Financial Reporting Analysis: Standards, Stakeholders and Objectives

VerifiedAdded on 2021/02/19

|15

|4799

|44

Report

AI Summary

This report provides a comprehensive analysis of financial reporting, exploring its context, purpose, and the key principles and qualitative characteristics that underpin it. It examines the conceptual and regulatory frameworks, including the roles of IASB and IFRS, and assesses the benefits of financial information for various stakeholders, both internal (managers, employees) and external (creditors, investors, suppliers). The report delves into how financial reporting contributes to meeting organisational objectives and fostering business growth, using Deloitte as a case study to illustrate these concepts. It further discusses the presentation of financial statements as per IAS 1, the interpretation and communication of financial performance, and the differences between international accounting standards (IAS) and international financial reporting standards (IFRS). The advantages of the international financial reporting system and the degree of compliance with IFRS are also evaluated, providing a complete overview of the subject.

FINANCIAL

REPORTING

REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTIONS...................................................................................................................................3

1. Context and purpose of financial reporting.............................................................................3

2. Conceptual, regulatory framework, key principle and qualitative characteristics. ................4

3. Main stakeholders of organisations and benefits of financial information for them.............6

4. Value of financial reporting for meeting the organisational objectives and growth...............7

5. Presentation of financial statements as per IAS 1...................................................................8

6. Interpretation and communication of financial performance of listed company in the FTSE

100.............................................................................................................................................10

7. Difference between international accounting standard and international financial reporting

standard.....................................................................................................................................12

8. Evaluation of advantage of international financial reporting system....................................13

9. Degree of compliance with the international financial reporting standards..........................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

QUESTIONS...................................................................................................................................3

1. Context and purpose of financial reporting.............................................................................3

2. Conceptual, regulatory framework, key principle and qualitative characteristics. ................4

3. Main stakeholders of organisations and benefits of financial information for them.............6

4. Value of financial reporting for meeting the organisational objectives and growth...............7

5. Presentation of financial statements as per IAS 1...................................................................8

6. Interpretation and communication of financial performance of listed company in the FTSE

100.............................................................................................................................................10

7. Difference between international accounting standard and international financial reporting

standard.....................................................................................................................................12

8. Evaluation of advantage of international financial reporting system....................................13

9. Degree of compliance with the international financial reporting standards..........................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

The financial reporting can be defined as a process of presenting the financial statements

and information to the managers and external stakeholders (Pelger, 2016). The main purpose of

these reports is to aware stakeholders about financial performance of a company during a

specific period of time. In the context of organisations, there are a wide range of operations and

activities which are being performed by different departments. Herein, it is essential to know

about the performance of all the activities in the terms of profit and this is done with the help of

financial reports. Eventually, the financial reports are prepared and presented at the end of an

accounting period. To understand in broad sense about term financial reporting, Deloitte

company is selected which provides financial services to wide range of customers.

Herein, the project report, conceptual and regulatory framework of the financial reports is

mentioned. As well as benefit to the stakeholder of these reports is also discussed. Apart from it,

variation between the international accounting standard and international financial-reporting

standard is included in the report. Along with, various type of financial reports and statements

such as P&L account, balance sheet etc. are prepared on the basis of given information and data.

QUESTIONS

1. Context and purpose of financial reporting.

Financial reporting:

It is concerned with the disclosure of company's financial statements to the management

and the owners i.e. the shareholders for the purpose of disclosing the financial health of the

organisation (Perera and Chand, 2015). It is the analysis of financial statements prepared in an

organisation which majorly consists of income & expenditure statement, cash flow statement and

balance sheet. It is a legal onus on the firm to disclose what its current financial health is to its

shareholders and promoters . The meeting of financial reporting standards by the organisation

ensures the stakeholders most importantly the shareholders that their stakes are duly taken care

of. It is a vital part of sustainable corporate governance. Disclosing timely financial statements to

public and government helps organisation in building a compliance rapport along with

establishing market reliance.

Purpose of financial reporting:

The financial reporting can be defined as a process of presenting the financial statements

and information to the managers and external stakeholders (Pelger, 2016). The main purpose of

these reports is to aware stakeholders about financial performance of a company during a

specific period of time. In the context of organisations, there are a wide range of operations and

activities which are being performed by different departments. Herein, it is essential to know

about the performance of all the activities in the terms of profit and this is done with the help of

financial reports. Eventually, the financial reports are prepared and presented at the end of an

accounting period. To understand in broad sense about term financial reporting, Deloitte

company is selected which provides financial services to wide range of customers.

Herein, the project report, conceptual and regulatory framework of the financial reports is

mentioned. As well as benefit to the stakeholder of these reports is also discussed. Apart from it,

variation between the international accounting standard and international financial-reporting

standard is included in the report. Along with, various type of financial reports and statements

such as P&L account, balance sheet etc. are prepared on the basis of given information and data.

QUESTIONS

1. Context and purpose of financial reporting.

Financial reporting:

It is concerned with the disclosure of company's financial statements to the management

and the owners i.e. the shareholders for the purpose of disclosing the financial health of the

organisation (Perera and Chand, 2015). It is the analysis of financial statements prepared in an

organisation which majorly consists of income & expenditure statement, cash flow statement and

balance sheet. It is a legal onus on the firm to disclose what its current financial health is to its

shareholders and promoters . The meeting of financial reporting standards by the organisation

ensures the stakeholders most importantly the shareholders that their stakes are duly taken care

of. It is a vital part of sustainable corporate governance. Disclosing timely financial statements to

public and government helps organisation in building a compliance rapport along with

establishing market reliance.

