Regulation of Financial Reporting System and Analysis of Equity and Debt Components in Mining Industry

VerifiedAdded on 2023/06/07

|15

|2823

|392

AI Summary

This report consists of a detailed analysis over the level of disclosure that should be maintained by an organization and also it has been discussed that it should be regulated in the managerial framework of an organization or not. The report also contains a discussion about IFRS and the AASB. The report will also be concluded with the study of four public companies based on their equity and debt components.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

qwertyuiopasdfghjklzxcvbnmqwertyui

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

HA2032 Corporate and Financial Accounting

opasdfghjklzxcvbnmqwertyuiopasdfgh

jklzxcvbnmqwertyuiopasdfghjklzxcvb

nmqwertyuiopasdfghjklzxcvbnmqwer

tyuiopasdfghjklzxcvbnmqwertyuiopas

dfghjklzxcvbnmqwertyuiopasdfghjklzx

cvbnmqwertyuiopasdfghjklzxcvbnmq

wertyuiopasdfghjklzxcvbnmqwertyuio

pasdfghjklzxcvbnmqwertyuiopasdfghj

klzxcvbnmqwertyuiopasdfghjklzxcvbn

mqwertyuiopasdfghjklzxcvbnmqwerty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmrty

uiopasdfghjklzxcvbnmqwertyuiopasdf

ghjklzxcvbnmqwertyuiopasdfghjklzxc

vbnmqwertyuiopasdfghjklzxcvbnmqw

HA2032 Corporate and Financial Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Financial accounting

Executive summary

It has been noticed that in today's world, organizations have increased the uses of financial

reporting in their systems and also have maintained levels of disclosure for maintaining good

relationships with their investors. However, the company should also maintain a level under

which it is disclosing the information to the investors. This report consists of a detailed analysis

over the level of disclosure that should be maintained by an organization and also it has been

discussed that it should be regulated in the managerial framework of an organization or not. The

report also contains a discussion about IFRS and the AASB. The report will also be concluded

with the study of four public companies based on their equity and debt components.

2

Executive summary

It has been noticed that in today's world, organizations have increased the uses of financial

reporting in their systems and also have maintained levels of disclosure for maintaining good

relationships with their investors. However, the company should also maintain a level under

which it is disclosing the information to the investors. This report consists of a detailed analysis

over the level of disclosure that should be maintained by an organization and also it has been

discussed that it should be regulated in the managerial framework of an organization or not. The

report also contains a discussion about IFRS and the AASB. The report will also be concluded

with the study of four public companies based on their equity and debt components.

2

Financial accounting

Contents

Introduction.................................................................................................................................................4

i. Corporate regulations..........................................................................................................................5

ii. Accounting standard setting.................................................................................................................5

Owner’s equity............................................................................................................................................7

iii. Item of equity.........................................................................................................................................7

iv. Comparative analysis of the debt and equity position...........................................................................10

Conclusion.................................................................................................................................................11

References.................................................................................................................................................12

Appendix...................................................................................................................................................13

Appendix – 1 Owner’s Equity.....................................................................................................................13

Appendix 2 - Comparative analysis of the debt and equity position.........................................................14

3

Contents

Introduction.................................................................................................................................................4

i. Corporate regulations..........................................................................................................................5

ii. Accounting standard setting.................................................................................................................5

Owner’s equity............................................................................................................................................7

iii. Item of equity.........................................................................................................................................7

iv. Comparative analysis of the debt and equity position...........................................................................10

Conclusion.................................................................................................................................................11

References.................................................................................................................................................12

Appendix...................................................................................................................................................13

Appendix – 1 Owner’s Equity.....................................................................................................................13

Appendix 2 - Comparative analysis of the debt and equity position.........................................................14

3

Financial accounting

Introduction

Every organization should try and disclose the required terms and conditions to various type of

user so that the decision-making process can be carried out by them. In today's world, it has been

observed that the principle of disclosure is not being able to fulfil the needs of the financial

reporting of users. The environment is divided between two groups of people among which half

are satisfied with the information they have been provided with and the other half is not satisfied

with the information and is earthling to know more about the financial statements of the

organization (Porter & Norton, 2014). Hence a regulation of financial reporting system should be

carried out so that the management can disclose certain information in relation to the financial

position of the company to the users. If the company or disclose the information voluntarily, then

it can face many issues in near future.

