Financial Reporting: IFRS, IAS, and Financial Statement Analysis

VerifiedAdded on 2021/02/20

|14

|4016

|63

Report

AI Summary

This financial reporting report provides a comprehensive overview of the subject, beginning with an introduction to financial reporting and its purpose, emphasizing the importance of financial statements for various stakeholders such as investors and creditors. It delves into the conceptual and regulatory frameworks, explaining their requirements and qualitative characteristics of financial statements like understandability, relevance, reliability, and comparability. The report identifies key stakeholders and the benefits they derive from financial information. It explores how financial reporting aligns with organizational objectives and growth. The report includes financial statements as per IAS 1, analyzes the financial performance of the Admiral Group, differentiates between International Accounting Standards (IAS) and International Financial Reporting Standards (IFRS), and highlights the benefits and compliance variations of IFRS across the world. The report concludes with a summary of the key findings and references used throughout the study.

FINANCIAL REPORTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1. Context and purpose of financial reporting.............................................................................3

2. Conceptual and regulatory framework and the qualitative characteristics of financial

statements....................................................................................................................................4

3. Main stakeholders of an organization and the benefit to them from financial information....5

4. Requirement of financial reporting accomplishing the organization objectives and growth..6

5 Financial Statements as per IAS 1..........................................................................................7

6 Financial Statement of Admiral Group and interpretation on financial performance of the

company......................................................................................................................................9

7 Difference between International Accounting Standards (IAS) and International Financial

Reporting System (IFRS)............................................................................................................9

8 Benefits of IFRS.....................................................................................................................10

9 Varying degree of compliance in IFRS across world and factors impacting compliance ....11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1. Context and purpose of financial reporting.............................................................................3

2. Conceptual and regulatory framework and the qualitative characteristics of financial

statements....................................................................................................................................4

3. Main stakeholders of an organization and the benefit to them from financial information....5

4. Requirement of financial reporting accomplishing the organization objectives and growth..6

5 Financial Statements as per IAS 1..........................................................................................7

6 Financial Statement of Admiral Group and interpretation on financial performance of the

company......................................................................................................................................9

7 Difference between International Accounting Standards (IAS) and International Financial

Reporting System (IFRS)............................................................................................................9

8 Benefits of IFRS.....................................................................................................................10

9 Varying degree of compliance in IFRS across world and factors impacting compliance ....11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Financial reporting deals with communicating financial information of company such as

income statements, statement of financial position to users of financial statement such as

creditors, investors and other stakeholders of company. Financial reporting is defined as

presentation of financial information in form of statements in an understandable form. It also

includes communication to outsiders in form of minutes, management analysis and reports. The

objective of this study to know the role and importance of financial reporting. The report will

reveal about the conceptual and regulatory framework requirement and purpose behind using it.

Study will cover value of financial reporting to achieve its goals and objectives. It will give a n

understanding about the International Accounting Standards (IAS) and International Financial

Reporting Standards (IFRS) and the difference between the two. How IFRS is benefiting

companies across the world in preparation of financial statements.

TASK 1

1. Context and purpose of financial reporting

Financial reporting: It refers to the process of communicating information regarding

financial statement to its users such as different shareholders, creditors, investors etc. Financial

reporting helps the stakeholders to take the useful decision regarding investment (Schaltegger

and Burritt, 2017). It presents the financial statements such as income statements, cash flow,

balance sheet etc. to the internal and external stakeholders of the company.

Purpose of financial reporting

Report financial statements: The main purpose of financial reporting is to present

financial statements to its stakeholders. Financial statements such as balance sheet, profit and

loss account & cash flow statements are present to the internal and external stakeholders of the

company. They present the financial report in the annual or periodic meeting of the company to

highlights the achievements to the stakeholders.

Decision making: Financial report helps the top management to take effective and

efficient decision regarding the company. It emphasis the true and exact financial position of

company to the management (Beck, Dumay and Frost, 2017). It helps to improve their policies

and strategies to gain competitive advantage and earn higher profit in market.

Providing information: The aim of financial reporting is providing financial information

to the various stakeholders such as customer, shareholders, investors, suppliers, creditors etc. It

Financial reporting deals with communicating financial information of company such as

income statements, statement of financial position to users of financial statement such as

creditors, investors and other stakeholders of company. Financial reporting is defined as

presentation of financial information in form of statements in an understandable form. It also

includes communication to outsiders in form of minutes, management analysis and reports. The

objective of this study to know the role and importance of financial reporting. The report will

reveal about the conceptual and regulatory framework requirement and purpose behind using it.

Study will cover value of financial reporting to achieve its goals and objectives. It will give a n

understanding about the International Accounting Standards (IAS) and International Financial

Reporting Standards (IFRS) and the difference between the two. How IFRS is benefiting

companies across the world in preparation of financial statements.

