Financial Reporting Analysis: IFRS, Financial Ratios, and Stakeholders

VerifiedAdded on 2020/07/22

|17

|4508

|325

Report

AI Summary

This report provides a detailed analysis of financial reporting, beginning with an introduction to its context and objectives. It outlines the conceptual and regulatory framework, emphasizing qualitative characteristics that enhance the reliability of financial statements. The report identifies key stakeholders, explaining the benefits of financial information to each group, such as investors, creditors, employees, and shareholders. It assesses the value of financial reporting in meeting organizational objectives and fostering market growth. Furthermore, it presents financial statements, including the income statement, statement of changes in equity, and statement of financial position for ROB plc. The report then interprets the financial performance of Marks & Spencer using various financial ratios and explains the differences between IAS and IFRS, evaluating the advantages of IFRS and factors affecting its compliance worldwide. The report concludes with a summary of the key findings and a list of references.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

1. Outlining context and objective of FR...............................................................................1

2. Requirement of Conceptual and regulatory framework and Qualitative information that

make financial statements more reliable................................................................................2

3. Identifying key stakeholders Along with explaining benefits of information to them.......3

4. Assessing financial reporting's value to meet objectives of organisation and grow in market

................................................................................................................................................4

5. Presentation of financial statements...................................................................................5

6. Interpretation of financial performance of Marks & Spencer with the help of some financial

ratios.......................................................................................................................................7

7. Explaining difference among IAS as well as IFRS..........................................................11

8. Evaluation of benefits or advantages of IFRS..................................................................11

9. Factors affecting compliance with IFRS across the world...............................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

1. Outlining context and objective of FR...............................................................................1

2. Requirement of Conceptual and regulatory framework and Qualitative information that

make financial statements more reliable................................................................................2

3. Identifying key stakeholders Along with explaining benefits of information to them.......3

4. Assessing financial reporting's value to meet objectives of organisation and grow in market

................................................................................................................................................4

5. Presentation of financial statements...................................................................................5

6. Interpretation of financial performance of Marks & Spencer with the help of some financial

ratios.......................................................................................................................................7

7. Explaining difference among IAS as well as IFRS..........................................................11

8. Evaluation of benefits or advantages of IFRS..................................................................11

9. Factors affecting compliance with IFRS across the world...............................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION

A business operating its activities on regular basis, needs to prepare and produce its

financial reports at the end of each financial year. It is essential for every organisation whether

from service industry or manufacturing industry. These reports provide financial information to

its internal as well as external users that enables them in taking economic decisions for future.

This also helps in identifying and analysing an entity's liquidity, solvency, profitability and

financial position. It mainly includes statements such as income statement, Statement of financial

position, cash flow statement and statement of changes in equity. In the present report conceptual

and regulatory framework of financial statements has been provided with explaining qualitative

characteristics and preparation of financial statements for ROB plc along with explaining

application of and difference between IFRS and IASB.

1. Outlining context and objective of FR

Financial reporting is considered as one of the pivotal aspect within every organisation

where it supports to analyse financial transactions come into consideration. When such values

are properly tracked within firm then management able to know performance in the market

where it operates. There are some objectives and purposes due to which accountants apply FR

within working environment. Some basic as well as key objectives due to which FR used are

such as follows:

FR helps to the manager for assessing as well as tracking all the transactions related to

financial aspects occur within firm. Such things are like profit, revenue, income, return

on investment, indirect costs, liquidity condition, expenses etc (Nandwa, 2016). If level

of total costs is the low as compared to targeted then firm able to make beneficial

strategies and resolve this issue.

In order to prepare financial plans, apply at the workplace, evaluate, monitor as well as

execute then FR is one of the highly supportive concept. Due to this, financial objectives

will be achieved easily and business performance will be enhanced as well.

FR helps to disclose receipts and payments made within one accounting period in front of

internal stakeholders. Therefore, decisions for making investment and doing expenses can

be made in profitable manner.

1

A business operating its activities on regular basis, needs to prepare and produce its

financial reports at the end of each financial year. It is essential for every organisation whether

from service industry or manufacturing industry. These reports provide financial information to

its internal as well as external users that enables them in taking economic decisions for future.

This also helps in identifying and analysing an entity's liquidity, solvency, profitability and

financial position. It mainly includes statements such as income statement, Statement of financial

position, cash flow statement and statement of changes in equity. In the present report conceptual

and regulatory framework of financial statements has been provided with explaining qualitative

characteristics and preparation of financial statements for ROB plc along with explaining

application of and difference between IFRS and IASB.

1. Outlining context and objective of FR

Financial reporting is considered as one of the pivotal aspect within every organisation

where it supports to analyse financial transactions come into consideration. When such values

are properly tracked within firm then management able to know performance in the market

where it operates. There are some objectives and purposes due to which accountants apply FR

within working environment. Some basic as well as key objectives due to which FR used are

such as follows:

FR helps to the manager for assessing as well as tracking all the transactions related to

financial aspects occur within firm. Such things are like profit, revenue, income, return

on investment, indirect costs, liquidity condition, expenses etc (Nandwa, 2016). If level

of total costs is the low as compared to targeted then firm able to make beneficial

strategies and resolve this issue.

In order to prepare financial plans, apply at the workplace, evaluate, monitor as well as

execute then FR is one of the highly supportive concept. Due to this, financial objectives

will be achieved easily and business performance will be enhanced as well.

FR helps to disclose receipts and payments made within one accounting period in front of

internal stakeholders. Therefore, decisions for making investment and doing expenses can

be made in profitable manner.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Considering and applying FR within working environment, entrepreneur can assess that

business is up to which level financially sound (Objectives of financial reporting, 2015).

On the basis of this, plans and strategies made for improving financial performance.

Apart from this, for representing assets, liabilities, capital funded by owner etc. among

stakeholders of business also FR is taken into consideration.

