Importance of IFRS in Financial Reporting

VerifiedAdded on 2020/11/12

|15

|4197

|177

AI Summary

The report concludes that IFRS plays an integral role in financial statement preparation and reporting, ensuring transparency and neutrality. It is crucial for businesses to comply with IFRS standards to provide accurate and comparable financial information, enabling stakeholders to make informed decisions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL

REPORTING

REPORTING

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

1. Explanation of Financial Reporting and its purpose in business entity..................................1

2. Description regarding the requirement, purpose and principles of the regulatory and

conceptual framework ................................................................................................................3

3. Identification of the different stakeholders of the organisation and analysing the benefits of

financial information ..................................................................................................................4

4. Examining the meaning of financial reporting for meeting organisational objectives and

growth ........................................................................................................................................5

5. Interpretation of the financial statements of the business entity.............................................6

6. Evaluation of last two years of financial statements of company and their use to interpret

and communicate the financial performance..............................................................................8

7. Differentiation between IAS and IFRS.................................................................................10

8. Evaluation of the benefits of International Financial Reporting Standard (IFRS)................11

9. Ascertainment of varying degree of compliance associated to IFRS ..................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

MAIN BODY ..................................................................................................................................1

1. Explanation of Financial Reporting and its purpose in business entity..................................1

2. Description regarding the requirement, purpose and principles of the regulatory and

conceptual framework ................................................................................................................3

3. Identification of the different stakeholders of the organisation and analysing the benefits of

financial information ..................................................................................................................4

4. Examining the meaning of financial reporting for meeting organisational objectives and

growth ........................................................................................................................................5

5. Interpretation of the financial statements of the business entity.............................................6

6. Evaluation of last two years of financial statements of company and their use to interpret

and communicate the financial performance..............................................................................8

7. Differentiation between IAS and IFRS.................................................................................10

8. Evaluation of the benefits of International Financial Reporting Standard (IFRS)................11

9. Ascertainment of varying degree of compliance associated to IFRS ..................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The financial reporting refers to the process of preparing statements that depicts the

business entity's financial status to management, investors and the government. It involves the

communication of the financial information, such as financial statements to its internal and

external users. Financial reporting comprises with the preparation of the financial statements and

disclosure of the financial statements according to the International Financial Reporting

Standards. Reporting involves the financial statements like balance sheets, income statement,

statement of owner's equity and statement of cash flows. But the financial reporting is broader

concept than the preparation of the financial statement (Bertoni and De Rosa, 2012). Moreover,

the financial reporting pertain communication of all financial facts from the business to internal

users (it includes managing directors, BOD' s, equity shareholders etc.) and external users (it

includes the tax authorities, potential investors, government authorities, financial institutions).

This report pertain the information about the Mark and Spencer of United Kingdom. The

purpose of this report is show the context and aim of the financial reporting, requirements as well

as the principles of conceptual framework, stakeholders of the business entity, preparation and

the disclosure of the financial statements and their objectives. Along with this, the report also

pertain the context of benefits of International Financial Reporting standards (IFRS) and

International Accounting Standards (IAS). Although the difference between the IFRS and IAS

also mentioned in the report.

MAIN BODY

1. Explanation of Financial Reporting and its purpose in business entity

Financial Reporting is the form of financial results of a business entity to its useful users.

Financial reporting encompasses the financial statements which involves the consolidate incomes

statement, consolidate statement of balance sheet and consolidate statement of cash flows, along

with these statements the report pertain the footnote notes for more details regarding the relevant

accounting framework and events occurs after the preparation of financial statements of the

business entity like Mark and Spencer (UK). These financial statements are to disclose for its

useful users like the tax authorities, investors, managing directors, BOD' s, equity shareholders

etc. Moreover, the financial reporting consists disclosure of financial statements, press releases

and conference calls about the earning of quarters and other business entity's relevant

1

The financial reporting refers to the process of preparing statements that depicts the

business entity's financial status to management, investors and the government. It involves the

communication of the financial information, such as financial statements to its internal and

external users. Financial reporting comprises with the preparation of the financial statements and

disclosure of the financial statements according to the International Financial Reporting

Standards. Reporting involves the financial statements like balance sheets, income statement,

statement of owner's equity and statement of cash flows. But the financial reporting is broader

concept than the preparation of the financial statement (Bertoni and De Rosa, 2012). Moreover,

the financial reporting pertain communication of all financial facts from the business to internal

users (it includes managing directors, BOD' s, equity shareholders etc.) and external users (it

includes the tax authorities, potential investors, government authorities, financial institutions).

This report pertain the information about the Mark and Spencer of United Kingdom. The

purpose of this report is show the context and aim of the financial reporting, requirements as well

as the principles of conceptual framework, stakeholders of the business entity, preparation and

the disclosure of the financial statements and their objectives. Along with this, the report also

pertain the context of benefits of International Financial Reporting standards (IFRS) and

International Accounting Standards (IAS). Although the difference between the IFRS and IAS

also mentioned in the report.

MAIN BODY

1. Explanation of Financial Reporting and its purpose in business entity

Financial Reporting is the form of financial results of a business entity to its useful users.

Financial reporting encompasses the financial statements which involves the consolidate incomes

statement, consolidate statement of balance sheet and consolidate statement of cash flows, along

with these statements the report pertain the footnote notes for more details regarding the relevant

accounting framework and events occurs after the preparation of financial statements of the

business entity like Mark and Spencer (UK). These financial statements are to disclose for its

useful users like the tax authorities, investors, managing directors, BOD' s, equity shareholders

etc. Moreover, the financial reporting consists disclosure of financial statements, press releases

and conference calls about the earning of quarters and other business entity's relevant

1

information. Along with this, the annual or quarter reports of stockholders, disclosure of

financial report online on entity's website, disclosing reports to the government authorities as

well as the reports to the securities exchange commission (SEC). Overall, the Transparency of

financial records are beneficial in accomplishment of desired organisational goals that are

required to execute organisational operations(Nobes, 2014). Marks and Spencer is prepares and

reports the financial statements in order to make smooth functioning of business entity and to

perform all the business operations effectively. Purpose and importance of financial reporting is

as follows:

Financial reporting provides the financial information and helps the mangers of the

business entity like Marks and Spencer in performing their daily management activities

and the business operation.

It is beneficial in evaluating the market value, financial performance of the business

entity like Mark and Spencer for performing the management functioning like planning

and decision making.

Financial reporting ensures the transparency of the financial statements of the business by

the disclosing the annual reports to its internal and external users (Zimmerman, 2013).

Beneficial for managers in process of planning and controlling the future business

activities.

Financial reporting facilitates the annual results of the entity's operational work to

external stakeholders to increase sales with the motive to increase revenues and profit and

the market share.

Financial reporting helps the business entity in getting the funds or loans from the

financial institutions, as the reporting shows the financial position and the market share of

the entity so it helps in acquiring loans from the financial institution.

