Financial Reporting Analysis: Wesfarmers Limited PPE Disclosures

VerifiedAdded on 2020/04/01

|9

|2099

|79

Report

AI Summary

This report analyzes the market disclosures of Wesfarmers Limited, an ASX-listed company, focusing on its property, plant, and equipment (PPE) disclosures to assess how well they meet the objectives of general purpose financial reporting. The report evaluates the disclosures against the qualitative characteristics outlined in the IASB's conceptual framework, including relevance, reliability, understandability, and comparability. The analysis, presented from the perspective of an accounting graduate to the CFO, examines Wesfarmers' compliance with AASB 116 and identifies areas where disclosures could be improved to better align with the objectives of financial reporting. The report discusses the use of historical cost, straight-line depreciation, and recommends adopting fair value accounting and reducing balance depreciation to enhance the relevance and understandability of the financial information. The conclusion emphasizes the importance of adhering to the conceptual framework's qualitative characteristics for effective financial reporting, and provides recommendations for improvement.

Master of Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The present report analyses the market disclosure made by an ASX listed company

for understanding the importance of meeting the objectives of general purpose financial

reporting for business corporations. This is done to ensure that the financial reports meet the

objective of general purpose financial reporting. The qualitative characteristics outlined by

the conceptual framework (CF) developed by IASB are relevancy, reliability,

understandability and comparability. The report has been prepared on the perspective of an

accounting graduate submitting the analysis of disclosures of the company selected in relation

to PPE to the Chief Financial Officer (CFO).

The present report analyses the market disclosure made by an ASX listed company

for understanding the importance of meeting the objectives of general purpose financial

reporting for business corporations. This is done to ensure that the financial reports meet the

objective of general purpose financial reporting. The qualitative characteristics outlined by

the conceptual framework (CF) developed by IASB are relevancy, reliability,

understandability and comparability. The report has been prepared on the perspective of an

accounting graduate submitting the analysis of disclosures of the company selected in relation

to PPE to the Chief Financial Officer (CFO).

Contents

Introduction................................................................................................................................4

Explanation of General purpose financial reporting objectives and the qualitative

characteristics of useful financial information as per CF...........................................................4

Extent of Wesfarmers Limited annual report meeting the disclosure requirements for PPE as

per AASB 116............................................................................................................................5

Critical analysis of extent of disclosures on PPE of Wesfarmers to satisfy the fundamental

and enhancing qualitative characteristics of useful financial information.................................6

Critical discussion to the extent of the disclosures of Wesfarmers on PPE aligned with the

objective of general purpose financial reporting and recommendations for improvement.......7

Conclusion..................................................................................................................................8

References..................................................................................................................................9

Introduction................................................................................................................................4

Explanation of General purpose financial reporting objectives and the qualitative

characteristics of useful financial information as per CF...........................................................4

Extent of Wesfarmers Limited annual report meeting the disclosure requirements for PPE as

per AASB 116............................................................................................................................5

Critical analysis of extent of disclosures on PPE of Wesfarmers to satisfy the fundamental

and enhancing qualitative characteristics of useful financial information.................................6

Critical discussion to the extent of the disclosures of Wesfarmers on PPE aligned with the

objective of general purpose financial reporting and recommendations for improvement.......7

Conclusion..................................................................................................................................8

References..................................................................................................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

The business corporations around the world are emphasizing on developing high-

quality financial reports as per the qualitative characteristics of conceptual accounting

framework. The IASB (International Accounting Standards Board) has directed all the

business corporations to develop their financial reports as per the qualitative characteristics

prescribed in its conceptual framework for financial reporting. The report specifically

addresses the deviations observed in meeting the objective of general purpose financial

reporting by the company in relation to Property, Plant and Equipment (PPE). The company

selected for the purpose is Wesfarmers Limited, a supermarket giant in Australia involved in

variety of business operations including chemicals, fertilizers, industrial products, home

improvement and many others. The report reviews the disclosures made by the company in

relation to PPE and their alignment with the CF objective and qualitative characteristics

based on board of director’s decision on the perspective of an accounting graduate.

