Managing Financial Resources in the Hospitality Industry

VerifiedAdded on 2023/06/16

|13

|3495

|457

AI Summary

This report discusses GAAP, financial statements, stakeholders, and ratio analysis in the context of the hospitality industry. It covers topics such as generally accepted accounting principles, users of financial statements, supplement components of financial statements, and financial reporting concepts. It also includes a detailed analysis of Smart Resort Limited's financial ratios. Course code, course name, and college/university are not mentioned.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

MANAGING FINANCIAL

RESOURCES IN

HOSPITALITY INDUSTRY

RESOURCES IN

HOSPITALITY INDUSTRY

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Q1................................................................................................................................................3

Q2................................................................................................................................................4

Q3................................................................................................................................................5

Q4................................................................................................................................................6

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY..................................................................................................................................3

Q1................................................................................................................................................3

Q2................................................................................................................................................4

Q3................................................................................................................................................5

Q4................................................................................................................................................6

CONCLUSION..............................................................................................................................11

REFERENCES................................................................................................................................1

INTRODUCTION

Accounting refers to the process that is considered with the recording of transaction related

with the business. It is the base that would lead to the preparation of the financial statement

(Elliott and Elliot, 2017). With the making of analysis of the financial statement the financial

health of the company would be analysed. It is to be noted that while preparing the financial

statement the companies would need to consider the GAAP. This report would discuss the

concept of GAAP, the major financial statement of the company in the context of the use of

various stakeholders. Likewise, a detailed analysis of the financial statement through ratio

analysis would also be a part of the report.

MAIN BODY

Q1

Generally accepted accounting principles:

It refers to a common set of accounting principles, procedures, standards which are issued

by the Financial Accounting Standards Board. Every company need to follow the accounting

standards and the principles while preparing the financial statements and the accounts. GAAP is

an integration of various standards and the accepted ways of recording and reporting of

accounting information (Baker and Persson, 2021). It includes the approved accounting practices

and the methods that would be used by the companies. It includes various principles including

the regularity that is related with the adherence of rules and regulations, principle of consistency

which states that the companies need to be consistent with the use of accounting standards,

principle of sincerity which is related with the maintaining of accuracy and impartiality,

performance of method that is related with the following of consistent procedures for the making

of the financial statements, principle of prudence that would not allow the speculation in relation

with the financial data and many more.

Users of financial statements:

It includes the owners, managers, Customers, Competitors, Government, Suppliers,

lenders, employees, investors and various other (Ariana, Bagiada and Sukayasa, 2018). These are

considered as major stakeholders of the company that may have an interest in the organization

and also have power that they may affect the organization. They are main users because they

Accounting refers to the process that is considered with the recording of transaction related

with the business. It is the base that would lead to the preparation of the financial statement

(Elliott and Elliot, 2017). With the making of analysis of the financial statement the financial

health of the company would be analysed. It is to be noted that while preparing the financial

statement the companies would need to consider the GAAP. This report would discuss the

concept of GAAP, the major financial statement of the company in the context of the use of

various stakeholders. Likewise, a detailed analysis of the financial statement through ratio

analysis would also be a part of the report.

MAIN BODY

Q1

Generally accepted accounting principles:

It refers to a common set of accounting principles, procedures, standards which are issued

by the Financial Accounting Standards Board. Every company need to follow the accounting

standards and the principles while preparing the financial statements and the accounts. GAAP is

an integration of various standards and the accepted ways of recording and reporting of

accounting information (Baker and Persson, 2021). It includes the approved accounting practices

and the methods that would be used by the companies. It includes various principles including

the regularity that is related with the adherence of rules and regulations, principle of consistency

which states that the companies need to be consistent with the use of accounting standards,

principle of sincerity which is related with the maintaining of accuracy and impartiality,

performance of method that is related with the following of consistent procedures for the making

of the financial statements, principle of prudence that would not allow the speculation in relation

with the financial data and many more.

Users of financial statements:

It includes the owners, managers, Customers, Competitors, Government, Suppliers,

lenders, employees, investors and various other (Ariana, Bagiada and Sukayasa, 2018). These are

considered as major stakeholders of the company that may have an interest in the organization

and also have power that they may affect the organization. They are main users because they

need to make decision with the company and they have an interest within the company

performance.

Need of information for decision makers:

As per the decision maker’s various information would be needed by them. This can be

understood with an example of decision maker i.e. Investor. With refers to an investor the

information that would be needed would include the income statement and financial position

statement. This is because with the help of these financial statement and its contained

information it would be able to make them analysis of the financial health and the performance

of the organization and accordingly they would make the decision of investment.

In the same way with the analysis of the information of the financial statement including the

profit and loss account or the balance sheet the company’s managers or the management would

also able to make decision related with the making of any change in the organization’s policies

and rules (Lee and Tweedie, 2020). Likewise, the statement of equity the shareholder of the firm

would be able to take decision regarding their binding with the firm or not. This would be right

to states that as per the need and use of various financial statement the concerned user would

take the information and make decision in relation with the firm.