Purpose of financial reporting:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It helps the management to take profound strategic decisions about the future goals by

relying on the financial data provided by statements which discloses the current position.

This information helps the managers in creating a base index of for future projections.

The relevancy of information paves a way for emancipating future business strategies.

The second most prominent purpose of financial reporting is it discloses the key success

factors and loss factors to the investors who have provided additional capital to the

business. It is a mandatory as well as ethical norm to do so. To safeguard the interests of

investors from fraudulent practices related to insider trading, financial scams etc., every

nation has devised certain corporate laws requiring companies to disclose data to public

and government.

Meeting financial reporting standards facilitates the statutory audit by providing well

crafted documents to assist audit. Since it bores a good name to the company hence

makes it easy for it to gather capital from international and national sources easily as

compared to non compliant organisations.

2. Conceptual, regulatory framework, key principle and qualitative characteristics.

Conceptual & Regulatory framework :

Conceptual framework for reporting is promulgated by International accounting

standards board (IASB) which is the regulatory body for IFRS (Krishnan and Zhang, 2014). The

framework is very crucial in designing standards for different industries functioning in an

economy. It drafts the fundamental concepts for financial reporting in designing standards and

ensure that standards are conceptually in consistency with the norms. Conceptual framework

helps companies in formulating accounting policies where IFRS standards doesn't apply to an

individual , at the same time makes it easier for the stakeholders to easily understand the

standards. Regulatory framework is necessary for financial reporting to control the ways to

report the statements. It creates scope for the companies, rectifies any errors and timely updates

the standards. It ensures steady and full implementation of standards. The regulatory structure

consists of National financial standards, national law, market regulations, security exchange

rules. UK has accounting standards board As its own financial reporting authority. It is

authorised by companies act 2006. There are other legislations like Sarbanes Oxley act which

affects the accountability in UK.

relying on the financial data provided by statements which discloses the current position.

This information helps the managers in creating a base index of for future projections.

The relevancy of information paves a way for emancipating future business strategies.

The second most prominent purpose of financial reporting is it discloses the key success

factors and loss factors to the investors who have provided additional capital to the

business. It is a mandatory as well as ethical norm to do so. To safeguard the interests of

investors from fraudulent practices related to insider trading, financial scams etc., every

nation has devised certain corporate laws requiring companies to disclose data to public

and government.

Meeting financial reporting standards facilitates the statutory audit by providing well

crafted documents to assist audit. Since it bores a good name to the company hence

makes it easy for it to gather capital from international and national sources easily as

compared to non compliant organisations.

2. Conceptual, regulatory framework, key principle and qualitative characteristics.

Conceptual & Regulatory framework :

Conceptual framework for reporting is promulgated by International accounting

standards board (IASB) which is the regulatory body for IFRS (Krishnan and Zhang, 2014). The

framework is very crucial in designing standards for different industries functioning in an

economy. It drafts the fundamental concepts for financial reporting in designing standards and

ensure that standards are conceptually in consistency with the norms. Conceptual framework

helps companies in formulating accounting policies where IFRS standards doesn't apply to an

individual , at the same time makes it easier for the stakeholders to easily understand the

standards. Regulatory framework is necessary for financial reporting to control the ways to

report the statements. It creates scope for the companies, rectifies any errors and timely updates

the standards. It ensures steady and full implementation of standards. The regulatory structure

consists of National financial standards, national law, market regulations, security exchange

rules. UK has accounting standards board As its own financial reporting authority. It is

authorised by companies act 2006. There are other legislations like Sarbanes Oxley act which

affects the accountability in UK.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Key principles : key principles of reporting includes basic core characteristics of

reporting which should exist in any reporting system to ensure better implementation. They key

principles are:

Full disclosure : Companies are required to fully disclose their financial statements

prepared on the basis of prescribed international formats (Wolfson, 2014). These

statements shall be available to general public to help them in making an informed

decision prior to making an investment. The investors should be able to make yes or no

decisions adhering to financial statements. They shall be prepared with the practice of

prudence and just and fair measures.

Consistency : The financial statements shall be prepared on year to year basis

consecutively and consistently. They should behave in contrast to the previous year's

statements to determine the consistency in companies reports. It helps the investors in

comparing between companies consistency and reliability.

Purpose : Statements shall be prepared with specific purpose of reporting reliable

information to the public.

Qualitative characteristics of financial reporting :

The financial reporting information shall have some qualitative features in relevance to

the quantitative features. The reports are required to meet quality standards to demonstrate the

precision with which financial statements are prepared. This gives a glimpse of how ethical and

law abiding a business firm is. The basic qualitative characteristics of financial reporting are :

Faithful representation : The financial information provided in financial reports should

disseminate what it purports to present. It should be prepared on the principles of justice

and prudence(Rotimi 2012). They shall clearly state the position of assets and liabilities

and cash inflow and outflow. The data provide should be fair, free from bias and

prejudice, accurate and precise.

Relevance : The information provided in financial statements should be relevant to the

period for which they are prepared along with company's operations, financial health and

progress. The data relevancy is important to the investors in making informed decision

about the investment.

reporting which should exist in any reporting system to ensure better implementation. They key

principles are:

Full disclosure : Companies are required to fully disclose their financial statements

prepared on the basis of prescribed international formats (Wolfson, 2014). These

statements shall be available to general public to help them in making an informed

decision prior to making an investment. The investors should be able to make yes or no

decisions adhering to financial statements. They shall be prepared with the practice of

prudence and just and fair measures.

Consistency : The financial statements shall be prepared on year to year basis

consecutively and consistently. They should behave in contrast to the previous year's

statements to determine the consistency in companies reports. It helps the investors in

comparing between companies consistency and reliability.

