Comprehensive Financial Analysis of Unite Group plc for 2018

VerifiedAdded on 2023/01/19

|9

|1999

|28

Report

AI Summary

This report presents a detailed financial analysis of Unite Group plc for the year ended December 2018. It begins with the calculation of various financial ratios, including profitability (return on capital employed, return on equity, gross profit margin, operating profit margin, and asset turnover), liqui...

FINANCIAL REPORTING FOR

BUSINESSES

BUSINESSES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTIONS...................................................................................................................................1

a) Calculation of profitability, liquidity, efficiency and gearing ratio for the year ended

December, 2018 of Unite Group plc............................................................................................1

b) Analysis of the performance and position of Unite Group plc on the basis of above

calculations..................................................................................................................................2

C) Analysis of change in lease accounting rules from IAS 17 Leases to IFRS 16 Leases.........5

REFERENCES................................................................................................................................7

QUESTIONS...................................................................................................................................1

a) Calculation of profitability, liquidity, efficiency and gearing ratio for the year ended

December, 2018 of Unite Group plc............................................................................................1

b) Analysis of the performance and position of Unite Group plc on the basis of above

calculations..................................................................................................................................2

C) Analysis of change in lease accounting rules from IAS 17 Leases to IFRS 16 Leases.........5

REFERENCES................................................................................................................................7

