Financial Reporting Analysis: Rita PLC, IFRS, and Stakeholder Impact

VerifiedAdded on 2020/07/22

|12

|3097

|63

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, focusing on the conceptual and regulatory framework of International Financial Reporting Standards (IFRS). It explores the purpose and key principles of the IFRS framework, emphasizing its role in providing relevant and reliable financial information to various stakeholders, including investors, creditors, and employees. The report identifies and discusses the main stakeholders of an organization, highlighting the importance of financial information in their decision-making processes. Furthermore, it presents the financial statements of Rita PLC, including an income statement, statement of changes in equity, and balance sheet, along with detailed working notes. The report also includes an analysis of the financial performance of Inter-Continental Group hotel, using liquidity, profitability, and solvency ratios to assess its financial health. Finally, the report sheds light on the differences between IFRS and IAS and the importance of financial reporting objectives.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

CHANGES TO ACCOUNTING REQUIREMENTS.....................................................................1

Data Collection............................................................................................................................1

REFERENCES................................................................................................................................2

Research Methodology................................................................................................................2

Customer Segmentation..............................................................................................................2

INTRODUCTION...........................................................................................................................1

CHANGES TO ACCOUNTING REQUIREMENTS.....................................................................1

Data Collection............................................................................................................................1

REFERENCES................................................................................................................................2

Research Methodology................................................................................................................2

Customer Segmentation..............................................................................................................2

INTRODUCTION

Financial reporting for any organisation is important in order to disclose its financial

information. It includes financial statements like income statement, statement of changes in

equity, statement of financial position and cash flow statement. Financial reporting of any

organisation is subjected to the principles and regulatory framework of various standards. The

present report provides the conceptual and regulatory framework of IFRS. It also determines the

key stakeholders of an organisation and importance of financial information to them. In the

present report, financial statements of Rita plc have been prepared along with the analysis of

financial performance of Inter-Continental Group hotel using ratio analysis. The study also shed

some light on difference between IFRS and IAS.

Purpose and key principles of regulatory framework

To define the nature and purpose of accounting, conceptual and regulatory framework

has been provided. These principles consider the theoretical issues and conceptual issues that are

surrounded to the financial reporting. These principles and framework are referred as Generally

Accepted Accounting Principle (GAAP), in accordance to the financial reporting. The

conceptual framework of financial reporting provides theoretical basis to determine and

communicate the financial information to its users (Conceptual Framework for Financial

Reporting, 2017). The main motive of financial reporting is to provide the necessary information

to its users that can affect the economic decision making. IFRS framework addresses to:

Financial reporting objectives:

To provide information that is used to take future economic decisions regarding, holding,

selling or buying debt or equity instruments to the primary users of financial reporting.

Potential users include lenders, investors, creditors, etc. Financial information is also used by its users to identify the responsibility of

management in effectual utilisation of the organisation's existing resources and not only

to assess the cash flows of the company.

Reporting entity

1

Financial reporting for any organisation is important in order to disclose its financial

information. It includes financial statements like income statement, statement of changes in

equity, statement of financial position and cash flow statement. Financial reporting of any

organisation is subjected to the principles and regulatory framework of various standards. The

present report provides the conceptual and regulatory framework of IFRS. It also determines the

key stakeholders of an organisation and importance of financial information to them. In the

present report, financial statements of Rita plc have been prepared along with the analysis of

financial performance of Inter-Continental Group hotel using ratio analysis. The study also shed

some light on difference between IFRS and IAS.

Purpose and key principles of regulatory framework

To define the nature and purpose of accounting, conceptual and regulatory framework

has been provided. These principles consider the theoretical issues and conceptual issues that are

surrounded to the financial reporting. These principles and framework are referred as Generally

Accepted Accounting Principle (GAAP), in accordance to the financial reporting. The

conceptual framework of financial reporting provides theoretical basis to determine and

communicate the financial information to its users (Conceptual Framework for Financial

Reporting, 2017). The main motive of financial reporting is to provide the necessary information

to its users that can affect the economic decision making. IFRS framework addresses to:

Financial reporting objectives:

To provide information that is used to take future economic decisions regarding, holding,

selling or buying debt or equity instruments to the primary users of financial reporting.

Potential users include lenders, investors, creditors, etc. Financial information is also used by its users to identify the responsibility of

management in effectual utilisation of the organisation's existing resources and not only

to assess the cash flows of the company.

Reporting entity

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

An entity that that need to report its financial information to its users is termed as

reporting entity. It is also known as accounting entity. All the entities that are part of some another company or are the subsidiary or the parent

company of any other entity are also the reporting entity (Ahmed, Neel and Wang, 2013).

Parent company should report its financial statements in consolidated form.

Qualitative features of financial information:

Along with the quantitative features, financial information must also persist some

qualitative feature that make the report more understandable and reliable. Report having

qualitative features could provide the most important and useful information to its users that

helps them in taking future economic decisions. Therefore, financial information of any entity

should contain the following qualitative features:

Materiality: This refers to a specific information of an entity. Materiality refers to the

importance. Entity should only provide that information that could be material for any

user in its decision. Accountants and auditor of the company should consider the aspect

of materiality in the financial information.

Understandability: an information to be understandable should be presented in such a

form that can be comprehend by the reader easily.

Relevance: Information presented in the financial reporting should only be related to the

reporting entity. This refers the characteristic of relevance. Relevant financial information

can make a significant difference in the decision making of the users because it contains

both predictive value and confirmatory value (Bonetti, Magnan and Parbonetti, 2016).

Comparability: Another qualitative characteristic a report must contain is comparability.

That means users must be able to compare the financial performance of the company with

another companies or across the period. Faithful Representation: Financial reports of the company should depict true and fair

view. That means the data present in financial report should be free from misstatement.

Others:

2

reporting entity. It is also known as accounting entity. All the entities that are part of some another company or are the subsidiary or the parent

company of any other entity are also the reporting entity (Ahmed, Neel and Wang, 2013).

