Financial Reporting Analysis: Godwin PLC and Marks & Spencer Report

VerifiedAdded on 2020/10/22

|19

|4936

|487

Report

AI Summary

This report provides a comprehensive overview of financial reporting, starting with its context and purpose, and delving into the conceptual and regulatory frameworks that govern it. It highlights the importance of qualitative characteristics in financial reporting and explores the benefits of financial information to various stakeholders, including employees, owners, investors, and creditors. The report examines the value of financial reporting for organizational growth and objectives, using Godwin PLC's financial statements (income statement, changes in equity, balance sheet, and cash flow statement) as a practical example. It also includes an interpretation of Marks and Spencer's financial statements and compares International Accounting Standards (IAS) with International Financial Reporting Standards (IFRS), emphasizing the advantages of IFRS. The report concludes by discussing the varying degrees of compliance with IFRS and their implications.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

1. Context and purpose of financial reporting.............................................................................4

2. Requirement of conceptual and regulatory framework and importance of qualitative

characteristics..............................................................................................................................5

3. Benefits of financial information to stakeholders....................................................................6

4. Value of financial reporting for organisational growth and objective.....................................7

5. statements analysis...................................................................................................................8

(a): Income statements.................................................................................................................8

(b): Changes in equity..................................................................................................................9

(c) Balance Sheet of Godwin PLC...............................................................................................9

(d): Statement of cash flow........................................................................................................10

6. Interpretation of Financial Statements of Marks and Spencer...............................................11

7. International Accounting Standard (IAS) vs International Financial Reporting Standards

(IFRS)........................................................................................................................................12

8. Benefits of International Financial Reporting Standard (IFRS)............................................13

9. Varying degrees of compliance with IFRS............................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

APENDIX......................................................................................................................................18

INTRODUCTION...........................................................................................................................4

1. Context and purpose of financial reporting.............................................................................4

2. Requirement of conceptual and regulatory framework and importance of qualitative

characteristics..............................................................................................................................5

3. Benefits of financial information to stakeholders....................................................................6

4. Value of financial reporting for organisational growth and objective.....................................7

5. statements analysis...................................................................................................................8

(a): Income statements.................................................................................................................8

(b): Changes in equity..................................................................................................................9

(c) Balance Sheet of Godwin PLC...............................................................................................9

(d): Statement of cash flow........................................................................................................10

6. Interpretation of Financial Statements of Marks and Spencer...............................................11

7. International Accounting Standard (IAS) vs International Financial Reporting Standards

(IFRS)........................................................................................................................................12

8. Benefits of International Financial Reporting Standard (IFRS)............................................13

9. Varying degrees of compliance with IFRS............................................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

APENDIX......................................................................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In any industry, whether manufacturing and service, multiple departments work for

business to achieve its objective and every department is connected with finance department.

Financial reporting helps to keep financial and accounting aspects of each and every department

of business. Financial reporting is a process of producing financial statements that discloses

financial status of business. Financial status helps to make decision to management and also to

interested investors. These statements show financial growth of business and also how well funds

are utilised in business to generate revenues. Every organisation works to earn revenues and

managing funds helps to earn more with financial reporting (Bertoni and De Rosa, 2012). Marks

and Spencer is working towards effective financial reporting and to achieve it a report which

consist of various things is prepared. This report consists of purpose of financial reporting,

conceptual and regulatory framework of financial reporting. This also includes qualitative

characteristics that improve financial reporting, stakeholders that are benefited by financial

reporting. Values and objective. Importance and benefits of IAS and IFRS.

1. Context and purpose of financial reporting

Financial reporting is described as disclosure of financial results and related information

to management and external shareholders. Financial status of an organisation can be measured by

various financial statements that represent financial condition of business. These statements are

profit and loss account, balance sheet, cash flow statements. General purpose of financial

reporting is to provide information about results of operations, financial position and cash flow

of organisation. This information is used by the readers of financial statements to make decision

regarding allocation of resources.

Financial reporting plays a vital role in words economies. Its primary purpose is to

provide financial information to owners of company when there is division in management and

ownership of company. This occurs in companies like Marks and Spencer which is a public

limited company that means share capital of company is collected from public at large. These

companies trade in shares through stock exchange (Nobes, 2014). There is geographical disparity

in shareholding pattern and that restricts owners to involve in management of company.

Directors are appointed by shareholders who takes decision about all the aspects in company.

Owners receive annual financial statements that describes them about financial performance of

4

In any industry, whether manufacturing and service, multiple departments work for

business to achieve its objective and every department is connected with finance department.

Financial reporting helps to keep financial and accounting aspects of each and every department

of business. Financial reporting is a process of producing financial statements that discloses

financial status of business. Financial status helps to make decision to management and also to

interested investors. These statements show financial growth of business and also how well funds

are utilised in business to generate revenues. Every organisation works to earn revenues and

managing funds helps to earn more with financial reporting (Bertoni and De Rosa, 2012). Marks

and Spencer is working towards effective financial reporting and to achieve it a report which

consist of various things is prepared. This report consists of purpose of financial reporting,

conceptual and regulatory framework of financial reporting. This also includes qualitative

characteristics that improve financial reporting, stakeholders that are benefited by financial

reporting. Values and objective. Importance and benefits of IAS and IFRS.

