Financial Reporting: Analysis of Financial Statements and Reporting

VerifiedAdded on 2021/02/20

|18

|3630

|500

Report

AI Summary

This report delves into the realm of financial reporting, encompassing its context, purpose, and the regulatory frameworks that govern it. It explores the conceptual underpinnings, key principles, and qualitative characteristics of financial reporting, alongside an analysis of the main stakeholders and the benefits they derive from financial reports. The report examines the value of financial reporting in meeting organizational objectives and fostering growth, including the preparation of financial statements based on provided information. Furthermore, it provides an interpretation and communication of financial performance, comparing IAS and IFRS, and highlighting the advantages of international financial reporting systems, concluding with a discussion on compliance levels with international financial reporting standards. The report includes examples from Financial angles and British American Tobacco to illustrate key concepts.

FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Explanation of context and purpose of financial-reporting.....................................................3

2. Conceptual, regulatory framework, key principle and qualitative characteristics..................4

3. Main stakeholders of companies and what benefit they get from financial reports. ..............5

4. The value of financial reporting for meeting organisational objectives and growth..............6

5. Preparation of main financial statements on the basis of given information..........................7

6. Interpretation and communication of financial performance..................................................9

7. Comparison between IAS and IFRS.....................................................................................14

8. Advantage of International financial reporting system.........................................................15

9. Degree of compliance with international financial-reporting standards...............................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

1. Explanation of context and purpose of financial-reporting.....................................................3

2. Conceptual, regulatory framework, key principle and qualitative characteristics..................4

3. Main stakeholders of companies and what benefit they get from financial reports. ..............5

4. The value of financial reporting for meeting organisational objectives and growth..............6

5. Preparation of main financial statements on the basis of given information..........................7

6. Interpretation and communication of financial performance..................................................9

7. Comparison between IAS and IFRS.....................................................................................14

8. Advantage of International financial reporting system.........................................................15

9. Degree of compliance with international financial-reporting standards...............................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

The term financial reporting may be defined as a way of making communication of

financial information with the internal and external stakeholders (Schooley and English, 2015).

Under this, financial statements such as balance sheet, income statement, statement of change in

owner's equity section etc. being used to gather information about financial transactions of

companies. Basically, the financial reporting is useful for internal stakeholders for making

effective decisions as well as for external stakeholders in taking investment decisions. Herein,

the project report purpose and conceptual framework of financial reporting is mentioned. In

addition, evaluation of financial reporting standards and difference in financial reporting at the

international level is also done.

To better understand about the financial reporting a large accountancy firm is selected

that is “Financial angles”. This company is located in London and provide financial services to

their various clients.

MAIN BODY

1. Explanation of context and purpose of financial-reporting.

The financial-reporting can be defined as process of gathering and communicating

financial information of companies with various kind of stakeholders so that financial position of

companies can be assessed. In the absence of this, it can be difficult to manage companies

internal and external operations. Most of companies prepare financial reports at the end of

financial year. Such as in the aspect of above Financial angles company, their accountants

produce these reports so that they can evaluate company's financial condition. Below the purpose

of financial reporting are mentioned that are as follows:

Assess financial condition- It is one of the important purpose of financial reporting that is

linked with assessment of financial position of companies (Sikka and Stittle, 2017). This

becomes possible because of financial information that is collected from various kind of

financial statements. As well as on the basis of it, managers of companies take futuristic

decisions effectively.

Compare actual result with budget- Another purpose of financial reporting is related with

comparison of actual result with budgeted performance. In other words, companies set

The term financial reporting may be defined as a way of making communication of

financial information with the internal and external stakeholders (Schooley and English, 2015).

Under this, financial statements such as balance sheet, income statement, statement of change in

owner's equity section etc. being used to gather information about financial transactions of

companies. Basically, the financial reporting is useful for internal stakeholders for making

effective decisions as well as for external stakeholders in taking investment decisions. Herein,

the project report purpose and conceptual framework of financial reporting is mentioned. In

addition, evaluation of financial reporting standards and difference in financial reporting at the

international level is also done.

To better understand about the financial reporting a large accountancy firm is selected

that is “Financial angles”. This company is located in London and provide financial services to

their various clients.

MAIN BODY

1. Explanation of context and purpose of financial-reporting.

The financial-reporting can be defined as process of gathering and communicating

financial information of companies with various kind of stakeholders so that financial position of

companies can be assessed. In the absence of this, it can be difficult to manage companies

internal and external operations. Most of companies prepare financial reports at the end of

financial year. Such as in the aspect of above Financial angles company, their accountants

produce these reports so that they can evaluate company's financial condition. Below the purpose

of financial reporting are mentioned that are as follows:

Assess financial condition- It is one of the important purpose of financial reporting that is

linked with assessment of financial position of companies (Sikka and Stittle, 2017). This

becomes possible because of financial information that is collected from various kind of

financial statements. As well as on the basis of it, managers of companies take futuristic

decisions effectively.