4

Introduction

Every organization should try and disclose the required terms and conditions to various type of

user so that the decision-making process can be carried out by them. In today's world, it has been

observed that the principle of disclosure is not being able to fulfil the needs of the financial

reporting of users. The environment is divided between two groups of people among which half

are satisfied with the information they have been provided with and the other half is not satisfied

with the information and is earthling to know more about the financial statements of the

organization (Porter & Norton, 2014). Hence a regulation of financial reporting system should be

carried out so that the management can disclose certain information in relation to the financial

position of the company to the users. If the company or disclose the information voluntarily, then

it can face many issues in near future.

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Financial accounting

i. Corporate regulations

There are a various set of information that is not to be disclosed by the organization as the

information is of no use to the normal public but if disclosed can damage the managerial

framework of the organization.

All the organizations of a similar industry should try and regulate under a common approach to

making any type of disclosure. The manager should try and not make any type of immaterial

disclosure which makes cause a loss to the organization. It is also the duty of the auditor to help

and make the particular disclosures that are needed to be disclosed by an organization and also

stop any irrelevant disclosures that are already being made by it (Vaitilingam, 2014). Every

organization should be regulated through a structured financial accounting system which will

help the manager to gain the freedom of disclosure of information on a voluntary basis. The use

of financial regulation will also help the users to compare the organization start with other

companies in the same industry. Regulation of control should be made in order to get more

reliable sources for disclosure of information. It should be duly noted by the manager that the

information is disclosed only on the basis of requirement and not on the voluntary basis.

Transparency should be maintained in the accounting statements as it satisfies the major

objective of financial reporting (Petty et. al, 2012). Hence, it can also be concluded that the

process of financial reporting is idealistic in nature and every organization should have a limit on

the information which is disclosed by them. The basic idea of transparency in the financial

reporting system means that necessary information should be conveyed to the users but not all

information should be conveyed voluntarily to them. Too much information will hamper the

objective of financial reporting and thus may lead to an insensible act to be carried out by the

organization (Parrino, Kidwell & Bates, 2012).

ii. Accounting standard setting

The international financial reporting system or IFRS can be defined as the unified term which

helps the organization to collect data and present them under the prescribed regulations of IASB.

The concept of IFRS contains broad strategic implementation which has been observed by the

FRC and AASB, thus making it necessary for the organizations reporting under Corporations Act

2001 to adopt this method in order to prepare their financial statements. The adoption of this

5

i. Corporate regulations

There are a various set of information that is not to be disclosed by the organization as the

information is of no use to the normal public but if disclosed can damage the managerial

framework of the organization.

All the organizations of a similar industry should try and regulate under a common approach to

making any type of disclosure. The manager should try and not make any type of immaterial

disclosure which makes cause a loss to the organization. It is also the duty of the auditor to help

and make the particular disclosures that are needed to be disclosed by an organization and also

stop any irrelevant disclosures that are already being made by it (Vaitilingam, 2014). Every

organization should be regulated through a structured financial accounting system which will

help the manager to gain the freedom of disclosure of information on a voluntary basis. The use

of financial regulation will also help the users to compare the organization start with other

companies in the same industry. Regulation of control should be made in order to get more

reliable sources for disclosure of information. It should be duly noted by the manager that the

information is disclosed only on the basis of requirement and not on the voluntary basis.

Transparency should be maintained in the accounting statements as it satisfies the major

objective of financial reporting (Petty et. al, 2012). Hence, it can also be concluded that the

process of financial reporting is idealistic in nature and every organization should have a limit on

the information which is disclosed by them. The basic idea of transparency in the financial

reporting system means that necessary information should be conveyed to the users but not all

information should be conveyed voluntarily to them. Too much information will hamper the

objective of financial reporting and thus may lead to an insensible act to be carried out by the

organization (Parrino, Kidwell & Bates, 2012).

ii. Accounting standard setting

The international financial reporting system or IFRS can be defined as the unified term which

helps the organization to collect data and present them under the prescribed regulations of IASB.

The concept of IFRS contains broad strategic implementation which has been observed by the

FRC and AASB, thus making it necessary for the organizations reporting under Corporations Act

2001 to adopt this method in order to prepare their financial statements. The adoption of this

5

Financial accounting

method also helps the organization to ensure if the financial statements have been prepared under

the guidelines of AASB. The AASB is said to have a neutral policy in relation to the transactions

which states that every event should be recorded in the accounts whether it is in the profit or non-

profit sector of the organization (Deegan, 2011).