TASK 1

1. Context and purpose of financial reporting

Financial reporting: It refers to the process of communicating information regarding

financial statement to its users such as different shareholders, creditors, investors etc. Financial

reporting helps the stakeholders to take the useful decision regarding investment (Schaltegger

and Burritt, 2017). It presents the financial statements such as income statements, cash flow,

balance sheet etc. to the internal and external stakeholders of the company.

Purpose of financial reporting

Report financial statements: The main purpose of financial reporting is to present

financial statements to its stakeholders. Financial statements such as balance sheet, profit and

loss account & cash flow statements are present to the internal and external stakeholders of the

company. They present the financial report in the annual or periodic meeting of the company to

highlights the achievements to the stakeholders.

Decision making: Financial report helps the top management to take effective and

efficient decision regarding the company. It emphasis the true and exact financial position of

company to the management (Beck, Dumay and Frost, 2017). It helps to improve their policies

and strategies to gain competitive advantage and earn higher profit in market.

Providing information: The aim of financial reporting is providing financial information

to the various stakeholders such as customer, shareholders, investors, suppliers, creditors etc. It

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

helps to aware the stakeholders regarding the wealth of the company to encourage them to invest

in the company.

2. Conceptual and regulatory framework and the qualitative characteristics of financial

statements

Conceptual framework: It refers to the system which provide a set of rules and standard

to the company to perform their task according the standard. It helps to record financial

transaction and to measures its accuracy and performance (Lewandowski, 2016). Conceptual

framework are used to set the functions, limit and nature of financial statements.

Requirement and purpose of conceptual framework

Conceptual framework are required to set accounting standard for the company.

It requires to solve the accounting disputes and problems by defining the standards.

Conceptual framework is used to record financial transaction by following all the

accounting standard which help to ensure the accuracy and reliability of the work.

Regulatory framework: It refers to the set of rules and regulation which guide that what

should be recorded in financial report and how to present them in financial statements. It helps

the company to present their data in final reports.

Requirement and purpose of regulatory framework

It requires in financial reporting ensuring the information provided by the company to the

stakeholders are able to meet their requirements.

Regulatory framework present the financial data in accurate manner which helps to

increase the motivation of financial information users.

It is required to regulate and monitor the behaviour of company and its directors with the

investors. It helps them to ensure that company production is in concern with investors

interest.

Qualitative characteristics of financial statements

Understandability: It refers that the presented data and information regarding the

financial position must be understandable to the users. It helps them to improve their

understandability and helps to take useful decisions. Understandability refers that the information

are clearly presented and the additional information are also provided in footnote so the user can

understand the reason behind the results.

in the company.

2. Conceptual and regulatory framework and the qualitative characteristics of financial

statements

Conceptual framework: It refers to the system which provide a set of rules and standard

to the company to perform their task according the standard. It helps to record financial

transaction and to measures its accuracy and performance (Lewandowski, 2016). Conceptual

framework are used to set the functions, limit and nature of financial statements.

Requirement and purpose of conceptual framework

Conceptual framework are required to set accounting standard for the company.

It requires to solve the accounting disputes and problems by defining the standards.

Conceptual framework is used to record financial transaction by following all the

accounting standard which help to ensure the accuracy and reliability of the work.

Regulatory framework: It refers to the set of rules and regulation which guide that what

should be recorded in financial report and how to present them in financial statements. It helps

the company to present their data in final reports.

Requirement and purpose of regulatory framework

It requires in financial reporting ensuring the information provided by the company to the

stakeholders are able to meet their requirements.

Regulatory framework present the financial data in accurate manner which helps to

increase the motivation of financial information users.

It is required to regulate and monitor the behaviour of company and its directors with the

investors. It helps them to ensure that company production is in concern with investors

interest.

Qualitative characteristics of financial statements

Understandability: It refers that the presented data and information regarding the

financial position must be understandable to the users. It helps them to improve their

understandability and helps to take useful decisions. Understandability refers that the information

are clearly presented and the additional information are also provided in footnote so the user can

understand the reason behind the results.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Relevance: It refers that the information provided by the company must be in precise and

accurate format, so they user can use the information according to their requirement (Nobes and

Stadler, 2015). The presented information must be scrutinized to provide only relevant

information.

Reliability: It means that the information present by the company to the stakeholders

must be reliable and free from any biases so the investor can take the decision without any

misleading. The reliability of data increase the trust or faith of financial users (Schroeder,

Clarkand Cathey, 2019).

Comparability: The presented data must be comparable to the previous year financial

data so the user can identify the trend of financial position. It means that the data must be

provided in the same format to compare the information with different financial periods.

3. Main stakeholders of an organization and the benefit to them from financial information.

Stakeholders are those people who have stake or interest in growth or failure of an

organization. Theses stakeholders are affected in some or other way if business is folded

tomorrow (Progunova and et.al., 2018). They are not limited to those working directly with or

for company. There are internal and external stakeholders of company.