Importance of the Financial Reporting to the business entity

Financial reapportion is essential part of the accounting, as the report is use to analyse the

financial as well as the operational performance of the business entity.

Financial reporting is crucial for targeting the large number of potential investors.

It is inevitable in the process of decision making and planning for the future business

operations (Flower, 2016).

2

financial report online on entity's website, disclosing reports to the government authorities as

well as the reports to the securities exchange commission (SEC). Overall, the Transparency of

financial records are beneficial in accomplishment of desired organisational goals that are

required to execute organisational operations(Nobes, 2014). Marks and Spencer is prepares and

reports the financial statements in order to make smooth functioning of business entity and to

perform all the business operations effectively. Purpose and importance of financial reporting is

as follows:

Financial reporting provides the financial information and helps the mangers of the

business entity like Marks and Spencer in performing their daily management activities

and the business operation.

It is beneficial in evaluating the market value, financial performance of the business

entity like Mark and Spencer for performing the management functioning like planning

and decision making.

Financial reporting ensures the transparency of the financial statements of the business by

the disclosing the annual reports to its internal and external users (Zimmerman, 2013).

Beneficial for managers in process of planning and controlling the future business

activities.

Financial reporting facilitates the annual results of the entity's operational work to

external stakeholders to increase sales with the motive to increase revenues and profit and

the market share.

Financial reporting helps the business entity in getting the funds or loans from the

financial institutions, as the reporting shows the financial position and the market share of

the entity so it helps in acquiring loans from the financial institution.

Importance of the Financial Reporting to the business entity

Financial reapportion is essential part of the accounting, as the report is use to analyse the

financial as well as the operational performance of the business entity.

Financial reporting is crucial for targeting the large number of potential investors.

It is inevitable in the process of decision making and planning for the future business

operations (Flower, 2016).

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Financial reporting is also crucial for acquiring funds from abroad, while acquiring

foreign capital and investment then the perfect financial reporting is inevitable to attract

foreign investors.

It is important for making the comparatively analysis of the business entity with the other

entity. Also helps in comparison of past and present performance of the entity. This

comparison helps in ascertaining the performance as well as growth of the business

entity.

Financial reporting is very crucial in analysing the market position of the business entity

like Mark and Spencer.

Financial reporting of financial statements is inevitable for bidding bidding, government

supplies and labour contracts because it provides overview of the company to external

parties.

2. Description regarding the requirement, purpose and principles of the regulatory and

conceptual framework

Regulatory and Conceptual Framework: In the context of the financial reporting the

material fact of the conceptual framework pertain the dealing with the fundamental of financial

reporting issues like objectives and users of the annual reports, concepts that makes accounting

report useful, the context of the financial statements and the concepts of accounting that are

recognising concept and measuring concept must be considers in preparation of the annual

reports.

Regulatory framework pertain the rules and regulations framed by the UK government

and made mandatory to follow by all the business entities of UK. Marks and Spencer follows the

rules and regulations that are framed by the International Accounting Standard Board (IASB) as

it is beneficial for the entity in analysing the financial statements more effectively (Hope,

Thomas and Vyas, 2013). The regulations framed in the form of IFRS which is explained below:

International Financial Reporting Standards (IFRS): IFRS are introduced by the

board of International Accounting Standard (IAS). It is the framework comprises with the rules

and regulations which must followed by the business entities in context of preparation and

reporting of the financial statements. Some of the key principles are mentioned below:

3

foreign capital and investment then the perfect financial reporting is inevitable to attract

foreign investors.

It is important for making the comparatively analysis of the business entity with the other

entity. Also helps in comparison of past and present performance of the entity. This

comparison helps in ascertaining the performance as well as growth of the business

entity.

Financial reporting is very crucial in analysing the market position of the business entity

like Mark and Spencer.

Financial reporting of financial statements is inevitable for bidding bidding, government

supplies and labour contracts because it provides overview of the company to external

parties.

2. Description regarding the requirement, purpose and principles of the regulatory and

conceptual framework

Regulatory and Conceptual Framework: In the context of the financial reporting the

material fact of the conceptual framework pertain the dealing with the fundamental of financial

reporting issues like objectives and users of the annual reports, concepts that makes accounting

report useful, the context of the financial statements and the concepts of accounting that are

recognising concept and measuring concept must be considers in preparation of the annual

reports.

Regulatory framework pertain the rules and regulations framed by the UK government

and made mandatory to follow by all the business entities of UK. Marks and Spencer follows the

rules and regulations that are framed by the International Accounting Standard Board (IASB) as

it is beneficial for the entity in analysing the financial statements more effectively (Hope,

Thomas and Vyas, 2013). The regulations framed in the form of IFRS which is explained below:

International Financial Reporting Standards (IFRS): IFRS are introduced by the

board of International Accounting Standard (IAS). It is the framework comprises with the rules

and regulations which must followed by the business entities in context of preparation and

reporting of the financial statements. Some of the key principles are mentioned below:

3

IFRS 1: It is related with First-Time adoption of International Financial Reporting

Standards, adoption refers to follow and prepares as well as report the financial statements

according to IFRS schedule.

IFRS 3: It is concerned with the Business Combinations in context of merger and

acquisition.

IFRS 9: It is concerned with the Financial instruments, it means classification and

measurement of financial instruments, impairment of financial assets and hedge accounting.

IFRS 10: It is concerned with the Consolidate Financial Statements, refers to preparation

of the financial statements in consolidated format.

Purpose of the regulatory and conceptual framework are as follows.

Act as a guide in preparation and reporting of the annual report of business entity like

Mark and Spencer.

Ensuring preparation and reporting of annual reports of all business entities in single

consolidate format, that makes the task of comparison easy.

Ensures the global language of financial preparation and reporting so that the entities can

execute at international level by acquiring international capitals and investments.

Makes easy for government to understand the accounting practices and standards adapted

and followed by the entities in preparing and reporting of business reports (Zeff, 2013).

All these benefits and Principles of regulatory conceptual framework helps the Marks and

Spencer in prominent preparation and reporting of financial statement and in smooth as well as

long survival of business.

3. Identification of the different stakeholders of the organisation and analysing the benefits of

financial information

The stakeholders refers to the crucial individual members of the entity, as without their

support the entity would cease to exist. The stakeholders are of two types internal stakeholders

and the external stakeholders as all the entity has the stakeholders. The Mark and Spencer also

has several stakeholders who supports the entity in decision making, acquiring funds, future

operational planning and in making increment in sales. Some of the internal and the external

stakeholders of Business entity like Mark and Spencer are mentioned below:

4

Standards, adoption refers to follow and prepares as well as report the financial statements

according to IFRS schedule.

IFRS 3: It is concerned with the Business Combinations in context of merger and

acquisition.

IFRS 9: It is concerned with the Financial instruments, it means classification and

measurement of financial instruments, impairment of financial assets and hedge accounting.

