Financial Reporting: Purpose, Framework, Stakeholders, and Analysis

VerifiedAdded on 2020/07/23

|15

|4898

|54

Report

AI Summary

This report provides a comprehensive overview of financial reporting, beginning with its fundamental purpose of providing financial information to stakeholders, including investors, lenders, and management, to facilitate informed decision-making. It delves into the conceptual and regulatory frameworks, emphasizing the importance of IASB guidelines and qualitative characteristics such as relevance, materiality, understandability, comparability, and reliability. The report examines the roles of various stakeholders, including managers, investors, and creditors, and their reliance on financial statements for assessing a company's performance and financial health. It further explores the presentation of financial statements, including balance sheets, income statements, and cash flow statements, along with the use of financial ratios for analysis. The report also distinguishes between IAS and IFRS, discusses the benefits of IFRS adoption, and addresses the varying degrees of IFRS compliance globally. Overall, the report underscores the significance of financial reporting in ensuring transparency, accountability, and effective economic decision-making.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Purpose of financial reporting............................................................................................1

2. Conceptual and regulatory framework of financial reporting and qualitative characteristics

of financial information..........................................................................................................3

3. Discuss different types of stakeholders..............................................................................5

4. Value of financial reporting to company ...........................................................................6

5. Presentation of financial statements...................................................................................7

6. Financial ratios and interpretations....................................................................................8

7. Distinguish between IAS and IFRS....................................................................................9

8. Discussing benefits of IFRS.............................................................................................10

9. Varying degrees of compliance of IFRS by the companies in the world.........................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1. Purpose of financial reporting............................................................................................1

2. Conceptual and regulatory framework of financial reporting and qualitative characteristics

of financial information..........................................................................................................3

3. Discuss different types of stakeholders..............................................................................5

4. Value of financial reporting to company ...........................................................................6

5. Presentation of financial statements...................................................................................7

6. Financial ratios and interpretations....................................................................................8

7. Distinguish between IAS and IFRS....................................................................................9

8. Discussing benefits of IFRS.............................................................................................10

9. Varying degrees of compliance of IFRS by the companies in the world.........................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

The information regarding financial statements are required to be presented in a way

which is then is assessed by users of financial information. This is achieved by preparing

financial reports by the company. The enclosed report deals with importance of financial

reporting which has great importance in business world and overcoming international scandals

quite effectively. Financial reporting is helpful for management and that to external users such as

investors, lenders that directly provide funds to organisation for effective functioning. Such

stakeholders’ take the economic decisions quite effectually. This is essential so that transparency

of financial position of the company is reflected in the best possible way.

TASK 1

1. Purpose of financial reporting

The purpose of financial reporting is to prepare reports of the organisation so that it may

be able to keep perfect record of each and every transactions and activities taking place in the

organisation. This is however, not an easy task but require efficient accountants so that proper

reports may be prepared. Financial reporting tells business whether it is making profit or loss in

the current period in the best possible and productive way (Ge, Li and McVay, 2017).

Another purpose of preparing financial reporting is to provide financial performance o

the company to its stakeholders be it investors or shareholders. This is essential as lenders and

inventor’s keep eye on company that whether firm is using resources provided to it wisely or not.

If not then company loses it valuable investors. As such, financial reporting is required to be

furnished to them so that performance may be evaluated nicely. Moreover, company should

perform well so that profits are made in large quantum with much ease by utilising scarce

resources.

The scandals going internationally is a major issue in the current scenario. Thus, financial

reporting is important tool so that organisation may be able to provide fair financial reports to

stakeholders and as such, transparency and clarity is maintained effectively by firm (Cohen,

Krishnamoorthy and Wright, 2017). Moreover, perfect records of daily activities are listed in

financial reports. It has also section of liabilities and assets described in it, which is important to

1

The information regarding financial statements are required to be presented in a way

which is then is assessed by users of financial information. This is achieved by preparing

financial reports by the company. The enclosed report deals with importance of financial

reporting which has great importance in business world and overcoming international scandals

quite effectively. Financial reporting is helpful for management and that to external users such as

investors, lenders that directly provide funds to organisation for effective functioning. Such

stakeholders’ take the economic decisions quite effectually. This is essential so that transparency

of financial position of the company is reflected in the best possible way.

TASK 1

1. Purpose of financial reporting

The purpose of financial reporting is to prepare reports of the organisation so that it may

be able to keep perfect record of each and every transactions and activities taking place in the

organisation. This is however, not an easy task but require efficient accountants so that proper

reports may be prepared. Financial reporting tells business whether it is making profit or loss in

the current period in the best possible and productive way (Ge, Li and McVay, 2017).

Another purpose of preparing financial reporting is to provide financial performance o

the company to its stakeholders be it investors or shareholders. This is essential as lenders and

inventor’s keep eye on company that whether firm is using resources provided to it wisely or not.

If not then company loses it valuable investors. As such, financial reporting is required to be

furnished to them so that performance may be evaluated nicely. Moreover, company should

perform well so that profits are made in large quantum with much ease by utilising scarce

resources.

The scandals going internationally is a major issue in the current scenario. Thus, financial

reporting is important tool so that organisation may be able to provide fair financial reports to

stakeholders and as such, transparency and clarity is maintained effectively by firm (Cohen,

Krishnamoorthy and Wright, 2017). Moreover, perfect records of daily activities are listed in

financial reports. It has also section of liabilities and assets described in it, which is important to

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

stakeholders whether they are external or internal. It is also reported in that how business is using

capital and how profits are being generated by it.