Explanation of General purpose financial reporting objectives and the qualitative

characteristics of useful financial information as per CF

The objective of general purpose financial reporting as advocated by the IASB is to

provide useful financial information of a reporting entity to the end-users including potential

investors, lenders and creditors. The disclosure of all the necessary financial information to

the stakeholders of a business entity is essential for supporting their decision-making process

through gaining a complete understanding of its financial resources. The decisions include

buying or lending equity and debt instruments, providing or settling loans and similar

investment decisions. As such, the IASB has developed conceptual accounting framework for

financial reporting that has stated the qualitative characteristics that financial information of a

reporting entity must possess in order to meet the needs of end-users. The fundamental

qualitative characteristics are relevance, faithful presentation, understandability and

comparability (Macve, 2015).

The relevance principle of CF states that financial information should be relevant

enough to make a difference in the decisions of the end-users. Thus, as per this qualitative

characteristic, the financial information disclosed must have both predictive and confirmatory

value. The confirmatory value should provide feedback about its current and past

performance while predictive value should be able to provide an analysis of its future

The business corporations around the world are emphasizing on developing high-

quality financial reports as per the qualitative characteristics of conceptual accounting

framework. The IASB (International Accounting Standards Board) has directed all the

business corporations to develop their financial reports as per the qualitative characteristics

prescribed in its conceptual framework for financial reporting. The report specifically

addresses the deviations observed in meeting the objective of general purpose financial

reporting by the company in relation to Property, Plant and Equipment (PPE). The company

selected for the purpose is Wesfarmers Limited, a supermarket giant in Australia involved in

variety of business operations including chemicals, fertilizers, industrial products, home

improvement and many others. The report reviews the disclosures made by the company in

relation to PPE and their alignment with the CF objective and qualitative characteristics

based on board of director’s decision on the perspective of an accounting graduate.

Explanation of General purpose financial reporting objectives and the qualitative

characteristics of useful financial information as per CF

The objective of general purpose financial reporting as advocated by the IASB is to

provide useful financial information of a reporting entity to the end-users including potential

investors, lenders and creditors. The disclosure of all the necessary financial information to

the stakeholders of a business entity is essential for supporting their decision-making process

through gaining a complete understanding of its financial resources. The decisions include

buying or lending equity and debt instruments, providing or settling loans and similar

investment decisions. As such, the IASB has developed conceptual accounting framework for

financial reporting that has stated the qualitative characteristics that financial information of a

reporting entity must possess in order to meet the needs of end-users. The fundamental

qualitative characteristics are relevance, faithful presentation, understandability and

comparability (Macve, 2015).

The relevance principle of CF states that financial information should be relevant

enough to make a difference in the decisions of the end-users. Thus, as per this qualitative

characteristic, the financial information disclosed must have both predictive and confirmatory

value. The confirmatory value should provide feedback about its current and past

performance while predictive value should be able to provide an analysis of its future

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance. The faithful presentation of the financial reports states that financial

information disclosures should be complete, neutral and error-free. Thus, it should provide an

in-depth understanding of the phenomena involved through depicting all the necessary

descriptions and explanations. On the other hand, the comparability qualitative

characteristics requires that financial information provided to the end-users must provide an

analysis of the increase or decrease in the current financial performance of an entity in

comparison to the past performances. In addition to this, the understandability of financial

information ensures that it is simple to be understood by the end-users within involving any

complexity (Harvey, McLaney and Atrill, 2013).

Extent of Wesfarmers Limited annual report meeting the disclosure requirements for

PPE as per AASB 116

The accounting standard of AASB 116 has provided the guidelines to all the ASX

listed business entities to value the property, plant and equipment (PPE). The standards has

prescribed to take into account the carrying amounts and the deprecation and impairment

charges related to PPE at the time of their measurement during financial reporting. As per the

standard, the carrying value of an asset is recognized after deducting all the accumulated

deprecation and impairment losses. The useful life of an asset is the period over which an

asset is expected to be available for future use by an entity. The recoverable amount of an

asset is said to be higher of either fair value of an asset loss cost to sell or its value in use. The

impairment loss can be recognized to be the amount by which its carrying value exceeds the

recoverable amount. The annual report of Wesfarmers Limited has stated the effective

compliance of the company with the AASB 116 in relation to identification and recognition

of property, plant and equipment (Compiled AASB 116 Standards, 2017).

