Financial Reporting System - Sample Assignment

VerifiedAdded on 2021/01/01

|18

|5522

|498

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Reporting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENT

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Context and purpose of financial accounting..........................................................................1

2. Requirement, purpose and key principles of regulatory and conceptual framework..............2

3. Main Stakeholders of an organisation and their benefits from financial information............4

4. Value of financial reporting for meeting organisational growth and objectives.....................5

5. Financial statements of the organisation.................................................................................6

A: Statement of profit and loss:..................................................................................................6

B: Statement of financial position:..............................................................................................7

6. Use of financial statements of a company to interpret and communicate financial

performance.................................................................................................................................8

7 Difference between IAS and IFRS...........................................................................................9

8 Evaluation of benefits of IFRS...............................................................................................10

9 Ascertaining the varying degree of compliance with IFRS...................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................13

INTRODUCTION...........................................................................................................................1

MAIN BODY...................................................................................................................................1

1. Context and purpose of financial accounting..........................................................................1

2. Requirement, purpose and key principles of regulatory and conceptual framework..............2

3. Main Stakeholders of an organisation and their benefits from financial information............4

4. Value of financial reporting for meeting organisational growth and objectives.....................5

5. Financial statements of the organisation.................................................................................6

A: Statement of profit and loss:..................................................................................................6

B: Statement of financial position:..............................................................................................7

6. Use of financial statements of a company to interpret and communicate financial

performance.................................................................................................................................8

7 Difference between IAS and IFRS...........................................................................................9

8 Evaluation of benefits of IFRS...............................................................................................10

9 Ascertaining the varying degree of compliance with IFRS...................................................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

APPENDIX....................................................................................................................................13

INTRODUCTION

Financial reporting is a technique which is required for every company to formulate its

financial statements like income statement, balance sheet and cash flow statements. All of them

may help internal as well as external stakeholders to analyse actual position, financial health and

evaluate performance of the organisation. The process of financial reporting guides the managers

and investors to make strategic and investment decisions (Al-Matari, 2013). They determine the

organisational performance and then managers make decisions to make improvements and

investors pass judgement to invest their money in the business or not. Shareholders evaluate

financial information that are recorded in the statements to analyse than their money is used

effectively or not. Company chosen for this report is Marks and Spencer which is based in UK.

The assignments aims at context and purpose of financial reporting, requirement, purpose and

key principles of conceptual and regulatory framework, main stakeholders of the company, value

of financial statements to attain organisational objectives and growth, preparation of financial

statements and comparison of two years statements, benefits of IFRS and difference between

IFRS and IAS.

MAIN BODY

1. Context and purpose of financial accounting

Financial reporting: It is the process of recording finance related business information

in financial statements so that stakeholders may analyse organisational performance and

financial strength. According to IASB organisations are required to formulate financial

statements to present actual status of the company in front of its shareholders. Appropriate and

transparent information may help the business entities to operate business effectively. It is very

important to follow all the accounting related principles, rules and regulations while recording

data in different statements so that it may help to depict actual position of the organisation. For

Marks and Spencer it is also very important to keep appropriate financial statements so that its

stakeholders may analyse it performance. Transparent records helps to achieve predetermined

organisational goals that are required to execute business. Marks and Spencer is preparing its

financial statements regularly that helps to operate business globally and to run all the activities

effectively. Purpose and importance of financial reporting is as follows:

Purpose of financial reporting:

1

Financial reporting is a technique which is required for every company to formulate its

financial statements like income statement, balance sheet and cash flow statements. All of them

may help internal as well as external stakeholders to analyse actual position, financial health and

evaluate performance of the organisation. The process of financial reporting guides the managers

and investors to make strategic and investment decisions (Al-Matari, 2013). They determine the

organisational performance and then managers make decisions to make improvements and

investors pass judgement to invest their money in the business or not. Shareholders evaluate

financial information that are recorded in the statements to analyse than their money is used

effectively or not. Company chosen for this report is Marks and Spencer which is based in UK.

The assignments aims at context and purpose of financial reporting, requirement, purpose and

key principles of conceptual and regulatory framework, main stakeholders of the company, value

of financial statements to attain organisational objectives and growth, preparation of financial

statements and comparison of two years statements, benefits of IFRS and difference between

IFRS and IAS.

MAIN BODY

1. Context and purpose of financial accounting

Financial reporting: It is the process of recording finance related business information

in financial statements so that stakeholders may analyse organisational performance and

financial strength. According to IASB organisations are required to formulate financial

statements to present actual status of the company in front of its shareholders. Appropriate and

transparent information may help the business entities to operate business effectively. It is very

important to follow all the accounting related principles, rules and regulations while recording

data in different statements so that it may help to depict actual position of the organisation. For

Marks and Spencer it is also very important to keep appropriate financial statements so that its

stakeholders may analyse it performance. Transparent records helps to achieve predetermined

organisational goals that are required to execute business. Marks and Spencer is preparing its

financial statements regularly that helps to operate business globally and to run all the activities

effectively. Purpose and importance of financial reporting is as follows:

Purpose of financial reporting:

1

Financial reporting is done by Marks and Spencer to facilitate mangers while forming

strategic decisions so that objectives can be achieved.

It helps to evaluate market value, financial status and health of the company so that

effective strategies can be formulated.

General purpose of financial reporting is to analyse the outcomes of those actions which

has been taken by the organisation in a particular period of time.

To provide results of the operations to the external stakeholders to increase sales, profits

and market share (Chae and Oh, 2016).

Help managers of the company to make effective planning for future period.

Importance of financial reporting:

Financial reporting is very important for the organisations to analyse the financial

performance.

For stakeholders financial reporting is very important as it may help them to analyse that

their money is effectively used or not.

While organisations are willing to raise foreign capital and investment than appropriate

financial reporting may help to attract international investors.

Properly managed financial statements are very important fro bidding, government

supplies and labour contracts because it provides overview of the company to external

parties.

It is very important to analyse actual performance and market position of the company.

2. Requirement, purpose and key principles of regulatory and conceptual framework

Regulatory and conceptual framework: Conceptual framework is a type of analytical

element with few variable quantity and textual matter. It is applied by organisations when an

overall performance and status of business is required. It is mainly used by companies to make

abstract differentiation and arrange business ideas. Regulatory framework is the set of legal rules

and regulations that are set by legal authorities of UK for all the companies who are executing

business activities there. According to the rules every company is required to conduct financial

reporting for their business because it is required to determine actual position and financial status

of the organisations. Marks and Spencer is following all the regulations that are set by IASB

because it may help the stakeholders to analyse organisational performance effectively. These

regulations are imposed in the form of IFRS which is explained below:

2

strategic decisions so that objectives can be achieved.

It helps to evaluate market value, financial status and health of the company so that

effective strategies can be formulated.

General purpose of financial reporting is to analyse the outcomes of those actions which

has been taken by the organisation in a particular period of time.

To provide results of the operations to the external stakeholders to increase sales, profits

and market share (Chae and Oh, 2016).

Help managers of the company to make effective planning for future period.

Importance of financial reporting:

Financial reporting is very important for the organisations to analyse the financial

performance.

For stakeholders financial reporting is very important as it may help them to analyse that

their money is effectively used or not.

While organisations are willing to raise foreign capital and investment than appropriate

financial reporting may help to attract international investors.

Properly managed financial statements are very important fro bidding, government

supplies and labour contracts because it provides overview of the company to external

parties.

It is very important to analyse actual performance and market position of the company.

2. Requirement, purpose and key principles of regulatory and conceptual framework

Regulatory and conceptual framework: Conceptual framework is a type of analytical

element with few variable quantity and textual matter. It is applied by organisations when an

overall performance and status of business is required. It is mainly used by companies to make

abstract differentiation and arrange business ideas. Regulatory framework is the set of legal rules

and regulations that are set by legal authorities of UK for all the companies who are executing

business activities there. According to the rules every company is required to conduct financial

reporting for their business because it is required to determine actual position and financial status

of the organisations. Marks and Spencer is following all the regulations that are set by IASB

because it may help the stakeholders to analyse organisational performance effectively. These

regulations are imposed in the form of IFRS which is explained below:

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

IFRS: It is International Financial Reporting Standards that are introduced by IASB

(International Accounting Standards Board). IFRS is the set of different principles that are set by

regulatory authority. Few IFRS are explained below that are also known as principles of

regulatory and conceptual framework:

IFRS 1: It is related to first time implementation of international financial reporting

standards in which companies adopt IFRS first time. It directs the organisations to

formulate all the financial statements effectively and appropriately.

IFRS 3: This is related to business combinations in which mergers and acquisitions are

described. It help organisations to combine all their assets and liabilities so that debts can

be paid to overcome from business crisis (Eker and Aytaç, 2016).

