Financial Reporting Disclosures in the Australian Corporate Sector

VerifiedAdded on 2023/04/20

|13

|2275

|115

AI Summary

This research report analyzes the property, plant, and equipment (PPE) disclosures of BHP Billiton in its latest annual report and assesses its compliance with the requirements of AASB 116 and the qualitative characteristics of useful financial information. The report concludes that BHP Billiton has complied with all aspects of AASB 116 and the IASB conceptual framework.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN

CORPORATE SECTOR

Financial Reporting Disclosures in the Australian Corporate Sector

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

ACCG224 S3 2018 SID

CORPORATE SECTOR

Financial Reporting Disclosures in the Australian Corporate Sector

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

ACCG224 S3 2018 SID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Table of Contents

Executive Summary:..................................................................................................................2

Introduction:...............................................................................................................................3

1. Objective of general purpose financial reporting and qualitative characteristics of useful

financial information:.................................................................................................................3

2. Extent to which the latest annual report of BHP Billiton meets the disclosure requirements

for PPE as per AASB 116:.........................................................................................................4

3. Extent to which the PPE disclosures of BHP Billiton satisfy fundamental and enhancing

qualitative characteristics of useful financial information:........................................................5

4. Alignment of the PPE disclosures with the objective of general purpose financial reporting

and actions for improvement for BHP Billiton:.........................................................................6

Conclusion:................................................................................................................................6

References:.................................................................................................................................7

Appendix:...................................................................................................................................8

s

1 | P a g e

ACCG224 S3 2018 SID

SECTOR

Table of Contents

Executive Summary:..................................................................................................................2

Introduction:...............................................................................................................................3

1. Objective of general purpose financial reporting and qualitative characteristics of useful

financial information:.................................................................................................................3

2. Extent to which the latest annual report of BHP Billiton meets the disclosure requirements

for PPE as per AASB 116:.........................................................................................................4

3. Extent to which the PPE disclosures of BHP Billiton satisfy fundamental and enhancing

qualitative characteristics of useful financial information:........................................................5

4. Alignment of the PPE disclosures with the objective of general purpose financial reporting

and actions for improvement for BHP Billiton:.........................................................................6

Conclusion:................................................................................................................................6

References:.................................................................................................................................7

Appendix:...................................................................................................................................8

s

1 | P a g e

ACCG224 S3 2018 SID

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Executive Summary:

The primary emphasis of the research report is to analyse the PPE disclosures of BHP

Billiton according to its latest annual report and whether it satisfies the objective of the

conceptual framework. It investigates and assesses the ways through which PPE obtains the

obligations of AASB 116 and qualitative characteristics. The PPE appearance accomplishes

the requirement of accounting standards and thus, BHP Billiton has complied with all aspects

of AASB 116 and IASB conceptual framework.

2 | P a g e

ACCG224 S3 2018 SID

SECTOR

Executive Summary:

The primary emphasis of the research report is to analyse the PPE disclosures of BHP

Billiton according to its latest annual report and whether it satisfies the objective of the

conceptual framework. It investigates and assesses the ways through which PPE obtains the

obligations of AASB 116 and qualitative characteristics. The PPE appearance accomplishes

the requirement of accounting standards and thus, BHP Billiton has complied with all aspects

of AASB 116 and IASB conceptual framework.

2 | P a g e

ACCG224 S3 2018 SID

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Introduction:

The objective of the report is to provide faithful and accurate representation of the

financial statements, which is crucial for all business organisations owing to the effects on the

community status and self-assurance of the investors. The scope of the paper would initially

focus on elucidating the objectives of general purpose financial reporting along with

qualitative characteristics of valuable financial information. The second section would lay

stress on analysing the latest published annual report of an ASX listed organisation to

understand whether the same fulfils the PPE disclosures in accordance with AASB 116. For

this reason, BHP Billiton is taken into consideration, which is a leading organisation in the

Australian mining sector and it is involved in producing metallurgical coal, iron ore, uranium

and copper (BHP 2018). Thirdly, the paper would emphasise on ascertaining the extent to

which the disclosures on PPE meet the enhancing and fundamental qualitative characteristics

of financial information. Finally, the report would shed light on evaluating the alignment of

the PPE disclosures of the organisation with the general purpose financial reporting (GPFR)

objectives and accordingly, actions for improvement would be recommended.

1. Objective of general purpose financial reporting and qualitative characteristics of

useful financial information:

In accordance with “IASB OB1- OB21”, GPFR is the base of the conceptual

framework and it intends to provide financial information to the investors, users, lenders and

other creditors so that they could undertake effective investment decisions in an organisation,

which is BHP Billiton in this case (Aasb.gov.au 2018). The information obtained from GPFR

enables the investors in comprehending and undertaking straightforward methodology for

estimating the net cash flows and dividends in future. As a result, the investors could

understand the strengths and drawbacks of the organisation by using the liquidity ratio. For

instance, any changes in cash and property, plant and equipment (PPE) could have direct

impact on the liquidity ratio. With the help of this ratio, it is possible to analyse the existing

financial position of the organisation and its ability to generate money. In addition, it

provides non-financial information such as expectations of the management and economic

resources (Chand, Patel and White 2015).

3 | P a g e

ACCG224 S3 2018 SID

SECTOR

Introduction:

The objective of the report is to provide faithful and accurate representation of the

financial statements, which is crucial for all business organisations owing to the effects on the

community status and self-assurance of the investors. The scope of the paper would initially

focus on elucidating the objectives of general purpose financial reporting along with

qualitative characteristics of valuable financial information. The second section would lay

stress on analysing the latest published annual report of an ASX listed organisation to

understand whether the same fulfils the PPE disclosures in accordance with AASB 116. For

this reason, BHP Billiton is taken into consideration, which is a leading organisation in the

Australian mining sector and it is involved in producing metallurgical coal, iron ore, uranium

and copper (BHP 2018). Thirdly, the paper would emphasise on ascertaining the extent to

which the disclosures on PPE meet the enhancing and fundamental qualitative characteristics

of financial information. Finally, the report would shed light on evaluating the alignment of

the PPE disclosures of the organisation with the general purpose financial reporting (GPFR)

objectives and accordingly, actions for improvement would be recommended.