The carrying value of PPE is measured on the cost basis through deducting all the

significant deprecation and impairment losses as per the AASB 116. The items of property,

plant and equipment is put to sale or is disposed when it is regarded to bring no future

economic benefits to the company. The significant gain or loss arising from its sale is

reported in the income statement of the period when the corresponding items is derecognized.

The company has also provided disclosure regarding the key estimates taken by the

management in estimating the useful life, residual value and amortization methods for its

items of PPE (2017 Annual Report: Wesfarmers, 2017). Thus, it can be said that Wesfarmers

information disclosures should be complete, neutral and error-free. Thus, it should provide an

in-depth understanding of the phenomena involved through depicting all the necessary

descriptions and explanations. On the other hand, the comparability qualitative

characteristics requires that financial information provided to the end-users must provide an

analysis of the increase or decrease in the current financial performance of an entity in

comparison to the past performances. In addition to this, the understandability of financial

information ensures that it is simple to be understood by the end-users within involving any

complexity (Harvey, McLaney and Atrill, 2013).

Extent of Wesfarmers Limited annual report meeting the disclosure requirements for

PPE as per AASB 116

The accounting standard of AASB 116 has provided the guidelines to all the ASX

listed business entities to value the property, plant and equipment (PPE). The standards has

prescribed to take into account the carrying amounts and the deprecation and impairment

charges related to PPE at the time of their measurement during financial reporting. As per the

standard, the carrying value of an asset is recognized after deducting all the accumulated

deprecation and impairment losses. The useful life of an asset is the period over which an

asset is expected to be available for future use by an entity. The recoverable amount of an

asset is said to be higher of either fair value of an asset loss cost to sell or its value in use. The

impairment loss can be recognized to be the amount by which its carrying value exceeds the

recoverable amount. The annual report of Wesfarmers Limited has stated the effective

compliance of the company with the AASB 116 in relation to identification and recognition

of property, plant and equipment (Compiled AASB 116 Standards, 2017).

The carrying value of PPE is measured on the cost basis through deducting all the

significant deprecation and impairment losses as per the AASB 116. The items of property,

plant and equipment is put to sale or is disposed when it is regarded to bring no future

economic benefits to the company. The significant gain or loss arising from its sale is

reported in the income statement of the period when the corresponding items is derecognized.

The company has also provided disclosure regarding the key estimates taken by the

management in estimating the useful life, residual value and amortization methods for its

items of PPE (2017 Annual Report: Wesfarmers, 2017). Thus, it can be said that Wesfarmers

