Financial Reporting Analysis: Marks & Spencer Financial Performance

VerifiedAdded on 2020/12/29

|12

|3437

|426

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, using Marks & Spencer as a case study. It begins with an introduction to financial reporting, its context, purpose, and objectives, and then delves into the conceptual and regulatory frameworks, including IFRS and IAS. The report explores the stakeholders of an organization and their benefits from financial information. It then analyzes Marks & Spencer's financial statements, including the statement of profit and loss, changes in equity, and statement of financial position, along with a two-year financial statement analysis using key financial ratios. The report also highlights the differences between IAS and IFRS and the importance of financial reporting in organizational growth. Overall, the report provides a detailed overview of financial reporting principles and their practical application in a real-world business context.

Financial Reporting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Analyse the context and purpose of financial reporting ........................................................1

2. Conceptual and regulatory framework and qualitative characteristics of financial

information..................................................................................................................................2

3. Stakeholders of an organisation and its benefits from financial information.........................2

4) Importance of financial reporting in context of organisational objectives and growth..........3

5. Analysis of financial statement of organisation......................................................................4

6. Two years financial statement analysis of Marks & Spencer ................................................5

7. Difference between International Financial reporting standards and International

Accounting system .....................................................................................................................6

8. Benefits of international financial reporting standards ..........................................................7

9. Degrees of compliance with IFRS and its factors which influence company.........................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

.......................................................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Analyse the context and purpose of financial reporting ........................................................1

2. Conceptual and regulatory framework and qualitative characteristics of financial

information..................................................................................................................................2

3. Stakeholders of an organisation and its benefits from financial information.........................2

4) Importance of financial reporting in context of organisational objectives and growth..........3

5. Analysis of financial statement of organisation......................................................................4

6. Two years financial statement analysis of Marks & Spencer ................................................5

7. Difference between International Financial reporting standards and International

Accounting system .....................................................................................................................6

8. Benefits of international financial reporting standards ..........................................................7

9. Degrees of compliance with IFRS and its factors which influence company.........................8

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

.......................................................................................................................................................10

INTRODUCTION

Financial reporting provides the finance related information to an organisation. Through

it position of a corporation can be understand and which help the business to take effective

decisions. In the report chosen company is Mark & Spencer which is British Multinational

retailer from United Kingdom. It main aim of this is to analyse the financial statement of

organisation. It covers the following topics such as: context, purpose and objectives of financial

reporting, regulatory framework & key principles, benefits and statement of profit & loss

account, changes in equity and balance sheet. Apart from this it discuss about the difference

between IAS and IFRS.

TASK 1

1. Analyse the context and purpose of financial reporting

Financial reporting helps the company to get financial results of its business related to a

particular period of time. It involves statement of cash flow, balance sheet and profit and loss

account. It helps the business to know its position through which an organisation can understand

it is in profit making or loss making situation.

Financial reporting provides useful information and data to corporation which helps it to

take important decisions related to money related matters. It gives appropriate and realistic

financial information to the stakeholders of company and on the basis of this they take

investment related decisions. Management of Mark & Spencer can make planning and strategies

on the basis of financial information.

Purpose of financial reporting are as follows:

To provide accurate information related to profits and financial position of corporation.

To gives data to the management for planning and strategic decisions.

It provides required information regarding obtaining and managing assets of the business.

To effectively control financial resources with in the company (Shivakumar, 2013).

The main objective is to analyse the current status related to financial matters for a

specific time period of time.

It helps to an organisation in making essential decisions so that it can expand its business

and make effective investment as a result Mark & Spencer can generates more returns. So

Financial reporting provides the finance related information to an organisation. Through

it position of a corporation can be understand and which help the business to take effective

decisions. In the report chosen company is Mark & Spencer which is British Multinational

retailer from United Kingdom. It main aim of this is to analyse the financial statement of

organisation. It covers the following topics such as: context, purpose and objectives of financial

reporting, regulatory framework & key principles, benefits and statement of profit & loss

account, changes in equity and balance sheet. Apart from this it discuss about the difference

between IAS and IFRS.

TASK 1

1. Analyse the context and purpose of financial reporting

Financial reporting helps the company to get financial results of its business related to a

particular period of time. It involves statement of cash flow, balance sheet and profit and loss

account. It helps the business to know its position through which an organisation can understand

it is in profit making or loss making situation.

Financial reporting provides useful information and data to corporation which helps it to

take important decisions related to money related matters. It gives appropriate and realistic

financial information to the stakeholders of company and on the basis of this they take

investment related decisions. Management of Mark & Spencer can make planning and strategies

on the basis of financial information.

Purpose of financial reporting are as follows:

To provide accurate information related to profits and financial position of corporation.

To gives data to the management for planning and strategic decisions.

It provides required information regarding obtaining and managing assets of the business.

To effectively control financial resources with in the company (Shivakumar, 2013).

The main objective is to analyse the current status related to financial matters for a

specific time period of time.

It helps to an organisation in making essential decisions so that it can expand its business

and make effective investment as a result Mark & Spencer can generates more returns. So

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

financial reporting is very important for a corporation through which management can

know about its financial position.

2. Conceptual and regulatory framework and qualitative characteristics of financial information

Conceptual and regulatory framework

Conceptual framework incorporates regarding the quantitative and subjective issues. The

structure can be followed by various disciplines but it particularly accompanying to financial

reporting, a regulatory and conceptual framework which is provided by IASB. It provides better

information and financial data so that Mark & Spencer can take better decisions and effectively

control its operational activities. It helps to develop relevant ideas to evaluate essential capital

support. Organisation can use regulatory and conceptual framework to control its unnecessary

financial activities and follows the rules and regulations as per the guidelines of IASB. These

guidelines are forced as IFRS. Necessity of IFRS are as follows:

Fundamental accounting concepts are set and controlled by International financial

reporting standards. IFRS can be use by companies for better control and it improves accounting

controls and the standards (Kim and Zhou, 2014).

