

The relative cash position of both the companies has been fairly rich in the sense that both the

firms have been able to accumulate a substantial amount of cash balance at the end of 2017.

However, a closer look into the cash movement of both the groups’ shows that BHP has been

extremely efficient in terms of cash accumulation which may be corroborated from the fact the

cash position of BHP was $6,613 million in 2015 which increased to $10,276 million in 2016

and subsequently $14,108 million in 2017.

Page 8 of 15

extent of $2,675 million (Riotinto.com, 2018). Dividend payment has also been fluctuating with

an overall stable rate as far as figures of 2015 and 2017 are concerned. Repayment of borrowing

is another critical item in the cash flow statement which is also very much fluctuating with

movement from $3 billion to $9 billion in 2016 and again less than $3 billion in 2017

(Riotinto.com, 2018).

3.2 Comparative Analysis of Cash Position

The relative cash position of both the companies has been fairly rich in the sense that both the

firms have been able to accumulate a substantial amount of cash balance at the end of 2017.

However, a closer look into the cash movement of both the groups’ shows that BHP has been

extremely efficient in terms of cash accumulation which may be corroborated from the fact the

cash position of BHP was $6,613 million in 2015 which increased to $10,276 million in 2016

and subsequently $14,108 million in 2017.

Page 8 of 15

4.0 Comparative Analysis of Other Comprehensive Income Statement

Comprehensive income statement mainly lists the revenue items that are not being considered in

the income statement but critical to consider while finalizing the share of profit to be transferred

to stockholders account and retained earnings (Damant, 2003). The section below briefly

discusses the line items and their respective changes in yearly basis for both the companies.

4.1 Comparative Analysis of Line Items

BHP:

In case of BHP, the line items that have appeared in the other comprehensive income statement

of the company are primarily of two types namely the items that are being reclassified in the

income statement subsequently and the items that are not being reclassified in the income

statement. Proceeds from available for sale investments, cash flow hedges and related gains

transferred to equity, exchange fluctuations are taken to equity, tax recognized within the ambit

of other comprehensive income are some of the examples of other comprehensive income

reclassified in the income statement (Bhp.com, 2018). On the other hand, re-measurement gains

on medical and pension schemes, related tax expenses are those items that are not being

reclassified in the income statement but have appeared in the other comprehensive income

statement of the company for the years under review (Bhp.com, 2018).

Rio Tinto:

In the case of Rio Tinto, the actuarial gains or losses on post-retirement benefit plans, related tax

implications on both current tax change and deferred tax charge are reclassified in the income

statement. In addition, the cash flow hedges, gains or losses on the revaluation of available for

Page 9 of 15

Comprehensive income statement mainly lists the revenue items that are not being considered in

the income statement but critical to consider while finalizing the share of profit to be transferred

to stockholders account and retained earnings (Damant, 2003). The section below briefly

discusses the line items and their respective changes in yearly basis for both the companies.

4.1 Comparative Analysis of Line Items

BHP:

In case of BHP, the line items that have appeared in the other comprehensive income statement

of the company are primarily of two types namely the items that are being reclassified in the

income statement subsequently and the items that are not being reclassified in the income

statement. Proceeds from available for sale investments, cash flow hedges and related gains

transferred to equity, exchange fluctuations are taken to equity, tax recognized within the ambit

of other comprehensive income are some of the examples of other comprehensive income

reclassified in the income statement (Bhp.com, 2018). On the other hand, re-measurement gains

on medical and pension schemes, related tax expenses are those items that are not being

reclassified in the income statement but have appeared in the other comprehensive income

statement of the company for the years under review (Bhp.com, 2018).

Rio Tinto:

In the case of Rio Tinto, the actuarial gains or losses on post-retirement benefit plans, related tax

implications on both current tax change and deferred tax charge are reclassified in the income

statement. In addition, the cash flow hedges, gains or losses on the revaluation of available for

Page 9 of 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

sale securities and assets are not being reclassified in the income statement. Therefore, it may be

noted that both the companies have followed similar types of standards and policies with respect

to income recognition and tax charging thereon leading to a similar approach for another

comprehensive income statement (Riotinto.com, 2018).