Purpose : Statements shall be prepared with specific purpose of reporting reliable

information to the public.

Qualitative characteristics of financial reporting :

The financial reporting information shall have some qualitative features in relevance to

the quantitative features. The reports are required to meet quality standards to demonstrate the

precision with which financial statements are prepared. This gives a glimpse of how ethical and

law abiding a business firm is. The basic qualitative characteristics of financial reporting are :

Faithful representation : The financial information provided in financial reports should

disseminate what it purports to present. It should be prepared on the principles of justice

and prudence(Rotimi 2012). They shall clearly state the position of assets and liabilities

and cash inflow and outflow. The data provide should be fair, free from bias and

prejudice, accurate and precise.

Relevance : The information provided in financial statements should be relevant to the

period for which they are prepared along with company's operations, financial health and

progress. The data relevancy is important to the investors in making informed decision

about the investment.

Understandable : The financial statements should be easily understandable and clearly

self explanatory to help the investors understand the organisation position.

Comparable : The financial statements shall be prepared based on consistent accounting

standards to help the stakeholders in comparing past data to the current data.

Timeliness : The information should be prepared on time and shall be disclosed onh timely

manner before it looses its credibility to influence decisions. Generally they are prepared on year

to year basis.

3. Main stakeholders of organisations and benefits of financial information for them.

The stakeholders can be defined as a person or organisation which has their interest in

the financial performance companies (Powers, Robinson and Stomberg, 2016). Eventually, the

stakeholders may impact to the company's activities, plans and policies. There are two kinds of

stakeholders which are internal and external stakeholders. Both have their interest in the financial

performance of organisations. In the context of Deloitte company, they have both kind of

stakeholders which are described in broad sense below:

Internal stakeholders- These are the stakeholders which take part in day to day

activities of organisation. As well as can be effected directly by plans and policies of companies.

Herein, below some types of internal stakeholders are mentioned below:

Managers- The managers are those who are important for making plans and strategies for

the companies. These are one of the important internal stakeholders for the companies.

The financial reports of companies are very important for the managers. This is why

because on the basis of these reports, they draw a pattern on which companies can

operate their activities. For example in above mentioned company, their manager

evaluate the financial reports for the purpose of internal decision-making.

self explanatory to help the investors understand the organisation position.

Comparable : The financial statements shall be prepared based on consistent accounting

standards to help the stakeholders in comparing past data to the current data.

Timeliness : The information should be prepared on time and shall be disclosed onh timely

manner before it looses its credibility to influence decisions. Generally they are prepared on year

to year basis.

3. Main stakeholders of organisations and benefits of financial information for them.

The stakeholders can be defined as a person or organisation which has their interest in

the financial performance companies (Powers, Robinson and Stomberg, 2016). Eventually, the

stakeholders may impact to the company's activities, plans and policies. There are two kinds of

stakeholders which are internal and external stakeholders. Both have their interest in the financial

performance of organisations. In the context of Deloitte company, they have both kind of

stakeholders which are described in broad sense below:

Internal stakeholders- These are the stakeholders which take part in day to day

activities of organisation. As well as can be effected directly by plans and policies of companies.

Herein, below some types of internal stakeholders are mentioned below:

Managers- The managers are those who are important for making plans and strategies for

the companies. These are one of the important internal stakeholders for the companies.

The financial reports of companies are very important for the managers. This is why

because on the basis of these reports, they draw a pattern on which companies can

operate their activities. For example in above mentioned company, their manager

evaluate the financial reports for the purpose of internal decision-making.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Employees- These are kind of internal stakeholders who perform the activities and

functions of the organisations for purpose of getting salary and wages (Kantudu and

Samaila, 2015). Eventually, the financial reports are beneficial for them, because if

company's financial reports are showing higher profits then employees will be awarded

accordingly. As well as employees can ensure about their incentives, bonus and salary to

get on time. Same as in above respective company Deloitte the financial reports are

useful for their employees to get information about financial position.

External stakeholders- These are the stakeholders who do not participate in day to day

activities of the organisation but can be effected organisational policies and plans indirectly.

Such as in Deloitte company, they have various kind of external stakeholders who show their

interest in the financial performance of the company to make investment. Some stakeholders are

mentioned below:

Creditors- These are kind of external stakeholders who are associated with providing the

financial services to the companies on credit basis. The financial reports of company are

very beneficial for them in taking decision about making credit transaction with the

companies. In the Deloitte company, their creditors provide financial assistance to them

on the basis of their financial reports.

Investors- These are kind of stakeholders who invest the money in the activities of

organisations with an expectation to get the higher return (Chen, Lobo and Wang, 2013).

The financial reports are beneficial for them like in above respective company, they make

the investment on the basis of debt to equity ratio.

Suppliers- These are the stakeholders which supply the goods and services on credit or

cash. When they supply the material on credit then they provide it on the basis of

financial reports. If company's financial condition is not good then suppliers will not

provide material on credit.

4. Value of financial reporting for meeting the organisational objectives and growth.

The financial reports for meeting the organisational objectives and growth. This is why

because on the basis of it, companies make plans and policies.

Financial reporting for meeting the objectives- The financial reports are useful for the

companies in achieving the goals and objectives of the organisation. This is so because on with

functions of the organisations for purpose of getting salary and wages (Kantudu and

Samaila, 2015). Eventually, the financial reports are beneficial for them, because if

company's financial reports are showing higher profits then employees will be awarded

accordingly. As well as employees can ensure about their incentives, bonus and salary to

get on time. Same as in above respective company Deloitte the financial reports are

useful for their employees to get information about financial position.