Furthermore, financial report also prepared for the purpose of providing information to

the stakeholders that capital is in adequate manner and whether company can lead to future

growth with much ease. In simple words, it is also listed that capital is sufficient or not for

carrying out future activities in the best possible way. Moreover, financial reporting provides

much needed information to lenders and investors and as such, firm’s value is created nicely and

as a result, clarity is being observed (Bonsall, S. B. and et.al, 2017).

Financial reporting consists of financial statement such as balance sheet, cash flow

statement, income statement, changes in shareholder’s' equity. It also contains notes to accounts

or workings represents information entered in financial statements. Annual reports are also

furnished in it effectively. This is done with a purpose to give clarity of financial strength of

company and financial health of it easily. Apart from providing information to stakeholders, it

also provides same to statutory auditors which is essential so that true and fairness of financial

statements may be ascertained with much ease.

The information regarding economic resources used in the organisation for its

functionality is also provided and where money is spent is also provided to shareholders. This

means that complete record of financial performance of firm is being listed in financial reporting

and as such, users of such information are quite benefited effectually. Moreover, auditors are

also benefited, as it is require by them to test the accuracy of financial statements. Taxation

authorities also require this so that company may pay tax wisely. The financial reporting also is

used for the purpose of bidding and labour contract and for government supplies as well.

Financial reporting helps firm to abide by various rules and laws, which are required by

government so that business is carried out in fair manner and is not detrimental in the public

interest. For this, organisation is required to file financial statements to ROC (Registrar of

Companies) for legal purpose. As such, it is also required for legal purpose as well. Moreover, it

is also essential for financial analysis, benchmarking, and financial planning as well. Moreover,

decision making is also achieved by it effectively (Johnston and Petacchi, 2017). It is also used

for the purpose to raise capital from domestic or locally and also tat from international as well.

This helps organisation to have much capital from domestic and overseas so that it may be able

2

capital and how profits are being generated by it.

Furthermore, financial report also prepared for the purpose of providing information to

the stakeholders that capital is in adequate manner and whether company can lead to future

growth with much ease. In simple words, it is also listed that capital is sufficient or not for

carrying out future activities in the best possible way. Moreover, financial reporting provides

much needed information to lenders and investors and as such, firm’s value is created nicely and

as a result, clarity is being observed (Bonsall, S. B. and et.al, 2017).

Financial reporting consists of financial statement such as balance sheet, cash flow

statement, income statement, changes in shareholder’s' equity. It also contains notes to accounts

or workings represents information entered in financial statements. Annual reports are also

furnished in it effectively. This is done with a purpose to give clarity of financial strength of

company and financial health of it easily. Apart from providing information to stakeholders, it

also provides same to statutory auditors which is essential so that true and fairness of financial

statements may be ascertained with much ease.

The information regarding economic resources used in the organisation for its

functionality is also provided and where money is spent is also provided to shareholders. This

means that complete record of financial performance of firm is being listed in financial reporting

and as such, users of such information are quite benefited effectually. Moreover, auditors are

also benefited, as it is require by them to test the accuracy of financial statements. Taxation

authorities also require this so that company may pay tax wisely. The financial reporting also is

used for the purpose of bidding and labour contract and for government supplies as well.

Financial reporting helps firm to abide by various rules and laws, which are required by

government so that business is carried out in fair manner and is not detrimental in the public

interest. For this, organisation is required to file financial statements to ROC (Registrar of

Companies) for legal purpose. As such, it is also required for legal purpose as well. Moreover, it

is also essential for financial analysis, benchmarking, and financial planning as well. Moreover,

decision making is also achieved by it effectively (Johnston and Petacchi, 2017). It is also used

for the purpose to raise capital from domestic or locally and also tat from international as well.

This helps organisation to have much capital from domestic and overseas so that it may be able

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

to function effectively in the market and may satisfied demands of customers easily. Thus, it

fulfils needs effectively and with much ease.

Financial reporting is used in the context to provide clarity to stakeholders’ about the

financial performance of it so that more and more of shareholders’ subscribe shares. Moreover,

investors’ may also provide funds, which are required for carrying out operations in effectual

manner. Public at large is benefited by such information and management comes to know about

the effectiveness or weakness of company (Naranjo, Saavedra and Verdi, 2017). Thus,

management takes several steps to restructure performance of the company so it may be able to

achieve goals and objectives in desired way. As a result, financial reporting is the backbone of

the company.

2. Conceptual and regulatory framework of financial reporting and qualitative characteristics of

financial information

The financial reporting is important for organisation, as it is required by professional

bodies in effective format and in legal framework. In this regard, IASB (International

Accounting Standards Board) has given guidelines and framework within which information is

required by the board. This framework is required to be followed by each and every organisation.

This binds organisation in way, which exhibits meaningful information, and also which can be

comparable easily. External users of accounting information, which is then useful for them,

require the same information.

The principles, which are required by organisation given by professional body, is

numerous. The economic resources and claims must be provided by organisation to users of

accounting information, which is then generated in financial reports so that they all may be able

to provide liquidity and profitability of information to users. They assess liquidity and as such,

business’s strengths and weaknesses are also reflected in such reports which is required by body

to be furnished in financial report of the company.

Accrual accounting must also be furnished in financial reports. This provides information

of cash flow generated by organisation in a particular period of time. The changes in economic

resources must be furnished in income statement section (Qualitative Characteristics of

Financial Information). On the other hand, cash flows generated in current period must be

included in cash flow statement. The professional body also requires that information must be

3

fulfils needs effectively and with much ease.

Financial reporting is used in the context to provide clarity to stakeholders’ about the

financial performance of it so that more and more of shareholders’ subscribe shares. Moreover,

investors’ may also provide funds, which are required for carrying out operations in effectual

manner. Public at large is benefited by such information and management comes to know about

the effectiveness or weakness of company (Naranjo, Saavedra and Verdi, 2017). Thus,

management takes several steps to restructure performance of the company so it may be able to

achieve goals and objectives in desired way. As a result, financial reporting is the backbone of

the company.