1. Objective of general purpose financial reporting and qualitative characteristics of

useful financial information:

In accordance with “IASB OB1- OB21”, GPFR is the base of the conceptual

framework and it intends to provide financial information to the investors, users, lenders and

other creditors so that they could undertake effective investment decisions in an organisation,

which is BHP Billiton in this case (Aasb.gov.au 2018). The information obtained from GPFR

enables the investors in comprehending and undertaking straightforward methodology for

estimating the net cash flows and dividends in future. As a result, the investors could

understand the strengths and drawbacks of the organisation by using the liquidity ratio. For

instance, any changes in cash and property, plant and equipment (PPE) could have direct

impact on the liquidity ratio. With the help of this ratio, it is possible to analyse the existing

financial position of the organisation and its ability to generate money. In addition, it

provides non-financial information such as expectations of the management and economic

resources (Chand, Patel and White 2015).

3 | P a g e

ACCG224 S3 2018 SID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

As per “IASB QC1- QC39”, there are two qualitative characteristics of financial

information, which include enhancing and fundamental qualitative characteristics. The

enhancing characteristics constitute of verifiability, understandability, comparability and

timeliness, which assist in improving the usefulness of financial information. On the other

hand, fundamental characteristics include faithful representation and relevance, which are

simple and crucial to prepare financial reports (Aasb.gov.au 2018).

In terms of fundamental characteristics, relevance denotes financial information that

could affect decision-making in case of omissions or misstatements and it is termed as

materiality as well. Secondly, faithful representation implies that the financial reports should

be complete, neutral and error-free.

In terms of qualitative characteristics, verifiability implies the faithful representation

of information, which would assist the users in reaching agreement within the financial

statements. Understandability denotes the characteristics of financial information along with

representing information in clear and understandable manner. Comparability enables the

users in identifying and gaining overview of the similarities and variations among items and

this is beneficial at the time of contrasting a similar item with a different organisation.

Finally, timeliness signifies that the organisation needs to complete the financial reports

within time for the decision-makers.

2. Extent to which the latest annual report of BHP Billiton meets the disclosure

requirements for PPE as per AASB 116:

According to “Paragraph 73 of AASB 116”, the financial statements need to disclose

the measurement bases used for its property, plant and equipment in order to ascertain the

following:

Gross carrying amount

Depreciation methods

Depreciation rates or useful lives

Gross carrying amount and accumulated depreciation at the start and end of the year

Reconciliation of the carrying value at the start and end of the year (Aasb.gov.au

2018)

4 | P a g e

ACCG224 S3 2018 SID

SECTOR

As per “IASB QC1- QC39”, there are two qualitative characteristics of financial

information, which include enhancing and fundamental qualitative characteristics. The

enhancing characteristics constitute of verifiability, understandability, comparability and

timeliness, which assist in improving the usefulness of financial information. On the other

hand, fundamental characteristics include faithful representation and relevance, which are

simple and crucial to prepare financial reports (Aasb.gov.au 2018).

In terms of fundamental characteristics, relevance denotes financial information that

could affect decision-making in case of omissions or misstatements and it is termed as

materiality as well. Secondly, faithful representation implies that the financial reports should

be complete, neutral and error-free.

In terms of qualitative characteristics, verifiability implies the faithful representation

of information, which would assist the users in reaching agreement within the financial

statements. Understandability denotes the characteristics of financial information along with

representing information in clear and understandable manner. Comparability enables the

users in identifying and gaining overview of the similarities and variations among items and

this is beneficial at the time of contrasting a similar item with a different organisation.

Finally, timeliness signifies that the organisation needs to complete the financial reports

within time for the decision-makers.

2. Extent to which the latest annual report of BHP Billiton meets the disclosure

requirements for PPE as per AASB 116:

According to “Paragraph 73 of AASB 116”, the financial statements need to disclose

the measurement bases used for its property, plant and equipment in order to ascertain the

following:

Gross carrying amount

Depreciation methods

Depreciation rates or useful lives

Gross carrying amount and accumulated depreciation at the start and end of the year

Reconciliation of the carrying value at the start and end of the year (Aasb.gov.au

2018)