External stakeholders- These are the stakeholders who do not participate in day to day

activities of the organisation but can be effected organisational policies and plans indirectly.

Such as in Deloitte company, they have various kind of external stakeholders who show their

interest in the financial performance of the company to make investment. Some stakeholders are

mentioned below:

Creditors- These are kind of external stakeholders who are associated with providing the

financial services to the companies on credit basis. The financial reports of company are

very beneficial for them in taking decision about making credit transaction with the

companies. In the Deloitte company, their creditors provide financial assistance to them

on the basis of their financial reports.

Investors- These are kind of stakeholders who invest the money in the activities of

organisations with an expectation to get the higher return (Chen, Lobo and Wang, 2013).

The financial reports are beneficial for them like in above respective company, they make

the investment on the basis of debt to equity ratio.

Suppliers- These are the stakeholders which supply the goods and services on credit or

cash. When they supply the material on credit then they provide it on the basis of

financial reports. If company's financial condition is not good then suppliers will not

provide material on credit.

4. Value of financial reporting for meeting the organisational objectives and growth.

The financial reports for meeting the organisational objectives and growth. This is why

because on the basis of it, companies make plans and policies.

Financial reporting for meeting the objectives- The financial reports are useful for the

companies in achieving the goals and objectives of the organisation. This is so because on with

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the help of these reports companies can analyse about actual financial position of company and

accordingly can make plan to achieve the objectives. Such as in the Deliotte company, they

evaluate the financial performance of their activities with the help of income statements, balance

sheets etc. and make effective strategies to complete their goals. For example previous year's

profit & loss account presenting the high profit then they will continue the same plan and

policies in current year.

Financial reporting for growth of business- Additionally, the financial reporting are also

important for growth of the companies. The financial reports conclude about the effort of all

business activities and operations in terms of profit. As well as if companies will show their

financial reports to the external stakeholders then company's reputation will enhance and it may

help in growth of business. Such as in the Deliotte company, they produce and present the

financial reports in front of external stakeholders and they invest in the company accordingly.

Hence, it can be said that the financial reports are useful in the growth of business in an effective

manner.

Financial reporting for development of business- Apart from it, the financial reports are

also important for development of the business (Assaf, Josiassen and Cvelbar, 2012). This is

why because on the basis of financial statements, companies can take decisions about expanding

the business. Eventually, in the absence of financial reports companies can not make capital

expenditure. As well as without evaluation of the financial reports it can be risky for the

companies to take further decisions. Like in the above respective company, they take expenditure

decisions on the basis of their financial reports. So overall, the financial reports are useful in the

development of business.

