Financial Reporting Analysis of Millennium and Copthorne Hotels plc

VerifiedAdded on 2023/01/17

|19

|3681

|57

Report

AI Summary

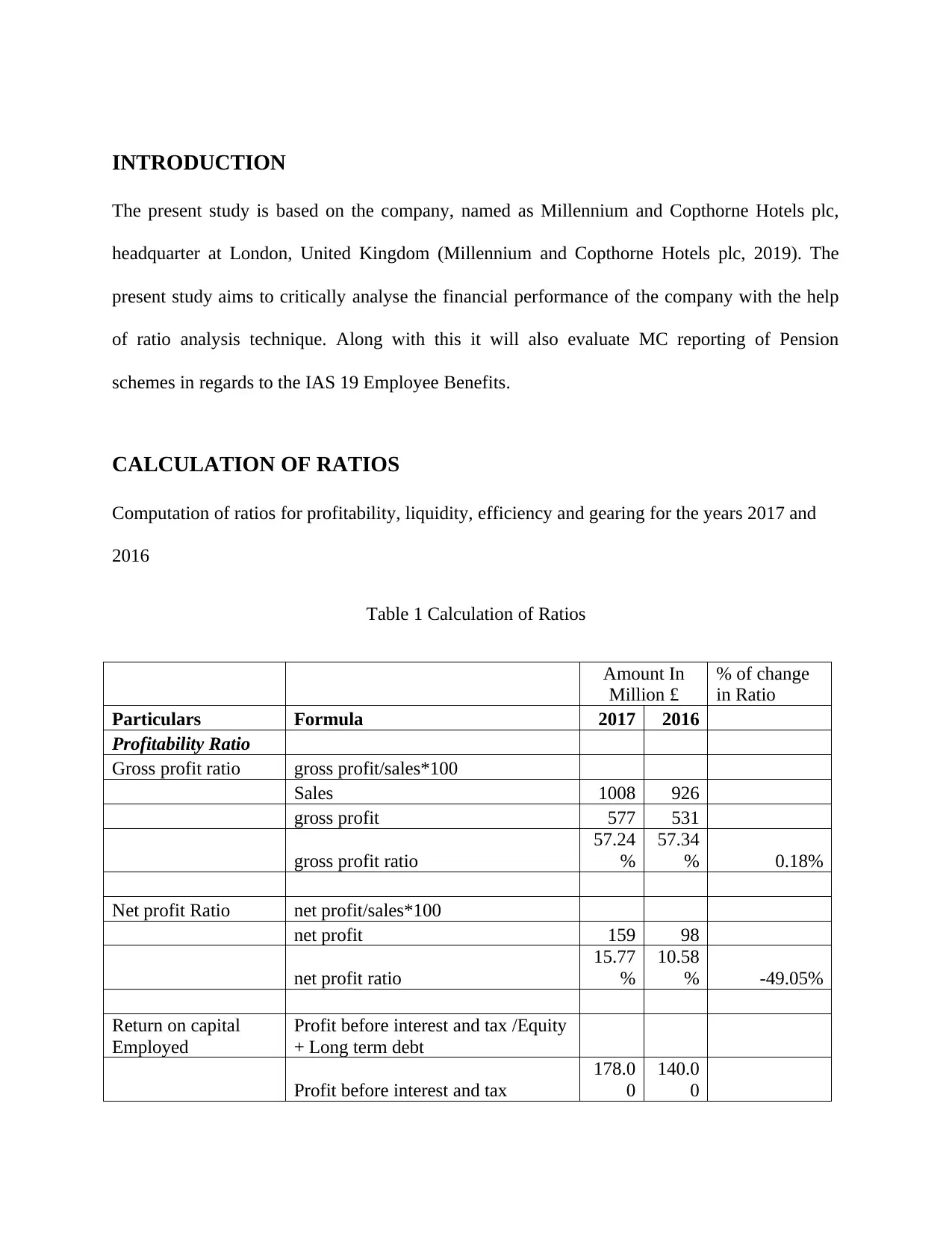

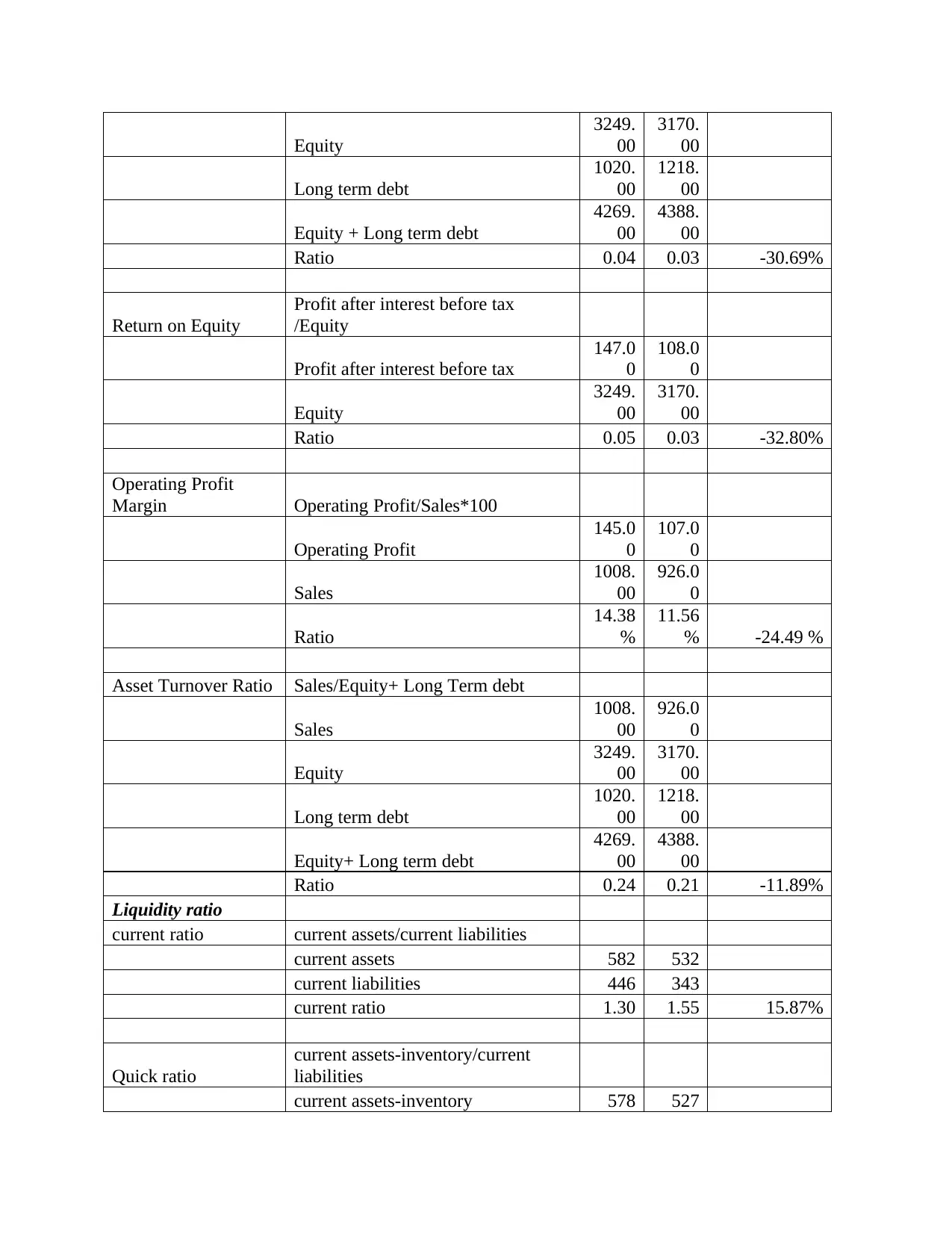