1. Context and purpose of financial reporting

Financial reporting is described as disclosure of financial results and related information

to management and external shareholders. Financial status of an organisation can be measured by

various financial statements that represent financial condition of business. These statements are

profit and loss account, balance sheet, cash flow statements. General purpose of financial

reporting is to provide information about results of operations, financial position and cash flow

of organisation. This information is used by the readers of financial statements to make decision

regarding allocation of resources.

Financial reporting plays a vital role in words economies. Its primary purpose is to

provide financial information to owners of company when there is division in management and

ownership of company. This occurs in companies like Marks and Spencer which is a public

limited company that means share capital of company is collected from public at large. These

companies trade in shares through stock exchange (Nobes, 2014). There is geographical disparity

in shareholding pattern and that restricts owners to involve in management of company.

Directors are appointed by shareholders who takes decision about all the aspects in company.

Owners receive annual financial statements that describes them about financial performance of

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business. Without this reporting system owners will be less inclines on the part regarding use of

their invested capital. Other purpose of financial reporting is that it makes financial statements to

comply will all the IFRS that makes financial reporting fair. IFRS provides set standards that are

required to be followed while preparing financial reporting. Financial reporting is also used by

various interested investors to make investing decision. Financial reporting is also used for

making comparison between two accounting years of company and also to compare financial

performance of competitor (Ball, Jayaraman and Shivakumar, 2012). Financial reporting is used

to compare financial performance of two years and variations are recorded. Management use this

information to make planes for future.

2. Requirement of conceptual and regulatory framework and importance of qualitative

characteristics

In financial reporting conceptual framework is a theory of accounting prepared by

following financial standards. Objective of the framework document is to set out a concept that

underline the presentation of financial statements. It is important to understand that conceptual

framework provides set standards on basis of which financial statements are prepared. This give

consistency in financial statements as basis is same and that makes comparison easy. Conceptual

framework deals with fundamental financial reporting issues such as objectives and users of

financial statements, characteristics that makes accounting more useful. It is required to solve

disputes in financial in accounting as fundamental principles are used to prepare financial

statements.

Regulatory framework is a series of steps taken by a regulator to develop responsive

regulations. A regulatory framework is necessary for number of reasons for Marks and Spencer.

Regulatory framework ensures that needs of users of financial statements are met with basic

minimum information. This ensures that all information provided is relevant in economic area

that provides comparability and consistency. When regulations are followed in preparation of

financial statements confidence of users increases in reports (Dyreng, Mayew and Williams,

2012).

Financial information is necessary to make various decision by international management

of Marks and Spencer. To make information more reliable and fair quality of information

provided is considered necessary to be taken care. There are three main quality factors that

information must have is relevance, faithful representation and under stability. Information

5

their invested capital. Other purpose of financial reporting is that it makes financial statements to

comply will all the IFRS that makes financial reporting fair. IFRS provides set standards that are

required to be followed while preparing financial reporting. Financial reporting is also used by

various interested investors to make investing decision. Financial reporting is also used for

making comparison between two accounting years of company and also to compare financial

performance of competitor (Ball, Jayaraman and Shivakumar, 2012). Financial reporting is used

to compare financial performance of two years and variations are recorded. Management use this

information to make planes for future.

2. Requirement of conceptual and regulatory framework and importance of qualitative

characteristics

In financial reporting conceptual framework is a theory of accounting prepared by

following financial standards. Objective of the framework document is to set out a concept that

underline the presentation of financial statements. It is important to understand that conceptual

framework provides set standards on basis of which financial statements are prepared. This give

consistency in financial statements as basis is same and that makes comparison easy. Conceptual

framework deals with fundamental financial reporting issues such as objectives and users of

financial statements, characteristics that makes accounting more useful. It is required to solve

disputes in financial in accounting as fundamental principles are used to prepare financial

statements.

Regulatory framework is a series of steps taken by a regulator to develop responsive

regulations. A regulatory framework is necessary for number of reasons for Marks and Spencer.

Regulatory framework ensures that needs of users of financial statements are met with basic

minimum information. This ensures that all information provided is relevant in economic area

that provides comparability and consistency. When regulations are followed in preparation of

financial statements confidence of users increases in reports (Dyreng, Mayew and Williams,

2012).

Financial information is necessary to make various decision by international management

of Marks and Spencer. To make information more reliable and fair quality of information

provided is considered necessary to be taken care. There are three main quality factors that

information must have is relevance, faithful representation and under stability. Information

5

provided in financial statements should have some basis on which they are prepared that creates

relevancy of information provided. Statements should be formed in such manner that they are

easy to understand by public at large even to those who have no knowledge of finances.