4 | P a g e

ACCG224 S3 2018 SID

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

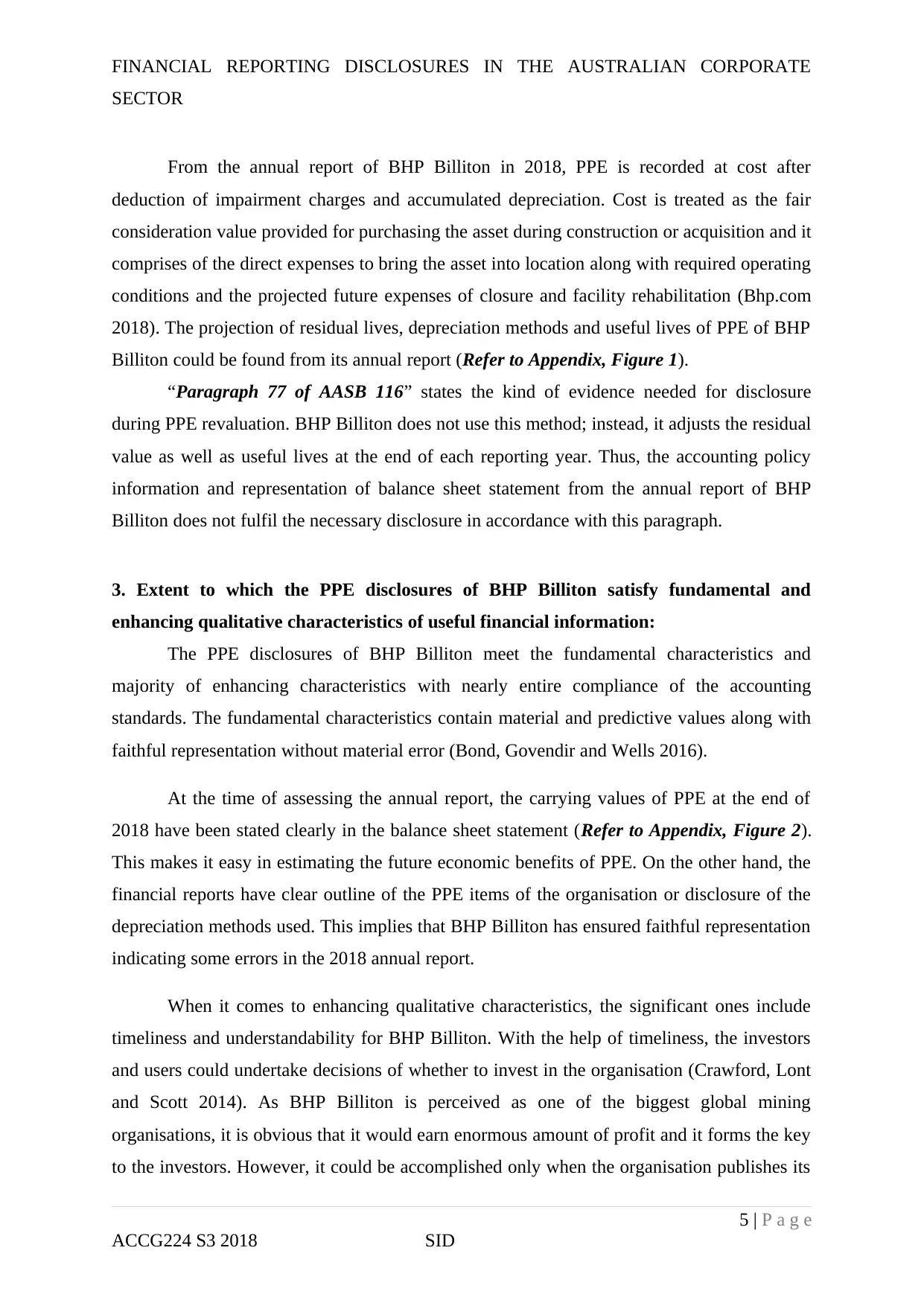

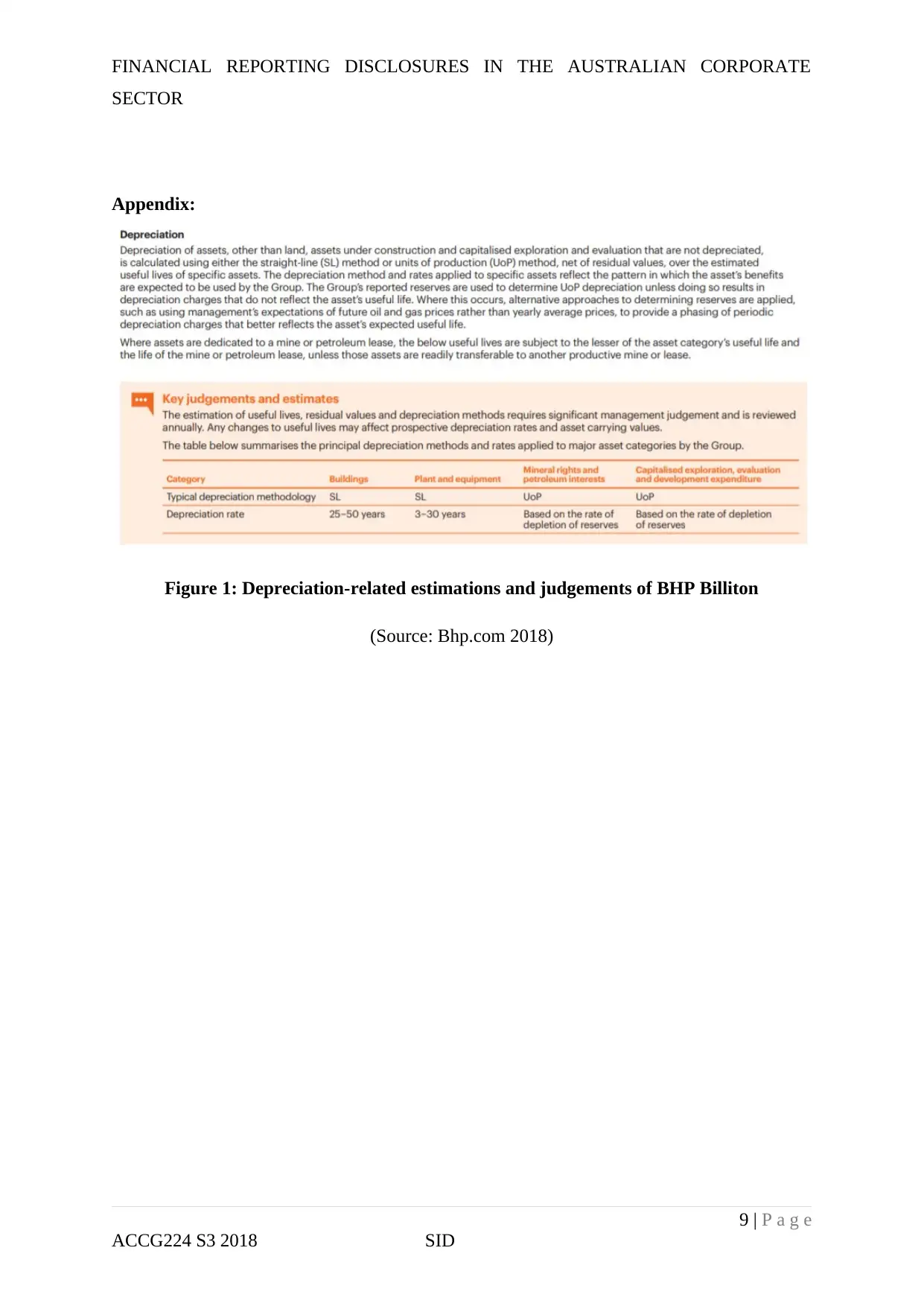

From the annual report of BHP Billiton in 2018, PPE is recorded at cost after

deduction of impairment charges and accumulated depreciation. Cost is treated as the fair

consideration value provided for purchasing the asset during construction or acquisition and it

comprises of the direct expenses to bring the asset into location along with required operating

conditions and the projected future expenses of closure and facility rehabilitation (Bhp.com

2018). The projection of residual lives, depreciation methods and useful lives of PPE of BHP

Billiton could be found from its annual report (Refer to Appendix, Figure 1).

“Paragraph 77 of AASB 116” states the kind of evidence needed for disclosure

during PPE revaluation. BHP Billiton does not use this method; instead, it adjusts the residual

value as well as useful lives at the end of each reporting year. Thus, the accounting policy

information and representation of balance sheet statement from the annual report of BHP

Billiton does not fulfil the necessary disclosure in accordance with this paragraph.

3. Extent to which the PPE disclosures of BHP Billiton satisfy fundamental and

enhancing qualitative characteristics of useful financial information:

The PPE disclosures of BHP Billiton meet the fundamental characteristics and

majority of enhancing characteristics with nearly entire compliance of the accounting

standards. The fundamental characteristics contain material and predictive values along with

faithful representation without material error (Bond, Govendir and Wells 2016).