2. Conceptual and regulatory framework of financial reporting and qualitative characteristics of

financial information

The financial reporting is important for organisation, as it is required by professional

bodies in effective format and in legal framework. In this regard, IASB (International

Accounting Standards Board) has given guidelines and framework within which information is

required by the board. This framework is required to be followed by each and every organisation.

This binds organisation in way, which exhibits meaningful information, and also which can be

comparable easily. External users of accounting information, which is then useful for them,

require the same information.

The principles, which are required by organisation given by professional body, is

numerous. The economic resources and claims must be provided by organisation to users of

accounting information, which is then generated in financial reports so that they all may be able

to provide liquidity and profitability of information to users. They assess liquidity and as such,

business’s strengths and weaknesses are also reflected in such reports which is required by body

to be furnished in financial report of the company.

Accrual accounting must also be furnished in financial reports. This provides information

of cash flow generated by organisation in a particular period of time. The changes in economic

resources must be furnished in income statement section (Qualitative Characteristics of

Financial Information). On the other hand, cash flows generated in current period must be

included in cash flow statement. The professional body also requires that information must be

3

furnished by listing elements of financial statements. This means that elements directly related to

assets, liabilities and that to equity as well. These elements are related to financial position.

Furthermore, income statement should have elements regarding revenue and expenses as well.

The financial reporting is required to be done in a way so that legal framework provided

by professional bodies are fulfilled in the most productive way (Naranjo, Saavedra and Verdi,

2017). Besides this, for having effective preparation of financial reporting it is required that

financial information is prepared effectually. The qualities and attributes of financial information

are as follows :

1. Relevance –

The relevance concept states that users of accounting information should record all

information in financial information, which provides help to make effective decisions. In simple

words, the information should be recorded only if it aids in decision making of users o financial

information. They can be external and internal stakeholders, which are directly involved with the

company. Thus, the same information must be recorded in such way, which enhances decision

making of stakeholders.

2. Materiality –

The principle states that only material information should be recorded in books of

accounts. This is because only material information affects decisions of users of accounting

information. Accountants are required to follow guidelines, which are imparted by professional

bodies in a way so that it may be relevant for them to make effective and better economic

decisions effectually. Accountants when preparing financial information should ignore non-

material information. This will provide effective information to them and as such, legal

framework will be adorned by it (Towery, 2017).

3. Understandability –

Users of accounting information quite easily should present the financial information in

effective way and that also in standard way, which may be easily understandable. Thus, financial

information should be stated and presented in simple form and terms so that users may assess it

easily and as such, decisions may be taken in effectual manner.

4. Comparability –

4

assets, liabilities and that to equity as well. These elements are related to financial position.

Furthermore, income statement should have elements regarding revenue and expenses as well.

The financial reporting is required to be done in a way so that legal framework provided

by professional bodies are fulfilled in the most productive way (Naranjo, Saavedra and Verdi,

2017). Besides this, for having effective preparation of financial reporting it is required that

financial information is prepared effectually. The qualities and attributes of financial information

are as follows :

1. Relevance –

The relevance concept states that users of accounting information should record all

information in financial information, which provides help to make effective decisions. In simple

words, the information should be recorded only if it aids in decision making of users o financial

information. They can be external and internal stakeholders, which are directly involved with the

company. Thus, the same information must be recorded in such way, which enhances decision

making of stakeholders.

2. Materiality –

The principle states that only material information should be recorded in books of

accounts. This is because only material information affects decisions of users of accounting

information. Accountants are required to follow guidelines, which are imparted by professional

bodies in a way so that it may be relevant for them to make effective and better economic

decisions effectually. Accountants when preparing financial information should ignore non-

material information. This will provide effective information to them and as such, legal

framework will be adorned by it (Towery, 2017).

3. Understandability –

Users of accounting information quite easily should present the financial information in

effective way and that also in standard way, which may be easily understandable. Thus, financial

information should be stated and presented in simple form and terms so that users may assess it

easily and as such, decisions may be taken in effectual manner.

4. Comparability –

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The financial information must be easily comparable. The economic decisions is taken

with the help of information which is then compared by users within inter firm and intra firm.

Thus, it is essential that users of accounting information in the easiest way must present financial

information in a way that must be easily comparable. Thus, they may do interpretations in the

best possible manner.

5. Reliability –

It is required in such principle that reliable the company should present information.

Professional and legal regulatory bodies require this so that errors and mistakes related to

omissions may not be made by accounting professionals while doing accounting jobs (Durnev,

Li and Magnan, 2017). Thus, the company presents reliable information to users of financial

information quite effectively. Thus, this is required that organisation must be able to present

reliable information to users of accounting information.

Thus, financial reporting is required to be accomplish in a way, which is easily

recognised by users of accounting information and to professional bodies as well. This will

provide business effective and legal framework of accounting records and thus, financial

statements will be prepared with much ease. Thus, eventually financial reports will be prepared

with much ease having adequate information of financial performance of the company in

effectual way.

3. Discuss different types of stakeholders

1. Managers-

Managers are important part of the company and as such, they ensure proper control over

the operational activities of the business. The management is required to ensure that proper

accounting records may be maintained by the accounting professionals and as a result, true and

fair financial statements may be prepared and as such, financial reporting is provided to users of

such information (Chen and et.al, 2011).

2. Investors-

They are the people who invests in the company. These are essential for the organisation

as capital is provided by them. The financial information is quite useful for them as they are able

to take better and effective decisions regarding whether to invest in the company. As such,

5

with the help of information which is then compared by users within inter firm and intra firm.

