Impact of IFRS 16 on Financial Statements

VerifiedAdded on 2020/12/07

|13

|2912

|86

Homework Assignment

AI Summary

This assignment examines the effects of IFRS 16 on a company's financial statements compared to IAS 17. It analyzes how the recognition of lease liabilities under IFRS 16 impacts operating expenses, finance costs (interest expense), and depreciation. The document discusses the presentation of these items within the financial statements and highlights key differences between the two standards.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

2019Financial Reporting for Businesses

Financial analysis of

UNITE GROUP.

Financial analysis of

UNITE GROUP.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

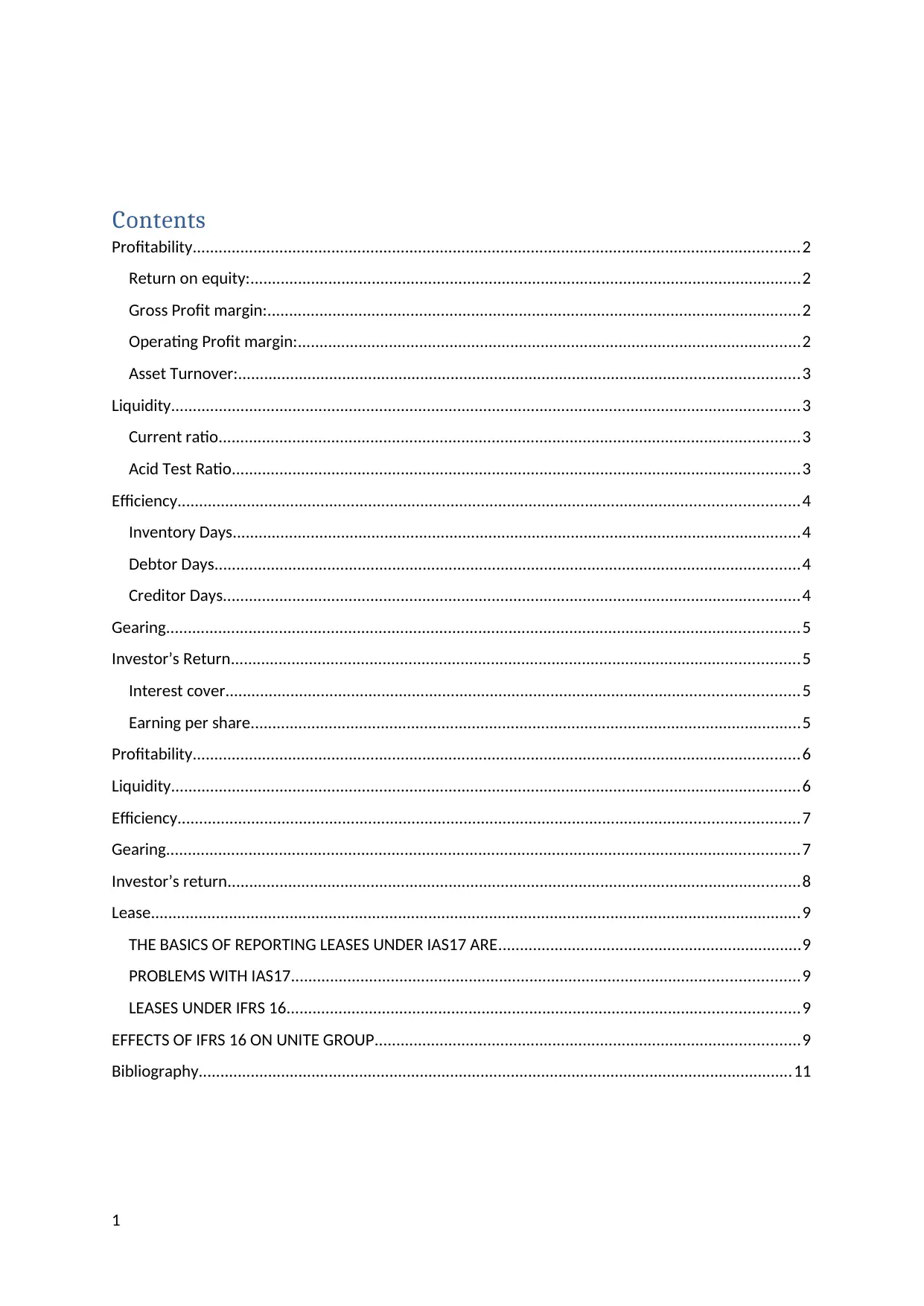

Contents

Profitability............................................................................................................................................2

Return on equity:...............................................................................................................................2

Gross Profit margin:...........................................................................................................................2

Operating Profit margin:....................................................................................................................2

Asset Turnover:.................................................................................................................................3

Liquidity.................................................................................................................................................3

Current ratio......................................................................................................................................3

Acid Test Ratio...................................................................................................................................3

Efficiency...............................................................................................................................................4

Inventory Days...................................................................................................................................4

Debtor Days.......................................................................................................................................4

Creditor Days.....................................................................................................................................4