Compare actual result with budget- Another purpose of financial reporting is related with

comparison of actual result with budgeted performance. In other words, companies set

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

their financial goals before starting of a financial year and these financial reports evaluate

actual result to compare with estimated results. Hence, these financial reports are crucial

in analysing actual performance of companies. Such as in above, Financial angles

company, their managers compare the actual result with estimated results.

Accountability to donors and stakeholders- The financial reports makes a company

accountable towards their external stakeholders such as investors, customers, suppliers

etc. This is so because financial reports reflects the result of all business activities in front

of stakeholders and on the basis of it they take future decisions regarding to investment.

Like the above company, they are accountable for their donors and stakeholders by

providing actual financial results.

2. Conceptual, regulatory framework, key principle and qualitative characteristics.

Conceptual framework of financial reporting- The conceptual framework of financial

reporting is linked with producing financial reporting on a regular time interval (Cho and Yun,

2015). Basically, companies prepare financial reports at the end of financial year. The external

stakeholders of companies are suppliers, customers etc. who want to see financial performance

of companies with help of financial reports.

Regulatory framework of financial reporting- The regulatory framework of financial

reporting is associated with implementation of accounting rules, regulation and standards so that

prepared financial statements can become reliable and transparent for users. In the aspect of

above accountancy firm, financial angel their accountants use below mentioned accounting

principals that are as follows:

Full disclosure-As per this principal of financial reporting, it is essential for accountant to

use all kind of financial information about company in preparation of financial reports.

They should not hide any important information and must include in financial statements.

This principal is important to apply because if companies' accountants will disclose entire

information about company's financial position, then their financial statements will

become more reliable and accountable. In above company, their accountant use this

principal in order to prepare their financial statements more useful and accountable to

their stakeholders.

actual result to compare with estimated results. Hence, these financial reports are crucial

in analysing actual performance of companies. Such as in above, Financial angles

company, their managers compare the actual result with estimated results.

Accountability to donors and stakeholders- The financial reports makes a company

accountable towards their external stakeholders such as investors, customers, suppliers

etc. This is so because financial reports reflects the result of all business activities in front

of stakeholders and on the basis of it they take future decisions regarding to investment.

Like the above company, they are accountable for their donors and stakeholders by

providing actual financial results.

2. Conceptual, regulatory framework, key principle and qualitative characteristics.

Conceptual framework of financial reporting- The conceptual framework of financial

reporting is linked with producing financial reporting on a regular time interval (Cho and Yun,

2015). Basically, companies prepare financial reports at the end of financial year. The external

stakeholders of companies are suppliers, customers etc. who want to see financial performance

of companies with help of financial reports.

Regulatory framework of financial reporting- The regulatory framework of financial

reporting is associated with implementation of accounting rules, regulation and standards so that

prepared financial statements can become reliable and transparent for users. In the aspect of

above accountancy firm, financial angel their accountants use below mentioned accounting

principals that are as follows:

Full disclosure-As per this principal of financial reporting, it is essential for accountant to

use all kind of financial information about company in preparation of financial reports.

They should not hide any important information and must include in financial statements.

This principal is important to apply because if companies' accountants will disclose entire

information about company's financial position, then their financial statements will

become more reliable and accountable. In above company, their accountant use this

principal in order to prepare their financial statements more useful and accountable to

their stakeholders.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Materiality – This is a kind of accounting principal that states that in some cases, use of

accounting standards can be neglected when its effect is minor on company's financial

statements (Ewert and Wagenhofer, 2016). Herein, it is important to know that this

principal rarely used by companies.

Qualitative characteristics of financial reports

Comparability- It is a kind of characteristics of financial reports that states that, these

reports can be compared by previous year's reports.

Relevance- Another feature of financial reports is that, information included in the

reports have relevance with company's financial transactions.

3. Main stakeholders of companies and what benefit they get from financial reports.

The stakeholders are those who have interest in company's financial performance and

activities for their own purposes. Basically, there are two types of stakeholders which are internal

and external. Below description of these stakeholders is done that is as follows:

(a) Internal stakeholder- These are kind of stakeholders who involves themselves in companies'

day to day operations. As well as they have right to take decision about companies operations

and activities. Herein, some types of internal stakeholders are described below such as:

Managers- These stakeholders are being considered as higher level of internal

stakeholders in companies. This is so because, they have right to take decisions on crucial

situations. As well they manage all financial and human resources of entities by making

effective plans and policies. The managers are required to access financial information of

about company for preparation of effective plans and strategies.

Employees- These stakeholders are linked with the performing companies activities and

operations on a daily basis in return they get salaries and wages (Oussii and Boulila

Taktak, 2018). To accomplish companies goals and objectives, their role is too crucial.

As well as their expectation and growth depends on companies financial performance.

This is why, they show interest in companies' financial information.