Qualitative characteristics which makes financial information realistic:

International financial reporting standards are extensively used by companies so that it

can it can set its standards as per the rules and regulations of IFRS. It is essential at international

level so that financial information can be get more accurately and reliable. International financial

reporting standards are recognised by the international Organisation of Securities Commission

for the purpose of utilization IFRS for effective management and control in the company. So

Mark & Spencer can apply this concept and improves it financial management system (Jung,

and Weber, 2014).

3. Stakeholders of an organisation and its benefits from financial information

Stakeholders

Stakeholders are the group of persons who have interest in the company. From the

decisions and actions of an organisation they can get influenced and their interest has affected. It

involves directors, employees, suppliers, creditors, government, shareholders etc. These are the

authorise persons which associated with investment and other organisational decisions. Business

of Mark & Spencer can affect the stakeholders in both positive and negative way.

Internal stakeholders of Mark & Spencer and its benefits from financial information

know about its financial position.

2. Conceptual and regulatory framework and qualitative characteristics of financial information

Conceptual and regulatory framework

Conceptual framework incorporates regarding the quantitative and subjective issues. The

structure can be followed by various disciplines but it particularly accompanying to financial

reporting, a regulatory and conceptual framework which is provided by IASB. It provides better

information and financial data so that Mark & Spencer can take better decisions and effectively

control its operational activities. It helps to develop relevant ideas to evaluate essential capital

support. Organisation can use regulatory and conceptual framework to control its unnecessary

financial activities and follows the rules and regulations as per the guidelines of IASB. These

guidelines are forced as IFRS. Necessity of IFRS are as follows:

Fundamental accounting concepts are set and controlled by International financial

reporting standards. IFRS can be use by companies for better control and it improves accounting

controls and the standards (Kim and Zhou, 2014).

Qualitative characteristics which makes financial information realistic:

International financial reporting standards are extensively used by companies so that it

can it can set its standards as per the rules and regulations of IFRS. It is essential at international

level so that financial information can be get more accurately and reliable. International financial

reporting standards are recognised by the international Organisation of Securities Commission

for the purpose of utilization IFRS for effective management and control in the company. So

Mark & Spencer can apply this concept and improves it financial management system (Jung,

and Weber, 2014).

3. Stakeholders of an organisation and its benefits from financial information

Stakeholders

Stakeholders are the group of persons who have interest in the company. From the

decisions and actions of an organisation they can get influenced and their interest has affected. It

involves directors, employees, suppliers, creditors, government, shareholders etc. These are the

authorise persons which associated with investment and other organisational decisions. Business

of Mark & Spencer can affect the stakeholders in both positive and negative way.

Internal stakeholders of Mark & Spencer and its benefits from financial information

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stakeholders are the group of persons or individuals who can get influenced by a strategy

or project of company. It involves management, employees, owners and shareholders who have

some interest whether directly or indirectly in the organisation. Internal management of Mark &

Spencer can be affected by the actions or activities of internal stakeholder. It helps to an

organisation to accomplish its goals and objectives because they are connected with corporation

and engaged with its operational activities. It has been considered that less than fifty percent of

workers turnover counted in Mark & Spencer, its reflects the positive sign for the corporation.

Stakeholders can take their investment decisions on the basis of financial information of

company and its has good financial position as compare to the competitors (Hasnan and

Mahenthiran, 2012).

External stakeholders of Mark & Spencer and its benefits from financial information

External stakeholders are those persons who are associated with the organisation and can

be affected from the actions or decisions of company. External stakeholders of Mark & Spencer

are such as follows consultants, vendors, government regulators, suppliers, consumer and bank.

Consumers can take advantage by quality services and products of corporation, bank provides

better returns on the investment of it. So these group of persons can take benefit from the

financial information because on the behalf of this they make investment decisions. It shows the

intelligence of persons.

4) Importance of financial reporting in context of organisational objectives and growth

Financial reporting is essential for an organisation because it helps to a company

regarding expansion and investment decisions. Mark & Spencer can use this so that it can know

the financial position of its business. Importance of financial reporting are as follows:

Financial reporting can be used by company to enhanced their position and financial

structure. It helps the management to take effective decisions (Flower, 2016).

It provides useful information and data through which a company can know about its

financial position.

It provides the guidelines to an organisation and according to that they have to follow the

structure of financial report. Mark & Spencer can prepare its reports on the basis of

financial reporting system.

It helps the corporation to develops its strategies so that management can be enhanced.

or project of company. It involves management, employees, owners and shareholders who have

some interest whether directly or indirectly in the organisation. Internal management of Mark &

Spencer can be affected by the actions or activities of internal stakeholder. It helps to an

organisation to accomplish its goals and objectives because they are connected with corporation

and engaged with its operational activities. It has been considered that less than fifty percent of

workers turnover counted in Mark & Spencer, its reflects the positive sign for the corporation.

Stakeholders can take their investment decisions on the basis of financial information of

company and its has good financial position as compare to the competitors (Hasnan and

Mahenthiran, 2012).

External stakeholders of Mark & Spencer and its benefits from financial information

External stakeholders are those persons who are associated with the organisation and can

be affected from the actions or decisions of company. External stakeholders of Mark & Spencer

are such as follows consultants, vendors, government regulators, suppliers, consumer and bank.

Consumers can take advantage by quality services and products of corporation, bank provides

better returns on the investment of it. So these group of persons can take benefit from the

financial information because on the behalf of this they make investment decisions. It shows the

intelligence of persons.