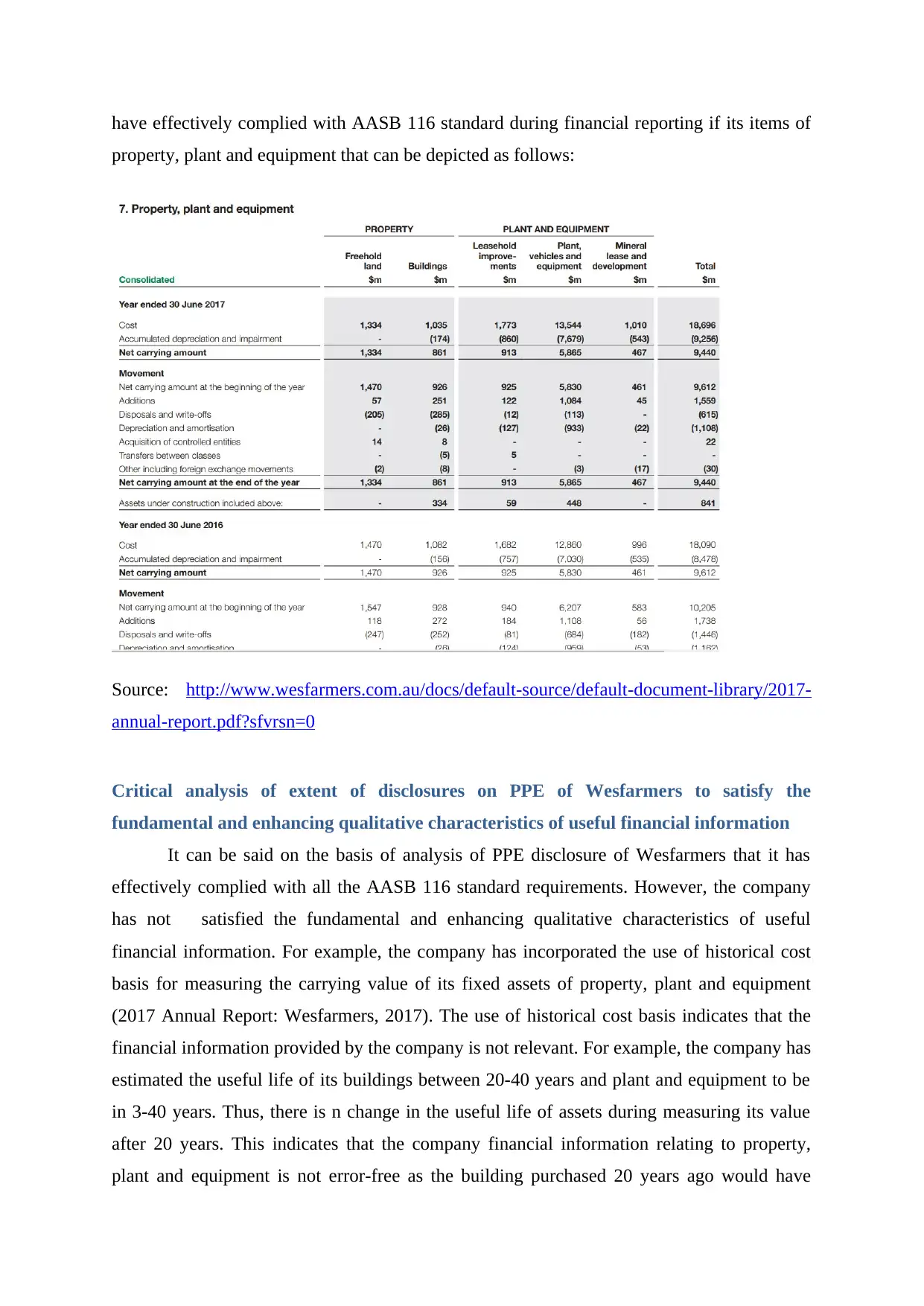

have effectively complied with AASB 116 standard during financial reporting if its items of

property, plant and equipment that can be depicted as follows:

Source: http://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-

annual-report.pdf?sfvrsn=0

Critical analysis of extent of disclosures on PPE of Wesfarmers to satisfy the

fundamental and enhancing qualitative characteristics of useful financial information

It can be said on the basis of analysis of PPE disclosure of Wesfarmers that it has

effectively complied with all the AASB 116 standard requirements. However, the company

has not satisfied the fundamental and enhancing qualitative characteristics of useful

financial information. For example, the company has incorporated the use of historical cost

basis for measuring the carrying value of its fixed assets of property, plant and equipment

(2017 Annual Report: Wesfarmers, 2017). The use of historical cost basis indicates that the

financial information provided by the company is not relevant. For example, the company has

estimated the useful life of its buildings between 20-40 years and plant and equipment to be

in 3-40 years. Thus, there is n change in the useful life of assets during measuring its value

after 20 years. This indicates that the company financial information relating to property,

plant and equipment is not error-free as the building purchased 20 years ago would have

property, plant and equipment that can be depicted as follows:

Source: http://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-

annual-report.pdf?sfvrsn=0

Critical analysis of extent of disclosures on PPE of Wesfarmers to satisfy the

fundamental and enhancing qualitative characteristics of useful financial information

It can be said on the basis of analysis of PPE disclosure of Wesfarmers that it has

effectively complied with all the AASB 116 standard requirements. However, the company

has not satisfied the fundamental and enhancing qualitative characteristics of useful

financial information. For example, the company has incorporated the use of historical cost

basis for measuring the carrying value of its fixed assets of property, plant and equipment

