Financial Reporting in Global Markets: Tesco Company Analysis Report

VerifiedAdded on 2023/01/09

|23

|6182

|2

Report

AI Summary

This report provides a comprehensive analysis of financial reporting in global markets, using the Tesco company as a case study. It delves into the regulatory frameworks governing financial accounting, including IFRS and GAAP, and their impact on financial statements. The report examines the purpose of financial reporting in meeting organizational objectives, development, and growth, and interprets profit & loss statements, balance sheets, and cash flows. It also explores the benefits of International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), models of financial reporting and auditing, and critically evaluates the differences and importance of IFRS in different countries. The report also explores factors that influence international differences in financial reporting and concludes with an overview of the key findings and implications for stakeholders. The report covers key stakeholders such as shareholders, employees, investors, suppliers, etc.

Financial Reporting in

Global Market

Global Market

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................................4

TASK 1..........................................................................................................................................................4

P1 Regulatory frameworks and governance of financial accounting:......................................................4

Governance of financial reporting...........................................................................................................6

P2 Purpose of financial reporting for meeting organisational objectives, development and growth:.......7

P3 Interpretation of profit & loss, balance sheet and cash flows..............................................................9

P5 Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS)...................................................................................................................................12

P6 Models of financial reporting and auditing.......................................................................................14

P7 Critically evaluate the differences and importance of IFRS in different countries............................15

Factors influence the international differences in financial reporting....................................................16

Models of financial reporting and auditing............................................................................................16

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

TASK 1..........................................................................................................................................................4

P1 Regulatory frameworks and governance of financial accounting:......................................................4

Governance of financial reporting...........................................................................................................6

P2 Purpose of financial reporting for meeting organisational objectives, development and growth:.......7

P3 Interpretation of profit & loss, balance sheet and cash flows..............................................................9

P5 Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS)...................................................................................................................................12

P6 Models of financial reporting and auditing.......................................................................................14

P7 Critically evaluate the differences and importance of IFRS in different countries............................15

Factors influence the international differences in financial reporting....................................................16

Models of financial reporting and auditing............................................................................................16

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION

Financial reporting can be considered as a system of displaying to employees and senior

interested parties the financial reports and details. The primary function of these documents is to

raise awareness among citizens about a corporation’s financial over a given time period. There

are a large variety of decisions and processes produced by various agencies in the context of the

organization (Aifuwa and Embele, 2019). Awareness of the results of all the operations in terms

of benefit is important here and that this is achieved with the aid of annual disclosures. The

annual reports are finally drawn up and published at the end of each accounting period. This

report based on the Tesco Company which is established in UK and large sector organisation.

Now this Financial Reports report format, conceptual and regulatory structure is described.

Including the advantage of those findings to the stockholder is also addressed. In addition to this,

the report contains variations between the international accounting standard and the international

financial reporting requirement. From the background of provided details and data, various types

of financial reports and statements, including such P&L account, balance sheet etc. are prepared.

TASK 1

P1 Regulatory frameworks and governance of financial accounting:

Financial reporting: This includes the submission to the managers and the holders i.e. the

investors of the company’s financial statements for the purpose of obtaining information the

financial condition of the corporation. It is the assessment of audited financial statements in an

organization that consists mainly of statement of revenue &spending, report of financial position

and income statement. It is a legal duty for the company to report to its creditors and

stakeholders and what overall monetary condition is. The institution's compliance with financial

reporting guarantees that perhaps the interested parties, most pertinently the stockholders, are

cared for properly of their investments. This is an integral part of effective financial regulation.

Government and political review of accurate financial reports helps companies develop an

enforcement relationship together with consumer dependency. That is accompanied by the core

objective of financial reporting:

1. Reporting to management employees who analysis in operational preparation and decision-

making for TESCO.

Financial reporting can be considered as a system of displaying to employees and senior

interested parties the financial reports and details. The primary function of these documents is to

raise awareness among citizens about a corporation’s financial over a given time period. There

are a large variety of decisions and processes produced by various agencies in the context of the

organization (Aifuwa and Embele, 2019). Awareness of the results of all the operations in terms

of benefit is important here and that this is achieved with the aid of annual disclosures. The

annual reports are finally drawn up and published at the end of each accounting period. This

report based on the Tesco Company which is established in UK and large sector organisation.

Now this Financial Reports report format, conceptual and regulatory structure is described.

Including the advantage of those findings to the stockholder is also addressed. In addition to this,

the report contains variations between the international accounting standard and the international

financial reporting requirement. From the background of provided details and data, various types

of financial reports and statements, including such P&L account, balance sheet etc. are prepared.

TASK 1

P1 Regulatory frameworks and governance of financial accounting:

Financial reporting: This includes the submission to the managers and the holders i.e. the

investors of the company’s financial statements for the purpose of obtaining information the

financial condition of the corporation. It is the assessment of audited financial statements in an

organization that consists mainly of statement of revenue &spending, report of financial position

and income statement. It is a legal duty for the company to report to its creditors and

stakeholders and what overall monetary condition is. The institution's compliance with financial

reporting guarantees that perhaps the interested parties, most pertinently the stockholders, are

cared for properly of their investments. This is an integral part of effective financial regulation.

Government and political review of accurate financial reports helps companies develop an

enforcement relationship together with consumer dependency. That is accompanied by the core

objective of financial reporting:

1. Reporting to management employees who analysis in operational preparation and decision-

making for TESCO.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Offering supporters, creditors, shareholders and other stakeholders with suitable

documentation and knowledge to allow people to make reasonable and rational funding and

financial choices.

3. To transmit the true and truthful picture of a business organisation to stakeholders and the

world at large (Alzeban, 2019).

4. To assess whether companies use their financial and other business resources efficiently.

5. To provide detailed reports on the corporate growth and growth to the diverse stakeholders.

6. Assessing and reporting the effectiveness of initiatives faced by business organizations to

diverse participants.

