Financial Reporting: Fair Value, Impairment, and Intangible Assets

VerifiedAdded on 2020/03/16

|13

|2533

|51

Report

AI Summary

This report provides a detailed analysis of financial reporting, addressing key areas such as fair value measurement, asset impairment, intangible assets, and employee benefits, all within the framework of Australian Accounting Standards Board (AASB) standards. The report begins with an examination of fair value accounting, outlining relevant issues, accounting justifications, and valuation techniques, especially considering its application to non-profit organizations like aged care homes. It then explores the accounting treatment of asset impairment, including detailed calculations and journal entries for revaluation, depreciation, and impairment losses. The report also delves into the complexities of accounting for intangible assets, differentiating between internally generated and acquired assets, and highlighting the conditions for capitalization. Finally, the report addresses employee benefits, specifically defined benefit plans, providing calculations and journal entries for net defined benefit liability, net interest, and reconciliation, offering a comprehensive understanding of financial reporting principles and practices.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

FInancial Reporting.........................................................................................................................1

Question 1........................................................................................................................................2

Provisions:...................................................................................................................................2

Issues:..........................................................................................................................................2

Highest and Best Use:..................................................................................................................2

Application to aged care home:...................................................................................................3

Question2.........................................................................................................................................3

Accounting Justification:.............................................................................................................3

Relevant Issues:...........................................................................................................................3

Calculations & General Journal Entries 1/7/16 to 30/6/17:.........................................................3

Calculations & General Journal Entries 1/8/18:..........................................................................5

Calculations & General Journal Entries 30/6/18:........................................................................5

Question 3........................................................................................................................................6

Accounting Justification:.............................................................................................................6

Relevant Issues:...........................................................................................................................7

Difference between two phases:..................................................................................................7

Accounting for Research and Development:...............................................................................7

Conclusion:..................................................................................................................................8

Question 4........................................................................................................................................8

Accounting Justification:.............................................................................................................8

Deficit of Fund.............................................................................................................................8

Net Defined Benefit Liability......................................................................................................8

Net Interest...................................................................................................................................8

Reconciliation..............................................................................................................................9

FInancial Reporting.........................................................................................................................1

Question 1........................................................................................................................................2

Provisions:...................................................................................................................................2

Issues:..........................................................................................................................................2

Highest and Best Use:..................................................................................................................2

Application to aged care home:...................................................................................................3

Question2.........................................................................................................................................3

Accounting Justification:.............................................................................................................3

Relevant Issues:...........................................................................................................................3

Calculations & General Journal Entries 1/7/16 to 30/6/17:.........................................................3

Calculations & General Journal Entries 1/8/18:..........................................................................5

Calculations & General Journal Entries 30/6/18:........................................................................5

Question 3........................................................................................................................................6

Accounting Justification:.............................................................................................................6

Relevant Issues:...........................................................................................................................7

Difference between two phases:..................................................................................................7

Accounting for Research and Development:...............................................................................7

Conclusion:..................................................................................................................................8

Question 4........................................................................................................................................8

Accounting Justification:.............................................................................................................8

Deficit of Fund.............................................................................................................................8

Net Defined Benefit Liability......................................................................................................8

Net Interest...................................................................................................................................8

Reconciliation..............................................................................................................................9

References......................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 1

Accounting Justification:

AASB 13 defines “fair value” and it also provides standard guidelines for determination of fair

value. Further it also outlines the disclosures to be made for fair value measurement. As per

AASB 13 fair value measurement is market based and not entity specific based.

Relevant Issues:

Financial Institutions use fair value method for valuation of financial instruments in normal

course of business. However it involves a lot of judgment and prudence while valuing tangible

assets (International Accounting Standards Board, 2014). Unrealized Loss and Gains which are

accruing to the concern on account of using fair value method doesn’t reflect the importance of

that relevant asset to the organization. Moreover there are also inconsistencies regarding

individual businesses practices in using fair value for plant and equipment.

1& 2 Determine subject of measurement and valuation premise:

For determination of fair value it is important to whether the non-financial asset which is being

valued is used in manner from which it can yield highest returns as on the date of measurement.

It takes into account the ability of market participant to generate economic benefits from the use

of non-financial asset or by transferring it to another market competitor who would use the asset

in best and highest manner (Hu, Percy and Yao, 2015). The highest and best use of non-financial

asset also considers use of the asset that whether it is physically possible, legally permissible and

financially feasible or not.