Parent company should report its financial statements in consolidated form.

Qualitative features of financial information:

Along with the quantitative features, financial information must also persist some

qualitative feature that make the report more understandable and reliable. Report having

qualitative features could provide the most important and useful information to its users that

helps them in taking future economic decisions. Therefore, financial information of any entity

should contain the following qualitative features:

Materiality: This refers to a specific information of an entity. Materiality refers to the

importance. Entity should only provide that information that could be material for any

user in its decision. Accountants and auditor of the company should consider the aspect

of materiality in the financial information.

Understandability: an information to be understandable should be presented in such a

form that can be comprehend by the reader easily.

Relevance: Information presented in the financial reporting should only be related to the

reporting entity. This refers the characteristic of relevance. Relevant financial information

can make a significant difference in the decision making of the users because it contains

both predictive value and confirmatory value (Bonetti, Magnan and Parbonetti, 2016).

Comparability: Another qualitative characteristic a report must contain is comparability.

That means users must be able to compare the financial performance of the company with

another companies or across the period. Faithful Representation: Financial reports of the company should depict true and fair

view. That means the data present in financial report should be free from misstatement.

Others:

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial statement's definition and meaning.

Capital and capital framework concepts.

Recognition and measurement criteria of information presented in the financial

statements.

Main stakeholders of an organisation

Stakeholders for any company are those persons and group of persons that have potential

interest in the activities of the organisation. These are the main pillars of the organisation

because without their support, an organisation will not be able to perform its activities effectively

and will cease to exist. Main stakeholders can be decided into two segments:

External stakeholders:

Customers: A company operates to provide products and services to its customers i.e. goods or

services in which a company deals in is for the need of its customers. Therefore, every

organisation in order to survive need more and more customers. Priority of the company should

be the need of its customers. These stakeholders are the one who have an ability to make a

business successful or unsuccessful. Therefore, company must keep innovating its goods and

services and the rate that it offers should provide a good value of money in order to retain its

customers.

Creditors: Creditors are those stakeholders that lends their money to finance the business unit for

its ventures, assets or short term and long-term requirements (Brigham, 2014.). This mainly

includes banks and financial institutions that provides loan to the company for its major

purchases of fixed assets or inventories. Therefore, main expectation of these stakeholders from

the company is that it meets the payment requirements responsibly at time.

Other business partners: For smooth running of the business, an organisation need to maintain

good and healthy relations with its other business partners. Healthy long-term relationships with

other business partners can help the company in succeeding in long run. Through Good relations

with suppliers, company can achieve in making better strategies and its organisational goals and

objectives. Suppliers and other business partners are the most critical stakeholders in today's era.

3

Capital and capital framework concepts.

Recognition and measurement criteria of information presented in the financial

statements.

Main stakeholders of an organisation

Stakeholders for any company are those persons and group of persons that have potential

interest in the activities of the organisation. These are the main pillars of the organisation

because without their support, an organisation will not be able to perform its activities effectively

and will cease to exist. Main stakeholders can be decided into two segments:

External stakeholders:

Customers: A company operates to provide products and services to its customers i.e. goods or

services in which a company deals in is for the need of its customers. Therefore, every

organisation in order to survive need more and more customers. Priority of the company should

be the need of its customers. These stakeholders are the one who have an ability to make a

business successful or unsuccessful. Therefore, company must keep innovating its goods and

services and the rate that it offers should provide a good value of money in order to retain its

customers.

Creditors: Creditors are those stakeholders that lends their money to finance the business unit for

its ventures, assets or short term and long-term requirements (Brigham, 2014.). This mainly

includes banks and financial institutions that provides loan to the company for its major

purchases of fixed assets or inventories. Therefore, main expectation of these stakeholders from

the company is that it meets the payment requirements responsibly at time.

Other business partners: For smooth running of the business, an organisation need to maintain

good and healthy relations with its other business partners. Healthy long-term relationships with

other business partners can help the company in succeeding in long run. Through Good relations

with suppliers, company can achieve in making better strategies and its organisational goals and

objectives. Suppliers and other business partners are the most critical stakeholders in today's era.

3

Government: Every country has its own rules and regulations; therefore, organisations need to

adhere to those rules and regulations of the country in which they are situated (Brüggemann, Hitz

and Sellhorn, 2013). Compliance with rules and regulations helps the companies in avoiding

prosecutions and disputes. Activities and decisions of government have significant affect to the

operational activities of an organisation. Therefore, maintaining good relations with government

and other local authority is also essential for any company.

Internal stakeholders:

Employees: Workers and employees for any company are the main active and working

stakeholders. As they are the one who produce the services and products of the company in

which it deals with. Employees are the one who make an organisation. Retention of employee in

the organisation should be the main aim of the organisation. Antagonize of company's employee

may suffer it services.

Shareholders: Shareholders of the company are considered as the owners. They invest amount in

the company as capital to bring the organisation in existence (Leuz and Wysocki, 2016). Need of

the shareholders should be the main priority of the company. Board of directors acts on the

behalf of shareholders, therefore board could be replaced any time if they will not act

responsibly.

Importance of financial information to stakeholders:

Stakeholders take economic decisions regarding their investments by analysing the

financial information of the company. Therefore, where the investments of the entity are heading

is main concern of the stakeholders. Following are the importance of financial information to the

stakeholders:

To determine how efficient are the operations of the company.

To identify the overall revenues and expenses of the company.

To determine whether the company is earning profits or is suffering from loss.

To assess the optimum utilisation of company's resources.

Future business expansion opportunities of the company.

4

adhere to those rules and regulations of the country in which they are situated (Brüggemann, Hitz

and Sellhorn, 2013). Compliance with rules and regulations helps the companies in avoiding

prosecutions and disputes. Activities and decisions of government have significant affect to the

operational activities of an organisation. Therefore, maintaining good relations with government

and other local authority is also essential for any company.