Information provided should be true and fair there should be no biased information that leads to

misleading decision making to investors and to managers of businesses.

3. Benefits of financial information to stakeholders

Stakeholders are the persons who can affect or are affected by actions taken by Marks

and Spencer Stakeholder is any person, organisation, social group or society at large who have

stake in an organisation. Stakeholders are directly and indirectly affected by actions taken by

organisation (Hope, Thomas and Vyas, 2013). Stakeholder is an investor in businesses whose

action determines results of business decision. Every organisation deal with two type of

stakeholders internal and external stakeholders.

Internal stakeholders are the one who are already committed to serving to organisation as

directors, employees and owners of business. These stakeholders are related to business and

directly affected by every decision taken by business. Financial information is used by various

stakeholders and benefits of this information to different internal stakeholders are as follows-

Employees- Organisations growth and employee’s growth both move together.

Employees prefer to work with a company that is continuously growing and to measure

growth financial statements are very important. When financial status of a company is

really good and scope of continuous growth is there then that leads to attract and retain

efficient employees.

Owners- Financial information of business is required by owners to calculate efficiency

of utilisation of funds invested by them. Financial information helps to measure growth in

business during an accounting year and if any variation is there from set standards then

that must be mentioned.

External stakeholders are the one who are not directly related with business but indirectly

got affected by actions and policies of business. These stakeholders are not within the business

but are affected by performance of business entities. External stakeholders of Marks and Spencer

who are benefited with financial reporting are as follows-

Investors- Financial information serves as basis for investors to make investing decision

in company. Before making any investment decision past performance if business is

6

relevancy of information provided. Statements should be formed in such manner that they are

easy to understand by public at large even to those who have no knowledge of finances.

Information provided should be true and fair there should be no biased information that leads to

misleading decision making to investors and to managers of businesses.

3. Benefits of financial information to stakeholders

Stakeholders are the persons who can affect or are affected by actions taken by Marks

and Spencer Stakeholder is any person, organisation, social group or society at large who have

stake in an organisation. Stakeholders are directly and indirectly affected by actions taken by

organisation (Hope, Thomas and Vyas, 2013). Stakeholder is an investor in businesses whose

action determines results of business decision. Every organisation deal with two type of

stakeholders internal and external stakeholders.

Internal stakeholders are the one who are already committed to serving to organisation as

directors, employees and owners of business. These stakeholders are related to business and

directly affected by every decision taken by business. Financial information is used by various

stakeholders and benefits of this information to different internal stakeholders are as follows-

Employees- Organisations growth and employee’s growth both move together.

Employees prefer to work with a company that is continuously growing and to measure

growth financial statements are very important. When financial status of a company is

really good and scope of continuous growth is there then that leads to attract and retain

efficient employees.

Owners- Financial information of business is required by owners to calculate efficiency

of utilisation of funds invested by them. Financial information helps to measure growth in

business during an accounting year and if any variation is there from set standards then

that must be mentioned.

External stakeholders are the one who are not directly related with business but indirectly

got affected by actions and policies of business. These stakeholders are not within the business

but are affected by performance of business entities. External stakeholders of Marks and Spencer

who are benefited with financial reporting are as follows-

Investors- Financial information serves as basis for investors to make investing decision

in company. Before making any investment decision past performance if business is

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

considered and that is evaluated by its financial statements. Every investor invests in a

company that shows profits and scope of growth in their financial reporting.

Creditors- Creditors are the person to whom business needs to repay its dues. In business

transactions are done and paid on credit basis and a financially sound business is

considered more viable to provide credit. Creditors use financial reporting information to

know about financial condition of business to whom they are serving credit. This is

important to secure funds.

4. Value of financial reporting for organisational growth and objective

Financial reporting is considered as one of the important factor that influences growth

and objective of businesses. Marks and Spencer is an organisation that focus on objectives like

increasing market base, increasing credit rating and increasing profits. To attain these objective

organisation needs to grow on continuous basis. To know growth of a business its financial

statements are considered as basis. When financial conditions are increasing that reflects growth

of business. When organisation is growing and increasing on continuous basis that reflects that

objectives of business are achieved by business organisation (Bentley, Omer and Sharp, 2013).

Financial reporting should reflect fair financial position to conclude effective growth of business.

Organisation works towards achieving various objectives and one of the most important

objective is continuous growth with increasing revenue. Marks and Spencer is working towards

achieving its objective and preparation of financial reporting helps them to achieving these

objectives. As internal management of company requires financial information to allocate

various resources that are available with company. Internal management makes planes for

company that are needed to be initiated in future to achieve future objectives. Management of

company prepares planes that are based on past results. Growth plans are designed for every

financial year and that plan includes new objectives and also if any variance in past performance

then effective measures to cope up with that is also included.

Financial performance of business is a huge concern for different stakeholders of

business. Information regarding financial performance of business is gathered for financial

statements that shows true and fair view of financial status of business. A financially sound

business attracts more investors as more returns are expected from investing in this company.