2. Requirement of Conceptual and regulatory framework and Qualitative information that make

financial statements more reliable

Conceptual framework on financial accounting provides purpose and nature of

accounting. Conceptual framework need to consider conceptual and theoretical issues that are

surrounded to financial reporting along with formulating consistent foundation that provides aid

to development of accounting standards. In the context of financial reporting it can also be seen

as Generally Accepted Accounting Principles that provides evaluation of existing practices along

with development of new and improved practices (Conceptual Framework for Financial

Reporting, 2017). It also provides basis on how financial information should be communicated

and presented to its potential users.

Following are the contents of conceptual and regulatory framework:

Identification of objectives of financial statements: The Framework helps in identifying

objectives of preparation of financial statements. It can be summarised as follows:

Foremost objective of financial reporting is to provide relevant information to its users that are

potential investors, creditors and other lenders and stakeholders (Ahmed, Neel and Wang, 2013).

The information is used by the users to make future economic decisions regarding selling,

buying or holding equity. Through financial reporting information regarding entity's resources

can be assessed along with analysing efficiency of management responsibilities.

Reporting entity: An entity is said to be a reporting entity when its financial information and

financial statements is helpful for its users and significantly affects their decisions i.e. in order to

make economic decisions users rely over entity's financial information, such entity is regarded as

reporting entity as per conceptual and regulatory framework of financial accounting

(Brüggemann, Hitz and Sellhorn, 2013).

2

business is up to which level financially sound (Objectives of financial reporting, 2015).

On the basis of this, plans and strategies made for improving financial performance.

Apart from this, for representing assets, liabilities, capital funded by owner etc. among

stakeholders of business also FR is taken into consideration.

2. Requirement of Conceptual and regulatory framework and Qualitative information that make

financial statements more reliable

Conceptual framework on financial accounting provides purpose and nature of

accounting. Conceptual framework need to consider conceptual and theoretical issues that are

surrounded to financial reporting along with formulating consistent foundation that provides aid

to development of accounting standards. In the context of financial reporting it can also be seen

as Generally Accepted Accounting Principles that provides evaluation of existing practices along

with development of new and improved practices (Conceptual Framework for Financial

Reporting, 2017). It also provides basis on how financial information should be communicated

and presented to its potential users.

Following are the contents of conceptual and regulatory framework:

Identification of objectives of financial statements: The Framework helps in identifying

objectives of preparation of financial statements. It can be summarised as follows:

Foremost objective of financial reporting is to provide relevant information to its users that are

potential investors, creditors and other lenders and stakeholders (Ahmed, Neel and Wang, 2013).

The information is used by the users to make future economic decisions regarding selling,

buying or holding equity. Through financial reporting information regarding entity's resources

can be assessed along with analysing efficiency of management responsibilities.

Reporting entity: An entity is said to be a reporting entity when its financial information and

financial statements is helpful for its users and significantly affects their decisions i.e. in order to

make economic decisions users rely over entity's financial information, such entity is regarded as

reporting entity as per conceptual and regulatory framework of financial accounting

(Brüggemann, Hitz and Sellhorn, 2013).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Further, it also provides framework on qualitative characteristics that useful financial

information should possess:

Qualitative characteristics helps in identifying the type of information that are likely to be

most useful to its users for making economic decisions. Following are the characteristics:

Relevance: as per the framework, the information that is been presented in financial statements

must be relevant for its users i.e. it must be related to the reporting entity. An information is said

to be relevant when it contains confirmatory value, predictive value or both. These values can

significantly arise difference in the decisions of users.

Materiality: Information must be material i.e. only that data should be presented in reports that is

material or important to the organisation in terms of either Qualitative or quantitative (Ignore and

Kusa, 2013). For example, a transaction of £10, cannot affect the profitability of company if

presented in financial reports or not hence, it can be said that the information is not material.

Faithful Representation: This refers to that economic phenomena of accounting information i.e.

number and words must provide true and fair view along with being free from misstatements.

Verifiability: Financial reports must have the characteristic of communicating underlying

economics of the company's business.

Comparability: The usefulness of financial information will increase if they would be

comparable with the information of other entity or with the past year information so that

performance can be evaluated.

Understandability: It should be presented in such a form that can enable a reader having nominal

knowledge to easily comprehend it.

3. Identifying key stakeholders Along with explaining benefits of information to them

Key stakeholder is any person who is directly or indirectly affected by the decision

making and functioning of organisations activities and operations. In other words, person that

have vested their interest in an entity in any form are referred as organisation's main

stakeholders. These can be classified as follows:

External Stakeholders

3

information should possess:

Qualitative characteristics helps in identifying the type of information that are likely to be

most useful to its users for making economic decisions. Following are the characteristics:

Relevance: as per the framework, the information that is been presented in financial statements

must be relevant for its users i.e. it must be related to the reporting entity. An information is said

to be relevant when it contains confirmatory value, predictive value or both. These values can

significantly arise difference in the decisions of users.

Materiality: Information must be material i.e. only that data should be presented in reports that is

material or important to the organisation in terms of either Qualitative or quantitative (Ignore and

Kusa, 2013). For example, a transaction of £10, cannot affect the profitability of company if

presented in financial reports or not hence, it can be said that the information is not material.

Faithful Representation: This refers to that economic phenomena of accounting information i.e.

number and words must provide true and fair view along with being free from misstatements.

Verifiability: Financial reports must have the characteristic of communicating underlying

economics of the company's business.

Comparability: The usefulness of financial information will increase if they would be

comparable with the information of other entity or with the past year information so that

performance can be evaluated.

Understandability: It should be presented in such a form that can enable a reader having nominal

knowledge to easily comprehend it.