Internal stakeholders:

Employees: Workers and employees for any company are the main active and working

stakeholders. As they are the one who produce the services and products of the company in

which it deals with. Employees are the one who make an organisation. Retention of employee in

the organisation should be the main aim of the organisation. Antagonize of company's employee

may suffer it services.

Shareholders: Shareholders of the company are considered as the owners. They invest amount in

the company as capital to bring the organisation in existence (Leuz and Wysocki, 2016). Need of

the shareholders should be the main priority of the company. Board of directors acts on the

behalf of shareholders, therefore board could be replaced any time if they will not act

responsibly.

Importance of financial information to stakeholders:

Stakeholders take economic decisions regarding their investments by analysing the

financial information of the company. Therefore, where the investments of the entity are heading

is main concern of the stakeholders. Following are the importance of financial information to the

stakeholders:

To determine how efficient are the operations of the company.

To identify the overall revenues and expenses of the company.

To determine whether the company is earning profits or is suffering from loss.

To assess the optimum utilisation of company's resources.

Future business expansion opportunities of the company.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

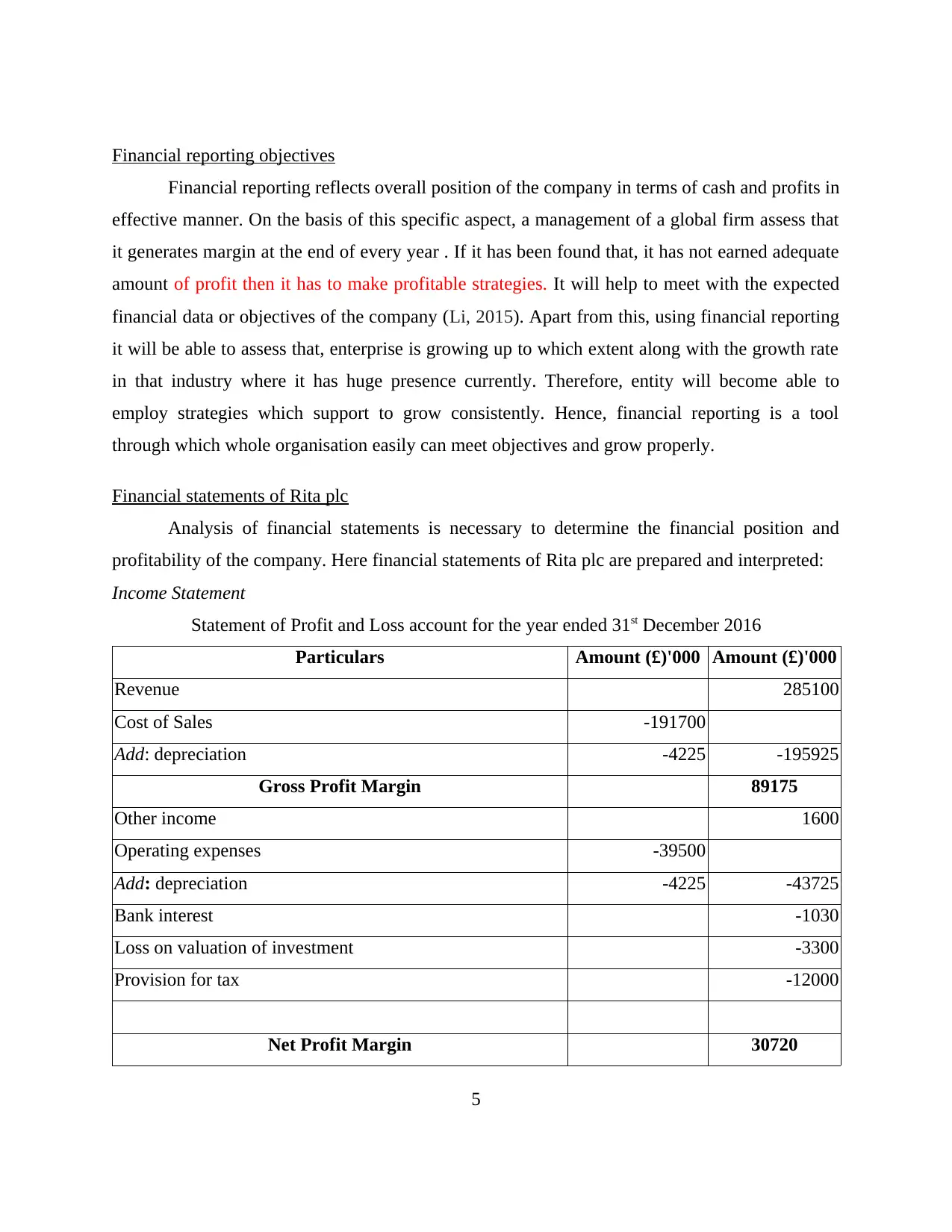

Financial reporting objectives

Financial reporting reflects overall position of the company in terms of cash and profits in

effective manner. On the basis of this specific aspect, a management of a global firm assess that

it generates margin at the end of every year . If it has been found that, it has not earned adequate

amount of profit then it has to make profitable strategies. It will help to meet with the expected

financial data or objectives of the company (Li, 2015). Apart from this, using financial reporting

it will be able to assess that, enterprise is growing up to which extent along with the growth rate

in that industry where it has huge presence currently. Therefore, entity will become able to

employ strategies which support to grow consistently. Hence, financial reporting is a tool

through which whole organisation easily can meet objectives and grow properly.