QUESTIONS

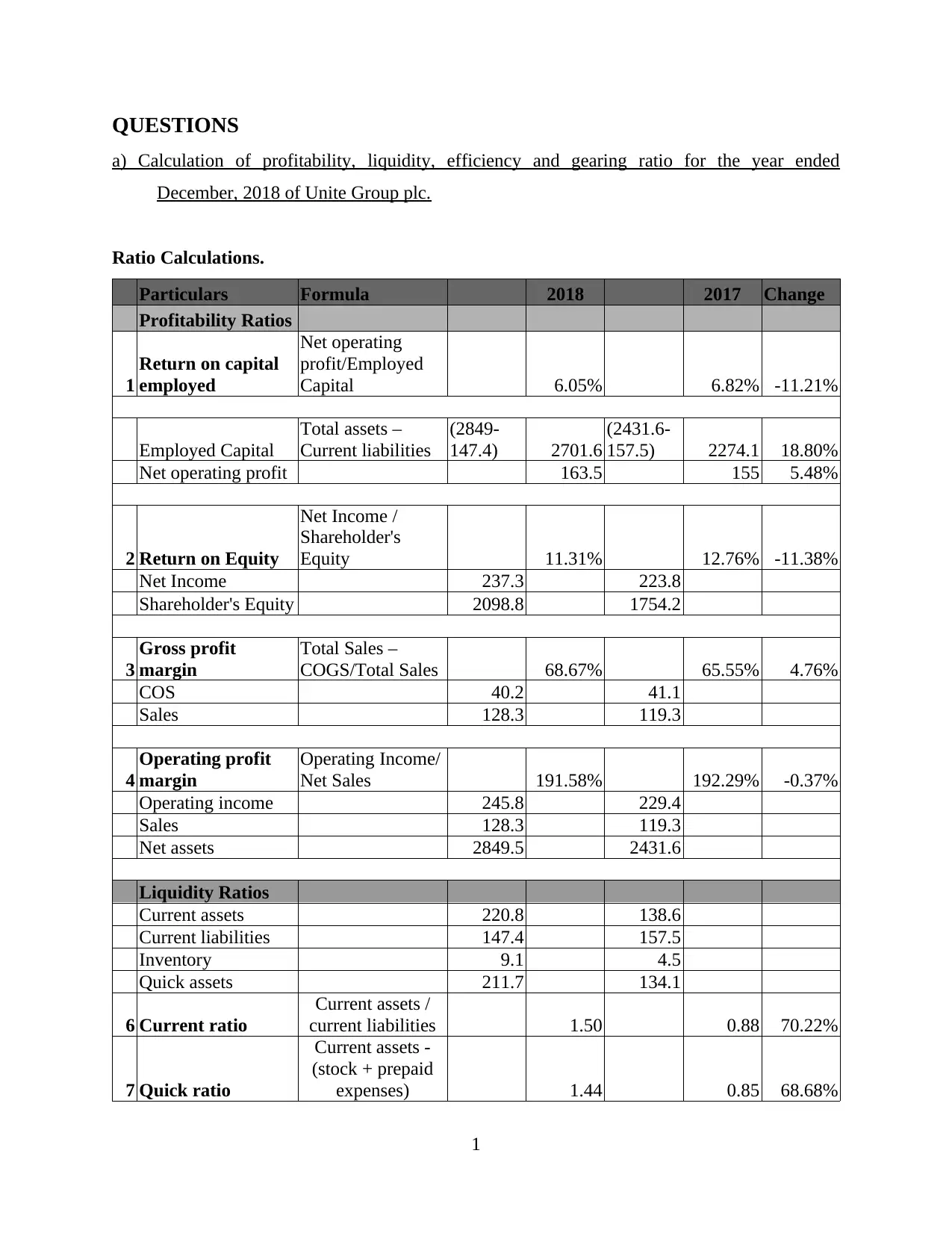

a) Calculation of profitability, liquidity, efficiency and gearing ratio for the year ended

December, 2018 of Unite Group plc.

Ratio Calculations.

Particulars Formula 2018 2017 Change

Profitability Ratios

1

Return on capital

employed

Net operating

profit/Employed

Capital 6.05% 6.82% -11.21%

Employed Capital

Total assets –

Current liabilities

(2849-

147.4) 2701.6

(2431.6-

157.5) 2274.1 18.80%

Net operating profit 163.5 155 5.48%

2 Return on Equity

Net Income /

Shareholder's

Equity 11.31% 12.76% -11.38%

Net Income 237.3 223.8

Shareholder's Equity 2098.8 1754.2

3

Gross profit

margin

Total Sales –

COGS/Total Sales 68.67% 65.55% 4.76%

COS 40.2 41.1

Sales 128.3 119.3

4

Operating profit

margin

Operating Income/

Net Sales 191.58% 192.29% -0.37%

Operating income 245.8 229.4

Sales 128.3 119.3

Net assets 2849.5 2431.6

Liquidity Ratios

Current assets 220.8 138.6

Current liabilities 147.4 157.5

Inventory 9.1 4.5

Quick assets 211.7 134.1

6 Current ratio

Current assets /

current liabilities 1.50 0.88 70.22%

7 Quick ratio

Current assets -

(stock + prepaid

expenses) 1.44 0.85 68.68%

1

a) Calculation of profitability, liquidity, efficiency and gearing ratio for the year ended

December, 2018 of Unite Group plc.

Ratio Calculations.

Particulars Formula 2018 2017 Change

Profitability Ratios

1

Return on capital

employed

Net operating

profit/Employed

Capital 6.05% 6.82% -11.21%

Employed Capital

Total assets –

Current liabilities

(2849-

147.4) 2701.6

(2431.6-

157.5) 2274.1 18.80%

Net operating profit 163.5 155 5.48%

2 Return on Equity

Net Income /

Shareholder's

Equity 11.31% 12.76% -11.38%

Net Income 237.3 223.8

Shareholder's Equity 2098.8 1754.2

3

Gross profit

margin

Total Sales –

COGS/Total Sales 68.67% 65.55% 4.76%

COS 40.2 41.1

Sales 128.3 119.3

4

Operating profit

margin

Operating Income/

Net Sales 191.58% 192.29% -0.37%

Operating income 245.8 229.4

Sales 128.3 119.3

Net assets 2849.5 2431.6

Liquidity Ratios

Current assets 220.8 138.6

Current liabilities 147.4 157.5

Inventory 9.1 4.5

Quick assets 211.7 134.1

6 Current ratio

Current assets /

current liabilities 1.50 0.88 70.22%

7 Quick ratio

Current assets -

(stock + prepaid

expenses) 1.44 0.85 68.68%

1

You're viewing a preview

Unlock full access by subscribing today!