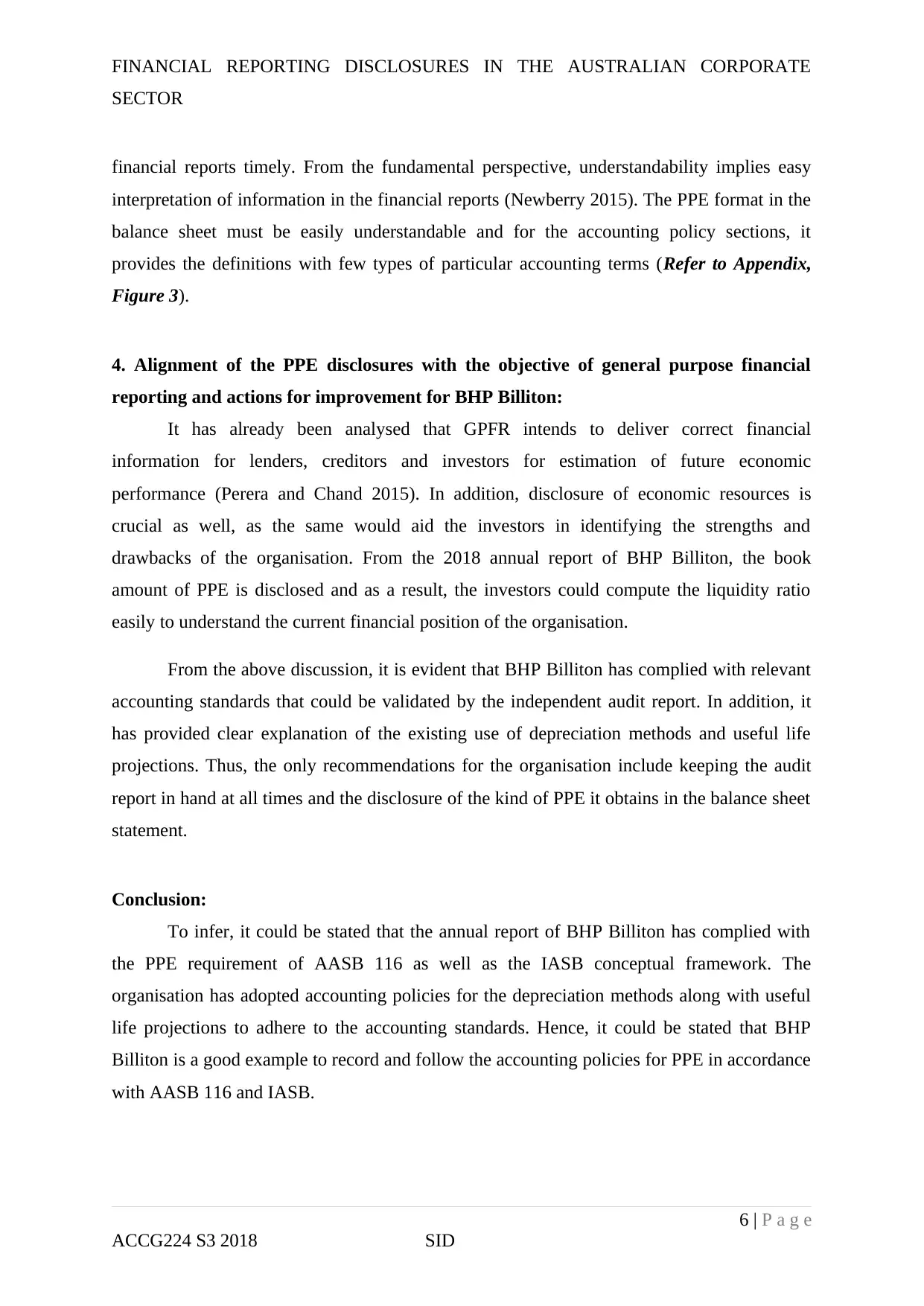

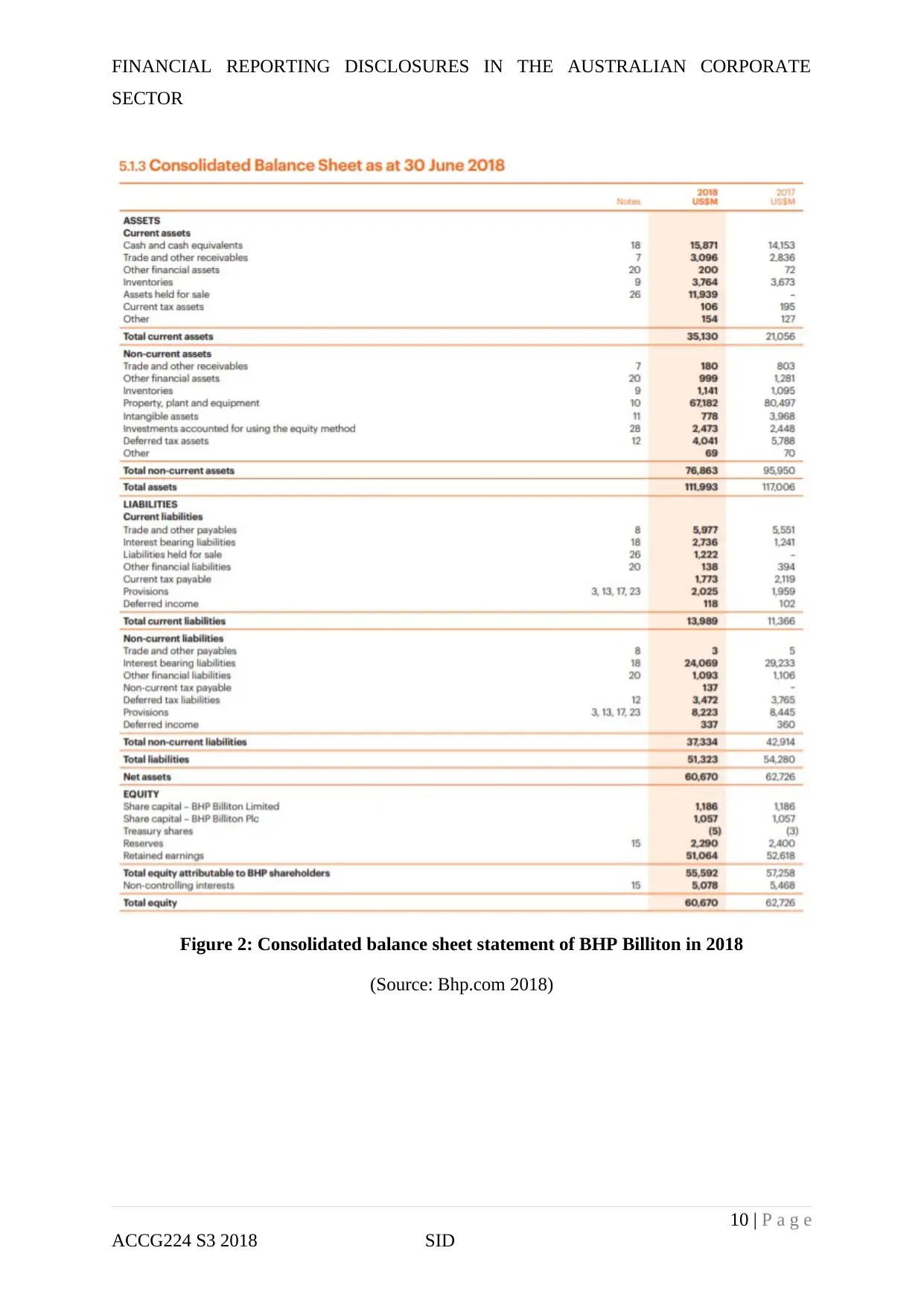

At the time of assessing the annual report, the carrying values of PPE at the end of

2018 have been stated clearly in the balance sheet statement (Refer to Appendix, Figure 2).

This makes it easy in estimating the future economic benefits of PPE. On the other hand, the

financial reports have clear outline of the PPE items of the organisation or disclosure of the

depreciation methods used. This implies that BHP Billiton has ensured faithful representation

indicating some errors in the 2018 annual report.

When it comes to enhancing qualitative characteristics, the significant ones include

timeliness and understandability for BHP Billiton. With the help of timeliness, the investors

and users could undertake decisions of whether to invest in the organisation (Crawford, Lont

and Scott 2014). As BHP Billiton is perceived as one of the biggest global mining

organisations, it is obvious that it would earn enormous amount of profit and it forms the key

to the investors. However, it could be accomplished only when the organisation publishes its

5 | P a g e

ACCG224 S3 2018 SID

SECTOR

From the annual report of BHP Billiton in 2018, PPE is recorded at cost after

deduction of impairment charges and accumulated depreciation. Cost is treated as the fair

consideration value provided for purchasing the asset during construction or acquisition and it

comprises of the direct expenses to bring the asset into location along with required operating

conditions and the projected future expenses of closure and facility rehabilitation (Bhp.com

2018). The projection of residual lives, depreciation methods and useful lives of PPE of BHP

Billiton could be found from its annual report (Refer to Appendix, Figure 1).