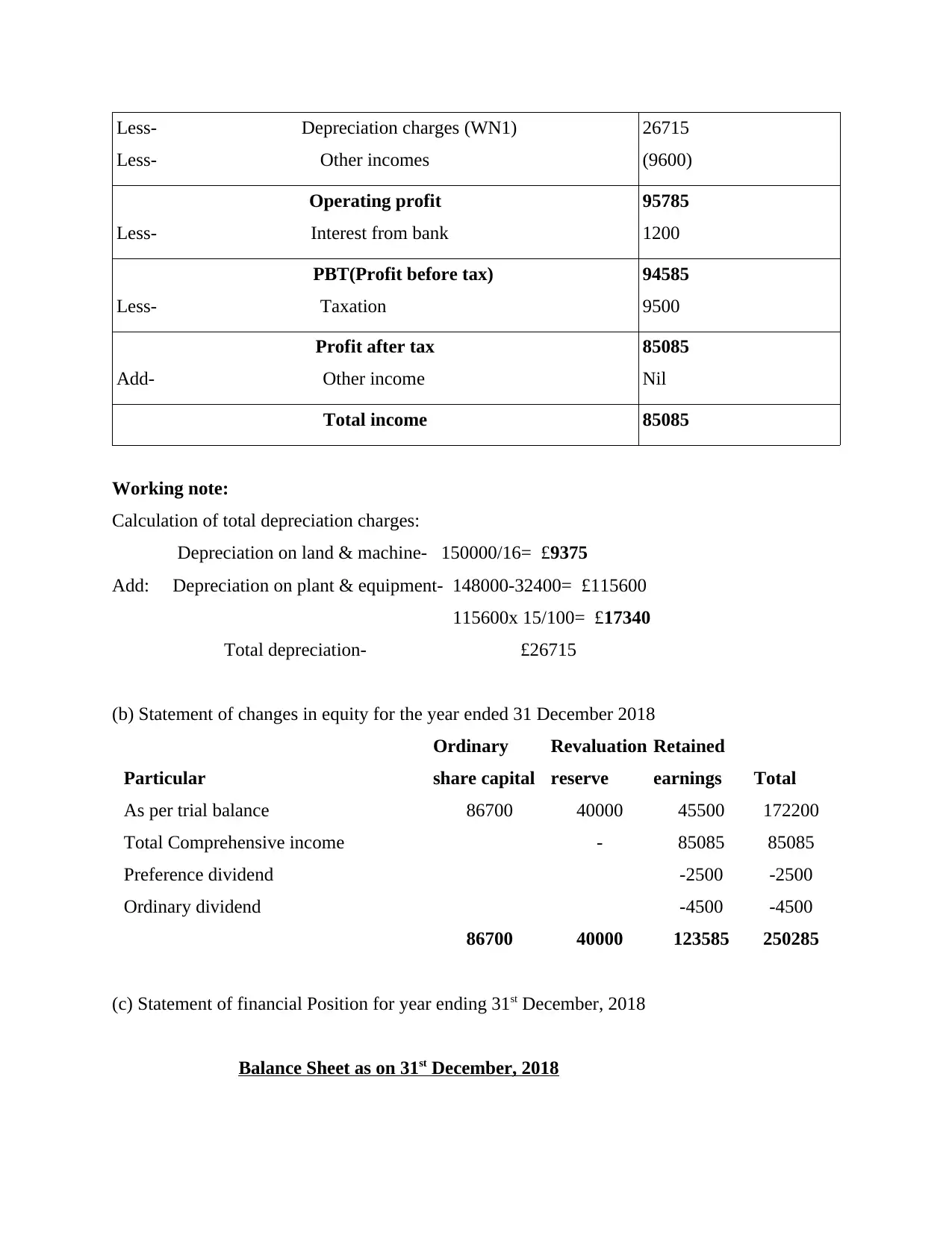

5. Presentation of financial statements as per IAS 1.

(a) Profit and loss statement for year ending 31 December, 2018

Particular Amount (in £'000)

Revenue

Less- Cost of good sales

585100

(391700)

Gross profit

Less- Operating expenditures

193400

80500

accordingly can make plan to achieve the objectives. Such as in the Deliotte company, they

evaluate the financial performance of their activities with the help of income statements, balance

sheets etc. and make effective strategies to complete their goals. For example previous year's

profit & loss account presenting the high profit then they will continue the same plan and

policies in current year.

Financial reporting for growth of business- Additionally, the financial reporting are also

important for growth of the companies. The financial reports conclude about the effort of all

business activities and operations in terms of profit. As well as if companies will show their

financial reports to the external stakeholders then company's reputation will enhance and it may

help in growth of business. Such as in the Deliotte company, they produce and present the

financial reports in front of external stakeholders and they invest in the company accordingly.

Hence, it can be said that the financial reports are useful in the growth of business in an effective

manner.

Financial reporting for development of business- Apart from it, the financial reports are

also important for development of the business (Assaf, Josiassen and Cvelbar, 2012). This is

why because on the basis of financial statements, companies can take decisions about expanding

the business. Eventually, in the absence of financial reports companies can not make capital

expenditure. As well as without evaluation of the financial reports it can be risky for the

companies to take further decisions. Like in the above respective company, they take expenditure

decisions on the basis of their financial reports. So overall, the financial reports are useful in the

development of business.

5. Presentation of financial statements as per IAS 1.

(a) Profit and loss statement for year ending 31 December, 2018

Particular Amount (in £'000)

Revenue

Less- Cost of good sales

585100

(391700)

Gross profit

Less- Operating expenditures

193400

80500

Less- Depreciation charges (WN1)

Less- Other incomes

26715

(9600)

Operating profit

Less- Interest from bank

95785

1200

PBT(Profit before tax)

Less- Taxation

94585

9500

Profit after tax

Add- Other income

85085

Nil

Total income 85085

Working note:

Calculation of total depreciation charges:

Depreciation on land & machine- 150000/16= £9375

Add: Depreciation on plant & equipment- 148000-32400= £115600

115600x 15/100= £17340

Total depreciation- £26715

(b) Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluation

reserve

Retained

earnings Total

As per trial balance 86700 40000 45500 172200

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

(c) Statement of financial Position for year ending 31st December, 2018

Balance Sheet as on 31st December, 2018

Less- Other incomes

26715

(9600)

Operating profit

Less- Interest from bank

95785

1200

PBT(Profit before tax)

Less- Taxation

94585

9500

Profit after tax

Add- Other income

85085

Nil

Total income 85085

Working note:

Calculation of total depreciation charges:

Depreciation on land & machine- 150000/16= £9375

Add: Depreciation on plant & equipment- 148000-32400= £115600

115600x 15/100= £17340

Total depreciation- £26715

(b) Statement of changes in equity for the year ended 31 December 2018

Particular

Ordinary

share capital

Revaluation

reserve

Retained

earnings Total

As per trial balance 86700 40000 45500 172200

Total Comprehensive income - 85085 85085

Preference dividend -2500 -2500

Ordinary dividend -4500 -4500

86700 40000 123585 250285

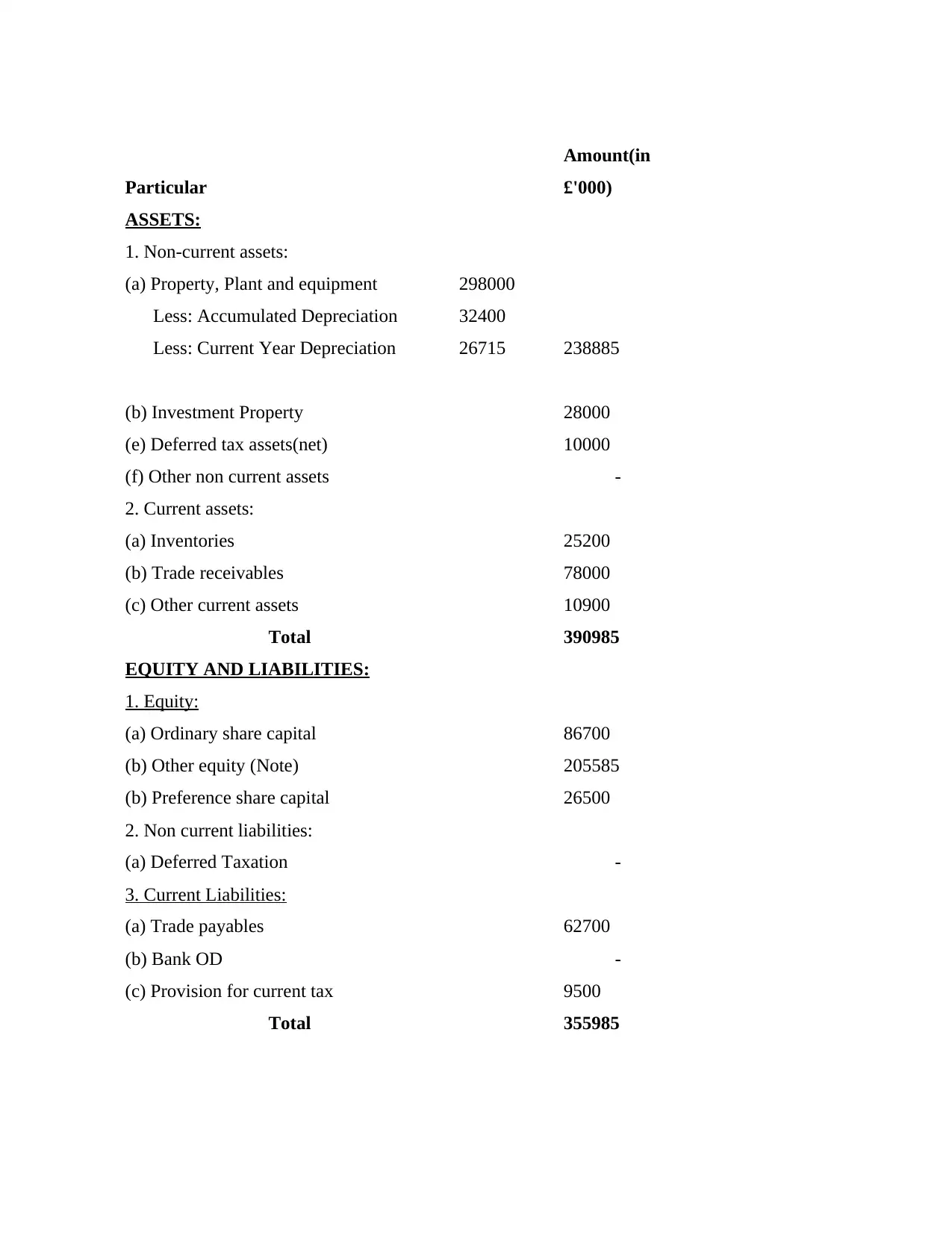

(c) Statement of financial Position for year ending 31st December, 2018

Balance Sheet as on 31st December, 2018

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particular

Amount(in

£'000)

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

1. Equity:

(a) Ordinary share capital 86700

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

(a) Deferred Taxation -

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD -

(c) Provision for current tax 9500

Total 355985

Amount(in

£'000)

ASSETS:

1. Non-current assets:

(a) Property, Plant and equipment 298000

Less: Accumulated Depreciation 32400

Less: Current Year Depreciation 26715 238885

(b) Investment Property 28000

(e) Deferred tax assets(net) 10000

(f) Other non current assets -

2. Current assets:

(a) Inventories 25200

(b) Trade receivables 78000

(c) Other current assets 10900

Total 390985

EQUITY AND LIABILITIES:

1. Equity:

(a) Ordinary share capital 86700

(b) Other equity (Note) 205585

(b) Preference share capital 26500

2. Non current liabilities:

(a) Deferred Taxation -

3. Current Liabilities:

(a) Trade payables 62700

(b) Bank OD -

(c) Provision for current tax 9500

Total 355985

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

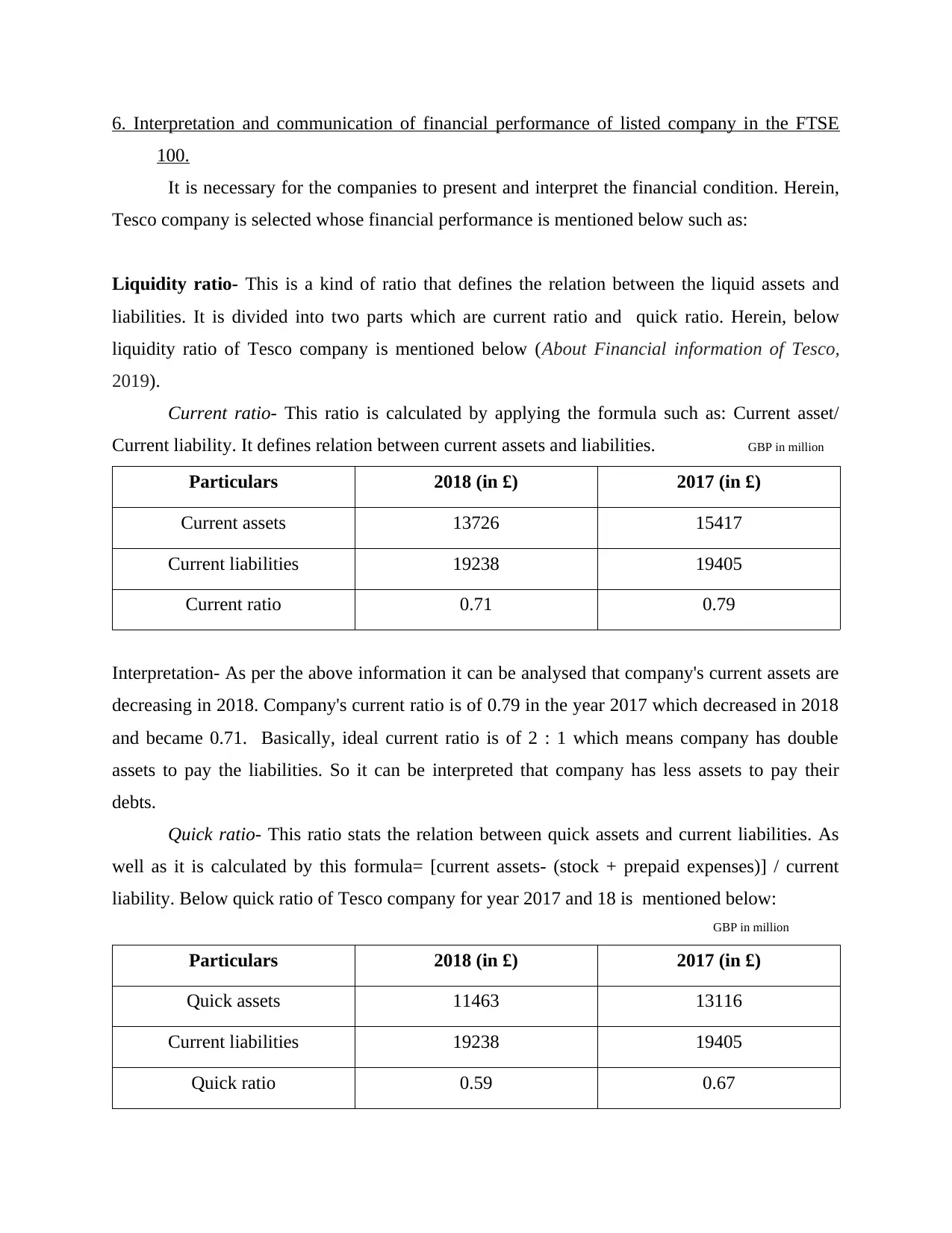

6. Interpretation and communication of financial performance of listed company in the FTSE

100.

It is necessary for the companies to present and interpret the financial condition. Herein,

Tesco company is selected whose financial performance is mentioned below such as:

Liquidity ratio- This is a kind of ratio that defines the relation between the liquid assets and

liabilities. It is divided into two parts which are current ratio and quick ratio. Herein, below

liquidity ratio of Tesco company is mentioned below (About Financial information of Tesco,

2019).

Current ratio- This ratio is calculated by applying the formula such as: Current asset/

Current liability. It defines relation between current assets and liabilities. GBP in million

Particulars 2018 (in £) 2017 (in £)

Current assets 13726 15417

Current liabilities 19238 19405

Current ratio 0.71 0.79

Interpretation- As per the above information it can be analysed that company's current assets are

decreasing in 2018. Company's current ratio is of 0.79 in the year 2017 which decreased in 2018

and became 0.71. Basically, ideal current ratio is of 2 : 1 which means company has double

assets to pay the liabilities. So it can be interpreted that company has less assets to pay their

debts.

Quick ratio- This ratio stats the relation between quick assets and current liabilities. As

well as it is calculated by this formula= [current assets- (stock + prepaid expenses)] / current

liability. Below quick ratio of Tesco company for year 2017 and 18 is mentioned below:

GBP in million

Particulars 2018 (in £) 2017 (in £)

Quick assets 11463 13116

Current liabilities 19238 19405

Quick ratio 0.59 0.67

100.

It is necessary for the companies to present and interpret the financial condition. Herein,

Tesco company is selected whose financial performance is mentioned below such as:

Liquidity ratio- This is a kind of ratio that defines the relation between the liquid assets and

liabilities. It is divided into two parts which are current ratio and quick ratio. Herein, below

liquidity ratio of Tesco company is mentioned below (About Financial information of Tesco,

2019).

Current ratio- This ratio is calculated by applying the formula such as: Current asset/

Current liability. It defines relation between current assets and liabilities. GBP in million

Particulars 2018 (in £) 2017 (in £)

Current assets 13726 15417

Current liabilities 19238 19405

Current ratio 0.71 0.79

Interpretation- As per the above information it can be analysed that company's current assets are

decreasing in 2018. Company's current ratio is of 0.79 in the year 2017 which decreased in 2018

and became 0.71. Basically, ideal current ratio is of 2 : 1 which means company has double

assets to pay the liabilities. So it can be interpreted that company has less assets to pay their

debts.

Quick ratio- This ratio stats the relation between quick assets and current liabilities. As

well as it is calculated by this formula= [current assets- (stock + prepaid expenses)] / current

liability. Below quick ratio of Tesco company for year 2017 and 18 is mentioned below:

GBP in million

Particulars 2018 (in £) 2017 (in £)

Quick assets 11463 13116

Current liabilities 19238 19405

Quick ratio 0.59 0.67

Interpretation- On the basis of above information about the quick ratio of above company it can

be analysed that company's quick assets is decreasing in 2018. In 2017, it is of £13116 which

decreased in became of £11463. Basically, the ideal quick ratio is of 1:1 which means company

should have quick assets equal to the current liabilities. So it can be interpreted that above

company do not have enough quick assets to pay their liabilities.