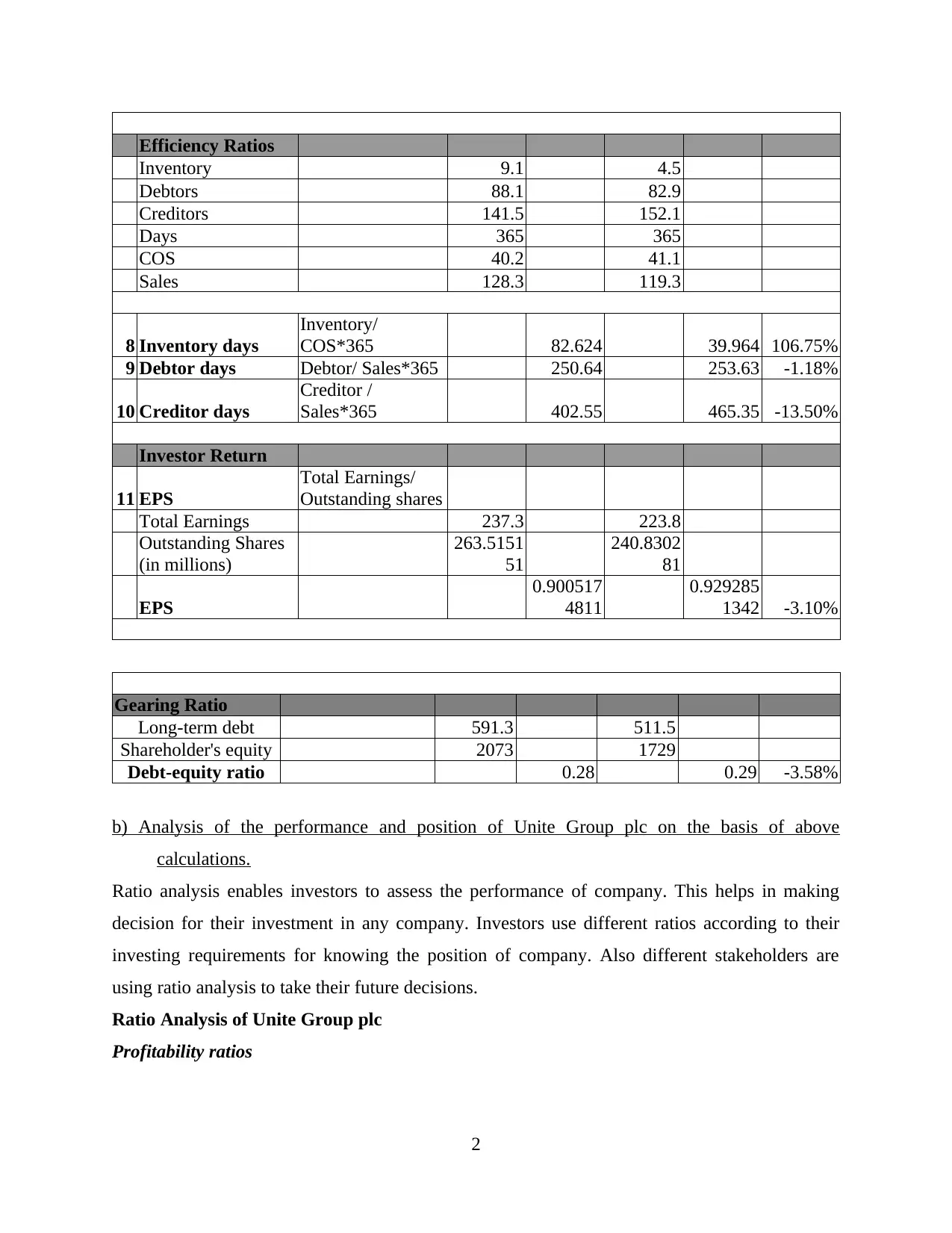

Efficiency Ratios

Inventory 9.1 4.5

Debtors 88.1 82.9

Creditors 141.5 152.1

Days 365 365

COS 40.2 41.1

Sales 128.3 119.3

8 Inventory days

Inventory/

COS*365 82.624 39.964 106.75%

9 Debtor days Debtor/ Sales*365 250.64 253.63 -1.18%

10 Creditor days

Creditor /

Sales*365 402.55 465.35 -13.50%

Investor Return

11 EPS

Total Earnings/

Outstanding shares

Total Earnings 237.3 223.8

Outstanding Shares

(in millions)

263.5151

51

240.8302

81

EPS

0.900517

4811

0.929285

1342 -3.10%

Gearing Ratio

Long-term debt 591.3 511.5

Shareholder's equity 2073 1729

Debt-equity ratio 0.28 0.29 -3.58%

b) Analysis of the performance and position of Unite Group plc on the basis of above

calculations.

Ratio analysis enables investors to assess the performance of company. This helps in making

decision for their investment in any company. Investors use different ratios according to their

investing requirements for knowing the position of company. Also different stakeholders are

using ratio analysis to take their future decisions.

Ratio Analysis of Unite Group plc

Profitability ratios

2

Inventory 9.1 4.5

Debtors 88.1 82.9

Creditors 141.5 152.1

Days 365 365

COS 40.2 41.1

Sales 128.3 119.3

8 Inventory days

Inventory/

COS*365 82.624 39.964 106.75%

9 Debtor days Debtor/ Sales*365 250.64 253.63 -1.18%

10 Creditor days

Creditor /

Sales*365 402.55 465.35 -13.50%

Investor Return

11 EPS

Total Earnings/

Outstanding shares

Total Earnings 237.3 223.8

Outstanding Shares

(in millions)

263.5151

51

240.8302

81

EPS

0.900517

4811

0.929285

1342 -3.10%

Gearing Ratio

Long-term debt 591.3 511.5

Shareholder's equity 2073 1729

Debt-equity ratio 0.28 0.29 -3.58%

b) Analysis of the performance and position of Unite Group plc on the basis of above

calculations.

Ratio analysis enables investors to assess the performance of company. This helps in making

decision for their investment in any company. Investors use different ratios according to their

investing requirements for knowing the position of company. Also different stakeholders are