Financial statements of Rita plc

Analysis of financial statements is necessary to determine the financial position and

profitability of the company. Here financial statements of Rita plc are prepared and interpreted:

Income Statement

Statement of Profit and Loss account for the year ended 31st December 2016

Particulars Amount (£)'000 Amount (£)'000

Revenue 285100

Cost of Sales -191700

Add: depreciation -4225 -195925

Gross Profit Margin 89175

Other income 1600

Operating expenses -39500

Add: depreciation -4225 -43725

Bank interest -1030

Loss on valuation of investment -3300

Provision for tax -12000

Net Profit Margin 30720

5

Financial reporting reflects overall position of the company in terms of cash and profits in

effective manner. On the basis of this specific aspect, a management of a global firm assess that

it generates margin at the end of every year . If it has been found that, it has not earned adequate

amount of profit then it has to make profitable strategies. It will help to meet with the expected

financial data or objectives of the company (Li, 2015). Apart from this, using financial reporting

it will be able to assess that, enterprise is growing up to which extent along with the growth rate

in that industry where it has huge presence currently. Therefore, entity will become able to

employ strategies which support to grow consistently. Hence, financial reporting is a tool

through which whole organisation easily can meet objectives and grow properly.

Financial statements of Rita plc

Analysis of financial statements is necessary to determine the financial position and

profitability of the company. Here financial statements of Rita plc are prepared and interpreted:

Income Statement

Statement of Profit and Loss account for the year ended 31st December 2016

Particulars Amount (£)'000 Amount (£)'000

Revenue 285100

Cost of Sales -191700

Add: depreciation -4225 -195925

Gross Profit Margin 89175

Other income 1600

Operating expenses -39500

Add: depreciation -4225 -43725

Bank interest -1030

Loss on valuation of investment -3300

Provision for tax -12000

Net Profit Margin 30720

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

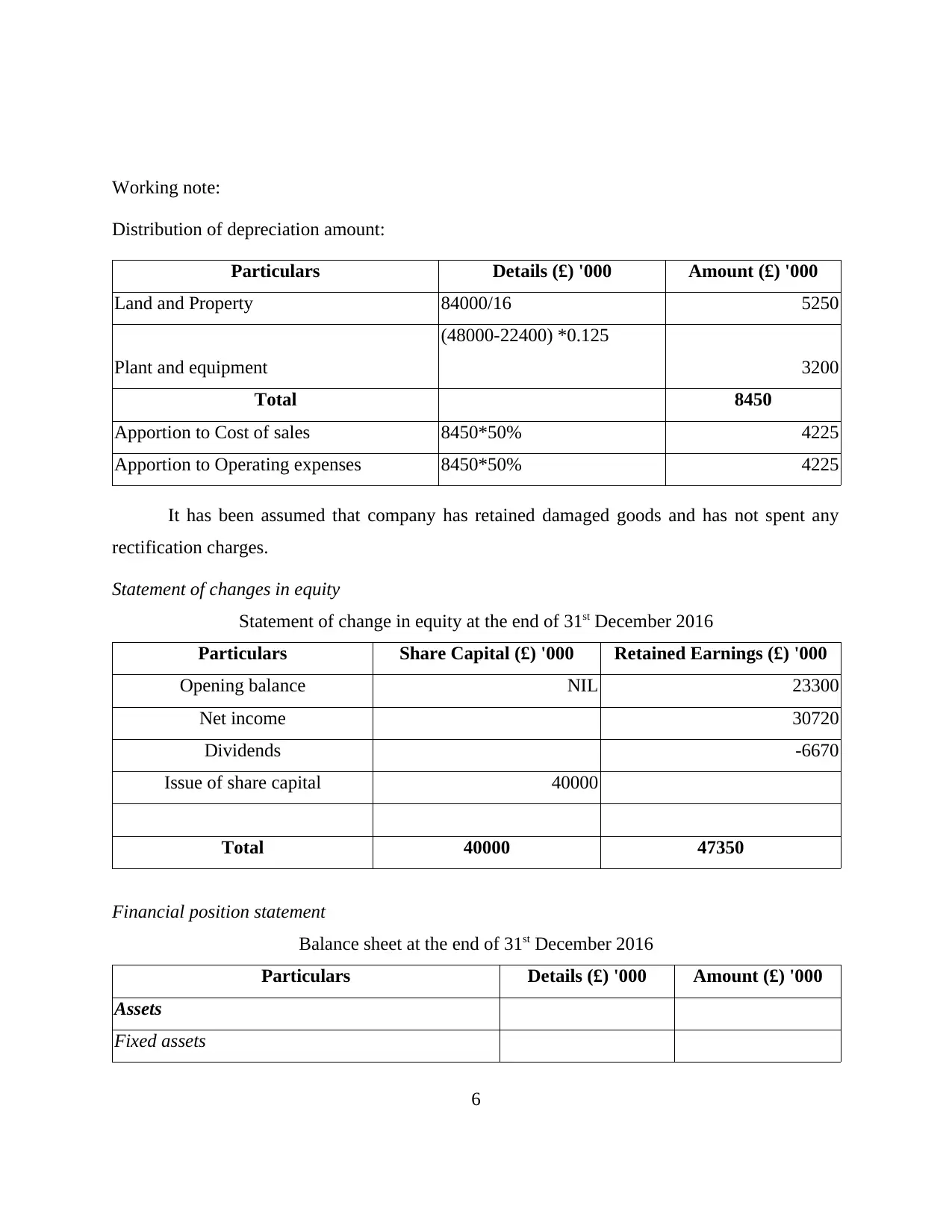

Working note:

Distribution of depreciation amount:

Particulars Details (£) '000 Amount (£) '000

Land and Property 84000/16 5250

Plant and equipment

(48000-22400) *0.125

3200

Total 8450

Apportion to Cost of sales 8450*50% 4225

Apportion to Operating expenses 8450*50% 4225

It has been assumed that company has retained damaged goods and has not spent any

rectification charges.

Statement of changes in equity

Statement of change in equity at the end of 31st December 2016

Particulars Share Capital (£) '000 Retained Earnings (£) '000

Opening balance NIL 23300

Net income 30720

Dividends -6670

Issue of share capital 40000

Total 40000 47350

Financial position statement

Balance sheet at the end of 31st December 2016

Particulars Details (£) '000 Amount (£) '000

Assets

Fixed assets

6

Distribution of depreciation amount:

Particulars Details (£) '000 Amount (£) '000

Land and Property 84000/16 5250

Plant and equipment

(48000-22400) *0.125

3200

Total 8450

Apportion to Cost of sales 8450*50% 4225

Apportion to Operating expenses 8450*50% 4225

It has been assumed that company has retained damaged goods and has not spent any

rectification charges.