3. Determine Market

For some asset and liability it may be possible that market information may not be available.

However market information is available or not objective remains the same in both the cases i.e.

to determine a price at which transaction will take place between two independent parties under

the prevailing market conditions (Palea, 2014). As per views of Liang and Riedl (2013) in other

words it is an exit price from the purview of independent party that holds the asset or owes the

liability.

Accounting Justification:

AASB 13 defines “fair value” and it also provides standard guidelines for determination of fair

value. Further it also outlines the disclosures to be made for fair value measurement. As per

AASB 13 fair value measurement is market based and not entity specific based.

Relevant Issues:

Financial Institutions use fair value method for valuation of financial instruments in normal

course of business. However it involves a lot of judgment and prudence while valuing tangible

assets (International Accounting Standards Board, 2014). Unrealized Loss and Gains which are

accruing to the concern on account of using fair value method doesn’t reflect the importance of

that relevant asset to the organization. Moreover there are also inconsistencies regarding

individual businesses practices in using fair value for plant and equipment.

1& 2 Determine subject of measurement and valuation premise:

For determination of fair value it is important to whether the non-financial asset which is being

valued is used in manner from which it can yield highest returns as on the date of measurement.

It takes into account the ability of market participant to generate economic benefits from the use

of non-financial asset or by transferring it to another market competitor who would use the asset

in best and highest manner (Hu, Percy and Yao, 2015). The highest and best use of non-financial

asset also considers use of the asset that whether it is physically possible, legally permissible and

financially feasible or not.

3. Determine Market

For some asset and liability it may be possible that market information may not be available.

However market information is available or not objective remains the same in both the cases i.e.

to determine a price at which transaction will take place between two independent parties under

the prevailing market conditions (Palea, 2014). As per views of Liang and Riedl (2013) in other

words it is an exit price from the purview of independent party that holds the asset or owes the

liability.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4. Determine valuation technique:

AASB 13 directs the chief accountant to reflect assets market price considering its best and

highest use for determination of fair value. But this creates problem for the non-profit

organization. If the asset of the non-profit organization i.e. old age homes if provided to market

participant for building flats (which will be its best and highest use) then the fair value would be

much higher as depicted in the books. This also doesn’t depict the importance of asset to the

organization. It only states that value should be market based and situation based. It only focuses

or considers the value which would have been deprived by the market participant by using it or

by selling it. Thus in this case fair value may not reflect actual value and it also creates lot of

problem and confusion (Hoyle, Schaefer and Doupnik, 2015).

QUESTION 2

Accounting Justification:

AASB 136 provides accounting treatment relating to impairment of assets. Provision relating to

accounting of impairment loss has been provided in Para 58 to 64 in specified accounting

standard.

Relevant Issues:

In accordance with provided facts, Peewee Ltd, has acquired assets A& B and further sold asset

B and purchased C. As the asset has been revalued at the end of each year; thus calculation

relating to impairment of same has been provided below.