4) Importance of financial reporting in context of organisational objectives and growth

Financial reporting is essential for an organisation because it helps to a company

regarding expansion and investment decisions. Mark & Spencer can use this so that it can know

the financial position of its business. Importance of financial reporting are as follows:

Financial reporting can be used by company to enhanced their position and financial

structure. It helps the management to take effective decisions (Flower, 2016).

It provides useful information and data through which a company can know about its

financial position.

It provides the guidelines to an organisation and according to that they have to follow the

structure of financial report. Mark & Spencer can prepare its reports on the basis of

financial reporting system.

It helps the corporation to develops its strategies so that management can be enhanced.

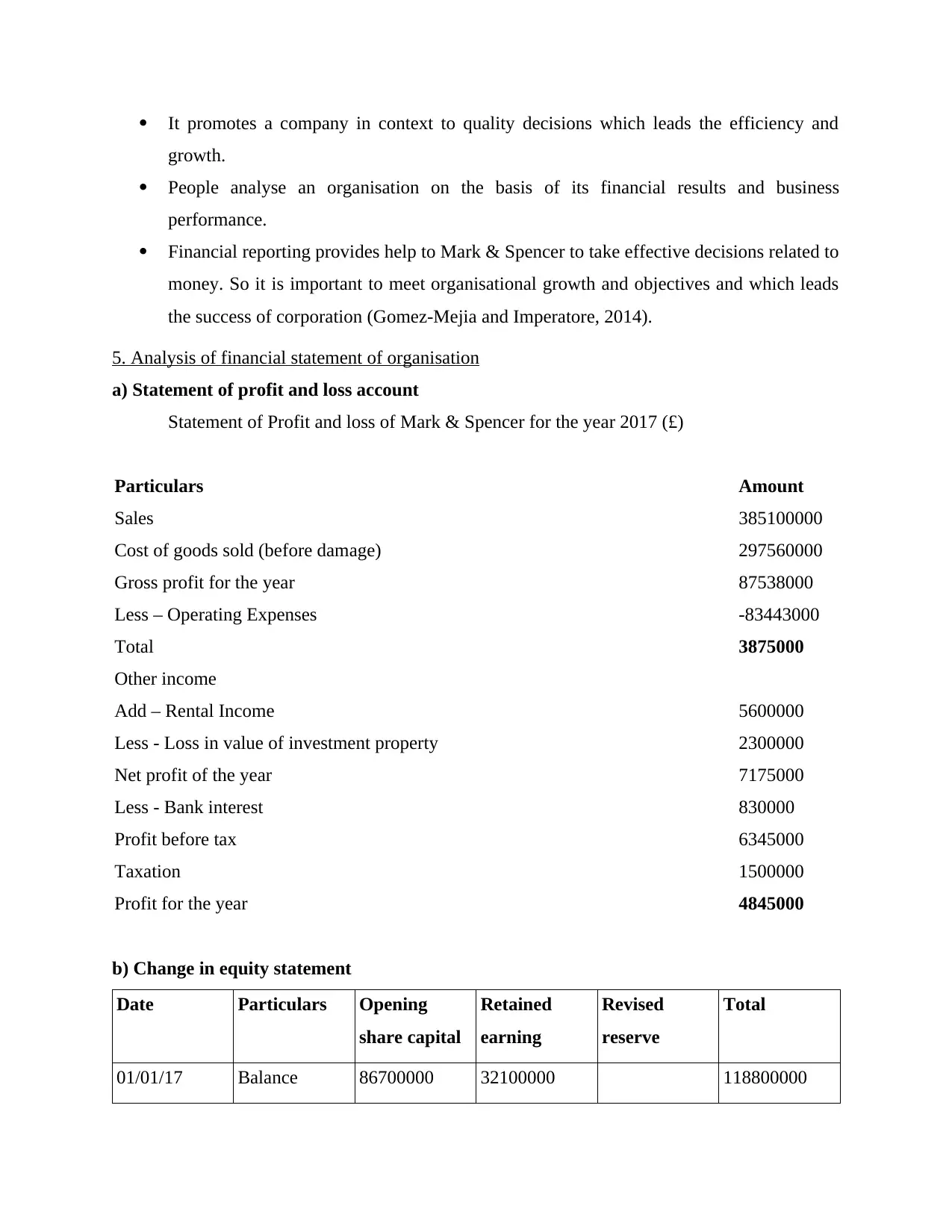

It promotes a company in context to quality decisions which leads the efficiency and

growth.

People analyse an organisation on the basis of its financial results and business

performance.

Financial reporting provides help to Mark & Spencer to take effective decisions related to

money. So it is important to meet organisational growth and objectives and which leads

the success of corporation (Gomez-Mejia and Imperatore, 2014).

5. Analysis of financial statement of organisation

a) Statement of profit and loss account

Statement of Profit and loss of Mark & Spencer for the year 2017 (£)

Particulars Amount

Sales 385100000

Cost of goods sold (before damage) 297560000

Gross profit for the year 87538000

Less – Operating Expenses -83443000

Total 3875000

Other income

Add – Rental Income 5600000

Less - Loss in value of investment property 2300000

Net profit of the year 7175000

Less - Bank interest 830000

Profit before tax 6345000

Taxation 1500000

Profit for the year 4845000

b) Change in equity statement

Date Particulars Opening

share capital

Retained

earning

Revised

reserve

Total

01/01/17 Balance 86700000 32100000 118800000

growth.

People analyse an organisation on the basis of its financial results and business

performance.

Financial reporting provides help to Mark & Spencer to take effective decisions related to

money. So it is important to meet organisational growth and objectives and which leads

the success of corporation (Gomez-Mejia and Imperatore, 2014).

