Analysis of Financial Ratios in Corporate Management

VerifiedAdded on 2020/04/15

|15

|3422

|72

AI Summary

The assignment provides an analysis of essential financial metrics such as Return on Assets (ROA), which measures profitability relative to total assets, indicating efficient asset utilization. It also covers valuation models like Discounted Cash Flow (DCF) that project future cash flows and discount them back to present value to determine a company's intrinsic worth. The Internal Rate of Return (IRR) is discussed as another critical tool for evaluating investment efficiency. These methodologies are crucial for investors and analysts in understanding and predicting business performance, aiding strategic decision-making and risk assessment.

Running head: FINANCIAL REPORTING OF BUSINESS

Financial reporting of business

Name of the student

Name of the university

Author note

Financial reporting of business

Name of the student

Name of the university

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL REPORTING OF BUSINESS

Table of Contents

Part (a)........................................................................................................................................2

Ratio calculation.........................................................................................................................2

Part (b)........................................................................................................................................5

Analysis of ratio.........................................................................................................................5

Part (c)......................................................................................................................................10

Reporting on plant, property and equipment............................................................................10

Reference..................................................................................................................................13

Table of Contents

Part (a)........................................................................................................................................2

Ratio calculation.........................................................................................................................2

Part (b)........................................................................................................................................5

Analysis of ratio.........................................................................................................................5

Part (c)......................................................................................................................................10

Reporting on plant, property and equipment............................................................................10

Reference..................................................................................................................................13