3. Identifying key stakeholders Along with explaining benefits of information to them

Key stakeholder is any person who is directly or indirectly affected by the decision

making and functioning of organisations activities and operations. In other words, person that

have vested their interest in an entity in any form are referred as organisation's main

stakeholders. These can be classified as follows:

External Stakeholders

3

Creditors and other Investors: These individuals have provided goods on credit basis to the

business entity or have provided their money as loan to the entity (Brigham, 2014.). Therefore,

knowing liquidity position and solvency position of the company is important to them in order to

determine whether t will be able to refund their money within stipulated time.

Local Authority and Government: Government of the country in which the business is operating

is also a key stakeholder in order to determine profitability to secure its taxation revenue. Also,

to ensure that the policies of company is adhered to required regulations and legislations.

Customers: Customers are those stakeholders that can either make or break the company. An

organisation to become successful need to consider expectations and requirements of its

customers along with fulfilling customer satisfaction.

Internal Stakeholders

Employees: Employees are the main pillars of company, without whom a business cannot

operate its functions efficiently (Bonetti, Magnan and Parbonetti, 2016). The only interest they

have vested in company is their salaries. They assess financial information to determine whether

the company is in position to pay off their salaries on time or not.

Shareholders: Shareholders are considered as owners of business they are only interested in

knowing profit earning ability of an entity.

Following are the benefits of financial information to stakeholders:

Identification of earning capacity of business.

To get an idea about company's future plans, tactics and strategies.

To determine the value of assets and liabilities that a business possess.

To determine entity's liquidity, solvency and profitability position.

4. Assessing financial reporting's value to meet objectives of organisation and grow in market

A concept in which various kinds of financial transactions are recorded, analysed and

final accounts are prepared is known as financial reporting. It provides opportunity to managers

as well as accountants for assessing each and every transaction comes into consideration at the

workplace. During this, if any kind of problem or malpractices seen then firm able to make

strategies for resolving it. Considering to financial reporting, the firm able to prepare all the

4

business entity or have provided their money as loan to the entity (Brigham, 2014.). Therefore,

knowing liquidity position and solvency position of the company is important to them in order to

determine whether t will be able to refund their money within stipulated time.

Local Authority and Government: Government of the country in which the business is operating

is also a key stakeholder in order to determine profitability to secure its taxation revenue. Also,

to ensure that the policies of company is adhered to required regulations and legislations.

Customers: Customers are those stakeholders that can either make or break the company. An

organisation to become successful need to consider expectations and requirements of its

customers along with fulfilling customer satisfaction.

Internal Stakeholders

Employees: Employees are the main pillars of company, without whom a business cannot

operate its functions efficiently (Bonetti, Magnan and Parbonetti, 2016). The only interest they

have vested in company is their salaries. They assess financial information to determine whether

the company is in position to pay off their salaries on time or not.

Shareholders: Shareholders are considered as owners of business they are only interested in

knowing profit earning ability of an entity.

Following are the benefits of financial information to stakeholders:

Identification of earning capacity of business.

To get an idea about company's future plans, tactics and strategies.

To determine the value of assets and liabilities that a business possess.

To determine entity's liquidity, solvency and profitability position.

4. Assessing financial reporting's value to meet objectives of organisation and grow in market

A concept in which various kinds of financial transactions are recorded, analysed and

final accounts are prepared is known as financial reporting. It provides opportunity to managers

as well as accountants for assessing each and every transaction comes into consideration at the

workplace. During this, if any kind of problem or malpractices seen then firm able to make

strategies for resolving it. Considering to financial reporting, the firm able to prepare all the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

accounts properly along with in the appropriate structure (Ball, Jayaraman and Shivakumar,

2012).

Once the financials are appropriately structured then performance of whole business can

be easily determined in the industry where it has presence. Due to this specific procedure, actual

business performance can be interpreted where correction actions taken, if required then. On the

basis of this, management able to meet aims and objectives which are prepared while preparing

financial plans or operating in the market. For instance: with the help of financial reporting, firm

able to known profitability position along with making comparison with the last accounting

period. Herein, if low or negligible growth evaluated then strategies for managing cost and

enhancing profit will be applied. Therefore, objectives will be achieved easily which is clear sign

of grow in the market.