Thus, it is essential that users of accounting information in the easiest way must present financial

information in a way that must be easily comparable. Thus, they may do interpretations in the

best possible manner.

5. Reliability –

It is required in such principle that reliable the company should present information.

Professional and legal regulatory bodies require this so that errors and mistakes related to

omissions may not be made by accounting professionals while doing accounting jobs (Durnev,

Li and Magnan, 2017). Thus, the company presents reliable information to users of financial

information quite effectively. Thus, this is required that organisation must be able to present

reliable information to users of accounting information.

Thus, financial reporting is required to be accomplish in a way, which is easily

recognised by users of accounting information and to professional bodies as well. This will

provide business effective and legal framework of accounting records and thus, financial

statements will be prepared with much ease. Thus, eventually financial reports will be prepared

with much ease having adequate information of financial performance of the company in

effectual way.

3. Discuss different types of stakeholders

1. Managers-

Managers are important part of the company and as such, they ensure proper control over

the operational activities of the business. The management is required to ensure that proper

accounting records may be maintained by the accounting professionals and as a result, true and

fair financial statements may be prepared and as such, financial reporting is provided to users of

such information (Chen and et.al, 2011).

2. Investors-

They are the people who invests in the company. These are essential for the organisation

as capital is provided by them. The financial information is quite useful for them as they are able

to take better and effective decisions regarding whether to invest in the company. As such,

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profitability position of organisation is ascertained by them. Profitability is judged by them in the

best possible way by seeking financial statements and decision is taken when adequate return can

be obtained.

3. Creditors-

The creditors are also benefited by financial information as they take decisions whether

to lend loan to company and as such, financial statements are much needed to ascertain financial

performance of the company (Costello, 2011). They ascertain liquidity position of the company

and comes to conclusion whether to provide funds to firm or not. As a result, financial

information is required by them so that loans are provided by company within stipulated time.

4. Value of financial reporting to company

The business is benefited by financial reporting as it helps them to pay taxes and other

liabilities with much ease. As such, it is important for business to produce accurate financial

reports to users of such information. The government scrutinises financial reports so that fair

taxes are paid by business in the most productive way. The financial report highlight financial

statements information which is then reviewed by government and taxation authorities.

Moreover, internal decisions are made by management of the company with much ease.

By going through, financial report management is able to highlight whether firm is making

profits or not. The strengths and weaknesses are also scrutinised by managers and as such, ways

to remove weaknesses are provided by them and as a result, financial report are useful for them.

By seeking financial reports, capital is analysed and company is able to seek how much money is

left out of after paying all expenditures and salaries to employees (McGuire, Omer and Sharp,

2011).

Furthermore, it is creates value to organisation regarding whether, it will be profitable

and efficient in future or not. As such, company is able to make out whether, sufficient capital to

meet requirements of various departments. This results in forecasting for future and is helpful for

the company. If company is planning to purchase stock, then financial reports help to make

decisions whether it should be purchased or plan should be dropped.

6

best possible way by seeking financial statements and decision is taken when adequate return can

be obtained.

3. Creditors-

The creditors are also benefited by financial information as they take decisions whether

to lend loan to company and as such, financial statements are much needed to ascertain financial

performance of the company (Costello, 2011). They ascertain liquidity position of the company

and comes to conclusion whether to provide funds to firm or not. As a result, financial

information is required by them so that loans are provided by company within stipulated time.

4. Value of financial reporting to company

The business is benefited by financial reporting as it helps them to pay taxes and other

liabilities with much ease. As such, it is important for business to produce accurate financial

reports to users of such information. The government scrutinises financial reports so that fair

taxes are paid by business in the most productive way. The financial report highlight financial

statements information which is then reviewed by government and taxation authorities.

Moreover, internal decisions are made by management of the company with much ease.

By going through, financial report management is able to highlight whether firm is making

profits or not. The strengths and weaknesses are also scrutinised by managers and as such, ways

to remove weaknesses are provided by them and as a result, financial report are useful for them.

By seeking financial reports, capital is analysed and company is able to seek how much money is

left out of after paying all expenditures and salaries to employees (McGuire, Omer and Sharp,

2011).

Furthermore, it is creates value to organisation regarding whether, it will be profitable

and efficient in future or not. As such, company is able to make out whether, sufficient capital to

meet requirements of various departments. This results in forecasting for future and is helpful for

the company. If company is planning to purchase stock, then financial reports help to make

decisions whether it should be purchased or plan should be dropped.