2FINANCIAL REPORTING OF BUSINESS

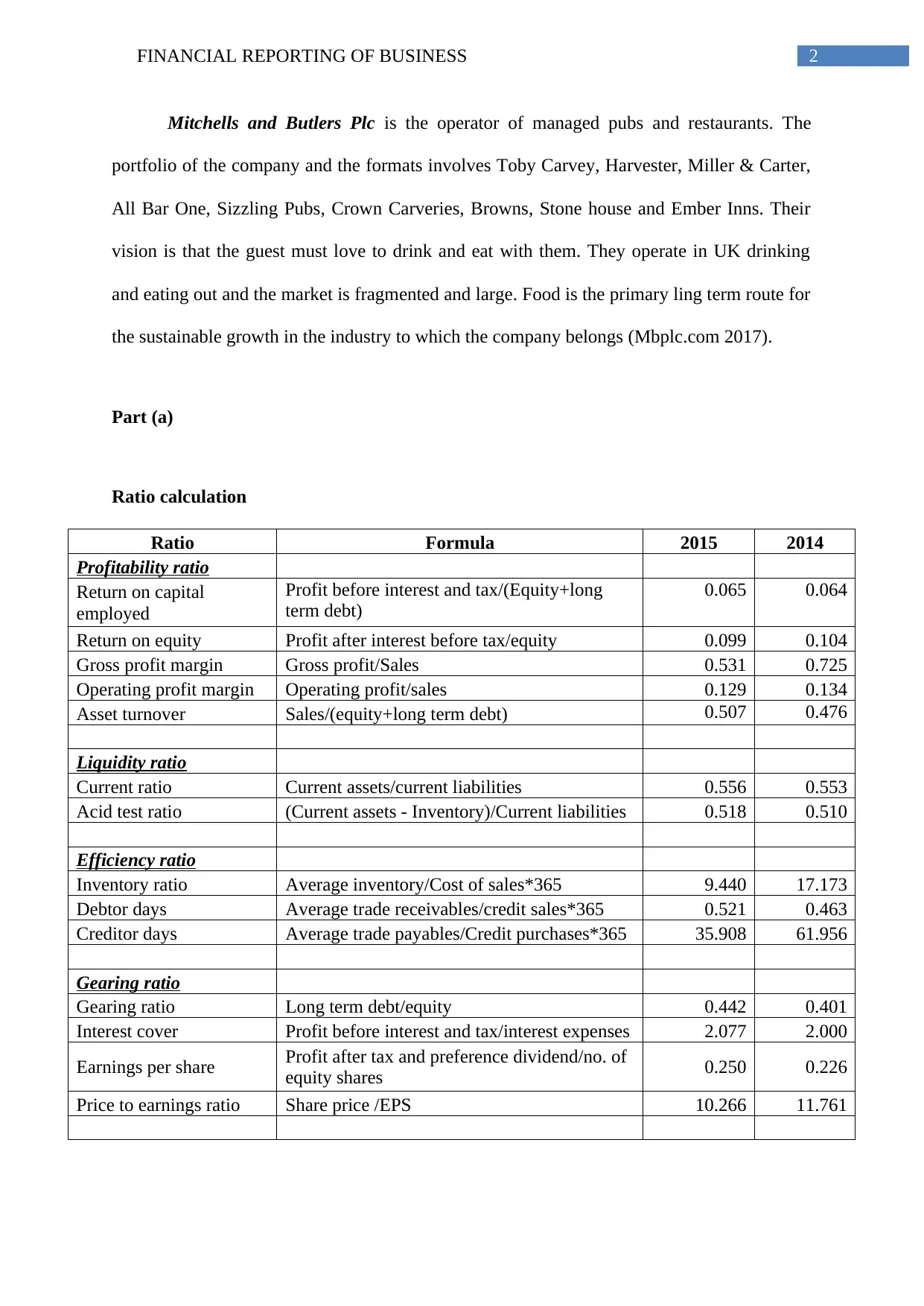

Mitchells and Butlers Plc is the operator of managed pubs and restaurants. The

portfolio of the company and the formats involves Toby Carvey, Harvester, Miller & Carter,

All Bar One, Sizzling Pubs, Crown Carveries, Browns, Stone house and Ember Inns. Their

vision is that the guest must love to drink and eat with them. They operate in UK drinking

and eating out and the market is fragmented and large. Food is the primary ling term route for

the sustainable growth in the industry to which the company belongs (Mbplc.com 2017).

Part (a)

Ratio calculation

Ratio Formula 2015 2014

Profitability ratio

Return on capital

employed

Profit before interest and tax/(Equity+long

term debt)

0.065 0.064

Return on equity Profit after interest before tax/equity 0.099 0.104

Gross profit margin Gross profit/Sales 0.531 0.725

Operating profit margin Operating profit/sales 0.129 0.134

Asset turnover Sales/(equity+long term debt) 0.507 0.476

Liquidity ratio

Current ratio Current assets/current liabilities 0.556 0.553

Acid test ratio (Current assets - Inventory)/Current liabilities 0.518 0.510

Efficiency ratio

Inventory ratio Average inventory/Cost of sales*365 9.440 17.173

Debtor days Average trade receivables/credit sales*365 0.521 0.463

Creditor days Average trade payables/Credit purchases*365 35.908 61.956

Gearing ratio

Gearing ratio Long term debt/equity 0.442 0.401

Interest cover Profit before interest and tax/interest expenses 2.077 2.000

Earnings per share Profit after tax and preference dividend/no. of

equity shares 0.250 0.226

Price to earnings ratio Share price /EPS 10.266 11.761

Mitchells and Butlers Plc is the operator of managed pubs and restaurants. The

portfolio of the company and the formats involves Toby Carvey, Harvester, Miller & Carter,

All Bar One, Sizzling Pubs, Crown Carveries, Browns, Stone house and Ember Inns. Their

vision is that the guest must love to drink and eat with them. They operate in UK drinking

and eating out and the market is fragmented and large. Food is the primary ling term route for

the sustainable growth in the industry to which the company belongs (Mbplc.com 2017).

Part (a)

Ratio calculation

Ratio Formula 2015 2014

Profitability ratio

Return on capital

employed

Profit before interest and tax/(Equity+long

term debt)