(b) External stakeholders- These are kind of stakeholders who show interest in companies'

financial performance from out side. They does not involve themselves in day to day operations

and activities. Herein, some types of internal stakeholders are described below such as:

accounting standards can be neglected when its effect is minor on company's financial

statements (Ewert and Wagenhofer, 2016). Herein, it is important to know that this

principal rarely used by companies.

Qualitative characteristics of financial reports

Comparability- It is a kind of characteristics of financial reports that states that, these

reports can be compared by previous year's reports.

Relevance- Another feature of financial reports is that, information included in the

reports have relevance with company's financial transactions.

3. Main stakeholders of companies and what benefit they get from financial reports.

The stakeholders are those who have interest in company's financial performance and

activities for their own purposes. Basically, there are two types of stakeholders which are internal

and external. Below description of these stakeholders is done that is as follows:

(a) Internal stakeholder- These are kind of stakeholders who involves themselves in companies'

day to day operations. As well as they have right to take decision about companies operations

and activities. Herein, some types of internal stakeholders are described below such as:

Managers- These stakeholders are being considered as higher level of internal

stakeholders in companies. This is so because, they have right to take decisions on crucial

situations. As well they manage all financial and human resources of entities by making

effective plans and policies. The managers are required to access financial information of

about company for preparation of effective plans and strategies.

Employees- These stakeholders are linked with the performing companies activities and

operations on a daily basis in return they get salaries and wages (Oussii and Boulila

Taktak, 2018). To accomplish companies goals and objectives, their role is too crucial.

As well as their expectation and growth depends on companies financial performance.

This is why, they show interest in companies' financial information.

(b) External stakeholders- These are kind of stakeholders who show interest in companies'

financial performance from out side. They does not involve themselves in day to day operations

and activities. Herein, some types of internal stakeholders are described below such as:

Creditors- These are kind of stakeholders which are involved in the process of providing

financial assistance to companies on credit (Young, Cohen and Bens, 2018). Herein, it is

important to know that they consider only those companies whose credit score is better

and this can be done by help of analysis of financial information. This is why they show

interest in companies' financial performance.

Suppliers- These are very important stakeholders of companies, this is so because they

sell goods to companies on credit. Hence, it is important to organisations that they should

present their financial results in front of external stakeholders. As well as the suppliers

take benefit from financial performance of companies in order to decide whether they

should sell goods on credit or not.

4. The value of financial reporting for meeting organisational objectives and growth.

The financial-reporting is crucial in aspect of achieving the organisational objectives and

growth. This becomes possible only because under financial reports, companies' financial

position is assessed in a descriptive manner which becomes a basis of planning to grab objectives

and goals.

Financial reporting for meeting organisational objectives- The financial reporting is

crucial in aspect of meeting organisational objectives (Hoyle, Schaefer and Doupnik, 2015). This

is so because by help of these financial reports, companies can make their futuristic strategies

that leads in achieving objectives on time. Like in the aspect of above company, the financial-

reporting helps them in achieving goals and objectives because of proper analysis of financial

position.

Financial reporting for achieving the growth- In addition, the financial reports are also

useful for achieving higher growth of companies. This is so because if organisations will

presents their financial performance to stakeholders then they will be influenced to invest in

companies' activities. Such as in above Financial angels company, they use financial reports in

order to achieve the higher growth.

5. Preparation of main financial statements on the basis of given information.

financial assistance to companies on credit (Young, Cohen and Bens, 2018). Herein, it is

important to know that they consider only those companies whose credit score is better

and this can be done by help of analysis of financial information. This is why they show

interest in companies' financial performance.

Suppliers- These are very important stakeholders of companies, this is so because they

sell goods to companies on credit. Hence, it is important to organisations that they should

present their financial results in front of external stakeholders. As well as the suppliers

take benefit from financial performance of companies in order to decide whether they

should sell goods on credit or not.

4. The value of financial reporting for meeting organisational objectives and growth.

The financial-reporting is crucial in aspect of achieving the organisational objectives and

growth. This becomes possible only because under financial reports, companies' financial

position is assessed in a descriptive manner which becomes a basis of planning to grab objectives

and goals.

Financial reporting for meeting organisational objectives- The financial reporting is

crucial in aspect of meeting organisational objectives (Hoyle, Schaefer and Doupnik, 2015). This

is so because by help of these financial reports, companies can make their futuristic strategies

that leads in achieving objectives on time. Like in the aspect of above company, the financial-

reporting helps them in achieving goals and objectives because of proper analysis of financial

position.

Financial reporting for achieving the growth- In addition, the financial reports are also

useful for achieving higher growth of companies. This is so because if organisations will

presents their financial performance to stakeholders then they will be influenced to invest in

companies' activities. Such as in above Financial angels company, they use financial reports in

order to achieve the higher growth.