More investors will bring more funds to company and availability of more capital to invest will

be there with the company. When company is getting more funds as investors that increases

7

company that shows profits and scope of growth in their financial reporting.

Creditors- Creditors are the person to whom business needs to repay its dues. In business

transactions are done and paid on credit basis and a financially sound business is

considered more viable to provide credit. Creditors use financial reporting information to

know about financial condition of business to whom they are serving credit. This is

important to secure funds.

4. Value of financial reporting for organisational growth and objective

Financial reporting is considered as one of the important factor that influences growth

and objective of businesses. Marks and Spencer is an organisation that focus on objectives like

increasing market base, increasing credit rating and increasing profits. To attain these objective

organisation needs to grow on continuous basis. To know growth of a business its financial

statements are considered as basis. When financial conditions are increasing that reflects growth

of business. When organisation is growing and increasing on continuous basis that reflects that

objectives of business are achieved by business organisation (Bentley, Omer and Sharp, 2013).

Financial reporting should reflect fair financial position to conclude effective growth of business.

Organisation works towards achieving various objectives and one of the most important

objective is continuous growth with increasing revenue. Marks and Spencer is working towards

achieving its objective and preparation of financial reporting helps them to achieving these

objectives. As internal management of company requires financial information to allocate

various resources that are available with company. Internal management makes planes for

company that are needed to be initiated in future to achieve future objectives. Management of

company prepares planes that are based on past results. Growth plans are designed for every

financial year and that plan includes new objectives and also if any variance in past performance

then effective measures to cope up with that is also included.

Financial performance of business is a huge concern for different stakeholders of

business. Information regarding financial performance of business is gathered for financial

statements that shows true and fair view of financial status of business. A financially sound

business attracts more investors as more returns are expected from investing in this company.

More investors will bring more funds to company and availability of more capital to invest will

be there with the company. When company is getting more funds as investors that increases

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

public image of company. Availability of more funds to business creates more investing

opportunities and helps them to earn more and increase revenues. Good financial performance

attracts more suppliers to serve credit. Business that enjoys more credit facility can utilise its

fund in other productive activities. Marks and Spencer enjoys good financial status that reduces

requirement of funds as payments needs to be made in time intervals. A good credit rating of a

company helps to generate more funds on credit whenever demanded. Creditors to evaluate

financial performance requires financial statements of company that represents its financial

status.

Good financial condition attracts more and more consumers as a company which earns

more have a positive image for consumers. This positive image also increases consumer base as

one consumer influence other one to buy goods and services of company. When consumer base

increases that ultimately leads to increase in sales and also market share of company will

increase. When market share of company will increase that ultimately leads to more profits for

company. Company will achieve one of the most important objective of profit maximisation by

effective financial reporting (Fu, Kraft and Zhang, 2012). More profits will bring more earnings

to owners and investors and value of company will increase in market. This increased image will

help company to attain its future objectives more efficiently in minimum time period.

5. statements analysis

(a): Income statements

Godwin PLC Statement of Profit and

Loss for the year ended 31 December

8

opportunities and helps them to earn more and increase revenues. Good financial performance

attracts more suppliers to serve credit. Business that enjoys more credit facility can utilise its

fund in other productive activities. Marks and Spencer enjoys good financial status that reduces

requirement of funds as payments needs to be made in time intervals. A good credit rating of a

company helps to generate more funds on credit whenever demanded. Creditors to evaluate

financial performance requires financial statements of company that represents its financial

status.

Good financial condition attracts more and more consumers as a company which earns

more have a positive image for consumers. This positive image also increases consumer base as

one consumer influence other one to buy goods and services of company. When consumer base

increases that ultimately leads to increase in sales and also market share of company will

increase. When market share of company will increase that ultimately leads to more profits for

company. Company will achieve one of the most important objective of profit maximisation by

effective financial reporting (Fu, Kraft and Zhang, 2012). More profits will bring more earnings

to owners and investors and value of company will increase in market. This increased image will

help company to attain its future objectives more efficiently in minimum time period.