0.065 0.064

Return on equity Profit after interest before tax/equity 0.099 0.104

Gross profit margin Gross profit/Sales 0.531 0.725

Operating profit margin Operating profit/sales 0.129 0.134

Asset turnover Sales/(equity+long term debt) 0.507 0.476

Liquidity ratio

Current ratio Current assets/current liabilities 0.556 0.553

Acid test ratio (Current assets - Inventory)/Current liabilities 0.518 0.510

Efficiency ratio

Inventory ratio Average inventory/Cost of sales*365 9.440 17.173

Debtor days Average trade receivables/credit sales*365 0.521 0.463

Creditor days Average trade payables/Credit purchases*365 35.908 61.956

Gearing ratio

Gearing ratio Long term debt/equity 0.442 0.401

Interest cover Profit before interest and tax/interest expenses 2.077 2.000

Earnings per share Profit after tax and preference dividend/no. of

equity shares 0.250 0.226

Price to earnings ratio Share price /EPS 10.266 11.761

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL REPORTING OF BUSINESS

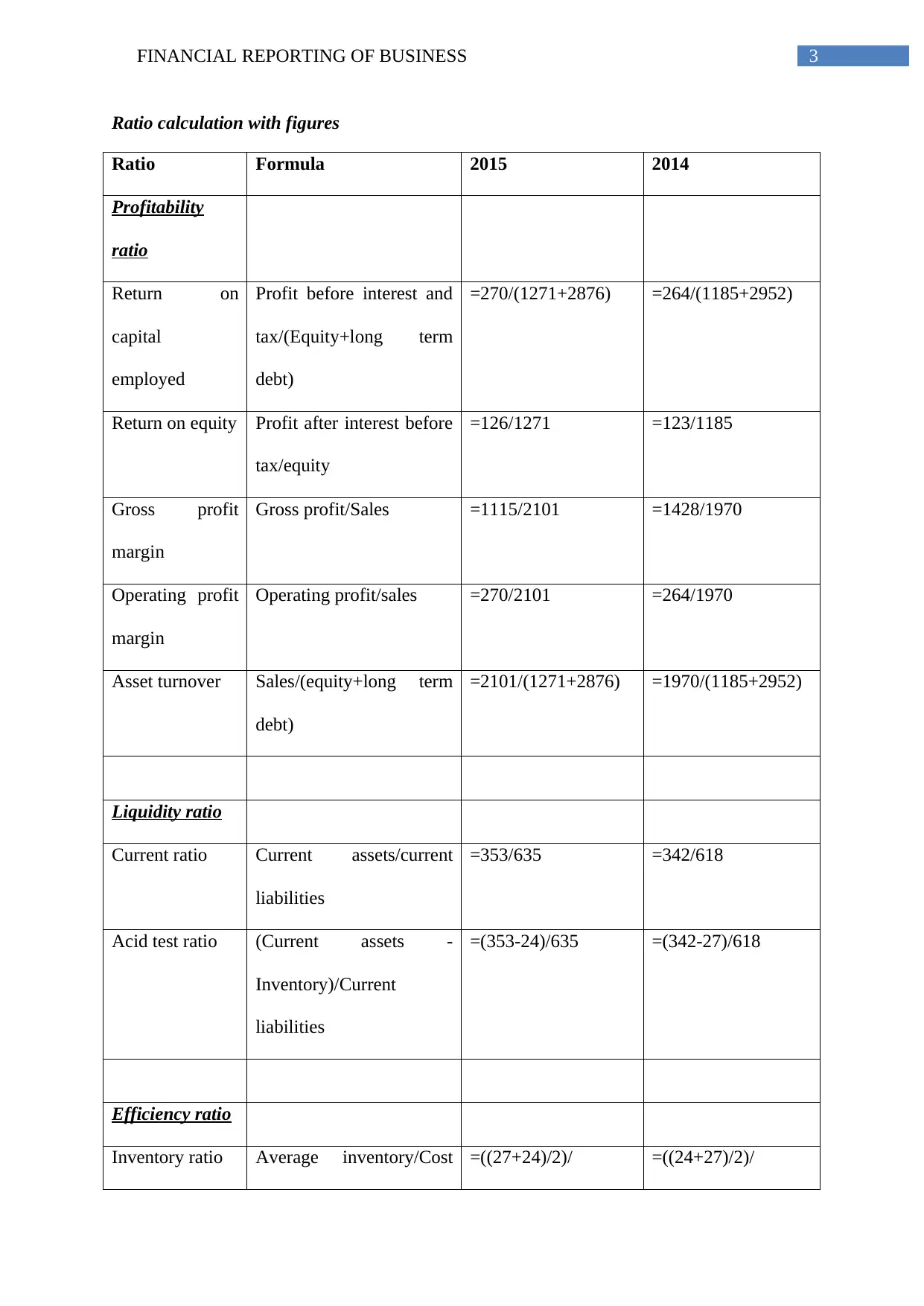

Ratio calculation with figures

Ratio Formula 2015 2014

Profitability

ratio

Return on

capital

employed

Profit before interest and

tax/(Equity+long term

debt)

=270/(1271+2876) =264/(1185+2952)