6

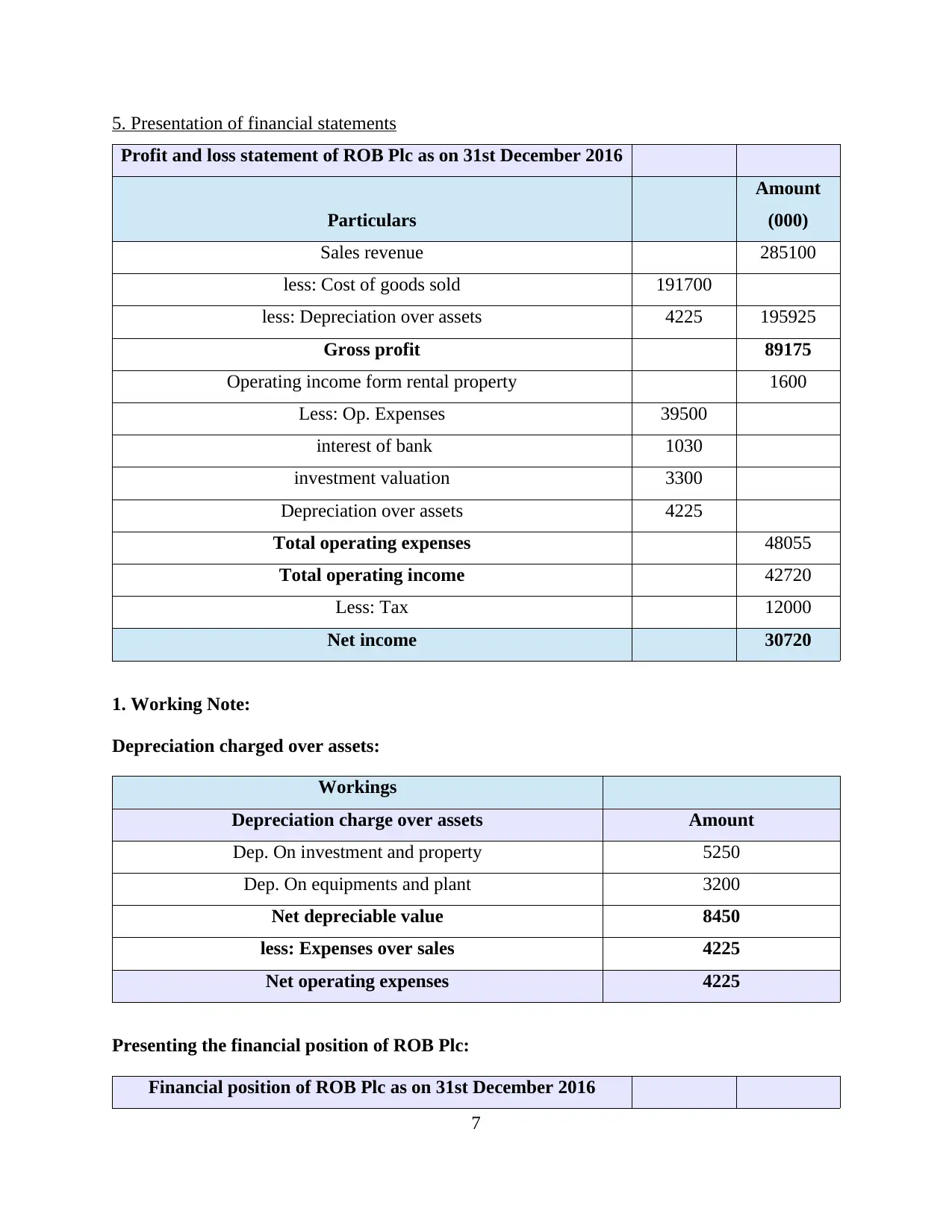

5. Presentation of financial statements

Profit and loss statement of ROB Plc as on 31st December 2016

Particulars

Amount

(000)

Sales revenue 285100

less: Cost of goods sold 191700

less: Depreciation over assets 4225 195925

Gross profit 89175

Operating income form rental property 1600

Less: Op. Expenses 39500

interest of bank 1030

investment valuation 3300

Depreciation over assets 4225

Total operating expenses 48055

Total operating income 42720

Less: Tax 12000

Net income 30720

1. Working Note:

Depreciation charged over assets:

Workings

Depreciation charge over assets Amount

Dep. On investment and property 5250

Dep. On equipments and plant 3200

Net depreciable value 8450

less: Expenses over sales 4225

Net operating expenses 4225

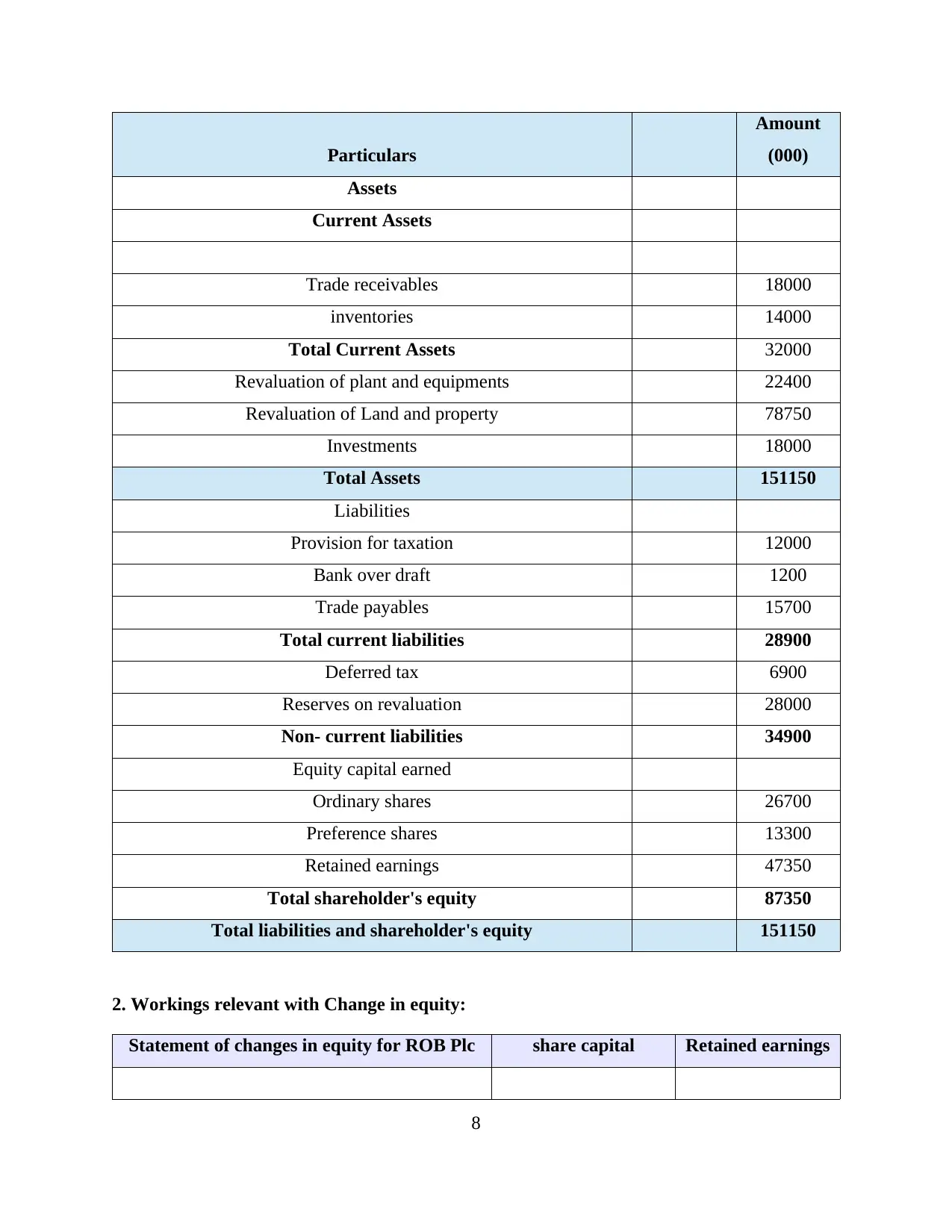

Presenting the financial position of ROB Plc:

Financial position of ROB Plc as on 31st December 2016

7

Profit and loss statement of ROB Plc as on 31st December 2016

Particulars

Amount

(000)

Sales revenue 285100

less: Cost of goods sold 191700

less: Depreciation over assets 4225 195925

Gross profit 89175

Operating income form rental property 1600

Less: Op. Expenses 39500

interest of bank 1030

investment valuation 3300

Depreciation over assets 4225

Total operating expenses 48055

Total operating income 42720

Less: Tax 12000

Net income 30720

1. Working Note:

Depreciation charged over assets:

Workings

Depreciation charge over assets Amount

Dep. On investment and property 5250

Dep. On equipments and plant 3200

Net depreciable value 8450

less: Expenses over sales 4225

Net operating expenses 4225

Presenting the financial position of ROB Plc:

Financial position of ROB Plc as on 31st December 2016

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Particulars

Amount

(000)

Assets

Current Assets

Trade receivables 18000

inventories 14000

Total Current Assets 32000

Revaluation of plant and equipments 22400

Revaluation of Land and property 78750

Investments 18000

Total Assets 151150

Liabilities

Provision for taxation 12000

Bank over draft 1200

Trade payables 15700

Total current liabilities 28900

Deferred tax 6900

Reserves on revaluation 28000

Non- current liabilities 34900

Equity capital earned

Ordinary shares 26700

Preference shares 13300

Retained earnings 47350

Total shareholder's equity 87350

Total liabilities and shareholder's equity 151150

2. Workings relevant with Change in equity:

Statement of changes in equity for ROB Plc share capital Retained earnings

8

Amount

(000)