using ratio analysis to take their future decisions.

Ratio Analysis of Unite Group plc

Profitability ratios

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gross profit margin ratio of group has improved from the previous years by 4.76 percent.

Gross profit margin should be high as company is serving more in service sector as company do

not have manufacturing costs. Gross profit margin of the company has improved because the

cost of sales and operating expenses in comparison to previous year have decreased as against

the revenues. Since revenues have increased and cost are decreased margin has increased.

Operating profit margin of company has decreased by 0.37 percent. The operating margin

of company is high as company receives major revenues from share in joint ventures. Valuation

gains on property are recorded in income statement that rise the operating margin as against

revenues from company's business. Decrease is seen due to release of shares in few joint

ventures.

Asset turnover ratio of company shows a decrease of 8.23 percent. Revenues of company

has not increased of company as against the increase in its total assets. Also it covers only

revenues of company not of its joint ventures.

Return on capital employed of company has worsened from previous years it has

decreased by 11.25%. company has acquired new investments property and also the cash and

cash equivalent of the company are 123.6 million in year 2018 where it was only 51.2 million in

2017. This has increased the asset of company where the revenues have not shown rise as against

increase in assets. Where return on equity of company has decreased by 11.38 percent. Company

has issued new shares and also the balance in retained earnings and share premium have

increased. Total shareholders equity has raised which will increase the valuation of company but

return over equity is decreased as revenues are shared among increased shares.

Liquidity Ratios

Liquidity ratios of company are showing high improvisation compared to last year.

