Financial Reporting: BT Group Plc Financial Statement Analysis

VerifiedAdded on 2021/02/21

|17

|4672

|56

Report

AI Summary

This report provides a detailed analysis of financial reporting, focusing on BT Group Plc. It begins by defining financial reporting and its context, emphasizing its importance for internal and external stakeholders. The report then explores the conceptual and regulatory frameworks, including qualitative characteristics of financial information, and identifies key stakeholders and how they benefit from financial data. It further examines the value of financial reporting in meeting organizational objectives and growth, followed by an overview of the preparation of different financial statements, including examples of adjustments and calculations. The report also addresses the interpretation and communication of financial performance, differences between IAS and IFRS, benefits of IFRS, and varying degrees of compliance. The analysis includes specific examples related to BT Group Plc, such as the application of accounting principles and the impact of financial reporting on stakeholder decisions. The report concludes by summarizing the key findings and their implications for BT Group Plc's financial management and strategic decision-making.

Financial

Reporting

Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Context and purpose of financial reporting.............................................................................1

2. Conceptual and regulatory framework with qualitative characteristics of financial

information...................................................................................................................................2

3. Main key stakeholders of an organisation and the way in which they get benefited from

financial information....................................................................................................................3

4. Value of financial reporting for meeting organisational objectives and growth.....................4

5. Preparation of different financial statements...........................................................................5

6. Use of financial statements for interpreting and communicating financial performance of

organisation..................................................................................................................................8

7. Difference between IAS and IFRS........................................................................................11

8. Different benefits of IFRS.....................................................................................................11

9. Varying degrees of compliance with IFRS............................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Context and purpose of financial reporting.............................................................................1

2. Conceptual and regulatory framework with qualitative characteristics of financial

information...................................................................................................................................2

3. Main key stakeholders of an organisation and the way in which they get benefited from

financial information....................................................................................................................3

4. Value of financial reporting for meeting organisational objectives and growth.....................4

5. Preparation of different financial statements...........................................................................5

6. Use of financial statements for interpreting and communicating financial performance of

organisation..................................................................................................................................8

7. Difference between IAS and IFRS........................................................................................11

8. Different benefits of IFRS.....................................................................................................11

9. Varying degrees of compliance with IFRS............................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Financial reporting can be defined as the process which is followed by business entities to

record all the financial data in the books of accounting. Main purpose of it is to determine actual

position of the company within the market so that appropriate information regarding it could be

rendered to internal and external stakeholders (Albring, Elder and Xu, 2018). With the help of it

accounting professional and managers can formulate strategies decisions for future so that

performance of business could be enhanced. The organisation which is selected for this report is

BT Group Plc which is British Multinational Telecommunication enterprise. It is mainly

established in London, United Kingdom and founded in year 1969. This assignment covers

various topics such as context and purpose of financial reporting, the way in which it helps to

meet organisational objectives and growth, conceptual and regulatory framework, main

stakeholders etc. Along with this, interpretation and communication of financial performance,

different between IAS and IFRS, benefits of IFRS and varying degrees of compliance are also

covered under this project.

MAIN BODY

1. Context and purpose of financial reporting

Context of financial reporting: The process which is used by business entities to

communicate business information with all the internal and external stakeholders is known as

financial reporting. For all the organisations such as BT Group Plc it is very important to conduct

it on yearly basis so that large number of investors could be attracted and long term objectives

could be achieved. It also guides managers and other top executives to determine that the efforts

which were made by them for betterment of business. If companies are not able to form final

accounts appropriately then it may leave negative impact upon the activities which are performed

for business execution.

In order to reach the objective of profit maximisation, customer satisfaction and attracting

investors it is very important for BT Group Plc to make sure that financial reporting is conducted

on yearly basis (Chen and Gavious, 2017). With the help of it actual status of business could be

determined which helps to reach business goals. Different types of statements such as income

statement, balance sheet and cash flow statement. With the help of them stakeholders such as

1

Financial reporting can be defined as the process which is followed by business entities to

record all the financial data in the books of accounting. Main purpose of it is to determine actual

position of the company within the market so that appropriate information regarding it could be

rendered to internal and external stakeholders (Albring, Elder and Xu, 2018). With the help of it

accounting professional and managers can formulate strategies decisions for future so that

performance of business could be enhanced. The organisation which is selected for this report is

BT Group Plc which is British Multinational Telecommunication enterprise. It is mainly

established in London, United Kingdom and founded in year 1969. This assignment covers

various topics such as context and purpose of financial reporting, the way in which it helps to

meet organisational objectives and growth, conceptual and regulatory framework, main

stakeholders etc. Along with this, interpretation and communication of financial performance,

different between IAS and IFRS, benefits of IFRS and varying degrees of compliance are also

covered under this project.

MAIN BODY

1. Context and purpose of financial reporting

Context of financial reporting: The process which is used by business entities to

communicate business information with all the internal and external stakeholders is known as

financial reporting. For all the organisations such as BT Group Plc it is very important to conduct

it on yearly basis so that large number of investors could be attracted and long term objectives

could be achieved. It also guides managers and other top executives to determine that the efforts

which were made by them for betterment of business. If companies are not able to form final

accounts appropriately then it may leave negative impact upon the activities which are performed

for business execution.

In order to reach the objective of profit maximisation, customer satisfaction and attracting

investors it is very important for BT Group Plc to make sure that financial reporting is conducted

on yearly basis (Chen and Gavious, 2017). With the help of it actual status of business could be

determined which helps to reach business goals. Different types of statements such as income

statement, balance sheet and cash flow statement. With the help of them stakeholders such as

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

shareholders, investors, suppliers and creditors determine that organisation is financially strong

or not to formulate decision regarding investing money or providing credit to the company.