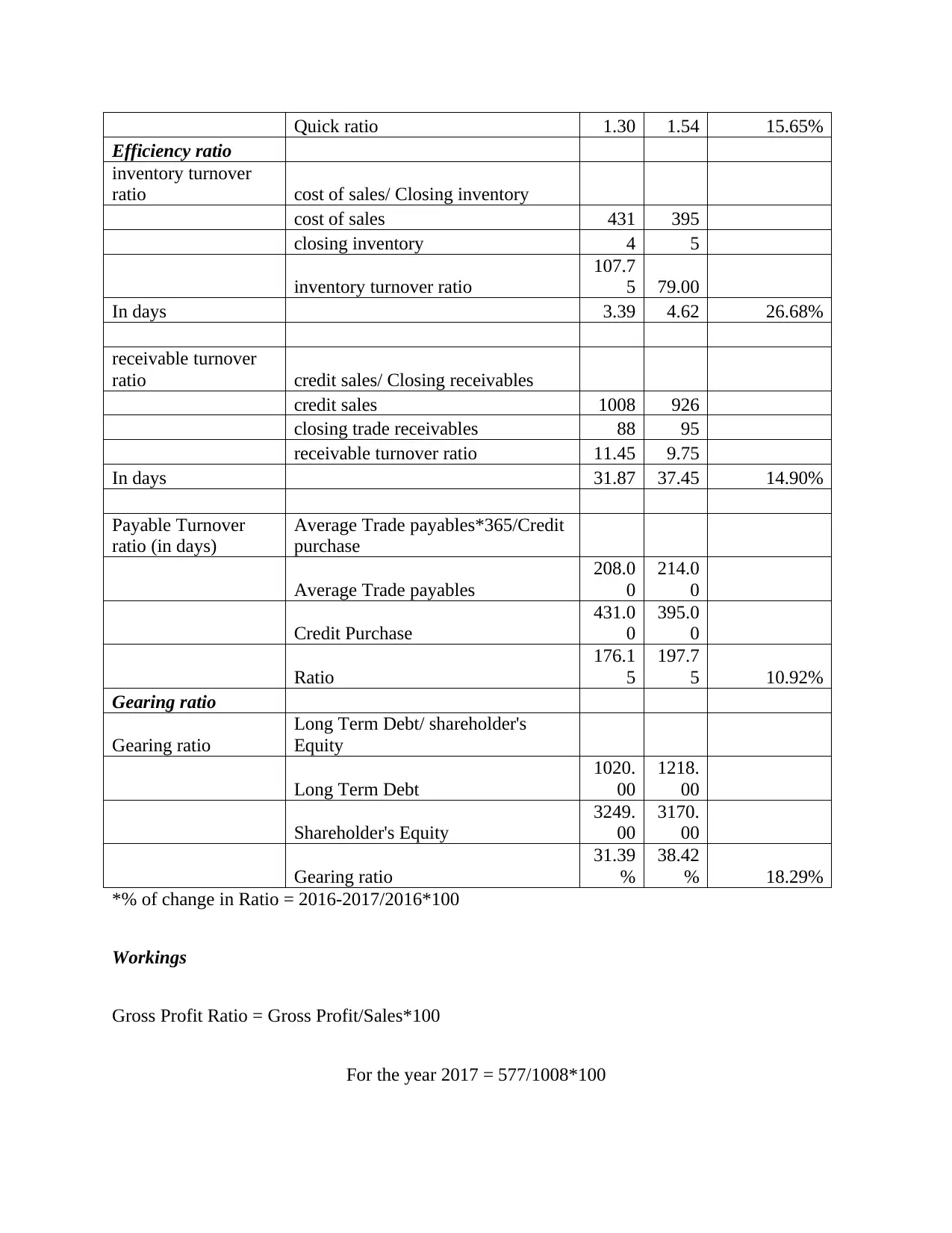

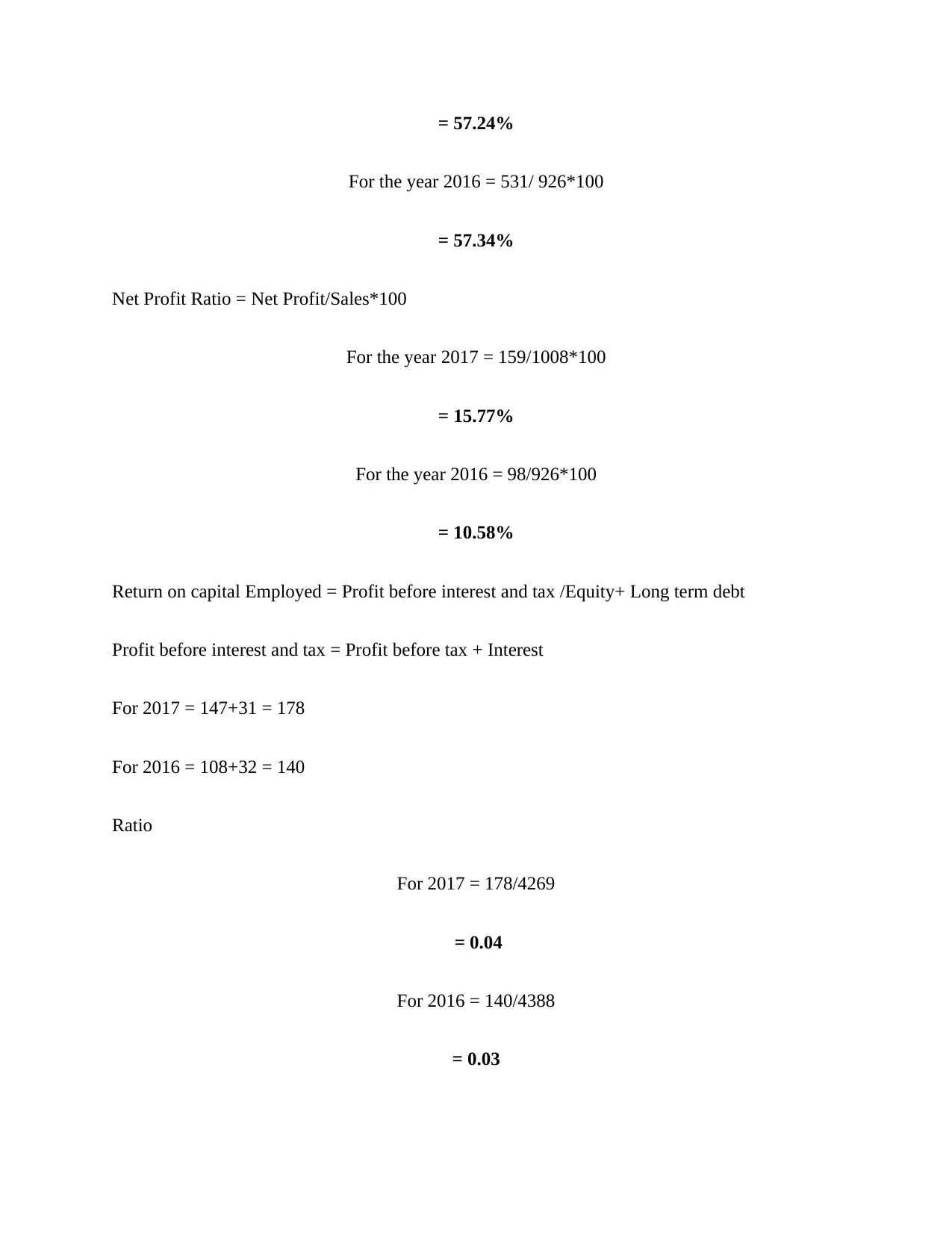

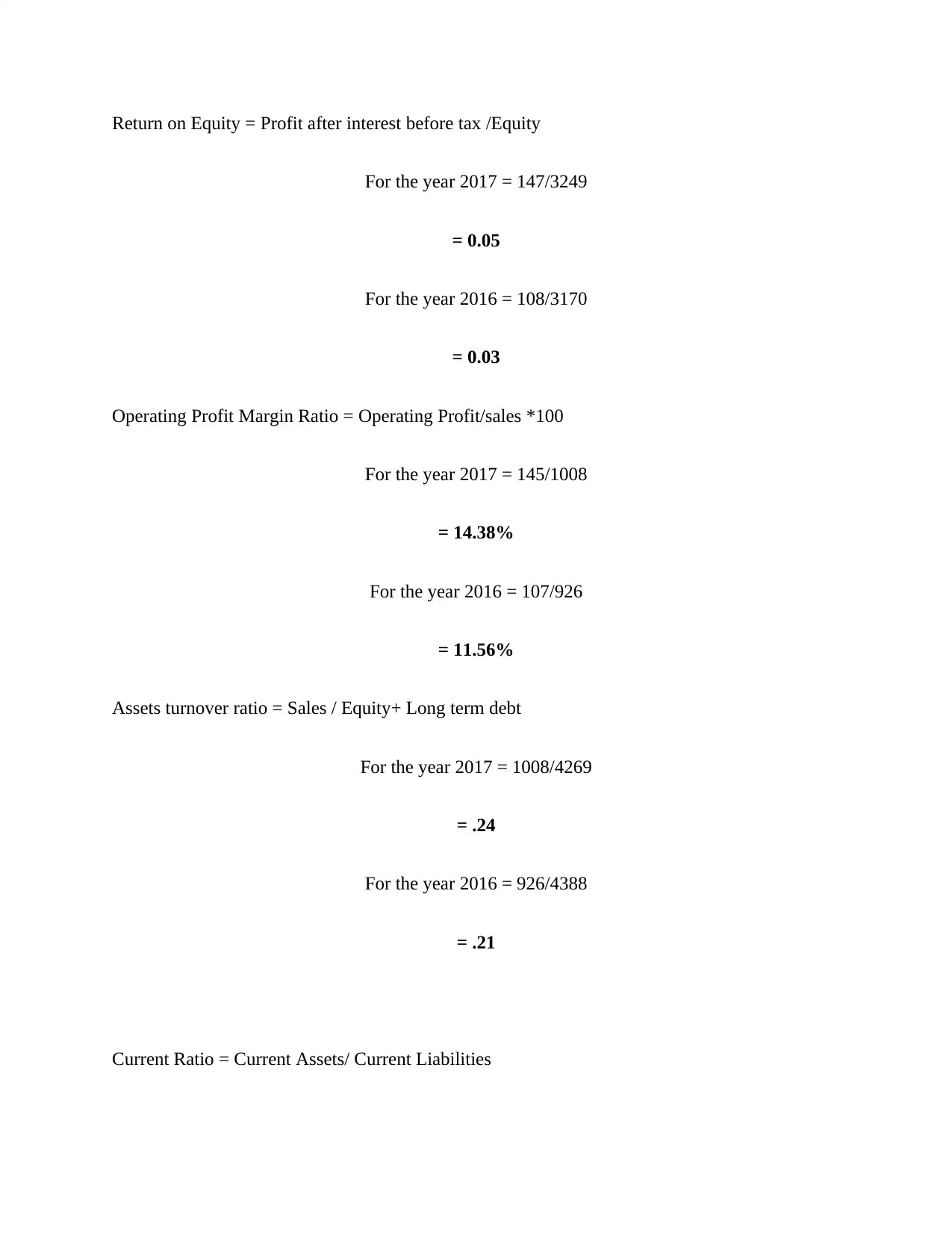

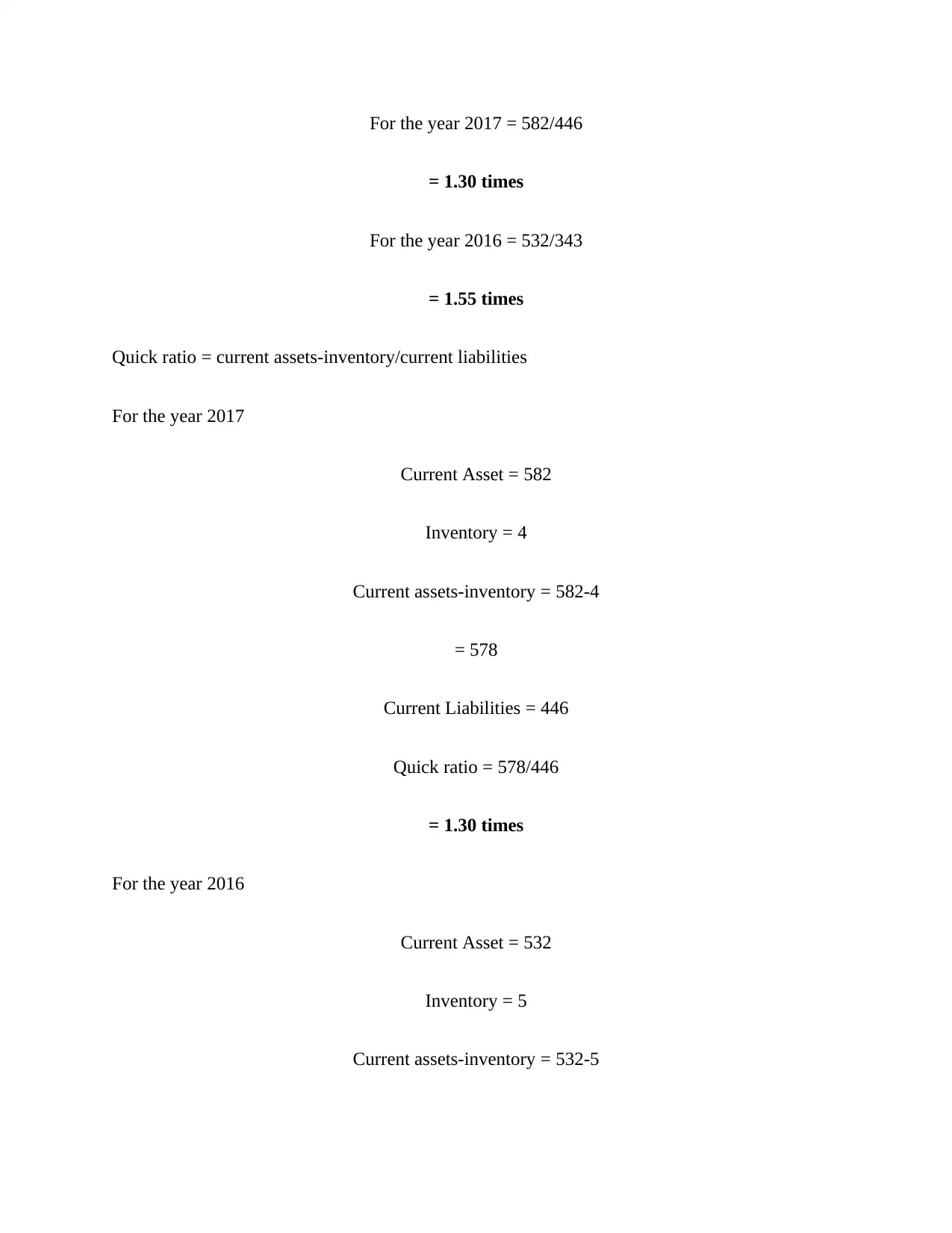

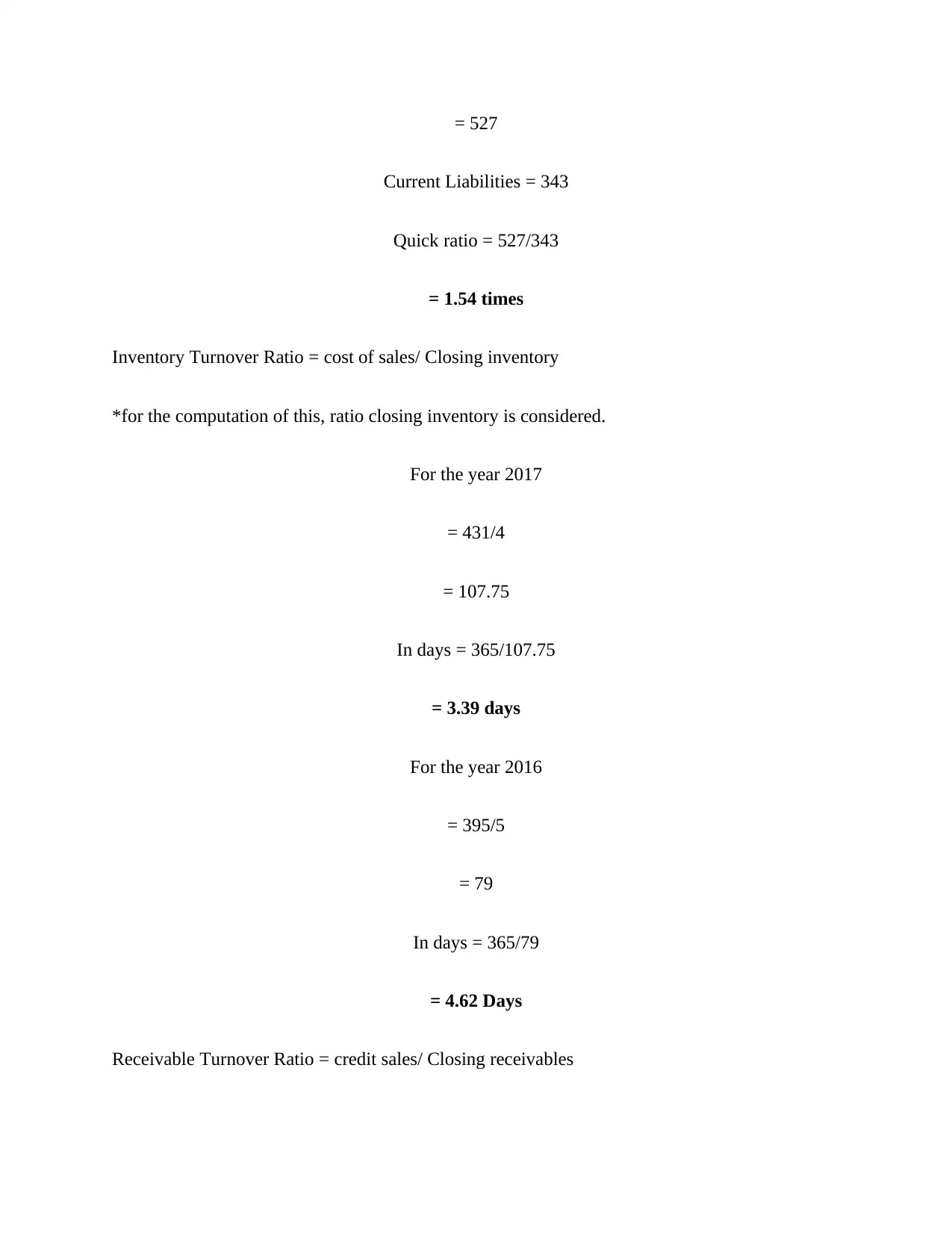

This report provides a comprehensive financial analysis of Millennium and Copthorne Hotels plc. It begins with an introduction outlining the study's objectives, which include a critical examination of the company's financial performance using ratio analysis and an evaluation of its reporting of pension schemes in accordance with IAS 19 Employee Benefits. The report then details the calculation of various financial ratios, including profitability, liquidity, efficiency, and gearing ratios, for the years 2017 and 2016. It presents the formulas, calculations, and percentage changes for each ratio. Following the ratio calculations, the report offers a performance and position analysis, interpreting the results and drawing conclusions about the company's financial health. The analysis covers profitability, liquidity, efficiency, and gearing, providing insights into the company's strengths and weaknesses. Finally, the report addresses the reporting requirements of IAS 19 Employee Benefits, focusing specifically on pension schemes, and concludes with a summary of the findings and a list of references.

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.