“Paragraph 77 of AASB 116” states the kind of evidence needed for disclosure

during PPE revaluation. BHP Billiton does not use this method; instead, it adjusts the residual

value as well as useful lives at the end of each reporting year. Thus, the accounting policy

information and representation of balance sheet statement from the annual report of BHP

Billiton does not fulfil the necessary disclosure in accordance with this paragraph.

3. Extent to which the PPE disclosures of BHP Billiton satisfy fundamental and

enhancing qualitative characteristics of useful financial information:

The PPE disclosures of BHP Billiton meet the fundamental characteristics and

majority of enhancing characteristics with nearly entire compliance of the accounting

standards. The fundamental characteristics contain material and predictive values along with

faithful representation without material error (Bond, Govendir and Wells 2016).

At the time of assessing the annual report, the carrying values of PPE at the end of

2018 have been stated clearly in the balance sheet statement (Refer to Appendix, Figure 2).

This makes it easy in estimating the future economic benefits of PPE. On the other hand, the

financial reports have clear outline of the PPE items of the organisation or disclosure of the

depreciation methods used. This implies that BHP Billiton has ensured faithful representation

indicating some errors in the 2018 annual report.

When it comes to enhancing qualitative characteristics, the significant ones include

timeliness and understandability for BHP Billiton. With the help of timeliness, the investors

and users could undertake decisions of whether to invest in the organisation (Crawford, Lont

and Scott 2014). As BHP Billiton is perceived as one of the biggest global mining

organisations, it is obvious that it would earn enormous amount of profit and it forms the key

to the investors. However, it could be accomplished only when the organisation publishes its

