7239AFE Financial Risk Management Project: Trimester 1, 2019

VerifiedAdded on 2023/04/08

|14

|1900

|411

Project

AI Summary

This document presents a detailed solution to a Financial Risk Management project, addressing key concepts from various modules. It includes calculations for the balance of an account over time, the amount that can be withdrawn after retirement, and the current market value of debt. The solution calculates the cost of equity, preference shares, and the weighted average cost of capital (WACC) with and without tax. Furthermore, it evaluates project profitability using ARR, payback period, NPV, and IRR, along with an EAA analysis. The project delves into currency risk, calculating profit margins at spot rates, identifying hedging needs, and exploring various hedging strategies like forward contracts, option hedging, and worst-case protection. The document also offers low-cost hedging examples and references.

Running head: FINANCIAL RISK MANAGEMENT

Financial Risk Management

Name of the Student:

Name of the University:

Authors Note:

Financial Risk Management

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL RISK MANAGEMENT

1

Table of Contents

Question 1:.................................................................................................................................3

1. Balance of the account at the end of 45 years:.......................................................................3

2. Amount of money withdraws after retirement each year:......................................................3

3. Amount of money withdraws forever after retirement each year:.........................................3

Problem 2:..................................................................................................................................3

1. Calculating current market value of the company’s debt:.....................................................3

2. Calculating cost of equity:.....................................................................................................4

3. Indicting the significance of beta:..........................................................................................4

4. Calculating cost of preference share:.....................................................................................5

5. Calculating cost of capital without tax:..................................................................................5

6. Calculating cost of capital with tax:.......................................................................................5

Problem 3:..................................................................................................................................6

1. Calculating ARR, Payback period, NPV and IRR of the project:.........................................6

2.a Calculating NPV of the project:...........................................................................................6

2.b Calculating and commenting on EAA of the both project:..................................................7

Problem 4:..................................................................................................................................7

1. Calculating the profit margin at spot rate, while finding the critical AUD/USD value and

detecting the ideal rate:..............................................................................................................7

2. Detecting the steps to analyse the needs for this company for hedging, while providing two

examples of situations in which the company does not have to hedge its FC risk:...................8