IFRS 10: It is concerned with the Consolidate Financial Statements, refers to preparation

of the financial statements in consolidated format.

Purpose of the regulatory and conceptual framework are as follows.

Act as a guide in preparation and reporting of the annual report of business entity like

Mark and Spencer.

Ensuring preparation and reporting of annual reports of all business entities in single

consolidate format, that makes the task of comparison easy.

Ensures the global language of financial preparation and reporting so that the entities can

execute at international level by acquiring international capitals and investments.

Makes easy for government to understand the accounting practices and standards adapted

and followed by the entities in preparing and reporting of business reports (Zeff, 2013).

All these benefits and Principles of regulatory conceptual framework helps the Marks and

Spencer in prominent preparation and reporting of financial statement and in smooth as well as

long survival of business.

3. Identification of the different stakeholders of the organisation and analysing the benefits of

financial information

The stakeholders refers to the crucial individual members of the entity, as without their

support the entity would cease to exist. The stakeholders are of two types internal stakeholders

and the external stakeholders as all the entity has the stakeholders. The Mark and Spencer also

has several stakeholders who supports the entity in decision making, acquiring funds, future

operational planning and in making increment in sales. Some of the internal and the external

stakeholders of Business entity like Mark and Spencer are mentioned below:

4

Internal stakeholders: these are the stakeholders who are the internal parties of the

organisation and are directly related to the operational activities of the business (Bevis, 2013).

Some of the internal stakeholders are as follows.

Shareholders: it refers to the equity shareholders of the entity who has right to

participate in the several activities of the business, as they are the owners of the business

entity.

Managers : These are internal members and are responsible for the operational activities,

manages the functioning of the business.

External Stakeholders: These are stakeholder or the individual interacts with the

business entity form outside , means these are the external parties having no control over the

functioning of the business but can influence the functioning of entity(Botzem, 2012). Some of

external stakeholders are.

Customer: The customers are the individual who buys or purchases the goods and

services produced by the business entity like Mark and Spencer.

Investors: These are the potential fund providers of the organisation may be same

country or of different country(foreign investors).

Creditors: These are the potential creditors of the entity like Mark and Spencer, as the

entity has the obligations which is payable to them in future. Example of creditors are

financial intuitions etc.

4. Examining the meaning of financial reporting for meeting organisational objectives and

growth

Financial reporting is beneficial for the organisation in achieving the desired objectives of

the organisations like Mark and Spencer. As the it ensures the proper format of the preparation of

the financial statement which helps the organisation in ascertaining the financial as well as

operational performance of the organisation. Not only this, it also helps in accomplishment of the

objectives of Marks and Spencer, some of the objectives like targeting the potential investors,

targeting large number of customers and ensuring them full satisfaction and maximising profits

and sales. All the objectives can be accomplished with the help of transparency in financial

information of Marks and Spencer. Investors get attracted toward those entities which ascertain

the performance year by year and whose performance as well as the market value is good in the

economy and capable for giving higher return on their investments (Tan, 2013). As Marks and

5

organisation and are directly related to the operational activities of the business (Bevis, 2013).

Some of the internal stakeholders are as follows.

Shareholders: it refers to the equity shareholders of the entity who has right to

participate in the several activities of the business, as they are the owners of the business

entity.

Managers : These are internal members and are responsible for the operational activities,

manages the functioning of the business.

External Stakeholders: These are stakeholder or the individual interacts with the

business entity form outside , means these are the external parties having no control over the

functioning of the business but can influence the functioning of entity(Botzem, 2012). Some of

external stakeholders are.

Customer: The customers are the individual who buys or purchases the goods and

services produced by the business entity like Mark and Spencer.

Investors: These are the potential fund providers of the organisation may be same

country or of different country(foreign investors).

Creditors: These are the potential creditors of the entity like Mark and Spencer, as the

entity has the obligations which is payable to them in future. Example of creditors are

financial intuitions etc.

4. Examining the meaning of financial reporting for meeting organisational objectives and

growth

Financial reporting is beneficial for the organisation in achieving the desired objectives of

the organisations like Mark and Spencer. As the it ensures the proper format of the preparation of

the financial statement which helps the organisation in ascertaining the financial as well as

operational performance of the organisation. Not only this, it also helps in accomplishment of the

objectives of Marks and Spencer, some of the objectives like targeting the potential investors,

targeting large number of customers and ensuring them full satisfaction and maximising profits

and sales. All the objectives can be accomplished with the help of transparency in financial

information of Marks and Spencer. Investors get attracted toward those entities which ascertain

the performance year by year and whose performance as well as the market value is good in the

economy and capable for giving higher return on their investments (Tan, 2013). As Marks and

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Spencer maintains the accurate records which makes easy for the investors to analyse its

performance and than invest their funds in entity.