7. To prove that Tesco is completely compliant with multiple governmental laws and regulations.

Regulatory framework of financial reporting

In order to manage processes and tracking within financial reports, a common system is

used by many individual business organizations to cover all aspects of financial reporting in

depth. The approving process ensures the far more detailed and suitable financial statements for

an organisation. It emphasizes compliance with generally accepted regulatory requirements to

allow uniform monitoring. IFRS (International Financial Reporting Standards) and GAAP

(Generally Accepted Accounting Principles) are part of the legislative framework, which

provides a collection of criteria, ideas, laws and concepts that accountants can follow when

working on different concerns. The legal framework is a series of phases that government

regulators are starting to take in order to increase the awareness various legislation. It is essential

for TESCO to comply with the legal framework, as it ensures that sufficient customer

information is exchanged with people and corporations. The main aim of the legal environment

is to provide continuity in accounting systems adopted by different business organizations

(Amidu, Yorke and Harvey, 2016). IFRS is a key component of the regulatory component, since

it offers specifications that assist in the sharpness of accounting records. The legal framework is

defined by government agencies and follows all the rules and legislation is also an objective. The

trust of shareholders and investor in companies like TESCO is powerful despite regular

accordance with statutory structure. Such structure is necessary for all publicly traded companies

documentation and knowledge to allow people to make reasonable and rational funding and

financial choices.

3. To transmit the true and truthful picture of a business organisation to stakeholders and the

world at large (Alzeban, 2019).

4. To assess whether companies use their financial and other business resources efficiently.

5. To provide detailed reports on the corporate growth and growth to the diverse stakeholders.

6. Assessing and reporting the effectiveness of initiatives faced by business organizations to

diverse participants.

7. To prove that Tesco is completely compliant with multiple governmental laws and regulations.

Regulatory framework of financial reporting

In order to manage processes and tracking within financial reports, a common system is

used by many individual business organizations to cover all aspects of financial reporting in

depth. The approving process ensures the far more detailed and suitable financial statements for

an organisation. It emphasizes compliance with generally accepted regulatory requirements to

allow uniform monitoring. IFRS (International Financial Reporting Standards) and GAAP

(Generally Accepted Accounting Principles) are part of the legislative framework, which

provides a collection of criteria, ideas, laws and concepts that accountants can follow when

working on different concerns. The legal framework is a series of phases that government

regulators are starting to take in order to increase the awareness various legislation. It is essential

for TESCO to comply with the legal framework, as it ensures that sufficient customer

information is exchanged with people and corporations. The main aim of the legal environment

is to provide continuity in accounting systems adopted by different business organizations

(Amidu, Yorke and Harvey, 2016). IFRS is a key component of the regulatory component, since

it offers specifications that assist in the sharpness of accounting records. The legal framework is

defined by government agencies and follows all the rules and legislation is also an objective. The

trust of shareholders and investor in companies like TESCO is powerful despite regular

accordance with statutory structure. Such structure is necessary for all publicly traded companies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accepting digital payments in order to attract potential shareholders. This also helps to address

different problems that can occur during the course of financial statements and increase

transparency. Prepared to follow are some major characteristics of the Financial Reporting

regulatory system including the following:

IFRS: International accounting principles are known as financial reporting guidelines for

publicly listed firms. The committee of the International accounting standard established certain

principles. These are key components of the complex legal framework for accounting. These

standards are agreed internationally by the organizations listed for conducting out financial

accounting and recording issues. These values act as a shared language for the valuation of the

company on a world basis, and as such the current share cost can be clearly understood and

comparable to all customers around the world. These criteria regard both benefits and drawbacks

of the corporation's organisation (Balsmeier and Vanhaverbeke, 2018).

GAAP: It means that business organization must be practiced when accounting standards

in a collection of generally accepted accounting principles, policies and practices. GAAP

provides a standardized basis for the disclosure of potential consumers of business issues.As per

general standards and regulation, GAAP helps regulate the field of finance. It aims to standardize

and control in all sectors the concepts, principles, and procedures used during reporting. GAAP

includes such issues as identification of sales, identification of balance sheets, and materiality.

GAAP's ultimate objective is to guarantee that the financial statements of a corporation are

accurate, accurate, and equivalent. This makes it possible for investor to make and derive

valuable information, particularly pattern items over a period of time, from either the financial

statements of the company. It also involves the evaluation of financial data across various

businesses.

Governance of financial reporting

In the current business climate, government regulators are focusing their efforts into

reinforcing executive compensation requirements for financial statements, with public companies

facing cash problems. Financial reporting laws specifically involve the owner, who is quite

responsible for giving views on the financial statements of the companies. The auditor may be an

internal auditor or a statutory auditor as per their responsibilities. Audit committee may be

employees of the government and are independent public inspectors. For the efficient

different problems that can occur during the course of financial statements and increase

transparency. Prepared to follow are some major characteristics of the Financial Reporting

regulatory system including the following:

IFRS: International accounting principles are known as financial reporting guidelines for

publicly listed firms. The committee of the International accounting standard established certain

principles. These are key components of the complex legal framework for accounting. These

standards are agreed internationally by the organizations listed for conducting out financial

accounting and recording issues. These values act as a shared language for the valuation of the

company on a world basis, and as such the current share cost can be clearly understood and

comparable to all customers around the world. These criteria regard both benefits and drawbacks

of the corporation's organisation (Balsmeier and Vanhaverbeke, 2018).

GAAP: It means that business organization must be practiced when accounting standards

in a collection of generally accepted accounting principles, policies and practices. GAAP

provides a standardized basis for the disclosure of potential consumers of business issues.As per

general standards and regulation, GAAP helps regulate the field of finance. It aims to standardize

and control in all sectors the concepts, principles, and procedures used during reporting. GAAP

includes such issues as identification of sales, identification of balance sheets, and materiality.

GAAP's ultimate objective is to guarantee that the financial statements of a corporation are

accurate, accurate, and equivalent. This makes it possible for investor to make and derive

valuable information, particularly pattern items over a period of time, from either the financial

statements of the company. It also involves the evaluation of financial data across various

businesses.