5. Analysis of financial statement of organisation

a) Statement of profit and loss account

Statement of Profit and loss of Mark & Spencer for the year 2017 (£)

Particulars Amount

Sales 385100000

Cost of goods sold (before damage) 297560000

Gross profit for the year 87538000

Less – Operating Expenses -83443000

Total 3875000

Other income

Add – Rental Income 5600000

Less - Loss in value of investment property 2300000

Net profit of the year 7175000

Less - Bank interest 830000

Profit before tax 6345000

Taxation 1500000

Profit for the year 4845000

b) Change in equity statement

Date Particulars Opening

share capital

Retained

earning

Revised

reserve

Total

01/01/17 Balance 86700000 32100000 118800000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

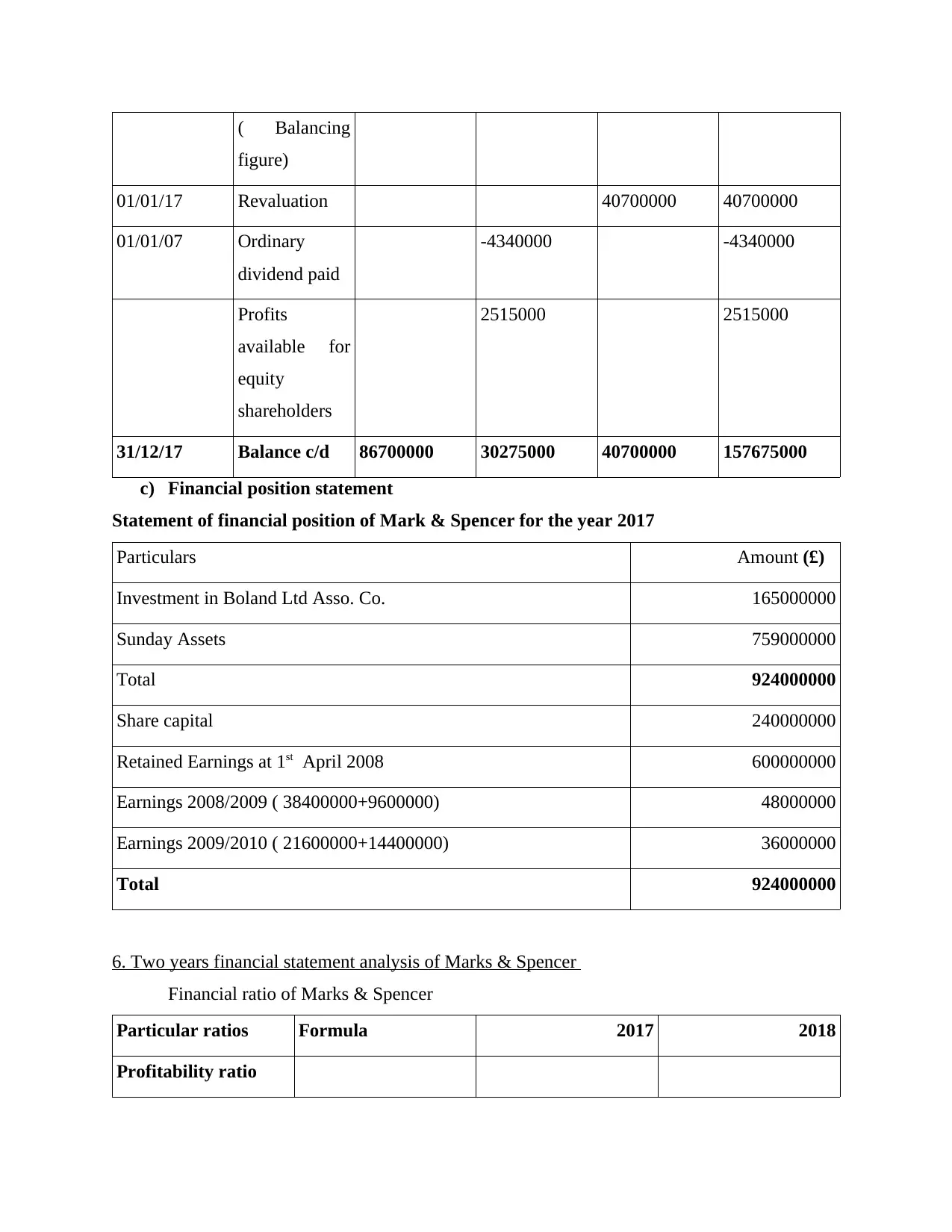

( Balancing

figure)

01/01/17 Revaluation 40700000 40700000

01/01/07 Ordinary

dividend paid

-4340000 -4340000

Profits

available for

equity

shareholders

2515000 2515000

31/12/17 Balance c/d 86700000 30275000 40700000 157675000

c) Financial position statement

Statement of financial position of Mark & Spencer for the year 2017

Particulars Amount (£)

Investment in Boland Ltd Asso. Co. 165000000

Sunday Assets 759000000

Total 924000000

Share capital 240000000

Retained Earnings at 1st April 2008 600000000

Earnings 2008/2009 ( 38400000+9600000) 48000000

Earnings 2009/2010 ( 21600000+14400000) 36000000

Total 924000000

6. Two years financial statement analysis of Marks & Spencer

Financial ratio of Marks & Spencer

Particular ratios Formula 2017 2018

Profitability ratio

figure)

01/01/17 Revaluation 40700000 40700000

01/01/07 Ordinary

dividend paid

-4340000 -4340000

Profits

available for

equity

shareholders

2515000 2515000

31/12/17 Balance c/d 86700000 30275000 40700000 157675000

c) Financial position statement

Statement of financial position of Mark & Spencer for the year 2017

Particulars Amount (£)