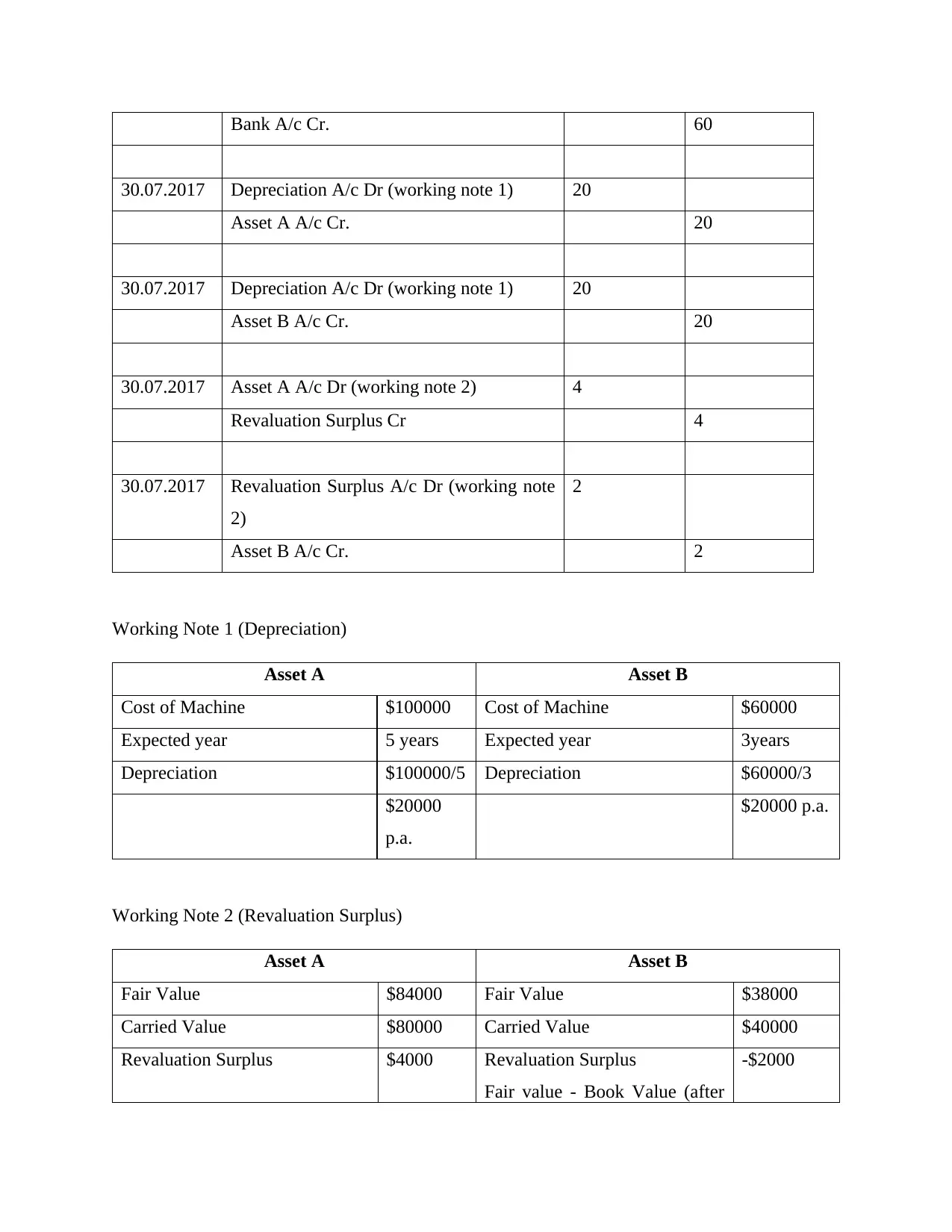

1. Calculations & General Journal Entries 1/7/16 to 30/6/17:

(Amount in $000)

Date Account Debit Credit

01.07.2016 Asset A A/c Dr. 100

Bank A/C 100

01.07.2016 Asset B A/c Dr. 60

AASB 13 directs the chief accountant to reflect assets market price considering its best and

highest use for determination of fair value. But this creates problem for the non-profit

organization. If the asset of the non-profit organization i.e. old age homes if provided to market

participant for building flats (which will be its best and highest use) then the fair value would be

much higher as depicted in the books. This also doesn’t depict the importance of asset to the

organization. It only states that value should be market based and situation based. It only focuses

or considers the value which would have been deprived by the market participant by using it or

by selling it. Thus in this case fair value may not reflect actual value and it also creates lot of

problem and confusion (Hoyle, Schaefer and Doupnik, 2015).

QUESTION 2

Accounting Justification:

AASB 136 provides accounting treatment relating to impairment of assets. Provision relating to

accounting of impairment loss has been provided in Para 58 to 64 in specified accounting

standard.

Relevant Issues:

In accordance with provided facts, Peewee Ltd, has acquired assets A& B and further sold asset

B and purchased C. As the asset has been revalued at the end of each year; thus calculation

relating to impairment of same has been provided below.

1. Calculations & General Journal Entries 1/7/16 to 30/6/17:

(Amount in $000)

Date Account Debit Credit

01.07.2016 Asset A A/c Dr. 100

Bank A/C 100

01.07.2016 Asset B A/c Dr. 60

Bank A/c Cr. 60

30.07.2017 Depreciation A/c Dr (working note 1) 20

Asset A A/c Cr. 20

30.07.2017 Depreciation A/c Dr (working note 1) 20

Asset B A/c Cr. 20

30.07.2017 Asset A A/c Dr (working note 2) 4

Revaluation Surplus Cr 4

30.07.2017 Revaluation Surplus A/c Dr (working note

2)

2

Asset B A/c Cr. 2

Working Note 1 (Depreciation)

Asset A Asset B

Cost of Machine $100000 Cost of Machine $60000

Expected year 5 years Expected year 3years

Depreciation $100000/5 Depreciation $60000/3

$20000

p.a.