IFRS 9: It is related to financial instruments in which direction for their treatment is

provided. It mainly focuses on classification and measurement of financial instruments,

impairment of financial assets and hedge accounting.

IFRS 10: It directs business entities to form their financial statements in consolidated

format so that all the transactions of parent and subsidiary company may be recorded in a

single statement to determine performance of the entity.

Purpose of regulatory and conceptual frameworks:

Main purpose of regulatory framework is to guide organisations to prepare financial

statements in appropriate manner.

Purpose of conceptual frameworks is to analyse overall performance of a business entity

so that stakeholders may take effective decisions about the company.

Another purpose of regulatory and conceptual frameworks is to set a global language so

that businesses can be execute at international level with the help of international capitals

and investments.

Both are formulated by the government to understand accounting practices and standards

that are followed by companies while formulating final accounts.

Qualitative features of financial information: Following are the characteristics of

financial information that helps to make the information more reliable. It can be understood with

the help of following points:

Relevance: It is very important for the companies to record relevant data in the financial

statements so that it may help to analyse actual performance and financial status. If the

3

(International Accounting Standards Board). IFRS is the set of different principles that are set by

regulatory authority. Few IFRS are explained below that are also known as principles of

regulatory and conceptual framework:

IFRS 1: It is related to first time implementation of international financial reporting

standards in which companies adopt IFRS first time. It directs the organisations to

formulate all the financial statements effectively and appropriately.

IFRS 3: This is related to business combinations in which mergers and acquisitions are

described. It help organisations to combine all their assets and liabilities so that debts can

be paid to overcome from business crisis (Eker and Aytaç, 2016).

IFRS 9: It is related to financial instruments in which direction for their treatment is

provided. It mainly focuses on classification and measurement of financial instruments,

impairment of financial assets and hedge accounting.

IFRS 10: It directs business entities to form their financial statements in consolidated

format so that all the transactions of parent and subsidiary company may be recorded in a

single statement to determine performance of the entity.

Purpose of regulatory and conceptual frameworks:

Main purpose of regulatory framework is to guide organisations to prepare financial

statements in appropriate manner.

Purpose of conceptual frameworks is to analyse overall performance of a business entity

so that stakeholders may take effective decisions about the company.

Another purpose of regulatory and conceptual frameworks is to set a global language so

that businesses can be execute at international level with the help of international capitals

and investments.

Both are formulated by the government to understand accounting practices and standards

that are followed by companies while formulating final accounts.

Qualitative features of financial information: Following are the characteristics of

financial information that helps to make the information more reliable. It can be understood with

the help of following points:

Relevance: It is very important for the companies to record relevant data in the financial

statements so that it may help to analyse actual performance and financial status. If the

3

information is not relevant than it cannot show the accurate performance and position of a

business.

Faithful representation: This feature may help to gain trust of stakeholders like

investors and shareholders because this will help them to assure that organisation is in

good condition and they may get long term benefits like higher returns on their

investments.

All the rules and principles of regulatory and conceptual framework are followed by

Marks and Spencer in order to expand their business with the help of increased investments and

good market image.

3. Main Stakeholders of an organisation and their benefits from financial information

Stakeholders refers to the internal or external parties of an organisation who have right to

get actual financial information of an organisation. Marks and Spencer is also having various

stakeholders who help to operate business effectively. Financial statements are evaluated by

them to make decisions that may affect the business execution ability of an enterprise. Marks and

Spencer is having various stakeholders that are customers, investors, managers, government,

shareholders and creditors. Benefits of financial information to the internal and stakeholders are

described below:

Internal stakeholders: All of them are directly related to the operations of the company.

They analyse financial statements to make effective decisions:

Shareholders: Shareholders of the company are the persons who provide funds to the

organisation. In Marks and Spencer shareholders use financial information to analyse that

their money is effectively used or not by the organisation.

Managers: Managers of Marks and Spencer get benefited by financial information as it

help them to make decisions by evaluating the organisational performance. If business is

not in good condition than they may implement appropriate strategies so that business

may overcome all the challenges.

External stakeholders: They are not directly in touch of the company but they have

right to gather financial information because they are a part of the organisation.

Investors: These are the group of of persons who invest money in business for the

purpose of acquiring higher profits. Financial information help them to determine exact

4

business.

Faithful representation: This feature may help to gain trust of stakeholders like

investors and shareholders because this will help them to assure that organisation is in

good condition and they may get long term benefits like higher returns on their

investments.

All the rules and principles of regulatory and conceptual framework are followed by

Marks and Spencer in order to expand their business with the help of increased investments and

good market image.

3. Main Stakeholders of an organisation and their benefits from financial information

Stakeholders refers to the internal or external parties of an organisation who have right to

get actual financial information of an organisation. Marks and Spencer is also having various

stakeholders who help to operate business effectively. Financial statements are evaluated by

them to make decisions that may affect the business execution ability of an enterprise. Marks and

Spencer is having various stakeholders that are customers, investors, managers, government,

shareholders and creditors. Benefits of financial information to the internal and stakeholders are

described below:

Internal stakeholders: All of them are directly related to the operations of the company.

They analyse financial statements to make effective decisions:

Shareholders: Shareholders of the company are the persons who provide funds to the

organisation. In Marks and Spencer shareholders use financial information to analyse that

their money is effectively used or not by the organisation.

Managers: Managers of Marks and Spencer get benefited by financial information as it

help them to make decisions by evaluating the organisational performance. If business is

not in good condition than they may implement appropriate strategies so that business

may overcome all the challenges.

External stakeholders: They are not directly in touch of the company but they have

right to gather financial information because they are a part of the organisation.

Investors: These are the group of of persons who invest money in business for the

purpose of acquiring higher profits. Financial information help them to determine exact

4

position of Marks and Spencer to make investment or not because if the company is not

in good condition than investors does not show interest in that business.

Creditors: The persons who provide goods on credit to Marks and Spencer are creditors

or suppliers. Financial information of the company is very beneficial for them as it may

help them to analyse that organisation is able to pay back their amount or not which has

been provided by them (Duncan, 2014).

Government: All the financial information of Marks and Spencer is determined by legal

authorities of UK to insure that organisation is not performing any illegal activity. It also

help the government to assure that company is paying tax appropriately.

Customers: Financial information is also beneficial for the customers as they may get

satisfied by analysing that market image of Marks and Spencer is good.

All the stakeholder of the Marks and Spencer get benefited with the help of financial

information because it help them to analyse organisational performance and financial health.

4. Value of financial reporting for meeting organisational growth and objectives

Financial reporting help the organisations to achieve objectives and identify growth

opportunity. Marks and Spencer is operating it business all around the world and for the

company it is very important to formulate appropriate financial statements so that all the

stakeholders of the company get satisfied and show more interest in the company. Objectives of

Marks and Spencer are to attract investors, satisfy customers and maximise profits and sales. All

the goals can be achieved with the help of transparent information in financial statements of

Marks and Spencer. Investors get attracted toward those company who are performing good in

the market and able to provide them higher return on their investments. As Marks and Spencer is

keeping accurate records which will help investors to analyse its performance and than enhance

their interest in the company.

Customer satisfaction is possible with the help of positive market image which can be

determined by them with the help of financial statements that are generated by the company

every year. If Marks and Spencer is having good image in the market than this may help

customers to be satisfied because they will get assured that they are using products of a good

company.

Profits can also be maximised with the help of financial statements because if Marks and

Spencer is performing good in the market than it will help to be more competitive in the market

5

in good condition than investors does not show interest in that business.

Creditors: The persons who provide goods on credit to Marks and Spencer are creditors

or suppliers. Financial information of the company is very beneficial for them as it may

help them to analyse that organisation is able to pay back their amount or not which has

been provided by them (Duncan, 2014).

Government: All the financial information of Marks and Spencer is determined by legal

authorities of UK to insure that organisation is not performing any illegal activity. It also

help the government to assure that company is paying tax appropriately.

Customers: Financial information is also beneficial for the customers as they may get

satisfied by analysing that market image of Marks and Spencer is good.

All the stakeholder of the Marks and Spencer get benefited with the help of financial

information because it help them to analyse organisational performance and financial health.

4. Value of financial reporting for meeting organisational growth and objectives

Financial reporting help the organisations to achieve objectives and identify growth

opportunity. Marks and Spencer is operating it business all around the world and for the

company it is very important to formulate appropriate financial statements so that all the

stakeholders of the company get satisfied and show more interest in the company. Objectives of

Marks and Spencer are to attract investors, satisfy customers and maximise profits and sales. All

the goals can be achieved with the help of transparent information in financial statements of

Marks and Spencer. Investors get attracted toward those company who are performing good in

the market and able to provide them higher return on their investments. As Marks and Spencer is

keeping accurate records which will help investors to analyse its performance and than enhance

their interest in the company.