5. statements analysis

(a): Income statements

Godwin PLC Statement of Profit and

Loss for the year ended 31 December

8

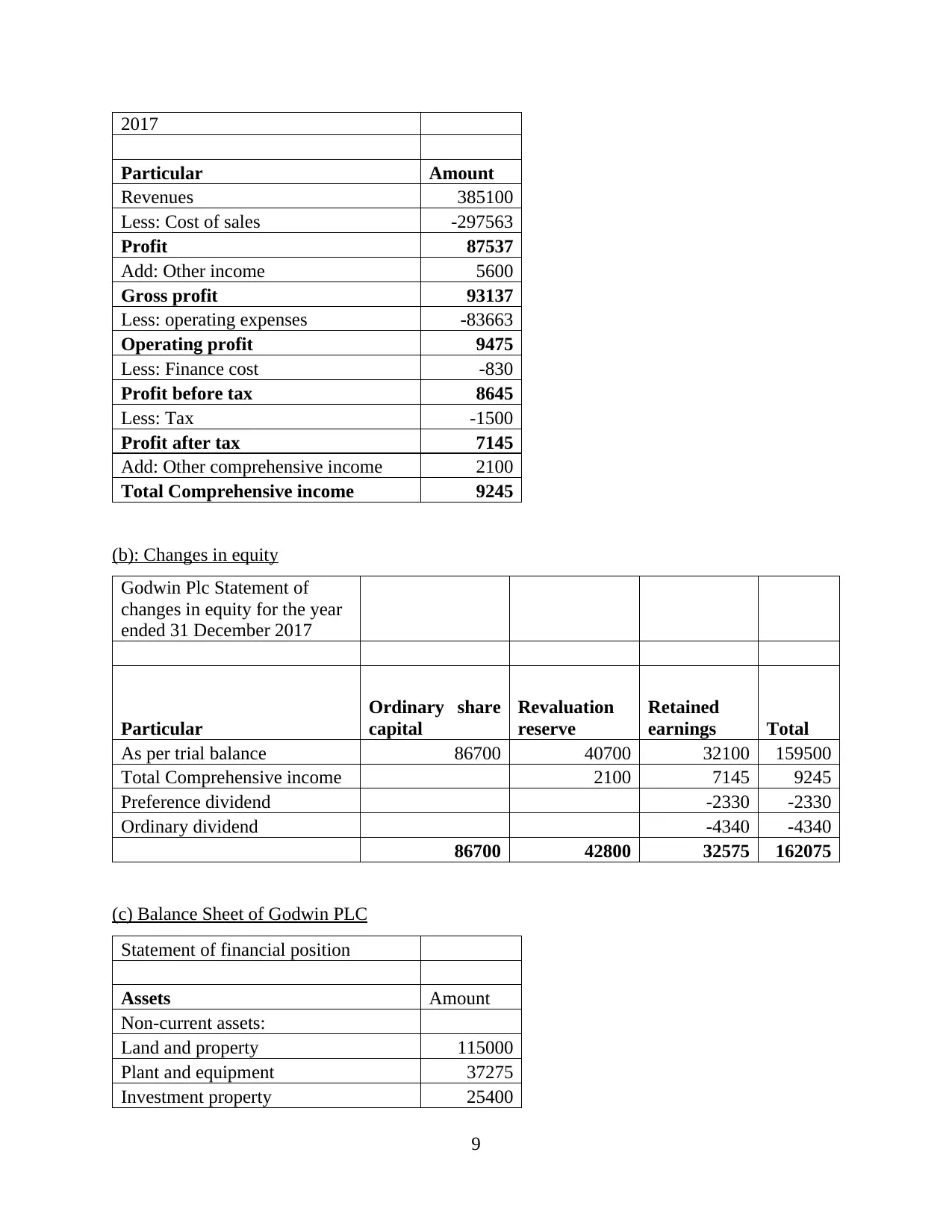

2017

Particular Amount

Revenues 385100

Less: Cost of sales -297563

Profit 87537

Add: Other income 5600

Gross profit 93137

Less: operating expenses -83663

Operating profit 9475

Less: Finance cost -830

Profit before tax 8645

Less: Tax -1500

Profit after tax 7145

Add: Other comprehensive income 2100

Total Comprehensive income 9245

(b): Changes in equity

Godwin Plc Statement of

changes in equity for the year

ended 31 December 2017

Particular

Ordinary share

capital

Revaluation

reserve

Retained

earnings Total

As per trial balance 86700 40700 32100 159500

Total Comprehensive income 2100 7145 9245

Preference dividend -2330 -2330

Ordinary dividend -4340 -4340

86700 42800 32575 162075

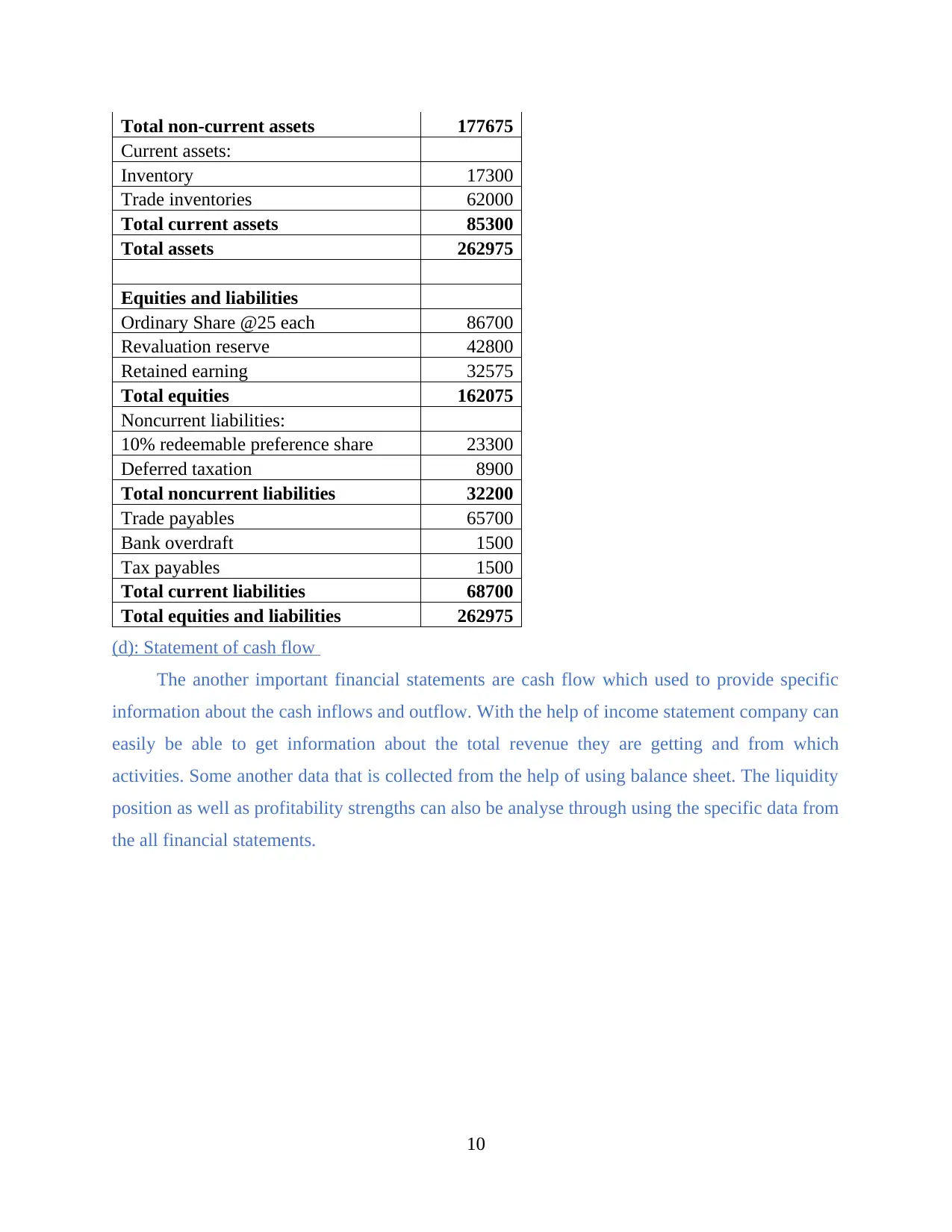

(c) Balance Sheet of Godwin PLC

Statement of financial position

Assets Amount

Non-current assets:

Land and property 115000

Plant and equipment 37275

Investment property 25400

9

Particular Amount

Revenues 385100

Less: Cost of sales -297563

Profit 87537

Add: Other income 5600

Gross profit 93137

Less: operating expenses -83663

Operating profit 9475

Less: Finance cost -830

Profit before tax 8645

Less: Tax -1500

Profit after tax 7145

Add: Other comprehensive income 2100

Total Comprehensive income 9245

(b): Changes in equity

Godwin Plc Statement of

changes in equity for the year

ended 31 December 2017

Particular