Governance of financial reporting

In the current business climate, government regulators are focusing their efforts into

reinforcing executive compensation requirements for financial statements, with public companies

facing cash problems. Financial reporting laws specifically involve the owner, who is quite

responsible for giving views on the financial statements of the companies. The auditor may be an

internal auditor or a statutory auditor as per their responsibilities. Audit committee may be

employees of the government and are independent public inspectors. For the efficient

performance of corporate statements, internally and externally or statutory accounting

professionals are important within TESCO. The powers of internal auditing are, therefore,

minimal comparable to external investigators (Hadi, Suryanto and Hussain, 2016). Many other

regulatory agencies, such as the IAB, the ASB, etc., are also committed to good financial

statement accounting, but these bodies have specific standards and regulations for proper

management compliance. Furthermore, regulatory authorities specify the laws and duties of

relevant stakeholders such as accountants. Effective financial reporting governance provides an

actual picture of the efficiency of the company in order to protect stakeholder interest. Tesco has

following the rules and principles of IAS regulatory framework.

P2 Purpose of financial reporting for meeting organisational objectives, development and

growth:

Financial statements, such as revenue and balance sheet reports, offer a true picture of

company goals by income statement. The corporate accounting position for a corporate

corporation, as it ensures long-term success and growth. In TESCO, cash revenues are recorded

by administrators under the financial accounts, income statement, of the financial reporting

system to show their true performance over a particular period (Kimbro and Xu, 2016). Other

significant financial investigation benefits, listed further below, were prepared to take:

• It assists managers to take in-depth organizational plans for future objectives by having to rely

mostly on monetary information provided by declarations that reveal the present position. It

knowledge helps administrators build a base table of estimates for the potential. Data

relevantness provides a pathway to emancipate prospective corporate strategy.

• The second most influential objective of financial statements is to reveal to shareholders that

have provides extra opportunities for growth the key attributes and risk and effects. To do this is

both an obligatory and moral practice.To protect investors' interests from illegal activities

including securities trading, economic scandals etc., and each country has adopted some business

legislation allowing corporations to report information to the community and government.

• Following revenue recognition requirements promotes legislative auditing by supplying

excellently-crafted review relevant documentation. This allows it easier for the firm to raise

professionals are important within TESCO. The powers of internal auditing are, therefore,

minimal comparable to external investigators (Hadi, Suryanto and Hussain, 2016). Many other

regulatory agencies, such as the IAB, the ASB, etc., are also committed to good financial

statement accounting, but these bodies have specific standards and regulations for proper

management compliance. Furthermore, regulatory authorities specify the laws and duties of

relevant stakeholders such as accountants. Effective financial reporting governance provides an

actual picture of the efficiency of the company in order to protect stakeholder interest. Tesco has

following the rules and principles of IAS regulatory framework.

P2 Purpose of financial reporting for meeting organisational objectives, development and

growth:

Financial statements, such as revenue and balance sheet reports, offer a true picture of

company goals by income statement. The corporate accounting position for a corporate

corporation, as it ensures long-term success and growth. In TESCO, cash revenues are recorded

by administrators under the financial accounts, income statement, of the financial reporting

system to show their true performance over a particular period (Kimbro and Xu, 2016). Other

significant financial investigation benefits, listed further below, were prepared to take:

• It assists managers to take in-depth organizational plans for future objectives by having to rely

mostly on monetary information provided by declarations that reveal the present position. It

knowledge helps administrators build a base table of estimates for the potential. Data

relevantness provides a pathway to emancipate prospective corporate strategy.

• The second most influential objective of financial statements is to reveal to shareholders that

have provides extra opportunities for growth the key attributes and risk and effects. To do this is

both an obligatory and moral practice.To protect investors' interests from illegal activities

including securities trading, economic scandals etc., and each country has adopted some business

legislation allowing corporations to report information to the community and government.

• Following revenue recognition requirements promotes legislative auditing by supplying

excellently-crafted review relevant documentation. This allows it easier for the firm to raise

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

money from foreign and regional markets relative to non compliance entities as it fascinates a

good reputation to the business(Lewis and Young, 2019).

Main users of financial statements or statistics are usually people in the shares of the

company or expenditure carrying significant insurable interest in business entity. In addition,

there are a few foreign markets worried with the long term operations and success anticipated of

the corporation. As decision makers are considered those human beings, peoples, collection of

individuals who've been explicitly or implicitly satisfied with the results, performance, financial

status or actual or prospective development of an organization. TESCO main stakeholders

include proprietors, upper executives, suppliers, clients and stockholders. The key importance of

financial details to the diverse participants as mentioned here are:

Internal stakeholders: those were people or companies of people who have been from

within connected yet are also now able to serve institutions such as boards of directors, inner

staff, volunteers and other staff. A few of these team members are addressed following, and their

benefits:

• Shareholders: investors are big TESCO owners and board members. Business is strongly

influenced by investor judgments and they affect organizational net worth. Investors hold a

shareholding in the revenue or net earnings of the organization in the form of earnings and value

of the company.

• Employees: Workers at TESCO would gain from ever using monetary information of the

products because it can help predict their potential development in the business and measure

their own results (Omran and Ramdhony, 2016).

External stakeholders: Groups of people, individuals, groups or organizations are not

actively engaged in Tesco but are interested or involved about the productivity, outcomes,

reports and statement of financial position including such investors, lenders and creditors,

suppliers, ruling party and regulatory bodies. Following are some of them mentioned:

• Investors: While using the monetary reports of the company, investors decide to invest in

the market and to retain an interest in the form of a return on capital in the earnings of the

company. They are often helping organizations in achieving the situation of profit margins.

good reputation to the business(Lewis and Young, 2019).

Main users of financial statements or statistics are usually people in the shares of the

company or expenditure carrying significant insurable interest in business entity. In addition,

there are a few foreign markets worried with the long term operations and success anticipated of

the corporation. As decision makers are considered those human beings, peoples, collection of

individuals who've been explicitly or implicitly satisfied with the results, performance, financial

status or actual or prospective development of an organization. TESCO main stakeholders

include proprietors, upper executives, suppliers, clients and stockholders. The key importance of

financial details to the diverse participants as mentioned here are:

Internal stakeholders: those were people or companies of people who have been from

within connected yet are also now able to serve institutions such as boards of directors, inner

staff, volunteers and other staff. A few of these team members are addressed following, and their

benefits:

• Shareholders: investors are big TESCO owners and board members. Business is strongly

influenced by investor judgments and they affect organizational net worth. Investors hold a

shareholding in the revenue or net earnings of the organization in the form of earnings and value

of the company.