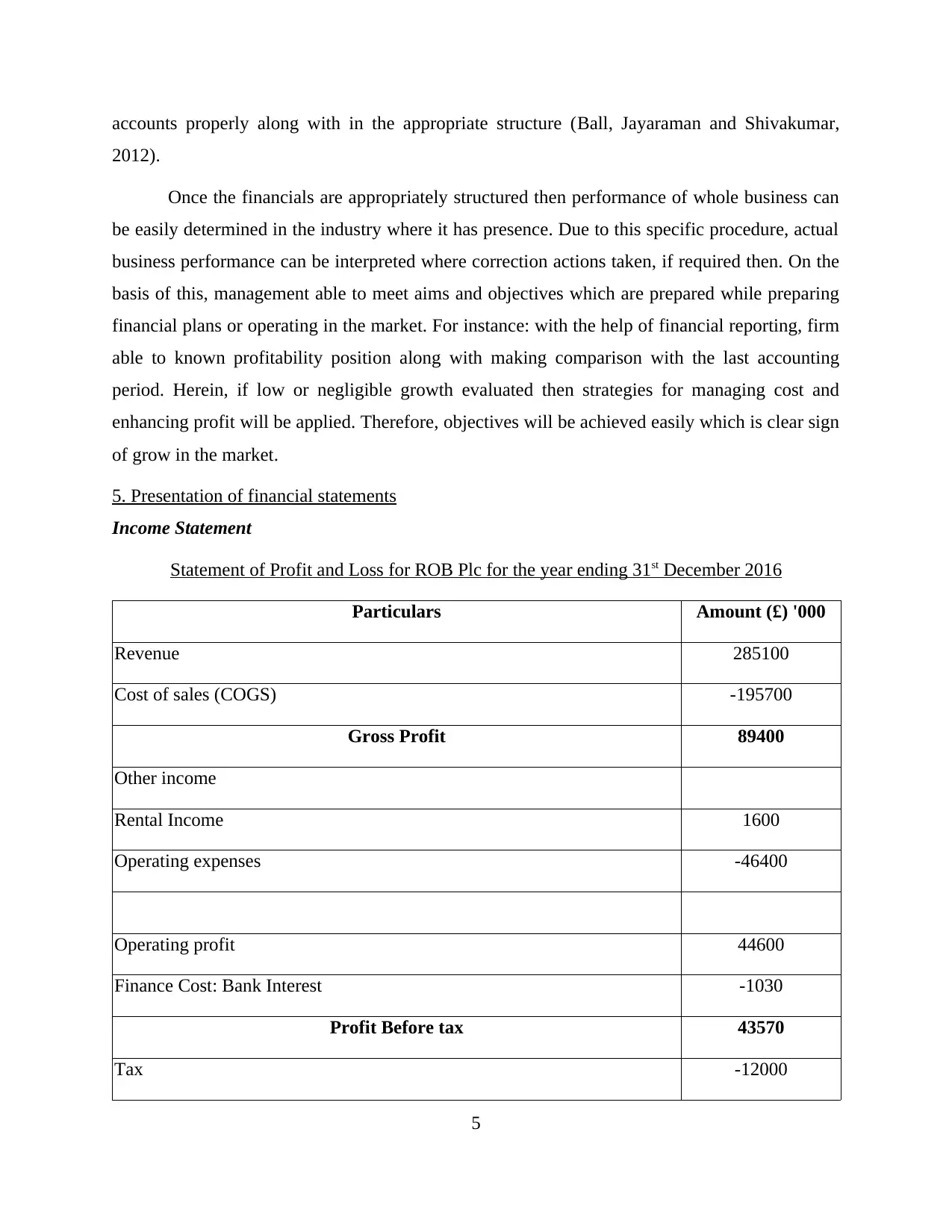

5. Presentation of financial statements

Income Statement

Statement of Profit and Loss for ROB Plc for the year ending 31st December 2016

Particulars Amount (£) '000

Revenue 285100

Cost of sales (COGS) -195700

Gross Profit 89400

Other income

Rental Income 1600

Operating expenses -46400

Operating profit 44600

Finance Cost: Bank Interest -1030

Profit Before tax 43570

Tax -12000

5

2012).

Once the financials are appropriately structured then performance of whole business can

be easily determined in the industry where it has presence. Due to this specific procedure, actual

business performance can be interpreted where correction actions taken, if required then. On the

basis of this, management able to meet aims and objectives which are prepared while preparing

financial plans or operating in the market. For instance: with the help of financial reporting, firm

able to known profitability position along with making comparison with the last accounting

period. Herein, if low or negligible growth evaluated then strategies for managing cost and

enhancing profit will be applied. Therefore, objectives will be achieved easily which is clear sign

of grow in the market.

5. Presentation of financial statements

Income Statement

Statement of Profit and Loss for ROB Plc for the year ending 31st December 2016

Particulars Amount (£) '000

Revenue 285100

Cost of sales (COGS) -195700

Gross Profit 89400

Other income

Rental Income 1600

Operating expenses -46400

Operating profit 44600

Finance Cost: Bank Interest -1030

Profit Before tax 43570

Tax -12000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Profit for the Year 31570