4.2 Comparative Analysis of Comprehensive Income Position

For Rio Tinto, the other comprehensive income has increased sizably in the last three years. In

the year 2015, the same was a loss of $3,749 million which increased almost 4 times to $11,939

million in the year 2017. Such increment is primarily attributable to the huge amount of currency

translation adjustment in the current year. However, such adjustment excludes the gain arising

out of the translation arising from Rio Tinto Limited's share capital. The same has been taken to

the group's statement of changes in equity. However, as far as BHP is concerned, the other

comprehensive income for the group has been increasing with fluctuations in the year 2016.

However, it may be observed that such an increase has happened because of higher profit and not

because of items in OCI statement in the year 2017.

Page 10 of 15

noted that both the companies have followed similar types of standards and policies with respect

to income recognition and tax charging thereon leading to a similar approach for another

comprehensive income statement (Riotinto.com, 2018).

4.2 Comparative Analysis of Comprehensive Income Position

For Rio Tinto, the other comprehensive income has increased sizably in the last three years. In

the year 2015, the same was a loss of $3,749 million which increased almost 4 times to $11,939

million in the year 2017. Such increment is primarily attributable to the huge amount of currency

translation adjustment in the current year. However, such adjustment excludes the gain arising

out of the translation arising from Rio Tinto Limited's share capital. The same has been taken to

the group's statement of changes in equity. However, as far as BHP is concerned, the other

comprehensive income for the group has been increasing with fluctuations in the year 2016.

However, it may be observed that such an increase has happened because of higher profit and not

because of items in OCI statement in the year 2017.

Page 10 of 15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5.0 Comparative Analysis of Corporate Income Tax

Corporate income tax is an important line item in the financial statement of the companies. The

report shows the different aspects of corporate income tax and related deferred tax assets and

liabilities position of both the companies.

5.1 Tax Expenses

Current tax expenses for BHP are increasing in the last three years. In the year 2015, the same

was $3,168 million, which reduced to $2,456 million in the year 2016 before increasing to

$4,288 million in the year 2017. On the other hand, the same for Rio Tinto has also been

increasing but such increase has shown a consistent growth during the period. The charge has

been increased from $1,132 million (2015) to $3,270 million (2017), which is almost three times.

5.2 Effective Tax Rate

The tax rate for BHP has been considered as Australian prima facie tax rate of 30%, whereas, the

same for Rio Tinto has been taken as UK prima facie tax rate of 19%. Therefore, it may be

observed that BHP has comparatively higher tax rate.

5.3 Deferred Tax Position

Deferred tax position may be discussed from two view point; one is related to income statement

which shows how much charges have been, made against the profit for deferred tax purpose and

the second one is related to balance sheet which establishes the deferred tax assets or liabilities

position of the business (Warsono, 2018).

For BHP, the deferred tax charge to the revenue has been heavily fluctuating from $498 (2015)

to negative $3,508 (2016) and then again negative $188 (2017). The balance sheet of BHP has

Page 11 of 15

Corporate income tax is an important line item in the financial statement of the companies. The

report shows the different aspects of corporate income tax and related deferred tax assets and

liabilities position of both the companies.

5.1 Tax Expenses

Current tax expenses for BHP are increasing in the last three years. In the year 2015, the same

was $3,168 million, which reduced to $2,456 million in the year 2016 before increasing to

$4,288 million in the year 2017. On the other hand, the same for Rio Tinto has also been

increasing but such increase has shown a consistent growth during the period. The charge has

been increased from $1,132 million (2015) to $3,270 million (2017), which is almost three times.

5.2 Effective Tax Rate

The tax rate for BHP has been considered as Australian prima facie tax rate of 30%, whereas, the

same for Rio Tinto has been taken as UK prima facie tax rate of 19%. Therefore, it may be

observed that BHP has comparatively higher tax rate.

5.3 Deferred Tax Position

Deferred tax position may be discussed from two view point; one is related to income statement

which shows how much charges have been, made against the profit for deferred tax purpose and

the second one is related to balance sheet which establishes the deferred tax assets or liabilities

position of the business (Warsono, 2018).

For BHP, the deferred tax charge to the revenue has been heavily fluctuating from $498 (2015)

to negative $3,508 (2016) and then again negative $188 (2017). The balance sheet of BHP has

Page 11 of 15

shown deferred tax assets of $5,788 million in the current year, whereas, the business also

created a provision for deferred tax liabilities to the extent of $3,765 million during the same

period (BHP, 2018).