• Employees: Workers at TESCO would gain from ever using monetary information of the

products because it can help predict their potential development in the business and measure

their own results (Omran and Ramdhony, 2016).

External stakeholders: Groups of people, individuals, groups or organizations are not

actively engaged in Tesco but are interested or involved about the productivity, outcomes,

reports and statement of financial position including such investors, lenders and creditors,

suppliers, ruling party and regulatory bodies. Following are some of them mentioned:

• Investors: While using the monetary reports of the company, investors decide to invest in

the market and to retain an interest in the form of a return on capital in the earnings of the

company. They are often helping organizations in achieving the situation of profit margins.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

• Suppliers: Distributors are stockholders which impact or predict the production and

consumption estimates. Wholesalers profit from association by marketing their goods or product

in large quantities (Perera and Chand, 2015).

TASK 2

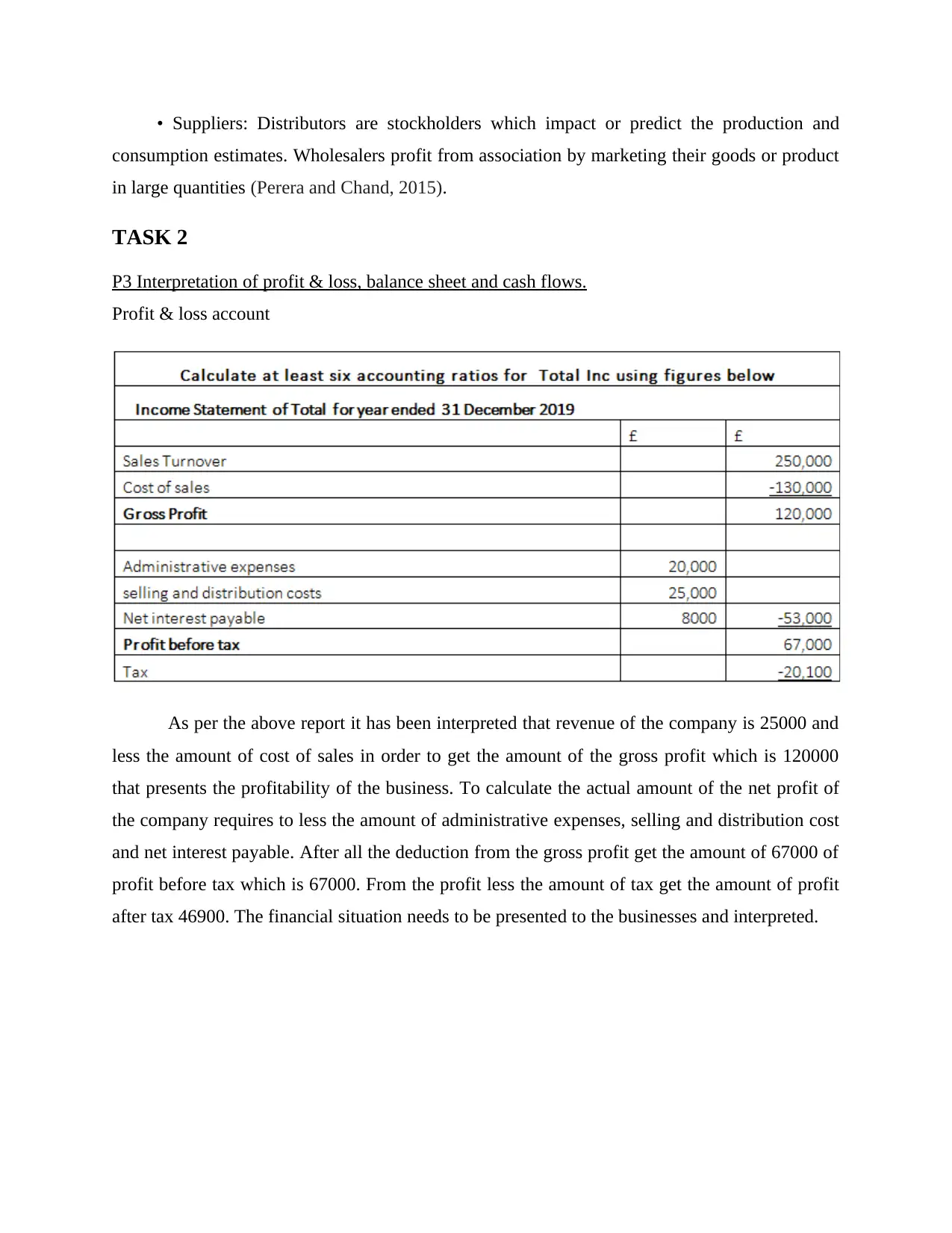

P3 Interpretation of profit & loss, balance sheet and cash flows.

Profit & loss account

As per the above report it has been interpreted that revenue of the company is 25000 and

less the amount of cost of sales in order to get the amount of the gross profit which is 120000

that presents the profitability of the business. To calculate the actual amount of the net profit of

the company requires to less the amount of administrative expenses, selling and distribution cost

and net interest payable. After all the deduction from the gross profit get the amount of 67000 of

profit before tax which is 67000. From the profit less the amount of tax get the amount of profit

after tax 46900. The financial situation needs to be presented to the businesses and interpreted.

consumption estimates. Wholesalers profit from association by marketing their goods or product

in large quantities (Perera and Chand, 2015).

TASK 2

P3 Interpretation of profit & loss, balance sheet and cash flows.

Profit & loss account

As per the above report it has been interpreted that revenue of the company is 25000 and

less the amount of cost of sales in order to get the amount of the gross profit which is 120000

that presents the profitability of the business. To calculate the actual amount of the net profit of

the company requires to less the amount of administrative expenses, selling and distribution cost

and net interest payable. After all the deduction from the gross profit get the amount of 67000 of

profit before tax which is 67000. From the profit less the amount of tax get the amount of profit

after tax 46900. The financial situation needs to be presented to the businesses and interpreted.