The AASB has been observed to adopt different accounting standards in the Australian

accounting standards in order to fulfil the strategic guidance policy of the financial reporting

Council. It is very important for the ascertainment of the fact that every Organisation in the

industry is using the IFRS system issued by IASB in Australia because of the continuous nature

of the principle that is required by the financial accounting. It's been observed that the

international market will be strongly influenced by the adoption of IFRS system in the

accounting sector of the organizations because all the companies of Australia will have a

decreased capital displayed in their balance sheet.

It has also been clearly observed that the implementation of IFRS is not compulsory for all the

members using are applying IASB because of the huge changes in the process that will be

required to be made in the financial sector of the industries (Davies & Crawford, 2012). Making

changes in the financial sector of the organizations is not very easy because of the diverse reach

of these applications. Hence, it is not being made necessary for every country in the IASB be to

follow the IFRS based accounting system. However, it should also be noted that the adoption of

IFRS system in the accounting sector of the organization will help to boost the economy of the

country and will also provide various benefits to the organization. Many countries that are

following the principle of GAAP should also try and dropped the IFRS accounting system so that

uniformity can be maintained and convergence will not become a problem in future. Hence, it is

not necessary for every organization to adopt the IFRS system but they should try to adopt it so

that uniformity can be maintained and the users can also differentiate and compare the forms in a

much-elaborated manner.

6

method also helps the organization to ensure if the financial statements have been prepared under

the guidelines of AASB. The AASB is said to have a neutral policy in relation to the transactions

which states that every event should be recorded in the accounts whether it is in the profit or non-

profit sector of the organization (Deegan, 2011).

The AASB has been observed to adopt different accounting standards in the Australian

accounting standards in order to fulfil the strategic guidance policy of the financial reporting

Council. It is very important for the ascertainment of the fact that every Organisation in the

industry is using the IFRS system issued by IASB in Australia because of the continuous nature

of the principle that is required by the financial accounting. It's been observed that the

international market will be strongly influenced by the adoption of IFRS system in the

accounting sector of the organizations because all the companies of Australia will have a

decreased capital displayed in their balance sheet.

It has also been clearly observed that the implementation of IFRS is not compulsory for all the

members using are applying IASB because of the huge changes in the process that will be

required to be made in the financial sector of the industries (Davies & Crawford, 2012). Making

changes in the financial sector of the organizations is not very easy because of the diverse reach

of these applications. Hence, it is not being made necessary for every country in the IASB be to

follow the IFRS based accounting system. However, it should also be noted that the adoption of

IFRS system in the accounting sector of the organization will help to boost the economy of the

country and will also provide various benefits to the organization. Many countries that are

following the principle of GAAP should also try and dropped the IFRS accounting system so that

uniformity can be maintained and convergence will not become a problem in future. Hence, it is

not necessary for every organization to adopt the IFRS system but they should try to adopt it so

that uniformity can be maintained and the users can also differentiate and compare the forms in a

much-elaborated manner.

6

Financial accounting

Owner’s equity

iii. Item of equity

The basic equity component comprises three factors:

• Contributed equity

• Reserves

• Retained earnings

Contributed equity- this generally contains the share capital of the organization and also the

shares that are held in trust by the organization. The contributed equity of the organization

depicts the amount of share capital that is owned by the company itself. The shareholders are the

owners of the company and an increase in the contributed equity is noticed at the time of issue of

new shares (Ross et. al, 2014). The new shares are issued in order to collect cash from the public

in return for a share in the company. Bonus shares are also issued to the existing shareholders as

compiled with the policy of the company.

In the below listed for public companies the major items that constitute the equity funds are as

follows:

• Contributed equity

• Reserves

• Retained earnings

Reserves: the reserves consist of different type of hedging reserves, translation reserves of

foreign currencies, remuneration reserves and general reserves. Any gain or loss on a particular

derivative instrument is being settled with the help of hedging Reserve. The remuneration

reserve is being made in order to derive the amount payable as remuneration but is not been

calculated accurately. The main reason behind this inaccuracy is the constant enhancement or

decline in the remunerations that take place with the change in time. Asset revaluation reserve is

also maintained by the organization in order to revaluation results going to the depreciation or

any other fluctuation in their prices because of the environmental impacts. Whereas the general

7

Owner’s equity

iii. Item of equity

The basic equity component comprises three factors:

• Contributed equity

• Reserves

• Retained earnings

Contributed equity- this generally contains the share capital of the organization and also the

shares that are held in trust by the organization. The contributed equity of the organization

depicts the amount of share capital that is owned by the company itself. The shareholders are the

owners of the company and an increase in the contributed equity is noticed at the time of issue of

new shares (Ross et. al, 2014). The new shares are issued in order to collect cash from the public

in return for a share in the company. Bonus shares are also issued to the existing shareholders as

compiled with the policy of the company.