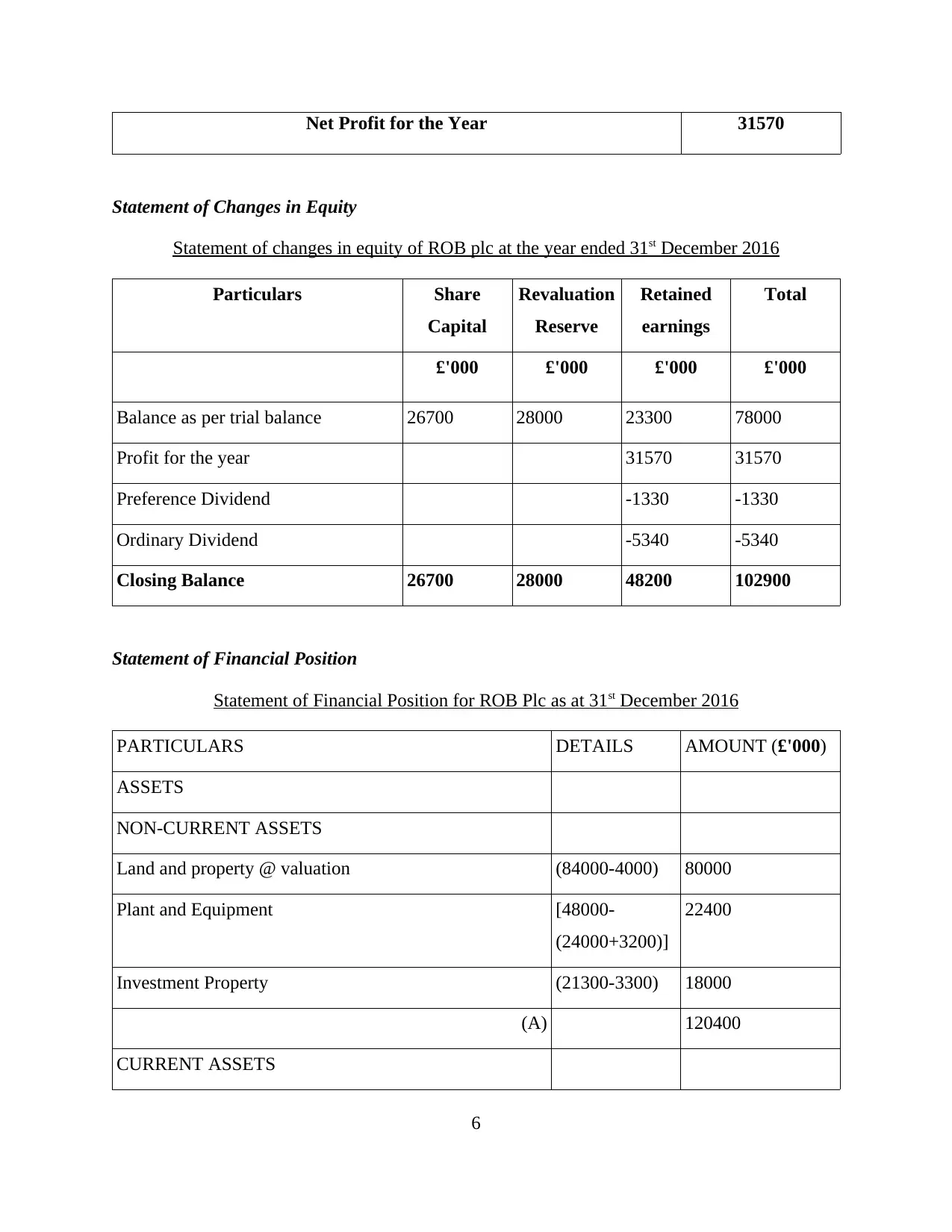

Statement of Changes in Equity

Statement of changes in equity of ROB plc at the year ended 31st December 2016

Particulars Share

Capital

Revaluation

Reserve

Retained

earnings

Total

£'000 £'000 £'000 £'000

Balance as per trial balance 26700 28000 23300 78000

Profit for the year 31570 31570

Preference Dividend -1330 -1330

Ordinary Dividend -5340 -5340

Closing Balance 26700 28000 48200 102900

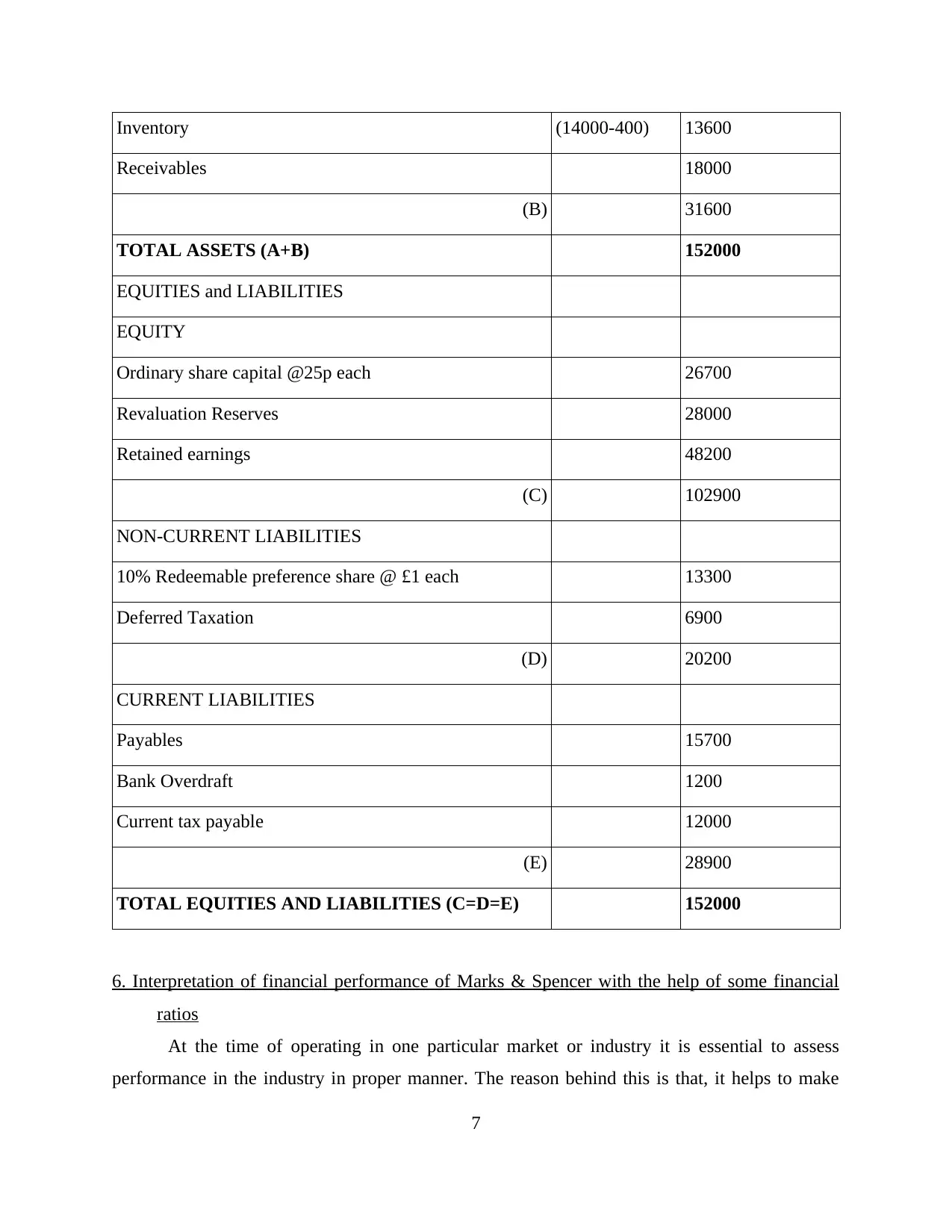

Statement of Financial Position

Statement of Financial Position for ROB Plc as at 31st December 2016

PARTICULARS DETAILS AMOUNT (£'000)

ASSETS

NON-CURRENT ASSETS

Land and property @ valuation (84000-4000) 80000

Plant and Equipment [48000-

(24000+3200)]