Purpose of financial reporting: For all the business enterprises it is vital to formulate

financial statements every year so that long term business goals could be achieved. Main

purposes of financial reporting is as follows:

Purpose of it is to provide data regarding results of operational activities which were

performed during the years to execute business in systematic manner.

Another purpose of financial reporting is to provide detailed information to stakeholders

so that their interest within the organisation could be enhanced.

2. Conceptual and regulatory framework with qualitative characteristics of financial information

Conceptual Framework: According to conceptual framework for all the organisations

whether these are small or large it is very important to formulate final accounts according to

specific concepts and principles. If all of them are not followed by companies then their financial

statements are not considered accurate. Some of the major concepts which are required to be

followed by BT Group Plc while forming final accounts are discussed below: Going concern concept: It is also known as fundamental principle of accounting which

demonstrates that a company will continue all its plans and operations during current and

net financial years. It is vital for BT Group Plc to follow it so that stakeholders can

analyse that all the existing assets will be used by enterprise to meet all its fiscal

obligations (Going concern concept, 2019).

Monetary unit concept: It states that the transactions which are recorded in the books of

accounts must have taken place in monetary terms. If it is not possible to measure them

then such entries should be ignored by accounting professionals of companies such as BT

Group Plc.

Regulatory framework: The regulatory framework of financial reporting is connected

with execution of accounting rules, regulation and standards so that prepared financial statements

can become optimistic and transparent for users (Chen and et.al, 2018). In the context of BT

group plc their accountants use below mentioned accounting principles that are as follows: Full Disclosure – The particular principal of financial accounting important for

accountant to utilise of all types of financial information regarding to business in produce

of financial reports. This concept defines that company should not hide any essential

2

or not to formulate decision regarding investing money or providing credit to the company.

Purpose of financial reporting: For all the business enterprises it is vital to formulate

financial statements every year so that long term business goals could be achieved. Main

purposes of financial reporting is as follows:

Purpose of it is to provide data regarding results of operational activities which were

performed during the years to execute business in systematic manner.

Another purpose of financial reporting is to provide detailed information to stakeholders

so that their interest within the organisation could be enhanced.

2. Conceptual and regulatory framework with qualitative characteristics of financial information

Conceptual Framework: According to conceptual framework for all the organisations

whether these are small or large it is very important to formulate final accounts according to

specific concepts and principles. If all of them are not followed by companies then their financial

statements are not considered accurate. Some of the major concepts which are required to be

followed by BT Group Plc while forming final accounts are discussed below: Going concern concept: It is also known as fundamental principle of accounting which

demonstrates that a company will continue all its plans and operations during current and

net financial years. It is vital for BT Group Plc to follow it so that stakeholders can

analyse that all the existing assets will be used by enterprise to meet all its fiscal

obligations (Going concern concept, 2019).

Monetary unit concept: It states that the transactions which are recorded in the books of

accounts must have taken place in monetary terms. If it is not possible to measure them

then such entries should be ignored by accounting professionals of companies such as BT

Group Plc.

Regulatory framework: The regulatory framework of financial reporting is connected

with execution of accounting rules, regulation and standards so that prepared financial statements

can become optimistic and transparent for users (Chen and et.al, 2018). In the context of BT

group plc their accountants use below mentioned accounting principles that are as follows: Full Disclosure – The particular principal of financial accounting important for

accountant to utilise of all types of financial information regarding to business in produce

of financial reports. This concept defines that company should not hide any essential

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information and must present in financial statements. It is essential to implement in the

organisation due to accountants will disclose overall information in the reference of

company's financial position. As a result financial statements will become more

optimistic and accountable. In selected company, the accountant apply principal of

financial reporting to develop their financial statements more useful and accountable to

their stakeholders.

Materiality – In this type of accounting principal that defines that in some reason apply

of accounting standards can be ignored when its impact in minor way on the company's

financial accounts. Thus, it is beneficial to know that this principal rarely applied by the

businesses (Coetzee, Janse van Rensburg and Schmulian, 2016).

Qualitative characteristics of financial information:

Comparability – In order to determine developments in the investigating entity's

productivity and financial situation, the data must be equivalent to the financial

statements described for other financial time period.

Relevance - The data must be applicable to customers' requirements, which is the

situation whenever the data affects users' financial choices. This may require reporting

particularly suitable data or data that may have an impact on users ' financial choices.

Understandability – The financial information must be presented into clear way that

easily understand by the users. It means that information must be shown with extra

information like supporting footnotes to assist in clarification.

3. Main key stakeholders of an organisation and the way in which they get benefited from

financial information

The stakeholders are those person who invest their money into particular company after

analysing financial performance of company and conduct activities for their own purposes. Main

it is categorised into two types of stakeholders such as internal and external. There is described

both types of stakeholders as follows:

(a) Internal Stakeholders – This type of stakeholders take interest into business activities and

take part to conduct daily basis operations (De Villiers, Venter and Hsiao, 2017). These person

have right to change policies of company and prepare effective strategies in critical situation.

Herein, some types of internal stakeholder such as:

3

organisation due to accountants will disclose overall information in the reference of

company's financial position. As a result financial statements will become more

optimistic and accountable. In selected company, the accountant apply principal of

financial reporting to develop their financial statements more useful and accountable to

their stakeholders.

Materiality – In this type of accounting principal that defines that in some reason apply

of accounting standards can be ignored when its impact in minor way on the company's

financial accounts. Thus, it is beneficial to know that this principal rarely applied by the

businesses (Coetzee, Janse van Rensburg and Schmulian, 2016).

Qualitative characteristics of financial information:

Comparability – In order to determine developments in the investigating entity's

productivity and financial situation, the data must be equivalent to the financial

statements described for other financial time period.

Relevance - The data must be applicable to customers' requirements, which is the

situation whenever the data affects users' financial choices. This may require reporting

particularly suitable data or data that may have an impact on users ' financial choices.