Internal Stakeholders

Who have direct involvement in strategy and operation of organization such as owners,

employees and managers.

Employees

They are primary internal stakeholder as they are having significant time and financial

investment . They have defining role in formulating strategies, tactics and operations carried

out by organizations. Financial statements help hem to formulate by analysing the current

position of company (Johnston and Petacchi, 2017).

Managers

Managers have substantial role to determine the strategies for organizations and in

making operational decisions. Manager have to make decisions for the organizations and for that

financial information is important so that they can give decision which will enhance the

business and its performance.

accurate format, so they user can use the information according to their requirement (Nobes and

Stadler, 2015). The presented information must be scrutinized to provide only relevant

information.

Reliability: It means that the information present by the company to the stakeholders

must be reliable and free from any biases so the investor can take the decision without any

misleading. The reliability of data increase the trust or faith of financial users (Schroeder,

Clarkand Cathey, 2019).

Comparability: The presented data must be comparable to the previous year financial

data so the user can identify the trend of financial position. It means that the data must be

provided in the same format to compare the information with different financial periods.

3. Main stakeholders of an organization and the benefit to them from financial information.

Stakeholders are those people who have stake or interest in growth or failure of an

organization. Theses stakeholders are affected in some or other way if business is folded

tomorrow (Progunova and et.al., 2018). They are not limited to those working directly with or

for company. There are internal and external stakeholders of company.

Internal Stakeholders

Who have direct involvement in strategy and operation of organization such as owners,

employees and managers.

Employees

They are primary internal stakeholder as they are having significant time and financial

investment . They have defining role in formulating strategies, tactics and operations carried

out by organizations. Financial statements help hem to formulate by analysing the current

position of company (Johnston and Petacchi, 2017).

Managers

Managers have substantial role to determine the strategies for organizations and in

making operational decisions. Manager have to make decisions for the organizations and for that

financial information is important so that they can give decision which will enhance the

business and its performance.

Owners

individuals having significant shareholding in the company are known as owners.

Owners frame substantial decisions for both internal an d external stakeholders of company.

Financial information give the owners position of the company whether it is performing as per

expectations or not (Kraft, Vashishtha and Venkatachalam, 2017).

External stakeholders

businesses have to consider external stakeholders while framing strategies or making decisions.

They are customers supplier government and others.

Customers

Purpose behind providing products and services is fulfilling the needs of consumers.

Customer use financial information for knowing the products of company are reliable and the

company is complying with all safety standards.

Suppliers

Suppliers are important stakeholders of company as success of one impacts the other.

Financial information about the company will help them to know whether the company should

be availed goods on credit or not (Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros,

2015).

Government

They have stake in the success of company as businesses are taxed by them. Financial

information help them to know whether the company is complying with the regulatory

framework or not.

4. Requirement of financial reporting accomplishing the organization objectives and growth

Financial reporting helps to meet the organization objectives by attracting large number

of investors towards the organization. The importance if financial reporting are as follows:

Financial reporting helps to facilitate the statutory audit to analyse the financial

statements and provide opinion to the company to improve their financial position and

grow in market.

It works as a backbone of the company and provide financial information to the

stakeholders to capture their attention to invest in company. It helps to increase the profit

of company and gain greater market and customer share.

individuals having significant shareholding in the company are known as owners.

Owners frame substantial decisions for both internal an d external stakeholders of company.

Financial information give the owners position of the company whether it is performing as per

expectations or not (Kraft, Vashishtha and Venkatachalam, 2017).

External stakeholders

businesses have to consider external stakeholders while framing strategies or making decisions.

They are customers supplier government and others.

Customers

Purpose behind providing products and services is fulfilling the needs of consumers.

Customer use financial information for knowing the products of company are reliable and the

company is complying with all safety standards.

Suppliers

Suppliers are important stakeholders of company as success of one impacts the other.

Financial information about the company will help them to know whether the company should

be availed goods on credit or not (Martínez‐Ferrero, Garcia‐Sanchez and Cuadrado‐Ballesteros,

2015).

Government

They have stake in the success of company as businesses are taxed by them. Financial

information help them to know whether the company is complying with the regulatory

framework or not.

4. Requirement of financial reporting accomplishing the organization objectives and growth

Financial reporting helps to meet the organization objectives by attracting large number

of investors towards the organization. The importance if financial reporting are as follows:

Financial reporting helps to facilitate the statutory audit to analyse the financial

statements and provide opinion to the company to improve their financial position and

grow in market.

It works as a backbone of the company and provide financial information to the

stakeholders to capture their attention to invest in company. It helps to increase the profit

of company and gain greater market and customer share.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial report are presents in the periodic meeting of company to aware the directors

and shareholders regarding the wealth of company (Keyes, 2016). It is used to take

efficient and effective decision to accomplish the organization objectives.