On the other hand, for Rio Tinto, deferred tax charge has been increasing yearly basis; from

negative $139 million in 2015 to $695 million in 2017. As far as assets and liabilities position is

concerned, the management has created $3,395 million in deferred tax assets and $3,628 deferred

tax liabilities (Riotinto.com, 2018).

It may, therefore, be shown that BHP has more asset position in terms of timing differences than

that of Rio Tinto. Such situation is subject to adjustment of subsequent year’s reversal of timing

differences and income tax provision accordingly. In this context, it may be worth to note that

the creation of deferred tax assets or liabilities are because of the variance in treatment of

different items of financial statements under both Income Tax Act and Corporations Act (Laux,

2011). For example, the depreciation is a classic example which is charged to profit under two

different approaches in both the Income Tax Act and Corporations Act as well. As a result, such

differences may occur which may primarily be construed to be arising out of timing differences.

5.4 Cash Tax Payment

Since the tax is provided for in the income statement, the exact amount of cash tax payment may

not be traceable from the income statement or the statement of profit or loss. Cash flow

statement shows the same for the relevant years.

An insight into the cash flow statement may reveal that Rio Tinto has paid almost $2,307 million

income tax to the government during the financial year 2017, whereas, the same for BHP has

been $2,585 million. In this context, it may be interesting to note that both the companies have

Page 12 of 15

created a provision for deferred tax liabilities to the extent of $3,765 million during the same

period (BHP, 2018).

On the other hand, for Rio Tinto, deferred tax charge has been increasing yearly basis; from

negative $139 million in 2015 to $695 million in 2017. As far as assets and liabilities position is

concerned, the management has created $3,395 million in deferred tax assets and $3,628 deferred

tax liabilities (Riotinto.com, 2018).

It may, therefore, be shown that BHP has more asset position in terms of timing differences than

that of Rio Tinto. Such situation is subject to adjustment of subsequent year’s reversal of timing

differences and income tax provision accordingly. In this context, it may be worth to note that

the creation of deferred tax assets or liabilities are because of the variance in treatment of

different items of financial statements under both Income Tax Act and Corporations Act (Laux,

2011). For example, the depreciation is a classic example which is charged to profit under two

different approaches in both the Income Tax Act and Corporations Act as well. As a result, such

differences may occur which may primarily be construed to be arising out of timing differences.

5.4 Cash Tax Payment

Since the tax is provided for in the income statement, the exact amount of cash tax payment may

not be traceable from the income statement or the statement of profit or loss. Cash flow

statement shows the same for the relevant years.

An insight into the cash flow statement may reveal that Rio Tinto has paid almost $2,307 million

income tax to the government during the financial year 2017, whereas, the same for BHP has

been $2,585 million. In this context, it may be interesting to note that both the companies have

Page 12 of 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

paid the almost similar amount of tax in spite of the fact that both the companies are subjected to

different tax bracket with varied degree of income.