Ordinary share

capital

Revaluation

reserve

Retained

earnings Total

As per trial balance 86700 40700 32100 159500

Total Comprehensive income 2100 7145 9245

Preference dividend -2330 -2330

Ordinary dividend -4340 -4340

86700 42800 32575 162075

(c) Balance Sheet of Godwin PLC

Statement of financial position

Assets Amount

Non-current assets:

Land and property 115000

Plant and equipment 37275

Investment property 25400

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total non-current assets 177675

Current assets:

Inventory 17300

Trade inventories 62000

Total current assets 85300

Total assets 262975

Equities and liabilities

Ordinary Share @25 each 86700

Revaluation reserve 42800

Retained earning 32575

Total equities 162075

Noncurrent liabilities:

10% redeemable preference share 23300

Deferred taxation 8900

Total noncurrent liabilities 32200

Trade payables 65700

Bank overdraft 1500

Tax payables 1500

Total current liabilities 68700

Total equities and liabilities 262975

(d): Statement of cash flow

The another important financial statements are cash flow which used to provide specific

information about the cash inflows and outflow. With the help of income statement company can

easily be able to get information about the total revenue they are getting and from which

activities. Some another data that is collected from the help of using balance sheet. The liquidity

position as well as profitability strengths can also be analyse through using the specific data from

the all financial statements.