Customer satisfaction is possible with the help of positive market image which can be

determined by them with the help of financial statements that are generated by the company

every year. If Marks and Spencer is having good image in the market than this may help

customers to be satisfied because they will get assured that they are using products of a good

company.

Profits can also be maximised with the help of financial statements because if Marks and

Spencer is performing good in the market than it will help to be more competitive in the market

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and acquire higher profits (Elbayoumi and Awadallah, 2017). Effective and accurate financial

statements can help an organisation to identify growth opportunities and than grab them to be

more competitive in the market. Final accounts of Marks and Spencer help to analyse

organisational efficiency and profits. This will guide the managers to determine the funds that

are acquired by the organisation in a year and they may take decision to invest the money

effectively to increase production that may help to enhance sales.

Financial statements also help to identify the business position in the market which will

help to grow the business faster because having a good position in the market will attract large

number of customers and help to expand the business by acquiring higher market share.

Competitive advantage in the market can also be measured with the help of financial statements

which will help to be the first choice of the customers. This will help to achieve growth in the

market.

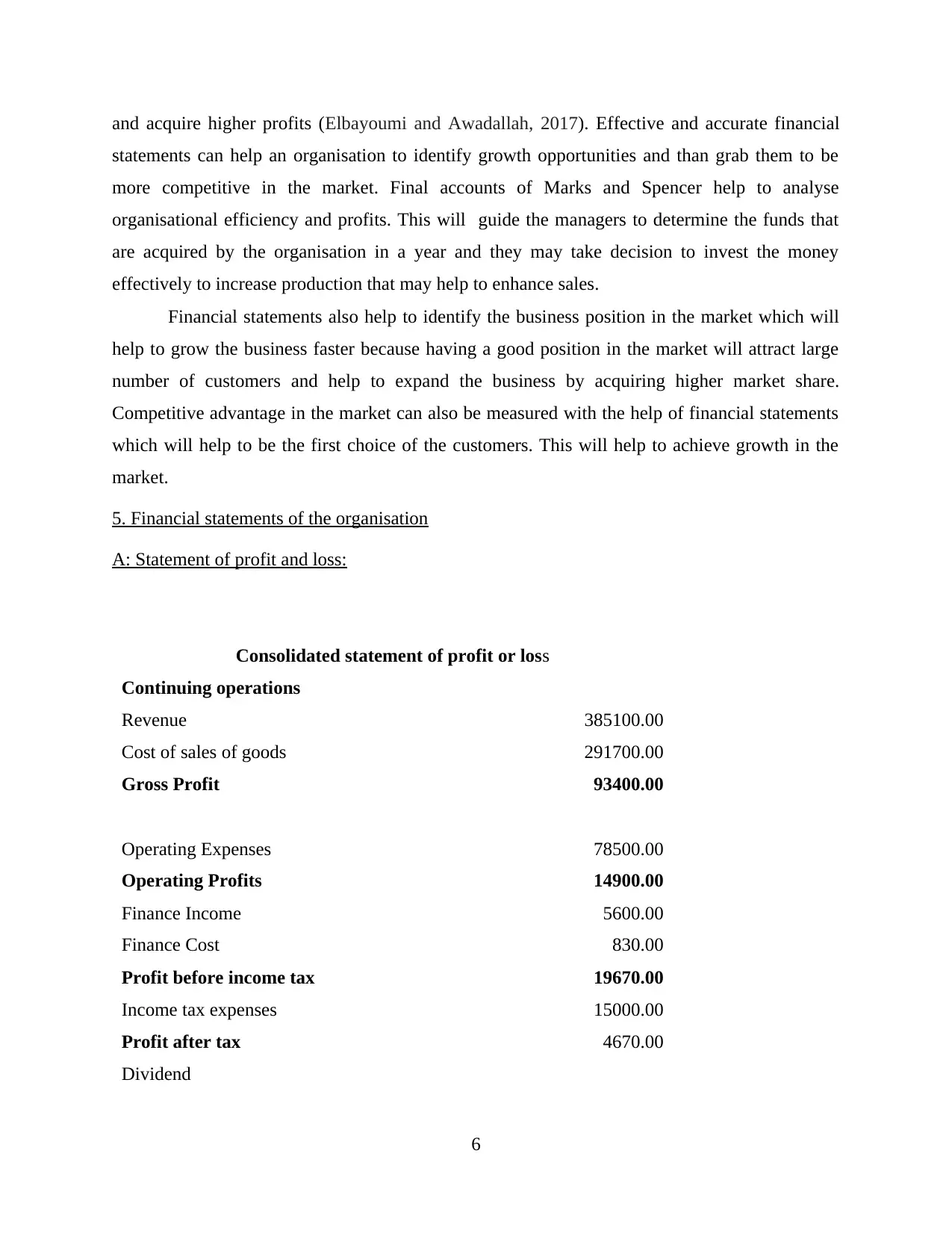

5. Financial statements of the organisation

A: Statement of profit and loss:

Consolidated statement of profit or loss

Continuing operations

Revenue 385100.00

Cost of sales of goods 291700.00

Gross Profit 93400.00

Operating Expenses 78500.00

Operating Profits 14900.00

Finance Income 5600.00

Finance Cost 830.00

Profit before income tax 19670.00

Income tax expenses 15000.00

Profit after tax 4670.00

Dividend

6

statements can help an organisation to identify growth opportunities and than grab them to be

more competitive in the market. Final accounts of Marks and Spencer help to analyse

organisational efficiency and profits. This will guide the managers to determine the funds that

are acquired by the organisation in a year and they may take decision to invest the money

effectively to increase production that may help to enhance sales.

Financial statements also help to identify the business position in the market which will

help to grow the business faster because having a good position in the market will attract large

number of customers and help to expand the business by acquiring higher market share.

Competitive advantage in the market can also be measured with the help of financial statements

which will help to be the first choice of the customers. This will help to achieve growth in the

market.

5. Financial statements of the organisation

A: Statement of profit and loss:

Consolidated statement of profit or loss

Continuing operations

Revenue 385100.00

Cost of sales of goods 291700.00

Gross Profit 93400.00

Operating Expenses 78500.00

Operating Profits 14900.00

Finance Income 5600.00

Finance Cost 830.00

Profit before income tax 19670.00

Income tax expenses 15000.00

Profit after tax 4670.00

Dividend

6

Equity 830.00

Preference 2330.00

Retained Earning 1510.00

Profit and loss account for company during a financial year help to ascertain the total

profit after making all adjustment such as tax expenses etc. The above mention P&L account for

the company shows gross profit of 93400, profit after deducting operating expenses is 14900,

profit before tax shows a balance of 19670 and profit after deducting tax amount 4670. There are

different adjustment to be made while calculating profit for the firm such as property, plant and

equipment balance, charges related to cost of good sold and expenses that are linked with

operating activity (Formisano, Fedele and Calabrese, 2018).