Investment in Boland Ltd Asso. Co. 165000000

Sunday Assets 759000000

Total 924000000

Share capital 240000000

Retained Earnings at 1st April 2008 600000000

Earnings 2008/2009 ( 38400000+9600000) 48000000

Earnings 2009/2010 ( 21600000+14400000) 36000000

Total 924000000

6. Two years financial statement analysis of Marks & Spencer

Financial ratio of Marks & Spencer

Particular ratios Formula 2017 2018

Profitability ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

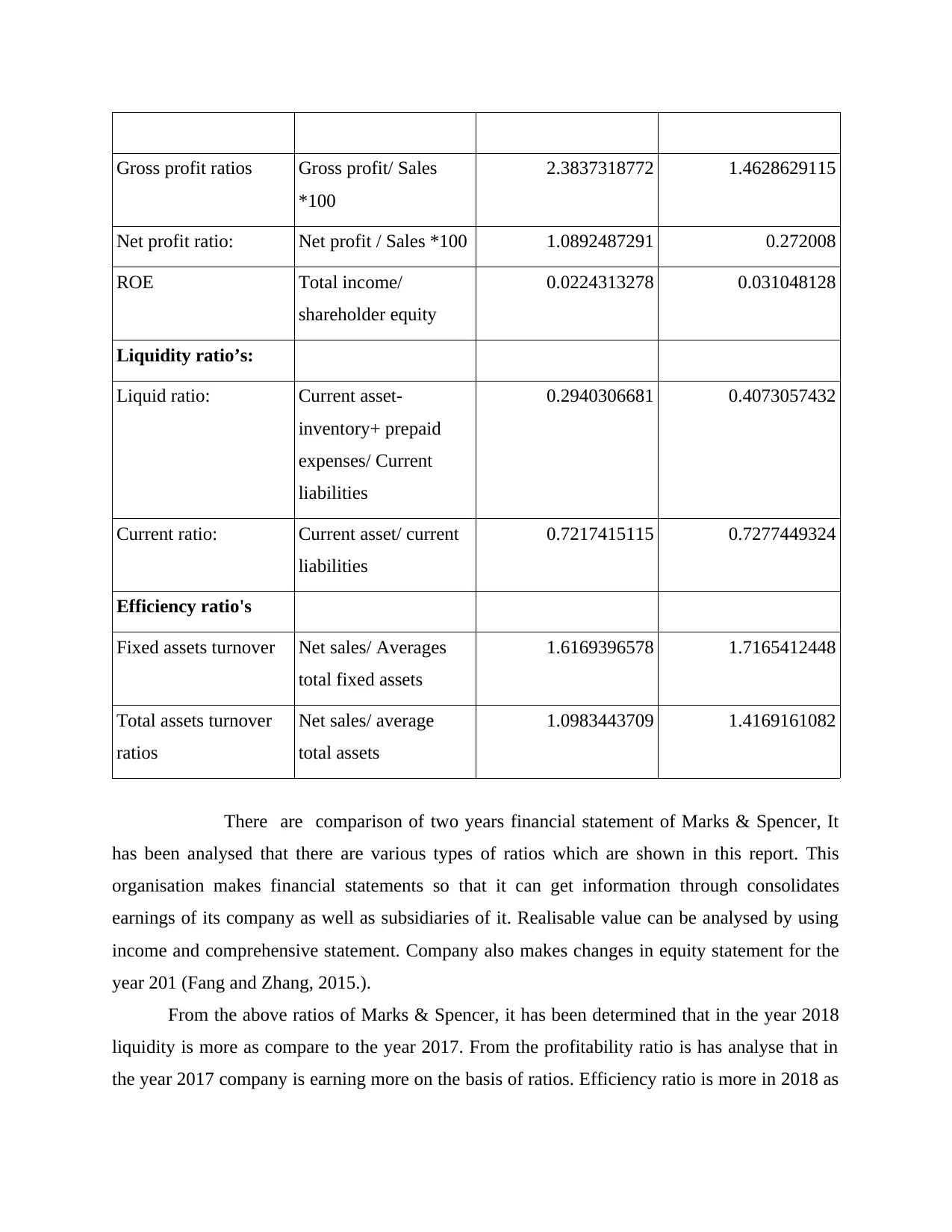

Gross profit ratios Gross profit/ Sales

*100

2.3837318772 1.4628629115

Net profit ratio: Net profit / Sales *100 1.0892487291 0.272008

ROE Total income/

shareholder equity

0.0224313278 0.031048128

Liquidity ratio’s:

Liquid ratio: Current asset-

inventory+ prepaid

expenses/ Current

liabilities

0.2940306681 0.4073057432

Current ratio: Current asset/ current

liabilities

0.7217415115 0.7277449324

Efficiency ratio's

Fixed assets turnover Net sales/ Averages

total fixed assets

1.6169396578 1.7165412448

Total assets turnover

ratios

Net sales/ average

total assets

1.0983443709 1.4169161082

There are comparison of two years financial statement of Marks & Spencer, It

has been analysed that there are various types of ratios which are shown in this report. This

organisation makes financial statements so that it can get information through consolidates

earnings of its company as well as subsidiaries of it. Realisable value can be analysed by using

income and comprehensive statement. Company also makes changes in equity statement for the

year 201 (Fang and Zhang, 2015.).