Understandability – The financial information must be presented into clear way that

easily understand by the users. It means that information must be shown with extra

information like supporting footnotes to assist in clarification.

3. Main key stakeholders of an organisation and the way in which they get benefited from

financial information

The stakeholders are those person who invest their money into particular company after

analysing financial performance of company and conduct activities for their own purposes. Main

it is categorised into two types of stakeholders such as internal and external. There is described

both types of stakeholders as follows:

(a) Internal Stakeholders – This type of stakeholders take interest into business activities and

take part to conduct daily basis operations (De Villiers, Venter and Hsiao, 2017). These person

have right to change policies of company and prepare effective strategies in critical situation.

Herein, some types of internal stakeholder such as:

3

Managers – It is defined as higher level of internal stakeholder in companies. They will

take appropriate decision in order to arrange different business activities that relates to

financial and human resource entities after producing operations and activities. The

manager are essential to access financial information in regard to company for creation of

impressive plans and strategies. The manager has right to make decision in critical

situation.

Employees – These types of internal stakeholders are connected with the performance of

business operations and functions on routine basis in return to get salary and wages. They

are playing important role in business activities and known as business assets. The

expectations and growth of staff members based on the companies financial performance.

So they take interest into financial information in the company (Fernández Méndez,

Arrondo García and Pathan, 2017).

(b) External stakeholders – These types of stakeholders also take interest into business

activities but from outside. They have not right to take part in board meeting and does not

involve into day to day activities of business. Herein, defined different types of external

stakeholders such as: Creditors – These types of stakeholders are taken interest in the procedure of providing

financial assistance to companies on credit. It is valuable to know that they focus on

company and their credit score which is better or not. This can be done after the examine

of financial statements. This is why because they take interest into company's financial

performance.

Suppliers – The suppliers of any company plays important role due to sell goods to

companies on credit. Thus, it is essential to show their financial statements in front of

suppliers due to analysis financial position of company at the market. On the basis of

financial information they take decision whether they should sell goods on credit or not.

4. Value of financial reporting for meeting organisational objectives and growth

Financial reporting important for every organisation that helps to accomplish

organisational objectives and growth. It becomes achievable when financial reports of company

is evaluated in a descriptive manner on the basis of planning to achieve objectives and goals

(Fradeani, Panizzolo and Metushi, 2016).

4

take appropriate decision in order to arrange different business activities that relates to

financial and human resource entities after producing operations and activities. The

manager are essential to access financial information in regard to company for creation of

impressive plans and strategies. The manager has right to make decision in critical

situation.

Employees – These types of internal stakeholders are connected with the performance of

business operations and functions on routine basis in return to get salary and wages. They

are playing important role in business activities and known as business assets. The

expectations and growth of staff members based on the companies financial performance.

So they take interest into financial information in the company (Fernández Méndez,

Arrondo García and Pathan, 2017).

(b) External stakeholders – These types of stakeholders also take interest into business

activities but from outside. They have not right to take part in board meeting and does not

involve into day to day activities of business. Herein, defined different types of external

stakeholders such as: Creditors – These types of stakeholders are taken interest in the procedure of providing

financial assistance to companies on credit. It is valuable to know that they focus on

company and their credit score which is better or not. This can be done after the examine

of financial statements. This is why because they take interest into company's financial

performance.

Suppliers – The suppliers of any company plays important role due to sell goods to

companies on credit. Thus, it is essential to show their financial statements in front of

suppliers due to analysis financial position of company at the market. On the basis of

financial information they take decision whether they should sell goods on credit or not.

4. Value of financial reporting for meeting organisational objectives and growth

Financial reporting important for every organisation that helps to accomplish

organisational objectives and growth. It becomes achievable when financial reports of company

is evaluated in a descriptive manner on the basis of planning to achieve objectives and goals

(Fradeani, Panizzolo and Metushi, 2016).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial reporting for meeting organisational objectives – It is important feature of

meeting organisational objectives. On the basis of financial report company take appropriate

decision and prepare effective strategies that leads in acquiring objectives on time. In the context

of BT Group Plc, the financial reporting helps in them in acquiring goals as well as objectives

after examine financial situation.

Financial reporting for achieving the growth – Additionally, financial reports are

utilised for acquiring higher growth in the company. On the basis of financial statements

company influence to investor for invest money in their company. As a result many investors

agree with proposal and business get benefits. Such as BT Group Plc utilise financial reports in

reference to accomplish the higher growth.

Financial reports for development of organisation – The another importance of

financial reports for development of organisation. When company apply all accounting standards

to make financial reports and present clearly so it will impact on goodwill in increasing way. To

prepare financial report on routine basis then all stakeholders may lead to improve reputation. So

financial statements essential for development of business (Habib and Bhuiyan, 2016).

So the financial reports of BT group plc valuable for organisational growth, objective and

development.

5. Preparation of different financial statements

(1)

Cost of damaged goods 2470

Realisable value 2670

Less- remedial cost -500

Net Realisable Value (NRV) 2170

Closing inventory TB 25000

Less- cost of damaged goods -2470

Add- NRV 2170

5

meeting organisational objectives. On the basis of financial report company take appropriate

decision and prepare effective strategies that leads in acquiring objectives on time. In the context

of BT Group Plc, the financial reporting helps in them in acquiring goals as well as objectives

after examine financial situation.

Financial reporting for achieving the growth – Additionally, financial reports are

utilised for acquiring higher growth in the company. On the basis of financial statements

company influence to investor for invest money in their company. As a result many investors

agree with proposal and business get benefits. Such as BT Group Plc utilise financial reports in

reference to accomplish the higher growth.

Financial reports for development of organisation – The another importance of

financial reports for development of organisation. When company apply all accounting standards

to make financial reports and present clearly so it will impact on goodwill in increasing way. To

prepare financial report on routine basis then all stakeholders may lead to improve reputation. So

financial statements essential for development of business (Habib and Bhuiyan, 2016).