Current ratio is increased which shows that liquidity position of company has strengthened. Rise

of cash and cash equivalents and trades receivable has increased current assets of company

where the current liabilities have decreased. Therefore the current ratio is improved. Quick ratio

along with above reason also the inventory has gone down causing an increase in ratio. Company

is in position to meet its short term obligations. Liquidity position of company will come down if

cash and cash equivalents come down to the level of previous year. Company has not made

payments on behalf of its subsidiaries this year therefore company is left wit enough liquid

assets for carrying out the operational activities and making payments for short term liabilities.

3

Gross profit margin should be high as company is serving more in service sector as company do

not have manufacturing costs. Gross profit margin of the company has improved because the

cost of sales and operating expenses in comparison to previous year have decreased as against

the revenues. Since revenues have increased and cost are decreased margin has increased.

Operating profit margin of company has decreased by 0.37 percent. The operating margin

of company is high as company receives major revenues from share in joint ventures. Valuation

gains on property are recorded in income statement that rise the operating margin as against

revenues from company's business. Decrease is seen due to release of shares in few joint

ventures.

Asset turnover ratio of company shows a decrease of 8.23 percent. Revenues of company

has not increased of company as against the increase in its total assets. Also it covers only

revenues of company not of its joint ventures.

Return on capital employed of company has worsened from previous years it has

decreased by 11.25%. company has acquired new investments property and also the cash and

cash equivalent of the company are 123.6 million in year 2018 where it was only 51.2 million in

2017. This has increased the asset of company where the revenues have not shown rise as against

increase in assets. Where return on equity of company has decreased by 11.38 percent. Company

has issued new shares and also the balance in retained earnings and share premium have

increased. Total shareholders equity has raised which will increase the valuation of company but

return over equity is decreased as revenues are shared among increased shares.

Liquidity Ratios

Liquidity ratios of company are showing high improvisation compared to last year.

Current ratio is increased which shows that liquidity position of company has strengthened. Rise

of cash and cash equivalents and trades receivable has increased current assets of company

where the current liabilities have decreased. Therefore the current ratio is improved. Quick ratio

along with above reason also the inventory has gone down causing an increase in ratio. Company

is in position to meet its short term obligations. Liquidity position of company will come down if

cash and cash equivalents come down to the level of previous year. Company has not made

payments on behalf of its subsidiaries this year therefore company is left wit enough liquid

assets for carrying out the operational activities and making payments for short term liabilities.

3

Strong liquidity position of company builds confidence in relevant stakeholders, where too much

of liquid assets show that company is not making productive use of money. Therefore it should

not be too high and not too low.

Efficiency Ratios

Efficiency ratios are calculated for knowing the efficiency of company in operating the

business operation of company. It includes inventory days, debtor days and creditor day.

Inventory days of company for year 2018 is 83 days. It has shown a rise from last year as

company has purchased and doubled the stocks as compared with previous year. Company

provides accommodation services for student and is not in manufacturing sector therefore it does

not have high inventory levels. Available inventory can be used by company for 83 days in a

year and may place according. Debtor days shows for the days that are given to debtors for

making payments for the sales. Debtor days of company are very high as sales are recorded

before the revenues earned as income is from rents of the accommodations. Collection from

debtors is high.

Creditor days of company have reduced from previous. Being in construction business it

is having high creditor days as construction of buildings take time and creditor for a given year

are high. Analysing the overall scenario of business, Unit Group is efficiently managing its

operations. Company is managing inventory properly, also the debtor days are less which show

cash collection are made on time and creditor days are high that is beneficial for the company.

This help to company to use the funds in operating its business effectively.

Investor Return

Return over investment in company is measured by earnings per share. Company is

having high reputation in market. EPS of company has decreased from last year with 3.10

percent. Company in year 2018 has issue new shares where the profit margins of the company

have decreased. Shares have been issued and margins have decreased resulting in reduction in

earnings of shareholders. EPS is decreased as profits are now distributed among increased

number of shareholder as compared with previous year.