3. Identifying the risk associated with future contracts:............................................................8

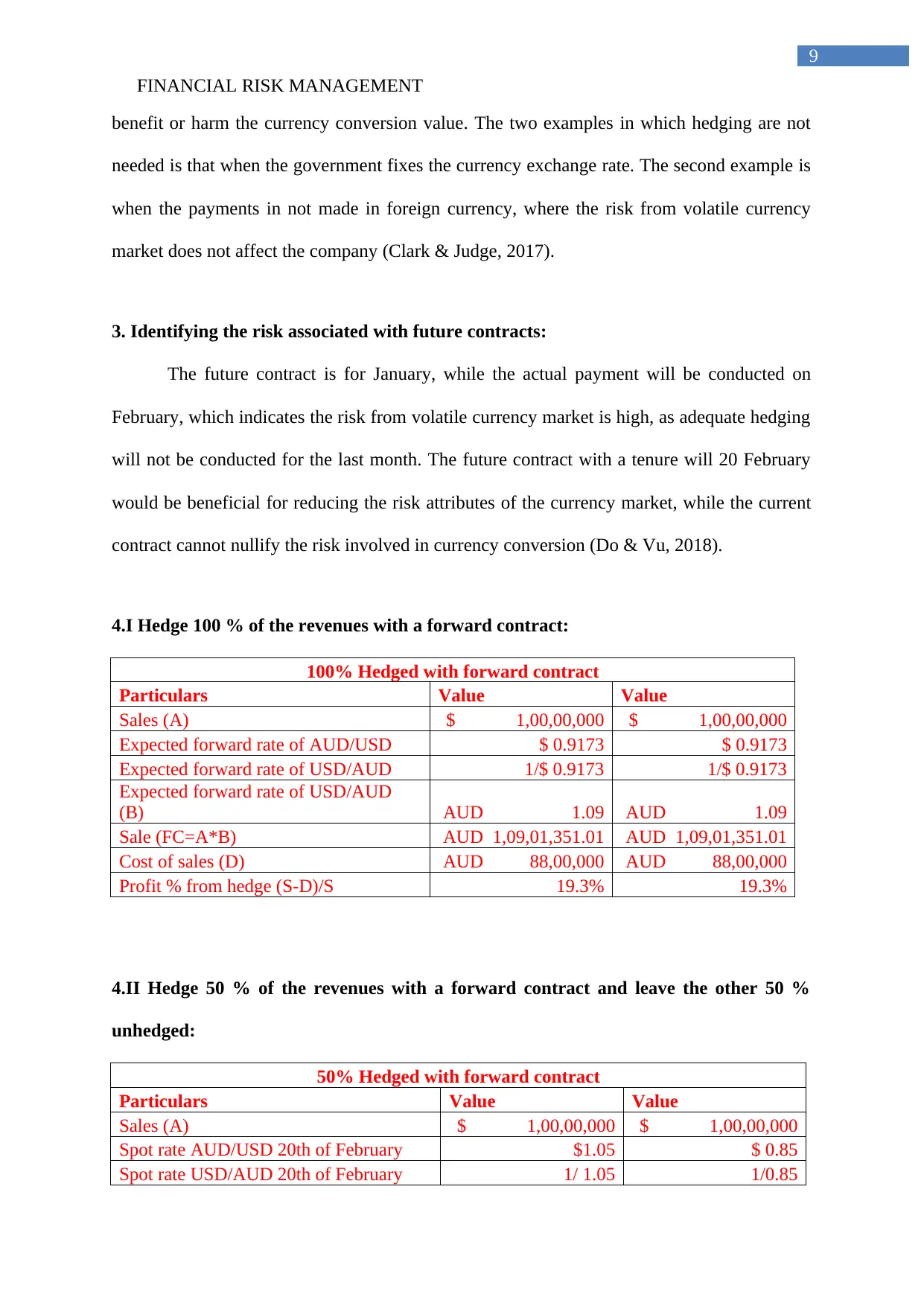

4.I Hedge 100 % of the revenues with a forward contract:........................................................9

4.II Hedge 50 % of the revenues with a forward contract and leave the other 50 % unhedged:

....................................................................................................................................................9

1

Table of Contents

Question 1:.................................................................................................................................3

1. Balance of the account at the end of 45 years:.......................................................................3

2. Amount of money withdraws after retirement each year:......................................................3

3. Amount of money withdraws forever after retirement each year:.........................................3

Problem 2:..................................................................................................................................3

1. Calculating current market value of the company’s debt:.....................................................3

2. Calculating cost of equity:.....................................................................................................4

3. Indicting the significance of beta:..........................................................................................4

4. Calculating cost of preference share:.....................................................................................5

5. Calculating cost of capital without tax:..................................................................................5

6. Calculating cost of capital with tax:.......................................................................................5

Problem 3:..................................................................................................................................6

1. Calculating ARR, Payback period, NPV and IRR of the project:.........................................6

2.a Calculating NPV of the project:...........................................................................................6

2.b Calculating and commenting on EAA of the both project:..................................................7

Problem 4:..................................................................................................................................7

1. Calculating the profit margin at spot rate, while finding the critical AUD/USD value and

detecting the ideal rate:..............................................................................................................7

2. Detecting the steps to analyse the needs for this company for hedging, while providing two

examples of situations in which the company does not have to hedge its FC risk:...................8

3. Identifying the risk associated with future contracts:............................................................8

4.I Hedge 100 % of the revenues with a forward contract:........................................................9

4.II Hedge 50 % of the revenues with a forward contract and leave the other 50 % unhedged:

....................................................................................................................................................9

FINANCIAL RISK MANAGEMENT

2

4.III Using option hedging:........................................................................................................9

4.IV Worst-case protection:.....................................................................................................10

4.V No hedge at all:.................................................................................................................10

5. Providing two examples of low-cost hedging strategies:.....................................................11

Reference and Bibliography:....................................................................................................12

2

4.III Using option hedging:........................................................................................................9

4.IV Worst-case protection:.....................................................................................................10

4.V No hedge at all:.................................................................................................................10

5. Providing two examples of low-cost hedging strategies:.....................................................11

Reference and Bibliography:....................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL RISK MANAGEMENT