5. Preparation of main financial statements on the basis of given information.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(a) Godwin plc income statement for year ended 31 December 2018

Particulars Amount (£)

Revenue

Less: Cost of sales w1

Gross profit

Less- Operating expenses w1

Operating profit

Add- Investment income

Less- Finance cost

Profit before tax

Less- Taxation

Profit for year

585100

(403639)

181461

(92139)

89322

9600

(1200)

97722

(9500)

88222

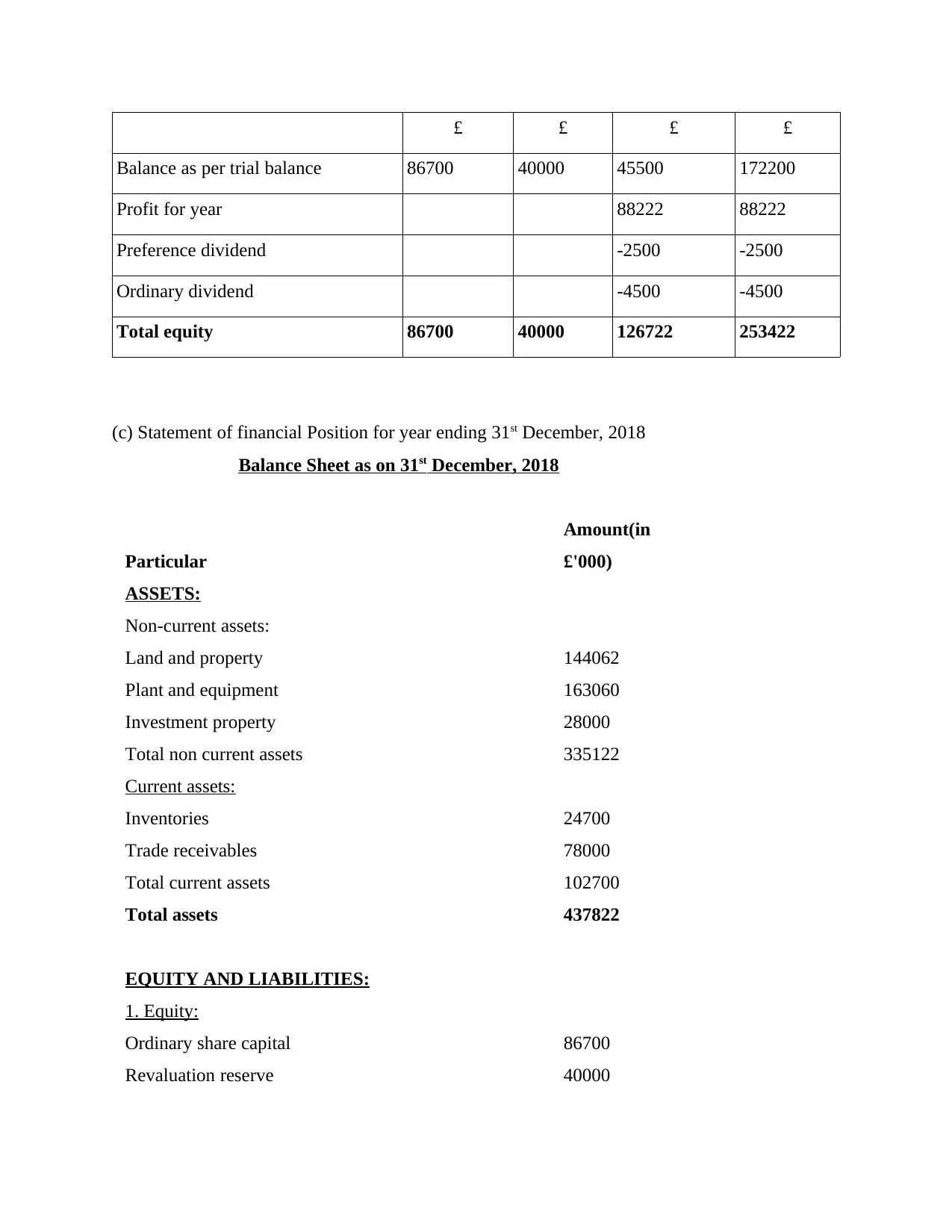

(b) Godwin plc statement of change in equity for year ended 31 December 2018

Ordinary

share capital

@ 25 p

Revaluation

reserves

Retained

earnings

Total

Particulars Amount (£)

Revenue

Less: Cost of sales w1

Gross profit

Less- Operating expenses w1

Operating profit

Add- Investment income

Less- Finance cost

Profit before tax

Less- Taxation

Profit for year

585100

(403639)

181461

(92139)

89322

9600

(1200)

97722

(9500)

88222

(b) Godwin plc statement of change in equity for year ended 31 December 2018

Ordinary

share capital

@ 25 p

Revaluation

reserves

Retained

earnings

Total

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

£ £ £ £

Balance as per trial balance 86700 40000 45500 172200

Profit for year 88222 88222

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

Total equity 86700 40000 126722 253422

(c) Statement of financial Position for year ending 31st December, 2018

Balance Sheet as on 31st December, 2018

Particular

Amount(in

£'000)