So the financial reports of BT group plc valuable for organisational growth, objective and

development.

5. Preparation of different financial statements

(1)

Cost of damaged goods 2470

Realisable value 2670

Less- remedial cost -500

Net Realisable Value (NRV) 2170

Closing inventory TB 25000

Less- cost of damaged goods -2470

Add- NRV 2170

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

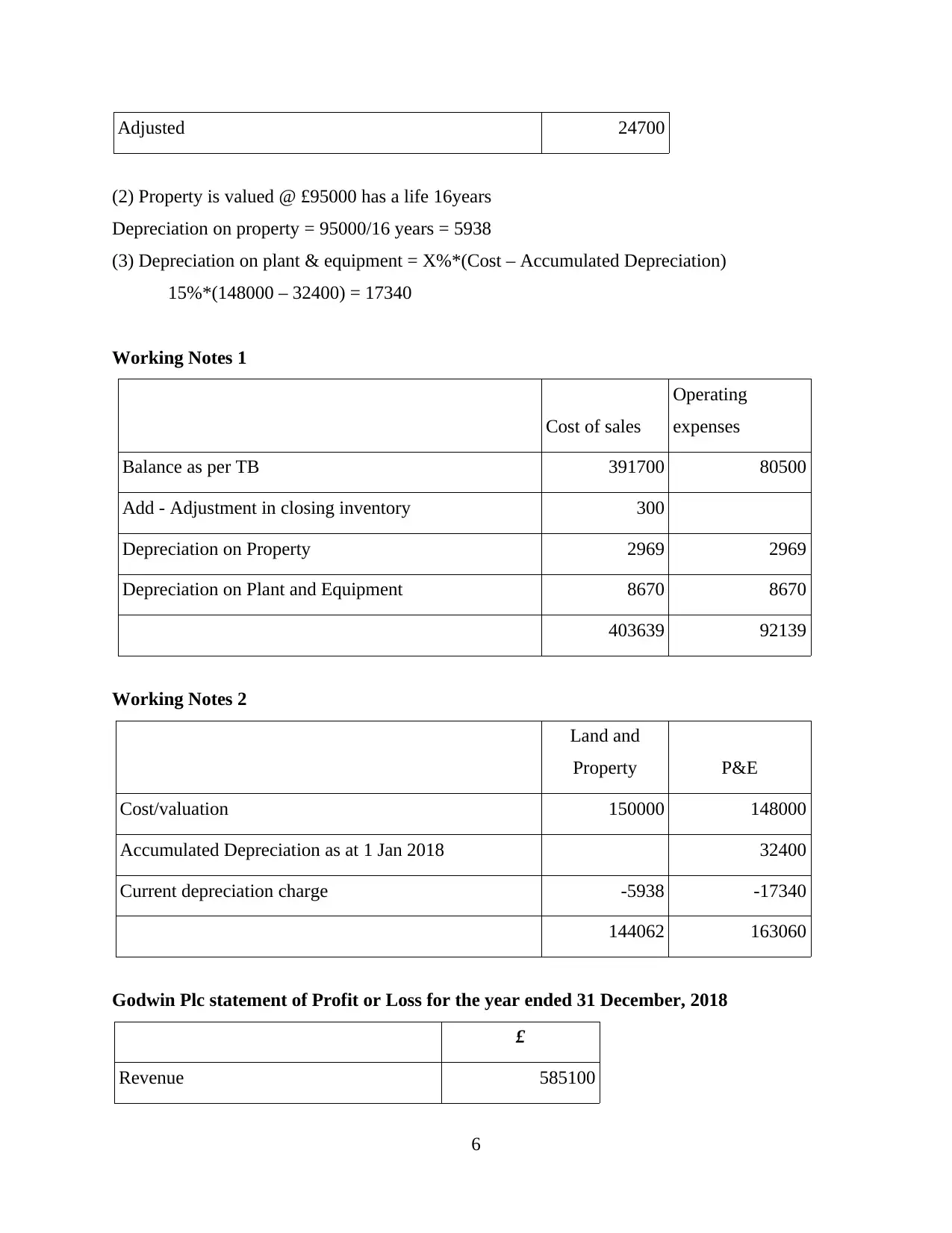

Adjusted 24700

(2) Property is valued @ £95000 has a life 16years

Depreciation on property = 95000/16 years = 5938

(3) Depreciation on plant & equipment = X%*(Cost – Accumulated Depreciation)