From the above ratios of Marks & Spencer, it has been determined that in the year 2018

liquidity is more as compare to the year 2017. From the profitability ratio is has analyse that in

the year 2017 company is earning more on the basis of ratios. Efficiency ratio is more in 2018 as

*100

2.3837318772 1.4628629115

Net profit ratio: Net profit / Sales *100 1.0892487291 0.272008

ROE Total income/

shareholder equity

0.0224313278 0.031048128

Liquidity ratio’s:

Liquid ratio: Current asset-

inventory+ prepaid

expenses/ Current

liabilities

0.2940306681 0.4073057432

Current ratio: Current asset/ current

liabilities

0.7217415115 0.7277449324

Efficiency ratio's

Fixed assets turnover Net sales/ Averages

total fixed assets

1.6169396578 1.7165412448

Total assets turnover

ratios

Net sales/ average

total assets

1.0983443709 1.4169161082

There are comparison of two years financial statement of Marks & Spencer, It

has been analysed that there are various types of ratios which are shown in this report. This

organisation makes financial statements so that it can get information through consolidates

earnings of its company as well as subsidiaries of it. Realisable value can be analysed by using

income and comprehensive statement. Company also makes changes in equity statement for the

year 201 (Fang and Zhang, 2015.).

From the above ratios of Marks & Spencer, it has been determined that in the year 2018

liquidity is more as compare to the year 2017. From the profitability ratio is has analyse that in

the year 2017 company is earning more on the basis of ratios. Efficiency ratio is more in 2018 as

compare to 2017. It shows that organisation has invested in fixed assets so its returns are

increased.

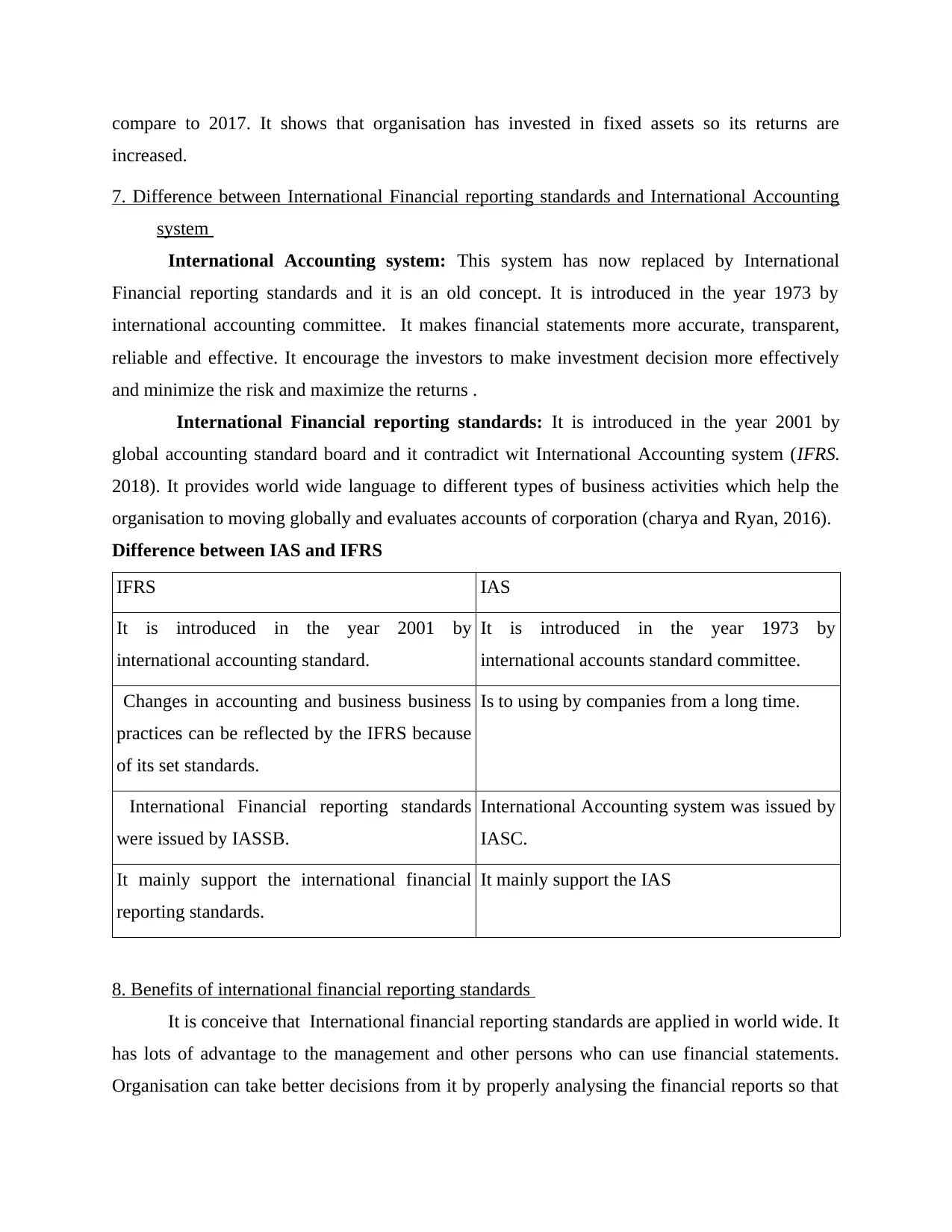

7. Difference between International Financial reporting standards and International Accounting

system

International Accounting system: This system has now replaced by International

Financial reporting standards and it is an old concept. It is introduced in the year 1973 by

international accounting committee. It makes financial statements more accurate, transparent,

reliable and effective. It encourage the investors to make investment decision more effectively

and minimize the risk and maximize the returns .

International Financial reporting standards: It is introduced in the year 2001 by

global accounting standard board and it contradict wit International Accounting system (IFRS.

2018). It provides world wide language to different types of business activities which help the

organisation to moving globally and evaluates accounts of corporation (charya and Ryan, 2016).

Difference between IAS and IFRS

IFRS IAS

It is introduced in the year 2001 by

international accounting standard.

It is introduced in the year 1973 by

international accounts standard committee.

Changes in accounting and business business

practices can be reflected by the IFRS because

of its set standards.

Is to using by companies from a long time.

International Financial reporting standards

were issued by IASSB.