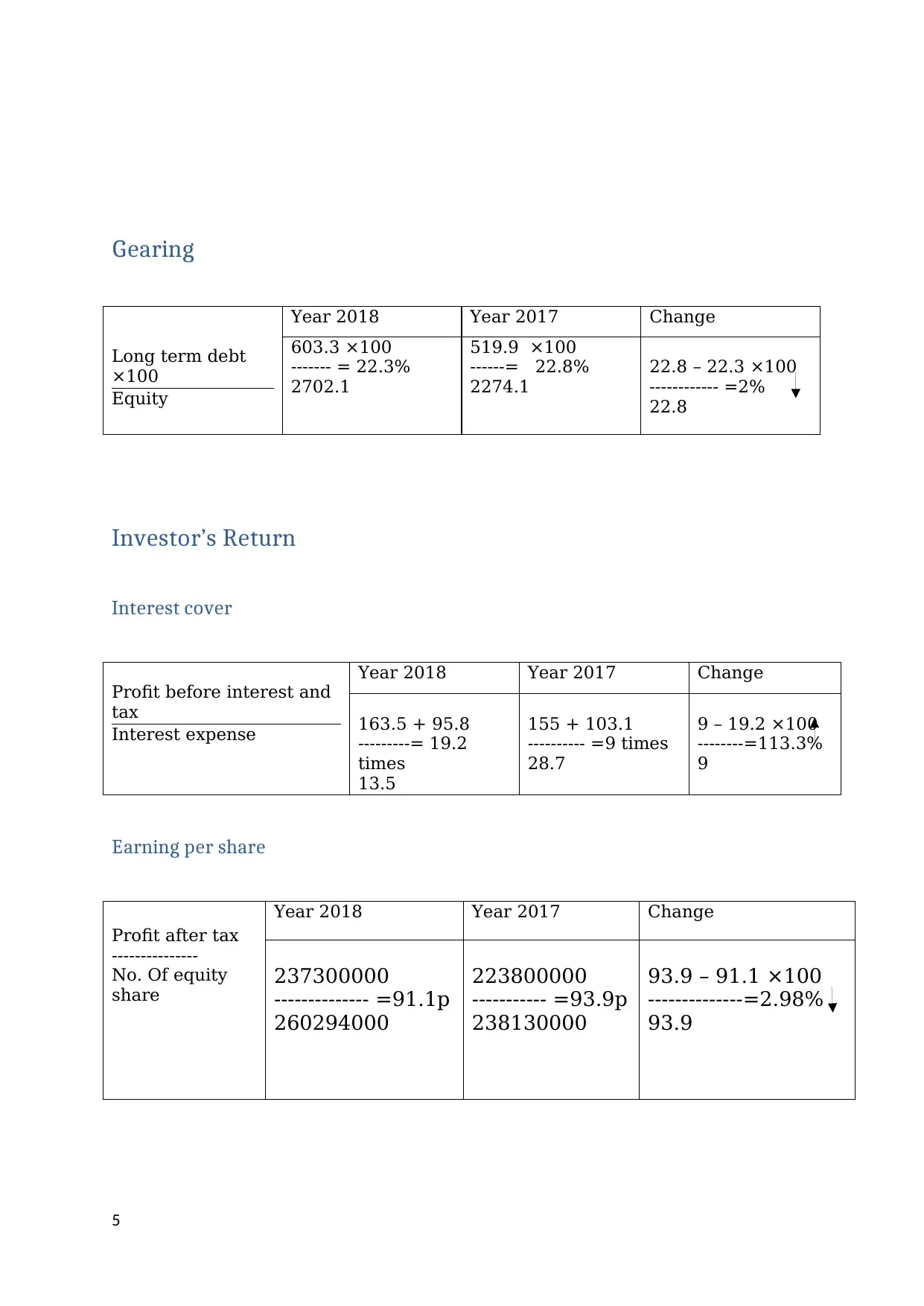

Gearing..................................................................................................................................................5

Investor’s Return...................................................................................................................................5

Interest cover....................................................................................................................................5

Earning per share...............................................................................................................................5

Profitability............................................................................................................................................6

Liquidity.................................................................................................................................................6

Efficiency...............................................................................................................................................7

Gearing..................................................................................................................................................7

Investor’s return....................................................................................................................................8

Lease......................................................................................................................................................9

THE BASICS OF REPORTING LEASES UNDER IAS17 ARE......................................................................9

PROBLEMS WITH IAS17.....................................................................................................................9

LEASES UNDER IFRS 16......................................................................................................................9

EFFECTS OF IFRS 16 ON UNITE GROUP..................................................................................................9

Bibliography.........................................................................................................................................11

1

Profitability............................................................................................................................................2

Return on equity:...............................................................................................................................2

Gross Profit margin:...........................................................................................................................2

Operating Profit margin:....................................................................................................................2

Asset Turnover:.................................................................................................................................3

Liquidity.................................................................................................................................................3

Current ratio......................................................................................................................................3

Acid Test Ratio...................................................................................................................................3

Efficiency...............................................................................................................................................4

Inventory Days...................................................................................................................................4

Debtor Days.......................................................................................................................................4

Creditor Days.....................................................................................................................................4

Gearing..................................................................................................................................................5

Investor’s Return...................................................................................................................................5

Interest cover....................................................................................................................................5

Earning per share...............................................................................................................................5

Profitability............................................................................................................................................6

Liquidity.................................................................................................................................................6

Efficiency...............................................................................................................................................7

Gearing..................................................................................................................................................7

Investor’s return....................................................................................................................................8

Lease......................................................................................................................................................9

THE BASICS OF REPORTING LEASES UNDER IAS17 ARE......................................................................9

PROBLEMS WITH IAS17.....................................................................................................................9

LEASES UNDER IFRS 16......................................................................................................................9

EFFECTS OF IFRS 16 ON UNITE GROUP..................................................................................................9

Bibliography.........................................................................................................................................11

1

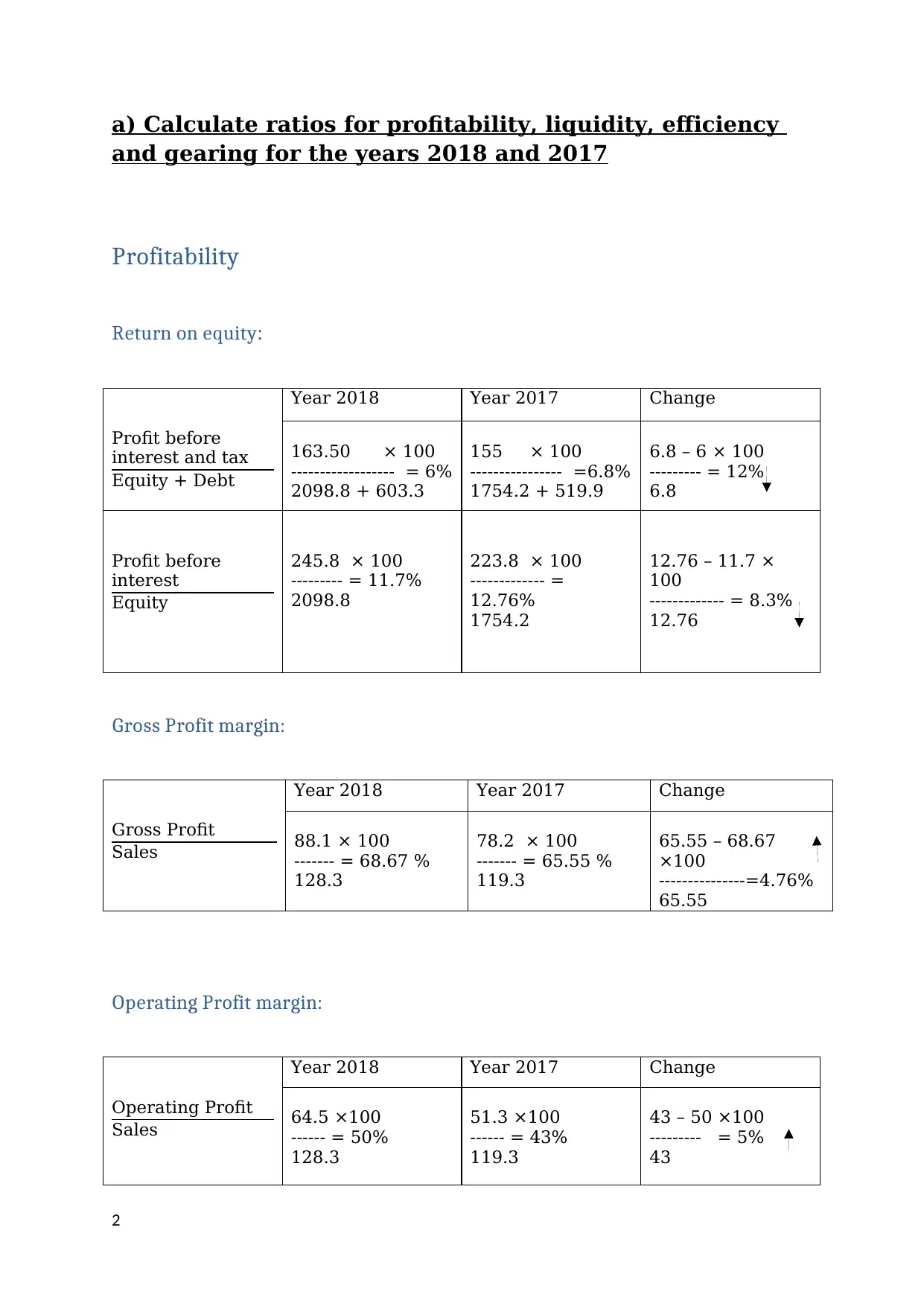

a) Calculate ratios for profitability, liquidity, efficiency

and gearing for the years 2018 and 2017

Profitability

Return on equity:

Profit before

interest and tax

Equity + Debt

Year 2018 Year 2017 Change

163.50 × 100

------------------ = 6%

2098.8 + 603.3

155 × 100

---------------- =6.8%

1754.2 + 519.9

6.8 – 6 × 100

--------- = 12%

6.8

Profit before

interest

Equity

245.8 × 100

--------- = 11.7%

2098.8

223.8 × 100

------------- =

12.76%

1754.2

12.76 – 11.7 ×

100

------------- = 8.3%

12.76

Gross Profit margin:

Gross Profit

Sales

Year 2018 Year 2017 Change

88.1 × 100

------- = 68.67 %

128.3

78.2 × 100

------- = 65.55 %

119.3

65.55 – 68.67

×100

---------------=4.76%

65.55

Operating Profit margin:

Operating Profit

Sales

Year 2018 Year 2017 Change

64.5 ×100

------ = 50%

128.3

51.3 ×100

------ = 43%

119.3

43 – 50 ×100

--------- = 5%

43

2

and gearing for the years 2018 and 2017

Profitability

Return on equity:

Profit before

interest and tax

Equity + Debt

Year 2018 Year 2017 Change

163.50 × 100

------------------ = 6%

2098.8 + 603.3

155 × 100

---------------- =6.8%

1754.2 + 519.9

6.8 – 6 × 100

--------- = 12%

6.8

Profit before

interest

Equity

245.8 × 100

--------- = 11.7%

2098.8

223.8 × 100

------------- =

12.76%

1754.2

12.76 – 11.7 ×

100

------------- = 8.3%

12.76

Gross Profit margin:

Gross Profit

Sales

Year 2018 Year 2017 Change

88.1 × 100

------- = 68.67 %

128.3

78.2 × 100

------- = 65.55 %

119.3

65.55 – 68.67

×100

---------------=4.76%

65.55

Operating Profit margin:

Operating Profit

Sales

Year 2018 Year 2017 Change

64.5 ×100

------ = 50%

128.3

51.3 ×100

------ = 43%

119.3

43 – 50 ×100

--------- = 5%

43

2

Asset Turnover:

Sales

Equity + Long

term debt

Year 2018 Year 2017 Change

128.3 ×100

---------- =

4.77%

2098.8 + 591.3

119.3 ×100

-------- = 5.27%

1754.2 + 511.5

5.27 – 4.77 ×100

------------ = 9.5 %

5.27

Liquidity

Current ratio

Current assets:

current liabilities

Year 2018 Year 2017 Change

220.80:147.4=

1.5:1

138.6:157.5=

0.88:1

0.88 – 1.5 ×100

----------- = 70%

0.88

Acid Test Ratio

Year 2018 Year 2017 Change

3

Sales

Equity + Long

term debt

Year 2018 Year 2017 Change

128.3 ×100

---------- =

4.77%

2098.8 + 591.3

119.3 ×100

-------- = 5.27%

1754.2 + 511.5

5.27 – 4.77 ×100

------------ = 9.5 %

5.27

Liquidity

Current ratio

Current assets:

current liabilities

Year 2018 Year 2017 Change

220.80:147.4=

1.5:1

138.6:157.5=

0.88:1

0.88 – 1.5 ×100

----------- = 70%

0.88

Acid Test Ratio

Year 2018 Year 2017 Change

3

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

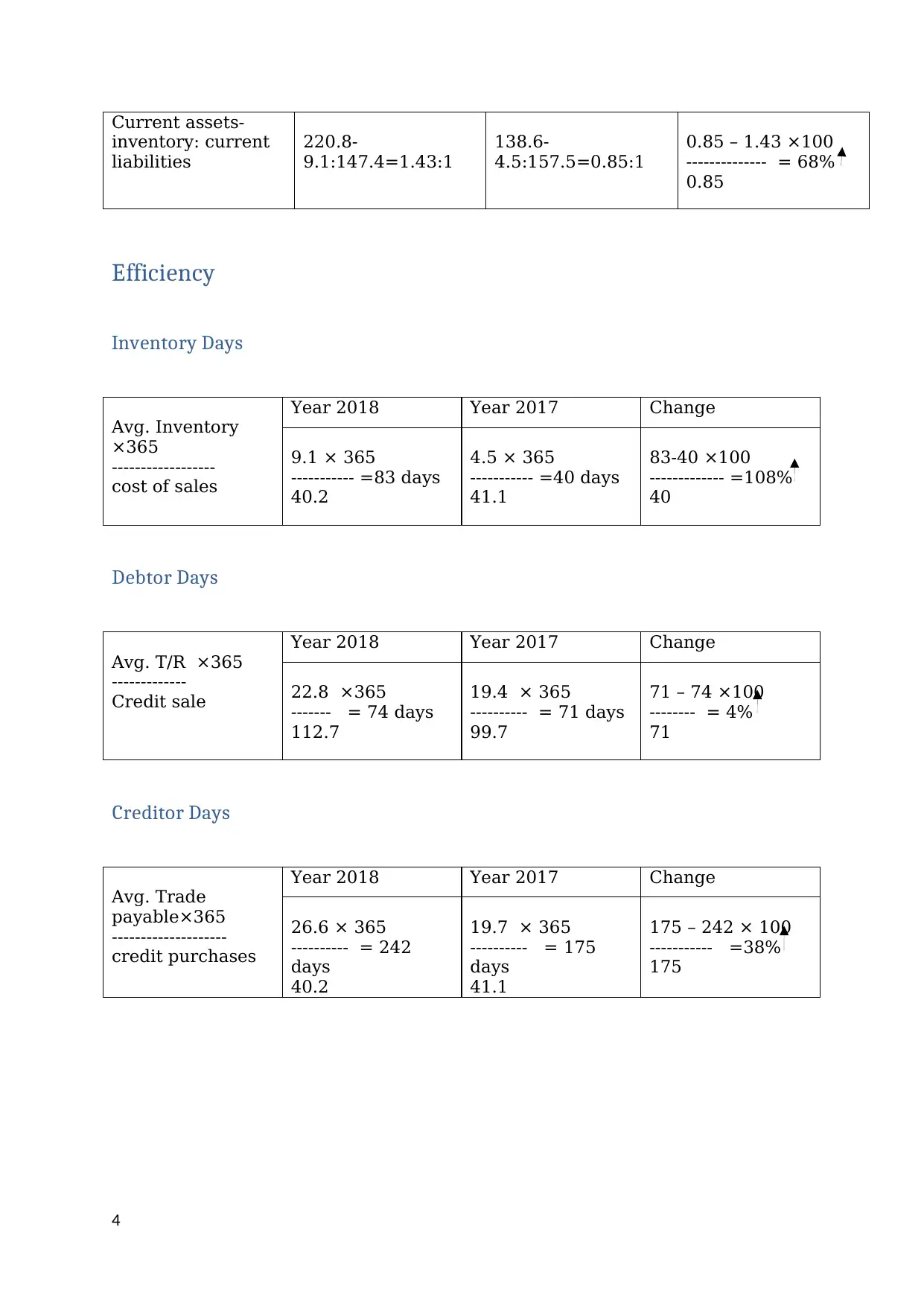

Current assets-

inventory: current

liabilities

220.8-

9.1:147.4=1.43:1

138.6-

4.5:157.5=0.85:1

0.85 – 1.43 ×100

-------------- = 68%

0.85

Efficiency

Inventory Days

Avg. Inventory

×365

------------------

cost of sales

Year 2018 Year 2017 Change

9.1 × 365

----------- =83 days

40.2

4.5 × 365

----------- =40 days

41.1

83-40 ×100

------------- =108%

40

Debtor Days

Avg. T/R ×365

-------------

Credit sale

Year 2018 Year 2017 Change

22.8 ×365

------- = 74 days

112.7

19.4 × 365

---------- = 71 days

99.7

71 – 74 ×100

-------- = 4%

71

Creditor Days

Avg. Trade

payable×365

--------------------

credit purchases

Year 2018 Year 2017 Change

26.6 × 365

---------- = 242

days

40.2

19.7 × 365

---------- = 175

days

41.1

175 – 242 × 100

----------- =38%

175

4

inventory: current

liabilities

220.8-

9.1:147.4=1.43:1

138.6-

4.5:157.5=0.85:1

0.85 – 1.43 ×100

-------------- = 68%

0.85

Efficiency

Inventory Days

Avg. Inventory

×365

------------------

cost of sales

Year 2018 Year 2017 Change

9.1 × 365

----------- =83 days

40.2

4.5 × 365

----------- =40 days

41.1

83-40 ×100

------------- =108%

40

Debtor Days

Avg. T/R ×365

-------------

Credit sale

Year 2018 Year 2017 Change

22.8 ×365

------- = 74 days

112.7

19.4 × 365

---------- = 71 days

99.7

71 – 74 ×100

-------- = 4%

71

Creditor Days

Avg. Trade

payable×365

--------------------

credit purchases

Year 2018 Year 2017 Change

26.6 × 365

---------- = 242

days

40.2

19.7 × 365

---------- = 175

days

41.1

175 – 242 × 100

----------- =38%

175

4

Gearing

Long term debt

×100

Equity

Year 2018 Year 2017 Change

603.3 ×100

------- = 22.3%

2702.1

519.9 ×100

------= 22.8%

2274.1

22.8 – 22.3 ×100

------------ =2%

22.8

Investor’s Return

Interest cover

Profit before interest and

tax

Interest expense

Year 2018 Year 2017 Change

163.5 + 95.8

---------= 19.2

times

13.5

155 + 103.1

---------- =9 times

28.7

9 – 19.2 ×100

--------=113.3%

9

Earning per share

Profit after tax

---------------

No. Of equity

share

Year 2018 Year 2017 Change

237300000

-------------- =91.1p

260294000

223800000

----------- =93.9p

238130000

93.9 – 91.1 ×100

--------------=2.98%

93.9

5

Long term debt

×100

Equity

Year 2018 Year 2017 Change

603.3 ×100

------- = 22.3%

2702.1

519.9 ×100

------= 22.8%

2274.1

22.8 – 22.3 ×100

------------ =2%

22.8

Investor’s Return

Interest cover

Profit before interest and

tax

Interest expense

Year 2018 Year 2017 Change

163.5 + 95.8

---------= 19.2

times

13.5

155 + 103.1

---------- =9 times

28.7

9 – 19.2 ×100

--------=113.3%

9

Earning per share

Profit after tax

---------------

No. Of equity

share

Year 2018 Year 2017 Change

237300000

-------------- =91.1p

260294000

223800000

----------- =93.9p

238130000

93.9 – 91.1 ×100

--------------=2.98%

93.9

5

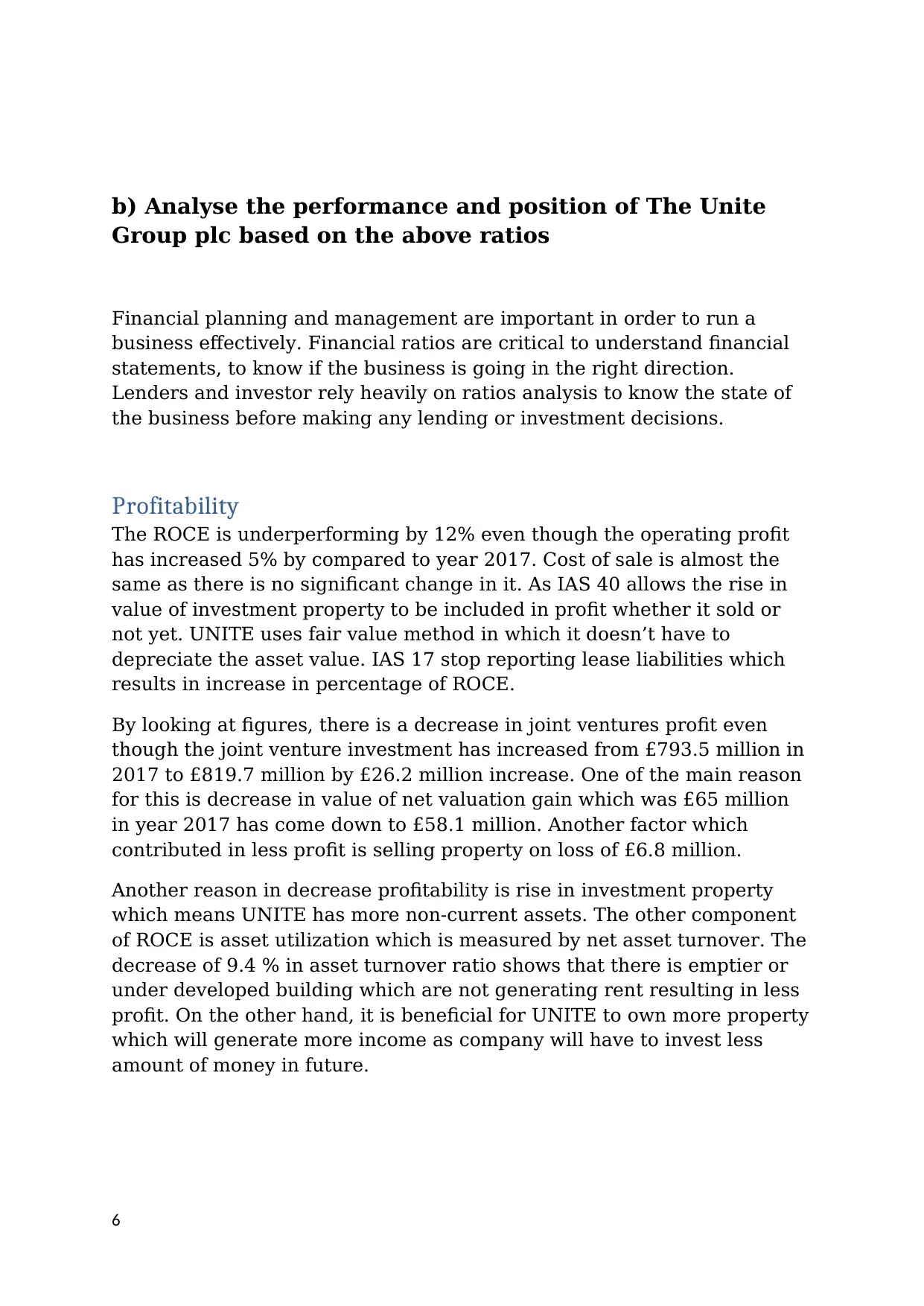

b) Analyse the performance and position of The Unite

Group plc based on the above ratios

Financial planning and management are important in order to run a

business effectively. Financial ratios are critical to understand financial

statements, to know if the business is going in the right direction.