$20000 p.a.

Working Note 2 (Revaluation Surplus)

Asset A Asset B

Fair Value $84000 Fair Value $38000

Carried Value $80000 Carried Value $40000

Revaluation Surplus $4000 Revaluation Surplus

Fair value - Book Value (after

-$2000

30.07.2017 Depreciation A/c Dr (working note 1) 20

Asset A A/c Cr. 20

30.07.2017 Depreciation A/c Dr (working note 1) 20

Asset B A/c Cr. 20

30.07.2017 Asset A A/c Dr (working note 2) 4

Revaluation Surplus Cr 4

30.07.2017 Revaluation Surplus A/c Dr (working note

2)

2

Asset B A/c Cr. 2

Working Note 1 (Depreciation)

Asset A Asset B

Cost of Machine $100000 Cost of Machine $60000

Expected year 5 years Expected year 3years

Depreciation $100000/5 Depreciation $60000/3

$20000

p.a.

$20000 p.a.

Working Note 2 (Revaluation Surplus)

Asset A Asset B

Fair Value $84000 Fair Value $38000

Carried Value $80000 Carried Value $40000

Revaluation Surplus $4000 Revaluation Surplus

Fair value - Book Value (after

-$2000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Fair value - Book Value (after

depreciation) (Hitz, 2013)

depreciation)

2. Calculations & General Journal Entries 1/8/18:

(Amount in $000)

Date Account Debit Credit

01.08 2018 Cash A/c 29

Revaluation A/c 2

Profit & Loss A/c 7

To Asset B A/c Cr. 38

(Being Loss recognized on sale of

machine)

01.08.2018 Cash A/c 80

To Asset C A/c 80

(Being Asset C purchased for cash)

01.08.2018 General reserve A/c 8

Revaluation Surplus A/c 2

To Share Capital A/c Cr. 10

(Bonus share issued during year)

3. Calculations & General Journal Entries 30/6/18:

(Amount in $000)

Date Account Debit Credit

30.06.2018 Depreciation A/c (working note 1) 21

To Asset A/c Cr 21

depreciation) (Hitz, 2013)

depreciation)

2. Calculations & General Journal Entries 1/8/18:

(Amount in $000)

Date Account Debit Credit

01.08 2018 Cash A/c 29

Revaluation A/c 2

Profit & Loss A/c 7

To Asset B A/c Cr. 38

(Being Loss recognized on sale of

machine)

01.08.2018 Cash A/c 80

To Asset C A/c 80

(Being Asset C purchased for cash)

01.08.2018 General reserve A/c 8

Revaluation Surplus A/c 2

To Share Capital A/c Cr. 10

(Bonus share issued during year)

3. Calculations & General Journal Entries 30/6/18:

(Amount in $000)