It is used to attract the customer and investors towards the company by following all the

conceptual and regulatory framework. Financial report present accurate and reliable

information which increase the trust of stakeholders and help to achieve the organization

objectives by increasing productivity and profitability (Lang and Stice-Lawrence, 2015).

5 Financial Statements as per IAS 1

Statement of Profit or Loss as on 31st December '2018

Statement of Profit or Loss as on 31st Dec'2018

GBP'000

Revenue from contracts with operation 585100

Cost of Sales 391700

Depreciation on pl. & equip. 8670

Depreciation on land & property 4688

Gross Profits 180042

Operating Expenses 80500

Bank interest 1200

Preference dividend 2500

Ordinary dividend 4500

Depreciation on land & property 4687

Depreciation on pl. & equip. 8670

Loss of damaged goods 2470 104527

75515

Rental income 9600

Profit before income & tax 85115

Income tax expense 9500

Profit from continuing operations 75615

and shareholders regarding the wealth of company (Keyes, 2016). It is used to take

efficient and effective decision to accomplish the organization objectives.

It is used to attract the customer and investors towards the company by following all the

conceptual and regulatory framework. Financial report present accurate and reliable

information which increase the trust of stakeholders and help to achieve the organization

objectives by increasing productivity and profitability (Lang and Stice-Lawrence, 2015).