Gearing Ratio

Gearing ratio shows the debt position of company. Debt to equity ratio of company has

decreased that company has improvised debt management. Long term borrowings of the

company has raised for completing the under construction investment properties. New shares

4

of liquid assets show that company is not making productive use of money. Therefore it should

not be too high and not too low.

Efficiency Ratios

Efficiency ratios are calculated for knowing the efficiency of company in operating the

business operation of company. It includes inventory days, debtor days and creditor day.

Inventory days of company for year 2018 is 83 days. It has shown a rise from last year as

company has purchased and doubled the stocks as compared with previous year. Company

provides accommodation services for student and is not in manufacturing sector therefore it does

not have high inventory levels. Available inventory can be used by company for 83 days in a

year and may place according. Debtor days shows for the days that are given to debtors for

making payments for the sales. Debtor days of company are very high as sales are recorded

before the revenues earned as income is from rents of the accommodations. Collection from

debtors is high.

Creditor days of company have reduced from previous. Being in construction business it

is having high creditor days as construction of buildings take time and creditor for a given year

are high. Analysing the overall scenario of business, Unit Group is efficiently managing its

operations. Company is managing inventory properly, also the debtor days are less which show

cash collection are made on time and creditor days are high that is beneficial for the company.

This help to company to use the funds in operating its business effectively.

Investor Return

Return over investment in company is measured by earnings per share. Company is

having high reputation in market. EPS of company has decreased from last year with 3.10

percent. Company in year 2018 has issue new shares where the profit margins of the company

have decreased. Shares have been issued and margins have decreased resulting in reduction in

earnings of shareholders. EPS is decreased as profits are now distributed among increased

number of shareholder as compared with previous year.

Gearing Ratio

Gearing ratio shows the debt position of company. Debt to equity ratio of company has

decreased that company has improvised debt management. Long term borrowings of the

company has raised for completing the under construction investment properties. New shares

4

You're viewing a preview

Unlock full access by subscribing today!

have been issued by company and the debts of the company has not raised high as against equity

of the shareholder's equity. Therefore the gearing ratio of company has reduced which is good

for company. This depicts that company do not raise high funds from markets for its investment

projects. It is having string financial position.

Company's performance from the previous year has enhanced due to new steps and

strategic decisions of company. Company is having string market position this can be analysed

through gearing ratio, profitability ratios and also the demand for the company shares has made

the company to issue new shares.

C) Analysis of change in lease accounting rules from IAS 17 Leases to IFRS 16 Leases.

Companies need different assets for making services and rendering services to consumers.

Companies generally lease assets than buying them. Accounting treatment of leases is an

important task for company.

IAS 17 standardise accounting treatment & disclosure of assets. Concept of substance

over form is applied over specific accounting areas of lease. IAS 17 deems it necessary in

accounting for substance of transactions. IAS 17 records transaction into operating and finance

lease. In operating lease lessees were not required to show lease in their balance sheet as asset or

liability they were only shown as expense in profit or loss. Only non cancellable operating lease

were represented as liability. And this liability was not shown in the financial statement of

company. The discrepancy was removed with invention of IFRS 16 by putting most lease on

balance sheet.

Under IFRS things have not changed much, but care has to be taken in case of certain

service contracts. Detailed guidance is provided by IFRS 16 for differentiating between lease or

service contracts. Accounting was done for both contracts whether it is operating or service

contract. Significant changes are seen in IFRS as now companies have to identify whether the

lease will be recorded under IFRS 16 or service contracts. It is a big change in lease accounting ,

recording of operating lease will bring major difference between many financial metrics.

Operating lease accounting treatment

Financial reporting impact

Capitalisation of operating leases , this would be shift in financial metrics for companies having

this types of lease. With the changes in financial ratios, metrics and liabilities companies would

now be required to have extra care for explaining the shift figures.

5

of the shareholder's equity. Therefore the gearing ratio of company has reduced which is good

for company. This depicts that company do not raise high funds from markets for its investment

projects. It is having string financial position.