Q2

Statement of income, financial position and cash flow statement:

Income statement:

This is one of the major financial statement that is related with the determination of the

profit and loss of the company (Guerard, Saxena and Gultekin, 2021). With the help of analysis

of this statement, it would be easy to determine that whether the company has earned profit and

incurred loss.

Statement of financial position:

This statement is related with the making of analysis of the financial position of the

company. With the help of this statement the financial position of the company in terms of the

position of assets and liabilities would be analysed (Bareja, Gawart and Giedroyc, 2017). It is

based on accounting equation i.e. Assets = Liabilities+ equities.

Statement of cash flow:

performance.

Need of information for decision makers:

As per the decision maker’s various information would be needed by them. This can be

understood with an example of decision maker i.e. Investor. With refers to an investor the

information that would be needed would include the income statement and financial position

statement. This is because with the help of these financial statement and its contained

information it would be able to make them analysis of the financial health and the performance

of the organization and accordingly they would make the decision of investment.

In the same way with the analysis of the information of the financial statement including the

profit and loss account or the balance sheet the company’s managers or the management would

also able to make decision related with the making of any change in the organization’s policies

and rules (Lee and Tweedie, 2020). Likewise, the statement of equity the shareholder of the firm

would be able to take decision regarding their binding with the firm or not. This would be right

to states that as per the need and use of various financial statement the concerned user would

take the information and make decision in relation with the firm.

Q2

Statement of income, financial position and cash flow statement:

Income statement:

This is one of the major financial statement that is related with the determination of the

profit and loss of the company (Guerard, Saxena and Gultekin, 2021). With the help of analysis

of this statement, it would be easy to determine that whether the company has earned profit and

incurred loss.

Statement of financial position:

This statement is related with the making of analysis of the financial position of the

company. With the help of this statement the financial position of the company in terms of the

position of assets and liabilities would be analysed (Bareja, Gawart and Giedroyc, 2017). It is

based on accounting equation i.e. Assets = Liabilities+ equities.

Statement of cash flow:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

This statement is related with the analysis of the cash inflows and outflows of the

company (Donelan and Liu, 2021). With the help of this statement the company would be able to

make analysis of the cash position in terms of its inflows and outflows from the company.

Loan creditors:

These includes those creditors from which the money is owned by the organization. This

means they make demand of money from the firm (Okolelova and et.al., 2019). In simple words

those creditors which offer loan to the company would be considered as trade creditors. They are

mostly interested in income statement and financial position of the company. This is because if

the company is incurring loss then it would be a point to notice by the loan creditor. Likewise,

earning of profit by the firm would be considered as positive aspect for the loan creditor because

it gives assurance that they would be able to get recovered of the loan. Likewise, with the

making of analysis of the financial position the loan creditor would be able to determine the

financial position of the company in the market that would enable them to make adequate

decision towards the company in terms of giving them loan or not.

Trade Creditors:

These are those individuals to whom the company need to make payment. These would

include the suppliers from whom the organization has owned raw material and now need

payment. In other words, trade creditors are the bills that an organization need to pay. They are

highly interested in the statement of income and cash flow. This is because with the analysis of

the cash flow the firm’s position related with the cash would be able to get analysed. This would

enable them information related with the cash availability that whether the company has

adequate cash or not. Likewise, with the analysis of the income statement they would analysis of

the financial position of the company that whether the company have capacity that they can

make repayment or not.

Q3

Component that supplement the financial statement:

There are various supplement components of the financial statement that would enable

the user to understand the financial statement. These supplement component would include the

notes to financial statements, auditor’s report, management discussion and analysis and various

other. With the making of understanding of these supplement it would be easy to make an

company (Donelan and Liu, 2021). With the help of this statement the company would be able to

make analysis of the cash position in terms of its inflows and outflows from the company.

Loan creditors:

These includes those creditors from which the money is owned by the organization. This

means they make demand of money from the firm (Okolelova and et.al., 2019). In simple words

those creditors which offer loan to the company would be considered as trade creditors. They are

mostly interested in income statement and financial position of the company. This is because if

the company is incurring loss then it would be a point to notice by the loan creditor. Likewise,

earning of profit by the firm would be considered as positive aspect for the loan creditor because

it gives assurance that they would be able to get recovered of the loan. Likewise, with the

making of analysis of the financial position the loan creditor would be able to determine the

financial position of the company in the market that would enable them to make adequate

decision towards the company in terms of giving them loan or not.

Trade Creditors:

These are those individuals to whom the company need to make payment. These would

include the suppliers from whom the organization has owned raw material and now need

payment. In other words, trade creditors are the bills that an organization need to pay. They are

highly interested in the statement of income and cash flow. This is because with the analysis of

the cash flow the firm’s position related with the cash would be able to get analysed. This would

enable them information related with the cash availability that whether the company has

adequate cash or not. Likewise, with the analysis of the income statement they would analysis of

the financial position of the company that whether the company have capacity that they can

make repayment or not.