Lenders and investor rely heavily on ratios analysis to know the state of

the business before making any lending or investment decisions.

Profitability

The ROCE is underperforming by 12% even though the operating profit

has increased 5% by compared to year 2017. Cost of sale is almost the

same as there is no significant change in it. As IAS 40 allows the rise in

value of investment property to be included in profit whether it sold or

not yet. UNITE uses fair value method in which it doesn’t have to

depreciate the asset value. IAS 17 stop reporting lease liabilities which

results in increase in percentage of ROCE.

By looking at figures, there is a decrease in joint ventures profit even

though the joint venture investment has increased from £793.5 million in

2017 to £819.7 million by £26.2 million increase. One of the main reason

for this is decrease in value of net valuation gain which was £65 million

in year 2017 has come down to £58.1 million. Another factor which

contributed in less profit is selling property on loss of £6.8 million.

Another reason in decrease profitability is rise in investment property

which means UNITE has more non-current assets. The other component

of ROCE is asset utilization which is measured by net asset turnover. The

decrease of 9.4 % in asset turnover ratio shows that there is emptier or

under developed building which are not generating rent resulting in less

profit. On the other hand, it is beneficial for UNITE to own more property

which will generate more income as company will have to invest less

amount of money in future.

6

Group plc based on the above ratios

Financial planning and management are important in order to run a

business effectively. Financial ratios are critical to understand financial

statements, to know if the business is going in the right direction.

Lenders and investor rely heavily on ratios analysis to know the state of

the business before making any lending or investment decisions.

Profitability

The ROCE is underperforming by 12% even though the operating profit

has increased 5% by compared to year 2017. Cost of sale is almost the

same as there is no significant change in it. As IAS 40 allows the rise in

value of investment property to be included in profit whether it sold or

not yet. UNITE uses fair value method in which it doesn’t have to

depreciate the asset value. IAS 17 stop reporting lease liabilities which

results in increase in percentage of ROCE.

By looking at figures, there is a decrease in joint ventures profit even

though the joint venture investment has increased from £793.5 million in

2017 to £819.7 million by £26.2 million increase. One of the main reason

for this is decrease in value of net valuation gain which was £65 million

in year 2017 has come down to £58.1 million. Another factor which

contributed in less profit is selling property on loss of £6.8 million.

Another reason in decrease profitability is rise in investment property

which means UNITE has more non-current assets. The other component

of ROCE is asset utilization which is measured by net asset turnover. The

decrease of 9.4 % in asset turnover ratio shows that there is emptier or

under developed building which are not generating rent resulting in less

profit. On the other hand, it is beneficial for UNITE to own more property

which will generate more income as company will have to invest less

amount of money in future.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Liquidity

UNITE group has a higher level of cover for its current liabilities. It

current ratio for year 2018 is 1.5:1 compared to 2017 0.88:1 increased

about 70% which mean it has more cash available to cover its current

liabilities. Its cash deposit is £123.6 million compared to £51.2 million.

This has helped by a successful rights issue.

Liquidity ratios decrease primarily due to additional current liabilities

that from lease accounting under IFRS 16 (IAS17) and Employee benefits

under IAS 19. UNITE group use DEFINED CONTRIBUTION PENSION

SCHEME which results in higher finance cost but no pension cost in its

balance sheet.

Some of this rights issue appear to have been used to reduce the bank

loan. It has put more money aside to clear the outstanding debts

resulting in decrease in trade payable which is good for investor point of

view. The increase in the cash at bank helped by successful rights issue

increase of 5.7 % which is a sign of shareholders support and confidence

in the future.

Efficiency

As UNITE Group has relatively low inventory levels this means it must

also have relatively low levels of trade payables which can confirm the

creditor ratios. UNITE has apayable period of 242 days is a clear

indication of supplier being generous with the credit period they extend

to UNITE group.

Efficiency ratios in UNITE tells the management team is effective in

using the minimum amount of assets in relation to a given amount of

sales. These ratios don’t always give a clear picture of the business. A

low rate of creditor’s turnover could be related to deliberate payment

delays which could affect its credit reputation. Desire to achieve higher

asset ratio could make the management to reduce the required

investment in fixed assets purchase.

7

UNITE group has a higher level of cover for its current liabilities. It

current ratio for year 2018 is 1.5:1 compared to 2017 0.88:1 increased

about 70% which mean it has more cash available to cover its current

liabilities. Its cash deposit is £123.6 million compared to £51.2 million.

This has helped by a successful rights issue.

Liquidity ratios decrease primarily due to additional current liabilities

that from lease accounting under IFRS 16 (IAS17) and Employee benefits

under IAS 19. UNITE group use DEFINED CONTRIBUTION PENSION

SCHEME which results in higher finance cost but no pension cost in its

balance sheet.

Some of this rights issue appear to have been used to reduce the bank

loan. It has put more money aside to clear the outstanding debts

resulting in decrease in trade payable which is good for investor point of

view. The increase in the cash at bank helped by successful rights issue

increase of 5.7 % which is a sign of shareholders support and confidence

in the future.

Efficiency

As UNITE Group has relatively low inventory levels this means it must

also have relatively low levels of trade payables which can confirm the

creditor ratios. UNITE has apayable period of 242 days is a clear

indication of supplier being generous with the credit period they extend

to UNITE group.

Efficiency ratios in UNITE tells the management team is effective in

using the minimum amount of assets in relation to a given amount of

sales. These ratios don’t always give a clear picture of the business. A

low rate of creditor’s turnover could be related to deliberate payment

delays which could affect its credit reputation. Desire to achieve higher

asset ratio could make the management to reduce the required

investment in fixed assets purchase.