ASSETS:

Non-current assets:

Land and property 144062

Plant and equipment 163060

Investment property 28000

Total non current assets 335122

Current assets:

Inventories 24700

Trade receivables 78000

Total current assets 102700

Total assets 437822

EQUITY AND LIABILITIES:

1. Equity:

Ordinary share capital 86700

Revaluation reserve 40000

Balance as per trial balance 86700 40000 45500 172200

Profit for year 88222 88222

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

Total equity 86700 40000 126722 253422

(c) Statement of financial Position for year ending 31st December, 2018

Balance Sheet as on 31st December, 2018

Particular

Amount(in

£'000)

ASSETS:

Non-current assets:

Land and property 144062

Plant and equipment 163060

Investment property 28000

Total non current assets 335122

Current assets:

Inventories 24700

Trade receivables 78000

Total current assets 102700

Total assets 437822

EQUITY AND LIABILITIES:

1. Equity:

Ordinary share capital 86700

Revaluation reserve 40000

Retained earnings 126722

Total equity 253422

Non current liabilities:

10% preference share capital 26500

Deferred taxation 10000

Total non current liabilities 36500

Current liabilities:

Trade payables 62700

Tax payables 9500

Bank overdraft 10900

Total current liabilities 83100

Total equity and liabilities 373022

6. Interpretation and communication of financial performance.

In this task of project report, a company listed in FTSE 100 is selected and name of

company is British American Tobacco selected. This companies' financial statements are

analysed and interpreted in such manner:

Income statement of British American Tobacco company

Total equity 253422

Non current liabilities:

10% preference share capital 26500

Deferred taxation 10000

Total non current liabilities 36500

Current liabilities:

Trade payables 62700

Tax payables 9500

Bank overdraft 10900

Total current liabilities 83100

Total equity and liabilities 373022

6. Interpretation and communication of financial performance.

In this task of project report, a company listed in FTSE 100 is selected and name of

company is British American Tobacco selected. This companies' financial statements are

analysed and interpreted in such manner:

Income statement of British American Tobacco company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