10

Current assets:

Inventory 17300

Trade inventories 62000

Total current assets 85300

Total assets 262975

Equities and liabilities

Ordinary Share @25 each 86700

Revaluation reserve 42800

Retained earning 32575

Total equities 162075

Noncurrent liabilities:

10% redeemable preference share 23300

Deferred taxation 8900

Total noncurrent liabilities 32200

Trade payables 65700

Bank overdraft 1500

Tax payables 1500

Total current liabilities 68700

Total equities and liabilities 262975

(d): Statement of cash flow

The another important financial statements are cash flow which used to provide specific

information about the cash inflows and outflow. With the help of income statement company can

easily be able to get information about the total revenue they are getting and from which

activities. Some another data that is collected from the help of using balance sheet. The liquidity

position as well as profitability strengths can also be analyse through using the specific data from

the all financial statements.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

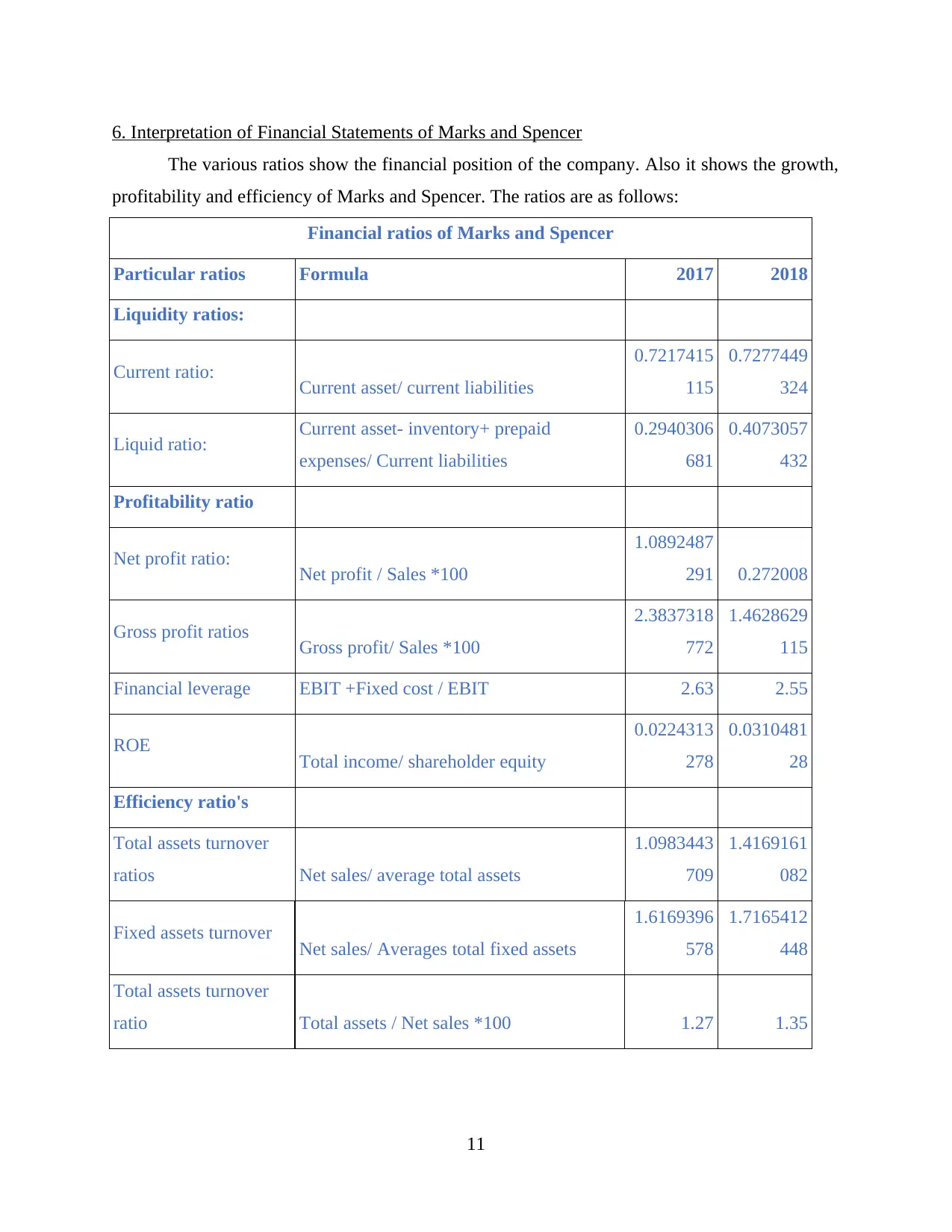

6. Interpretation of Financial Statements of Marks and Spencer

The various ratios show the financial position of the company. Also it shows the growth,

profitability and efficiency of Marks and Spencer. The ratios are as follows:

Financial ratios of Marks and Spencer

Particular ratios Formula 2017 2018

Liquidity ratios:

Current ratio: Current asset/ current liabilities

0.7217415

115

0.7277449

324

Liquid ratio: Current asset- inventory+ prepaid

expenses/ Current liabilities

0.2940306

681

0.4073057

432

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.0892487

291 0.272008

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

Financial leverage EBIT +Fixed cost / EBIT 2.63 2.55

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.0983443

709

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets

1.6169396

578

1.7165412

448

Total assets turnover

ratio Total assets / Net sales *100 1.27 1.35

11

The various ratios show the financial position of the company. Also it shows the growth,

profitability and efficiency of Marks and Spencer. The ratios are as follows:

Financial ratios of Marks and Spencer

Particular ratios Formula 2017 2018

Liquidity ratios:

Current ratio: Current asset/ current liabilities

0.7217415

115

0.7277449

324

Liquid ratio: Current asset- inventory+ prepaid

expenses/ Current liabilities

0.2940306

681

0.4073057

432

Profitability ratio

Net profit ratio: Net profit / Sales *100

1.0892487

291 0.272008

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

Financial leverage EBIT +Fixed cost / EBIT 2.63 2.55

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.0983443

709

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets

1.6169396

578

1.7165412

448

Total assets turnover

ratio Total assets / Net sales *100 1.27 1.35

11

1. Current Ratio for the year 2017 and 2018 are 0.73 and 0.72 respectively. This shows that

company has failed to meet out its short-terms obligations as compared to 2017.

2. Quick Ratio for the year 2017 and 2018 are 0.33 and 0.29 respectively. This indicates that

the most liquid assets such as cash and all cash equivalents and marketable securities

have reduced in 2018 (Bevis, 2013).

3. Financial Leverage shows the relationship of total debt to total assets. The leverage of

2017 and 2018 are 2.63 and 2.55 respectively. There is a decrease in financial leverage,

which means that the company has been able to repay its debts in 2018. Higher financial

leverage is bad for the company as it could the chances of bankruptcy is high.

4. Debt to Equity indicates the proportion of shareholders' equity and debt used to finance a

company's assets. The ratio for 2017 and 2018 are 0.54 and 0.56 respectively. The

increase in the ratio in 2018 shows that the financial soundness of the company is good

from the last year. In will attract creditors to invest in the company.

5. Return on Assets ratio indicates how much profit the company has earned by utilizing its

overall resources. The ratio is 1.40 for 2017 and 0.32 for 2018. There is a decrease in this

ratio from 1.08, which shows that company is not making enough profits from its assets.

6. Return on Equity reflects the relationship of the profitability with the equity. It is used for

measuring the earnings from the investment. The ratio is 3.55 for 2017 and 0.84 for 2018.

It has reduced by 2.71 from the last year. The fall indicates that company is failing to

make profits with the capital available in the company (Alali and Foote, 2012).

7. Receivables Turnover shows the number of times Marks and Spencer takes to collect its

average accounts receivable. It is used to measure the ability to give credits to the

customers and collect funds from the creditors within the specified time. The turnover are

94.38 and 95.86 for 2017 and 2018 respectively.

7. International Accounting Standard (IAS) vs International Financial Reporting

Standards (IFRS)

International Accounting Standard (IAS) International Financial Reporting

Standards (IFRS)

1. IAS are the standards applied on the

transactions shown in the financial statements.

1. IFRS are the revised and updated version of

existing IAS.

12

company has failed to meet out its short-terms obligations as compared to 2017.

2. Quick Ratio for the year 2017 and 2018 are 0.33 and 0.29 respectively. This indicates that

the most liquid assets such as cash and all cash equivalents and marketable securities

have reduced in 2018 (Bevis, 2013).

3. Financial Leverage shows the relationship of total debt to total assets. The leverage of

2017 and 2018 are 2.63 and 2.55 respectively. There is a decrease in financial leverage,

which means that the company has been able to repay its debts in 2018. Higher financial

leverage is bad for the company as it could the chances of bankruptcy is high.

4. Debt to Equity indicates the proportion of shareholders' equity and debt used to finance a

company's assets. The ratio for 2017 and 2018 are 0.54 and 0.56 respectively. The

increase in the ratio in 2018 shows that the financial soundness of the company is good

from the last year. In will attract creditors to invest in the company.

5. Return on Assets ratio indicates how much profit the company has earned by utilizing its

overall resources. The ratio is 1.40 for 2017 and 0.32 for 2018. There is a decrease in this

ratio from 1.08, which shows that company is not making enough profits from its assets.

6. Return on Equity reflects the relationship of the profitability with the equity. It is used for

measuring the earnings from the investment. The ratio is 3.55 for 2017 and 0.84 for 2018.

It has reduced by 2.71 from the last year. The fall indicates that company is failing to

make profits with the capital available in the company (Alali and Foote, 2012).

7. Receivables Turnover shows the number of times Marks and Spencer takes to collect its

average accounts receivable. It is used to measure the ability to give credits to the

customers and collect funds from the creditors within the specified time. The turnover are

94.38 and 95.86 for 2017 and 2018 respectively.

7. International Accounting Standard (IAS) vs International Financial Reporting

Standards (IFRS)

International Accounting Standard (IAS) International Financial Reporting

Standards (IFRS)

1. IAS are the standards applied on the

transactions shown in the financial statements.

1. IFRS are the revised and updated version of

existing IAS.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.