Statement of changes in equity

Statement of change in equity at the end of 31st December 2016

Particulars Share Capital (£) '000 Retained Earnings (£) '000

Opening balance NIL 23300

Net income 30720

Dividends -6670

Issue of share capital 40000

Total 40000 47350

Financial position statement

Balance sheet at the end of 31st December 2016

Particulars Details (£) '000 Amount (£) '000

Assets

Fixed assets

6

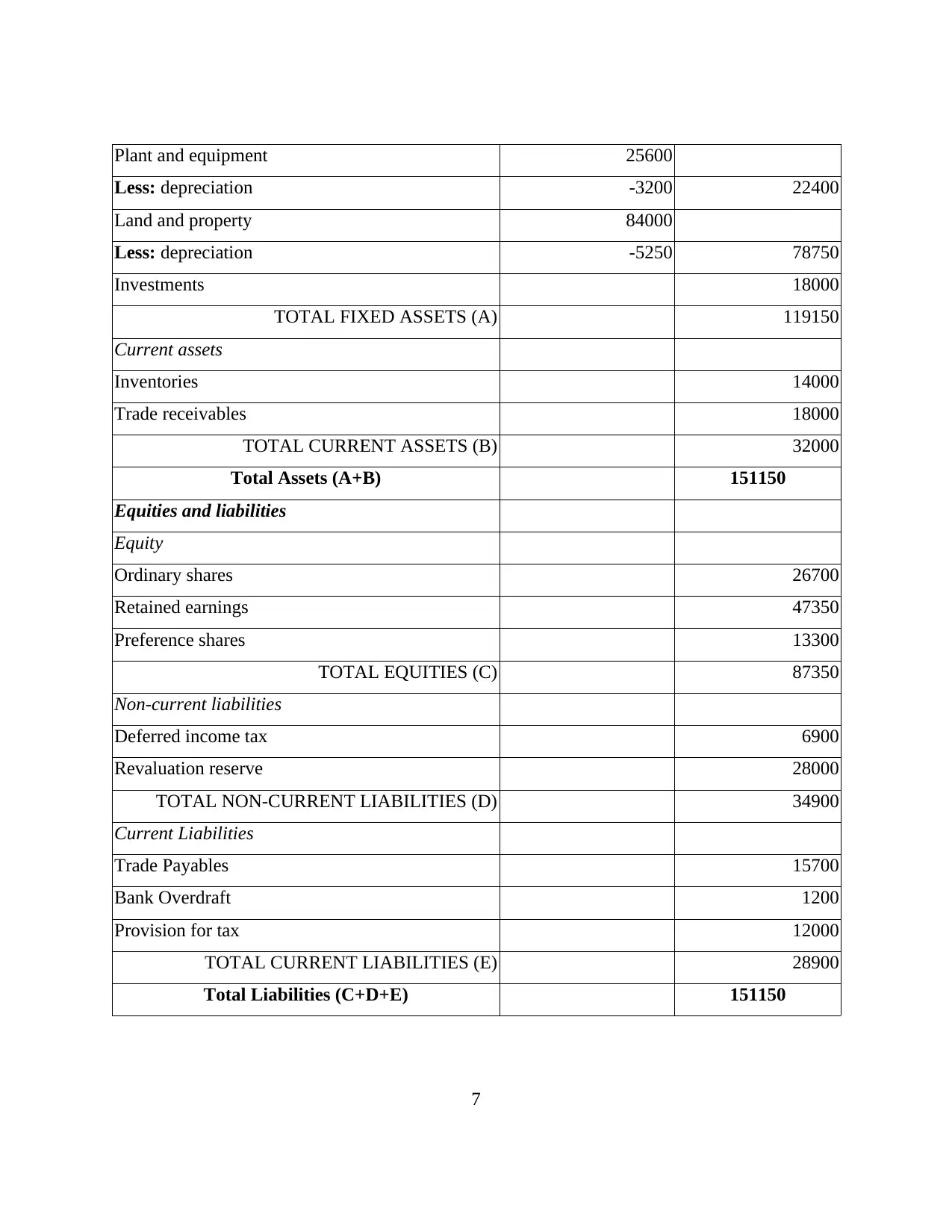

Plant and equipment 25600

Less: depreciation -3200 22400

Land and property 84000

Less: depreciation -5250 78750

Investments 18000

TOTAL FIXED ASSETS (A) 119150

Current assets

Inventories 14000

Trade receivables 18000

TOTAL CURRENT ASSETS (B) 32000

Total Assets (A+B) 151150

Equities and liabilities

Equity

Ordinary shares 26700

Retained earnings 47350

Preference shares 13300

TOTAL EQUITIES (C) 87350

Non-current liabilities

Deferred income tax 6900

Revaluation reserve 28000

TOTAL NON-CURRENT LIABILITIES (D) 34900

Current Liabilities

Trade Payables 15700

Bank Overdraft 1200

Provision for tax 12000

TOTAL CURRENT LIABILITIES (E) 28900

Total Liabilities (C+D+E) 151150

7

Less: depreciation -3200 22400

Land and property 84000

Less: depreciation -5250 78750

Investments 18000

TOTAL FIXED ASSETS (A) 119150

Current assets

Inventories 14000

Trade receivables 18000

TOTAL CURRENT ASSETS (B) 32000

Total Assets (A+B) 151150

Equities and liabilities

Equity

Ordinary shares 26700

Retained earnings 47350

Preference shares 13300

TOTAL EQUITIES (C) 87350

Non-current liabilities

Deferred income tax 6900

Revaluation reserve 28000

TOTAL NON-CURRENT LIABILITIES (D) 34900

Current Liabilities

Trade Payables 15700

Bank Overdraft 1200

Provision for tax 12000

TOTAL CURRENT LIABILITIES (E) 28900

Total Liabilities (C+D+E) 151150

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

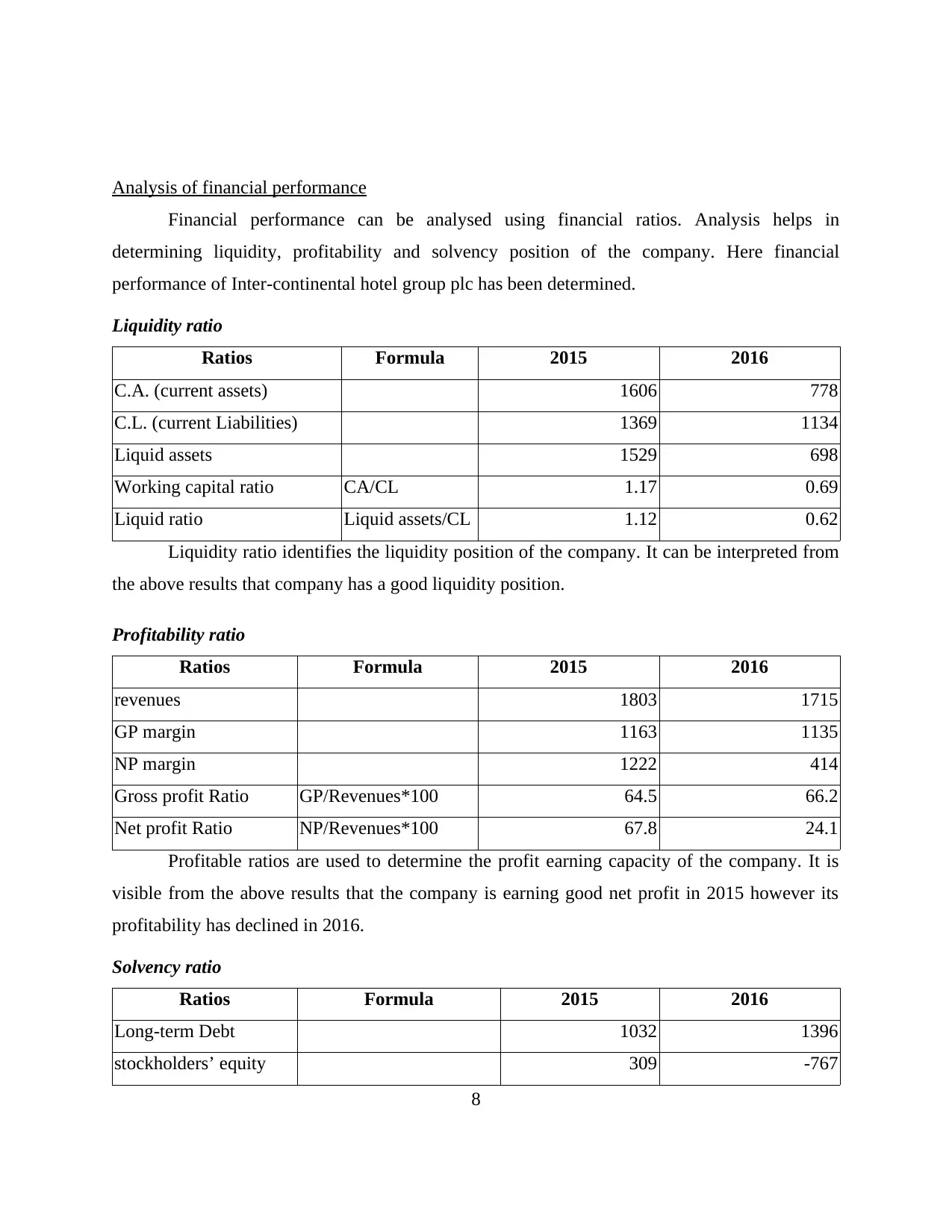

Analysis of financial performance

Financial performance can be analysed using financial ratios. Analysis helps in