In the below listed for public companies the major items that constitute the equity funds are as

follows:

• Contributed equity

• Reserves

• Retained earnings

Reserves: the reserves consist of different type of hedging reserves, translation reserves of

foreign currencies, remuneration reserves and general reserves. Any gain or loss on a particular

derivative instrument is being settled with the help of hedging Reserve. The remuneration

reserve is being made in order to derive the amount payable as remuneration but is not been

calculated accurately. The main reason behind this inaccuracy is the constant enhancement or

decline in the remunerations that take place with the change in time. Asset revaluation reserve is

also maintained by the organization in order to revaluation results going to the depreciation or

any other fluctuation in their prices because of the environmental impacts. Whereas the general

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial accounting

reserve is maintained in order to protect the organization in the time of need so that the functions

can be carried out at ease and flexibility.

Retained earnings: retained earnings are designing’s that are kept aside by an organization from

the total profit earned by it in order to enhance the operations of the organization and meet other

contingencies of the company in near future. These types of earnings are very important as they

also mean ploughing back of profit and also a safety reserve can be created with the help of these

earnings.

BHP Billiton

Refer Appendix- 1

It has been observed that the overall business of the organization have declined in the previous

years and may also result in it to fall in the market. The major reason behind this fall will be the

employee share awards that were exercised by the organization (BHP Billiton, 2017). There was

a huge reduction of reserves of the company and also transfers were to be made for the employee

share awards.

Fortescue

Refer Appendix 1

When analyzing fast moving consumer goods, the common stock of the organization was witness

to have an increase while the level of equity of the organization was observed to decline. A

deficiency has been noticed in the accumulated comprehensive income of the organization

because of the problems faced by it in the mining fields and other businesses (Fortescue Metals

Group, 2017).

Rio Tinto

Refer Appendix 1

The organization Rio Tinto was observed to have sufficient retained earnings and also it was

having an accumulated and comprehensive financial statement. The huge retained earnings of the

organization world because of the heavy profits earned by the organization in previous years

(Rio Tinto, 2017). High accumulated and comprehensive income was noticed in the financial

8

reserve is maintained in order to protect the organization in the time of need so that the functions

can be carried out at ease and flexibility.

Retained earnings: retained earnings are designing’s that are kept aside by an organization from

the total profit earned by it in order to enhance the operations of the organization and meet other

contingencies of the company in near future. These types of earnings are very important as they

also mean ploughing back of profit and also a safety reserve can be created with the help of these

earnings.

BHP Billiton

Refer Appendix- 1

It has been observed that the overall business of the organization have declined in the previous

years and may also result in it to fall in the market. The major reason behind this fall will be the

employee share awards that were exercised by the organization (BHP Billiton, 2017). There was

a huge reduction of reserves of the company and also transfers were to be made for the employee

share awards.

Fortescue

Refer Appendix 1

When analyzing fast moving consumer goods, the common stock of the organization was witness

to have an increase while the level of equity of the organization was observed to decline. A

deficiency has been noticed in the accumulated comprehensive income of the organization

because of the problems faced by it in the mining fields and other businesses (Fortescue Metals

Group, 2017).

Rio Tinto

Refer Appendix 1

The organization Rio Tinto was observed to have sufficient retained earnings and also it was

having an accumulated and comprehensive financial statement. The huge retained earnings of the

organization world because of the heavy profits earned by the organization in previous years

(Rio Tinto, 2017). High accumulated and comprehensive income was noticed in the financial

8

Financial accounting

statements of the organization because of the strong business conducted by the management staff

of Rio Tinto.

Orica Limited

Refer Appendix 1

It was observed for this organization that the equity component was falling continuously and a

fluctuation may result in its fall. This fall was a result of the huge increase in the material costs

of the organization because of existing contracts (Orica, 2017). However, it was also observed

that the company was having sufficient retained earnings which have been saved by it from the

profits it has earned in the past.

9

statements of the organization because of the strong business conducted by the management staff

of Rio Tinto.