International Accounting system was issued by

IASC.

It mainly support the international financial

reporting standards.

It mainly support the IAS

8. Benefits of international financial reporting standards

It is conceive that International financial reporting standards are applied in world wide. It

has lots of advantage to the management and other persons who can use financial statements.

Organisation can take better decisions from it by properly analysing the financial reports so that

increased.

7. Difference between International Financial reporting standards and International Accounting

system

International Accounting system: This system has now replaced by International

Financial reporting standards and it is an old concept. It is introduced in the year 1973 by

international accounting committee. It makes financial statements more accurate, transparent,

reliable and effective. It encourage the investors to make investment decision more effectively

and minimize the risk and maximize the returns .

International Financial reporting standards: It is introduced in the year 2001 by

global accounting standard board and it contradict wit International Accounting system (IFRS.

2018). It provides world wide language to different types of business activities which help the

organisation to moving globally and evaluates accounts of corporation (charya and Ryan, 2016).

Difference between IAS and IFRS

IFRS IAS

It is introduced in the year 2001 by

international accounting standard.

It is introduced in the year 1973 by

international accounts standard committee.

Changes in accounting and business business

practices can be reflected by the IFRS because

of its set standards.

Is to using by companies from a long time.

International Financial reporting standards

were issued by IASSB.

International Accounting system was issued by

IASC.

It mainly support the international financial

reporting standards.

It mainly support the IAS

8. Benefits of international financial reporting standards

It is conceive that International financial reporting standards are applied in world wide. It

has lots of advantage to the management and other persons who can use financial statements.

Organisation can take better decisions from it by properly analysing the financial reports so that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

it can take effective decisions in context to minimizing cost of investment and maximizing the r

returns. People properly analyse the reports and statements of Marks & Spencer and on the basis

of it they take investment decisions.

Effective comparability

Organisations can apply other standards as per the need and nature of business. So that it

is convenient for a company to compare with other corporations. In the world there are different

– different organisations who are established in various countries and they have applied its own

rules and regulations as per the government instructions of that nation. So it make the

comparison more effective because Marks & Spencer can apply those methods which can

generates more profits for it.

More flexibility

International financial reporting standards are based on the values rather than rules. It

provides freedom to an organisation to apply IFRS as per the needs and different situations. It

can help a corporation to accomplish its goals and objectives. (Chandar and Zheng, 2012).

Beneficial for new and small investors

International financial reporting standards provides help to the new and small investors

by provide appropriate and realist information which makes the analysing process simple and

easier. It is essential for Marks & Spencer to apply IFRS so that its investors can easily

understand the financial position of organisation and on the basis of this they can take investment

decisions.

9. Degrees of compliance with IFRS and its factors which influence company

International financial reporting standards are essential to be maintain and follow by the

companies. All organisations have to follow the rules, regulations and compliances which are

associated with it. Marks & Spencer can use this so that it can take advantage from it. It is

beneficial for the management as well as investors. Financial reporting system leads the

transparency and reliability in the financial statements of corporation. Through this more

accurate information can be communicate to the business which help the investors to take more

effective investment decisions. As a result they can generates more returns and earn more profits.

Compliances can make sure to the people that company has provided true and fair information to

the public. There are various factors which influence compliances with International financial

reporting standards are as described below:

returns. People properly analyse the reports and statements of Marks & Spencer and on the basis

of it they take investment decisions.

Effective comparability

Organisations can apply other standards as per the need and nature of business. So that it

is convenient for a company to compare with other corporations. In the world there are different

– different organisations who are established in various countries and they have applied its own

rules and regulations as per the government instructions of that nation. So it make the

comparison more effective because Marks & Spencer can apply those methods which can

generates more profits for it.

More flexibility

International financial reporting standards are based on the values rather than rules. It

provides freedom to an organisation to apply IFRS as per the needs and different situations. It

can help a corporation to accomplish its goals and objectives. (Chandar and Zheng, 2012).

Beneficial for new and small investors

International financial reporting standards provides help to the new and small investors

by provide appropriate and realist information which makes the analysing process simple and

easier. It is essential for Marks & Spencer to apply IFRS so that its investors can easily

understand the financial position of organisation and on the basis of this they can take investment

decisions.

9. Degrees of compliance with IFRS and its factors which influence company

International financial reporting standards are essential to be maintain and follow by the

companies. All organisations have to follow the rules, regulations and compliances which are

associated with it. Marks & Spencer can use this so that it can take advantage from it. It is

beneficial for the management as well as investors. Financial reporting system leads the

transparency and reliability in the financial statements of corporation. Through this more

accurate information can be communicate to the business which help the investors to take more

effective investment decisions. As a result they can generates more returns and earn more profits.

Compliances can make sure to the people that company has provided true and fair information to

the public. There are various factors which influence compliances with International financial

reporting standards are as described below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Size of the firm: Big companies have to follow more compliances as compare to the

small size of corporates. As a result it can protect their organisation from the government

interfere. It Marks & Spencer follow the compliances than its reputation can be enhanced in

market (Abbott and et. al,. 2016).

Profitability: If companies are earning more profits than it have to provide more accurate

information to its investor so that their belief can be increased and they can invest more.

Age of organisation: Old corporations areFang, V. W., Maffett, M. and Zhang, B., 2015.

more professional and they they know the importance of compliance in the company and its

benefits. It they does not follow than their reputation can be affected by it. New corporations

does not aware about the importance of compliances and if they does not maintain it than they

have to pay fine to the government.

IFRS provides help to an organisation to effectively follow the rules and regulations so

that its financial management can be enhanced.

CONCLUSION

From the above report, it has been concluded that financial reporting is very useful for the

organisation because it provides accurate and reliable information and data to company.