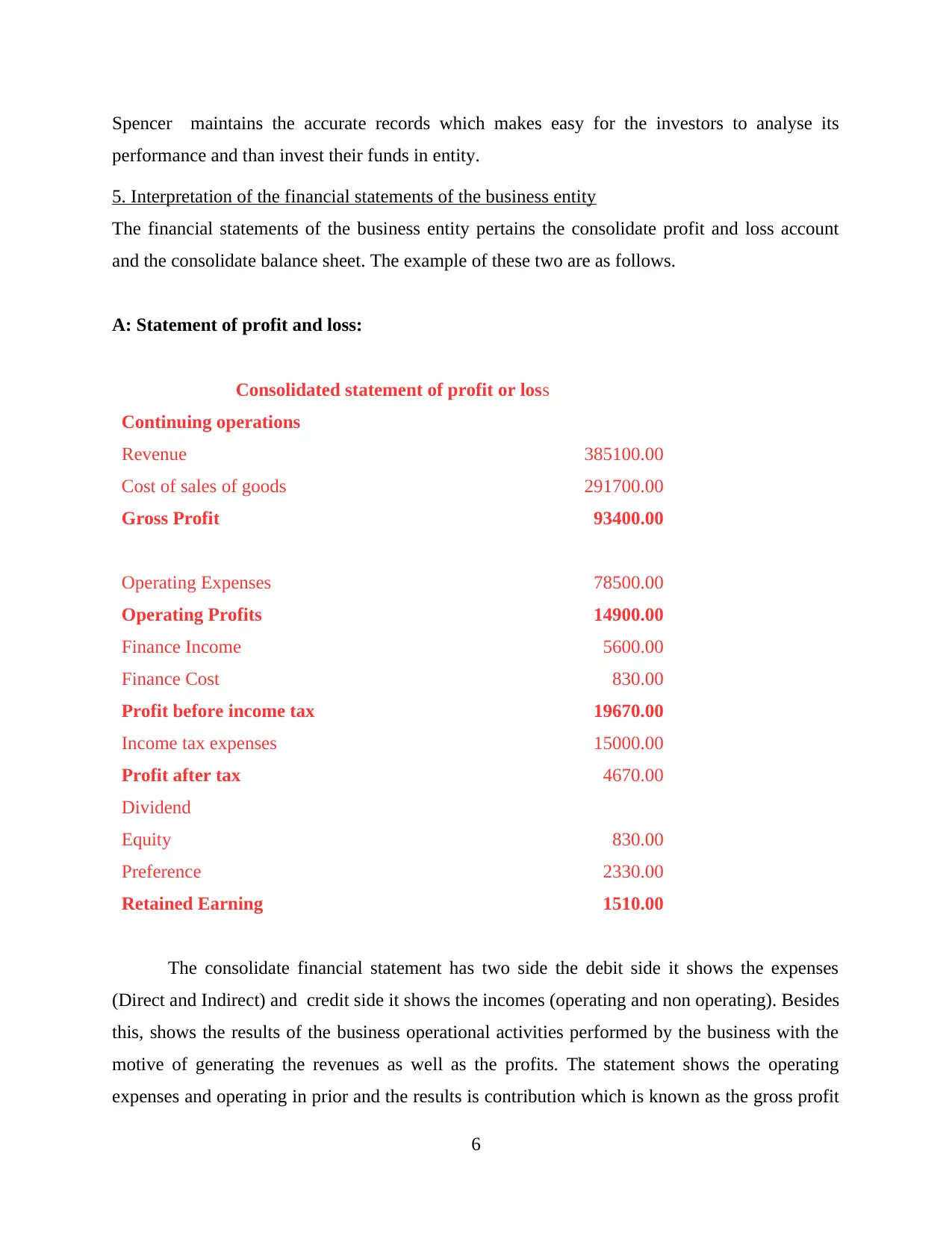

5. Interpretation of the financial statements of the business entity

The financial statements of the business entity pertains the consolidate profit and loss account

and the consolidate balance sheet. The example of these two are as follows.

A: Statement of profit and loss:

Consolidated statement of profit or loss

Continuing operations

Revenue 385100.00

Cost of sales of goods 291700.00

Gross Profit 93400.00

Operating Expenses 78500.00

Operating Profits 14900.00

Finance Income 5600.00

Finance Cost 830.00

Profit before income tax 19670.00

Income tax expenses 15000.00

Profit after tax 4670.00

Dividend

Equity 830.00

Preference 2330.00

Retained Earning 1510.00

The consolidate financial statement has two side the debit side it shows the expenses

(Direct and Indirect) and credit side it shows the incomes (operating and non operating). Besides

this, shows the results of the business operational activities performed by the business with the

motive of generating the revenues as well as the profits. The statement shows the operating

expenses and operating in prior and the results is contribution which is known as the gross profit

6

performance and than invest their funds in entity.

5. Interpretation of the financial statements of the business entity

The financial statements of the business entity pertains the consolidate profit and loss account

and the consolidate balance sheet. The example of these two are as follows.

A: Statement of profit and loss:

Consolidated statement of profit or loss

Continuing operations

Revenue 385100.00

Cost of sales of goods 291700.00

Gross Profit 93400.00

Operating Expenses 78500.00

Operating Profits 14900.00

Finance Income 5600.00

Finance Cost 830.00

Profit before income tax 19670.00

Income tax expenses 15000.00

Profit after tax 4670.00

Dividend

Equity 830.00

Preference 2330.00

Retained Earning 1510.00

The consolidate financial statement has two side the debit side it shows the expenses

(Direct and Indirect) and credit side it shows the incomes (operating and non operating). Besides

this, shows the results of the business operational activities performed by the business with the

motive of generating the revenues as well as the profits. The statement shows the operating

expenses and operating in prior and the results is contribution which is known as the gross profit

6

that is 93400, from the operating activities and then the statement shows the expenses and

incomes which are not related with the production and are known as the indirect expenses. At

last the final result shows the net profit which comes by deducting all indirect expenses from the

gross profit and from non operating income. The net profit that is 4670 transferable to the

balance sheet on liability side.

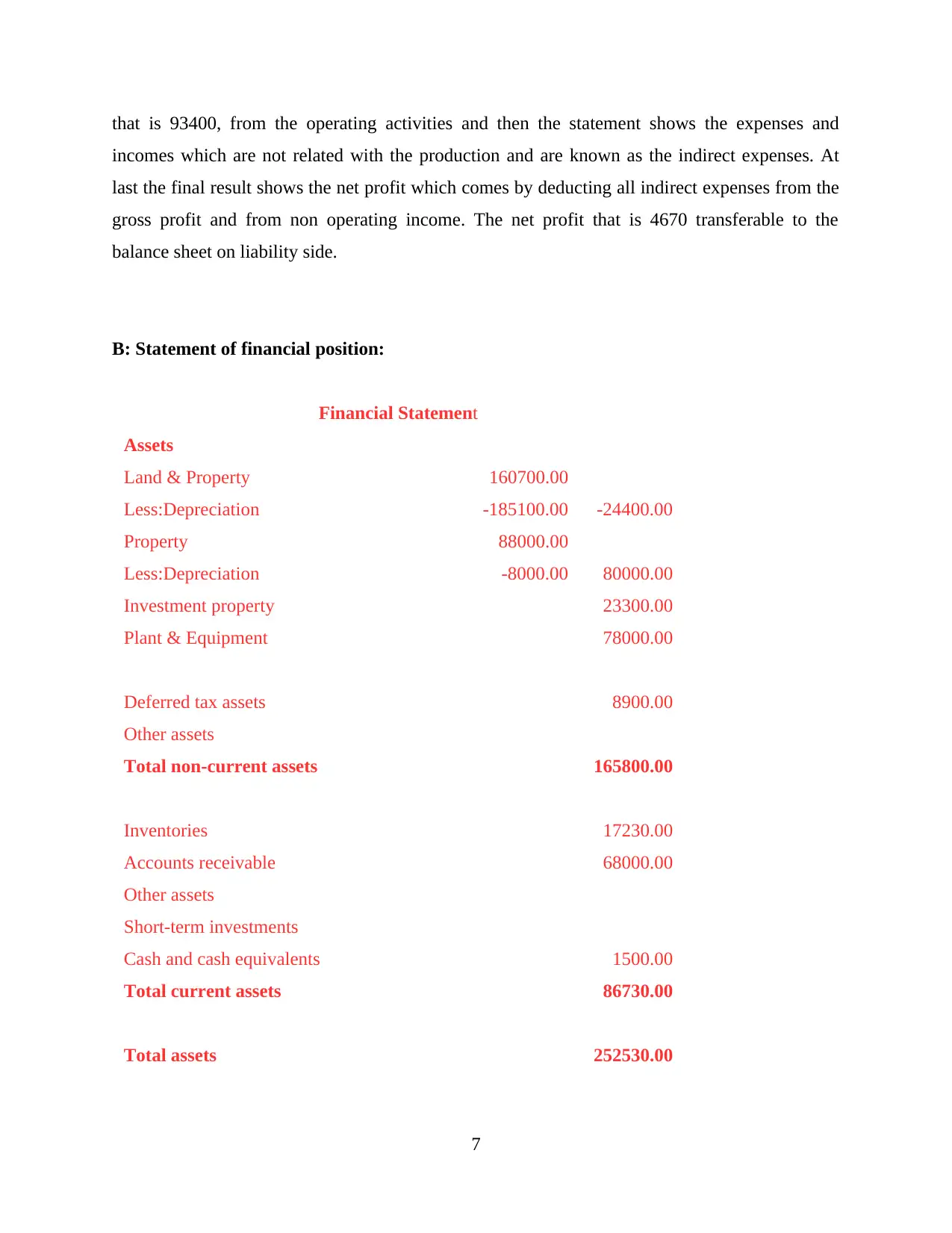

B: Statement of financial position:

Financial Statement

Assets

Land & Property 160700.00

Less:Depreciation -185100.00 -24400.00

Property 88000.00

Less:Depreciation -8000.00 80000.00

Investment property 23300.00

Plant & Equipment 78000.00

Deferred tax assets 8900.00

Other assets

Total non-current assets 165800.00

Inventories 17230.00

Accounts receivable 68000.00

Other assets

Short-term investments

Cash and cash equivalents 1500.00

Total current assets 86730.00

Total assets 252530.00

7

incomes which are not related with the production and are known as the indirect expenses. At

last the final result shows the net profit which comes by deducting all indirect expenses from the

gross profit and from non operating income. The net profit that is 4670 transferable to the

balance sheet on liability side.

B: Statement of financial position:

Financial Statement

Assets

Land & Property 160700.00

Less:Depreciation -185100.00 -24400.00

Property 88000.00

Less:Depreciation -8000.00 80000.00

Investment property 23300.00

Plant & Equipment 78000.00

Deferred tax assets 8900.00

Other assets

Total non-current assets 165800.00

Inventories 17230.00

Accounts receivable 68000.00

Other assets

Short-term investments

Cash and cash equivalents 1500.00

Total current assets 86730.00

Total assets 252530.00

7

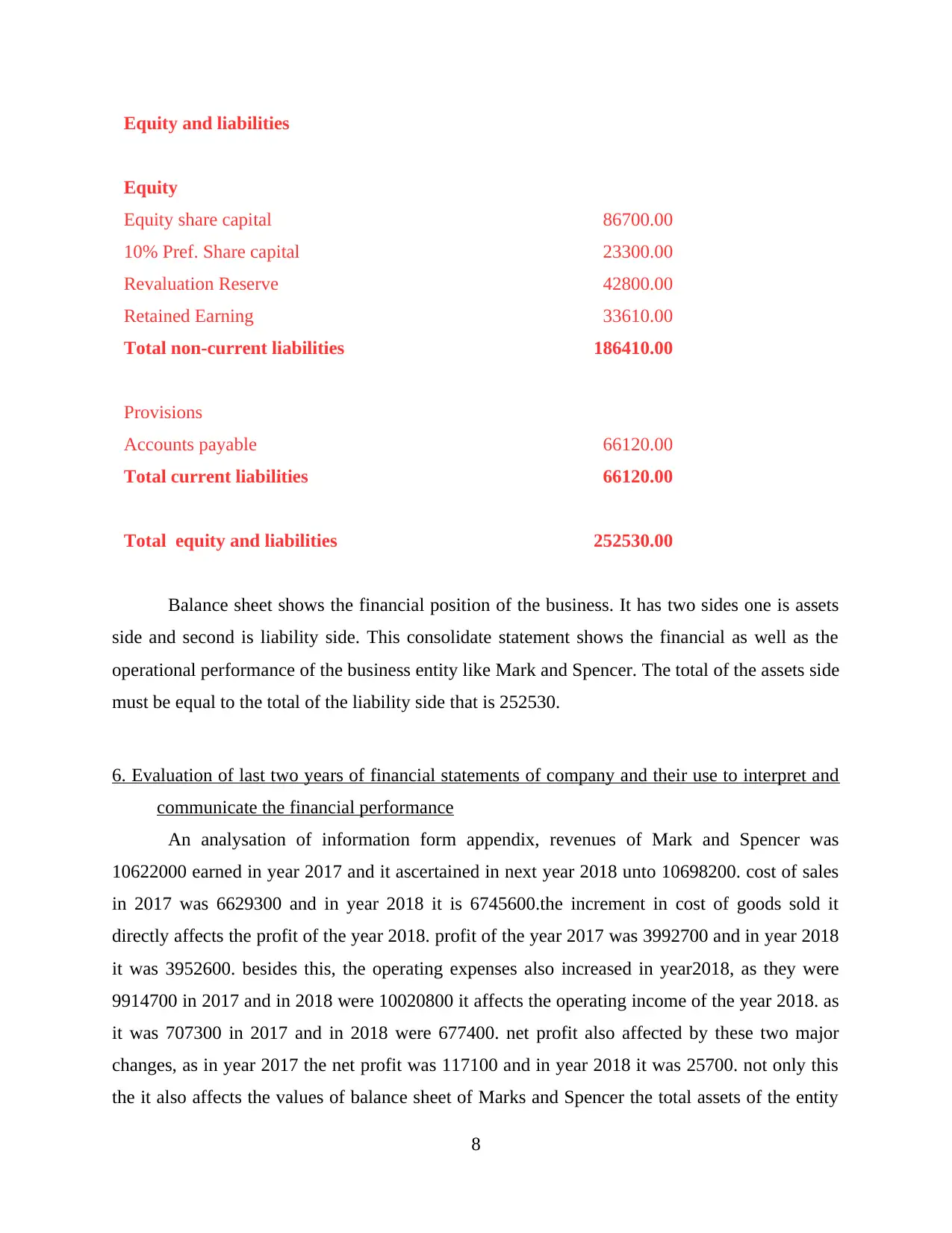

Equity and liabilities

Equity

Equity share capital 86700.00

10% Pref. Share capital 23300.00

Revaluation Reserve 42800.00

Retained Earning 33610.00

Total non-current liabilities 186410.00

Provisions

Accounts payable 66120.00

Total current liabilities 66120.00

Total equity and liabilities 252530.00

Balance sheet shows the financial position of the business. It has two sides one is assets

side and second is liability side. This consolidate statement shows the financial as well as the

operational performance of the business entity like Mark and Spencer. The total of the assets side

must be equal to the total of the liability side that is 252530.