5 Financial Statements as per IAS 1

Statement of Profit or Loss as on 31st December '2018

Statement of Profit or Loss as on 31st Dec'2018

GBP'000

Revenue from contracts with operation 585100

Cost of Sales 391700

Depreciation on pl. & equip. 8670

Depreciation on land & property 4688

Gross Profits 180042

Operating Expenses 80500

Bank interest 1200

Preference dividend 2500

Ordinary dividend 4500

Depreciation on land & property 4687

Depreciation on pl. & equip. 8670

Loss of damaged goods 2470 104527

75515

Rental income 9600

Profit before income & tax 85115

Income tax expense 9500

Profit from continuing operations 75615

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

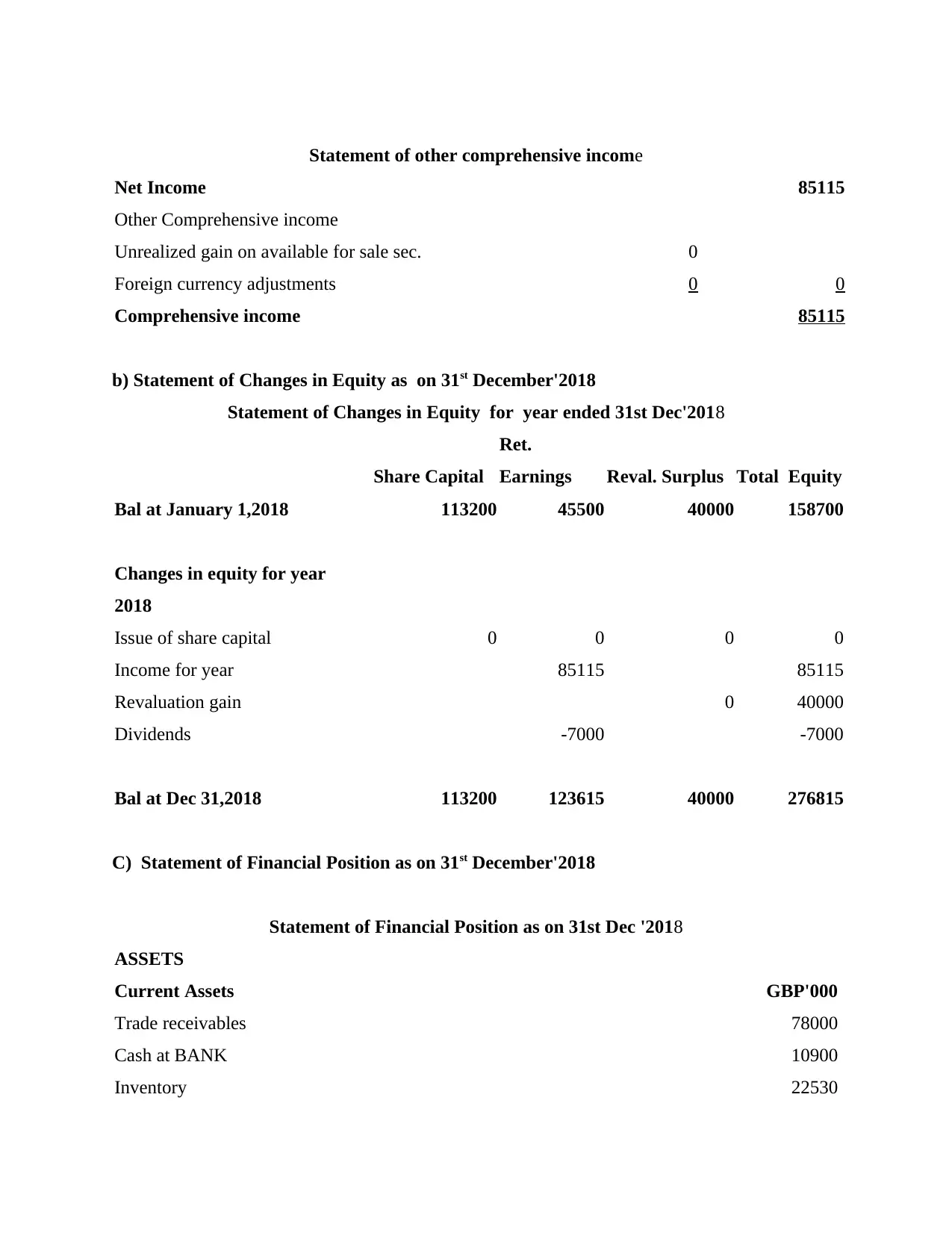

Statement of other comprehensive income

Net Income 85115

Other Comprehensive income

Unrealized gain on available for sale sec. 0

Foreign currency adjustments 0 0

Comprehensive income 85115

b) Statement of Changes in Equity as on 31st December'2018

Statement of Changes in Equity for year ended 31st Dec'2018

Share Capital

Ret.

Earnings Reval. Surplus Total Equity

Bal at January 1,2018 113200 45500 40000 158700

Changes in equity for year

2018

Issue of share capital 0 0 0 0

Income for year 85115 85115

Revaluation gain 0 40000

Dividends -7000 -7000

Bal at Dec 31,2018 113200 123615 40000 276815

C) Statement of Financial Position as on 31st December'2018

Statement of Financial Position as on 31st Dec '2018

ASSETS

Current Assets GBP'000

Trade receivables 78000

Cash at BANK 10900

Inventory 22530

Net Income 85115

Other Comprehensive income

Unrealized gain on available for sale sec. 0

Foreign currency adjustments 0 0

Comprehensive income 85115

b) Statement of Changes in Equity as on 31st December'2018

Statement of Changes in Equity for year ended 31st Dec'2018

Share Capital

Ret.