Return on equity Profit after interest before

tax/equity

=126/1271 =123/1185

Gross profit

margin

Gross profit/Sales =1115/2101 =1428/1970

Operating profit

margin

Operating profit/sales =270/2101 =264/1970

Asset turnover Sales/(equity+long term

debt)

=2101/(1271+2876) =1970/(1185+2952)

Liquidity ratio

Current ratio Current assets/current

liabilities

=353/635 =342/618

Acid test ratio (Current assets -

Inventory)/Current

liabilities

=(353-24)/635 =(342-27)/618

Efficiency ratio

Inventory ratio Average inventory/Cost =((27+24)/2)/ =((24+27)/2)/

Ratio calculation with figures

Ratio Formula 2015 2014

Profitability

ratio

Return on

capital

employed

Profit before interest and

tax/(Equity+long term

debt)

=270/(1271+2876) =264/(1185+2952)

Return on equity Profit after interest before

tax/equity

=126/1271 =123/1185

Gross profit

margin

Gross profit/Sales =1115/2101 =1428/1970

Operating profit

margin

Operating profit/sales =270/2101 =264/1970

Asset turnover Sales/(equity+long term

debt)

=2101/(1271+2876) =1970/(1185+2952)

Liquidity ratio

Current ratio Current assets/current

liabilities

=353/635 =342/618

Acid test ratio (Current assets -

Inventory)/Current

liabilities

=(353-24)/635 =(342-27)/618

Efficiency ratio

Inventory ratio Average inventory/Cost =((27+24)/2)/ =((24+27)/2)/

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL REPORTING OF BUSINESS

of sales*365 986*365 542*365

Debtor days Average trade

receivables/credit

sales*365

=((3+3)/2)/2101*365 =((2+3)/2)/1970*365

Creditor days Average trade

payables/Credit

purchases*365

=((100+94)/2)/

986*365

=((84+100)/2)/

542*365

Gearing ratio

Gearing ratio Long term debt/equity =1271/2876 =1185/2952

Interest cover Profit before interest and

tax/interest expenses

=270/130 =264/132

Earnings per

share

Profit after tax and

preference dividend/no. of

equity shares

=103000000/4125206

26

=93000000/4116378

85

Price to earnings

ratio

Share price /EPS =366.5/35.7 =417.5/35.5

of sales*365 986*365 542*365

Debtor days Average trade

receivables/credit

sales*365

=((3+3)/2)/2101*365 =((2+3)/2)/1970*365

Creditor days Average trade

payables/Credit

purchases*365

=((100+94)/2)/

986*365

=((84+100)/2)/

542*365

Gearing ratio

Gearing ratio Long term debt/equity =1271/2876 =1185/2952

Interest cover Profit before interest and

tax/interest expenses

=270/130 =264/132

Earnings per

share

Profit after tax and

preference dividend/no. of

equity shares

=103000000/4125206

26

=93000000/4116378

85

Price to earnings

ratio

Share price /EPS =366.5/35.7 =417.5/35.5

5FINANCIAL REPORTING OF BUSINESS

Part (b)

Analysis of ratio

Profitability ratio – the profitability ratio of the company are used for assessing the ability of

the business for generating the earnings as compared to the expenses and other related costs

expended during the particular period of time (Bodie, Kane and Marcus 2014). Under the

profitability ratio, having higher value as compared to the competitors and as compared to the

previous year’s indicates that the company is progressing.

Return on capital employed – it is the operating profit of the company as compared to

the capital employed. It calculates the company’s profitability through expressing the

operating profit as the percentage of the capital employed. From the above table it can

be identified that the return on capital employed of Mitchells and Butlers Plc is 6.5%

in 2015 as compared to 6.4% in 2014. Therefore, the company is stable in earning the

return on their capital (Heikal, Khaddafi and Ummah 2014).

Return on equity – this is the profitability ratio that calculates the company’s ability to

generate the profit from the investment of the shareholders in company. To be more

specific, the return on the equity indicates the amount of profit that the company earns

on each dollar of the shareholder’s equity. From the above table, it is recognized that

the return on equity of the company was 0.099 in 2015 as compared to 0.104 in 2014.

It indicated that the earning ability of the company is reduced in 2015 as compared to

the previous year (Atrill and McLaney 2016).