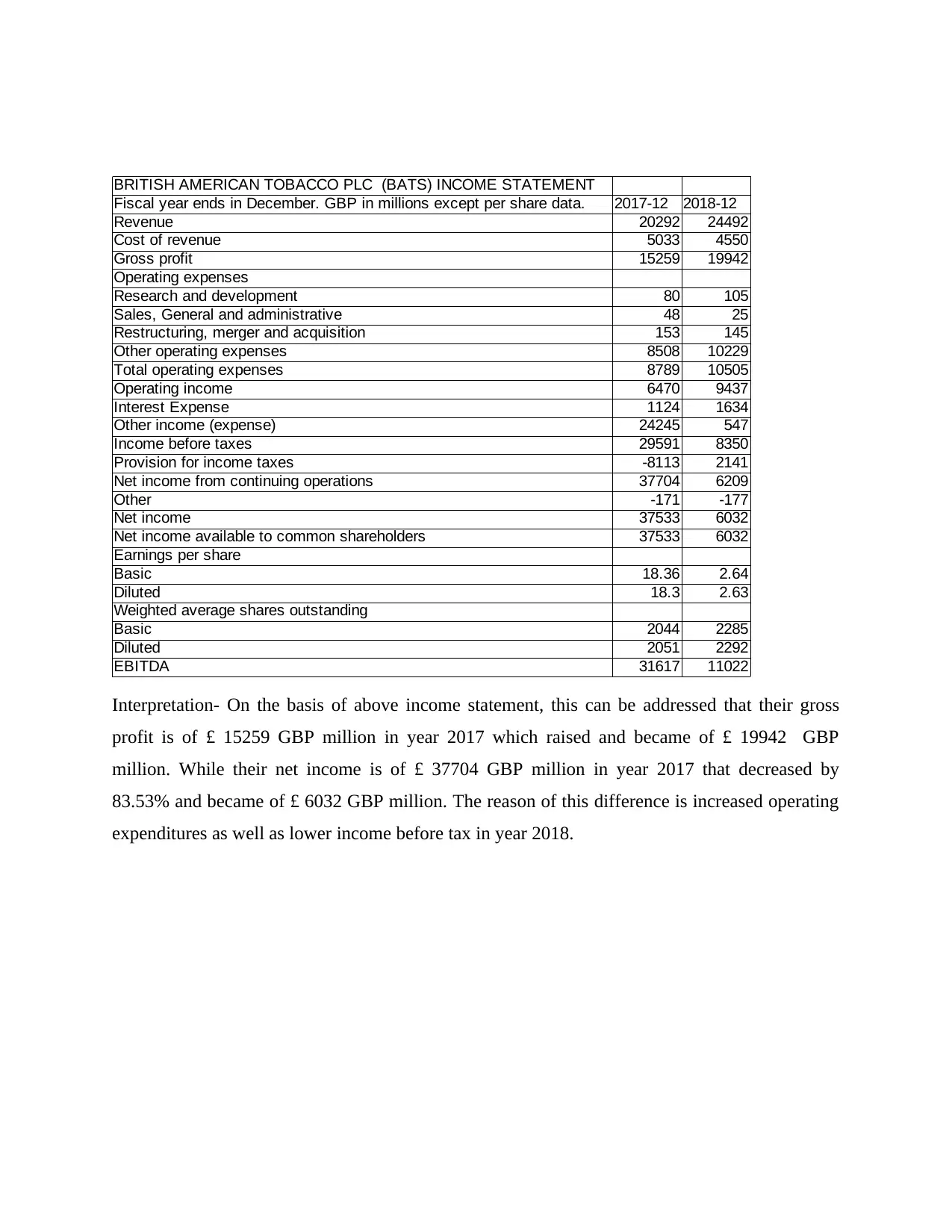

BRITISH AMERICAN TOBACCO PLC (BATS) INCOME STATEMENT

Fiscal year ends in December. GBP in millions except per share data. 2017-12 2018-12

Revenue 20292 24492

Cost of revenue 5033 4550

Gross profit 15259 19942

Operating expenses

Research and development 80 105

Sales, General and administrative 48 25

Restructuring, merger and acquisition 153 145

Other operating expenses 8508 10229

Total operating expenses 8789 10505

Operating income 6470 9437

Interest Expense 1124 1634

Other income (expense) 24245 547

Income before taxes 29591 8350

Provision for income taxes -8113 2141

Net income from continuing operations 37704 6209

Other -171 -177

Net income 37533 6032

Net income available to common shareholders 37533 6032

Earnings per share

Basic 18.36 2.64

Diluted 18.3 2.63

Weighted average shares outstanding

Basic 2044 2285

Diluted 2051 2292

EBITDA 31617 11022

Interpretation- On the basis of above income statement, this can be addressed that their gross

profit is of £ 15259 GBP million in year 2017 which raised and became of £ 19942 GBP

million. While their net income is of £ 37704 GBP million in year 2017 that decreased by

83.53% and became of £ 6032 GBP million. The reason of this difference is increased operating

expenditures as well as lower income before tax in year 2018.

Fiscal year ends in December. GBP in millions except per share data. 2017-12 2018-12

Revenue 20292 24492

Cost of revenue 5033 4550

Gross profit 15259 19942

Operating expenses

Research and development 80 105

Sales, General and administrative 48 25

Restructuring, merger and acquisition 153 145

Other operating expenses 8508 10229

Total operating expenses 8789 10505

Operating income 6470 9437

Interest Expense 1124 1634

Other income (expense) 24245 547

Income before taxes 29591 8350

Provision for income taxes -8113 2141

Net income from continuing operations 37704 6209

Other -171 -177

Net income 37533 6032

Net income available to common shareholders 37533 6032

Earnings per share

Basic 18.36 2.64

Diluted 18.3 2.63

Weighted average shares outstanding

Basic 2044 2285

Diluted 2051 2292

EBITDA 31617 11022

Interpretation- On the basis of above income statement, this can be addressed that their gross

profit is of £ 15259 GBP million in year 2017 which raised and became of £ 19942 GBP

million. While their net income is of £ 37704 GBP million in year 2017 that decreased by

83.53% and became of £ 6032 GBP million. The reason of this difference is increased operating

expenditures as well as lower income before tax in year 2018.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Balance sheet of British American Tobacco company

BRITISH AMERICAN TOBACCO PLC (BATS) BALANCE SHEET

Fiscal year ends in December. GBP in millions except per share data. 2017-12 2018-12

Assets

Current assets

Cash

Cash and cash equivalents 3131 2432

Short-term investments 65 178

Total cash 3196 2610

Receivables 4053 3588

Inventories 5864 6029

Other current assets 853 428

Total current assets 13966 12655

Non-current assets

Property, plant and equipment

Gross property, plant and equipment 8191 8654

Accumulated Depreciation -3309 -3488

Net property, plant and equipment 4882 5166

Goodwill 44147 46163

Intangible assets 73638 77850

Deferred income taxes 317 344

Prepaid pension benefit 1123 1147

Other long-term assets 2965 3017

Total non-current assets 127072 133687

Total assets 141038 146342

Liabilities and stockholders' equity

Liabilities

Current liabilities

Capital leases 5423 4225

Accounts payable 8847 10631

Taxes payable 720 853

Other current liabilities 554 620

Total current liabilities 15544 16329

Non-current liabilities

Deferred taxes liabilities 17129 17776

Pensions and other benefits 1821 1665

Minority interest 222 244

Other long-term liabilities 45518 44884

Total non-current liabilities 64690 64569

Total liabilities 80234 80898

Stockholders' equity

Common stock 614 614

Additional paid-in capital 26602 192

Retained earnings 36983 38557

Accumulated other comprehensive income -3395 26081

Total stockholders' equity 60804 65444

Total liabilities and stockholders' equity 141038 146342

Interpretation- As per the above balance sheet, this can be assessed that total assets of company

is of £141038 GBP million in year 2017 that raised and became of £146342 GBP million. In