Framework and its principle of financial reporting can help the corporation to manage finance

effectively. By using IFRS Marks & Spencer can make effective control and take better

decisions for expansion and investment. Analysis of balance sheet, changes in equity and ratio

analysis provide help to corporation to know its financial position and wealth. Compliances

which are associated to IFRS can help to an organisation in following the rules and regulations

so that errors can be minimize.

small size of corporates. As a result it can protect their organisation from the government

interfere. It Marks & Spencer follow the compliances than its reputation can be enhanced in

market (Abbott and et. al,. 2016).

Profitability: If companies are earning more profits than it have to provide more accurate

information to its investor so that their belief can be increased and they can invest more.

Age of organisation: Old corporations areFang, V. W., Maffett, M. and Zhang, B., 2015.

more professional and they they know the importance of compliance in the company and its

benefits. It they does not follow than their reputation can be affected by it. New corporations

does not aware about the importance of compliances and if they does not maintain it than they

have to pay fine to the government.

IFRS provides help to an organisation to effectively follow the rules and regulations so

that its financial management can be enhanced.

CONCLUSION

From the above report, it has been concluded that financial reporting is very useful for the

organisation because it provides accurate and reliable information and data to company.

Framework and its principle of financial reporting can help the corporation to manage finance

effectively. By using IFRS Marks & Spencer can make effective control and take better

decisions for expansion and investment. Analysis of balance sheet, changes in equity and ratio

analysis provide help to corporation to know its financial position and wealth. Compliances

which are associated to IFRS can help to an organisation in following the rules and regulations

so that errors can be minimize.

REFERENCES

Books and Journals

Abbott, L. and et. al,. 2016. Internal audit quality and financial reporting quality: The joint

importance of independence and competence. Journal of Accounting Research. 54(1).

pp.3-40.

Chandar, N., Chang, H. and Zheng, X., 2012. Does overlapping membership on audit and

compensation committees improve a firm's financial reporting quality?. Review of

Accounting and Finance. 11(2). pp.141-165.

charya, V. V. and Ryan, S. G., 2016. Banks’ financial reporting and financial system stability.

Journal of Accounting Research. 54(2). pp.277-340.

Fang, V. W., Maffett, M. and Zhang, B., 2015. Foreign institutional ownership and the global

convergence of financial reporting practices. Journal of Accounting Research. 53(3).

pp.593-631.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Gavana, G., Guggiola, G. and Marenzi, A., 2013. Evolving connections between tax and

financial reporting in Italy. Accounting in Europe. 10(1). pp.43-70.

Gomez-Mejia, L., Cruz, C. and Imperatore, C., 2014. Financial reporting and the protection of

socioemotional wealth in family-controlled firms. European Accounting Review. 23(3).

pp.387-402.

Hasnan, S., Rahman, R. A. and Mahenthiran, S., 2012. Management motive, weak governance,

earnings management, and fraudulent financial reporting: Malaysian evidence. Journal

of International Accounting Research. 12(1). pp.1-27.

Jung, B., Lee, W. J. and Weber, D. P., 2014. Financial reporting quality and labor investment

efficiency. Contemporary Accounting Research. 31(4). pp.1047-1076.

Kim, J. B., Shi, H. and Zhou, J., 2014. International Financial Reporting Standards, institutional

infrastructures, and implied cost of equity capital around the world. Review of

Quantitative Finance and Accounting. 42(3). pp.469-507.

Shivakumar, L., 2013. The role of financial reporting in debt contracting and in stewardship.

Accounting and Business Research. 43(4). pp.362-383.

Online

IFRS. 2018. [ Online]. Available Through:

<https://www.investopedia.com/terms/i/ifrs.asp>

Books and Journals

Abbott, L. and et. al,. 2016. Internal audit quality and financial reporting quality: The joint

importance of independence and competence. Journal of Accounting Research. 54(1).

pp.3-40.

Chandar, N., Chang, H. and Zheng, X., 2012. Does overlapping membership on audit and

compensation committees improve a firm's financial reporting quality?. Review of

Accounting and Finance. 11(2). pp.141-165.

charya, V. V. and Ryan, S. G., 2016. Banks’ financial reporting and financial system stability.

Journal of Accounting Research. 54(2). pp.277-340.

Fang, V. W., Maffett, M. and Zhang, B., 2015. Foreign institutional ownership and the global

convergence of financial reporting practices. Journal of Accounting Research. 53(3).

pp.593-631.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Gavana, G., Guggiola, G. and Marenzi, A., 2013. Evolving connections between tax and

financial reporting in Italy. Accounting in Europe. 10(1). pp.43-70.

Gomez-Mejia, L., Cruz, C. and Imperatore, C., 2014. Financial reporting and the protection of

socioemotional wealth in family-controlled firms. European Accounting Review. 23(3).

pp.387-402.

Hasnan, S., Rahman, R. A. and Mahenthiran, S., 2012. Management motive, weak governance,

earnings management, and fraudulent financial reporting: Malaysian evidence. Journal

of International Accounting Research. 12(1). pp.1-27.

Jung, B., Lee, W. J. and Weber, D. P., 2014. Financial reporting quality and labor investment

efficiency. Contemporary Accounting Research. 31(4). pp.1047-1076.

Kim, J. B., Shi, H. and Zhou, J., 2014. International Financial Reporting Standards, institutional

infrastructures, and implied cost of equity capital around the world. Review of

Quantitative Finance and Accounting. 42(3). pp.469-507.

Shivakumar, L., 2013. The role of financial reporting in debt contracting and in stewardship.

Accounting and Business Research. 43(4). pp.362-383.

Online

IFRS. 2018. [ Online]. Available Through:

<https://www.investopedia.com/terms/i/ifrs.asp>

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.