Orica Limited

Refer Appendix 1

It was observed for this organization that the equity component was falling continuously and a

fluctuation may result in its fall. This fall was a result of the huge increase in the material costs

of the organization because of existing contracts (Orica, 2017). However, it was also observed

that the company was having sufficient retained earnings which have been saved by it from the

profits it has earned in the past.

9

Financial accounting

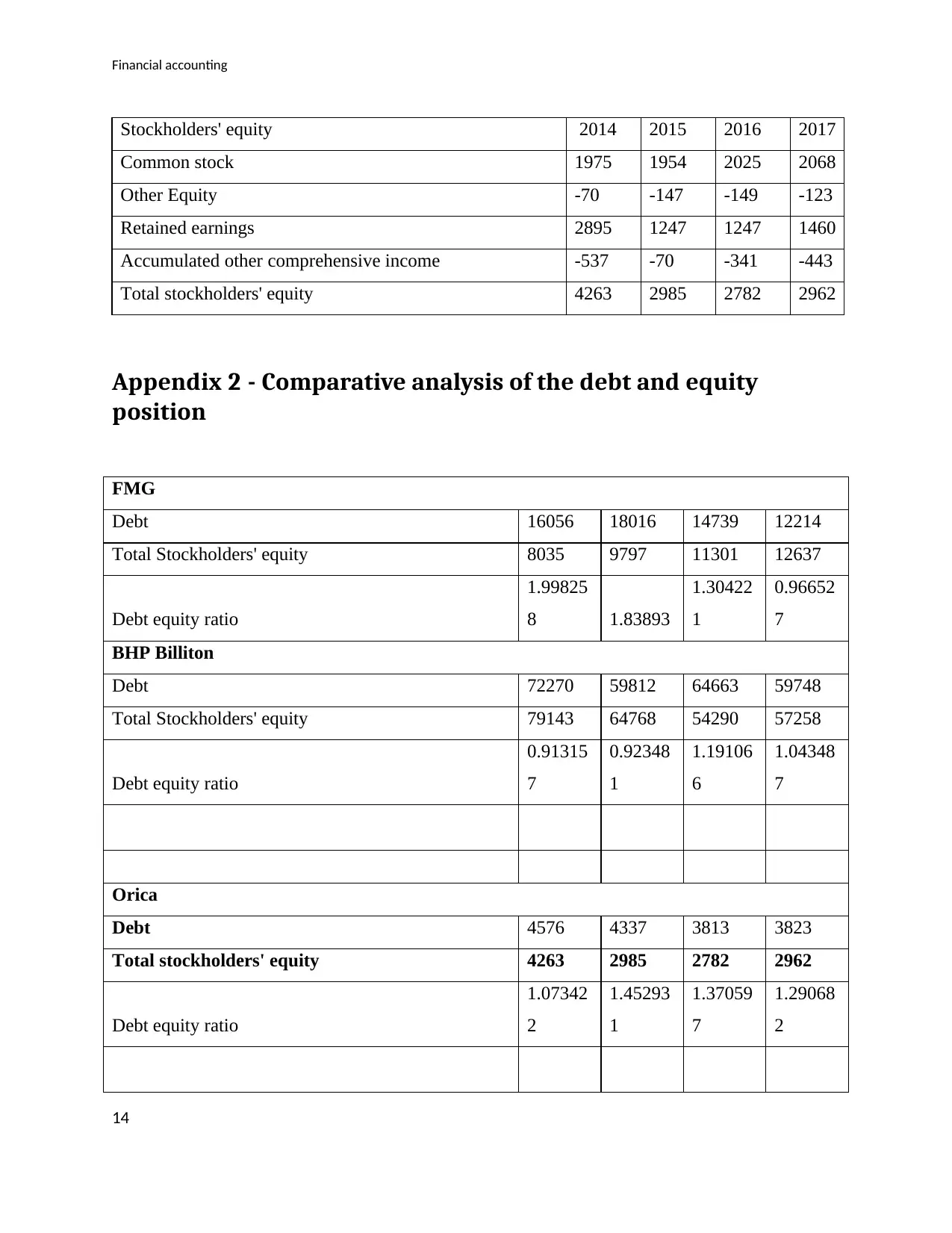

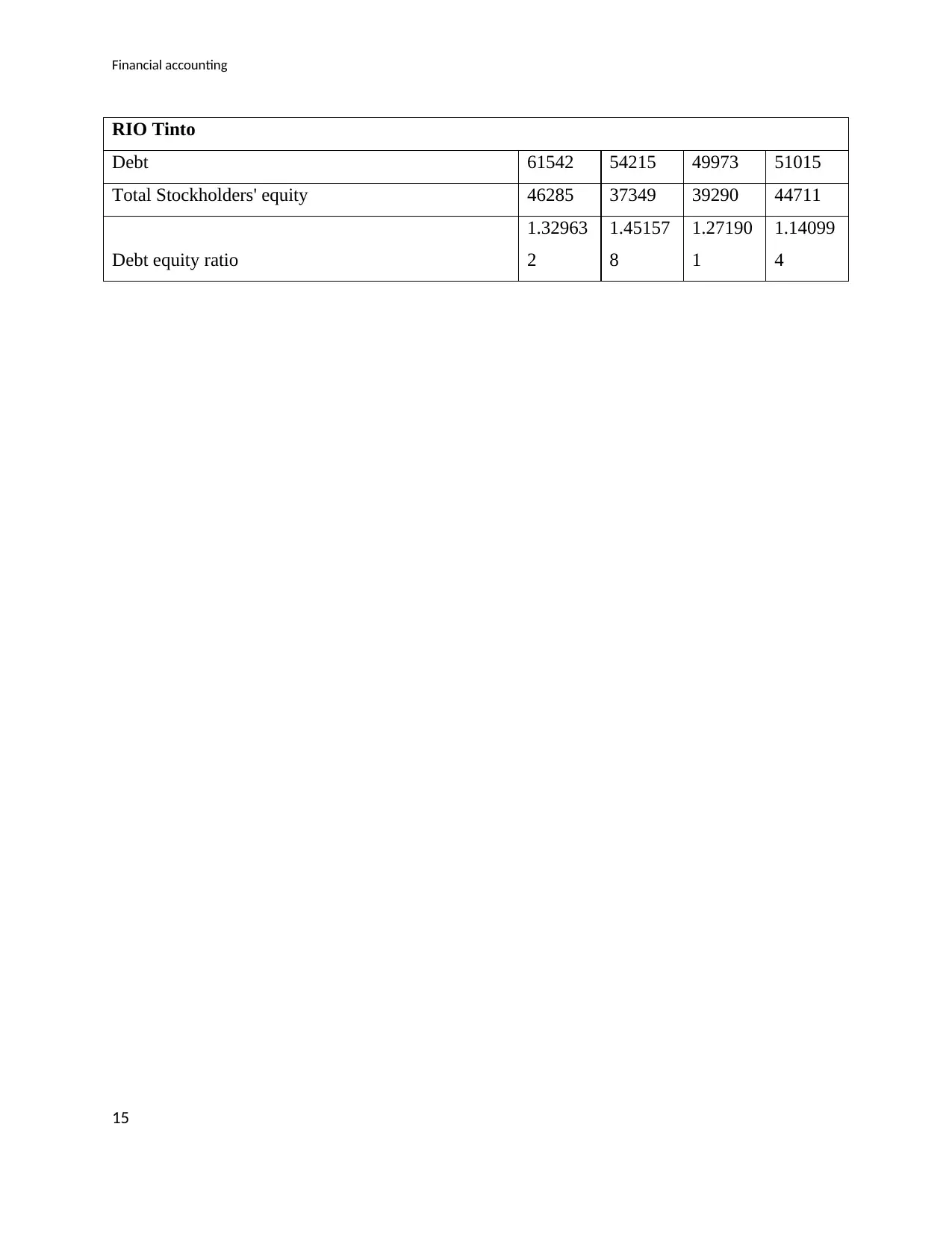

iv. Comparative analysis of the debt and equity position

Refer Appendix - 2

After the clear analysis of all the above data, it can be said that fast moving consumer goods are

having high debt to equity ratio which will affect the operations of the company and also may

cause a problem in fulfilment of the obligations. More points are needed to be driven towards the

payment of interest. The BHP Billiton organization is having equilibrium in the debt to equity

ratio which shows the efficiency of the management in relation to the financial structure of the

company. The company Orica make face problems in future if they continue to expand because

of the high debt to equity present in their financial structure. Rio Tinto even after having high

debt to equity can balance the same because of the high retained earnings that can be used in

order to fulfil the obligations. Even after a high debt to equity ratio the firm will recover all

losses with the help of exponential growth that is shown by it in the recent years.