Assets

Current Assets

Trade receivables 18000

inventories 14000

Total Current Assets 32000

Revaluation of plant and equipments 22400

Revaluation of Land and property 78750

Investments 18000

Total Assets 151150

Liabilities

Provision for taxation 12000

Bank over draft 1200

Trade payables 15700

Total current liabilities 28900

Deferred tax 6900

Reserves on revaluation 28000

Non- current liabilities 34900

Equity capital earned

Ordinary shares 26700

Preference shares 13300

Retained earnings 47350

Total shareholder's equity 87350

Total liabilities and shareholder's equity 151150

2. Workings relevant with Change in equity:

Statement of changes in equity for ROB Plc share capital Retained earnings

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

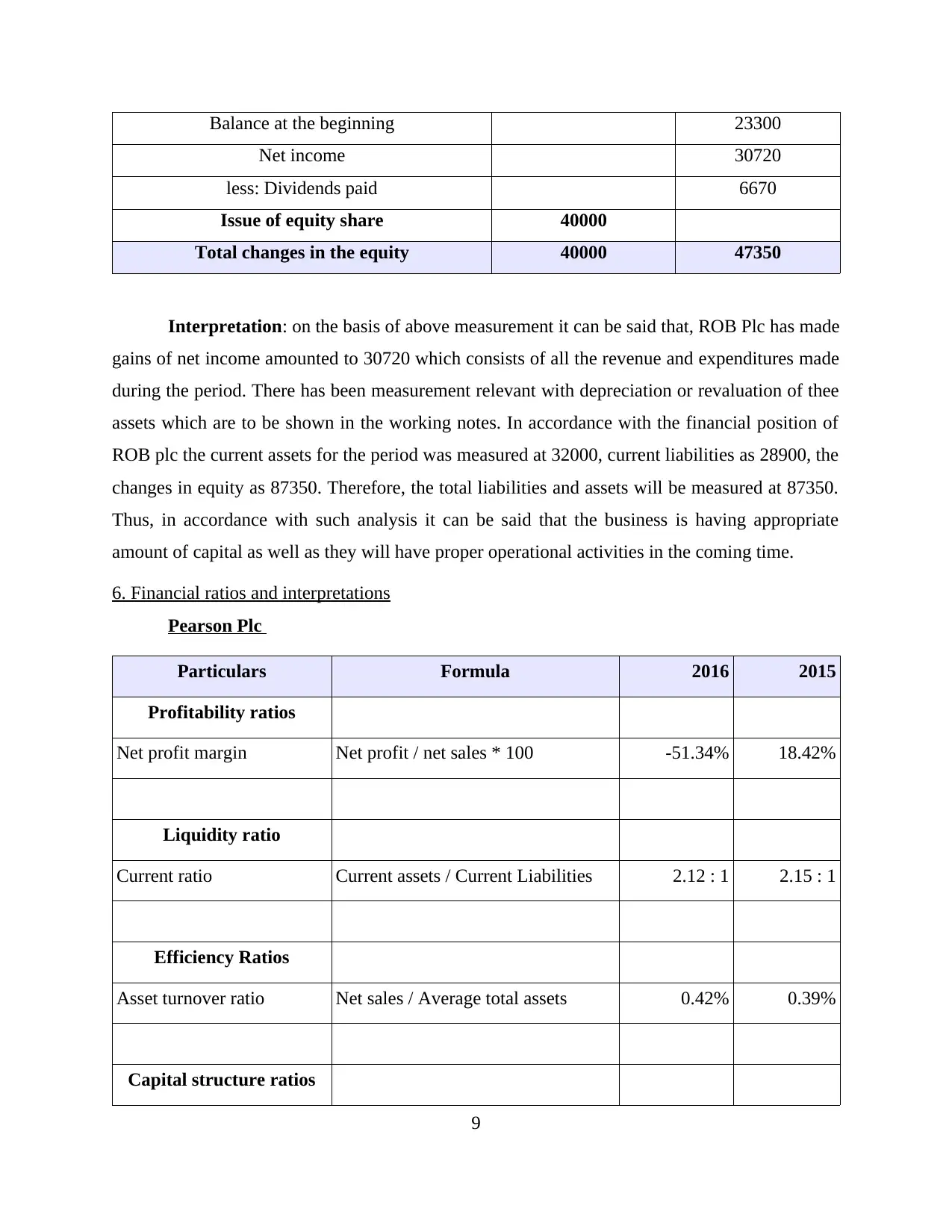

Balance at the beginning 23300

Net income 30720

less: Dividends paid 6670

Issue of equity share 40000

Total changes in the equity 40000 47350

Interpretation: on the basis of above measurement it can be said that, ROB Plc has made

gains of net income amounted to 30720 which consists of all the revenue and expenditures made

during the period. There has been measurement relevant with depreciation or revaluation of thee

assets which are to be shown in the working notes. In accordance with the financial position of

ROB plc the current assets for the period was measured at 32000, current liabilities as 28900, the

changes in equity as 87350. Therefore, the total liabilities and assets will be measured at 87350.

Thus, in accordance with such analysis it can be said that the business is having appropriate

amount of capital as well as they will have proper operational activities in the coming time.

