ACC520: Financial Reporting Assignment Analysis and Evaluation

VerifiedAdded on 2023/04/08

|10

|1978

|472

Homework Assignment

AI Summary

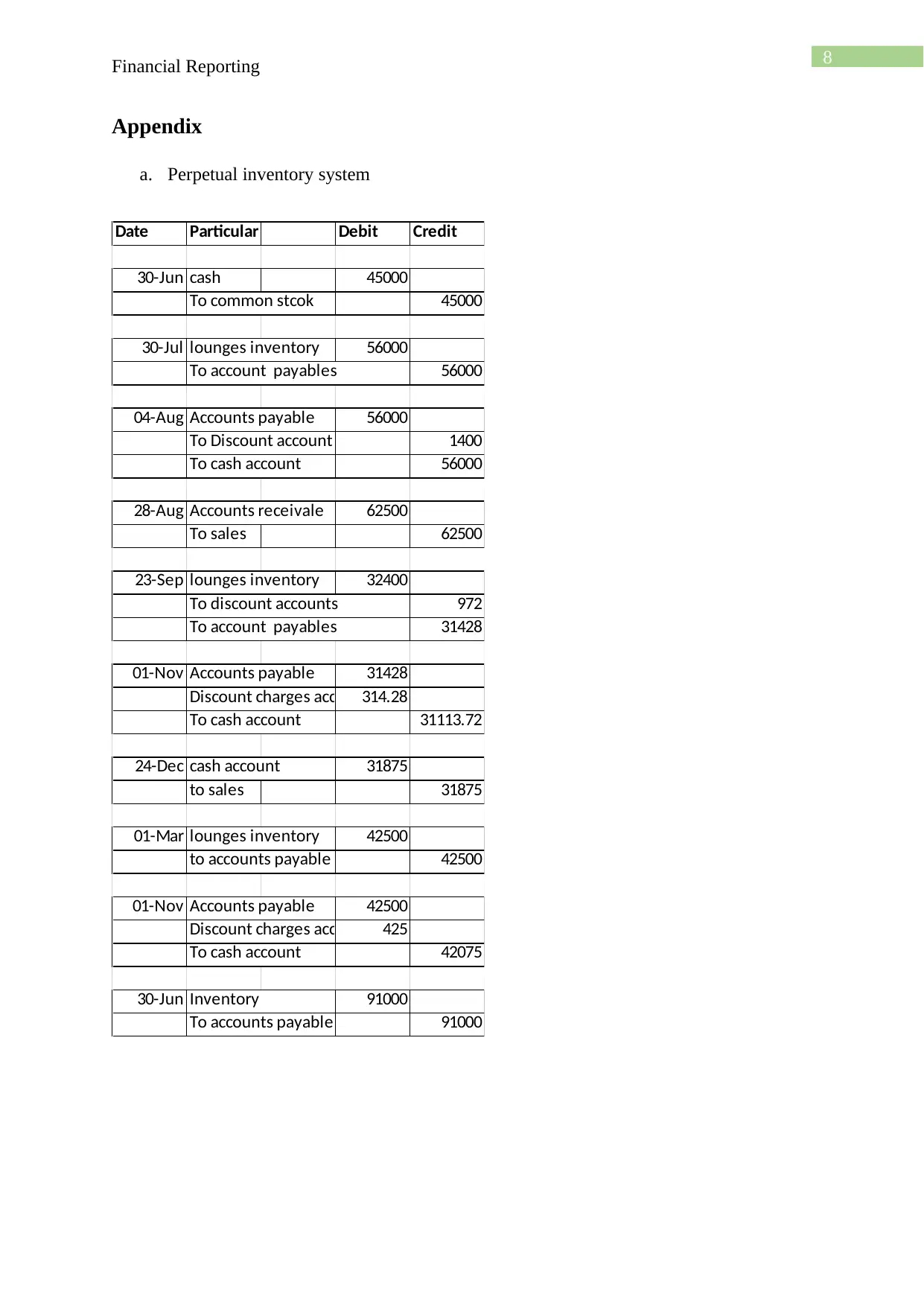

This assignment solution addresses key concepts in financial reporting, focusing on International Financial Reporting Standards (IFRS), corporate governance, and inventory management. It begins with an overview of IFRS, outlining its advantages (comparability, investor benefits, flexibility) and disadvantages (high cost, potential for manipulation, and limited global acceptance). The solution then analyzes a case study involving corporate governance failures, specifically violations of accountability, fairness, transparency, and responsibility. It examines the ethical and legal implications of misrepresenting financial statements and the roles of the board of directors and CFO. The assignment further delves into inventory valuation methods, comparing net realizable value and lower of cost methods, and contrasting periodic and perpetual inventory systems, including journal entries. The solution provides a comprehensive understanding of financial reporting principles and their practical application.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.