7

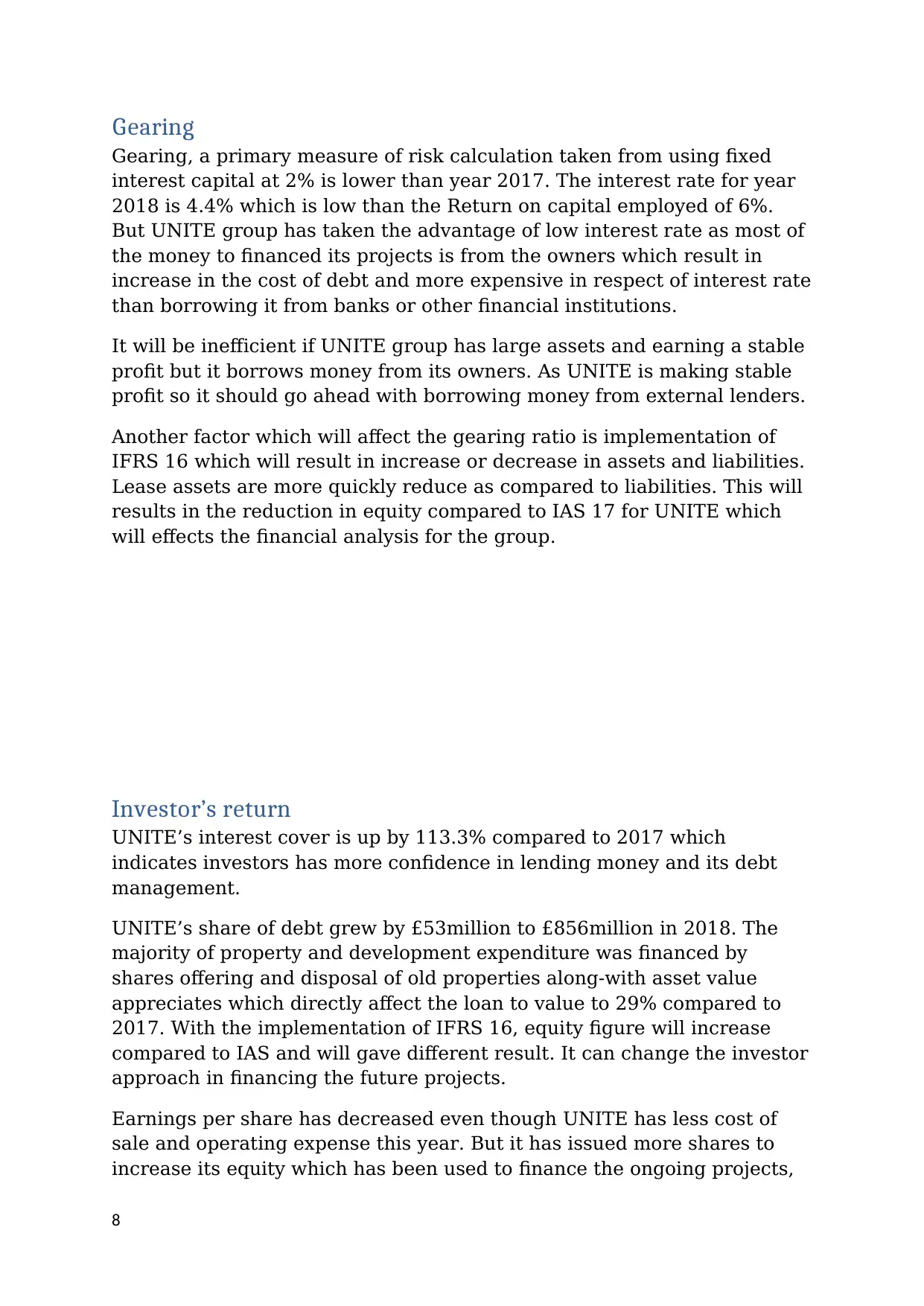

Gearing

Gearing, a primary measure of risk calculation taken from using fixed

interest capital at 2% is lower than year 2017. The interest rate for year

2018 is 4.4% which is low than the Return on capital employed of 6%.

But UNITE group has taken the advantage of low interest rate as most of

the money to financed its projects is from the owners which result in

increase in the cost of debt and more expensive in respect of interest rate

than borrowing it from banks or other financial institutions.

It will be inefficient if UNITE group has large assets and earning a stable

profit but it borrows money from its owners. As UNITE is making stable

profit so it should go ahead with borrowing money from external lenders.

Another factor which will affect the gearing ratio is implementation of

IFRS 16 which will result in increase or decrease in assets and liabilities.

Lease assets are more quickly reduce as compared to liabilities. This will

results in the reduction in equity compared to IAS 17 for UNITE which

will effects the financial analysis for the group.

Investor’s return

UNITE’s interest cover is up by 113.3% compared to 2017 which

indicates investors has more confidence in lending money and its debt

management.

UNITE’s share of debt grew by £53million to £856million in 2018. The

majority of property and development expenditure was financed by

shares offering and disposal of old properties along-with asset value

appreciates which directly affect the loan to value to 29% compared to

2017. With the implementation of IFRS 16, equity figure will increase

compared to IAS and will gave different result. It can change the investor

approach in financing the future projects.

Earnings per share has decreased even though UNITE has less cost of

sale and operating expense this year. But it has issued more shares to

increase its equity which has been used to finance the ongoing projects,

8

Gearing, a primary measure of risk calculation taken from using fixed

interest capital at 2% is lower than year 2017. The interest rate for year

2018 is 4.4% which is low than the Return on capital employed of 6%.

But UNITE group has taken the advantage of low interest rate as most of

the money to financed its projects is from the owners which result in

increase in the cost of debt and more expensive in respect of interest rate

than borrowing it from banks or other financial institutions.

It will be inefficient if UNITE group has large assets and earning a stable

profit but it borrows money from its owners. As UNITE is making stable

profit so it should go ahead with borrowing money from external lenders.

Another factor which will affect the gearing ratio is implementation of

IFRS 16 which will result in increase or decrease in assets and liabilities.

Lease assets are more quickly reduce as compared to liabilities. This will

results in the reduction in equity compared to IAS 17 for UNITE which

will effects the financial analysis for the group.

Investor’s return

UNITE’s interest cover is up by 113.3% compared to 2017 which

indicates investors has more confidence in lending money and its debt

management.

UNITE’s share of debt grew by £53million to £856million in 2018. The

majority of property and development expenditure was financed by

shares offering and disposal of old properties along-with asset value

appreciates which directly affect the loan to value to 29% compared to

2017. With the implementation of IFRS 16, equity figure will increase

compared to IAS and will gave different result. It can change the investor

approach in financing the future projects.

Earnings per share has decreased even though UNITE has less cost of

sale and operating expense this year. But it has issued more shares to

increase its equity which has been used to finance the ongoing projects,

8

most of its projects are still in pipeline which will increase its revenue in

coming years.

Based on the company development pipeline and existing properties, it is

believed the firm has the potential to pay out 34.1p per share in

dividends this year, giving a potential dividend yield of 3.2%.(Elliot and

Elliot, 2007)

c)Analysing the changes in lease accounting rules from

IAS 17 to IFRS 16 leases

Lease

A lease involves one party (lessee) obtaining the use of an asset from a

supplier (lessor). The asset is not paid fully but rather it is agreed to pay

the supplier in the future via instalment.

There are two different types of lease agreements. In FINANCE lease, all

major risks and rewards are transferred to the lessee. The payments

normally last the length of the useful life of an asset, thus no one else will

get to use the asset. Lessee can gain legal ownership of an asset at the

end of lease.

In OPERATING lease, lessor retain the legal ownership and risks and

reward of asset. At the end of the lease the asset is handed back to the

lessor.

9

coming years.