(2017 Annual Report: Wesfarmers, 2017). The use of historical cost basis indicates that the

financial information provided by the company is not relevant. For example, the company has

estimated the useful life of its buildings between 20-40 years and plant and equipment to be

in 3-40 years. Thus, there is n change in the useful life of assets during measuring its value

after 20 years. This indicates that the company financial information relating to property,

plant and equipment is not error-free as the building purchased 20 years ago would have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

different material value in the current market. Thus, the financial information is not relevant

as it has not taken into account the current value of property, plant and equipment through

adjusting their useful life as per the current market conditions (Compiled AASB 116

Standards, 2017).

In addition to this, the company calculates deprecation value through the use of

straight-line basis that is not effective method for measuring deprecation on some of the

equipments of the company such as computers due to rapid development in technologies.

Also, the method does not accurately reflect the difference in asset use from one period to

another and it does not match the costs with revenues of different types of long-term assets.

Thus, it can be said that the company does not comply with the understandability qualitative

characteristics of useful financial information through implementing the use of straight-line

deprecation method (2017 Annual Report: Wesfarmers, 2017). The end-users are not able to

match the revenue with expenses of long-term assets of the company with the use of the

depreciation method (Alexander, Britton and Jorissen, 2007).

Critical discussion to the extent of the disclosures of Wesfarmers on PPE aligned with

the objective of general purpose financial reporting and recommendations for

improvement

The objective of general purpose financial reporting is to protect the interests of end-

users through providing them materialistic financial information that can be used by them for

making investment decisions. As analyzed form the annual report of Wesfarmers Limited, the

company has valued the items of property, plant and equipment as per the AASB 116

standards. However, the company has not adequately met the relevancy and understandability

qualitative characteristic of conceptual accounting framework. Therefore, the company has

not appropriately aligned its PPE disclosures with the objective of general purpose financial

reporting. This is because the company has not provided the relevant and understandable

financial information relating to PPE to its end-users (2017 Annual Report: Wesfarmers,

2017). The company as such is recommended to incorporate the use of fair value accounting

in recognizing the carrying value of its long-term assets. The AASB 13 standard has provided

the guidelines to the business corporations regarding the use of fair value in measuring the

value of its fixed asset such a property, plant and equipment. The use of fair value would help

in identification of accurate value of recoverable amount, residual and useful life of assets

based on current market conditions (AASB 13, 2015).

as it has not taken into account the current value of property, plant and equipment through

adjusting their useful life as per the current market conditions (Compiled AASB 116

Standards, 2017).

In addition to this, the company calculates deprecation value through the use of

straight-line basis that is not effective method for measuring deprecation on some of the

equipments of the company such as computers due to rapid development in technologies.

Also, the method does not accurately reflect the difference in asset use from one period to

another and it does not match the costs with revenues of different types of long-term assets.

Thus, it can be said that the company does not comply with the understandability qualitative

characteristics of useful financial information through implementing the use of straight-line

deprecation method (2017 Annual Report: Wesfarmers, 2017). The end-users are not able to

match the revenue with expenses of long-term assets of the company with the use of the

depreciation method (Alexander, Britton and Jorissen, 2007).

Critical discussion to the extent of the disclosures of Wesfarmers on PPE aligned with

the objective of general purpose financial reporting and recommendations for

improvement

The objective of general purpose financial reporting is to protect the interests of end-

users through providing them materialistic financial information that can be used by them for

making investment decisions. As analyzed form the annual report of Wesfarmers Limited, the

company has valued the items of property, plant and equipment as per the AASB 116

standards. However, the company has not adequately met the relevancy and understandability

qualitative characteristic of conceptual accounting framework. Therefore, the company has

not appropriately aligned its PPE disclosures with the objective of general purpose financial

reporting. This is because the company has not provided the relevant and understandable

financial information relating to PPE to its end-users (2017 Annual Report: Wesfarmers,

2017). The company as such is recommended to incorporate the use of fair value accounting

in recognizing the carrying value of its long-term assets. The AASB 13 standard has provided

the guidelines to the business corporations regarding the use of fair value in measuring the

value of its fixed asset such a property, plant and equipment. The use of fair value would help

in identification of accurate value of recoverable amount, residual and useful life of assets

based on current market conditions (AASB 13, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The company is recommended to adjust the useful life of assets relating to items of

property, plant and equipment in order to record the realistic and reliable value of property,

plant and equipment. This is required by the company to provide relevant and reliable

information to the end-users about its items of PPE. In addition to this, the company is

recommended to incorporate the use of reducing balance method for calculating deprecation.