Gross profit margin – this ratio measures the financial health and the business model

of the company through revealing the percentage of money that is left from the

revenues after meeting the cost for selling the goods. The gross profit margin of the

Part (b)

Analysis of ratio

Profitability ratio – the profitability ratio of the company are used for assessing the ability of

the business for generating the earnings as compared to the expenses and other related costs

expended during the particular period of time (Bodie, Kane and Marcus 2014). Under the

profitability ratio, having higher value as compared to the competitors and as compared to the

previous year’s indicates that the company is progressing.

Return on capital employed – it is the operating profit of the company as compared to

the capital employed. It calculates the company’s profitability through expressing the

operating profit as the percentage of the capital employed. From the above table it can

be identified that the return on capital employed of Mitchells and Butlers Plc is 6.5%

in 2015 as compared to 6.4% in 2014. Therefore, the company is stable in earning the

return on their capital (Heikal, Khaddafi and Ummah 2014).

Return on equity – this is the profitability ratio that calculates the company’s ability to

generate the profit from the investment of the shareholders in company. To be more

specific, the return on the equity indicates the amount of profit that the company earns

on each dollar of the shareholder’s equity. From the above table, it is recognized that

the return on equity of the company was 0.099 in 2015 as compared to 0.104 in 2014.

It indicated that the earning ability of the company is reduced in 2015 as compared to

the previous year (Atrill and McLaney 2016).

Gross profit margin – this ratio measures the financial health and the business model

of the company through revealing the percentage of money that is left from the

revenues after meeting the cost for selling the goods. The gross profit margin of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL REPORTING OF BUSINESS

company for the year 2014 was 72.5% whereas the same reduced to 53.1% in 2015.

Therefore, the profitability margin of the company is reduced as compared to the

previous year (Robinson et al. 2015).

Operating profit margin – operating profit margin measures the operating efficiency

and pricing strategy of the company. It indicates the proportion of revenue that is left

after meeting the variable costs like raw materials, wages and salaries. The operating

profit margin of the company has been reduced to 12.9% from 13.4%. The reason

behind this is that the depreciation and amortisation cost is increased by £28 million

that led to reduction of operating profit of the company.

Asset turnover – it measures the efficiency of the company to generate earning from

sales using the assets. Asset turnover measures the net sales in percentage form for

revealing how the sales are created from each dollar of the assets of the company

(Melville 2015). It is identified that the company earned 50.7 cents in 2015 as

compared to 47.6 cents in 2014. The reason behind the increase in earnings is owing

to the increase in the revenue by £ 131 million.

Liquidity ratio – it analyzes the company’s ability to pay off the current liabilities on

becoming due. To be more specific, it reveals the company’s cash level and the ability to

transform other assets in cash for paying off the obligations and other liabilities (Delen,

Kuzey and Uyar 2013).

Current ratio – it is the efficiency ratio that indicated the efficiency of the company to

pay off the short-term obligation of the company with the available current assets.

From the table presented above it can be identified that for both the year the current

ratio of the company is 0.55 that means to say the company has enough asset to pay

off 55% of the liabilities. The reason behind this shortage is that a large portion of the

money is owed by the company towards trade payables and tax liabilities. Therefore,

company for the year 2014 was 72.5% whereas the same reduced to 53.1% in 2015.

Therefore, the profitability margin of the company is reduced as compared to the

previous year (Robinson et al. 2015).

Operating profit margin – operating profit margin measures the operating efficiency

and pricing strategy of the company. It indicates the proportion of revenue that is left

after meeting the variable costs like raw materials, wages and salaries. The operating

profit margin of the company has been reduced to 12.9% from 13.4%. The reason

behind this is that the depreciation and amortisation cost is increased by £28 million

that led to reduction of operating profit of the company.

Asset turnover – it measures the efficiency of the company to generate earning from

sales using the assets. Asset turnover measures the net sales in percentage form for

revealing how the sales are created from each dollar of the assets of the company

(Melville 2015). It is identified that the company earned 50.7 cents in 2015 as

compared to 47.6 cents in 2014. The reason behind the increase in earnings is owing

to the increase in the revenue by £ 131 million.

Liquidity ratio – it analyzes the company’s ability to pay off the current liabilities on

becoming due. To be more specific, it reveals the company’s cash level and the ability to

transform other assets in cash for paying off the obligations and other liabilities (Delen,

Kuzey and Uyar 2013).