22400

Investment Property (21300-3300) 18000

(A) 120400

CURRENT ASSETS

6

Statement of Changes in Equity

Statement of changes in equity of ROB plc at the year ended 31st December 2016

Particulars Share

Capital

Revaluation

Reserve

Retained

earnings

Total

£'000 £'000 £'000 £'000

Balance as per trial balance 26700 28000 23300 78000

Profit for the year 31570 31570

Preference Dividend -1330 -1330

Ordinary Dividend -5340 -5340

Closing Balance 26700 28000 48200 102900

Statement of Financial Position

Statement of Financial Position for ROB Plc as at 31st December 2016

PARTICULARS DETAILS AMOUNT (£'000)

ASSETS

NON-CURRENT ASSETS

Land and property @ valuation (84000-4000) 80000

Plant and Equipment [48000-

(24000+3200)]

22400

Investment Property (21300-3300) 18000

(A) 120400

CURRENT ASSETS

6

Inventory (14000-400) 13600

Receivables 18000

(B) 31600

TOTAL ASSETS (A+B) 152000

EQUITIES and LIABILITIES

EQUITY

Ordinary share capital @25p each 26700

Revaluation Reserves 28000

Retained earnings 48200

(C) 102900

NON-CURRENT LIABILITIES

10% Redeemable preference share @ £1 each 13300

Deferred Taxation 6900

(D) 20200

CURRENT LIABILITIES

Payables 15700

Bank Overdraft 1200

Current tax payable 12000

(E) 28900

TOTAL EQUITIES AND LIABILITIES (C=D=E) 152000

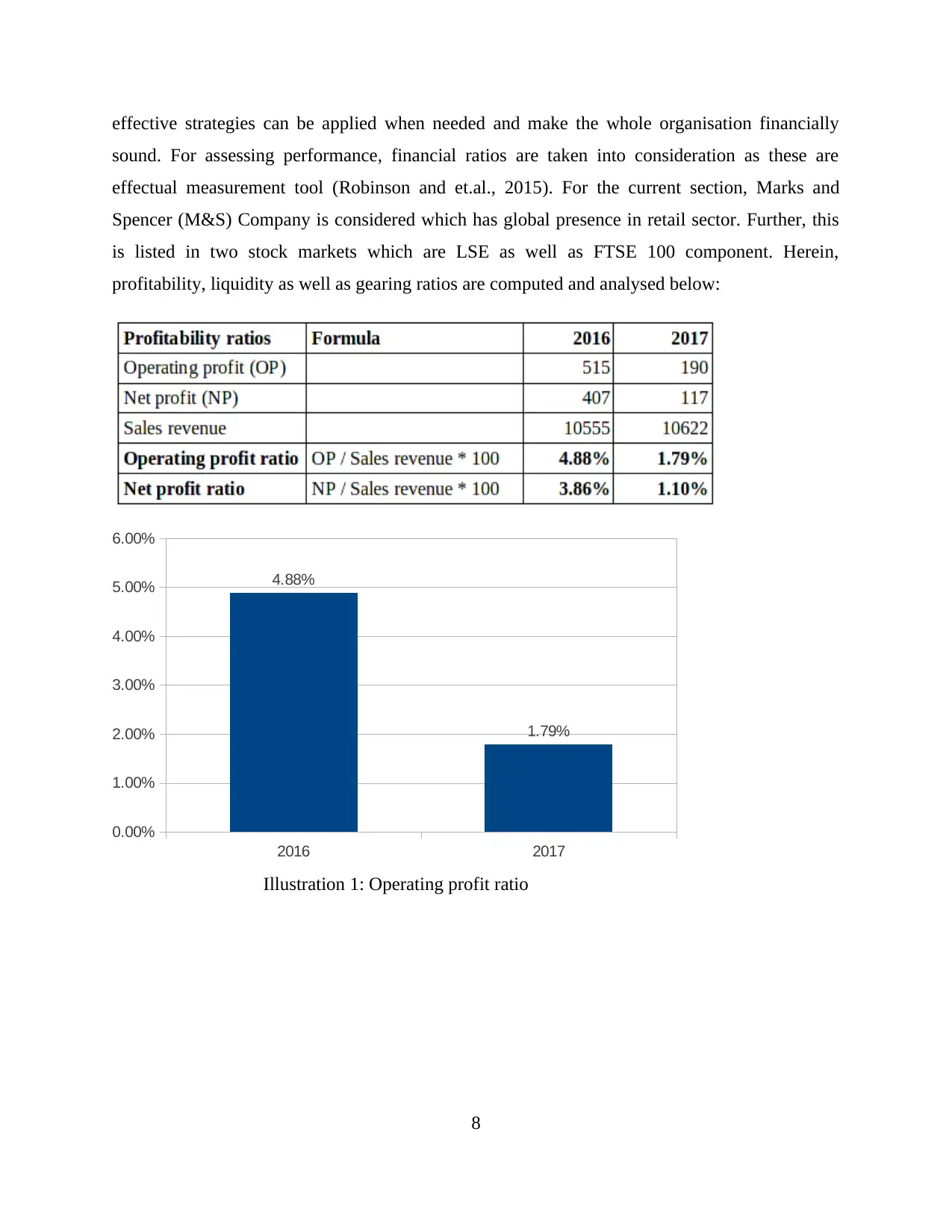

6. Interpretation of financial performance of Marks & Spencer with the help of some financial

ratios

At the time of operating in one particular market or industry it is essential to assess

performance in the industry in proper manner. The reason behind this is that, it helps to make