Q3

Component that supplement the financial statement:

There are various supplement components of the financial statement that would enable

the user to understand the financial statement. These supplement component would include the

notes to financial statements, auditor’s report, management discussion and analysis and various

other. With the making of understanding of these supplement it would be easy to make an

analysis of the financial statement and its related information. This can be understood as the

notes to the financial statement would enable the information related with the financial statement

including the information which would assist the user to understand the financial report. All the

supplementary and essential information would a part of notes to account (Telles, 2018).

Likewise, with the analysis of the auditor’s report the comment on the financial structure and

information would be able to understand. This is because the auditor’s report would contain the

information related with the financial position and performance of the company. In the same way

as the auditor report contain the opinion of auditor regarding the aspect that whether the

company would comply with the GAAP or not. This would enable the user to determine that

how well the company is performing and whether it is compiling with the required laws and

regulations or not. This shows that the auditor report is an important supplement of financial

statement because it would enable the company’s internal information and its working (Smith,

2019).

In the same way the management discussion report would also include the information

that is based on the analysis of the management towards the company. This is because it includes

the management report and information that is based on the internal analysis of the company

which would enable the user to have more knowledge and information towards the company and

its financial position and performance.

Financial reporting concepts:

Financial reporting refers to the concept that would assist the organization to make

communication of its financial information to the third party. This is an important concept that

would assist the organization to make informed the third party regarding its performance and

position. With the aspect of financial reporting the financial statement would be disclosed to the

user and the third party so that the performance of the company and its financial position would;

be enable to the users. This is usually made at the end of the financial year. This disclosure

would be made by the organization with the consideration of the stakeholders including the

customers, investors, shareholders, creditors, customers and various other.

Q4

Ratio analysis:

notes to the financial statement would enable the information related with the financial statement

including the information which would assist the user to understand the financial report. All the

supplementary and essential information would a part of notes to account (Telles, 2018).

Likewise, with the analysis of the auditor’s report the comment on the financial structure and

information would be able to understand. This is because the auditor’s report would contain the

information related with the financial position and performance of the company. In the same way

as the auditor report contain the opinion of auditor regarding the aspect that whether the

company would comply with the GAAP or not. This would enable the user to determine that

how well the company is performing and whether it is compiling with the required laws and

regulations or not. This shows that the auditor report is an important supplement of financial

statement because it would enable the company’s internal information and its working (Smith,

2019).

In the same way the management discussion report would also include the information

that is based on the analysis of the management towards the company. This is because it includes

the management report and information that is based on the internal analysis of the company

which would enable the user to have more knowledge and information towards the company and

its financial position and performance.

Financial reporting concepts:

Financial reporting refers to the concept that would assist the organization to make

communication of its financial information to the third party. This is an important concept that

would assist the organization to make informed the third party regarding its performance and

position. With the aspect of financial reporting the financial statement would be disclosed to the

user and the third party so that the performance of the company and its financial position would;

be enable to the users. This is usually made at the end of the financial year. This disclosure

would be made by the organization with the consideration of the stakeholders including the

customers, investors, shareholders, creditors, customers and various other.