6. Financial ratios and interpretations

Pearson Plc

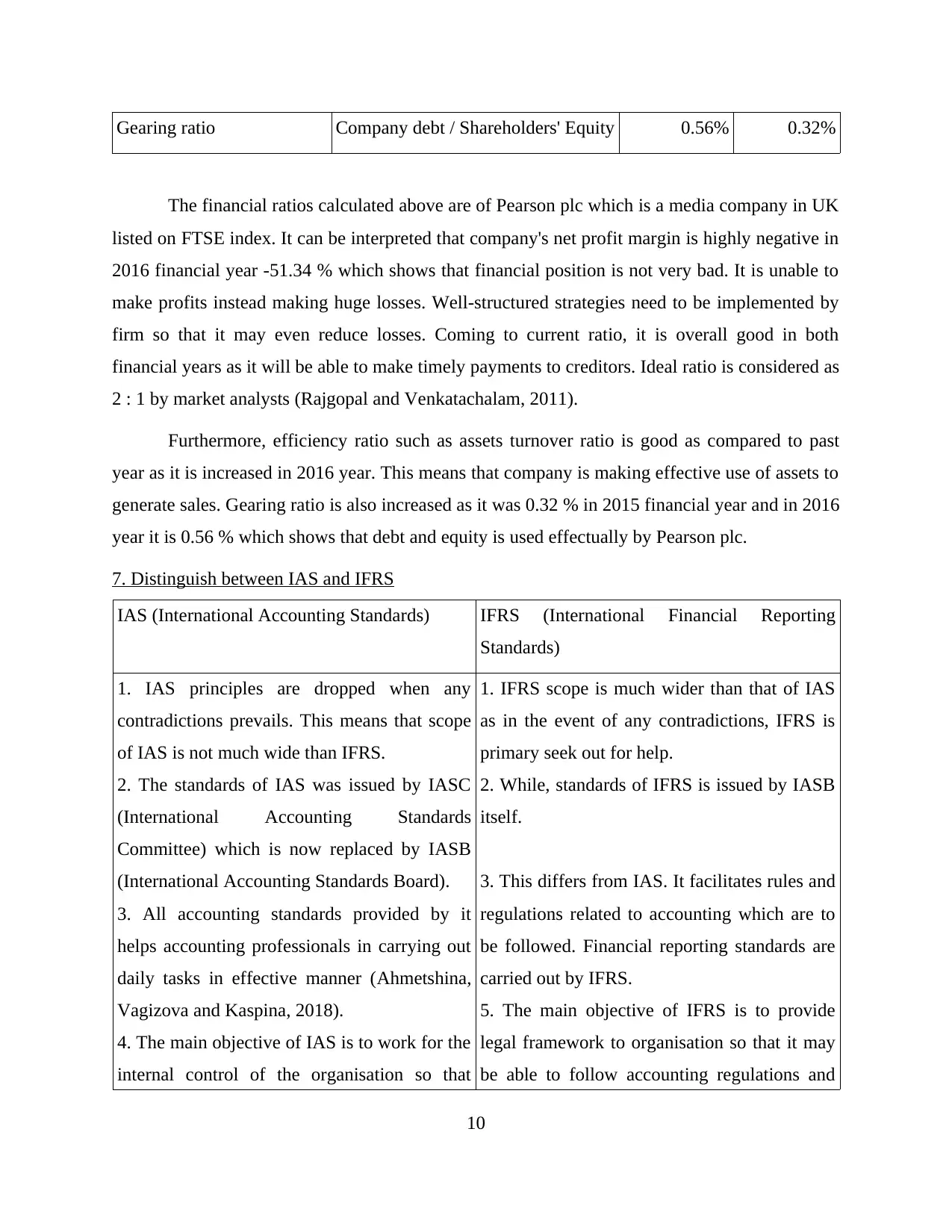

Particulars Formula 2016 2015

Profitability ratios

Net profit margin Net profit / net sales * 100 -51.34% 18.42%

Liquidity ratio

Current ratio Current assets / Current Liabilities 2.12 : 1 2.15 : 1

Efficiency Ratios

Asset turnover ratio Net sales / Average total assets 0.42% 0.39%

Capital structure ratios

9

Net income 30720

less: Dividends paid 6670

Issue of equity share 40000

Total changes in the equity 40000 47350

Interpretation: on the basis of above measurement it can be said that, ROB Plc has made

gains of net income amounted to 30720 which consists of all the revenue and expenditures made

during the period. There has been measurement relevant with depreciation or revaluation of thee

assets which are to be shown in the working notes. In accordance with the financial position of

ROB plc the current assets for the period was measured at 32000, current liabilities as 28900, the

changes in equity as 87350. Therefore, the total liabilities and assets will be measured at 87350.

Thus, in accordance with such analysis it can be said that the business is having appropriate

amount of capital as well as they will have proper operational activities in the coming time.

6. Financial ratios and interpretations

Pearson Plc

Particulars Formula 2016 2015

Profitability ratios

Net profit margin Net profit / net sales * 100 -51.34% 18.42%

Liquidity ratio

Current ratio Current assets / Current Liabilities 2.12 : 1 2.15 : 1

Efficiency Ratios

Asset turnover ratio Net sales / Average total assets 0.42% 0.39%

Capital structure ratios

9

Gearing ratio Company debt / Shareholders' Equity 0.56% 0.32%

The financial ratios calculated above are of Pearson plc which is a media company in UK

listed on FTSE index. It can be interpreted that company's net profit margin is highly negative in

2016 financial year -51.34 % which shows that financial position is not very bad. It is unable to

make profits instead making huge losses. Well-structured strategies need to be implemented by

firm so that it may even reduce losses. Coming to current ratio, it is overall good in both

financial years as it will be able to make timely payments to creditors. Ideal ratio is considered as

2 : 1 by market analysts (Rajgopal and Venkatachalam, 2011).

Furthermore, efficiency ratio such as assets turnover ratio is good as compared to past

year as it is increased in 2016 year. This means that company is making effective use of assets to

generate sales. Gearing ratio is also increased as it was 0.32 % in 2015 financial year and in 2016

year it is 0.56 % which shows that debt and equity is used effectually by Pearson plc.

7. Distinguish between IAS and IFRS

IAS (International Accounting Standards) IFRS (International Financial Reporting

Standards)

1. IAS principles are dropped when any

contradictions prevails. This means that scope

of IAS is not much wide than IFRS.

2. The standards of IAS was issued by IASC

(International Accounting Standards

Committee) which is now replaced by IASB

(International Accounting Standards Board).

3. All accounting standards provided by it

helps accounting professionals in carrying out

daily tasks in effective manner (Ahmetshina,

Vagizova and Kaspina, 2018).

4. The main objective of IAS is to work for the

internal control of the organisation so that

1. IFRS scope is much wider than that of IAS

as in the event of any contradictions, IFRS is

primary seek out for help.

2. While, standards of IFRS is issued by IASB

itself.

3. This differs from IAS. It facilitates rules and

regulations related to accounting which are to

be followed. Financial reporting standards are

carried out by IFRS.

5. The main objective of IFRS is to provide

legal framework to organisation so that it may

be able to follow accounting regulations and

10

The financial ratios calculated above are of Pearson plc which is a media company in UK

listed on FTSE index. It can be interpreted that company's net profit margin is highly negative in

2016 financial year -51.34 % which shows that financial position is not very bad. It is unable to

make profits instead making huge losses. Well-structured strategies need to be implemented by

firm so that it may even reduce losses. Coming to current ratio, it is overall good in both

financial years as it will be able to make timely payments to creditors. Ideal ratio is considered as

2 : 1 by market analysts (Rajgopal and Venkatachalam, 2011).

Furthermore, efficiency ratio such as assets turnover ratio is good as compared to past

year as it is increased in 2016 year. This means that company is making effective use of assets to

generate sales. Gearing ratio is also increased as it was 0.32 % in 2015 financial year and in 2016

year it is 0.56 % which shows that debt and equity is used effectually by Pearson plc.

7. Distinguish between IAS and IFRS

IAS (International Accounting Standards) IFRS (International Financial Reporting

Standards)

1. IAS principles are dropped when any

contradictions prevails. This means that scope

of IAS is not much wide than IFRS.

2. The standards of IAS was issued by IASC

(International Accounting Standards

Committee) which is now replaced by IASB

(International Accounting Standards Board).

3. All accounting standards provided by it

helps accounting professionals in carrying out

daily tasks in effective manner (Ahmetshina,

Vagizova and Kaspina, 2018).

4. The main objective of IAS is to work for the

internal control of the organisation so that

1. IFRS scope is much wider than that of IAS

as in the event of any contradictions, IFRS is

primary seek out for help.

2. While, standards of IFRS is issued by IASB

itself.

3. This differs from IAS. It facilitates rules and

regulations related to accounting which are to

be followed. Financial reporting standards are

carried out by IFRS.

5. The main objective of IFRS is to provide

legal framework to organisation so that it may

be able to follow accounting regulations and

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.