Company's performance from the previous year has enhanced due to new steps and

strategic decisions of company. Company is having string market position this can be analysed

through gearing ratio, profitability ratios and also the demand for the company shares has made

the company to issue new shares.

C) Analysis of change in lease accounting rules from IAS 17 Leases to IFRS 16 Leases.

Companies need different assets for making services and rendering services to consumers.

Companies generally lease assets than buying them. Accounting treatment of leases is an

important task for company.

IAS 17 standardise accounting treatment & disclosure of assets. Concept of substance

over form is applied over specific accounting areas of lease. IAS 17 deems it necessary in

accounting for substance of transactions. IAS 17 records transaction into operating and finance

lease. In operating lease lessees were not required to show lease in their balance sheet as asset or

liability they were only shown as expense in profit or loss. Only non cancellable operating lease

were represented as liability. And this liability was not shown in the financial statement of

company. The discrepancy was removed with invention of IFRS 16 by putting most lease on

balance sheet.

Under IFRS things have not changed much, but care has to be taken in case of certain

service contracts. Detailed guidance is provided by IFRS 16 for differentiating between lease or

service contracts. Accounting was done for both contracts whether it is operating or service

contract. Significant changes are seen in IFRS as now companies have to identify whether the

lease will be recorded under IFRS 16 or service contracts. It is a big change in lease accounting ,

recording of operating lease will bring major difference between many financial metrics.

Operating lease accounting treatment

Financial reporting impact

Capitalisation of operating leases , this would be shift in financial metrics for companies having

this types of lease. With the changes in financial ratios, metrics and liabilities companies would

now be required to have extra care for explaining the shift figures.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Definition

Lessees would now be required for identifying and separating non lease components for

accounting only necessary leases on balance sheet. Non lease component would be receive

increased attention ion negotiation phase.

Lessor interaction

In IAS 17 focus was laid on lease from operational perspective. And lessees used it for avoiding

recognition in balance sheet. Where IFRS 16 focused on negotiation of deals. Leasing will

become an important decisions for decisions relying on off balance sheet capabilities of

operating lease.

Advantages and Disadvantages of IFRS 16

Advantages

It introduces single accounting model of lease with term of more than one year for

recognising assets and liabilities. Leases will be accounted in financial statement of lessees.

Disadvantages

It is difficult process of differentiating between operating lease or service lease.

It will drive the decision of investors as all off balance sheet leases will be shown.

Unit group plc will now be recording off balance sheet leases recorded in IAS 17.

Company will now have to recognise sale and leaseback right of use asset in consolidated

statements initially measured at fair value using discounted cash flows. Company would now

have to hold the sale & leaseback right of use assets as investment property at fair value and

revaluing them at the end of every financial reporting period , any changes in values will be

recorded in consolidated income statement as gain or loss on revaluation of investment property.

6

Lessees would now be required for identifying and separating non lease components for

accounting only necessary leases on balance sheet. Non lease component would be receive

increased attention ion negotiation phase.

Lessor interaction

In IAS 17 focus was laid on lease from operational perspective. And lessees used it for avoiding

recognition in balance sheet. Where IFRS 16 focused on negotiation of deals. Leasing will

become an important decisions for decisions relying on off balance sheet capabilities of

operating lease.

Advantages and Disadvantages of IFRS 16

Advantages

It introduces single accounting model of lease with term of more than one year for

recognising assets and liabilities. Leases will be accounted in financial statement of lessees.

Disadvantages

It is difficult process of differentiating between operating lease or service lease.

It will drive the decision of investors as all off balance sheet leases will be shown.

Unit group plc will now be recording off balance sheet leases recorded in IAS 17.

Company will now have to recognise sale and leaseback right of use asset in consolidated

statements initially measured at fair value using discounted cash flows. Company would now

have to hold the sale & leaseback right of use assets as investment property at fair value and

revaluing them at the end of every financial reporting period , any changes in values will be

recorded in consolidated income statement as gain or loss on revaluation of investment property.

6

7

You're viewing a preview

Unlock full access by subscribing today!

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.