10

iv. Comparative analysis of the debt and equity position

Refer Appendix - 2

After the clear analysis of all the above data, it can be said that fast moving consumer goods are

having high debt to equity ratio which will affect the operations of the company and also may

cause a problem in fulfilment of the obligations. More points are needed to be driven towards the

payment of interest. The BHP Billiton organization is having equilibrium in the debt to equity

ratio which shows the efficiency of the management in relation to the financial structure of the

company. The company Orica make face problems in future if they continue to expand because

of the high debt to equity present in their financial structure. Rio Tinto even after having high

debt to equity can balance the same because of the high retained earnings that can be used in

order to fulfil the obligations. Even after a high debt to equity ratio the firm will recover all

losses with the help of exponential growth that is shown by it in the recent years.

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Financial accounting

Conclusion

After the clear analysis of all the data present above, it can be stated that the managers of the

organization should try and not disclose any materials voluntarily. Also, proper disclosure of

financial documents should be regulated. The study of the top four companies in the Mining

industry has also helped us to understand the importance of maintaining equilibrium in the debt

to equity of an organization so that proper functioning can be achieved.

11

Conclusion

After the clear analysis of all the data present above, it can be stated that the managers of the

organization should try and not disclose any materials voluntarily. Also, proper disclosure of

financial documents should be regulated. The study of the top four companies in the Mining

industry has also helped us to understand the importance of maintaining equilibrium in the debt

to equity of an organization so that proper functioning can be achieved.

11

Financial accounting

References

BHP Billiton. (2017) BHP Billiton annual report and accounts 2017. Available from:

https://www.bhp.com/investor-centre/annual-reporting-2017 [Accessed September 2018]

Davies, T. and Crawford, I. (2012) Financial accounting. Harlow, England: Pearson.

Deegan, C. M. (2011) In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Fortescue Metals Group. (2017) Fortescue Metal Group Annual report and accounts 2017

[Online]. Available at: https://www.fmgl.com.au/docs/default-source/default-document-library/

fy2017-annual-report.pdf?sfvrsn=1f931875_2 [Accessed 17 September 2018]

Orica. (2017) Orica Annual Report and accounts 2017 [online]. Available from:

http://www.orica.com/Investors/company-reports#.W5_QB84zbIU [Accessed 17 September

2018]

Parrino, R, Kidwell, D. & Bates, T. (2012) Fundamentals of corporate finance. Hoboken,

Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

Porter, G. and Norton, C. (2014) Financial Accounting: The Impact on Decision Maker. Texas:

Cengage Learning

Rio Tinto. (2017) Rio Tinto Annual Report and accounts 2017 [online]. Available from:

http://www.riotinto.com/documents/RT_2017_Annual_Report.pdf [Accessed 16 September

2018]

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. And Jordan, B.(2014)

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall.

12

References

BHP Billiton. (2017) BHP Billiton annual report and accounts 2017. Available from:

https://www.bhp.com/investor-centre/annual-reporting-2017 [Accessed September 2018]

Davies, T. and Crawford, I. (2012) Financial accounting. Harlow, England: Pearson.

Deegan, C. M. (2011) In Financial accounting theory. North Ryde, N.S.W: McGraw-Hill

Fortescue Metals Group. (2017) Fortescue Metal Group Annual report and accounts 2017

[Online]. Available at: https://www.fmgl.com.au/docs/default-source/default-document-library/

fy2017-annual-report.pdf?sfvrsn=1f931875_2 [Accessed 17 September 2018]

Orica. (2017) Orica Annual Report and accounts 2017 [online]. Available from:

http://www.orica.com/Investors/company-reports#.W5_QB84zbIU [Accessed 17 September

2018]

Parrino, R, Kidwell, D. & Bates, T. (2012) Fundamentals of corporate finance. Hoboken,

Petty, J. W, Titman, S., Keown, A. J., Martin, J. D., Burrow, M. and Nguyen, H. (2012)

Financial Management: Principles and Applications, 6th ed. Australia: Pearson Education

Australia.

Porter, G. and Norton, C. (2014) Financial Accounting: The Impact on Decision Maker. Texas:

Cengage Learning

Rio Tinto. (2017) Rio Tinto Annual Report and accounts 2017 [online]. Available from:

http://www.riotinto.com/documents/RT_2017_Annual_Report.pdf [Accessed 16 September

2018]

Ross, S., Christensen, M., Drew, M., Bianchi, R., Westerfield, R. And Jordan, B.(2014)

Fundamentals of Corporate Finance, 7th ed. North Ryde: McGraw-Hill Australia Pty Ltd.

Vaitilingam, R. (2014) The Financial Times Guide to Using the Financial Pages. London: FT

Prentice Hall.