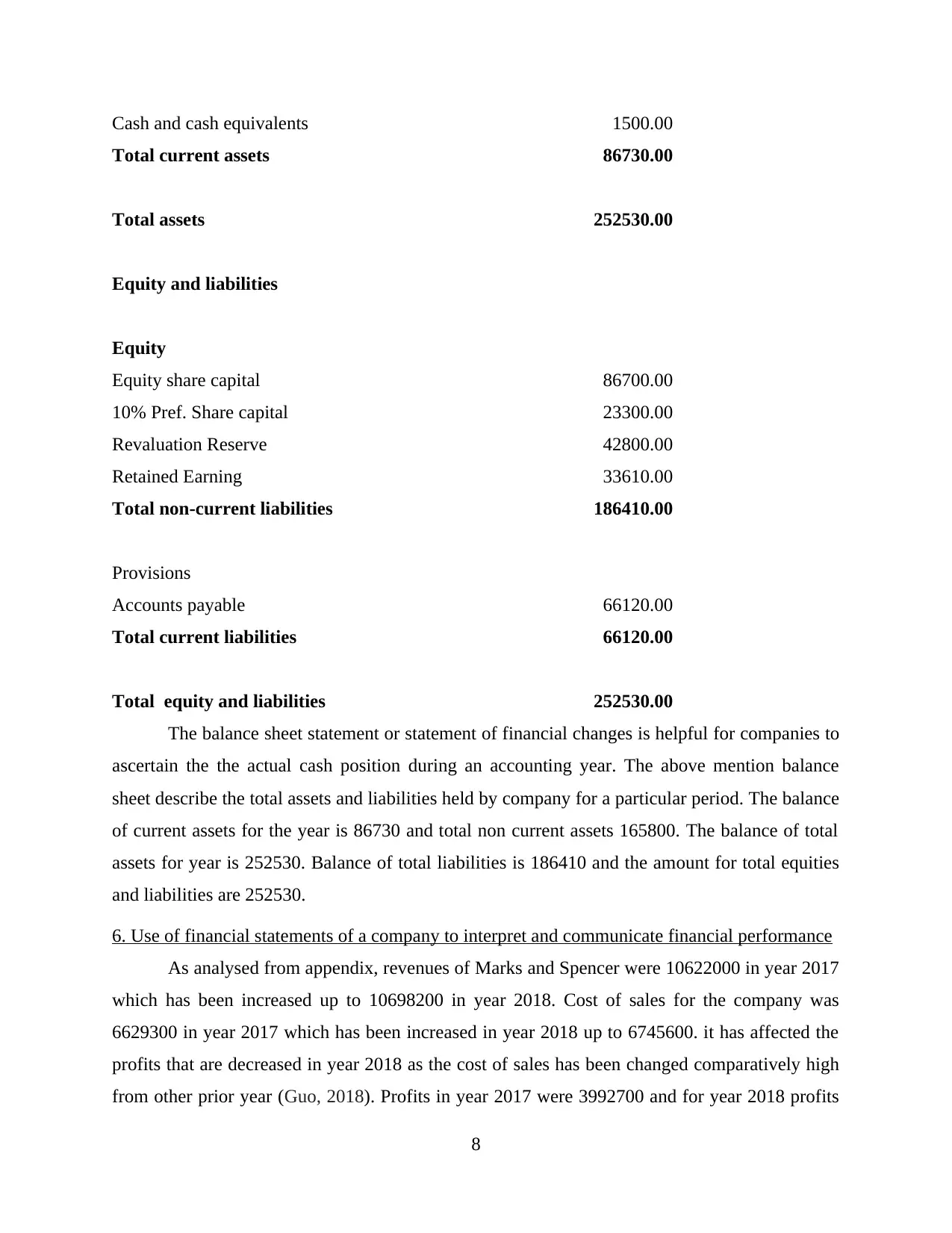

B: Statement of financial position:

Financial Statement

Assets

Land & Property 160700.00

Less:Depreciation -185100.00 -24400.00

Property 88000.00

Less:Depreciation -8000.00 80000.00

Investment property 23300.00

Plant & Equipment 78000.00

Deferred tax assets 8900.00

Other assets

Total non-current assets 165800.00

Inventories 17230.00

Accounts receivable 68000.00

Other assets

Short-term investments

7

Preference 2330.00

Retained Earning 1510.00

Profit and loss account for company during a financial year help to ascertain the total

profit after making all adjustment such as tax expenses etc. The above mention P&L account for

the company shows gross profit of 93400, profit after deducting operating expenses is 14900,

profit before tax shows a balance of 19670 and profit after deducting tax amount 4670. There are

different adjustment to be made while calculating profit for the firm such as property, plant and

equipment balance, charges related to cost of good sold and expenses that are linked with

operating activity (Formisano, Fedele and Calabrese, 2018).

B: Statement of financial position:

Financial Statement

Assets

Land & Property 160700.00

Less:Depreciation -185100.00 -24400.00

Property 88000.00

Less:Depreciation -8000.00 80000.00

Investment property 23300.00

Plant & Equipment 78000.00

Deferred tax assets 8900.00

Other assets

Total non-current assets 165800.00

Inventories 17230.00

Accounts receivable 68000.00

Other assets

Short-term investments

7

Cash and cash equivalents 1500.00

Total current assets 86730.00

Total assets 252530.00

Equity and liabilities

Equity

Equity share capital 86700.00

10% Pref. Share capital 23300.00

Revaluation Reserve 42800.00

Retained Earning 33610.00

Total non-current liabilities 186410.00

Provisions

Accounts payable 66120.00

Total current liabilities 66120.00

Total equity and liabilities 252530.00

The balance sheet statement or statement of financial changes is helpful for companies to

ascertain the the actual cash position during an accounting year. The above mention balance

sheet describe the total assets and liabilities held by company for a particular period. The balance

of current assets for the year is 86730 and total non current assets 165800. The balance of total

assets for year is 252530. Balance of total liabilities is 186410 and the amount for total equities

and liabilities are 252530.