Current ratio – it is the efficiency ratio that indicated the efficiency of the company to

pay off the short-term obligation of the company with the available current assets.

From the table presented above it can be identified that for both the year the current

ratio of the company is 0.55 that means to say the company has enough asset to pay

off 55% of the liabilities. The reason behind this shortage is that a large portion of the

money is owed by the company towards trade payables and tax liabilities. Therefore,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL REPORTING OF BUSINESS

the company shall pay off these liabilities to improve the current ratio (Elliott and

Elliot 2015).

Acid test ratio – this is the ability of the company to pay off the current obligation of

the company. The acid test ratio reveals the efficiency of the company to convert the

assets quickly into cash for paying off the current obligation. It can be seen from the

calculation that the acid test ratio for both the years is 0.51. It means to say the

company has enough assets to pay off 51% of the liabilities with the available quick

assets. The reason behind this is that the quick assets and liabilities of the company

are stable (Collier 2015).

Efficiency ratio – this is used for analyzing the ability of the company to use the liabilities

and assets internally. The efficiency ratio measures the receivable turnover, usage and

quantity of liability, liabilities repayments and the general usages of the machinery and

inventories.

Inventory turnover ratio – the inventory turnover ratio is the efficiency ratio that

reveals the efficiency of the company with regard to management of its inventory as

compared to the cost of the sales associated with the average inventory for specific

period. It can be seen from the calculation that the inventory turnover for 2014 was

17.17 times whereas the inventory turnover for 2015 was 9.44 times. Therefore, it can

be identified that the efficiency of the company with regard to inventory is reduced

(Brigham and Ehrhardt 2013). The reason behind that is the company is taking more

time to sell their inventories due to market demand fluctuation and competition in the

market for the substitute products.

Debtor days – it measures how quickly the cash is collected by the company from the

debtors. Longer times it takes to collect the cash more will be days for collecting the

receivables. It is also known as the debtor collection period. It can be identified from

the company shall pay off these liabilities to improve the current ratio (Elliott and

Elliot 2015).

Acid test ratio – this is the ability of the company to pay off the current obligation of

the company. The acid test ratio reveals the efficiency of the company to convert the

assets quickly into cash for paying off the current obligation. It can be seen from the

calculation that the acid test ratio for both the years is 0.51. It means to say the

company has enough assets to pay off 51% of the liabilities with the available quick

assets. The reason behind this is that the quick assets and liabilities of the company

are stable (Collier 2015).

Efficiency ratio – this is used for analyzing the ability of the company to use the liabilities

and assets internally. The efficiency ratio measures the receivable turnover, usage and

quantity of liability, liabilities repayments and the general usages of the machinery and

inventories.

Inventory turnover ratio – the inventory turnover ratio is the efficiency ratio that

reveals the efficiency of the company with regard to management of its inventory as

compared to the cost of the sales associated with the average inventory for specific

period. It can be seen from the calculation that the inventory turnover for 2014 was

17.17 times whereas the inventory turnover for 2015 was 9.44 times. Therefore, it can

be identified that the efficiency of the company with regard to inventory is reduced

(Brigham and Ehrhardt 2013). The reason behind that is the company is taking more

time to sell their inventories due to market demand fluctuation and competition in the

market for the substitute products.

Debtor days – it measures how quickly the cash is collected by the company from the

debtors. Longer times it takes to collect the cash more will be days for collecting the

receivables. It is also known as the debtor collection period. It can be identified from

8FINANCIAL REPORTING OF BUSINESS

the calculation that the debtor day of the company is increased in 2015 as compared to

2014. The reason may be that the company is allowing more credit to the debtors or

the debtors are not paying on time (Helfert 2011).

Creditor days - it measures how quickly the dues are paid by the company to the

creditors. Longer times it takes to pay the dues more will be days for paying the dues.

It is also known as the creditor payment period. It can be identified from the

calculation that the creditor days of the company are reduced in 2015 as compared to

2014. The reason may be that the company was able to pay off the dues on time or the

credit period allowed by the creditors has been reduced (Arnold 2013).

Gearing ratio – it measures the company’s borrowed funds proportion as compared to the

equity. High ratio indicates that the company has high debt proportion and low ratio indicated

low proportion of the debt to the equity. For both the year the gearing ratio of the company is

more or less same which indicates that the company is managing the same debt and equity

portion for both the years.