7

Receivables 18000

(B) 31600

TOTAL ASSETS (A+B) 152000

EQUITIES and LIABILITIES

EQUITY

Ordinary share capital @25p each 26700

Revaluation Reserves 28000

Retained earnings 48200

(C) 102900

NON-CURRENT LIABILITIES

10% Redeemable preference share @ £1 each 13300

Deferred Taxation 6900

(D) 20200

CURRENT LIABILITIES

Payables 15700

Bank Overdraft 1200

Current tax payable 12000

(E) 28900

TOTAL EQUITIES AND LIABILITIES (C=D=E) 152000

6. Interpretation of financial performance of Marks & Spencer with the help of some financial

ratios

At the time of operating in one particular market or industry it is essential to assess

performance in the industry in proper manner. The reason behind this is that, it helps to make

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

effective strategies can be applied when needed and make the whole organisation financially

sound. For assessing performance, financial ratios are taken into consideration as these are

effectual measurement tool (Robinson and et.al., 2015). For the current section, Marks and

Spencer (M&S) Company is considered which has global presence in retail sector. Further, this

is listed in two stock markets which are LSE as well as FTSE 100 component. Herein,

profitability, liquidity as well as gearing ratios are computed and analysed below:

2016 2017

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

4.88%

1.79%

Illustration 1: Operating profit ratio

8

sound. For assessing performance, financial ratios are taken into consideration as these are

effectual measurement tool (Robinson and et.al., 2015). For the current section, Marks and

Spencer (M&S) Company is considered which has global presence in retail sector. Further, this

is listed in two stock markets which are LSE as well as FTSE 100 component. Herein,

profitability, liquidity as well as gearing ratios are computed and analysed below:

2016 2017

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

4.88%

1.79%

Illustration 1: Operating profit ratio

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

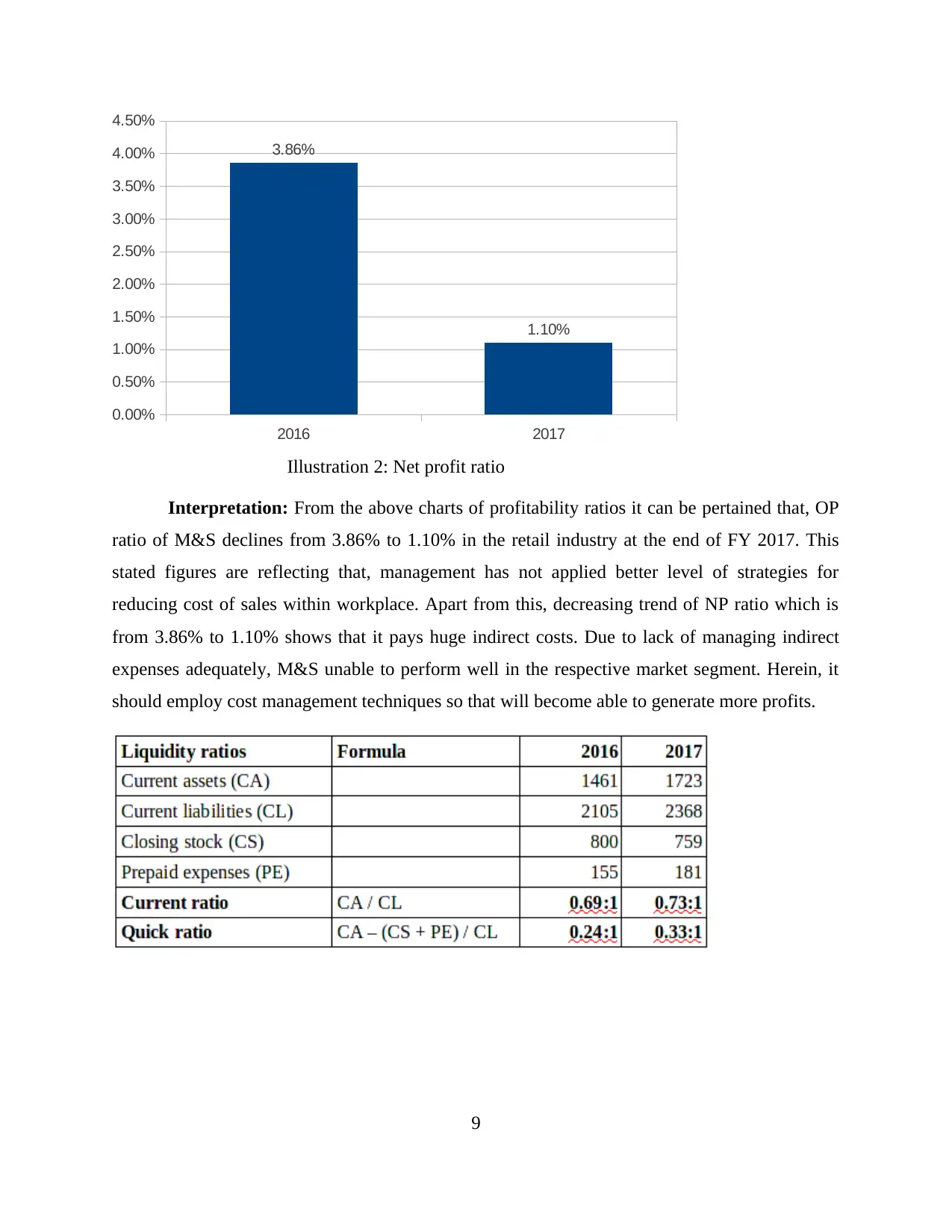

2016 2017

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

3.86%

1.10%

Illustration 2: Net profit ratio

Interpretation: From the above charts of profitability ratios it can be pertained that, OP

ratio of M&S declines from 3.86% to 1.10% in the retail industry at the end of FY 2017. This

stated figures are reflecting that, management has not applied better level of strategies for

reducing cost of sales within workplace. Apart from this, decreasing trend of NP ratio which is

from 3.86% to 1.10% shows that it pays huge indirect costs. Due to lack of managing indirect

expenses adequately, M&S unable to perform well in the respective market segment. Herein, it

should employ cost management techniques so that will become able to generate more profits.