Q4

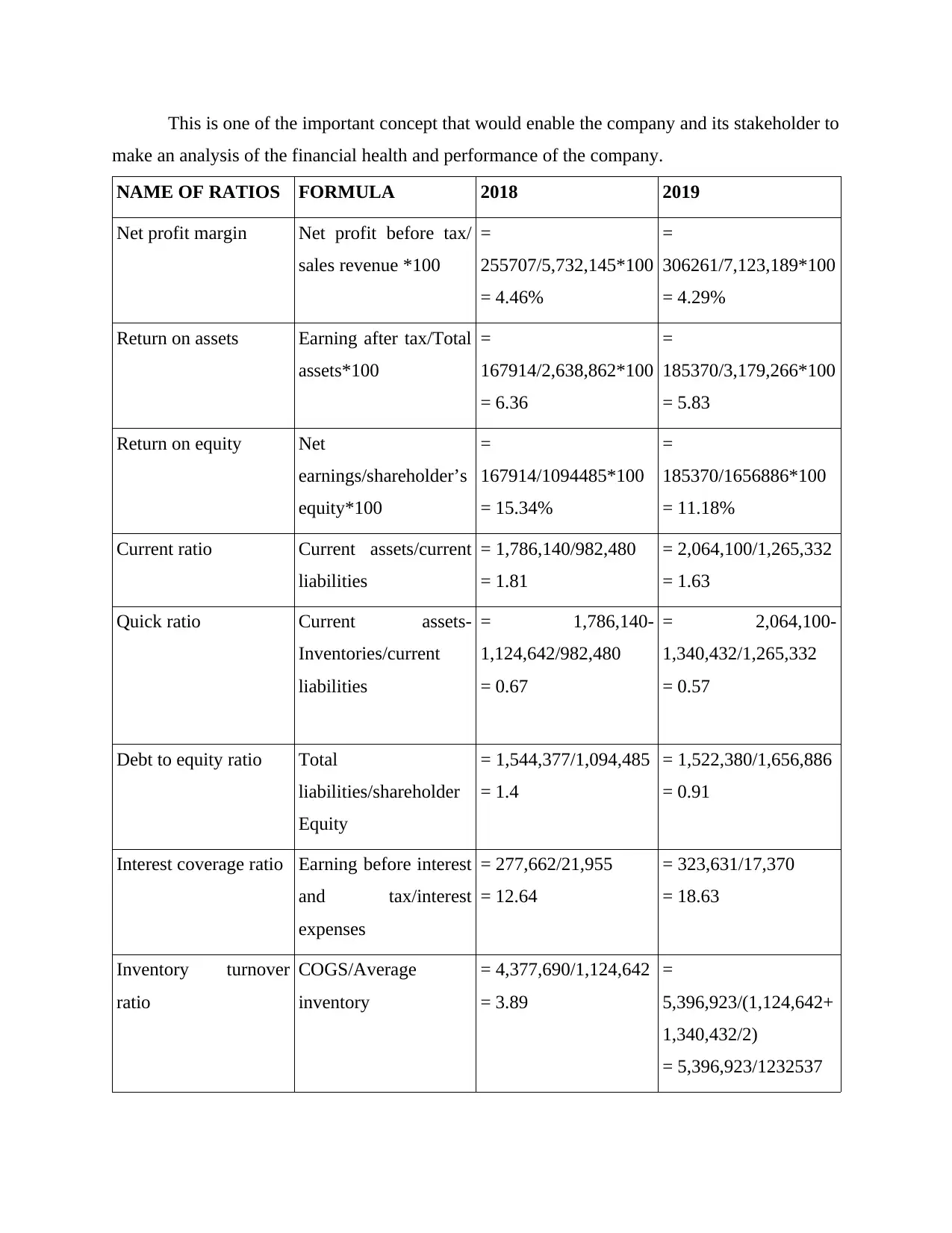

Ratio analysis:

This is one of the important concept that would enable the company and its stakeholder to

make an analysis of the financial health and performance of the company.

NAME OF RATIOS FORMULA 2018 2019

Net profit margin Net profit before tax/

sales revenue *100

=

255707/5,732,145*100

= 4.46%

=

306261/7,123,189*100

= 4.29%

Return on assets Earning after tax/Total

assets*100

=

167914/2,638,862*100

= 6.36

=

185370/3,179,266*100

= 5.83

Return on equity Net

earnings/shareholder’s

equity*100

=

167914/1094485*100

= 15.34%

=

185370/1656886*100

= 11.18%

Current ratio Current assets/current

liabilities

= 1,786,140/982,480

= 1.81

= 2,064,100/1,265,332

= 1.63

Quick ratio Current assets-

Inventories/current

liabilities

= 1,786,140-

1,124,642/982,480

= 0.67

= 2,064,100-

1,340,432/1,265,332

= 0.57

Debt to equity ratio Total

liabilities/shareholder

Equity

= 1,544,377/1,094,485

= 1.4

= 1,522,380/1,656,886

= 0.91

Interest coverage ratio Earning before interest

and tax/interest

expenses

= 277,662/21,955

= 12.64

= 323,631/17,370

= 18.63

Inventory turnover

ratio

COGS/Average

inventory

= 4,377,690/1,124,642

= 3.89

=

5,396,923/(1,124,642+

1,340,432/2)

= 5,396,923/1232537

make an analysis of the financial health and performance of the company.

NAME OF RATIOS FORMULA 2018 2019

Net profit margin Net profit before tax/

sales revenue *100

=

255707/5,732,145*100

= 4.46%

=

306261/7,123,189*100

= 4.29%

Return on assets Earning after tax/Total

assets*100

=

167914/2,638,862*100

= 6.36

=

185370/3,179,266*100

= 5.83

Return on equity Net

earnings/shareholder’s

equity*100

=

167914/1094485*100

= 15.34%

=

185370/1656886*100

= 11.18%

Current ratio Current assets/current

liabilities

= 1,786,140/982,480

= 1.81

= 2,064,100/1,265,332

= 1.63

Quick ratio Current assets-

Inventories/current

liabilities

= 1,786,140-

1,124,642/982,480

= 0.67

= 2,064,100-

1,340,432/1,265,332

= 0.57

Debt to equity ratio Total

liabilities/shareholder

Equity

= 1,544,377/1,094,485

= 1.4

= 1,522,380/1,656,886

= 0.91

Interest coverage ratio Earning before interest

and tax/interest

expenses

= 277,662/21,955

= 12.64

= 323,631/17,370

= 18.63

Inventory turnover

ratio

COGS/Average

inventory

= 4,377,690/1,124,642

= 3.89

=

5,396,923/(1,124,642+

1,340,432/2)