Interest coverage ratio – it measures the ability of the company to pay off the

interests on borrowings from the available operating profit of the company. The

interest coverage ratio of more than 1.5 indicates that the company is efficient paying

off its interest expenses. As per the calculation for both the years the interest

coverage ratio of the company is more than 2. That is to say the company has

sufficient operating income to cover up its interest expenses (Petty et al. 2015).

Earnings per share - as the earning per share of the company has increased from

0.226 in 2014 to 0.250 in 2015, it can be stated that the company is improving with

respect to create the return for the shareholders and attracting the potential investors

to invest in the company.

the calculation that the debtor day of the company is increased in 2015 as compared to

2014. The reason may be that the company is allowing more credit to the debtors or

the debtors are not paying on time (Helfert 2011).

Creditor days - it measures how quickly the dues are paid by the company to the

creditors. Longer times it takes to pay the dues more will be days for paying the dues.

It is also known as the creditor payment period. It can be identified from the

calculation that the creditor days of the company are reduced in 2015 as compared to

2014. The reason may be that the company was able to pay off the dues on time or the

credit period allowed by the creditors has been reduced (Arnold 2013).

Gearing ratio – it measures the company’s borrowed funds proportion as compared to the

equity. High ratio indicates that the company has high debt proportion and low ratio indicated

low proportion of the debt to the equity. For both the year the gearing ratio of the company is

more or less same which indicates that the company is managing the same debt and equity

portion for both the years.

Interest coverage ratio – it measures the ability of the company to pay off the

interests on borrowings from the available operating profit of the company. The

interest coverage ratio of more than 1.5 indicates that the company is efficient paying

off its interest expenses. As per the calculation for both the years the interest

coverage ratio of the company is more than 2. That is to say the company has

sufficient operating income to cover up its interest expenses (Petty et al. 2015).

Earnings per share - as the earning per share of the company has increased from

0.226 in 2014 to 0.250 in 2015, it can be stated that the company is improving with

respect to create the return for the shareholders and attracting the potential investors

to invest in the company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL REPORTING OF BUSINESS

Price to earnings ratio – it indicates the price that an investor is ready to pay for the

profit or earning of the company. The P/E ratio of the company is reduced from 11.76

to 10.27 over the year 2014 and 2015. A lower ratio indicates that the investor’s

interest in investing the company will be reduced (Bekaert and Hodrick 2017).

Price to earnings ratio – it indicates the price that an investor is ready to pay for the

profit or earning of the company. The P/E ratio of the company is reduced from 11.76

to 10.27 over the year 2014 and 2015. A lower ratio indicates that the investor’s

interest in investing the company will be reduced (Bekaert and Hodrick 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL REPORTING OF BUSINESS

Part (c)

Reporting on plant, property and equipment

The main objective of IAS 16 on plant property and equipment is prescribing the

accounting treatment for plant, property and equipment. The major issues here are the

recognition of the assets, determination of the carrying amount of the assets and the charges

of depreciation as well as the impairment losses that is to be recognized in association with

them (Picker et al. 2016). The items for plant, property and equipment shall be recognized

under assets while it is probable that the asset’s cost can be reliably measured and it is

probable that the future economic benefit in relation to the asset will flow to the company.

The principle of recognition is applicable to all the costs related to the plant, property and

equipment at the point of time while it is incurred (Svoboda and Bohušová 2017). The

associated costs includes the costs that are incurred for constructing and acquiring the assets

and subsequent costs incurred for replacing, adding or servicing the assets. It also identifies

that part of the assets which requires to be replaced regularly. IAS 16 allows 2 models for

accounting the cost of the assets –

Cost model – under this, the asset is valued at cost reduced by impairment and

accumulated depreciation

Revaluation model – under this the asset is carried on at revalued amount which is the

fair value of the asset reduced by the subsequent impairment and depreciation,

provided that the fair value of the asset can be reliably measured (Lapointe-Antunes

and Moore 2013).

On the other hand, the IAS 36 on impairment of assets ensures that the assets of the

company are not carried out at the values which are more than the recoverable amount of the

Part (c)

Reporting on plant, property and equipment

The main objective of IAS 16 on plant property and equipment is prescribing the

accounting treatment for plant, property and equipment. The major issues here are the

recognition of the assets, determination of the carrying amount of the assets and the charges

of depreciation as well as the impairment losses that is to be recognized in association with

them (Picker et al. 2016). The items for plant, property and equipment shall be recognized

under assets while it is probable that the asset’s cost can be reliably measured and it is

probable that the future economic benefit in relation to the asset will flow to the company.