Date Account Debit Credit

30.06.2018 Depreciation A/c (working note 1) 21

To Asset A/c Cr 21

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

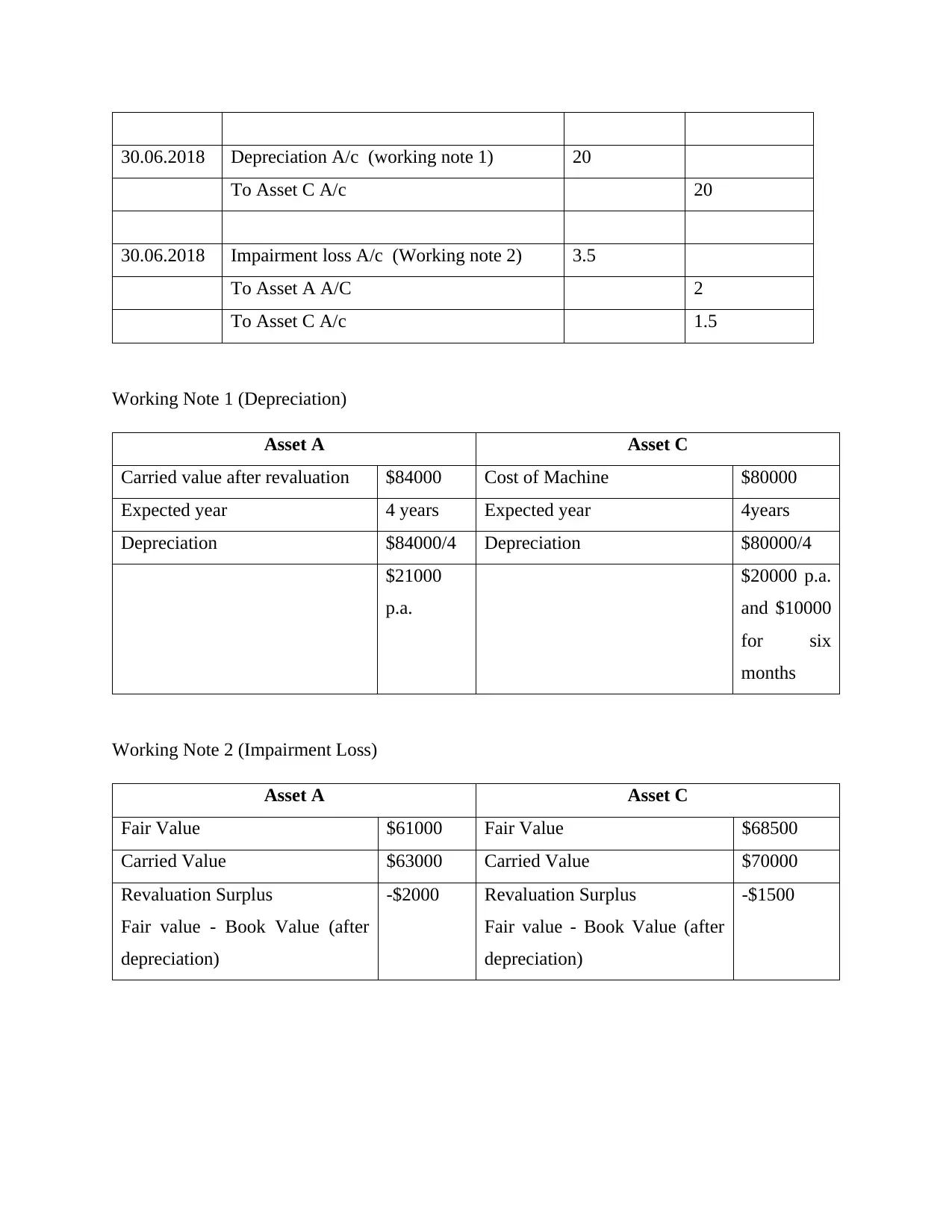

30.06.2018 Depreciation A/c (working note 1) 20

To Asset C A/c 20

30.06.2018 Impairment loss A/c (Working note 2) 3.5

To Asset A A/C 2

To Asset C A/c 1.5

Working Note 1 (Depreciation)

Asset A Asset C

Carried value after revaluation $84000 Cost of Machine $80000

Expected year 4 years Expected year 4years

Depreciation $84000/4 Depreciation $80000/4

$21000

p.a.

$20000 p.a.

and $10000

for six

months

Working Note 2 (Impairment Loss)

Asset A Asset C

Fair Value $61000 Fair Value $68500

Carried Value $63000 Carried Value $70000

Revaluation Surplus

Fair value - Book Value (after

depreciation)

-$2000 Revaluation Surplus

Fair value - Book Value (after

depreciation)

-$1500

To Asset C A/c 20

30.06.2018 Impairment loss A/c (Working note 2) 3.5

To Asset A A/C 2

To Asset C A/c 1.5

Working Note 1 (Depreciation)

Asset A Asset C

Carried value after revaluation $84000 Cost of Machine $80000

Expected year 4 years Expected year 4years

Depreciation $84000/4 Depreciation $80000/4

$21000

p.a.