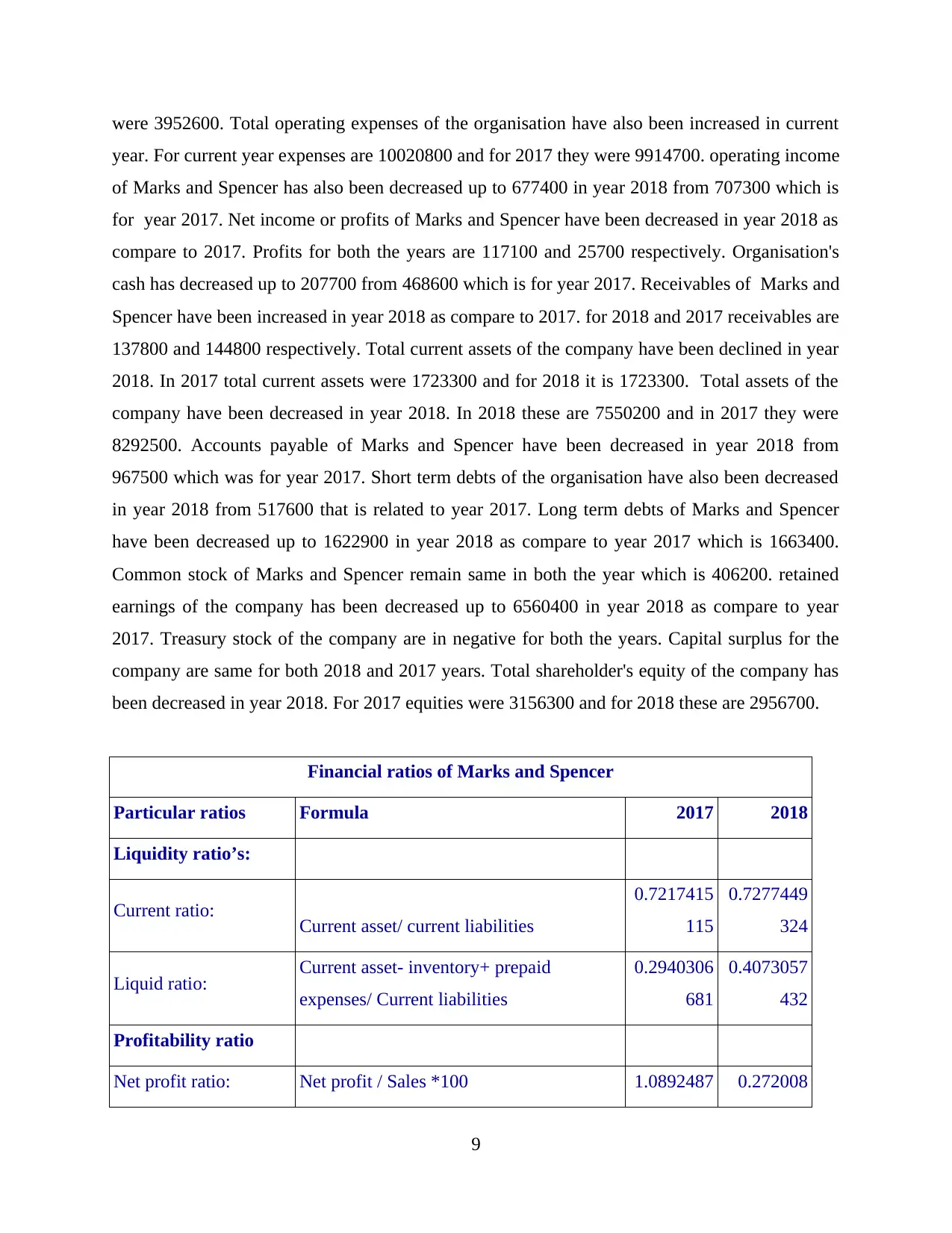

6. Use of financial statements of a company to interpret and communicate financial performance

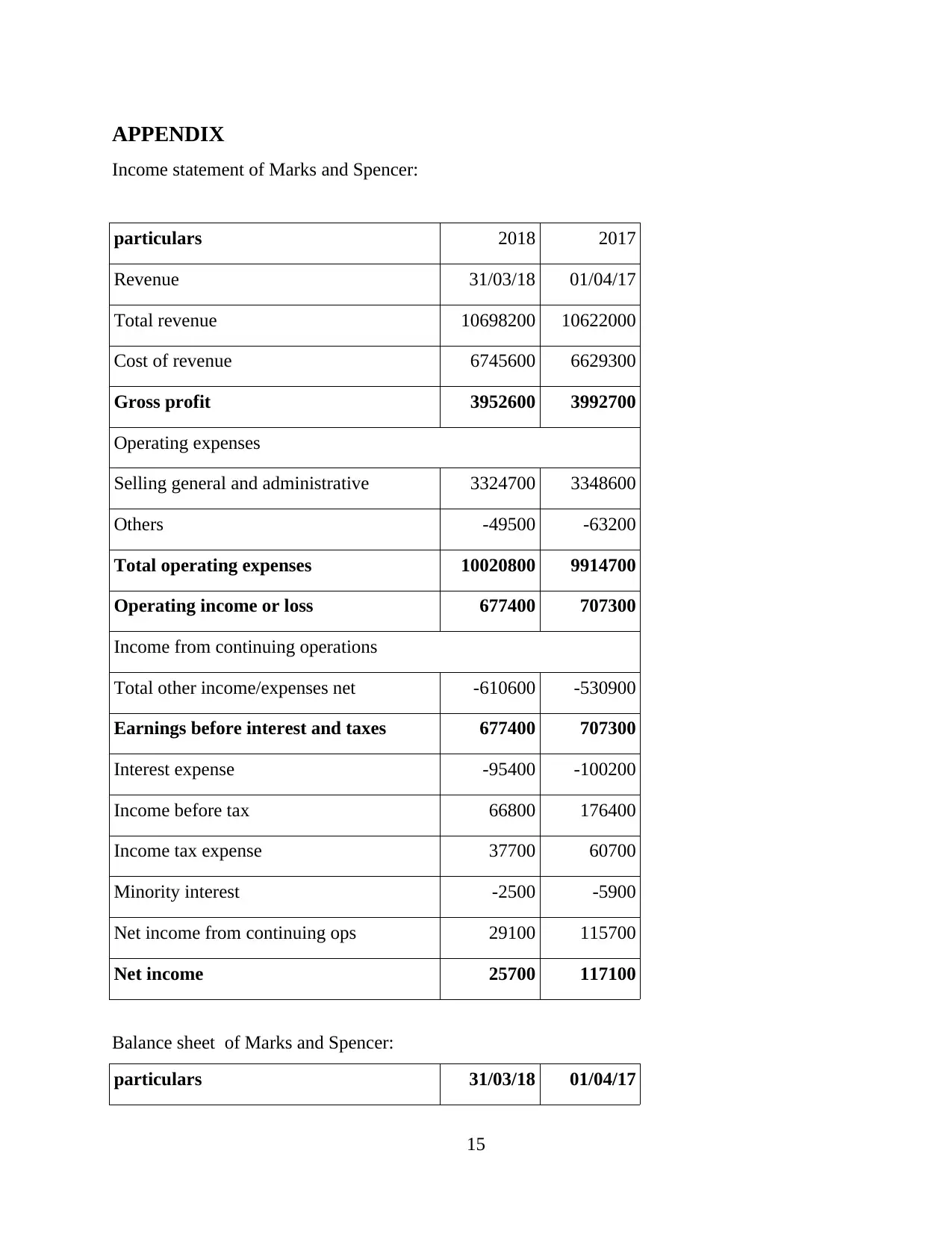

As analysed from appendix, revenues of Marks and Spencer were 10622000 in year 2017

which has been increased up to 10698200 in year 2018. Cost of sales for the company was

6629300 in year 2017 which has been increased in year 2018 up to 6745600. it has affected the

profits that are decreased in year 2018 as the cost of sales has been changed comparatively high

from other prior year (Guo, 2018). Profits in year 2017 were 3992700 and for year 2018 profits

8

Total current assets 86730.00

Total assets 252530.00

Equity and liabilities

Equity

Equity share capital 86700.00

10% Pref. Share capital 23300.00

Revaluation Reserve 42800.00

Retained Earning 33610.00

Total non-current liabilities 186410.00

Provisions

Accounts payable 66120.00

Total current liabilities 66120.00

Total equity and liabilities 252530.00

The balance sheet statement or statement of financial changes is helpful for companies to

ascertain the the actual cash position during an accounting year. The above mention balance

sheet describe the total assets and liabilities held by company for a particular period. The balance

of current assets for the year is 86730 and total non current assets 165800. The balance of total

assets for year is 252530. Balance of total liabilities is 186410 and the amount for total equities

and liabilities are 252530.

6. Use of financial statements of a company to interpret and communicate financial performance

As analysed from appendix, revenues of Marks and Spencer were 10622000 in year 2017

which has been increased up to 10698200 in year 2018. Cost of sales for the company was

6629300 in year 2017 which has been increased in year 2018 up to 6745600. it has affected the

profits that are decreased in year 2018 as the cost of sales has been changed comparatively high

from other prior year (Guo, 2018). Profits in year 2017 were 3992700 and for year 2018 profits

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

were 3952600. Total operating expenses of the organisation have also been increased in current

year. For current year expenses are 10020800 and for 2017 they were 9914700. operating income

of Marks and Spencer has also been decreased up to 677400 in year 2018 from 707300 which is

for year 2017. Net income or profits of Marks and Spencer have been decreased in year 2018 as

compare to 2017. Profits for both the years are 117100 and 25700 respectively. Organisation's

cash has decreased up to 207700 from 468600 which is for year 2017. Receivables of Marks and

Spencer have been increased in year 2018 as compare to 2017. for 2018 and 2017 receivables are

137800 and 144800 respectively. Total current assets of the company have been declined in year

2018. In 2017 total current assets were 1723300 and for 2018 it is 1723300. Total assets of the

company have been decreased in year 2018. In 2018 these are 7550200 and in 2017 they were

8292500. Accounts payable of Marks and Spencer have been decreased in year 2018 from

967500 which was for year 2017. Short term debts of the organisation have also been decreased

in year 2018 from 517600 that is related to year 2017. Long term debts of Marks and Spencer

have been decreased up to 1622900 in year 2018 as compare to year 2017 which is 1663400.

Common stock of Marks and Spencer remain same in both the year which is 406200. retained

earnings of the company has been decreased up to 6560400 in year 2018 as compare to year

2017. Treasury stock of the company are in negative for both the years. Capital surplus for the

company are same for both 2018 and 2017 years. Total shareholder's equity of the company has

been decreased in year 2018. For 2017 equities were 3156300 and for 2018 these are 2956700.

Financial ratios of Marks and Spencer

Particular ratios Formula 2017 2018

Liquidity ratio’s:

Current ratio: Current asset/ current liabilities

0.7217415

115

0.7277449

324

Liquid ratio: Current asset- inventory+ prepaid

expenses/ Current liabilities

0.2940306

681

0.4073057

432

Profitability ratio

Net profit ratio: Net profit / Sales *100 1.0892487 0.272008

9

year. For current year expenses are 10020800 and for 2017 they were 9914700. operating income

of Marks and Spencer has also been decreased up to 677400 in year 2018 from 707300 which is

for year 2017. Net income or profits of Marks and Spencer have been decreased in year 2018 as

compare to 2017. Profits for both the years are 117100 and 25700 respectively. Organisation's

cash has decreased up to 207700 from 468600 which is for year 2017. Receivables of Marks and

Spencer have been increased in year 2018 as compare to 2017. for 2018 and 2017 receivables are

137800 and 144800 respectively. Total current assets of the company have been declined in year

2018. In 2017 total current assets were 1723300 and for 2018 it is 1723300. Total assets of the

company have been decreased in year 2018. In 2018 these are 7550200 and in 2017 they were

8292500. Accounts payable of Marks and Spencer have been decreased in year 2018 from

967500 which was for year 2017. Short term debts of the organisation have also been decreased

in year 2018 from 517600 that is related to year 2017. Long term debts of Marks and Spencer

have been decreased up to 1622900 in year 2018 as compare to year 2017 which is 1663400.

Common stock of Marks and Spencer remain same in both the year which is 406200. retained

earnings of the company has been decreased up to 6560400 in year 2018 as compare to year

2017. Treasury stock of the company are in negative for both the years. Capital surplus for the

company are same for both 2018 and 2017 years. Total shareholder's equity of the company has

been decreased in year 2018. For 2017 equities were 3156300 and for 2018 these are 2956700.