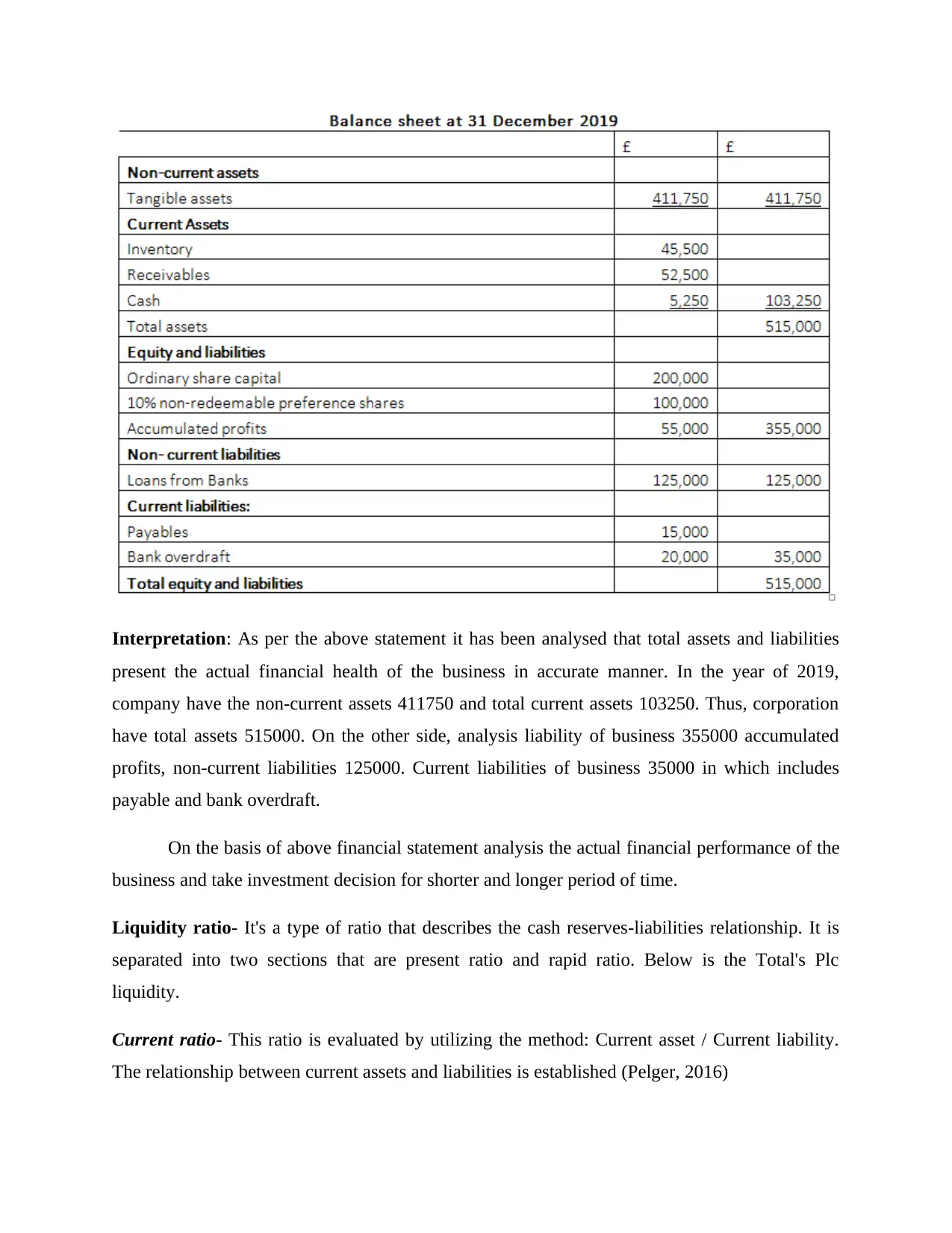

Interpretation: As per the above statement it has been analysed that total assets and liabilities

present the actual financial health of the business in accurate manner. In the year of 2019,

company have the non-current assets 411750 and total current assets 103250. Thus, corporation

have total assets 515000. On the other side, analysis liability of business 355000 accumulated

profits, non-current liabilities 125000. Current liabilities of business 35000 in which includes

payable and bank overdraft.

On the basis of above financial statement analysis the actual financial performance of the

business and take investment decision for shorter and longer period of time.

Liquidity ratio- It's a type of ratio that describes the cash reserves-liabilities relationship. It is

separated into two sections that are present ratio and rapid ratio. Below is the Total's Plc

liquidity.

Current ratio- This ratio is evaluated by utilizing the method: Current asset / Current liability.

The relationship between current assets and liabilities is established (Pelger, 2016)

present the actual financial health of the business in accurate manner. In the year of 2019,

company have the non-current assets 411750 and total current assets 103250. Thus, corporation

have total assets 515000. On the other side, analysis liability of business 355000 accumulated

profits, non-current liabilities 125000. Current liabilities of business 35000 in which includes

payable and bank overdraft.

On the basis of above financial statement analysis the actual financial performance of the

business and take investment decision for shorter and longer period of time.

Liquidity ratio- It's a type of ratio that describes the cash reserves-liabilities relationship. It is

separated into two sections that are present ratio and rapid ratio. Below is the Total's Plc

liquidity.

Current ratio- This ratio is evaluated by utilizing the method: Current asset / Current liability.

The relationship between current assets and liabilities is established (Pelger, 2016)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