= 5,396,923/1232537

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

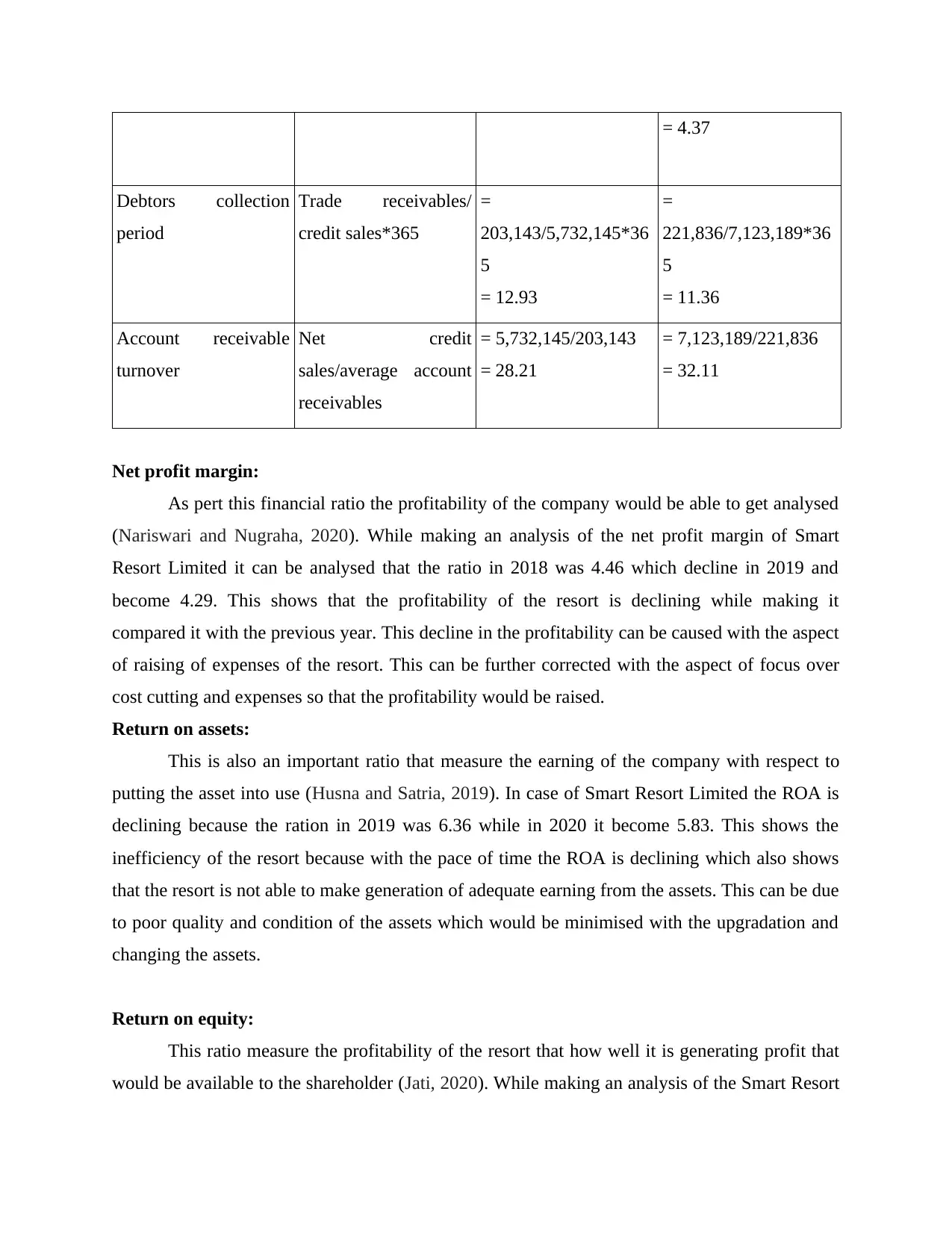

= 4.37

Debtors collection

period

Trade receivables/

credit sales*365

=

203,143/5,732,145*36

5

= 12.93

=

221,836/7,123,189*36

5

= 11.36

Account receivable

turnover

Net credit

sales/average account

receivables

= 5,732,145/203,143

= 28.21

= 7,123,189/221,836

= 32.11

Net profit margin:

As pert this financial ratio the profitability of the company would be able to get analysed

(Nariswari and Nugraha, 2020). While making an analysis of the net profit margin of Smart

Resort Limited it can be analysed that the ratio in 2018 was 4.46 which decline in 2019 and

become 4.29. This shows that the profitability of the resort is declining while making it

compared it with the previous year. This decline in the profitability can be caused with the aspect

of raising of expenses of the resort. This can be further corrected with the aspect of focus over

cost cutting and expenses so that the profitability would be raised.