determining liquidity, profitability and solvency position of the company. Here financial

performance of Inter-continental hotel group plc has been determined.

Liquidity ratio

Ratios Formula 2015 2016

C.A. (current assets) 1606 778

C.L. (current Liabilities) 1369 1134

Liquid assets 1529 698

Working capital ratio CA/CL 1.17 0.69

Liquid ratio Liquid assets/CL 1.12 0.62

Liquidity ratio identifies the liquidity position of the company. It can be interpreted from

the above results that company has a good liquidity position.

Profitability ratio

Ratios Formula 2015 2016

revenues 1803 1715

GP margin 1163 1135

NP margin 1222 414

Gross profit Ratio GP/Revenues*100 64.5 66.2

Net profit Ratio NP/Revenues*100 67.8 24.1

Profitable ratios are used to determine the profit earning capacity of the company. It is

visible from the above results that the company is earning good net profit in 2015 however its

profitability has declined in 2016.

Solvency ratio

Ratios Formula 2015 2016

Long-term Debt 1032 1396

stockholders’ equity 309 -767

8

Financial performance can be analysed using financial ratios. Analysis helps in

determining liquidity, profitability and solvency position of the company. Here financial

performance of Inter-continental hotel group plc has been determined.

Liquidity ratio

Ratios Formula 2015 2016

C.A. (current assets) 1606 778

C.L. (current Liabilities) 1369 1134

Liquid assets 1529 698

Working capital ratio CA/CL 1.17 0.69

Liquid ratio Liquid assets/CL 1.12 0.62

Liquidity ratio identifies the liquidity position of the company. It can be interpreted from

the above results that company has a good liquidity position.

Profitability ratio

Ratios Formula 2015 2016

revenues 1803 1715

GP margin 1163 1135

NP margin 1222 414

Gross profit Ratio GP/Revenues*100 64.5 66.2

Net profit Ratio NP/Revenues*100 67.8 24.1

Profitable ratios are used to determine the profit earning capacity of the company. It is

visible from the above results that the company is earning good net profit in 2015 however its

profitability has declined in 2016.