$20000 p.a.

and $10000

for six

months

Working Note 2 (Impairment Loss)

Asset A Asset C

Fair Value $61000 Fair Value $68500

Carried Value $63000 Carried Value $70000

Revaluation Surplus

Fair value - Book Value (after

depreciation)

-$2000 Revaluation Surplus

Fair value - Book Value (after

depreciation)

-$1500

QUESTION 3

Accounting Justification & Relevant Issues

AASB 138 (Intangible Assets) deals with the accounting and disclosure of Intangible Assets. It

also throws light on goodwill generated within the organization and expenditure done during

research and development phase. AASB 138 states that expenditure done during the

development phase should be recognized as intangible asset only when the following conditions

are satisfied:

1. Intangible Asset should can be use further or sold during at the end of development

phase.

2. There must be intention of organization of using the Intangible or selling it.

3. It must be capable to generate future economic benefits.

4. Adequate resources must be available to complete the development phase of the

Intangibles.

5. Expenditure done during the development phase and attributed to the Intangible should

be measurable.

1. Relevant Issues:

If conditions mentioned above aren’t fulfilled then expenditure incurred to create intangibles will

be charged to Revenue Account of that particular period and won’t be capitalized i.e. it won’t be

added to the cost of asset. Hence the expenditure incurred on internally generated goodwill

doesn’t include the total cost incurred (Yao and Percy , 2015). It also prohibits capitalization of

some intangible assets that are internally generated.

AASB 138 requires that expenditures incurred during development phase of internally generated

goodwill should be charged to Revenue account if the conditions mentioned in it are not met

(AASB 138.Intangible Assets, 2016). But if the conditions mentioned are met then these cost

should be capitalized or should be added to the cost of asset. Moreover AASB 138 also requires

assessing the useful life of internally generated goodwill. If the life of the goodwill is assessed

then the cost of asset will be amortized over the useful life of it but if the useful life of the asset

cannot be worked out then AASB 138 gives an option to amortize the cost of asset in maximum

Accounting Justification & Relevant Issues

AASB 138 (Intangible Assets) deals with the accounting and disclosure of Intangible Assets. It

also throws light on goodwill generated within the organization and expenditure done during

research and development phase. AASB 138 states that expenditure done during the

development phase should be recognized as intangible asset only when the following conditions

are satisfied:

1. Intangible Asset should can be use further or sold during at the end of development

phase.

2. There must be intention of organization of using the Intangible or selling it.

3. It must be capable to generate future economic benefits.

4. Adequate resources must be available to complete the development phase of the

Intangibles.

5. Expenditure done during the development phase and attributed to the Intangible should

be measurable.

1. Relevant Issues:

If conditions mentioned above aren’t fulfilled then expenditure incurred to create intangibles will

be charged to Revenue Account of that particular period and won’t be capitalized i.e. it won’t be

added to the cost of asset. Hence the expenditure incurred on internally generated goodwill

doesn’t include the total cost incurred (Yao and Percy , 2015). It also prohibits capitalization of

some intangible assets that are internally generated.

AASB 138 requires that expenditures incurred during development phase of internally generated

goodwill should be charged to Revenue account if the conditions mentioned in it are not met

(AASB 138.Intangible Assets, 2016). But if the conditions mentioned are met then these cost

should be capitalized or should be added to the cost of asset. Moreover AASB 138 also requires

assessing the useful life of internally generated goodwill. If the life of the goodwill is assessed

then the cost of asset will be amortized over the useful life of it but if the useful life of the asset

cannot be worked out then AASB 138 gives an option to amortize the cost of asset in maximum

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

amortization period i.e. 20 years. If the asset has indefinite life then the same would not be

amortized but will be assessed annually for adjustments of impairment.

2. Difference internally generated vs Acquired:

In case the intangible asset is purchase or acquired; then as per provision of AASB 3 the same is

accounted on its fair value on date of acquisition. In case of internally generated the expenditure

relating to research and development phase is done in following manner:

Research phase planning is done with the intent to gain scientific or technical knowledge and

understanding. It is important phase in creating internally generated goodwill. In the research

phase an organization conceptualize the discoveries which will go take place if all things go well.

This is an act of creating new processes that will be used to create new products. Development

phase comes after the research phase where discovered science in converted into a useful product

that organization can use to its benefits and asset is recognized only after it criteria of

development stage. (Zakaria and et.al. 2014).

3. Reason for Reluctance:

AASB 138 mandates only those organizations which are involved in medium and long term

contracts of research and development and to those who work in technology sector. Such

companies are required to reflect and disclose the asset internally generated.