Return on assets:

This is also an important ratio that measure the earning of the company with respect to

putting the asset into use (Husna and Satria, 2019). In case of Smart Resort Limited the ROA is

declining because the ration in 2019 was 6.36 while in 2020 it become 5.83. This shows the

inefficiency of the resort because with the pace of time the ROA is declining which also shows

that the resort is not able to make generation of adequate earning from the assets. This can be due

to poor quality and condition of the assets which would be minimised with the upgradation and

changing the assets.

Return on equity:

This ratio measure the profitability of the resort that how well it is generating profit that

would be available to the shareholder (Jati, 2020). While making an analysis of the Smart Resort

Debtors collection

period

Trade receivables/

credit sales*365

=

203,143/5,732,145*36

5

= 12.93

=

221,836/7,123,189*36

5

= 11.36

Account receivable

turnover

Net credit

sales/average account

receivables

= 5,732,145/203,143

= 28.21

= 7,123,189/221,836

= 32.11

Net profit margin:

As pert this financial ratio the profitability of the company would be able to get analysed

(Nariswari and Nugraha, 2020). While making an analysis of the net profit margin of Smart

Resort Limited it can be analysed that the ratio in 2018 was 4.46 which decline in 2019 and

become 4.29. This shows that the profitability of the resort is declining while making it

compared it with the previous year. This decline in the profitability can be caused with the aspect

of raising of expenses of the resort. This can be further corrected with the aspect of focus over

cost cutting and expenses so that the profitability would be raised.

Return on assets:

This is also an important ratio that measure the earning of the company with respect to

putting the asset into use (Husna and Satria, 2019). In case of Smart Resort Limited the ROA is

declining because the ration in 2019 was 6.36 while in 2020 it become 5.83. This shows the

inefficiency of the resort because with the pace of time the ROA is declining which also shows

that the resort is not able to make generation of adequate earning from the assets. This can be due

to poor quality and condition of the assets which would be minimised with the upgradation and

changing the assets.

Return on equity:

This ratio measure the profitability of the resort that how well it is generating profit that

would be available to the shareholder (Jati, 2020). While making an analysis of the Smart Resort

Limited it is found that the ratio in 2018 was 15.34% while in 2019 it become 11.18%. this

shows a decline in ratio i.e. the resort capability of earning the profit. It can be corrected with the

aspect of making more sales and raise the profitability.

Current ratio:

This ratio measures the liquidity of the company that how efficient the company is in

terms of making payment of its short term liability (Nuryani and Sunarsi, 2020). As the current

ratio of Smart Resort Limited in 2018 was 1.81 which decline in 2019 and become 1.63. This

shows that the Smart Resort Limited’s capability of making a repayment of its short term

liability is declining. This would be corrected with effective recovery of the cash so that adequate

funds would be available for the payment of liability.

Quick ratio:

It refers to the measurement of the company’s liquidity without making a sales of the

inventory. In case of Smart Resort Limited the quick ratio is declining because it was 0.67 in

2018 which decline and become 0.57 in 2019. This shows that the liquidity of the Smart Resort

is declining with reference to making a payment of its short term liability. This can be improved

with the aspect of making a raise in sales, improvisation of collection period and with various

other method too.

Debt to equity ratio:

It is used to make analyse the company’s leverage that analyse its financial structure in

terms of determining the proportion of debt and equity. While analysing the debt equity ratio of

Smart Resort Limited it is seen that the ratio in 2018 was 1.4 which decline in 2019 and become

0.91. this shows a decline in the ratio and leverage of the resort. This occurs because of the

raised proportion of shareholder equity which would be corrected through a focus on maintaining

a balance between the debts and equity.

Interest coverage ratio:

This ratio measure the proportionate amount of income that can be used to cover the

interest coverage in the future. in case of Smart Resort Limited the ratio is increasing because in

shows a decline in ratio i.e. the resort capability of earning the profit. It can be corrected with the

aspect of making more sales and raise the profitability.

Current ratio:

This ratio measures the liquidity of the company that how efficient the company is in

terms of making payment of its short term liability (Nuryani and Sunarsi, 2020). As the current

ratio of Smart Resort Limited in 2018 was 1.81 which decline in 2019 and become 1.63. This

shows that the Smart Resort Limited’s capability of making a repayment of its short term

liability is declining. This would be corrected with effective recovery of the cash so that adequate

funds would be available for the payment of liability.

Quick ratio:

It refers to the measurement of the company’s liquidity without making a sales of the

inventory. In case of Smart Resort Limited the quick ratio is declining because it was 0.67 in

2018 which decline and become 0.57 in 2019. This shows that the liquidity of the Smart Resort

is declining with reference to making a payment of its short term liability. This can be improved

with the aspect of making a raise in sales, improvisation of collection period and with various

other method too.