Financial ratios of Marks and Spencer

Particular ratios Formula 2017 2018

Liquidity ratio’s:

Current ratio: Current asset/ current liabilities

0.7217415

115

0.7277449

324

Liquid ratio: Current asset- inventory+ prepaid

expenses/ Current liabilities

0.2940306

681

0.4073057

432

Profitability ratio

Net profit ratio: Net profit / Sales *100 1.0892487 0.272008

9

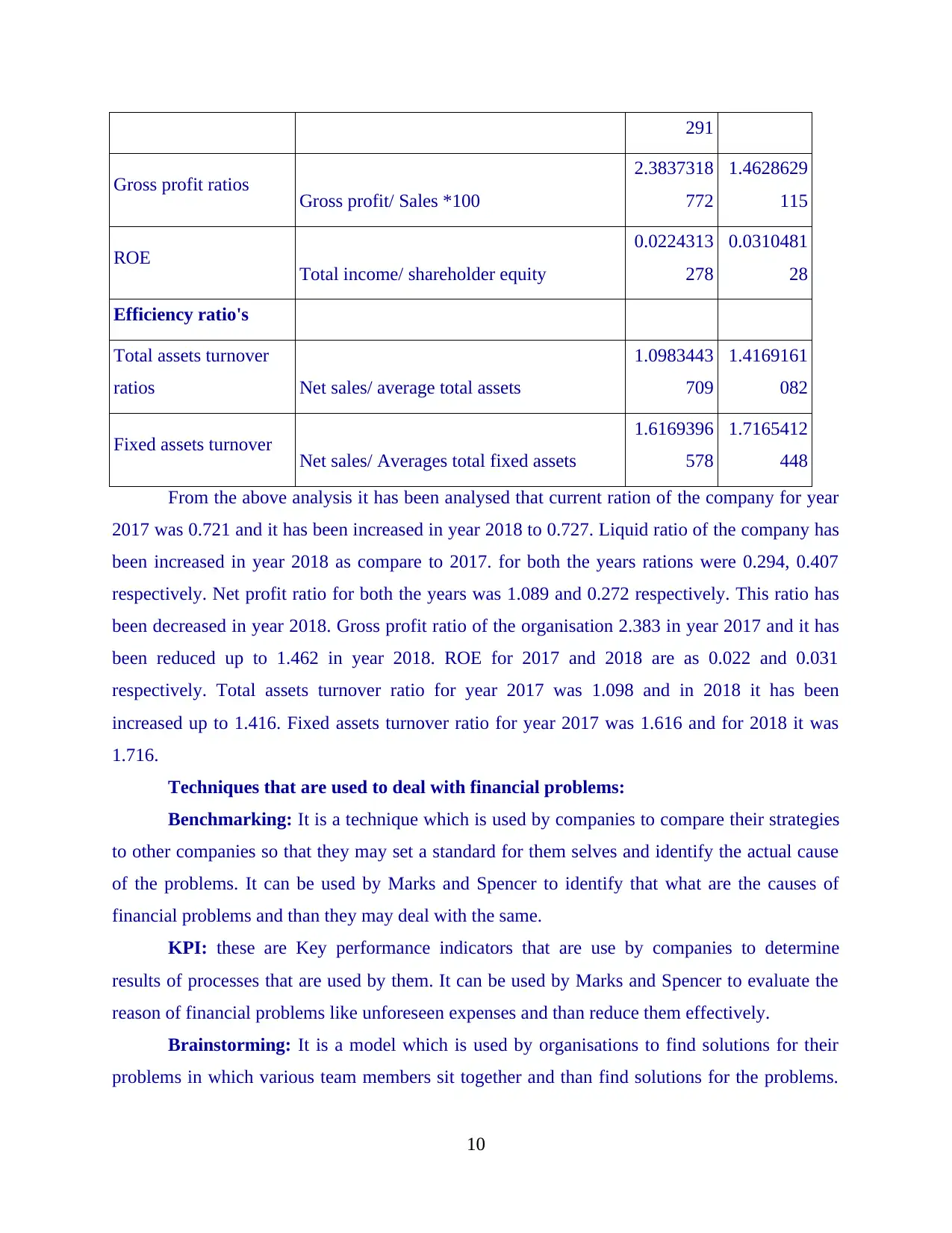

291

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.0983443

709

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets

1.6169396

578

1.7165412

448

From the above analysis it has been analysed that current ration of the company for year

2017 was 0.721 and it has been increased in year 2018 to 0.727. Liquid ratio of the company has

been increased in year 2018 as compare to 2017. for both the years rations were 0.294, 0.407

respectively. Net profit ratio for both the years was 1.089 and 0.272 respectively. This ratio has

been decreased in year 2018. Gross profit ratio of the organisation 2.383 in year 2017 and it has

been reduced up to 1.462 in year 2018. ROE for 2017 and 2018 are as 0.022 and 0.031

respectively. Total assets turnover ratio for year 2017 was 1.098 and in 2018 it has been

increased up to 1.416. Fixed assets turnover ratio for year 2017 was 1.616 and for 2018 it was

1.716.

Techniques that are used to deal with financial problems:

Benchmarking: It is a technique which is used by companies to compare their strategies

to other companies so that they may set a standard for them selves and identify the actual cause

of the problems. It can be used by Marks and Spencer to identify that what are the causes of

financial problems and than they may deal with the same.

KPI: these are Key performance indicators that are use by companies to determine

results of processes that are used by them. It can be used by Marks and Spencer to evaluate the

reason of financial problems like unforeseen expenses and than reduce them effectively.

Brainstorming: It is a model which is used by organisations to find solutions for their

problems in which various team members sit together and than find solutions for the problems.

10

Gross profit ratios Gross profit/ Sales *100

2.3837318

772

1.4628629

115

ROE Total income/ shareholder equity

0.0224313

278

0.0310481

28

Efficiency ratio's

Total assets turnover

ratios Net sales/ average total assets

1.0983443

709

1.4169161

082

Fixed assets turnover Net sales/ Averages total fixed assets

1.6169396

578

1.7165412

448

From the above analysis it has been analysed that current ration of the company for year

2017 was 0.721 and it has been increased in year 2018 to 0.727. Liquid ratio of the company has

been increased in year 2018 as compare to 2017. for both the years rations were 0.294, 0.407

respectively. Net profit ratio for both the years was 1.089 and 0.272 respectively. This ratio has

been decreased in year 2018. Gross profit ratio of the organisation 2.383 in year 2017 and it has

been reduced up to 1.462 in year 2018. ROE for 2017 and 2018 are as 0.022 and 0.031

respectively. Total assets turnover ratio for year 2017 was 1.098 and in 2018 it has been

increased up to 1.416. Fixed assets turnover ratio for year 2017 was 1.616 and for 2018 it was

1.716.

Techniques that are used to deal with financial problems:

Benchmarking: It is a technique which is used by companies to compare their strategies

to other companies so that they may set a standard for them selves and identify the actual cause

of the problems. It can be used by Marks and Spencer to identify that what are the causes of

financial problems and than they may deal with the same.

KPI: these are Key performance indicators that are use by companies to determine

results of processes that are used by them. It can be used by Marks and Spencer to evaluate the

reason of financial problems like unforeseen expenses and than reduce them effectively.

Brainstorming: It is a model which is used by organisations to find solutions for their

problems in which various team members sit together and than find solutions for the problems.

10

This technique can be used by managers of Marks and Spencer to resolve all the financial

problems by finding appropriate solutions for the problems.