15%*(148000 – 32400) = 17340

Working Notes 1

Cost of sales

Operating

expenses

Balance as per TB 391700 80500

Add - Adjustment in closing inventory 300

Depreciation on Property 2969 2969

Depreciation on Plant and Equipment 8670 8670

403639 92139

Working Notes 2

Land and

Property P&E

Cost/valuation 150000 148000

Accumulated Depreciation as at 1 Jan 2018 32400

Current depreciation charge -5938 -17340

144062 163060

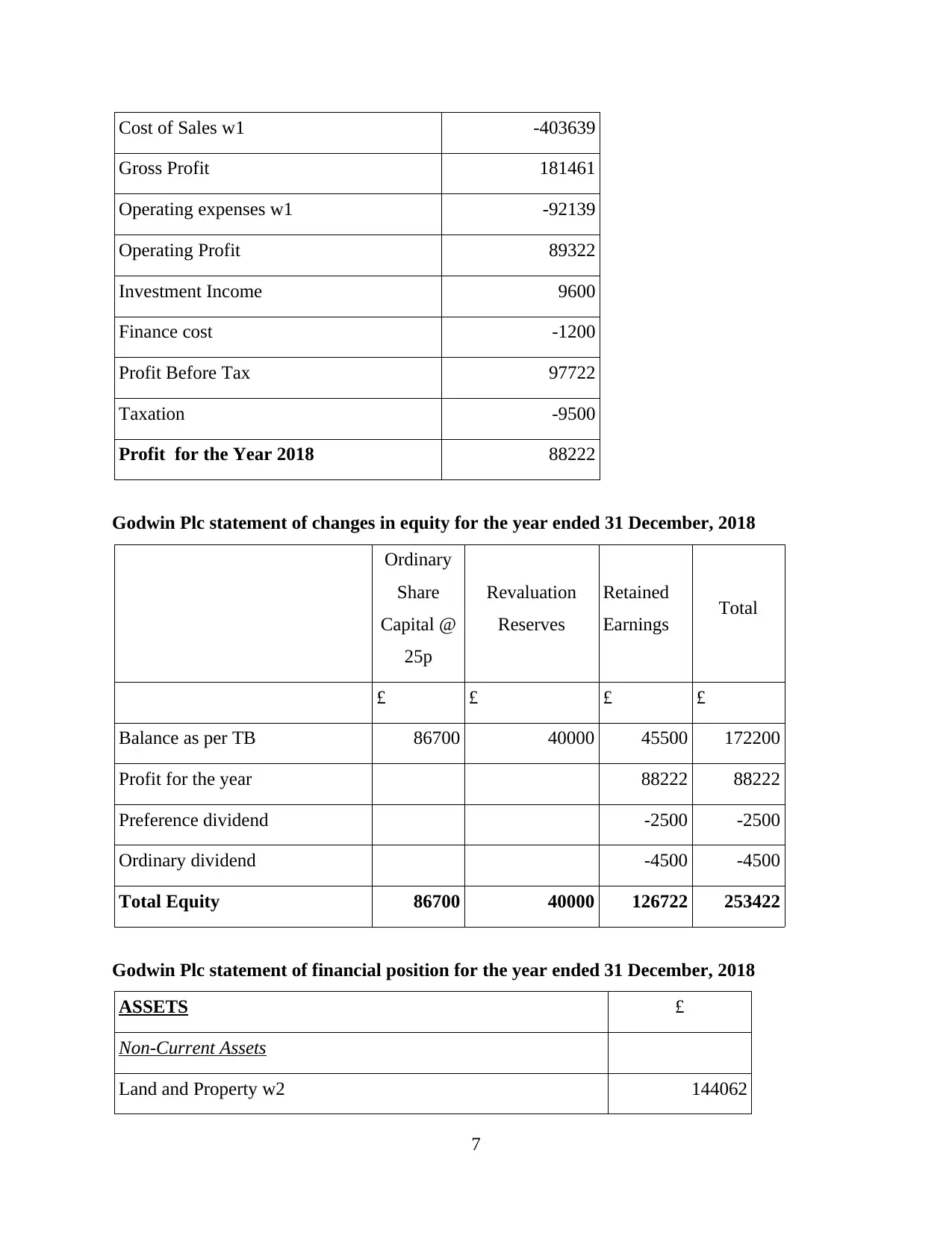

Godwin Plc statement of Profit or Loss for the year ended 31 December, 2018

£

Revenue 585100

6

(2) Property is valued @ £95000 has a life 16years

Depreciation on property = 95000/16 years = 5938

(3) Depreciation on plant & equipment = X%*(Cost – Accumulated Depreciation)