Debt to equity ratio:

It is used to make analyse the company’s leverage that analyse its financial structure in

terms of determining the proportion of debt and equity. While analysing the debt equity ratio of

Smart Resort Limited it is seen that the ratio in 2018 was 1.4 which decline in 2019 and become

0.91. this shows a decline in the ratio and leverage of the resort. This occurs because of the

raised proportion of shareholder equity which would be corrected through a focus on maintaining

a balance between the debts and equity.

Interest coverage ratio:

This ratio measure the proportionate amount of income that can be used to cover the

interest coverage in the future. in case of Smart Resort Limited the ratio is increasing because in

2018 it was 12.64 while in 2019 it become 18.63. this means that the resort is earning an

adequate percentage of income that would be used to make deal with the interest expenses. This

shows the positive performance of the resort.

Debtor collection period:

It refers to the period that would be required by the company to make a recovery of the

debt from the debtors. In case of Smart Resort Limited the ratio is declining i.e. from 12.93 of

2018 to 11.36 of 2019. This shows the efficiency of the resort in terms of making recovery of

dues from its debtor. With such ratio it would be abler to make faster recovery.

Account receivable turnover:

This ratio measures the efficiency of the company that how efficiently the company

would make recover its accounts receivables. This shows the number of time the company would

make the collection of average accounts receivable. While making an analysis of the Smart

Resort Limited it is found that the ratio was 28.21 in 2018 which become 32.11 in 2019. This

shows a rise in ratio which would further explained that the resort is performing well in terms of

making a recovery of its dues.

Performance of the resort:

While making an analysis of the performance of the Smart Resort Limited it can be said

that the financial performance of the resort is not well and it would be considered as moderate.

This is because while making a comparison of 2018 and 2019 it was found that the performance

of the resort is declining because of the poor results in the calculated ratio. At the same time this

can also be interpreted that certain ratio of the resort in the collection period, interest coverage

and various other would shows a positive result. But overall the financial performance of the

Smart Resort Limited is moderate.

In addition of this it would be made recommended to the resort that it need to make focus

over the marketing and other aspect that would lead to raise the sales of the resort so that its

profitability and various ratio would raise and improves.

adequate percentage of income that would be used to make deal with the interest expenses. This

shows the positive performance of the resort.

Debtor collection period:

It refers to the period that would be required by the company to make a recovery of the

debt from the debtors. In case of Smart Resort Limited the ratio is declining i.e. from 12.93 of

2018 to 11.36 of 2019. This shows the efficiency of the resort in terms of making recovery of

dues from its debtor. With such ratio it would be abler to make faster recovery.

Account receivable turnover:

This ratio measures the efficiency of the company that how efficiently the company

would make recover its accounts receivables. This shows the number of time the company would

make the collection of average accounts receivable. While making an analysis of the Smart

Resort Limited it is found that the ratio was 28.21 in 2018 which become 32.11 in 2019. This

shows a rise in ratio which would further explained that the resort is performing well in terms of

making a recovery of its dues.

Performance of the resort:

While making an analysis of the performance of the Smart Resort Limited it can be said

that the financial performance of the resort is not well and it would be considered as moderate.

This is because while making a comparison of 2018 and 2019 it was found that the performance

of the resort is declining because of the poor results in the calculated ratio. At the same time this

can also be interpreted that certain ratio of the resort in the collection period, interest coverage

and various other would shows a positive result. But overall the financial performance of the

Smart Resort Limited is moderate.

In addition of this it would be made recommended to the resort that it need to make focus

over the marketing and other aspect that would lead to raise the sales of the resort so that its

profitability and various ratio would raise and improves.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

CONCLUSION

From the above report it can be concluded that financial statement are important statement

of the company that would enable the financial information about the company. With the

analysis of eth financial statement, the financial health of the company would be able to get

evaluated. Likewise, ratio analysis would enable the determination of financial health of the

company in terms of measuring the performance of the company.

From the above report it can be concluded that financial statement are important statement

of the company that would enable the financial information about the company. With the

analysis of eth financial statement, the financial health of the company would be able to get

evaluated. Likewise, ratio analysis would enable the determination of financial health of the

company in terms of measuring the performance of the company.

REFERENCES

Books and journals

Ariana, I.M., Bagiada, I.M. and Sukayasa, I.K., 2018, October. User satisfaction on technical and

operational performance of spreadsheet-based financial accounting application. In 1st

International Conference on Social Sciences (ICSS 2018) (pp. 450-454). Atlantis Press.

Baker, C.R. and Persson, M.E., 2021. Principles Versus Rules-based Accounting Standards.

In Historical Developments in the Accountancy Profession, Financial Reporting, and

Accounting Theory. Emerald Publishing Limited.

Bareja, K., Gawart, M. and Giedroyc, M., 2017. Evolution of Intangible Assets Recognised in a

Statement of Financial Position. In Management Challenges in a Network Economy:

Proceedings of the MakeLearn and TIIM International Conference 2017 (pp. 481-481).

ToKnowPress.

Donelan, J.G. and Liu, Y., 2021. Using the Accounting Equation for Preparing the Statement of

Cash Flows. In Advances in Accounting Education: Teaching and Curriculum

Innovations. Emerald Publishing Limited.