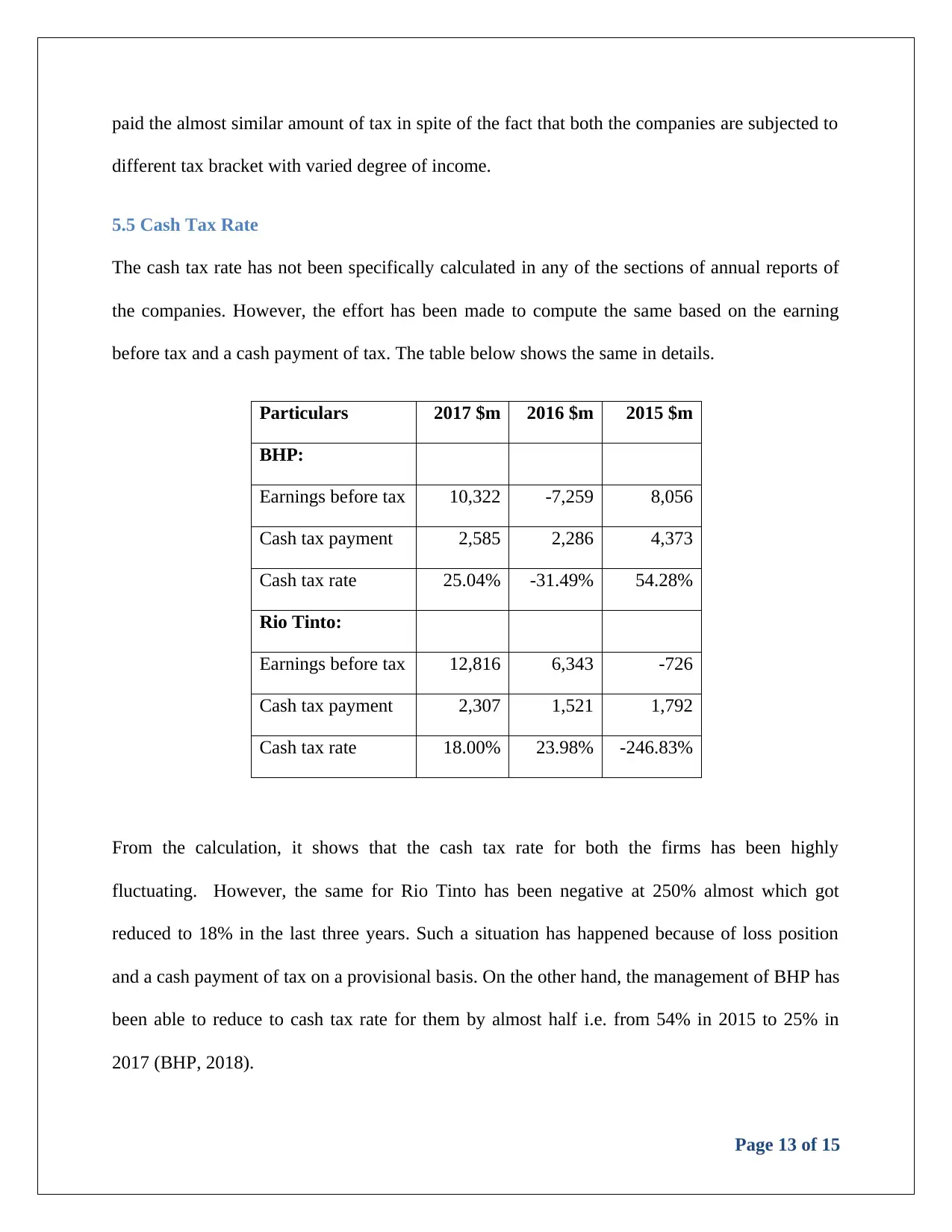

5.5 Cash Tax Rate

The cash tax rate has not been specifically calculated in any of the sections of annual reports of

the companies. However, the effort has been made to compute the same based on the earning

before tax and a cash payment of tax. The table below shows the same in details.

Particulars 2017 $m 2016 $m 2015 $m

BHP:

Earnings before tax 10,322 -7,259 8,056

Cash tax payment 2,585 2,286 4,373

Cash tax rate 25.04% -31.49% 54.28%

Rio Tinto:

Earnings before tax 12,816 6,343 -726

Cash tax payment 2,307 1,521 1,792

Cash tax rate 18.00% 23.98% -246.83%

From the calculation, it shows that the cash tax rate for both the firms has been highly

fluctuating. However, the same for Rio Tinto has been negative at 250% almost which got

reduced to 18% in the last three years. Such a situation has happened because of loss position

and a cash payment of tax on a provisional basis. On the other hand, the management of BHP has

been able to reduce to cash tax rate for them by almost half i.e. from 54% in 2015 to 25% in

2017 (BHP, 2018).

Page 13 of 15

different tax bracket with varied degree of income.

5.5 Cash Tax Rate

The cash tax rate has not been specifically calculated in any of the sections of annual reports of

the companies. However, the effort has been made to compute the same based on the earning

before tax and a cash payment of tax. The table below shows the same in details.

Particulars 2017 $m 2016 $m 2015 $m

BHP:

Earnings before tax 10,322 -7,259 8,056

Cash tax payment 2,585 2,286 4,373

Cash tax rate 25.04% -31.49% 54.28%

Rio Tinto:

Earnings before tax 12,816 6,343 -726

Cash tax payment 2,307 1,521 1,792

Cash tax rate 18.00% 23.98% -246.83%

From the calculation, it shows that the cash tax rate for both the firms has been highly

fluctuating. However, the same for Rio Tinto has been negative at 250% almost which got

reduced to 18% in the last three years. Such a situation has happened because of loss position

and a cash payment of tax on a provisional basis. On the other hand, the management of BHP has

been able to reduce to cash tax rate for them by almost half i.e. from 54% in 2015 to 25% in

2017 (BHP, 2018).