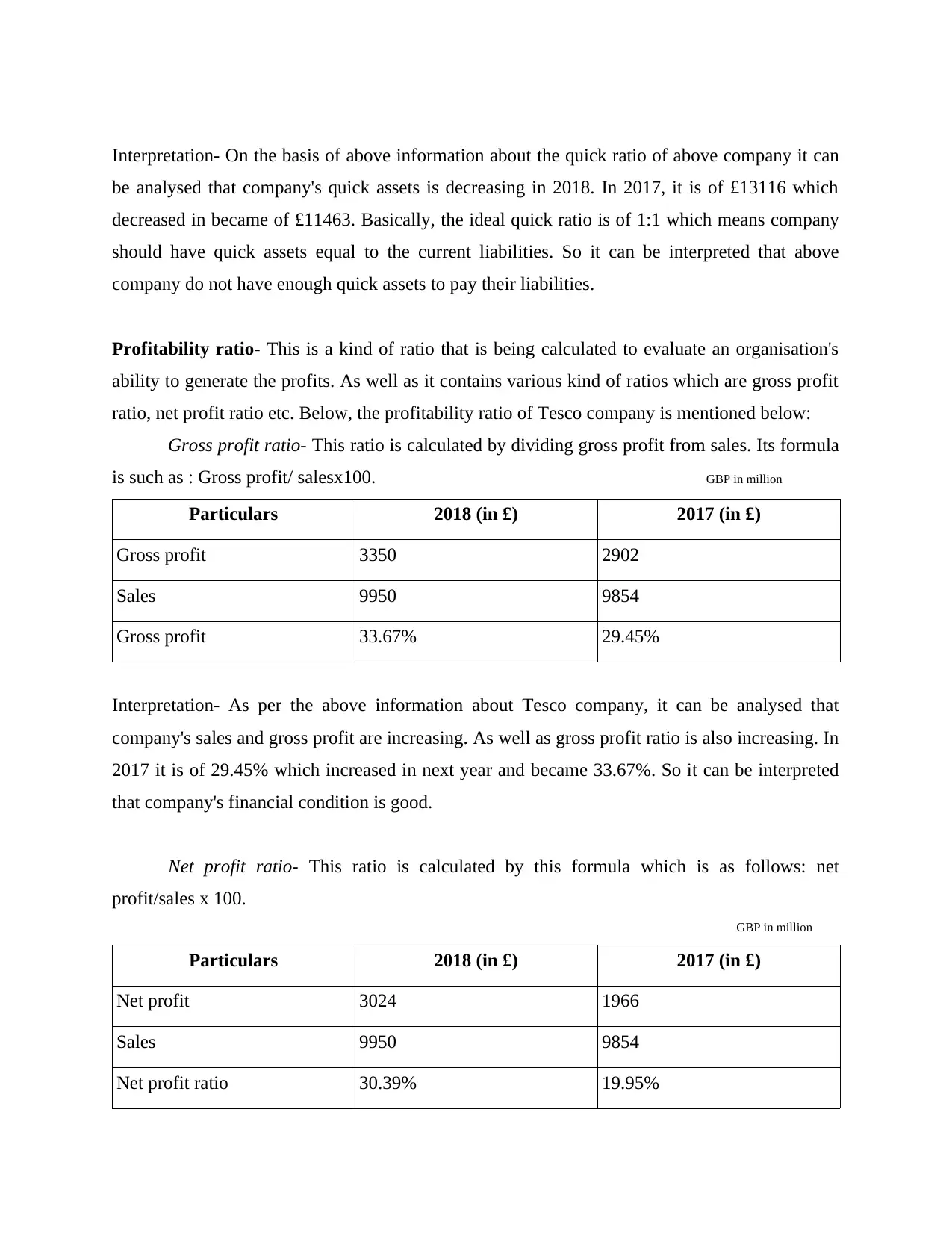

Profitability ratio- This is a kind of ratio that is being calculated to evaluate an organisation's

ability to generate the profits. As well as it contains various kind of ratios which are gross profit

ratio, net profit ratio etc. Below, the profitability ratio of Tesco company is mentioned below:

Gross profit ratio- This ratio is calculated by dividing gross profit from sales. Its formula

is such as : Gross profit/ salesx100. GBP in million

Particulars 2018 (in £) 2017 (in £)

Gross profit 3350 2902

Sales 9950 9854

Gross profit 33.67% 29.45%

Interpretation- As per the above information about Tesco company, it can be analysed that

company's sales and gross profit are increasing. As well as gross profit ratio is also increasing. In

2017 it is of 29.45% which increased in next year and became 33.67%. So it can be interpreted

that company's financial condition is good.

Net profit ratio- This ratio is calculated by this formula which is as follows: net

profit/sales x 100.

GBP in million

Particulars 2018 (in £) 2017 (in £)

Net profit 3024 1966

Sales 9950 9854

Net profit ratio 30.39% 19.95%

be analysed that company's quick assets is decreasing in 2018. In 2017, it is of £13116 which

decreased in became of £11463. Basically, the ideal quick ratio is of 1:1 which means company

should have quick assets equal to the current liabilities. So it can be interpreted that above

company do not have enough quick assets to pay their liabilities.

Profitability ratio- This is a kind of ratio that is being calculated to evaluate an organisation's

ability to generate the profits. As well as it contains various kind of ratios which are gross profit

ratio, net profit ratio etc. Below, the profitability ratio of Tesco company is mentioned below:

Gross profit ratio- This ratio is calculated by dividing gross profit from sales. Its formula

is such as : Gross profit/ salesx100. GBP in million

Particulars 2018 (in £) 2017 (in £)

Gross profit 3350 2902

Sales 9950 9854

Gross profit 33.67% 29.45%

Interpretation- As per the above information about Tesco company, it can be analysed that

company's sales and gross profit are increasing. As well as gross profit ratio is also increasing. In

2017 it is of 29.45% which increased in next year and became 33.67%. So it can be interpreted

that company's financial condition is good.

Net profit ratio- This ratio is calculated by this formula which is as follows: net

profit/sales x 100.

GBP in million

Particulars 2018 (in £) 2017 (in £)

Net profit 3024 1966

Sales 9950 9854

Net profit ratio 30.39% 19.95%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.