Based on the company development pipeline and existing properties, it is

believed the firm has the potential to pay out 34.1p per share in

dividends this year, giving a potential dividend yield of 3.2%.(Elliot and

Elliot, 2007)

c)Analysing the changes in lease accounting rules from

IAS 17 to IFRS 16 leases

Lease

A lease involves one party (lessee) obtaining the use of an asset from a

supplier (lessor). The asset is not paid fully but rather it is agreed to pay

the supplier in the future via instalment.

There are two different types of lease agreements. In FINANCE lease, all

major risks and rewards are transferred to the lessee. The payments

normally last the length of the useful life of an asset, thus no one else will

get to use the asset. Lessee can gain legal ownership of an asset at the

end of lease.

In OPERATING lease, lessor retain the legal ownership and risks and

reward of asset. At the end of the lease the asset is handed back to the

lessor.

9

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

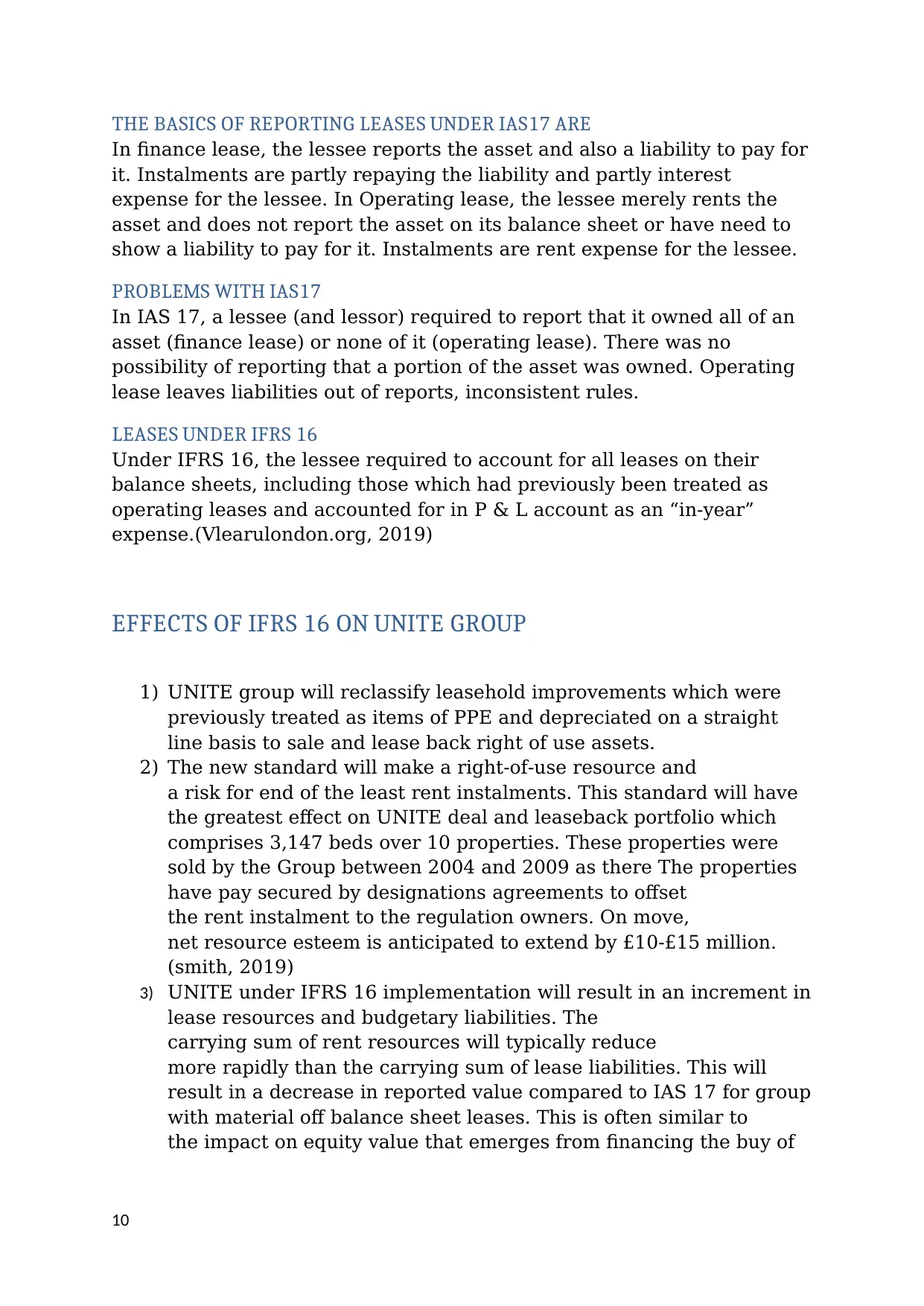

THE BASICS OF REPORTING LEASES UNDER IAS17 ARE

In finance lease, the lessee reports the asset and also a liability to pay for

it. Instalments are partly repaying the liability and partly interest

expense for the lessee. In Operating lease, the lessee merely rents the

asset and does not report the asset on its balance sheet or have need to

show a liability to pay for it. Instalments are rent expense for the lessee.

PROBLEMS WITH IAS17

In IAS 17, a lessee (and lessor) required to report that it owned all of an

asset (finance lease) or none of it (operating lease). There was no

possibility of reporting that a portion of the asset was owned. Operating

lease leaves liabilities out of reports, inconsistent rules.

LEASES UNDER IFRS 16

Under IFRS 16, the lessee required to account for all leases on their

balance sheets, including those which had previously been treated as

operating leases and accounted for in P & L account as an “in-year”

expense.(Vlearulondon.org, 2019)

EFFECTS OF IFRS 16 ON UNITE GROUP

1) UNITE group will reclassify leasehold improvements which were

previously treated as items of PPE and depreciated on a straight

line basis to sale and lease back right of use assets.

2) The new standard will make a right-of-use resource and

a risk for end of the least rent instalments. This standard will have

the greatest effect on UNITE deal and leaseback portfolio which

comprises 3,147 beds over 10 properties. These properties were

sold by the Group between 2004 and 2009 as there The properties

have pay secured by designations agreements to offset

the rent instalment to the regulation owners. On move,

net resource esteem is anticipated to extend by £10-£15 million.

(smith, 2019)

3) UNITE under IFRS 16 implementation will result in an increment in

lease resources and budgetary liabilities. The

carrying sum of rent resources will typically reduce

more rapidly than the carrying sum of lease liabilities. This will

result in a decrease in reported value compared to IAS 17 for group

with material off balance sheet leases. This is often similar to

the impact on equity value that emerges from financing the buy of

10

In finance lease, the lessee reports the asset and also a liability to pay for

it. Instalments are partly repaying the liability and partly interest

expense for the lessee. In Operating lease, the lessee merely rents the

asset and does not report the asset on its balance sheet or have need to

show a liability to pay for it. Instalments are rent expense for the lessee.

PROBLEMS WITH IAS17

In IAS 17, a lessee (and lessor) required to report that it owned all of an

asset (finance lease) or none of it (operating lease). There was no

possibility of reporting that a portion of the asset was owned. Operating

lease leaves liabilities out of reports, inconsistent rules.