Earnings Reval. Surplus Total Equity

Bal at January 1,2018 113200 45500 40000 158700

Changes in equity for year

2018

Issue of share capital 0 0 0 0

Income for year 85115 85115

Revaluation gain 0 40000

Dividends -7000 -7000

Bal at Dec 31,2018 113200 123615 40000 276815

C) Statement of Financial Position as on 31st December'2018

Statement of Financial Position as on 31st Dec '2018

ASSETS

Current Assets GBP'000

Trade receivables 78000

Cash at BANK 10900

Inventory 22530

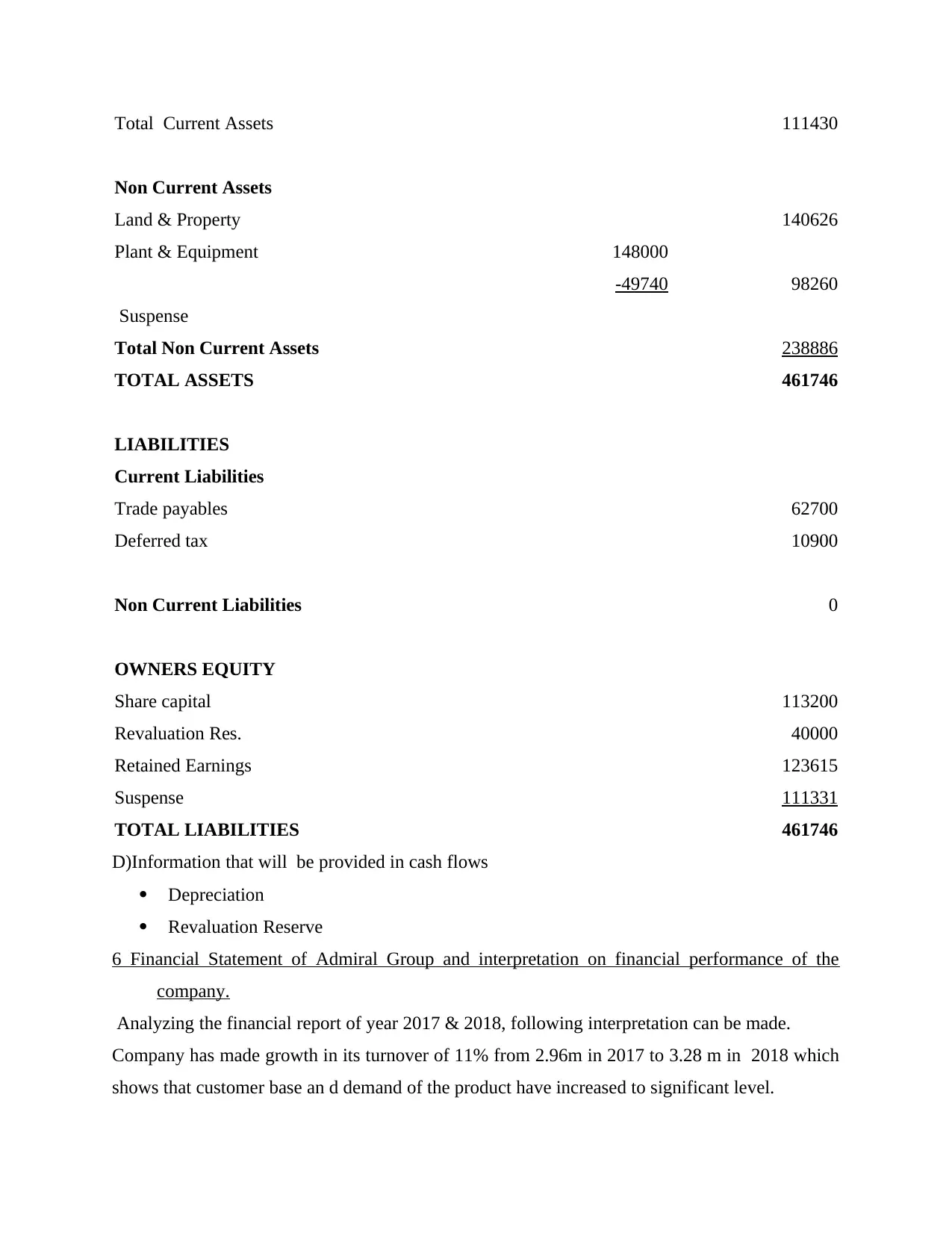

Total Current Assets 111430

Non Current Assets

Land & Property 140626

Plant & Equipment 148000

-49740 98260

Suspense

Total Non Current Assets 238886

TOTAL ASSETS 461746

LIABILITIES

Current Liabilities

Trade payables 62700

Deferred tax 10900

Non Current Liabilities 0

OWNERS EQUITY

Share capital 113200

Revaluation Res. 40000

Retained Earnings 123615

Suspense 111331

TOTAL LIABILITIES 461746

D)Information that will be provided in cash flows

Depreciation

Revaluation Reserve

6 Financial Statement of Admiral Group and interpretation on financial performance of the

company.

Analyzing the financial report of year 2017 & 2018, following interpretation can be made.

Company has made growth in its turnover of 11% from 2.96m in 2017 to 3.28 m in 2018 which

shows that customer base an d demand of the product have increased to significant level.

Non Current Assets

Land & Property 140626

Plant & Equipment 148000

-49740 98260

Suspense

Total Non Current Assets 238886

TOTAL ASSETS 461746

LIABILITIES

Current Liabilities

Trade payables 62700

Deferred tax 10900

Non Current Liabilities 0

OWNERS EQUITY

Share capital 113200

Revaluation Res. 40000

Retained Earnings 123615

Suspense 111331

TOTAL LIABILITIES 461746

D)Information that will be provided in cash flows

Depreciation

Revaluation Reserve

6 Financial Statement of Admiral Group and interpretation on financial performance of the

company.

Analyzing the financial report of year 2017 & 2018, following interpretation can be made.

Company has made growth in its turnover of 11% from 2.96m in 2017 to 3.28 m in 2018 which

shows that customer base an d demand of the product have increased to significant level.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Pretax profits o f company have increased to 479.3m in 2018 from 405.4m the growth

is seen because of change in assumption of Ogden discount rates leading to increase in profit

commission and underwriting profit. Ignoring the Ogden impact PBT has increased by 2 % to

over 413.3m .

UK customers and insurance turnover had grown by 13 % and 9% to over 5.2m and

2.6b. Significant increase was seen installment income which was driven as result of retention

of installment income

UK household show strong turnover growth though suffered loss around 3m in 2018

where from profit of 4.1m in 2017.

Improvements are seen in International Insurance results with reduction in loss to 1.1 m

in 2018 from loss of 14.3m in 2017. Where European insurance business has generated profits

of 6.4m in 2018 from a loss of 1.9m in 2017 .

Aggregate profit of 8.8m in 2018 from 7.1m in 2017 excluding minority share is seen in

price comparison.

Increase of 17% is seen in earning per share to 137.1 pence due to increased group profit

because of change in Ogden assumption rate. Excluding the change EPS would been 118.2

pence which is only 1% higher than in 2017.