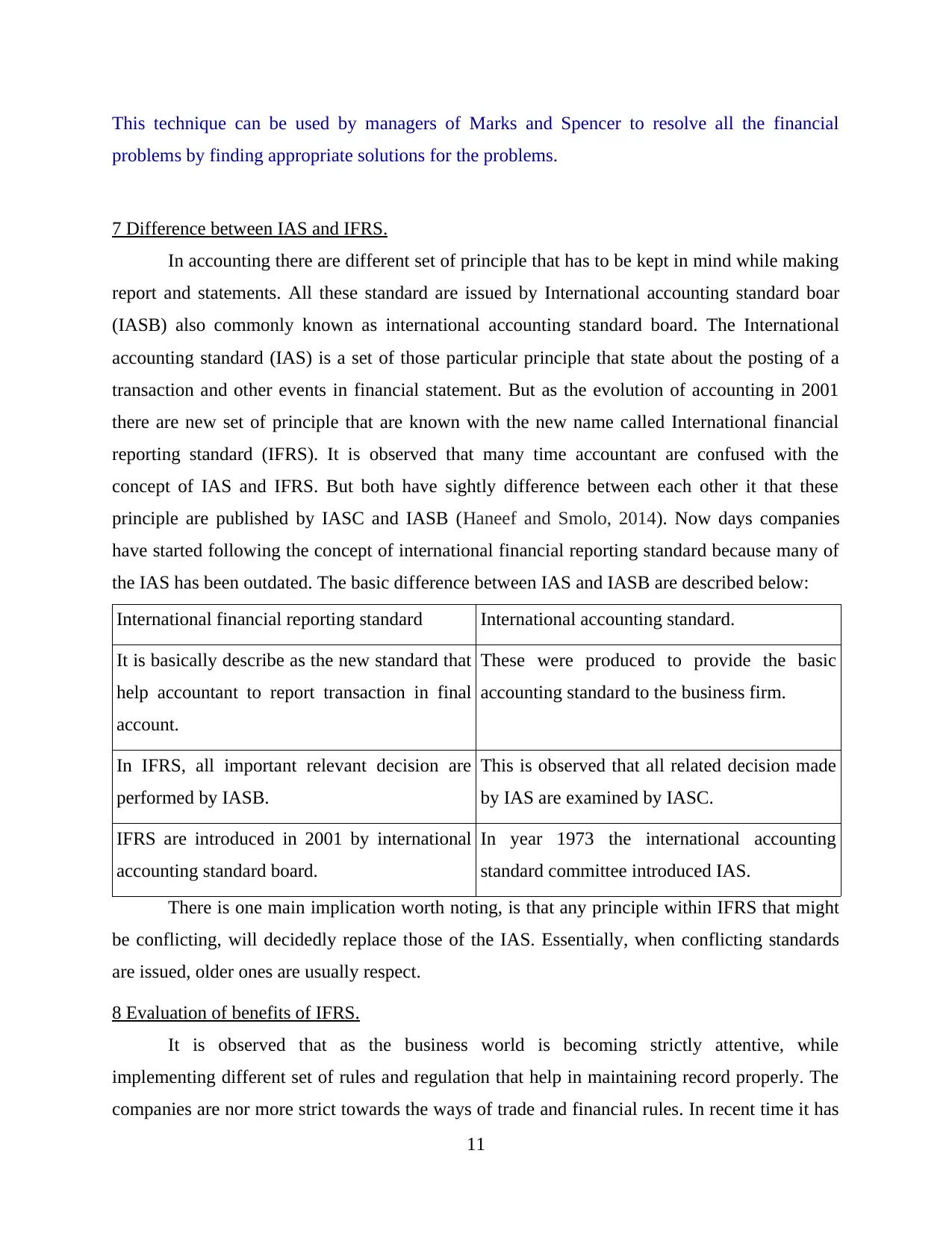

7 Difference between IAS and IFRS.

In accounting there are different set of principle that has to be kept in mind while making

report and statements. All these standard are issued by International accounting standard boar

(IASB) also commonly known as international accounting standard board. The International

accounting standard (IAS) is a set of those particular principle that state about the posting of a

transaction and other events in financial statement. But as the evolution of accounting in 2001

there are new set of principle that are known with the new name called International financial

reporting standard (IFRS). It is observed that many time accountant are confused with the

concept of IAS and IFRS. But both have sightly difference between each other it that these

principle are published by IASC and IASB (Haneef and Smolo, 2014). Now days companies

have started following the concept of international financial reporting standard because many of

the IAS has been outdated. The basic difference between IAS and IASB are described below:

International financial reporting standard International accounting standard.

It is basically describe as the new standard that

help accountant to report transaction in final

account.

These were produced to provide the basic

accounting standard to the business firm.

In IFRS, all important relevant decision are

performed by IASB.

This is observed that all related decision made

by IAS are examined by IASC.

IFRS are introduced in 2001 by international

accounting standard board.

In year 1973 the international accounting

standard committee introduced IAS.

There is one main implication worth noting, is that any principle within IFRS that might

be conflicting, will decidedly replace those of the IAS. Essentially, when conflicting standards

are issued, older ones are usually respect.

8 Evaluation of benefits of IFRS.

It is observed that as the business world is becoming strictly attentive, while

implementing different set of rules and regulation that help in maintaining record properly. The

companies are nor more strict towards the ways of trade and financial rules. In recent time it has

11

problems by finding appropriate solutions for the problems.

7 Difference between IAS and IFRS.

In accounting there are different set of principle that has to be kept in mind while making

report and statements. All these standard are issued by International accounting standard boar

(IASB) also commonly known as international accounting standard board. The International

accounting standard (IAS) is a set of those particular principle that state about the posting of a

transaction and other events in financial statement. But as the evolution of accounting in 2001

there are new set of principle that are known with the new name called International financial

reporting standard (IFRS). It is observed that many time accountant are confused with the

concept of IAS and IFRS. But both have sightly difference between each other it that these

principle are published by IASC and IASB (Haneef and Smolo, 2014). Now days companies

have started following the concept of international financial reporting standard because many of

the IAS has been outdated. The basic difference between IAS and IASB are described below:

International financial reporting standard International accounting standard.

It is basically describe as the new standard that

help accountant to report transaction in final

account.

These were produced to provide the basic

accounting standard to the business firm.

In IFRS, all important relevant decision are

performed by IASB.

This is observed that all related decision made

by IAS are examined by IASC.

IFRS are introduced in 2001 by international

accounting standard board.

In year 1973 the international accounting

standard committee introduced IAS.

There is one main implication worth noting, is that any principle within IFRS that might

be conflicting, will decidedly replace those of the IAS. Essentially, when conflicting standards

are issued, older ones are usually respect.

8 Evaluation of benefits of IFRS.

It is observed that as the business world is becoming strictly attentive, while

implementing different set of rules and regulation that help in maintaining record properly. The

companies are nor more strict towards the ways of trade and financial rules. In recent time it has

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

been noticed that many companies in almost every part of world have moved to the generally

accepted accounting standard principle (GAAP) towards the international financial reporting

standard (IFRS) (Hassaan, 2012). In which it is clearly mentioned that any relevant information

about the business happing must be revealed in financial statement and it also explain the process

of how to post transaction in report and statement. With the help these standard the companies

are able to solve many accounting problems that may led to the decrease in the profitability

level. The implementation of IFRS makes company financial statements clear and transparent

that makes shareholder and investor to know more about the company financial position. In case

if government founds any company not following the appropriate standard, they will be not

allowed to execute their business in future. There are basically some advantages of IFRS that are

explained below:

With the help and use of suitable accounting standard support companies to grow and

develop their operation that result in development of economy.

As companies uses the international accounting standard in their accounting system, that

makes the report and statement clear and transparent. This result in attracting more

number of investor from and outside the nation.

Companies using suitable IFRS provide shareholder the better understanding about the

business growth. It also help investor to make right investment that will have better

result.

The main advantage of using IFRS is that it help in increasing the fund from the foreign

market at very cheap rate.

By using IFRS standard in making report, internal manager ease the work of accountant

to analyse the statement and give their best opinion.

IFRS have a main advantage of developing the global language that help to develop the

understanding with investors from any part of world.

9 Ascertaining the varying degree of compliance with IFRS

In recent international financial reporting standard are becoming the world wide standard

of accounting that is accepted in almost every nation that guide public or private complainers

internal management to prepare and present financial statements. Recently there are thirteen

IFRS and 29 IASs that are followed by almost every company at global level. IFRS are types of

rule that arr to be followed by each kind of organisation whether they are large and small in size.

12

accepted accounting standard principle (GAAP) towards the international financial reporting

standard (IFRS) (Hassaan, 2012). In which it is clearly mentioned that any relevant information

about the business happing must be revealed in financial statement and it also explain the process

of how to post transaction in report and statement. With the help these standard the companies

are able to solve many accounting problems that may led to the decrease in the profitability

level. The implementation of IFRS makes company financial statements clear and transparent

that makes shareholder and investor to know more about the company financial position. In case

if government founds any company not following the appropriate standard, they will be not

allowed to execute their business in future. There are basically some advantages of IFRS that are

explained below:

With the help and use of suitable accounting standard support companies to grow and

develop their operation that result in development of economy.

As companies uses the international accounting standard in their accounting system, that

makes the report and statement clear and transparent. This result in attracting more

number of investor from and outside the nation.

Companies using suitable IFRS provide shareholder the better understanding about the

business growth. It also help investor to make right investment that will have better

result.

The main advantage of using IFRS is that it help in increasing the fund from the foreign

market at very cheap rate.

By using IFRS standard in making report, internal manager ease the work of accountant

to analyse the statement and give their best opinion.

IFRS have a main advantage of developing the global language that help to develop the

understanding with investors from any part of world.

9 Ascertaining the varying degree of compliance with IFRS

In recent international financial reporting standard are becoming the world wide standard

of accounting that is accepted in almost every nation that guide public or private complainers

internal management to prepare and present financial statements. Recently there are thirteen

IFRS and 29 IASs that are followed by almost every company at global level. IFRS are types of

rule that arr to be followed by each kind of organisation whether they are large and small in size.

12

It is observed that mark and Spencer has adapted the standard of IFRS that help in formation of

statement which are further helpful for stakeholder to make effective decision of investment. The

standard support companies and the principle of the disclosure target entities infract of clearly

setting the minimum compliance level. In general, compliance is the basic word that is related to

the. It has been evaluated that recently IFRS standard are set according to the disclosure of the

compliance in the context of both specific disclosure needs and the increasing level of principle

of disclosure (Nakashima and Okuda, 2016).

For example, in almost every country there are accounting rule to be followed by

companies that are slightly in some manner. This help them in formation of statement and

overcome different types of problems and issues. All standard may affect the capitalist decision

of investing as they may not be able to examine the financial statements of the company. In UK

government have implemented various accounting regulation for companies that guide Mark &

Spenser to prepare statement for an accounting year. The company is operating their business in

different part of world so it is not possible for their management to applies all kind of accounting

role. Therefore, it is importance for company to applies the international financial reporting

standard that help in maintaining the information properly. This result in attaining the

competitive advantage at world wide level (Zhao, 2017).