QUESTION 4

Accounting Justification:

AASB 119 ‘Employee benefits’; provides specification relating to employee benefits which

comprises defined benefit plan (AASB 119, Employee Benefit. (2016).). Recognizing procedure

for the same has been specified in Para 66 of AASB 119. Further, Para 26-30 specifies provision

regarding defined plans.

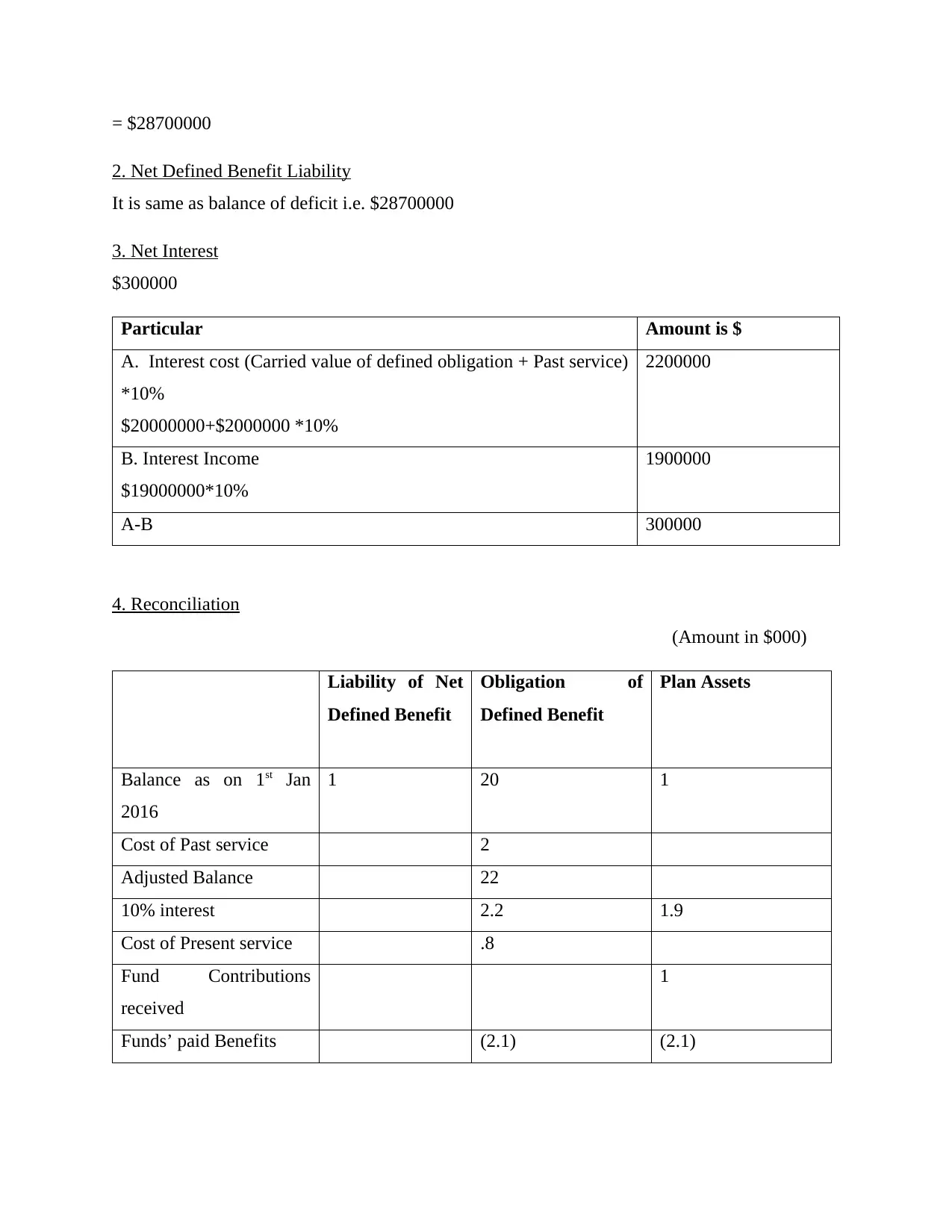

1. Deficit of Fund

Carried value of benefit obligation as on 31st December 2016 – Fair value of plan assets

$23000000- $20130000

amortized but will be assessed annually for adjustments of impairment.