Company is significantly growing in market with an increasing customers base that

shows company has built its brand image which is helping it to generate high revenues

7 Difference between International Accounting Standards (IAS) and International Financial

Reporting System (IFRS).

International accounting standard are the set of standards which provides methods of

reflecting specific transactions and events in the financial statements. In past , Board of

International accounting standards committee (IASC) was issuing International accounting

standards. From 2001, International Accounting Standard Board (IASB) has been issuing new

standards known as International Financing Reporting Standards (IFRS) (Bushee, Goodman

and Sunder, 2018). IASC is not authorized to have compliance requirement with its standards,

as publicly traded companies are required to prepare financial statements as per IAS (Difference

between IAS and IFRS. 2019).

In technical terms they are one in same thing. IFRS are the new standards that reflects

the changes in business and accounting practice from last 2 decades. Where IAS was used

is seen because of change in assumption of Ogden discount rates leading to increase in profit

commission and underwriting profit. Ignoring the Ogden impact PBT has increased by 2 % to

over 413.3m .

UK customers and insurance turnover had grown by 13 % and 9% to over 5.2m and

2.6b. Significant increase was seen installment income which was driven as result of retention

of installment income

UK household show strong turnover growth though suffered loss around 3m in 2018

where from profit of 4.1m in 2017.

Improvements are seen in International Insurance results with reduction in loss to 1.1 m

in 2018 from loss of 14.3m in 2017. Where European insurance business has generated profits

of 6.4m in 2018 from a loss of 1.9m in 2017 .

Aggregate profit of 8.8m in 2018 from 7.1m in 2017 excluding minority share is seen in

price comparison.

Increase of 17% is seen in earning per share to 137.1 pence due to increased group profit

because of change in Ogden assumption rate. Excluding the change EPS would been 118.2

pence which is only 1% higher than in 2017.

Company is significantly growing in market with an increasing customers base that

shows company has built its brand image which is helping it to generate high revenues

7 Difference between International Accounting Standards (IAS) and International Financial

Reporting System (IFRS).

International accounting standard are the set of standards which provides methods of

reflecting specific transactions and events in the financial statements. In past , Board of

International accounting standards committee (IASC) was issuing International accounting

standards. From 2001, International Accounting Standard Board (IASB) has been issuing new

standards known as International Financing Reporting Standards (IFRS) (Bushee, Goodman

and Sunder, 2018). IASC is not authorized to have compliance requirement with its standards,

as publicly traded companies are required to prepare financial statements as per IAS (Difference

between IAS and IFRS. 2019).

In technical terms they are one in same thing. IFRS are the new standards that reflects

the changes in business and accounting practice from last 2 decades. Where IAS was used

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

before the introduction of IFRS (Acharya and Ryan, 2016). Only 9 IFRS have been issued till

date and standards of IAS which have not been superseded by IFRS are still in usage. IAS are no

longer issued by IASB. Any standards that will be issued in future will be known as IFRS, and

in the event of contradiction between IAS and IFRS, always IFRS will prevail.

8 Benefits of IFRS

IFRS are the accounting rules that define the reporting of transaction in financial statements. It

also provides information regarding the inclusion and disclosure in financial statements. IFRS

has helped in resolving many problems of accounting world (Benefits of IFRS).

Benefits of IFRS

Single set for accounting standards around the globe.

IFRS will enable companies around the world in different segments to apply same set

of standards for every transaction. This will increase transparency that would allow cross border

investments. This will decrease cost of capital in providing high liquidity during every

transaction.

Reduction in timing, efforts and expenses to prepare multiple reports

IFRS will help organization in cutting down its time which is spend in preparation of

financial statements of company. They will also cut the cost of preparing financial statements as

company would not be required to follow multiple standards in its business. Number of reports

to be prepared by company may be reduced to just one for each year saving time and money

of company.

Easy monitoring and controlling of subsidiaries from other countries

Companies are preparing reports using IAS and GAAP which increased error risk and

auditing requirements for ensuring compliance (Williams and Dobelman, 2017). With the

adoption of IFRS every country has to prepare financial statements as per the above standard

that will help the parent companies to monitor and control the operations from even other

nations.

More flexible in accounting practices

IFRS uses principle based system rather than specific rules which are based on

philosophy. Motive of each standard is to come at reasonable valuation and for that different

ways can be used for the outcome. Structure gives freedom to adopt the global standards which

are useful for producing useful statements.

date and standards of IAS which have not been superseded by IFRS are still in usage. IAS are no

longer issued by IASB. Any standards that will be issued in future will be known as IFRS, and

in the event of contradiction between IAS and IFRS, always IFRS will prevail.

8 Benefits of IFRS

IFRS are the accounting rules that define the reporting of transaction in financial statements. It

also provides information regarding the inclusion and disclosure in financial statements. IFRS

has helped in resolving many problems of accounting world (Benefits of IFRS).