Solvency ratio

Ratios Formula 2015 2016

Long-term Debt 1032 1396

stockholders’ equity 309 -767

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

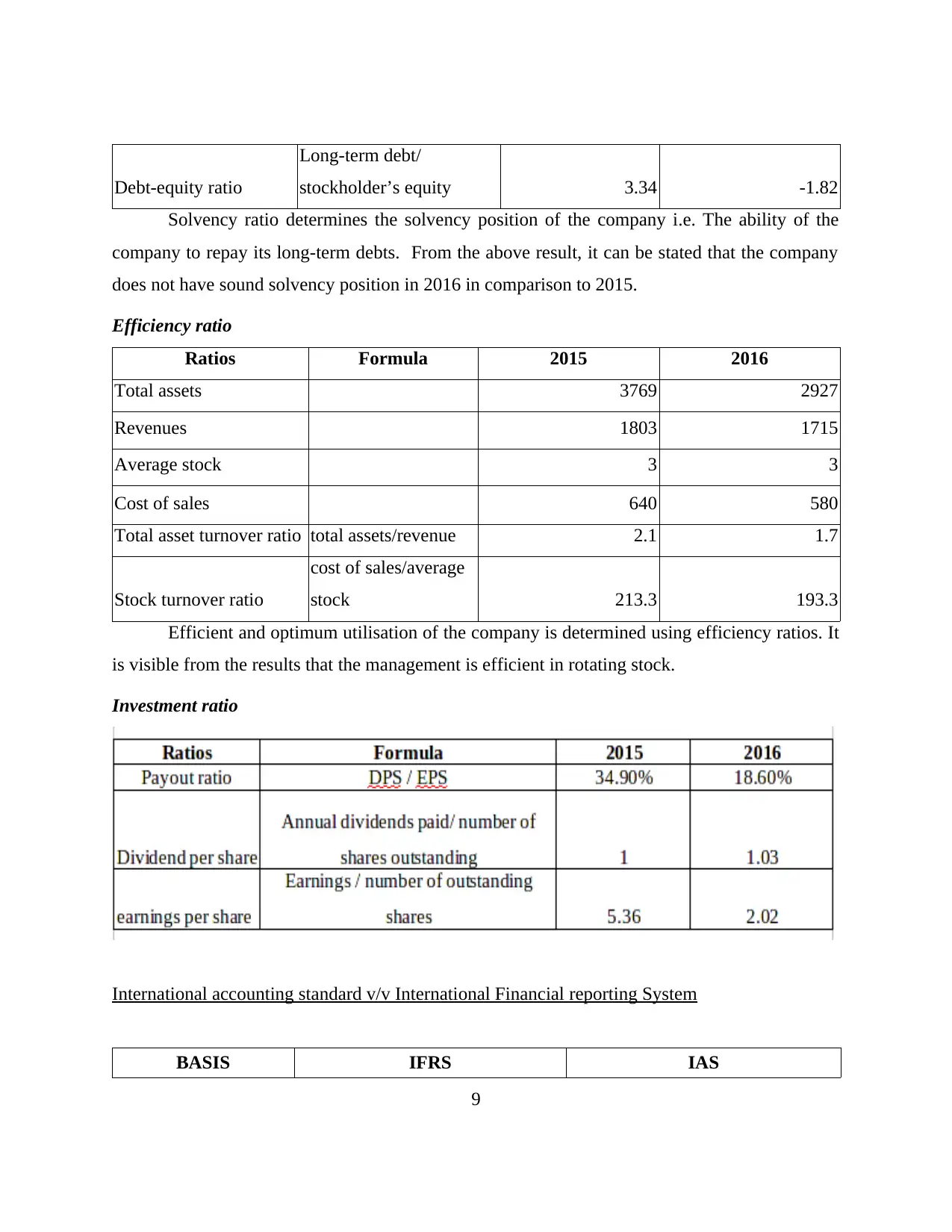

Debt-equity ratio

Long-term debt/

stockholder’s equity 3.34 -1.82

Solvency ratio determines the solvency position of the company i.e. The ability of the

company to repay its long-term debts. From the above result, it can be stated that the company

does not have sound solvency position in 2016 in comparison to 2015.

Efficiency ratio

Ratios Formula 2015 2016

Total assets 3769 2927

Revenues 1803 1715

Average stock 3 3

Cost of sales 640 580

Total asset turnover ratio total assets/revenue 2.1 1.7

Stock turnover ratio

cost of sales/average

stock 213.3 193.3

Efficient and optimum utilisation of the company is determined using efficiency ratios. It

is visible from the results that the management is efficient in rotating stock.