9

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

4.00%

4.50%

3.86%

1.10%

Illustration 2: Net profit ratio

Interpretation: From the above charts of profitability ratios it can be pertained that, OP

ratio of M&S declines from 3.86% to 1.10% in the retail industry at the end of FY 2017. This

stated figures are reflecting that, management has not applied better level of strategies for

reducing cost of sales within workplace. Apart from this, decreasing trend of NP ratio which is

from 3.86% to 1.10% shows that it pays huge indirect costs. Due to lack of managing indirect

expenses adequately, M&S unable to perform well in the respective market segment. Herein, it

should employ cost management techniques so that will become able to generate more profits.

9

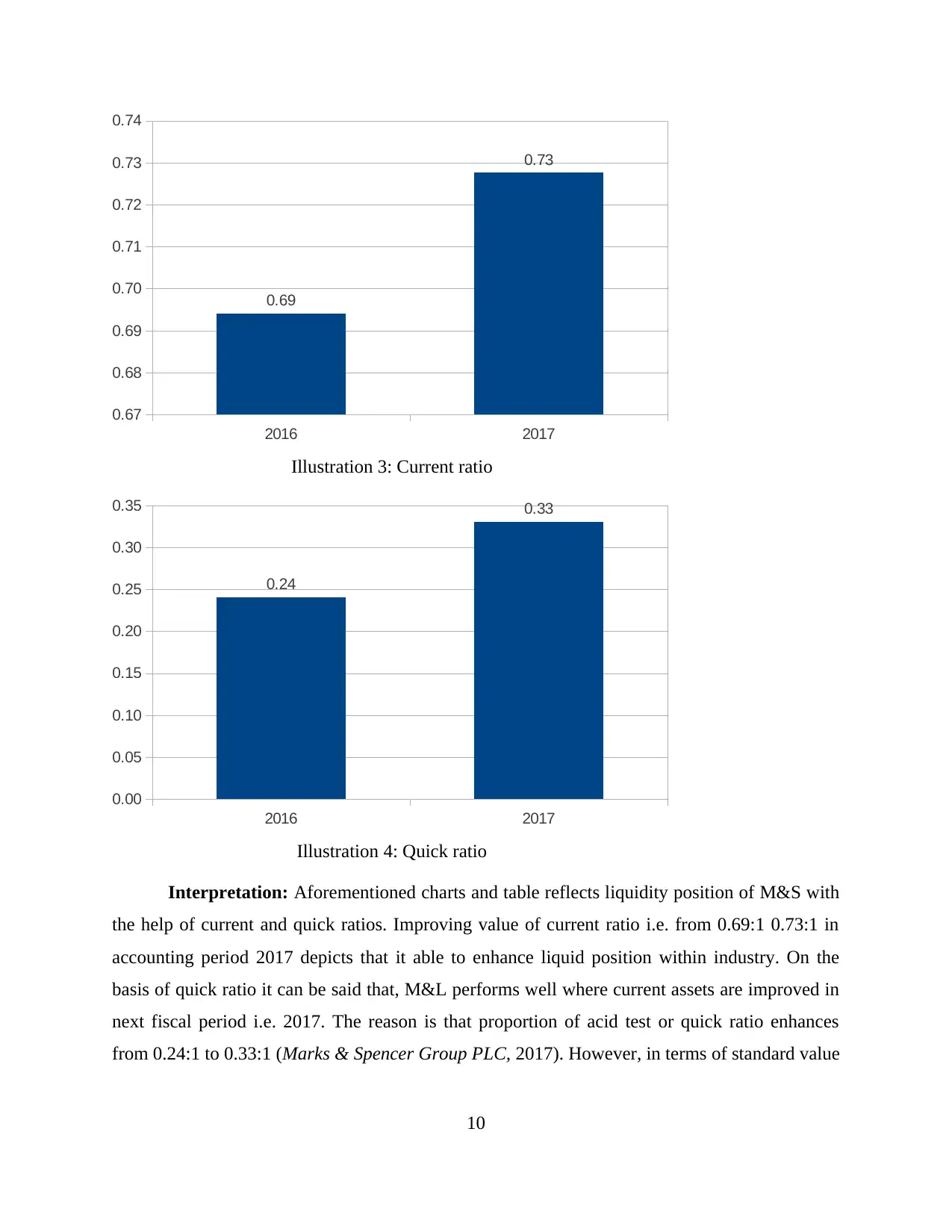

2016 2017

0.67

0.68

0.69

0.70

0.71

0.72

0.73

0.74

0.69

0.73

Illustration 3: Current ratio

2016 2017

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.24

0.33

Illustration 4: Quick ratio

Interpretation: Aforementioned charts and table reflects liquidity position of M&S with

the help of current and quick ratios. Improving value of current ratio i.e. from 0.69:1 0.73:1 in

accounting period 2017 depicts that it able to enhance liquid position within industry. On the

basis of quick ratio it can be said that, M&L performs well where current assets are improved in

next fiscal period i.e. 2017. The reason is that proportion of acid test or quick ratio enhances

from 0.24:1 to 0.33:1 (Marks & Spencer Group PLC, 2017). However, in terms of standard value

10

0.67

0.68

0.69

0.70

0.71

0.72

0.73

0.74

0.69

0.73

Illustration 3: Current ratio

2016 2017

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.24

0.33

Illustration 4: Quick ratio

Interpretation: Aforementioned charts and table reflects liquidity position of M&S with

the help of current and quick ratios. Improving value of current ratio i.e. from 0.69:1 0.73:1 in

accounting period 2017 depicts that it able to enhance liquid position within industry. On the

basis of quick ratio it can be said that, M&L performs well where current assets are improved in

next fiscal period i.e. 2017. The reason is that proportion of acid test or quick ratio enhances

from 0.24:1 to 0.33:1 (Marks & Spencer Group PLC, 2017). However, in terms of standard value

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.