BRITISH AMERICAN TOBACCO PLC (BATS) BALANCE SHEET

Fiscal year ends in December. GBP in millions except per share data. 2017-12 2018-12

Assets

Current assets

Cash

Cash and cash equivalents 3131 2432

Short-term investments 65 178

Total cash 3196 2610

Receivables 4053 3588

Inventories 5864 6029

Other current assets 853 428

Total current assets 13966 12655

Non-current assets

Property, plant and equipment

Gross property, plant and equipment 8191 8654

Accumulated Depreciation -3309 -3488

Net property, plant and equipment 4882 5166

Goodwill 44147 46163

Intangible assets 73638 77850

Deferred income taxes 317 344

Prepaid pension benefit 1123 1147

Other long-term assets 2965 3017

Total non-current assets 127072 133687

Total assets 141038 146342

Liabilities and stockholders' equity

Liabilities

Current liabilities

Capital leases 5423 4225

Accounts payable 8847 10631

Taxes payable 720 853

Other current liabilities 554 620

Total current liabilities 15544 16329

Non-current liabilities

Deferred taxes liabilities 17129 17776

Pensions and other benefits 1821 1665

Minority interest 222 244

Other long-term liabilities 45518 44884

Total non-current liabilities 64690 64569

Total liabilities 80234 80898

Stockholders' equity

Common stock 614 614

Additional paid-in capital 26602 192

Retained earnings 36983 38557

Accumulated other comprehensive income -3395 26081

Total stockholders' equity 60804 65444

Total liabilities and stockholders' equity 141038 146342

Interpretation- As per the above balance sheet, this can be assessed that total assets of company

is of £141038 GBP million in year 2017 that raised and became of £146342 GBP million. In

compare, companies' total liabilities are of £80234 GBP million in year 2017 and in year 2018, it

is of £80898 GBP million. It shows that company has enough assets for making payment of their

liabilities.