15%*(148000 – 32400) = 17340

Working Notes 1

Cost of sales

Operating

expenses

Balance as per TB 391700 80500

Add - Adjustment in closing inventory 300

Depreciation on Property 2969 2969

Depreciation on Plant and Equipment 8670 8670

403639 92139

Working Notes 2

Land and

Property P&E

Cost/valuation 150000 148000

Accumulated Depreciation as at 1 Jan 2018 32400

Current depreciation charge -5938 -17340

144062 163060

Godwin Plc statement of Profit or Loss for the year ended 31 December, 2018

£

Revenue 585100

6

Cost of Sales w1 -403639

Gross Profit 181461

Operating expenses w1 -92139

Operating Profit 89322

Investment Income 9600

Finance cost -1200

Profit Before Tax 97722

Taxation -9500

Profit for the Year 2018 88222

Godwin Plc statement of changes in equity for the year ended 31 December, 2018

Ordinary

Share

Capital @

25p

Revaluation

Reserves

Retained

Earnings Total

£ £ £ £

Balance as per TB 86700 40000 45500 172200

Profit for the year 88222 88222

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

Total Equity 86700 40000 126722 253422

Godwin Plc statement of financial position for the year ended 31 December, 2018

ASSETS £

Non-Current Assets

Land and Property w2 144062

7

Gross Profit 181461

Operating expenses w1 -92139

Operating Profit 89322

Investment Income 9600

Finance cost -1200

Profit Before Tax 97722

Taxation -9500

Profit for the Year 2018 88222

Godwin Plc statement of changes in equity for the year ended 31 December, 2018

Ordinary

Share

Capital @

25p

Revaluation

Reserves

Retained

Earnings Total

£ £ £ £

Balance as per TB 86700 40000 45500 172200

Profit for the year 88222 88222

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

Total Equity 86700 40000 126722 253422

Godwin Plc statement of financial position for the year ended 31 December, 2018

ASSETS £

Non-Current Assets

Land and Property w2 144062

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

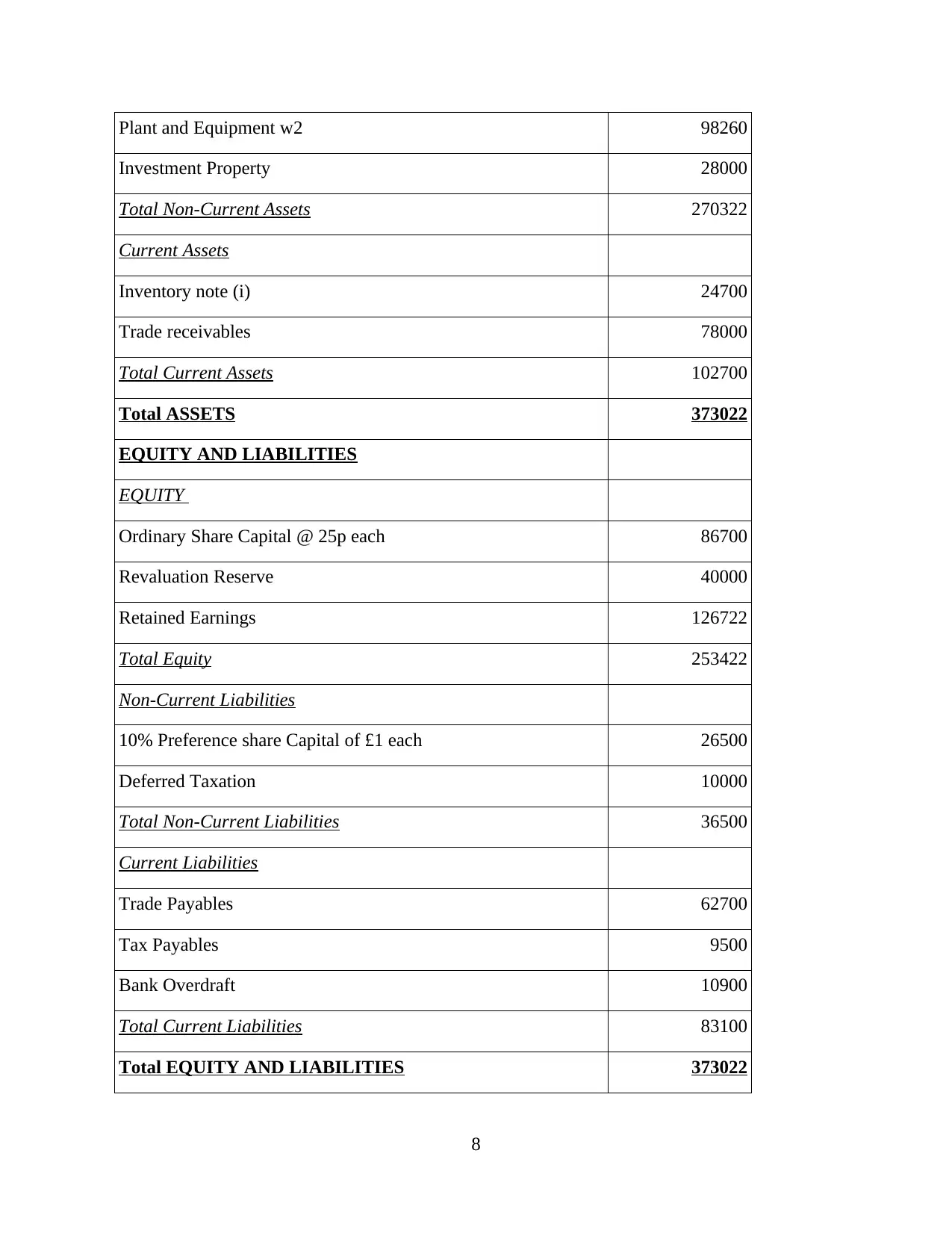

Plant and Equipment w2 98260

Investment Property 28000

Total Non-Current Assets 270322

Current Assets

Inventory note (i) 24700

Trade receivables 78000

Total Current Assets 102700

Total ASSETS 373022

EQUITY AND LIABILITIES

EQUITY

Ordinary Share Capital @ 25p each 86700

Revaluation Reserve 40000

Retained Earnings 126722

Total Equity 253422

Non-Current Liabilities

10% Preference share Capital of £1 each 26500

Deferred Taxation 10000

Total Non-Current Liabilities 36500

Current Liabilities

Trade Payables 62700

Tax Payables 9500

Bank Overdraft 10900

Total Current Liabilities 83100

Total EQUITY AND LIABILITIES 373022

8

Investment Property 28000

Total Non-Current Assets 270322

Current Assets

Inventory note (i) 24700

Trade receivables 78000

Total Current Assets 102700

Total ASSETS 373022

EQUITY AND LIABILITIES

EQUITY

Ordinary Share Capital @ 25p each 86700

Revaluation Reserve 40000

Retained Earnings 126722

Total Equity 253422

Non-Current Liabilities

10% Preference share Capital of £1 each 26500

Deferred Taxation 10000

Total Non-Current Liabilities 36500

Current Liabilities