12

Financial accounting

Appendix

Appendix – 1 Owner’s Equity

BHP Billiton

Stockholders' equity 2014 2015 2016 2017

Common stock 2255 2243 2243 2243

Retained earnings 74548 60044 49542 52618

Treasury stock -587 -76 -33 -3

Accumulated other comprehensive income 2927 2557 2538 2400

Total Stockholders' equity 79143 64768 54290 57258

Fortescue Metal Group

Stockholders' equity

Common stock 1368 1685 1752 1676

Other equity 71 60 44 51

Retained earnings 6593 8052 9504 10910

Accumulated other comprehensive income 2 0 0

Total Stockholders' equity 8035 9797 11301 12637

Rio Tinto

Stockholders' equity 2014 2015 2016 2017

Additional paid-in capital 9053 8474 8443 8666

Retained earnings 26110 19736 21631 23761

Accumulated other comprehensive income 11122 9139 9216 12284

Total Stockholders' equity 46285 37349 39290 44711

Orica Ltd

13

Appendix

Appendix – 1 Owner’s Equity

BHP Billiton

Stockholders' equity 2014 2015 2016 2017

Common stock 2255 2243 2243 2243

Retained earnings 74548 60044 49542 52618

Treasury stock -587 -76 -33 -3

Accumulated other comprehensive income 2927 2557 2538 2400

Total Stockholders' equity 79143 64768 54290 57258

Fortescue Metal Group

Stockholders' equity

Common stock 1368 1685 1752 1676

Other equity 71 60 44 51

Retained earnings 6593 8052 9504 10910

Accumulated other comprehensive income 2 0 0

Total Stockholders' equity 8035 9797 11301 12637

Rio Tinto

Stockholders' equity 2014 2015 2016 2017

Additional paid-in capital 9053 8474 8443 8666

Retained earnings 26110 19736 21631 23761

Accumulated other comprehensive income 11122 9139 9216 12284

Total Stockholders' equity 46285 37349 39290 44711

Orica Ltd

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial accounting

Stockholders' equity 2014 2015 2016 2017

Common stock 1975 1954 2025 2068

Other Equity -70 -147 -149 -123

Retained earnings 2895 1247 1247 1460

Accumulated other comprehensive income -537 -70 -341 -443

Total stockholders' equity 4263 2985 2782 2962

Appendix 2 - Comparative analysis of the debt and equity

position

FMG

Debt 16056 18016 14739 12214

Total Stockholders' equity 8035 9797 11301 12637

Debt equity ratio

1.99825

8 1.83893

1.30422

1

0.96652

7

BHP Billiton

Debt 72270 59812 64663 59748

Total Stockholders' equity 79143 64768 54290 57258

Debt equity ratio

0.91315

7

0.92348

1

1.19106

6

1.04348

7

Orica

Debt 4576 4337 3813 3823

Total stockholders' equity 4263 2985 2782 2962

Debt equity ratio

1.07342

2

1.45293

1

1.37059

7

1.29068

2

14

Stockholders' equity 2014 2015 2016 2017

Common stock 1975 1954 2025 2068

Other Equity -70 -147 -149 -123

Retained earnings 2895 1247 1247 1460

Accumulated other comprehensive income -537 -70 -341 -443

Total stockholders' equity 4263 2985 2782 2962

Appendix 2 - Comparative analysis of the debt and equity

position

FMG

Debt 16056 18016 14739 12214

Total Stockholders' equity 8035 9797 11301 12637

Debt equity ratio

1.99825

8 1.83893

1.30422

1

0.96652

7

BHP Billiton

Debt 72270 59812 64663 59748

Total Stockholders' equity 79143 64768 54290 57258

Debt equity ratio

0.91315

7

0.92348

1

1.19106

6

1.04348

7

Orica

Debt 4576 4337 3813 3823

Total stockholders' equity 4263 2985 2782 2962

Debt equity ratio

1.07342

2

1.45293

1

1.37059

7

1.29068

2

14

Financial accounting

RIO Tinto

Debt 61542 54215 49973 51015

Total Stockholders' equity 46285 37349 39290 44711

Debt equity ratio

1.32963

2

1.45157

8

1.27190

1

1.14099

4

15

RIO Tinto

Debt 61542 54215 49973 51015

Total Stockholders' equity 46285 37349 39290 44711

Debt equity ratio

1.32963

2

1.45157

8

1.27190

1

1.14099

4

15

1 out of 15

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.