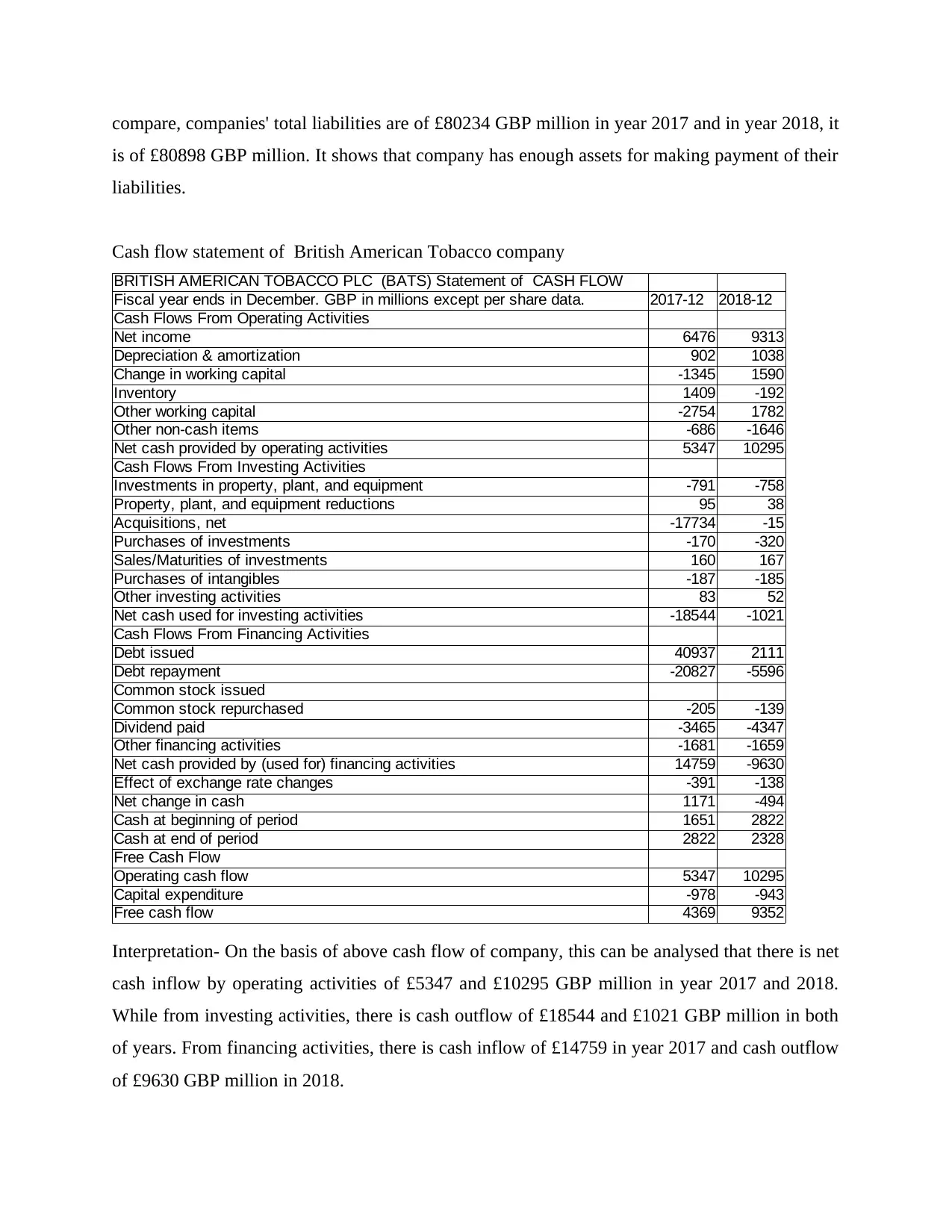

Cash flow statement of British American Tobacco company

BRITISH AMERICAN TOBACCO PLC (BATS) Statement of CASH FLOW

Fiscal year ends in December. GBP in millions except per share data. 2017-12 2018-12

Cash Flows From Operating Activities

Net income 6476 9313

Depreciation & amortization 902 1038

Change in working capital -1345 1590

Inventory 1409 -192

Other working capital -2754 1782

Other non-cash items -686 -1646

Net cash provided by operating activities 5347 10295

Cash Flows From Investing Activities

Investments in property, plant, and equipment -791 -758

Property, plant, and equipment reductions 95 38

Acquisitions, net -17734 -15

Purchases of investments -170 -320

Sales/Maturities of investments 160 167

Purchases of intangibles -187 -185

Other investing activities 83 52

Net cash used for investing activities -18544 -1021

Cash Flows From Financing Activities

Debt issued 40937 2111

Debt repayment -20827 -5596

Common stock issued

Common stock repurchased -205 -139

Dividend paid -3465 -4347

Other financing activities -1681 -1659

Net cash provided by (used for) financing activities 14759 -9630

Effect of exchange rate changes -391 -138

Net change in cash 1171 -494

Cash at beginning of period 1651 2822

Cash at end of period 2822 2328

Free Cash Flow

Operating cash flow 5347 10295

Capital expenditure -978 -943

Free cash flow 4369 9352

Interpretation- On the basis of above cash flow of company, this can be analysed that there is net

cash inflow by operating activities of £5347 and £10295 GBP million in year 2017 and 2018.

While from investing activities, there is cash outflow of £18544 and £1021 GBP million in both

of years. From financing activities, there is cash inflow of £14759 in year 2017 and cash outflow

of £9630 GBP million in 2018.

is of £80898 GBP million. It shows that company has enough assets for making payment of their

liabilities.

Cash flow statement of British American Tobacco company

BRITISH AMERICAN TOBACCO PLC (BATS) Statement of CASH FLOW

Fiscal year ends in December. GBP in millions except per share data. 2017-12 2018-12

Cash Flows From Operating Activities

Net income 6476 9313

Depreciation & amortization 902 1038

Change in working capital -1345 1590

Inventory 1409 -192

Other working capital -2754 1782

Other non-cash items -686 -1646

Net cash provided by operating activities 5347 10295

Cash Flows From Investing Activities

Investments in property, plant, and equipment -791 -758

Property, plant, and equipment reductions 95 38

Acquisitions, net -17734 -15

Purchases of investments -170 -320

Sales/Maturities of investments 160 167

Purchases of intangibles -187 -185

Other investing activities 83 52

Net cash used for investing activities -18544 -1021

Cash Flows From Financing Activities

Debt issued 40937 2111

Debt repayment -20827 -5596

Common stock issued

Common stock repurchased -205 -139

Dividend paid -3465 -4347

Other financing activities -1681 -1659

Net cash provided by (used for) financing activities 14759 -9630

Effect of exchange rate changes -391 -138

Net change in cash 1171 -494

Cash at beginning of period 1651 2822

Cash at end of period 2822 2328

Free Cash Flow

Operating cash flow 5347 10295

Capital expenditure -978 -943

Free cash flow 4369 9352

Interpretation- On the basis of above cash flow of company, this can be analysed that there is net

cash inflow by operating activities of £5347 and £10295 GBP million in year 2017 and 2018.

While from investing activities, there is cash outflow of £18544 and £1021 GBP million in both

of years. From financing activities, there is cash inflow of £14759 in year 2017 and cash outflow

of £9630 GBP million in 2018.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.