Trade Payables 62700

Tax Payables 9500

Bank Overdraft 10900

Total Current Liabilities 83100

Total EQUITY AND LIABILITIES 373022

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

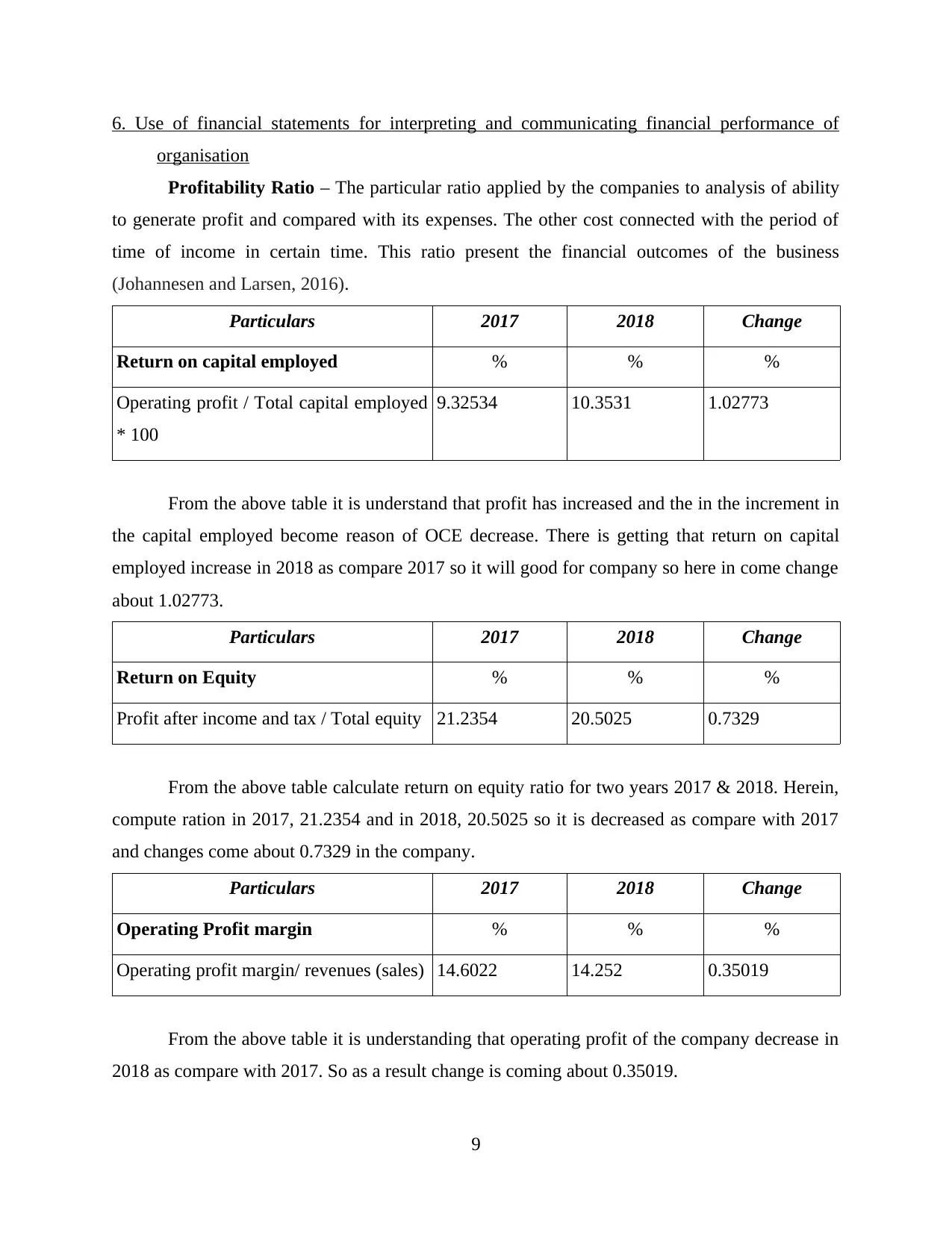

6. Use of financial statements for interpreting and communicating financial performance of

organisation

Profitability Ratio – The particular ratio applied by the companies to analysis of ability

to generate profit and compared with its expenses. The other cost connected with the period of

time of income in certain time. This ratio present the financial outcomes of the business

(Johannesen and Larsen, 2016).

Particulars 2017 2018 Change

Return on capital employed % % %

Operating profit / Total capital employed

* 100

9.32534 10.3531 1.02773

From the above table it is understand that profit has increased and the in the increment in

the capital employed become reason of OCE decrease. There is getting that return on capital

employed increase in 2018 as compare 2017 so it will good for company so here in come change

about 1.02773.

Particulars 2017 2018 Change

Return on Equity % % %

Profit after income and tax / Total equity 21.2354 20.5025 0.7329

From the above table calculate return on equity ratio for two years 2017 & 2018. Herein,

compute ration in 2017, 21.2354 and in 2018, 20.5025 so it is decreased as compare with 2017

and changes come about 0.7329 in the company.

Particulars 2017 2018 Change

Operating Profit margin % % %

Operating profit margin/ revenues (sales) 14.6022 14.252 0.35019

From the above table it is understanding that operating profit of the company decrease in

2018 as compare with 2017. So as a result change is coming about 0.35019.

9

organisation

Profitability Ratio – The particular ratio applied by the companies to analysis of ability

to generate profit and compared with its expenses. The other cost connected with the period of

time of income in certain time. This ratio present the financial outcomes of the business

(Johannesen and Larsen, 2016).

Particulars 2017 2018 Change

Return on capital employed % % %

Operating profit / Total capital employed

* 100

9.32534 10.3531 1.02773

From the above table it is understand that profit has increased and the in the increment in

the capital employed become reason of OCE decrease. There is getting that return on capital

employed increase in 2018 as compare 2017 so it will good for company so here in come change

about 1.02773.

Particulars 2017 2018 Change

Return on Equity % % %

Profit after income and tax / Total equity 21.2354 20.5025 0.7329

From the above table calculate return on equity ratio for two years 2017 & 2018. Herein,

compute ration in 2017, 21.2354 and in 2018, 20.5025 so it is decreased as compare with 2017

and changes come about 0.7329 in the company.

Particulars 2017 2018 Change

Operating Profit margin % % %

Operating profit margin/ revenues (sales) 14.6022 14.252 0.35019

From the above table it is understanding that operating profit of the company decrease in

2018 as compare with 2017. So as a result change is coming about 0.35019.