5 | P a g e

ACCG224 S3 2018 SID

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

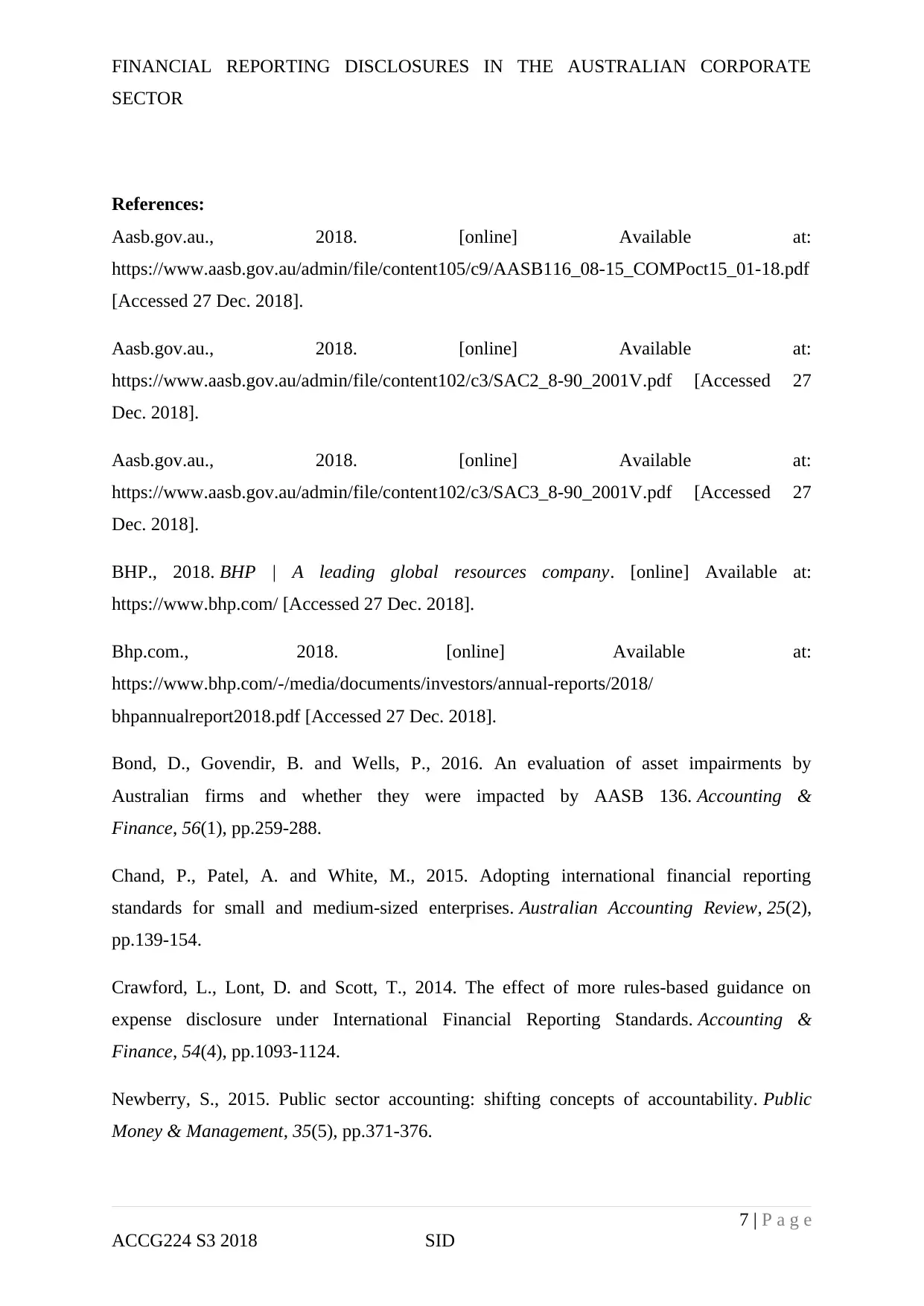

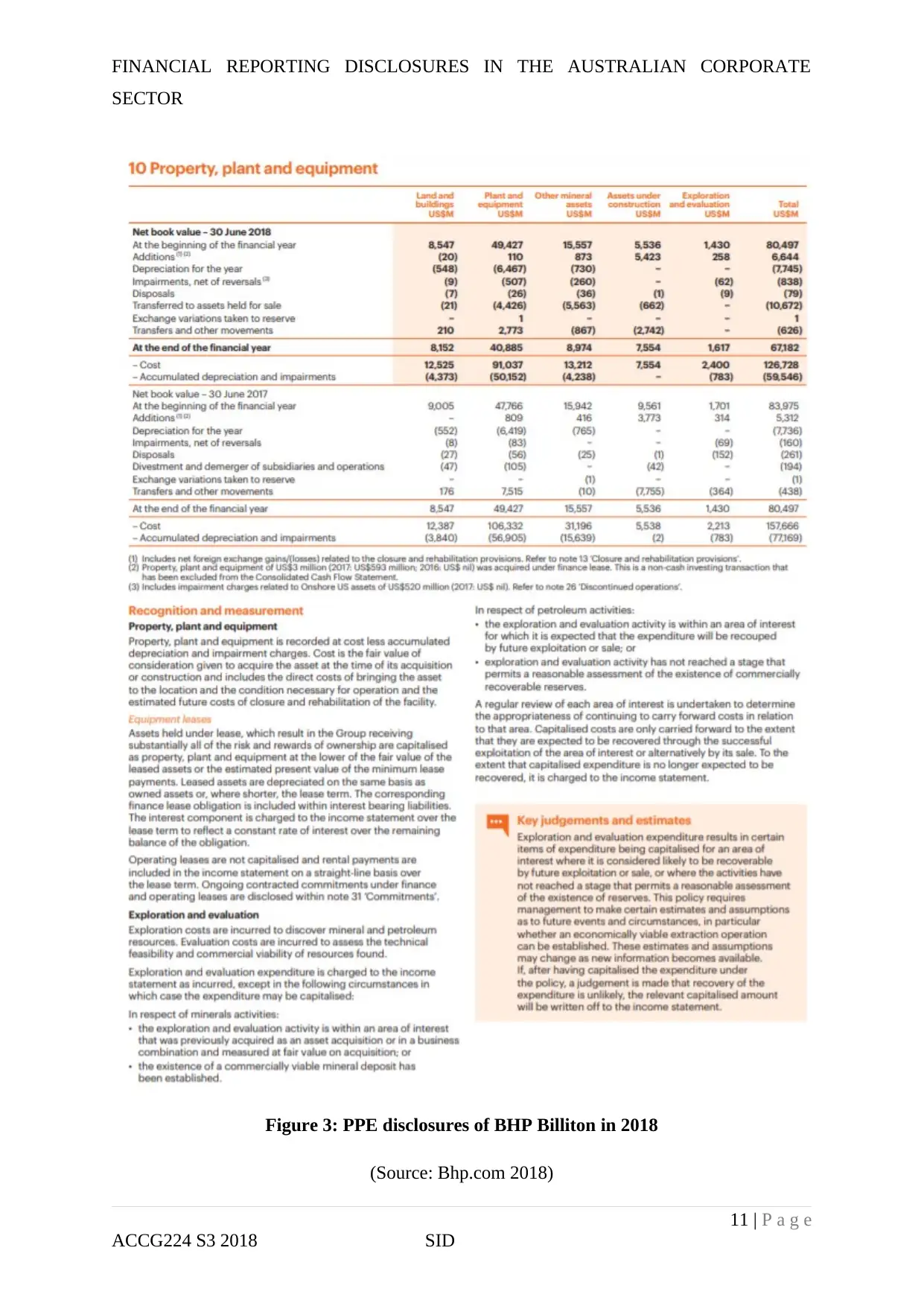

financial reports timely. From the fundamental perspective, understandability implies easy

interpretation of information in the financial reports (Newberry 2015). The PPE format in the

balance sheet must be easily understandable and for the accounting policy sections, it

provides the definitions with few types of particular accounting terms (Refer to Appendix,

Figure 3).

4. Alignment of the PPE disclosures with the objective of general purpose financial

reporting and actions for improvement for BHP Billiton:

It has already been analysed that GPFR intends to deliver correct financial

information for lenders, creditors and investors for estimation of future economic

performance (Perera and Chand 2015). In addition, disclosure of economic resources is

crucial as well, as the same would aid the investors in identifying the strengths and

drawbacks of the organisation. From the 2018 annual report of BHP Billiton, the book

amount of PPE is disclosed and as a result, the investors could compute the liquidity ratio

easily to understand the current financial position of the organisation.

From the above discussion, it is evident that BHP Billiton has complied with relevant

accounting standards that could be validated by the independent audit report. In addition, it

has provided clear explanation of the existing use of depreciation methods and useful life

projections. Thus, the only recommendations for the organisation include keeping the audit

report in hand at all times and the disclosure of the kind of PPE it obtains in the balance sheet

statement.

Conclusion:

To infer, it could be stated that the annual report of BHP Billiton has complied with

the PPE requirement of AASB 116 as well as the IASB conceptual framework. The

organisation has adopted accounting policies for the depreciation methods along with useful

life projections to adhere to the accounting standards. Hence, it could be stated that BHP

Billiton is a good example to record and follow the accounting policies for PPE in accordance

with AASB 116 and IASB.

6 | P a g e

ACCG224 S3 2018 SID

SECTOR

financial reports timely. From the fundamental perspective, understandability implies easy

interpretation of information in the financial reports (Newberry 2015). The PPE format in the

balance sheet must be easily understandable and for the accounting policy sections, it

provides the definitions with few types of particular accounting terms (Refer to Appendix,

Figure 3).