6. Evaluation of last two years of financial statements of company and their use to interpret and

communicate the financial performance

An analysation of information form appendix, revenues of Mark and Spencer was

10622000 earned in year 2017 and it ascertained in next year 2018 unto 10698200. cost of sales

in 2017 was 6629300 and in year 2018 it is 6745600.the increment in cost of goods sold it

directly affects the profit of the year 2018. profit of the year 2017 was 3992700 and in year 2018

it was 3952600. besides this, the operating expenses also increased in year2018, as they were

9914700 in 2017 and in 2018 were 10020800 it affects the operating income of the year 2018. as

it was 707300 in 2017 and in 2018 were 677400. net profit also affected by these two major

changes, as in year 2017 the net profit was 117100 and in year 2018 it was 25700. not only this

the it also affects the values of balance sheet of Marks and Spencer the total assets of the entity

8

Equity

Equity share capital 86700.00

10% Pref. Share capital 23300.00

Revaluation Reserve 42800.00

Retained Earning 33610.00

Total non-current liabilities 186410.00

Provisions

Accounts payable 66120.00

Total current liabilities 66120.00

Total equity and liabilities 252530.00

Balance sheet shows the financial position of the business. It has two sides one is assets

side and second is liability side. This consolidate statement shows the financial as well as the

operational performance of the business entity like Mark and Spencer. The total of the assets side

must be equal to the total of the liability side that is 252530.

6. Evaluation of last two years of financial statements of company and their use to interpret and

communicate the financial performance

An analysation of information form appendix, revenues of Mark and Spencer was

10622000 earned in year 2017 and it ascertained in next year 2018 unto 10698200. cost of sales

in 2017 was 6629300 and in year 2018 it is 6745600.the increment in cost of goods sold it

directly affects the profit of the year 2018. profit of the year 2017 was 3992700 and in year 2018

it was 3952600. besides this, the operating expenses also increased in year2018, as they were

9914700 in 2017 and in 2018 were 10020800 it affects the operating income of the year 2018. as

it was 707300 in 2017 and in 2018 were 677400. net profit also affected by these two major

changes, as in year 2017 the net profit was 117100 and in year 2018 it was 25700. not only this

the it also affects the values of balance sheet of Marks and Spencer the total assets of the entity

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

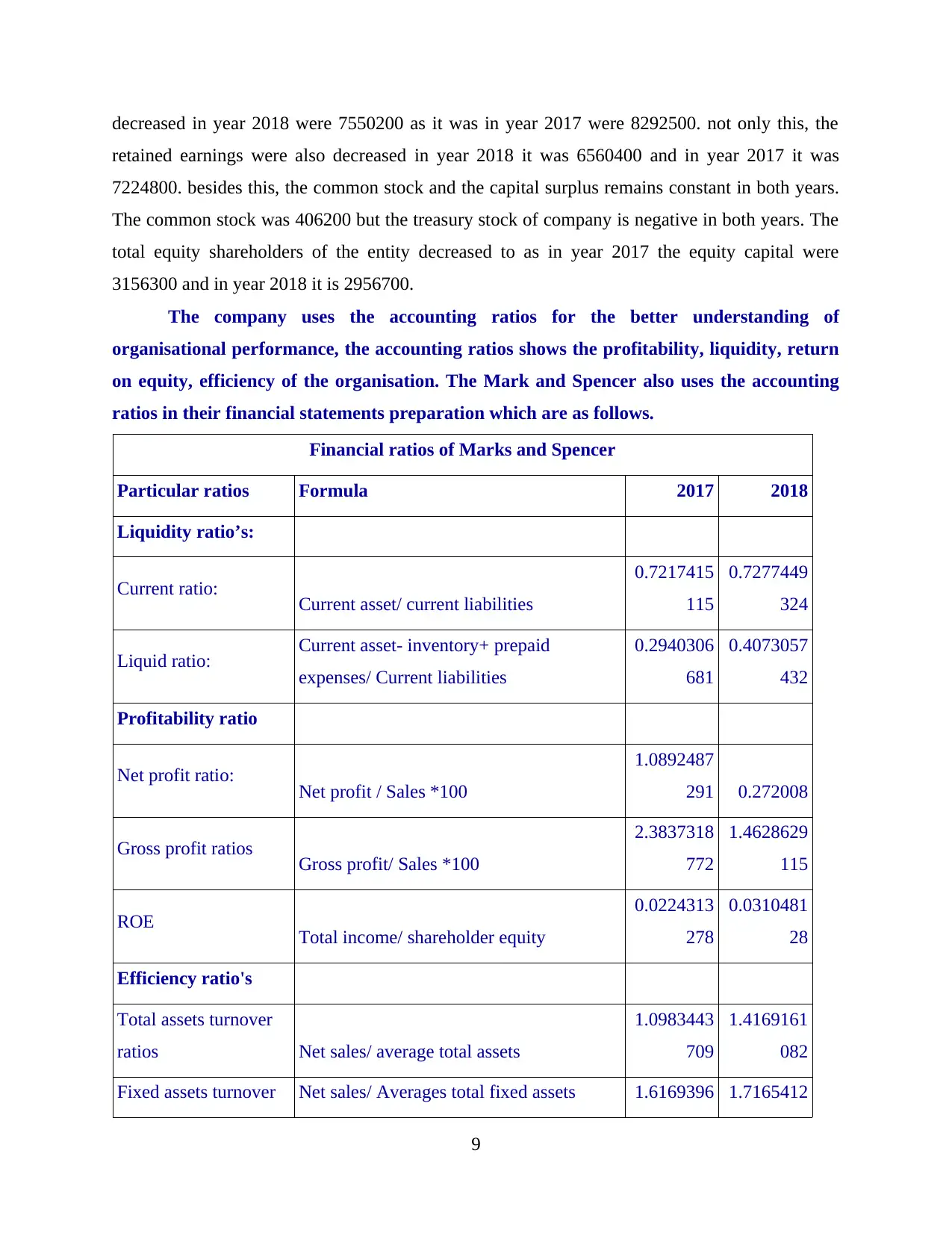

decreased in year 2018 were 7550200 as it was in year 2017 were 8292500. not only this, the

retained earnings were also decreased in year 2018 it was 6560400 and in year 2017 it was

7224800. besides this, the common stock and the capital surplus remains constant in both years.

The common stock was 406200 but the treasury stock of company is negative in both years. The

total equity shareholders of the entity decreased to as in year 2017 the equity capital were

3156300 and in year 2018 it is 2956700.

The company uses the accounting ratios for the better understanding of

organisational performance, the accounting ratios shows the profitability, liquidity, return

on equity, efficiency of the organisation. The Mark and Spencer also uses the accounting

ratios in their financial statements preparation which are as follows.

Financial ratios of Marks and Spencer

Particular ratios Formula 2017 2018

Liquidity ratio’s:

Current ratio: Current asset/ current liabilities

0.7217415

115

0.7277449

324

Liquid ratio: Current asset- inventory+ prepaid

expenses/ Current liabilities

0.2940306

681

0.4073057

432

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.0892487

291 0.272008

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.0983443

709

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets 1.6169396 1.7165412

9

retained earnings were also decreased in year 2018 it was 6560400 and in year 2017 it was

7224800. besides this, the common stock and the capital surplus remains constant in both years.