Investment ratio

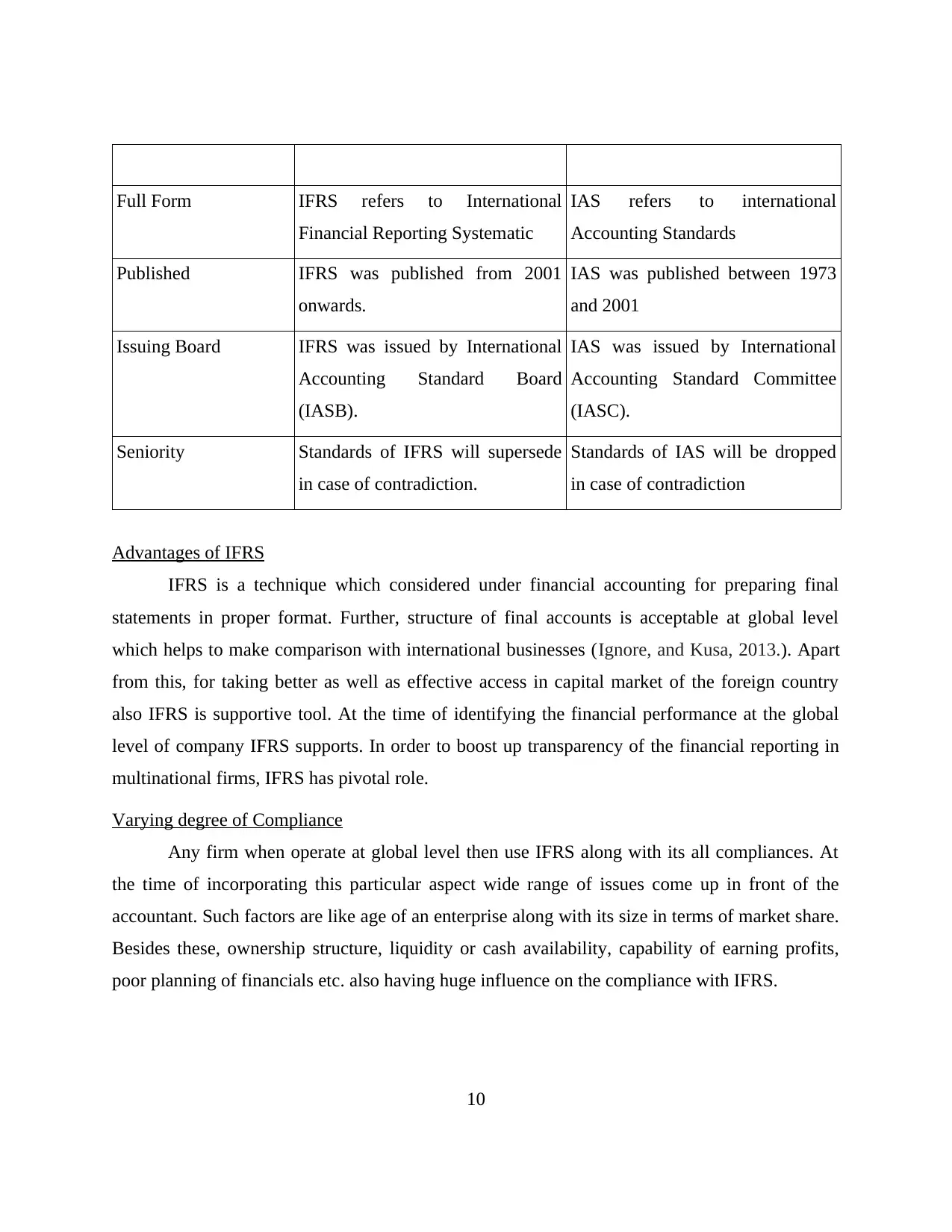

International accounting standard v/v International Financial reporting System

BASIS IFRS IAS

9

Long-term debt/

stockholder’s equity 3.34 -1.82

Solvency ratio determines the solvency position of the company i.e. The ability of the

company to repay its long-term debts. From the above result, it can be stated that the company

does not have sound solvency position in 2016 in comparison to 2015.

Efficiency ratio

Ratios Formula 2015 2016

Total assets 3769 2927

Revenues 1803 1715

Average stock 3 3

Cost of sales 640 580

Total asset turnover ratio total assets/revenue 2.1 1.7

Stock turnover ratio

cost of sales/average

stock 213.3 193.3

Efficient and optimum utilisation of the company is determined using efficiency ratios. It

is visible from the results that the management is efficient in rotating stock.

Investment ratio

International accounting standard v/v International Financial reporting System

BASIS IFRS IAS

9

Full Form IFRS refers to International

Financial Reporting Systematic

IAS refers to international

Accounting Standards

Published IFRS was published from 2001

onwards.

IAS was published between 1973

and 2001

Issuing Board IFRS was issued by International

Accounting Standard Board

(IASB).

IAS was issued by International

Accounting Standard Committee

(IASC).

Seniority Standards of IFRS will supersede

in case of contradiction.

Standards of IAS will be dropped

in case of contradiction

Advantages of IFRS

IFRS is a technique which considered under financial accounting for preparing final

statements in proper format. Further, structure of final accounts is acceptable at global level

which helps to make comparison with international businesses (Ignore, and Kusa, 2013.). Apart

from this, for taking better as well as effective access in capital market of the foreign country

also IFRS is supportive tool. At the time of identifying the financial performance at the global

level of company IFRS supports. In order to boost up transparency of the financial reporting in

multinational firms, IFRS has pivotal role.

Varying degree of Compliance

Any firm when operate at global level then use IFRS along with its all compliances. At

the time of incorporating this particular aspect wide range of issues come up in front of the

accountant. Such factors are like age of an enterprise along with its size in terms of market share.

Besides these, ownership structure, liquidity or cash availability, capability of earning profits,

poor planning of financials etc. also having huge influence on the compliance with IFRS.

10

Financial Reporting Systematic

IAS refers to international

Accounting Standards

Published IFRS was published from 2001

onwards.

IAS was published between 1973

and 2001

Issuing Board IFRS was issued by International

Accounting Standard Board

(IASB).

IAS was issued by International

Accounting Standard Committee

(IASC).

Seniority Standards of IFRS will supersede

in case of contradiction.

Standards of IAS will be dropped

in case of contradiction

Advantages of IFRS

IFRS is a technique which considered under financial accounting for preparing final

statements in proper format. Further, structure of final accounts is acceptable at global level

which helps to make comparison with international businesses (Ignore, and Kusa, 2013.). Apart

from this, for taking better as well as effective access in capital market of the foreign country

also IFRS is supportive tool. At the time of identifying the financial performance at the global

level of company IFRS supports. In order to boost up transparency of the financial reporting in

multinational firms, IFRS has pivotal role.

Varying degree of Compliance

Any firm when operate at global level then use IFRS along with its all compliances. At

the time of incorporating this particular aspect wide range of issues come up in front of the

accountant. Such factors are like age of an enterprise along with its size in terms of market share.

Besides these, ownership structure, liquidity or cash availability, capability of earning profits,

poor planning of financials etc. also having huge influence on the compliance with IFRS.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.