This method of deprecation is simple to be understood by the end-users as deprecation for

every year is calculated on the opening balance of an asset in his method. Also, it easily

matches the cost and revenues of the business and therefore simplifies for users to understand

the financial statements developed by the company as per the understandability principle of

conceptual accounting framework (Harvey, McLaney and Atrill, 2013).

Conclusion

It can be inferred from the overall discussion held in the report that business

corporations should satisfy the qualitative characteristics of conceptual accounting

framework for meeting the objective of general purpose financial reporting. The Wesfarmers

though have effectively complied with all the necessary AASB standard in relation to

property, plant and equipment need to incorporate some changes in its valuation techniques

for meeting the objective of financial reporting.

property, plant and equipment in order to record the realistic and reliable value of property,

plant and equipment. This is required by the company to provide relevant and reliable

information to the end-users about its items of PPE. In addition to this, the company is

recommended to incorporate the use of reducing balance method for calculating deprecation.

This method of deprecation is simple to be understood by the end-users as deprecation for

every year is calculated on the opening balance of an asset in his method. Also, it easily

matches the cost and revenues of the business and therefore simplifies for users to understand

the financial statements developed by the company as per the understandability principle of

conceptual accounting framework (Harvey, McLaney and Atrill, 2013).

Conclusion

It can be inferred from the overall discussion held in the report that business

corporations should satisfy the qualitative characteristics of conceptual accounting

framework for meeting the objective of general purpose financial reporting. The Wesfarmers

though have effectively complied with all the necessary AASB standard in relation to

property, plant and equipment need to incorporate some changes in its valuation techniques

for meeting the objective of financial reporting.

References

2017 Annual Report: Wesfarmers. 2017. [Online]. Available at:

http://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-annual-

report.pdf?sfvrsn=0 [Accessed on: 4 September 2017].

AASB 13. 2015. Fair Value Measurement. [Online]. Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB13_08-15.pdf [Accessed on: 4

September 2017].

Alexander, D., Britton, A. and Jorissen, A. 2007. International Financial Reporting and

Analysis. Cengage Learning EMEA.

Compiled AASB 116 Standards. 2017. [Online]. Available at:

http://www.aasb.gov.au/admin/file/content102/c3/AASB116_07-04_ERDRjun10_07-09.pdf

[Accessed on: 4 September 2017].

Harvey, D., McLaney, E. and Atrill, P. 2013. Accounting for Business. Routledge.

Macve, R. 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat? Routledge.

2017 Annual Report: Wesfarmers. 2017. [Online]. Available at:

http://www.wesfarmers.com.au/docs/default-source/default-document-library/2017-annual-

report.pdf?sfvrsn=0 [Accessed on: 4 September 2017].

AASB 13. 2015. Fair Value Measurement. [Online]. Available at:

http://www.aasb.gov.au/admin/file/content105/c9/AASB13_08-15.pdf [Accessed on: 4

September 2017].

Alexander, D., Britton, A. and Jorissen, A. 2007. International Financial Reporting and

Analysis. Cengage Learning EMEA.

Compiled AASB 116 Standards. 2017. [Online]. Available at:

http://www.aasb.gov.au/admin/file/content102/c3/AASB116_07-04_ERDRjun10_07-09.pdf

[Accessed on: 4 September 2017].

Harvey, D., McLaney, E. and Atrill, P. 2013. Accounting for Business. Routledge.

Macve, R. 2015. A Conceptual Framework for Financial Accounting and Reporting: Vision,

Tool, Or Threat? Routledge.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.