Benefits of IFRS

Single set for accounting standards around the globe.

IFRS will enable companies around the world in different segments to apply same set

of standards for every transaction. This will increase transparency that would allow cross border

investments. This will decrease cost of capital in providing high liquidity during every

transaction.

Reduction in timing, efforts and expenses to prepare multiple reports

IFRS will help organization in cutting down its time which is spend in preparation of

financial statements of company. They will also cut the cost of preparing financial statements as

company would not be required to follow multiple standards in its business. Number of reports

to be prepared by company may be reduced to just one for each year saving time and money

of company.

Easy monitoring and controlling of subsidiaries from other countries

Companies are preparing reports using IAS and GAAP which increased error risk and

auditing requirements for ensuring compliance (Williams and Dobelman, 2017). With the

adoption of IFRS every country has to prepare financial statements as per the above standard

that will help the parent companies to monitor and control the operations from even other

nations.

More flexible in accounting practices

IFRS uses principle based system rather than specific rules which are based on

philosophy. Motive of each standard is to come at reasonable valuation and for that different

ways can be used for the outcome. Structure gives freedom to adopt the global standards which

are useful for producing useful statements.

9 Varying degree of compliance in IFRS across world and factors impacting compliance

With the introduction of globalization focus is laid on harmonizing the accounting

practices around he world. Companies are adopting IFRS as it has made mandatory for

companies following IAS. Companies may follow the standards set by their national accounting

boards but at the same time they have to prepare statements as per the accounting standards set

by IFRS for reflecting different transactions and events appropriately in the statements.

Factors that are affecting compliance with IFRS are laws of different nations that require

compliance with their national standards. Taxation problems is making it difficult for companies

to follow IFRS as authorities are not able to figure out exact tax implications accurately (Leuz

and Wysocki, 2016).

The example of factors affecting can be seen in USA as companies in USA are following

IAS and GAAP and is making it difficult for them to prepare statements as per IFRS. It is

contradicting the rules of IFRS making it difficult for companies to make their statements

comparable.

CONCLUSION

Above study has given conclusions that financial reporting is important for preparing

financial statements such as income statement, balance sheet and cash flow statements. These

statements help in decision making by the managers of company as wells as outside investors

who are planning to invest in company. Financial reporting help to comply with conceptual

framework as they are important for setting accounting standards for company. Complying with

regulatory requirement will help in producing information that is important for stakeholders of

company. It also monitor and regulate the company behavior with that of its investors.

Qualitative characteristic of financial statements included understandability ,reliability, relevance

and comparability. Financial reporting helps company in meeting its objectives by attracting

investors for the company. Auditors are able to frame opinions on the company and its

performance by analyzing the financial statements of company. Company has to make decision

for framing strategies and concepts for operation by keeping in mind all the stakeholders of

company. As they are the individuals or groups who are interested and affected with success or

failure of company.

The International Accounting Standard (IAS) and International Financial Reporting

Framework (IFRS) are in technical term one in same thing. IAS were previously laid by board

With the introduction of globalization focus is laid on harmonizing the accounting

practices around he world. Companies are adopting IFRS as it has made mandatory for

companies following IAS. Companies may follow the standards set by their national accounting

boards but at the same time they have to prepare statements as per the accounting standards set

by IFRS for reflecting different transactions and events appropriately in the statements.

Factors that are affecting compliance with IFRS are laws of different nations that require

compliance with their national standards. Taxation problems is making it difficult for companies

to follow IFRS as authorities are not able to figure out exact tax implications accurately (Leuz

and Wysocki, 2016).

The example of factors affecting can be seen in USA as companies in USA are following

IAS and GAAP and is making it difficult for them to prepare statements as per IFRS. It is

contradicting the rules of IFRS making it difficult for companies to make their statements

comparable.

CONCLUSION

Above study has given conclusions that financial reporting is important for preparing

financial statements such as income statement, balance sheet and cash flow statements. These

statements help in decision making by the managers of company as wells as outside investors

who are planning to invest in company. Financial reporting help to comply with conceptual

framework as they are important for setting accounting standards for company. Complying with

regulatory requirement will help in producing information that is important for stakeholders of

company. It also monitor and regulate the company behavior with that of its investors.

Qualitative characteristic of financial statements included understandability ,reliability, relevance

and comparability. Financial reporting helps company in meeting its objectives by attracting

investors for the company. Auditors are able to frame opinions on the company and its

performance by analyzing the financial statements of company. Company has to make decision

for framing strategies and concepts for operation by keeping in mind all the stakeholders of

company. As they are the individuals or groups who are interested and affected with success or

failure of company.

The International Accounting Standard (IAS) and International Financial Reporting

Framework (IFRS) are in technical term one in same thing. IAS were previously laid by board

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.