Elliott, B. and Elliot, 2017. Financial Accounting and Reporting, 18th ed, Harlow: Pearson.

Guerard, J.B., Saxena, A. and Gultekin, M., 2021. The Annual Operating Statements: The

Income Statement and Cash Flow Statement. In Quantitative Corporate Finance (pp.

53-77). Springer, Cham.

Husna, A. and Satria, I., 2019. Effects of return on asset, debt to asset ratio, current ratio, firm

size, and dividend payout ratio on firm value. International Journal of Economics and

Financial Issues. 9(5). p.50.

Jati, W., 2020. Effect of Current Ratio and Return on Equity on Dividend Payout Ratio

Policy. Jurnal Ilmiah Ilmu Administrasi Publik. 10(1). pp.63-74.

Lee, T.A. and Tweedie, D.P., 2020. Shareholder Use and Understanding of Financial

Information (Vol. 38). Routledge.

Nariswari, T.N. and Nugraha, N.M., 2020. Profit Growth: Impact of Net Profit Margin, Gross

Profit Margin and Total Assests Turnover. International Journal of Finance & Banking

Studies (2147-4486), 9(4), pp.87-96.

Nuryani, Y. and Sunarsi, D., 2020. The Effect of Current Ratio and Debt to Equity Ratio on

Deviding Growth. JASa (Jurnal Akuntansi, Audit dan Sistem Informasi Akuntansi). 4(2).

pp.304-312.

Okolelova, and et.al., 2019, April. The essence of loan capital and the model of effectiveness of

its turnover. In Institute of Scientific Communications Conference (pp. 825-837).

Springer, Cham.

Smith, K., 2019. Tell me more: a content analysis of expanded auditor reporting in the United

Kingdom. Available at SSRN 2821399.

Telles, S.V., 2018. Readability and understandability of notes to the financial

statements (Doctoral dissertation, Universidade de São Paulo).

1

Books and journals

Ariana, I.M., Bagiada, I.M. and Sukayasa, I.K., 2018, October. User satisfaction on technical and

operational performance of spreadsheet-based financial accounting application. In 1st

International Conference on Social Sciences (ICSS 2018) (pp. 450-454). Atlantis Press.

Baker, C.R. and Persson, M.E., 2021. Principles Versus Rules-based Accounting Standards.

In Historical Developments in the Accountancy Profession, Financial Reporting, and

Accounting Theory. Emerald Publishing Limited.

Bareja, K., Gawart, M. and Giedroyc, M., 2017. Evolution of Intangible Assets Recognised in a

Statement of Financial Position. In Management Challenges in a Network Economy:

Proceedings of the MakeLearn and TIIM International Conference 2017 (pp. 481-481).

ToKnowPress.

Donelan, J.G. and Liu, Y., 2021. Using the Accounting Equation for Preparing the Statement of

Cash Flows. In Advances in Accounting Education: Teaching and Curriculum

Innovations. Emerald Publishing Limited.

Elliott, B. and Elliot, 2017. Financial Accounting and Reporting, 18th ed, Harlow: Pearson.

Guerard, J.B., Saxena, A. and Gultekin, M., 2021. The Annual Operating Statements: The

Income Statement and Cash Flow Statement. In Quantitative Corporate Finance (pp.

53-77). Springer, Cham.

Husna, A. and Satria, I., 2019. Effects of return on asset, debt to asset ratio, current ratio, firm

size, and dividend payout ratio on firm value. International Journal of Economics and

Financial Issues. 9(5). p.50.

Jati, W., 2020. Effect of Current Ratio and Return on Equity on Dividend Payout Ratio

Policy. Jurnal Ilmiah Ilmu Administrasi Publik. 10(1). pp.63-74.

Lee, T.A. and Tweedie, D.P., 2020. Shareholder Use and Understanding of Financial

Information (Vol. 38). Routledge.

Nariswari, T.N. and Nugraha, N.M., 2020. Profit Growth: Impact of Net Profit Margin, Gross

Profit Margin and Total Assests Turnover. International Journal of Finance & Banking

Studies (2147-4486), 9(4), pp.87-96.

Nuryani, Y. and Sunarsi, D., 2020. The Effect of Current Ratio and Debt to Equity Ratio on

Deviding Growth. JASa (Jurnal Akuntansi, Audit dan Sistem Informasi Akuntansi). 4(2).

pp.304-312.

Okolelova, and et.al., 2019, April. The essence of loan capital and the model of effectiveness of

its turnover. In Institute of Scientific Communications Conference (pp. 825-837).

Springer, Cham.

Smith, K., 2019. Tell me more: a content analysis of expanded auditor reporting in the United

Kingdom. Available at SSRN 2821399.

Telles, S.V., 2018. Readability and understandability of notes to the financial

statements (Doctoral dissertation, Universidade de São Paulo).

1

2

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.