The principle of recognition is applicable to all the costs related to the plant, property and

equipment at the point of time while it is incurred (Svoboda and Bohušová 2017). The

associated costs includes the costs that are incurred for constructing and acquiring the assets

and subsequent costs incurred for replacing, adding or servicing the assets. It also identifies

that part of the assets which requires to be replaced regularly. IAS 16 allows 2 models for

accounting the cost of the assets –

Cost model – under this, the asset is valued at cost reduced by impairment and

accumulated depreciation

Revaluation model – under this the asset is carried on at revalued amount which is the

fair value of the asset reduced by the subsequent impairment and depreciation,

provided that the fair value of the asset can be reliably measured (Lapointe-Antunes

and Moore 2013).

On the other hand, the IAS 36 on impairment of assets ensures that the assets of the

company are not carried out at the values which are more than the recoverable amount of the

11FINANCIAL REPORTING OF BUSINESS

assets. The recoverable amount is the higher value among the value in use and the fair value

reduced by disposal costs (Tsalavoutas, André and Dionysiou 2014). The company must

carry out the impairment test for the entire asset where there is the indication for impairment

with the exception to some intangible assets and goodwill. Further, the impairment test can be

carried out for the cash generating unit where the asset is not able to generate the cash

inflows, which is largely independent from the other assets. At the closing of each reporting

period the company is required to analyse whether any indication is there that an asset have a

chance to impair (Mazzi, Liberatore and Tsalavoutas 2016). Under IAS 36 there is a list of

internal and external indication list for impairment. If there, is any indication the recoverable

amount of the asset shall be calculated. The below mentioned asset’s recoverable amount are

annually measured to identify whether any indication is there that the asset may be impaired.

These assets are –

The intangible asset with the indefinite useful life

The intangible asset which is not yet available for the purpose of use

The goodwill that is acquired under the business combination.

External indication for impairment is the decline in the market value, increase in the

market rate of interest, negative changes in the economy, markets, laws or technology and the

net asset of the company is higher as compared to the market capitalisation. On the other

hand the internal sources for impairment are the physical damage or obsolescence, the asset is

idle or part of restructuring or held for the purpose of disposal or the worsening of the

economic performance as compared to expectation (Avallone and Quagli 2015).

Mitchell and Butlers Plc follow the IAS 16 for recognition of plant, property and

equipment. For example, the items for plant, property and equipment are recognized under

assets while it is probable that the asset’s cost can be reliably measured and it is probable that

assets. The recoverable amount is the higher value among the value in use and the fair value

reduced by disposal costs (Tsalavoutas, André and Dionysiou 2014). The company must

carry out the impairment test for the entire asset where there is the indication for impairment

with the exception to some intangible assets and goodwill. Further, the impairment test can be

carried out for the cash generating unit where the asset is not able to generate the cash

inflows, which is largely independent from the other assets. At the closing of each reporting

period the company is required to analyse whether any indication is there that an asset have a

chance to impair (Mazzi, Liberatore and Tsalavoutas 2016). Under IAS 36 there is a list of

internal and external indication list for impairment. If there, is any indication the recoverable

amount of the asset shall be calculated. The below mentioned asset’s recoverable amount are

annually measured to identify whether any indication is there that the asset may be impaired.

These assets are –

The intangible asset with the indefinite useful life

The intangible asset which is not yet available for the purpose of use

The goodwill that is acquired under the business combination.

External indication for impairment is the decline in the market value, increase in the

market rate of interest, negative changes in the economy, markets, laws or technology and the

net asset of the company is higher as compared to the market capitalisation. On the other

hand the internal sources for impairment are the physical damage or obsolescence, the asset is

idle or part of restructuring or held for the purpose of disposal or the worsening of the

economic performance as compared to expectation (Avallone and Quagli 2015).

Mitchell and Butlers Plc follow the IAS 16 for recognition of plant, property and

equipment. For example, the items for plant, property and equipment are recognized under

assets while it is probable that the asset’s cost can be reliably measured and it is probable that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.