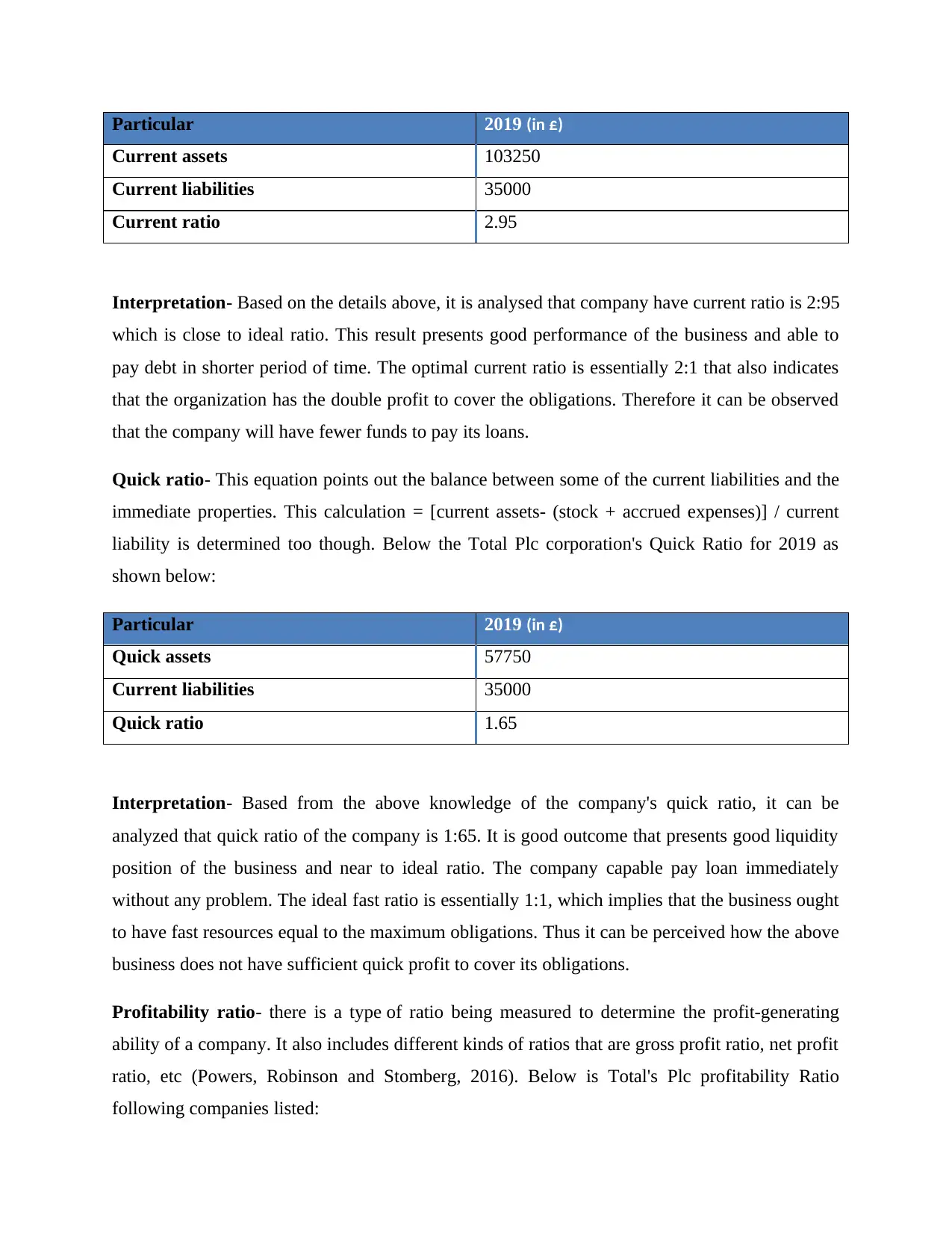

Particular 2019 (in £)

Current assets 103250

Current liabilities 35000

Current ratio 2.95

Interpretation- Based on the details above, it is analysed that company have current ratio is 2:95

which is close to ideal ratio. This result presents good performance of the business and able to

pay debt in shorter period of time. The optimal current ratio is essentially 2:1 that also indicates

that the organization has the double profit to cover the obligations. Therefore it can be observed

that the company will have fewer funds to pay its loans.

Quick ratio- This equation points out the balance between some of the current liabilities and the

immediate properties. This calculation = [current assets- (stock + accrued expenses)] / current

liability is determined too though. Below the Total Plc corporation's Quick Ratio for 2019 as

shown below:

Particular 2019 (in £)

Quick assets 57750

Current liabilities 35000

Quick ratio 1.65

Interpretation- Based from the above knowledge of the company's quick ratio, it can be

analyzed that quick ratio of the company is 1:65. It is good outcome that presents good liquidity

position of the business and near to ideal ratio. The company capable pay loan immediately

without any problem. The ideal fast ratio is essentially 1:1, which implies that the business ought

to have fast resources equal to the maximum obligations. Thus it can be perceived how the above

business does not have sufficient quick profit to cover its obligations.

Profitability ratio- there is a type of ratio being measured to determine the profit-generating

ability of a company. It also includes different kinds of ratios that are gross profit ratio, net profit

ratio, etc (Powers, Robinson and Stomberg, 2016). Below is Total's Plc profitability Ratio

following companies listed:

Current assets 103250

Current liabilities 35000

Current ratio 2.95

Interpretation- Based on the details above, it is analysed that company have current ratio is 2:95

which is close to ideal ratio. This result presents good performance of the business and able to

pay debt in shorter period of time. The optimal current ratio is essentially 2:1 that also indicates

that the organization has the double profit to cover the obligations. Therefore it can be observed

that the company will have fewer funds to pay its loans.

Quick ratio- This equation points out the balance between some of the current liabilities and the

immediate properties. This calculation = [current assets- (stock + accrued expenses)] / current

liability is determined too though. Below the Total Plc corporation's Quick Ratio for 2019 as

shown below:

Particular 2019 (in £)

Quick assets 57750

Current liabilities 35000

Quick ratio 1.65

Interpretation- Based from the above knowledge of the company's quick ratio, it can be

analyzed that quick ratio of the company is 1:65. It is good outcome that presents good liquidity

position of the business and near to ideal ratio. The company capable pay loan immediately

without any problem. The ideal fast ratio is essentially 1:1, which implies that the business ought

to have fast resources equal to the maximum obligations. Thus it can be perceived how the above

business does not have sufficient quick profit to cover its obligations.