9

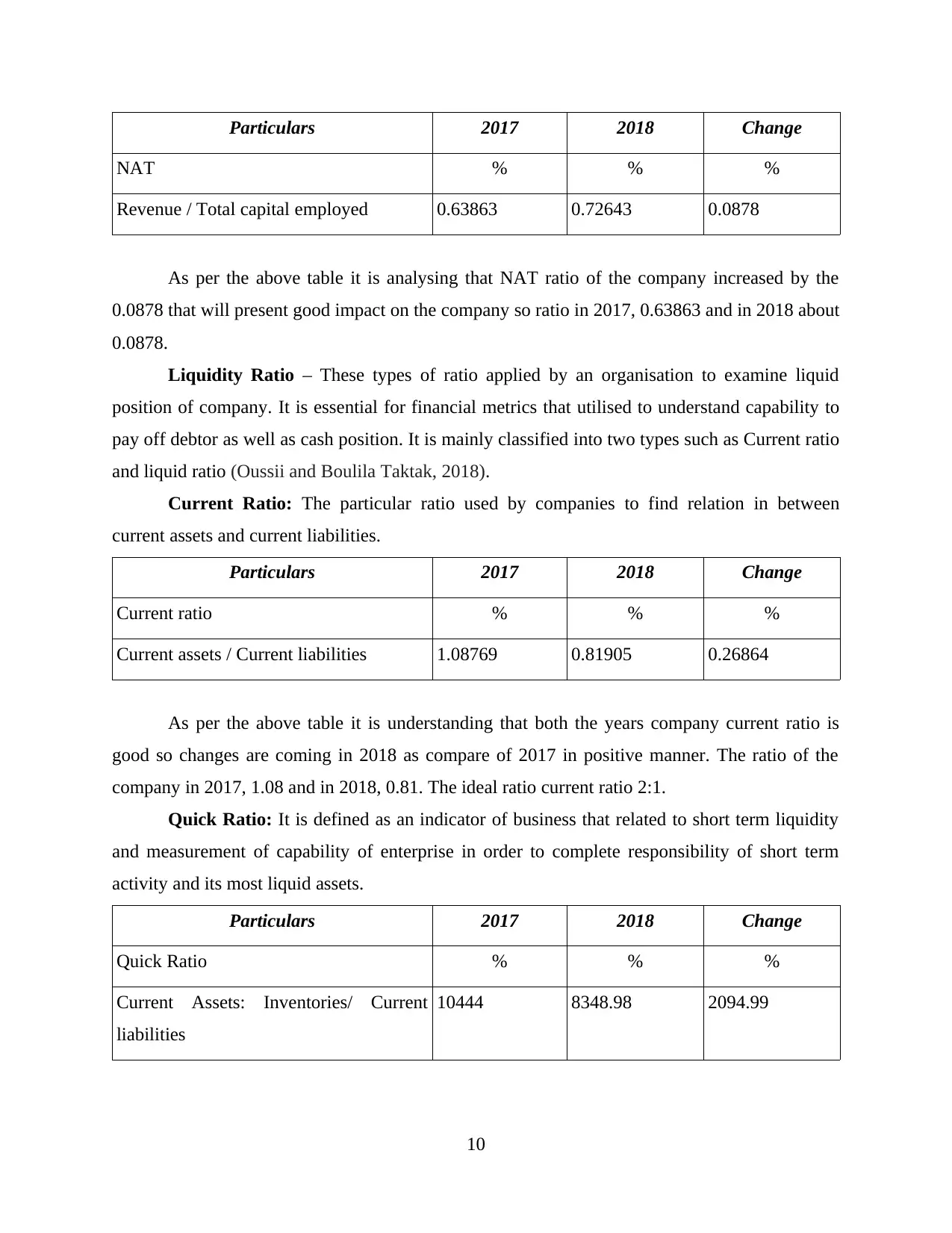

Particulars 2017 2018 Change

NAT % % %

Revenue / Total capital employed 0.63863 0.72643 0.0878

As per the above table it is analysing that NAT ratio of the company increased by the

0.0878 that will present good impact on the company so ratio in 2017, 0.63863 and in 2018 about

0.0878.

Liquidity Ratio – These types of ratio applied by an organisation to examine liquid

position of company. It is essential for financial metrics that utilised to understand capability to

pay off debtor as well as cash position. It is mainly classified into two types such as Current ratio

and liquid ratio (Oussii and Boulila Taktak, 2018).

Current Ratio: The particular ratio used by companies to find relation in between

current assets and current liabilities.

Particulars 2017 2018 Change

Current ratio % % %

Current assets / Current liabilities 1.08769 0.81905 0.26864

As per the above table it is understanding that both the years company current ratio is

good so changes are coming in 2018 as compare of 2017 in positive manner. The ratio of the

company in 2017, 1.08 and in 2018, 0.81. The ideal ratio current ratio 2:1.

Quick Ratio: It is defined as an indicator of business that related to short term liquidity

and measurement of capability of enterprise in order to complete responsibility of short term

activity and its most liquid assets.

Particulars 2017 2018 Change

Quick Ratio % % %

Current Assets: Inventories/ Current

liabilities

10444 8348.98 2094.99

10

NAT % % %

Revenue / Total capital employed 0.63863 0.72643 0.0878

As per the above table it is analysing that NAT ratio of the company increased by the

0.0878 that will present good impact on the company so ratio in 2017, 0.63863 and in 2018 about

0.0878.

Liquidity Ratio – These types of ratio applied by an organisation to examine liquid

position of company. It is essential for financial metrics that utilised to understand capability to

pay off debtor as well as cash position. It is mainly classified into two types such as Current ratio

and liquid ratio (Oussii and Boulila Taktak, 2018).

Current Ratio: The particular ratio used by companies to find relation in between

current assets and current liabilities.

Particulars 2017 2018 Change

Current ratio % % %

Current assets / Current liabilities 1.08769 0.81905 0.26864

As per the above table it is understanding that both the years company current ratio is

good so changes are coming in 2018 as compare of 2017 in positive manner. The ratio of the

company in 2017, 1.08 and in 2018, 0.81. The ideal ratio current ratio 2:1.

Quick Ratio: It is defined as an indicator of business that related to short term liquidity

and measurement of capability of enterprise in order to complete responsibility of short term

activity and its most liquid assets.

Particulars 2017 2018 Change

Quick Ratio % % %

Current Assets: Inventories/ Current

liabilities

10444 8348.98 2094.99

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.