4. Alignment of the PPE disclosures with the objective of general purpose financial

reporting and actions for improvement for BHP Billiton:

It has already been analysed that GPFR intends to deliver correct financial

information for lenders, creditors and investors for estimation of future economic

performance (Perera and Chand 2015). In addition, disclosure of economic resources is

crucial as well, as the same would aid the investors in identifying the strengths and

drawbacks of the organisation. From the 2018 annual report of BHP Billiton, the book

amount of PPE is disclosed and as a result, the investors could compute the liquidity ratio

easily to understand the current financial position of the organisation.

From the above discussion, it is evident that BHP Billiton has complied with relevant

accounting standards that could be validated by the independent audit report. In addition, it

has provided clear explanation of the existing use of depreciation methods and useful life

projections. Thus, the only recommendations for the organisation include keeping the audit

report in hand at all times and the disclosure of the kind of PPE it obtains in the balance sheet

statement.

Conclusion:

To infer, it could be stated that the annual report of BHP Billiton has complied with

the PPE requirement of AASB 116 as well as the IASB conceptual framework. The

organisation has adopted accounting policies for the depreciation methods along with useful

life projections to adhere to the accounting standards. Hence, it could be stated that BHP

Billiton is a good example to record and follow the accounting policies for PPE in accordance

with AASB 116 and IASB.

6 | P a g e

ACCG224 S3 2018 SID

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

References:

Aasb.gov.au., 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-15_COMPoct15_01-18.pdf

[Accessed 27 Dec. 2018].

Aasb.gov.au., 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/SAC2_8-90_2001V.pdf [Accessed 27

Dec. 2018].

Aasb.gov.au., 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/SAC3_8-90_2001V.pdf [Accessed 27

Dec. 2018].

BHP., 2018. BHP | A leading global resources company. [online] Available at:

https://www.bhp.com/ [Accessed 27 Dec. 2018].

Bhp.com., 2018. [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2018/

bhpannualreport2018.pdf [Accessed 27 Dec. 2018].

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by

Australian firms and whether they were impacted by AASB 136. Accounting &

Finance, 56(1), pp.259-288.

Chand, P., Patel, A. and White, M., 2015. Adopting international financial reporting

standards for small and medium‐sized enterprises. Australian Accounting Review, 25(2),

pp.139-154.

Crawford, L., Lont, D. and Scott, T., 2014. The effect of more rules‐based guidance on

expense disclosure under International Financial Reporting Standards. Accounting &

Finance, 54(4), pp.1093-1124.

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

7 | P a g e

ACCG224 S3 2018 SID

SECTOR

References:

Aasb.gov.au., 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content105/c9/AASB116_08-15_COMPoct15_01-18.pdf

[Accessed 27 Dec. 2018].

Aasb.gov.au., 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/SAC2_8-90_2001V.pdf [Accessed 27

Dec. 2018].

Aasb.gov.au., 2018. [online] Available at:

https://www.aasb.gov.au/admin/file/content102/c3/SAC3_8-90_2001V.pdf [Accessed 27

Dec. 2018].

BHP., 2018. BHP | A leading global resources company. [online] Available at:

https://www.bhp.com/ [Accessed 27 Dec. 2018].

Bhp.com., 2018. [online] Available at:

https://www.bhp.com/-/media/documents/investors/annual-reports/2018/

bhpannualreport2018.pdf [Accessed 27 Dec. 2018].

Bond, D., Govendir, B. and Wells, P., 2016. An evaluation of asset impairments by

Australian firms and whether they were impacted by AASB 136. Accounting &

Finance, 56(1), pp.259-288.

Chand, P., Patel, A. and White, M., 2015. Adopting international financial reporting

standards for small and medium‐sized enterprises. Australian Accounting Review, 25(2),

pp.139-154.

Crawford, L., Lont, D. and Scott, T., 2014. The effect of more rules‐based guidance on

expense disclosure under International Financial Reporting Standards. Accounting &

Finance, 54(4), pp.1093-1124.

Newberry, S., 2015. Public sector accounting: shifting concepts of accountability. Public

Money & Management, 35(5), pp.371-376.

7 | P a g e

ACCG224 S3 2018 SID

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Perera, D. and Chand, P., 2015. Issues in the adoption of international financial reporting

standards (IFRS) for small and medium-sized enterprises (SMES). Advances in

accounting, 31(1), pp.165-178.

8 | P a g e

ACCG224 S3 2018 SID

SECTOR

Perera, D. and Chand, P., 2015. Issues in the adoption of international financial reporting

standards (IFRS) for small and medium-sized enterprises (SMES). Advances in

accounting, 31(1), pp.165-178.

8 | P a g e

ACCG224 S3 2018 SID

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Appendix:

Figure 1: Depreciation-related estimations and judgements of BHP Billiton

(Source: Bhp.com 2018)

9 | P a g e

ACCG224 S3 2018 SID

SECTOR

Appendix:

Figure 1: Depreciation-related estimations and judgements of BHP Billiton

(Source: Bhp.com 2018)

9 | P a g e

ACCG224 S3 2018 SID

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Figure 2: Consolidated balance sheet statement of BHP Billiton in 2018

(Source: Bhp.com 2018)

10 | P a g e

ACCG224 S3 2018 SID

SECTOR

Figure 2: Consolidated balance sheet statement of BHP Billiton in 2018

(Source: Bhp.com 2018)

10 | P a g e

ACCG224 S3 2018 SID

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

Figure 3: PPE disclosures of BHP Billiton in 2018

(Source: Bhp.com 2018)

11 | P a g e

ACCG224 S3 2018 SID

SECTOR

Figure 3: PPE disclosures of BHP Billiton in 2018

(Source: Bhp.com 2018)

11 | P a g e

ACCG224 S3 2018 SID

FINANCIAL REPORTING DISCLOSURES IN THE AUSTRALIAN CORPORATE

SECTOR

12 | P a g e

ACCG224 S3 2018 SID

SECTOR

12 | P a g e

ACCG224 S3 2018 SID

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.