CONCLUSION

From the above project report it has been concluded that financial reporting is the process

of preparing financial statements that are required to analyse organisational performance and

financial status. It is very important for the companies to maintain their financial statements on

regular basis so that stakeholders such as customers, investors, shareholders, government and

managers can formulate their decisions according to financial health of the business. All the

business entities are directed by IFRS while they are generating their financial statements as it

may help them to formulate appropriate and accurate statements.

13

statement which are further helpful for stakeholder to make effective decision of investment. The

standard support companies and the principle of the disclosure target entities infract of clearly

setting the minimum compliance level. In general, compliance is the basic word that is related to

the. It has been evaluated that recently IFRS standard are set according to the disclosure of the

compliance in the context of both specific disclosure needs and the increasing level of principle

of disclosure (Nakashima and Okuda, 2016).

For example, in almost every country there are accounting rule to be followed by

companies that are slightly in some manner. This help them in formation of statement and

overcome different types of problems and issues. All standard may affect the capitalist decision

of investing as they may not be able to examine the financial statements of the company. In UK

government have implemented various accounting regulation for companies that guide Mark &

Spenser to prepare statement for an accounting year. The company is operating their business in

different part of world so it is not possible for their management to applies all kind of accounting

role. Therefore, it is importance for company to applies the international financial reporting

standard that help in maintaining the information properly. This result in attaining the

competitive advantage at world wide level (Zhao, 2017).

CONCLUSION

From the above project report it has been concluded that financial reporting is the process

of preparing financial statements that are required to analyse organisational performance and

financial status. It is very important for the companies to maintain their financial statements on

regular basis so that stakeholders such as customers, investors, shareholders, government and

managers can formulate their decisions according to financial health of the business. All the

business entities are directed by IFRS while they are generating their financial statements as it

may help them to formulate appropriate and accurate statements.

13

REFERENCES

Books and Journals:

Al-Matari, Y. A. A. T., 2013. Board of Directors, Audit Committee Characteristics and The

Performance of Public Listed Companies in Saudi Arabia (Doctoral dissertation,

Universiti Utara Malaysia).

Chae, S. J. and Oh, K., 2016. The Effect Of Family Firm On The Credit Rating: Evidence From

Republic Of Korea. Journal of Applied Business Research. 32(6). p.1575.

Duncan, K., 2014. Relationship between the audit function and effective governance.

Eker, M. and Aytaç, A., 2016. Effects of interaction between ERP and advanced managerial

accounting techniques on firm performance: Evidence From Turkey. Muhasebe ve

Finansman Dergisi. (72), pp.187-210.

Elbayoumi, A. F. and Awadallah, E. A., 2017. The Usefulness of Different Accounting Earnings

Measures: The Case of Egypt. GSTF Journal on Business Review (GBR). 2(2).

Formisano, V., Fedele, M. and Calabrese, M., 2018. The strategic priorities in the materiality

matrix of the banking enterprise. The TQM Journal.

Guo, N., 2018. Revisiting Corporate Financial Policy and the Value of Cash.

Haneef, R. and Smolo, E., 2014. Reshaping the Islamic finance industry: Applying the lessons

learned from the global financail crisis. Islamic Banking and Financial Crisis

Reputation Stability and Risks, pp.21-39.

Hassaan, M., 2012. Corporate governance and compliance with International Financial

Reporting Standards (IFRSs): evidence from two MENA stock exchanges (Doctoral

dissertation, Aston University).

Nakashima, M. and Okuda, S. Y., 2016. Implication of Internal Controls System and Accounting

Information System.

Zhao, S., 2017. Does Financial Development Necessarily Lead to Economic Growth? Evidence

from China’s Cities, 2007–2014. In MATEC Web of Conferences (Vol. 100, p. 05032).

EDP Sciences.

Online

IFRS. 2018. [Online] Available through:

<https://www.ifrs.com/>

14

Books and Journals:

Al-Matari, Y. A. A. T., 2013. Board of Directors, Audit Committee Characteristics and The

Performance of Public Listed Companies in Saudi Arabia (Doctoral dissertation,

Universiti Utara Malaysia).

Chae, S. J. and Oh, K., 2016. The Effect Of Family Firm On The Credit Rating: Evidence From

Republic Of Korea. Journal of Applied Business Research. 32(6). p.1575.

Duncan, K., 2014. Relationship between the audit function and effective governance.

Eker, M. and Aytaç, A., 2016. Effects of interaction between ERP and advanced managerial

accounting techniques on firm performance: Evidence From Turkey. Muhasebe ve

Finansman Dergisi. (72), pp.187-210.

Elbayoumi, A. F. and Awadallah, E. A., 2017. The Usefulness of Different Accounting Earnings

Measures: The Case of Egypt. GSTF Journal on Business Review (GBR). 2(2).

Formisano, V., Fedele, M. and Calabrese, M., 2018. The strategic priorities in the materiality

matrix of the banking enterprise. The TQM Journal.

Guo, N., 2018. Revisiting Corporate Financial Policy and the Value of Cash.

Haneef, R. and Smolo, E., 2014. Reshaping the Islamic finance industry: Applying the lessons

learned from the global financail crisis. Islamic Banking and Financial Crisis

Reputation Stability and Risks, pp.21-39.

Hassaan, M., 2012. Corporate governance and compliance with International Financial

Reporting Standards (IFRSs): evidence from two MENA stock exchanges (Doctoral

dissertation, Aston University).

Nakashima, M. and Okuda, S. Y., 2016. Implication of Internal Controls System and Accounting

Information System.

Zhao, S., 2017. Does Financial Development Necessarily Lead to Economic Growth? Evidence

from China’s Cities, 2007–2014. In MATEC Web of Conferences (Vol. 100, p. 05032).

EDP Sciences.

Online

IFRS. 2018. [Online] Available through:

<https://www.ifrs.com/>

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

APPENDIX

Income statement of Marks and Spencer:

particulars 2018 2017

Revenue 31/03/18 01/04/17

Total revenue 10698200 10622000

Cost of revenue 6745600 6629300

Gross profit 3952600 3992700

Operating expenses

Selling general and administrative 3324700 3348600

Others -49500 -63200

Total operating expenses 10020800 9914700

Operating income or loss 677400 707300

Income from continuing operations

Total other income/expenses net -610600 -530900

Earnings before interest and taxes 677400 707300

Interest expense -95400 -100200

Income before tax 66800 176400

Income tax expense 37700 60700

Minority interest -2500 -5900

Net income from continuing ops 29100 115700

Net income 25700 117100

Balance sheet of Marks and Spencer:

particulars 31/03/18 01/04/17

15

Income statement of Marks and Spencer:

particulars 2018 2017

Revenue 31/03/18 01/04/17

Total revenue 10698200 10622000

Cost of revenue 6745600 6629300

Gross profit 3952600 3992700

Operating expenses

Selling general and administrative 3324700 3348600

Others -49500 -63200

Total operating expenses 10020800 9914700

Operating income or loss 677400 707300

Income from continuing operations

Total other income/expenses net -610600 -530900

Earnings before interest and taxes 677400 707300

Interest expense -95400 -100200

Income before tax 66800 176400

Income tax expense 37700 60700

Minority interest -2500 -5900

Net income from continuing ops 29100 115700

Net income 25700 117100

Balance sheet of Marks and Spencer:

particulars 31/03/18 01/04/17

15

Current assets

Cash and cash equivalents 207700 468600

Net receivables 144800 137800

Inventory 781000 758500

Other current assets 10900 167700

Total current assets 1317900 1723300

Long-term investments 43600 51500

Property plant and equipment 4393900 4837800

Goodwill 77400 78400

Intangible assets 521800 630600

Other assets 1195600 970900

Total assets 7550200 8292500

Current liabilities

Accounts payable 872900 967500

Short/current debt 125300 517600

Other current liabilities 222600 224300

Total current liabilities 1826000 2368000

Long-term debt 1622900 1663400

Other liabilities 1099400 1062400

Minority interest -2500 -5900

Total liabilities 4596000 5142100

Stockholders' equity

Common stock 406200 406200

Retained earnings 6560400 6617600

16

Cash and cash equivalents 207700 468600

Net receivables 144800 137800

Inventory 781000 758500

Other current assets 10900 167700

Total current assets 1317900 1723300

Long-term investments 43600 51500

Property plant and equipment 4393900 4837800

Goodwill 77400 78400

Intangible assets 521800 630600

Other assets 1195600 970900

Total assets 7550200 8292500

Current liabilities

Accounts payable 872900 967500

Short/current debt 125300 517600

Other current liabilities 222600 224300

Total current liabilities 1826000 2368000

Long-term debt 1622900 1663400

Other liabilities 1099400 1062400

Minority interest -2500 -5900

Total liabilities 4596000 5142100

Stockholders' equity

Common stock 406200 406200

Retained earnings 6560400 6617600

16

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.