Profitability ratio- there is a type of ratio being measured to determine the profit-generating

ability of a company. It also includes different kinds of ratios that are gross profit ratio, net profit

ratio, etc (Powers, Robinson and Stomberg, 2016). Below is Total's Plc profitability Ratio

following companies listed:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

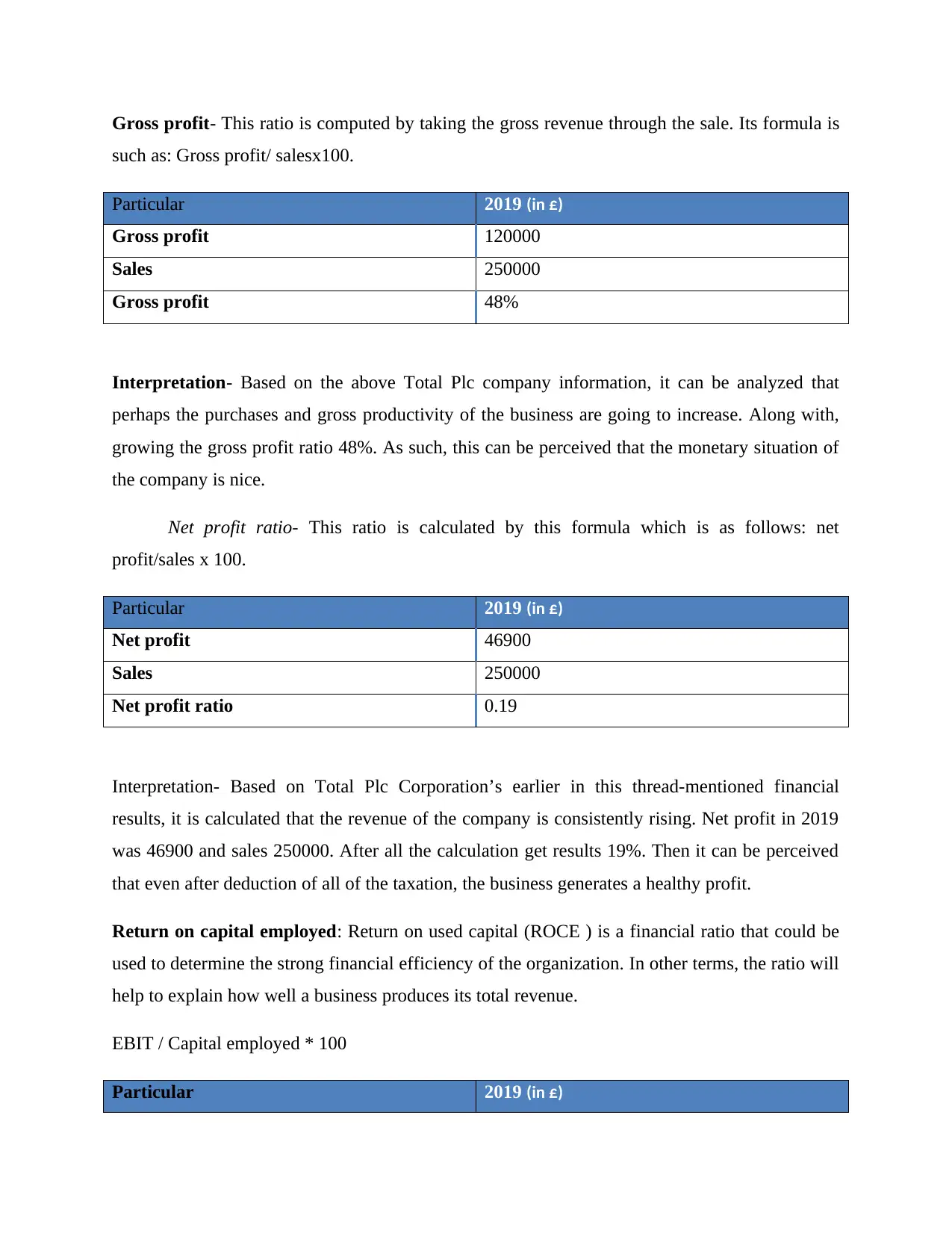

Gross profit- This ratio is computed by taking the gross revenue through the sale. Its formula is

such as: Gross profit/ salesx100.

Particular 2019 (in £)

Gross profit 120000

Sales 250000

Gross profit 48%

Interpretation- Based on the above Total Plc company information, it can be analyzed that

perhaps the purchases and gross productivity of the business are going to increase. Along with,

growing the gross profit ratio 48%. As such, this can be perceived that the monetary situation of

the company is nice.

Net profit ratio- This ratio is calculated by this formula which is as follows: net

profit/sales x 100.

Particular 2019 (in £)

Net profit 46900

Sales 250000

Net profit ratio 0.19

Interpretation- Based on Total Plc Corporation’s earlier in this thread-mentioned financial

results, it is calculated that the revenue of the company is consistently rising. Net profit in 2019

was 46900 and sales 250000. After all the calculation get results 19%. Then it can be perceived

that even after deduction of all of the taxation, the business generates a healthy profit.

Return on capital employed: Return on used capital (ROCE ) is a financial ratio that could be

used to determine the strong financial efficiency of the organization. In other terms, the ratio will

help to explain how well a business produces its total revenue.

EBIT / Capital employed * 100

Particular 2019 (in £)

such as: Gross profit/ salesx100.

Particular 2019 (in £)

Gross profit 120000

Sales 250000

Gross profit 48%

Interpretation- Based on the above Total Plc company information, it can be analyzed that

perhaps the purchases and gross productivity of the business are going to increase. Along with,

growing the gross profit ratio 48%. As such, this can be perceived that the monetary situation of

the company is nice.

Net profit ratio- This ratio is calculated by this formula which is as follows: net

profit/sales x 100.

Particular 2019 (in £)

Net profit 46900

Sales 250000

Net profit ratio 0.19

Interpretation- Based on Total Plc Corporation’s earlier in this thread-mentioned financial

results, it is calculated that the revenue of the company is consistently rising. Net profit in 2019

was 46900 and sales 250000. After all the calculation get results 19%. Then it can be perceived

that even after deduction of all of the taxation, the business generates a healthy profit.

Return on capital employed: Return on used capital (ROCE ) is a financial ratio that could be

used to determine the strong financial efficiency of the organization. In other terms, the ratio will

help to explain how well a business produces its total revenue.