LEASES UNDER IFRS 16

Under IFRS 16, the lessee required to account for all leases on their

balance sheets, including those which had previously been treated as

operating leases and accounted for in P & L account as an “in-year”

expense.(Vlearulondon.org, 2019)

EFFECTS OF IFRS 16 ON UNITE GROUP

1) UNITE group will reclassify leasehold improvements which were

previously treated as items of PPE and depreciated on a straight

line basis to sale and lease back right of use assets.

2) The new standard will make a right-of-use resource and

a risk for end of the least rent instalments. This standard will have

the greatest effect on UNITE deal and leaseback portfolio which

comprises 3,147 beds over 10 properties. These properties were

sold by the Group between 2004 and 2009 as there The properties

have pay secured by designations agreements to offset

the rent instalment to the regulation owners. On move,

net resource esteem is anticipated to extend by £10-£15 million.

(smith, 2019)

3) UNITE under IFRS 16 implementation will result in an increment in

lease resources and budgetary liabilities. The

carrying sum of rent resources will typically reduce

more rapidly than the carrying sum of lease liabilities. This will

result in a decrease in reported value compared to IAS 17 for group

with material off balance sheet leases. This is often similar to

the impact on equity value that emerges from financing the buy of

10

an asset, either through a former on balance sheet lease or a credit.

(IFRS, 2016)

4) Profit measures before interest and tax, such as EBIT or operating

profit, will also increase applying IFRS 16. This is because those

measures applying IFRS 16 exclude interest on lease liabilities

whereas, applying IAS 17, they included the entire expense related

to off balance sheet leases.

5) For UNITE Group that has material off balance sheet leases, IFRS

16 is anticipated to result in higher profit

before interest (for example, operating profit) compared to

the sums detailed applying IAS 17. This is because, applying IFRS

16, a company presents the certain interest in rent instalments for

former off balance sheet leases as portion of finance costs. On the

other hand, applying IAS 17, the whole cost related to

off balance sheet leases was included as portion of operating

expenses. The measure of the increase in operating profit, and

finance costs, depends on the importance of leasing to the

company, the length of its leases and the discount rates applied.

(IFRS, 2016)

6) Unlike IAS 17, for all leases (counting previous off balance sheet

leases), IFRS 16 requires a company to

recognise interest on lease liabilities separately from depreciation

of rent assets. A company is expected

to show interest cost as portion of finance costs,

and depreciation within a same line item to that in which it

presents depreciation of property, plant and equipment. Applying

IAS 17, lease instalments for off balance sheet leases

were generally presented within operating expenses.

Bibliography

1. Elliot, B. and Elliot, J. (2007). Financial Accounting and Reporting.

[online] Primo.anglia.ac.uk. Available at:

11

(IFRS, 2016)

4) Profit measures before interest and tax, such as EBIT or operating

profit, will also increase applying IFRS 16. This is because those

measures applying IFRS 16 exclude interest on lease liabilities

whereas, applying IAS 17, they included the entire expense related

to off balance sheet leases.

5) For UNITE Group that has material off balance sheet leases, IFRS

16 is anticipated to result in higher profit

before interest (for example, operating profit) compared to

the sums detailed applying IAS 17. This is because, applying IFRS

16, a company presents the certain interest in rent instalments for

former off balance sheet leases as portion of finance costs. On the

other hand, applying IAS 17, the whole cost related to

off balance sheet leases was included as portion of operating

expenses. The measure of the increase in operating profit, and

finance costs, depends on the importance of leasing to the

company, the length of its leases and the discount rates applied.

(IFRS, 2016)

6) Unlike IAS 17, for all leases (counting previous off balance sheet

leases), IFRS 16 requires a company to

recognise interest on lease liabilities separately from depreciation

of rent assets. A company is expected

to show interest cost as portion of finance costs,

and depreciation within a same line item to that in which it

presents depreciation of property, plant and equipment. Applying

IAS 17, lease instalments for off balance sheet leases

were generally presented within operating expenses.

Bibliography

1. Elliot, B. and Elliot, J. (2007). Financial Accounting and Reporting.

[online] Primo.anglia.ac.uk. Available at:

11

https://primo.anglia.ac.uk/primo-explore/fulldisplay?

docid=TN_proquest838989787&context=PC&vid=ANG_VU1&lang

=en_US&search_scope=CSCOP_APU_DEEP&adaptor=primo_centr

al_multiple_fe&tab=default_tab&query=sub,contains,Financial

%20Reporting,AND&sortby=rank&mode=advanced&pfilter=pfilter

,exact,books,AND&offset=0 [Accessed 18 Oct. 2019].

2. The Accounting Entity, Relevance, and Faithful Representation:

Linking Financial Statement Notes to the FASB and IASB

Conceptual Frameworks, Issues in Accounting Education, Nov

2013, Vol.28,issue 4,pg 1009 -1029

3. Unite-group.co.uk. (2018). Annual Report 2018 | Unite Group.

[online] Available at:

http://www.unite-group.co.uk/investors/annual-report-2018

[Accessed 11 Oct. 2019].

4. Anon, (2016). IFRS 16, Effects analysis. [online] Available at:

https://vlearulondon.org/pluginfile.php/97657/mod_resource/conten

t/1/ifrs16-effects-analysis.pdf [Accessed 22 Oct. 2019].

5. smith, R. (2019). [online] Unite-group.co.uk. Available at:

http://www.unite-group.co.uk/sites/default/files/2019-02/Preliminar

y-Financial-Results-Statement-2018.pdf [Accessed 25 Oct. 2019].

6. Vlearulondon.org. (2019). Anglia Ruskin University London: Log in

to the site. [online] Available at:

https://vlearulondon.org/course/view.php?id=927 [Accessed 15 Oct.

2019].

12

docid=TN_proquest838989787&context=PC&vid=ANG_VU1&lang

=en_US&search_scope=CSCOP_APU_DEEP&adaptor=primo_centr

al_multiple_fe&tab=default_tab&query=sub,contains,Financial

%20Reporting,AND&sortby=rank&mode=advanced&pfilter=pfilter

,exact,books,AND&offset=0 [Accessed 18 Oct. 2019].

2. The Accounting Entity, Relevance, and Faithful Representation:

Linking Financial Statement Notes to the FASB and IASB

Conceptual Frameworks, Issues in Accounting Education, Nov

2013, Vol.28,issue 4,pg 1009 -1029

3. Unite-group.co.uk. (2018). Annual Report 2018 | Unite Group.

[online] Available at:

http://www.unite-group.co.uk/investors/annual-report-2018

[Accessed 11 Oct. 2019].

4. Anon, (2016). IFRS 16, Effects analysis. [online] Available at:

https://vlearulondon.org/pluginfile.php/97657/mod_resource/conten

t/1/ifrs16-effects-analysis.pdf [Accessed 22 Oct. 2019].

5. smith, R. (2019). [online] Unite-group.co.uk. Available at:

http://www.unite-group.co.uk/sites/default/files/2019-02/Preliminar

y-Financial-Results-Statement-2018.pdf [Accessed 25 Oct. 2019].

6. Vlearulondon.org. (2019). Anglia Ruskin University London: Log in

to the site. [online] Available at:

https://vlearulondon.org/course/view.php?id=927 [Accessed 15 Oct.

2019].

12

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.