The common stock was 406200 but the treasury stock of company is negative in both years. The

total equity shareholders of the entity decreased to as in year 2017 the equity capital were

3156300 and in year 2018 it is 2956700.

The company uses the accounting ratios for the better understanding of

organisational performance, the accounting ratios shows the profitability, liquidity, return

on equity, efficiency of the organisation. The Mark and Spencer also uses the accounting

ratios in their financial statements preparation which are as follows.

Financial ratios of Marks and Spencer

Particular ratios Formula 2017 2018

Liquidity ratio’s:

Current ratio: Current asset/ current liabilities

0.7217415

115

0.7277449

324

Liquid ratio: Current asset- inventory+ prepaid

expenses/ Current liabilities

0.2940306

681

0.4073057

432

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.0892487

291 0.272008

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.0983443

709

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets 1.6169396 1.7165412

9

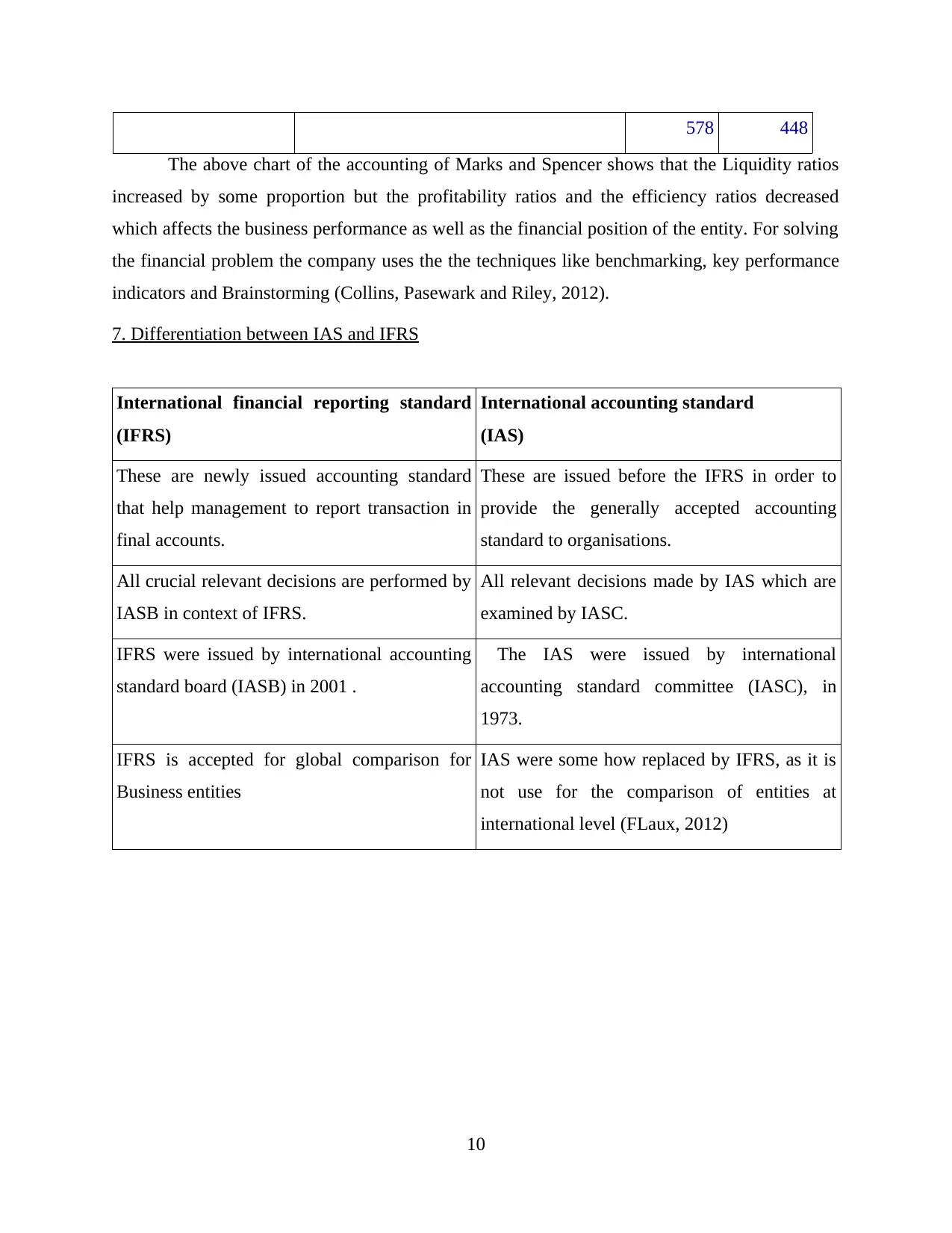

578 448

The above chart of the accounting of Marks and Spencer shows that the Liquidity ratios

increased by some proportion but the profitability ratios and the efficiency ratios decreased

which affects the business performance as well as the financial position of the entity. For solving

the financial problem the company uses the the techniques like benchmarking, key performance

indicators and Brainstorming (Collins, Pasewark and Riley, 2012).

7. Differentiation between IAS and IFRS

International financial reporting standard

(IFRS)

International accounting standard

(IAS)

These are newly issued accounting standard

that help management to report transaction in

final accounts.

These are issued before the IFRS in order to

provide the generally accepted accounting

standard to organisations.

All crucial relevant decisions are performed by

IASB in context of IFRS.

All relevant decisions made by IAS which are

examined by IASC.

IFRS were issued by international accounting

standard board (IASB) in 2001 .

The IAS were issued by international

accounting standard committee (IASC), in

1973.

IFRS is accepted for global comparison for

Business entities

IAS were some how replaced by IFRS, as it is

not use for the comparison of entities at

international level (FLaux, 2012)

10

The above chart of the accounting of Marks and Spencer shows that the Liquidity ratios

increased by some proportion but the profitability ratios and the efficiency ratios decreased

which affects the business performance as well as the financial position of the entity. For solving

the financial problem the company uses the the techniques like benchmarking, key performance

indicators and Brainstorming (Collins, Pasewark and Riley, 2012).

7. Differentiation between IAS and IFRS

International financial reporting standard

(IFRS)

International accounting standard

(IAS)

These are newly issued accounting standard

that help management to report transaction in

final accounts.

These are issued before the IFRS in order to

provide the generally accepted accounting

standard to organisations.

All crucial relevant decisions are performed by

IASB in context of IFRS.

All relevant decisions made by IAS which are

examined by IASC.

IFRS were issued by international accounting

standard board (IASB) in 2001 .

The IAS were issued by international

accounting standard committee (IASC), in

1973.

IFRS is accepted for global comparison for

Business entities

IAS were some how replaced by IFRS, as it is

not use for the comparison of entities at

international level (FLaux, 2012)

10

8. Evaluation of the benefits of International Financial Reporting Standard (IFRS)

There are some benefits of adapting IFRS enjoying by the business entities like Marks

and Spencer. Some of the benefits are discussed as follows.