2. Difference internally generated vs Acquired:

In case the intangible asset is purchase or acquired; then as per provision of AASB 3 the same is

accounted on its fair value on date of acquisition. In case of internally generated the expenditure

relating to research and development phase is done in following manner:

Research phase planning is done with the intent to gain scientific or technical knowledge and

understanding. It is important phase in creating internally generated goodwill. In the research

phase an organization conceptualize the discoveries which will go take place if all things go well.

This is an act of creating new processes that will be used to create new products. Development

phase comes after the research phase where discovered science in converted into a useful product

that organization can use to its benefits and asset is recognized only after it criteria of

development stage. (Zakaria and et.al. 2014).

3. Reason for Reluctance:

AASB 138 mandates only those organizations which are involved in medium and long term

contracts of research and development and to those who work in technology sector. Such

companies are required to reflect and disclose the asset internally generated.

QUESTION 4

Accounting Justification:

AASB 119 ‘Employee benefits’; provides specification relating to employee benefits which

comprises defined benefit plan (AASB 119, Employee Benefit. (2016).). Recognizing procedure

for the same has been specified in Para 66 of AASB 119. Further, Para 26-30 specifies provision

regarding defined plans.

1. Deficit of Fund

Carried value of benefit obligation as on 31st December 2016 – Fair value of plan assets

$23000000- $20130000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= $28700000

2. Net Defined Benefit Liability

It is same as balance of deficit i.e. $28700000

3. Net Interest

$300000

Particular Amount is $

A. Interest cost (Carried value of defined obligation + Past service)

*10%

$20000000+$2000000 *10%

2200000

B. Interest Income

$19000000*10%

1900000

A-B 300000

4. Reconciliation

(Amount in $000)

Liability of Net

Defined Benefit

Obligation of

Defined Benefit

Plan Assets

Balance as on 1st Jan

2016

1 20 1

Cost of Past service 2

Adjusted Balance 22

10% interest 2.2 1.9

Cost of Present service .8

Fund Contributions

received

1

Funds’ paid Benefits (2.1) (2.1)

2. Net Defined Benefit Liability

It is same as balance of deficit i.e. $28700000

3. Net Interest

$300000

Particular Amount is $

A. Interest cost (Carried value of defined obligation + Past service)

*10%

$20000000+$2000000 *10%

2200000

B. Interest Income

$19000000*10%

1900000

A-B 300000

4. Reconciliation

(Amount in $000)

Liability of Net

Defined Benefit

Obligation of

Defined Benefit

Plan Assets

Balance as on 1st Jan

2016

1 20 1

Cost of Past service 2

Adjusted Balance 22

10% interest 2.2 1.9

Cost of Present service .8

Fund Contributions

received

1

Funds’ paid Benefits (2.1) (2.1)

Return on Plan Assets

excluding Interest*

.33

Remeasured Actual loss

of Defined Benefit

Obligation

.1

Balance as 31st

December 2016

2.870 23 20.130

Return on plan asset excluding interest

Value as on 31.12.06 – Opening balance – contribution- paid benefits – Interest income

= $20130000 -$19000000 -$1900000 -$1000000- (2100000)

= $330000

5. Summary Journal

Journal Entry

(Amount in $000)

Date Particular Debit Credit

31st December

2016

Superannuation Expenses (P/L) 3 100

To Superannuation Income Account 230

To Bank A/c 1 000

To Superannuation liability A/c 1 870

Reconciliation

(Amount in $000)

Profit or Loss Other

comprehensive

Income

Bank Net DBL(A)

excluding Interest*

.33

Remeasured Actual loss

of Defined Benefit

Obligation

.1

Balance as 31st

December 2016

2.870 23 20.130

Return on plan asset excluding interest

Value as on 31.12.06 – Opening balance – contribution- paid benefits – Interest income

= $20130000 -$19000000 -$1900000 -$1000000- (2100000)

= $330000

5. Summary Journal

Journal Entry

(Amount in $000)

Date Particular Debit Credit

31st December

2016

Superannuation Expenses (P/L) 3 100

To Superannuation Income Account 230

To Bank A/c 1 000

To Superannuation liability A/c 1 870

Reconciliation

(Amount in $000)

Profit or Loss Other

comprehensive

Income

Bank Net DBL(A)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.