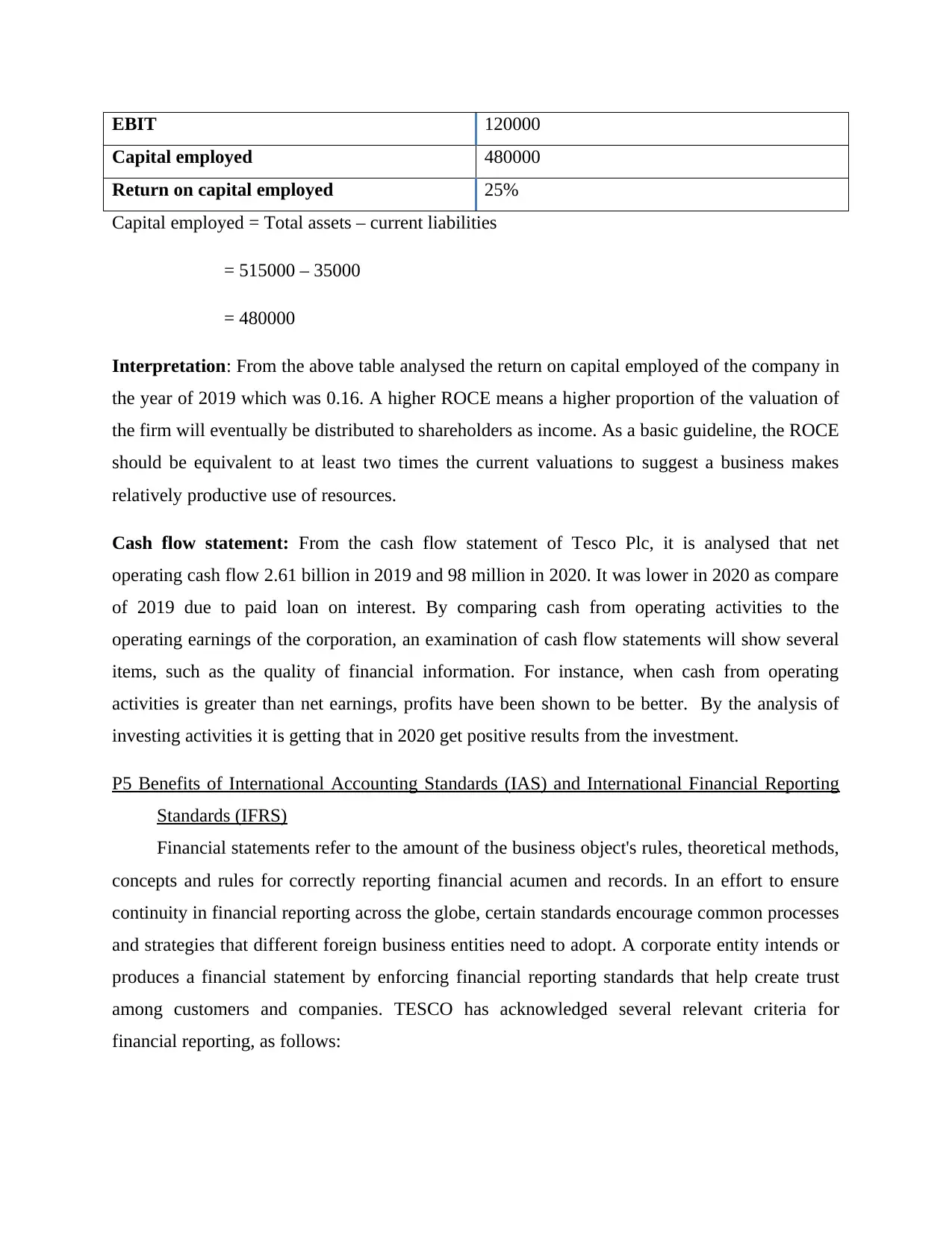

EBIT / Capital employed * 100

Particular 2019 (in £)

EBIT 120000

Capital employed 480000

Return on capital employed 25%

Capital employed = Total assets – current liabilities

= 515000 – 35000

= 480000

Interpretation: From the above table analysed the return on capital employed of the company in

the year of 2019 which was 0.16. A higher ROCE means a higher proportion of the valuation of

the firm will eventually be distributed to shareholders as income. As a basic guideline, the ROCE

should be equivalent to at least two times the current valuations to suggest a business makes

relatively productive use of resources.

Cash flow statement: From the cash flow statement of Tesco Plc, it is analysed that net

operating cash flow 2.61 billion in 2019 and 98 million in 2020. It was lower in 2020 as compare

of 2019 due to paid loan on interest. By comparing cash from operating activities to the

operating earnings of the corporation, an examination of cash flow statements will show several

items, such as the quality of financial information. For instance, when cash from operating

activities is greater than net earnings, profits have been shown to be better. By the analysis of

investing activities it is getting that in 2020 get positive results from the investment.

P5 Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS)

Financial statements refer to the amount of the business object's rules, theoretical methods,

concepts and rules for correctly reporting financial acumen and records. In an effort to ensure

continuity in financial reporting across the globe, certain standards encourage common processes

and strategies that different foreign business entities need to adopt. A corporate entity intends or

produces a financial statement by enforcing financial reporting standards that help create trust

among customers and companies. TESCO has acknowledged several relevant criteria for

financial reporting, as follows:

Capital employed 480000

Return on capital employed 25%

Capital employed = Total assets – current liabilities

= 515000 – 35000

= 480000

Interpretation: From the above table analysed the return on capital employed of the company in

the year of 2019 which was 0.16. A higher ROCE means a higher proportion of the valuation of

the firm will eventually be distributed to shareholders as income. As a basic guideline, the ROCE

should be equivalent to at least two times the current valuations to suggest a business makes

relatively productive use of resources.

Cash flow statement: From the cash flow statement of Tesco Plc, it is analysed that net

operating cash flow 2.61 billion in 2019 and 98 million in 2020. It was lower in 2020 as compare

of 2019 due to paid loan on interest. By comparing cash from operating activities to the

operating earnings of the corporation, an examination of cash flow statements will show several

items, such as the quality of financial information. For instance, when cash from operating

activities is greater than net earnings, profits have been shown to be better. By the analysis of

investing activities it is getting that in 2020 get positive results from the investment.

P5 Benefits of International Accounting Standards (IAS) and International Financial Reporting

Standards (IFRS)

Financial statements refer to the amount of the business object's rules, theoretical methods,

concepts and rules for correctly reporting financial acumen and records. In an effort to ensure

continuity in financial reporting across the globe, certain standards encourage common processes

and strategies that different foreign business entities need to adopt. A corporate entity intends or

produces a financial statement by enforcing financial reporting standards that help create trust

among customers and companies. TESCO has acknowledged several relevant criteria for

financial reporting, as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.