Appropriate accounting standards supports the entities in ascertaining their growth as

well as in developing their business and economy.

Beneficial in making the comparative analysis of entities of different country as the IFRS

are accepted globally.

IFRS ensures clearance and transparency in the financial statement of the companies.

It is beneficial in acquiring funds from foreign markets.

IFRS acts as the global language that makes easy to understand the financial position of

the businesses, as from the foreign investors point of view (Maffett, 2012).

IFRS standards while making financial reports, ensures the manager to ease the work of

accountant to analysing the statements properly and present their best opinion.

9. Ascertainment of varying degree of compliance associated to IFRS

The international financial reporting standard accepted as the world wide standard of

accounting, after accepted several developed nations. It represents a global language of

accounting and present a frame work for preparation of financial statement preparation and

reporting. Currently there are 17 IFRS and 29 IAS which are adapted by every company at

global level. IFRS is followed by every type of entity whether they are large and small in size.

The mark and Spencer following the standard of IFRS, it is beneficial in preparation of financial

statements which are useful for stakeholder in making right decisions about investments. Besides

this in basic, compliance is the common word which is related to the IFRS(Barth, 2013). It has

been analysed that IFRS standard are framed in accordance with the disclosure of the

compliance in both material facts that are disclosing the needs and the incrementing level of

principles of disclosure.

CONCLUSION

From the above report it has been concluded that the IFRS plays an integral role in

process of financial statement preparation and its reporting as it acts as the global language of

presenting the business performance and it ensures the neutral ground for the comparison of

11

There are some benefits of adapting IFRS enjoying by the business entities like Marks

and Spencer. Some of the benefits are discussed as follows.

Appropriate accounting standards supports the entities in ascertaining their growth as

well as in developing their business and economy.

Beneficial in making the comparative analysis of entities of different country as the IFRS

are accepted globally.

IFRS ensures clearance and transparency in the financial statement of the companies.

It is beneficial in acquiring funds from foreign markets.

IFRS acts as the global language that makes easy to understand the financial position of

the businesses, as from the foreign investors point of view (Maffett, 2012).

IFRS standards while making financial reports, ensures the manager to ease the work of

accountant to analysing the statements properly and present their best opinion.

9. Ascertainment of varying degree of compliance associated to IFRS

The international financial reporting standard accepted as the world wide standard of

accounting, after accepted several developed nations. It represents a global language of

accounting and present a frame work for preparation of financial statement preparation and

reporting. Currently there are 17 IFRS and 29 IAS which are adapted by every company at

global level. IFRS is followed by every type of entity whether they are large and small in size.

The mark and Spencer following the standard of IFRS, it is beneficial in preparation of financial

statements which are useful for stakeholder in making right decisions about investments. Besides

this in basic, compliance is the common word which is related to the IFRS(Barth, 2013). It has

been analysed that IFRS standard are framed in accordance with the disclosure of the

compliance in both material facts that are disclosing the needs and the incrementing level of

principles of disclosure.

CONCLUSION

From the above report it has been concluded that the IFRS plays an integral role in

process of financial statement preparation and its reporting as it acts as the global language of

presenting the business performance and it ensures the neutral ground for the comparison of

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

different business entities across different countries throughout the world. Thus, the financial

reporting becomes crucial and transparent process beneficial for all of its users.

12

reporting becomes crucial and transparent process beneficial for all of its users.

12

REFERENCES

Books and Journals

Bertoni, M.P.G.V.A.G. and De Rosa, B., 2012. Green accounting: an alternative approach to

reporting emission trading allowances in financial statements.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Hope, O.K., Thomas, W.B. and Vyas, D., 2013. Financial reporting quality of US private and

public firms. The Accounting Review, 88(5), pp.1715-1742.

Bevis, H.W., 2013. Corporate Financial Reporting in a Competitive Economy (RLE

Accounting). Routledge.

Botzem, S., 2012. The politics of accounting regulation: Organizing transnational standard

setting in financial reporting. Edward Elgar Publishing.

Tan, L., 2013. Creditor control rights, state of nature verification, and financial reporting

conservatism. Journal of Accounting and Economics, 55(1), pp.1-22.

Collins, D.L., Pasewark, W.R. and Riley, M.E., 2012. Financial reporting outcomes under rules-

based and principles-based accounting standards. Accounting Horizons, 26(4), pp.681-

705.

Laux, C., 2012. Financial instruments, financial reporting, and financial stability. Accounting

and business research, 42(3), pp.239-260.

Maffett, M., 2012. Financial reporting opacity and informed trading by international institutional

investors. Journal of Accounting and Economics, 54(2-3), pp.201-220.

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), pp.331-352.

Zeff, S.A., 2013. The objectives of financial reporting: a historical survey and analysis.

Accounting and Business Research, 43(4), pp.262-327.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Zimmerman, J.L., 2013. Myth: External financial reporting quality has a first-order effect on

firm value. Accounting Horizons, 27(4), pp.887-894.

13

Books and Journals

Bertoni, M.P.G.V.A.G. and De Rosa, B., 2012. Green accounting: an alternative approach to

reporting emission trading allowances in financial statements.

Nobes, C., 2014. International classification of financial reporting. Routledge.

Hope, O.K., Thomas, W.B. and Vyas, D., 2013. Financial reporting quality of US private and

public firms. The Accounting Review, 88(5), pp.1715-1742.

Bevis, H.W., 2013. Corporate Financial Reporting in a Competitive Economy (RLE

Accounting). Routledge.

Botzem, S., 2012. The politics of accounting regulation: Organizing transnational standard

setting in financial reporting. Edward Elgar Publishing.

Tan, L., 2013. Creditor control rights, state of nature verification, and financial reporting

conservatism. Journal of Accounting and Economics, 55(1), pp.1-22.

Collins, D.L., Pasewark, W.R. and Riley, M.E., 2012. Financial reporting outcomes under rules-

based and principles-based accounting standards. Accounting Horizons, 26(4), pp.681-

705.

Laux, C., 2012. Financial instruments, financial reporting, and financial stability. Accounting

and business research, 42(3), pp.239-260.

Maffett, M., 2012. Financial reporting opacity and informed trading by international institutional

investors. Journal of Accounting and Economics, 54(2-3), pp.201-220.

Barth, M.E., 2013. Measurement in financial reporting: The need for concepts. Accounting

Horizons, 28(2), pp.331-352.

Zeff, S.A., 2013. The objectives of financial reporting: a historical survey and analysis.

Accounting and Business Research, 43(4), pp.262-327.

Flower, J., 2016. European financial reporting: adapting to a changing world. Springer.

Zimmerman, J.L., 2013. Myth: External financial reporting quality has a first-order effect on

firm value. Accounting Horizons, 27(4), pp.887-894.

13

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.