Page 13 of 15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6.0 Conclusion

Based on the discussion and analysis performed in the preceding sections of the report, it may be

concluded that the financial reporting plays an integral part of overall responsibilities bracket of

corporate management. An efficient and understandable reporting helps the stakeholders to

assess the financial health of the business in a more efficient manner. Since the audited financial

statements have their own gravity in terms of reliability and trustworthiness, the investors and

prospective owner groups put much reliance on the facts and figure as mentioned in the annual

report of the companies. Therefore, the management should take utmost care while finalizing the

annual report in order to ensure smooth stakeholder management. An efficient and lucid financial

reporting in line with the related regulations and directives significantly contribute towards a

greater transparency, brand building and value creation for the business and thereby attaining

sustainability in the market in the long-run.

Page 14 of 15

Based on the discussion and analysis performed in the preceding sections of the report, it may be

concluded that the financial reporting plays an integral part of overall responsibilities bracket of

corporate management. An efficient and understandable reporting helps the stakeholders to

assess the financial health of the business in a more efficient manner. Since the audited financial

statements have their own gravity in terms of reliability and trustworthiness, the investors and

prospective owner groups put much reliance on the facts and figure as mentioned in the annual

report of the companies. Therefore, the management should take utmost care while finalizing the

annual report in order to ensure smooth stakeholder management. An efficient and lucid financial

reporting in line with the related regulations and directives significantly contribute towards a

greater transparency, brand building and value creation for the business and thereby attaining

sustainability in the market in the long-run.

Page 14 of 15

References

BHP. (2018). BHP | Investor centre. [online] Available at: https://www.bhp.com/investor-centre

[Accessed 15 Sep. 2018].

Bhp.com. (2018). BHP Annual Report 2017. [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2017/

bhpannualreport2017.pdf [Accessed 15 Sep. 2018].

Damant, D. (2003). The revolution ahead in financial reporting: a new world – what the income

statement means to financial reporting. Balance Sheet, 11(4), pp.10-18.

Finocchiaro, D. and Mendicino, C. (2015). Debt, Equity and the Equity Price Puzzle. SSRN

Electronic Journal.

Laux, R. (2011). The Association between Deferred Tax Assets and Liabilities and Future Tax

Payments. SSRN Electronic Journal.

Riotinto.com. (2018). Results & reports. [online] Available at:

https://www.riotinto.com/investors/results-and-reports-2146.aspx [Accessed 15 Sep. 2018].

Riotinto.com. (2018). Rio Tinto Annual Report 2017. [online] Available at:

https://www.riotinto.com/documents/RT_2017_Annual_Report.pdf [Accessed 15 Sep. 2018].

Warsono, W. (2018). Deferred Tax Assets and Deferred Tax Expense Against Tax Planning

Profit Management. Shirkah: Journal of Economics and Business, 2(2).

Page 15 of 15

BHP. (2018). BHP | Investor centre. [online] Available at: https://www.bhp.com/investor-centre

[Accessed 15 Sep. 2018].

Bhp.com. (2018). BHP Annual Report 2017. [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2017/

bhpannualreport2017.pdf [Accessed 15 Sep. 2018].

Damant, D. (2003). The revolution ahead in financial reporting: a new world – what the income

statement means to financial reporting. Balance Sheet, 11(4), pp.10-18.

Finocchiaro, D. and Mendicino, C. (2015). Debt, Equity and the Equity Price Puzzle. SSRN

Electronic Journal.

Laux, R. (2011). The Association between Deferred Tax Assets and Liabilities and Future Tax

Payments. SSRN Electronic Journal.

Riotinto.com. (2018). Results & reports. [online] Available at:

https://www.riotinto.com/investors/results-and-reports-2146.aspx [Accessed 15 Sep. 2018].

Riotinto.com. (2018). Rio Tinto Annual Report 2017. [online] Available at:

https://www.riotinto.com/documents/RT_2017_Annual_Report.pdf [Accessed 15 Sep. 2018].

Warsono, W. (2018). Deferred Tax Assets and Deferred Tax Expense Against Tax Planning

Profit Management. Shirkah: Journal of Economics and Business, 2(2).

Page 15 of 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.