3

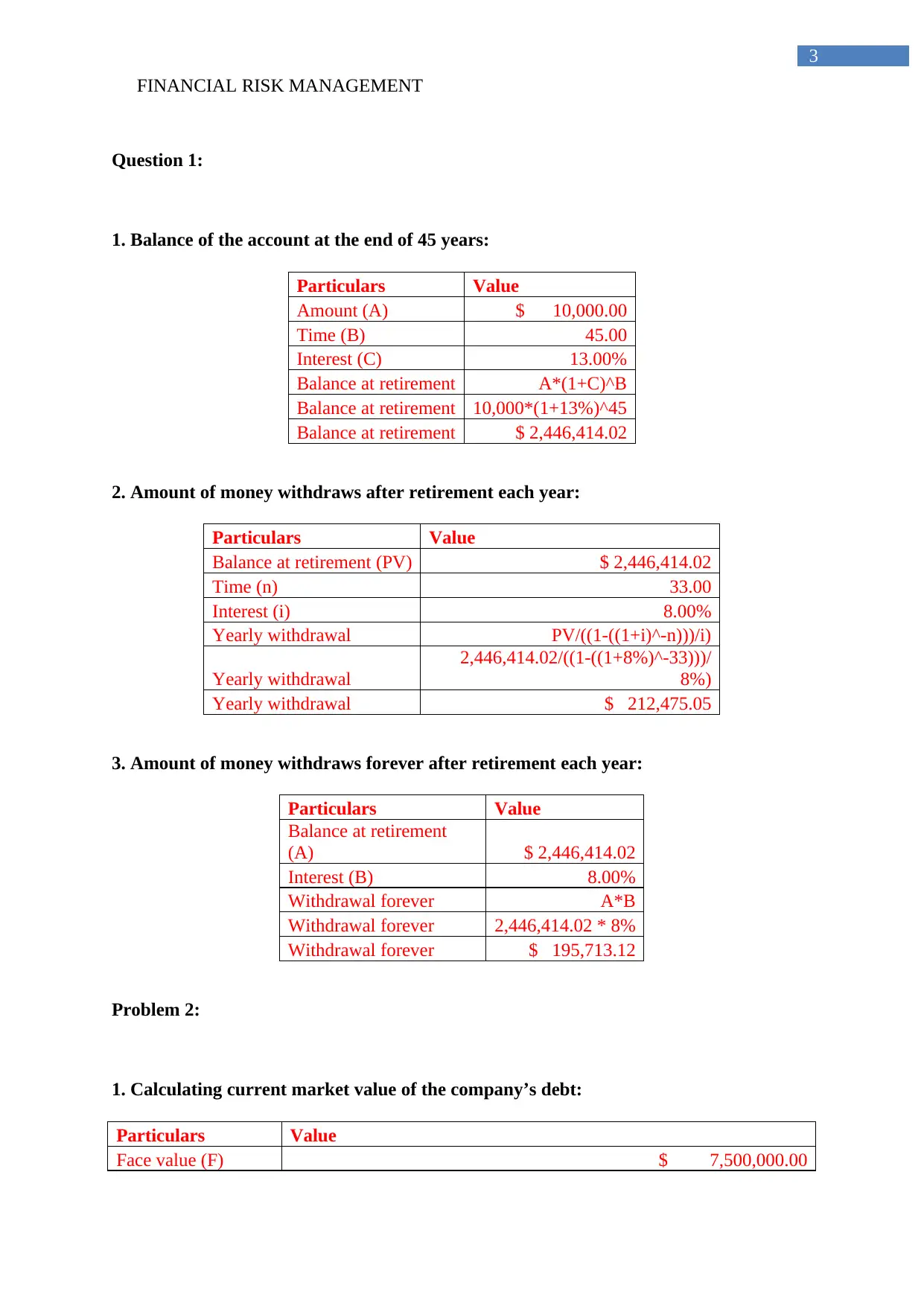

Question 1:

1. Balance of the account at the end of 45 years:

Particulars Value

Amount (A) $ 10,000.00

Time (B) 45.00

Interest (C) 13.00%

Balance at retirement A*(1+C)^B

Balance at retirement 10,000*(1+13%)^45

Balance at retirement $ 2,446,414.02

2. Amount of money withdraws after retirement each year:

Particulars Value

Balance at retirement (PV) $ 2,446,414.02

Time (n) 33.00

Interest (i) 8.00%

Yearly withdrawal PV/((1-((1+i)^-n)))/i)

Yearly withdrawal

2,446,414.02/((1-((1+8%)^-33)))/

8%)

Yearly withdrawal $ 212,475.05

3. Amount of money withdraws forever after retirement each year:

Particulars Value

Balance at retirement

(A) $ 2,446,414.02

Interest (B) 8.00%

Withdrawal forever A*B

Withdrawal forever 2,446,414.02 * 8%

Withdrawal forever $ 195,713.12

Problem 2:

1. Calculating current market value of the company’s debt:

Particulars Value

Face value (F) $ 7,500,000.00

3

Question 1:

1. Balance of the account at the end of 45 years:

Particulars Value

Amount (A) $ 10,000.00

Time (B) 45.00

Interest (C) 13.00%

Balance at retirement A*(1+C)^B

Balance at retirement 10,000*(1+13%)^45

Balance at retirement $ 2,446,414.02

2. Amount of money withdraws after retirement each year:

Particulars Value

Balance at retirement (PV) $ 2,446,414.02

Time (n) 33.00

Interest (i) 8.00%

Yearly withdrawal PV/((1-((1+i)^-n)))/i)

Yearly withdrawal

2,446,414.02/((1-((1+8%)^-33)))/

8%)

Yearly withdrawal $ 212,475.05

3. Amount of money withdraws forever after retirement each year:

Particulars Value

Balance at retirement

(A) $ 2,446,414.02

Interest (B) 8.00%

Withdrawal forever A*B

Withdrawal forever 2,446,414.02 * 8%

Withdrawal forever $ 195,713.12

Problem 2:

1. Calculating current market value of the company’s debt:

Particulars Value

Face value (F) $ 7,500,000.00

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL RISK MANAGEMENT

4

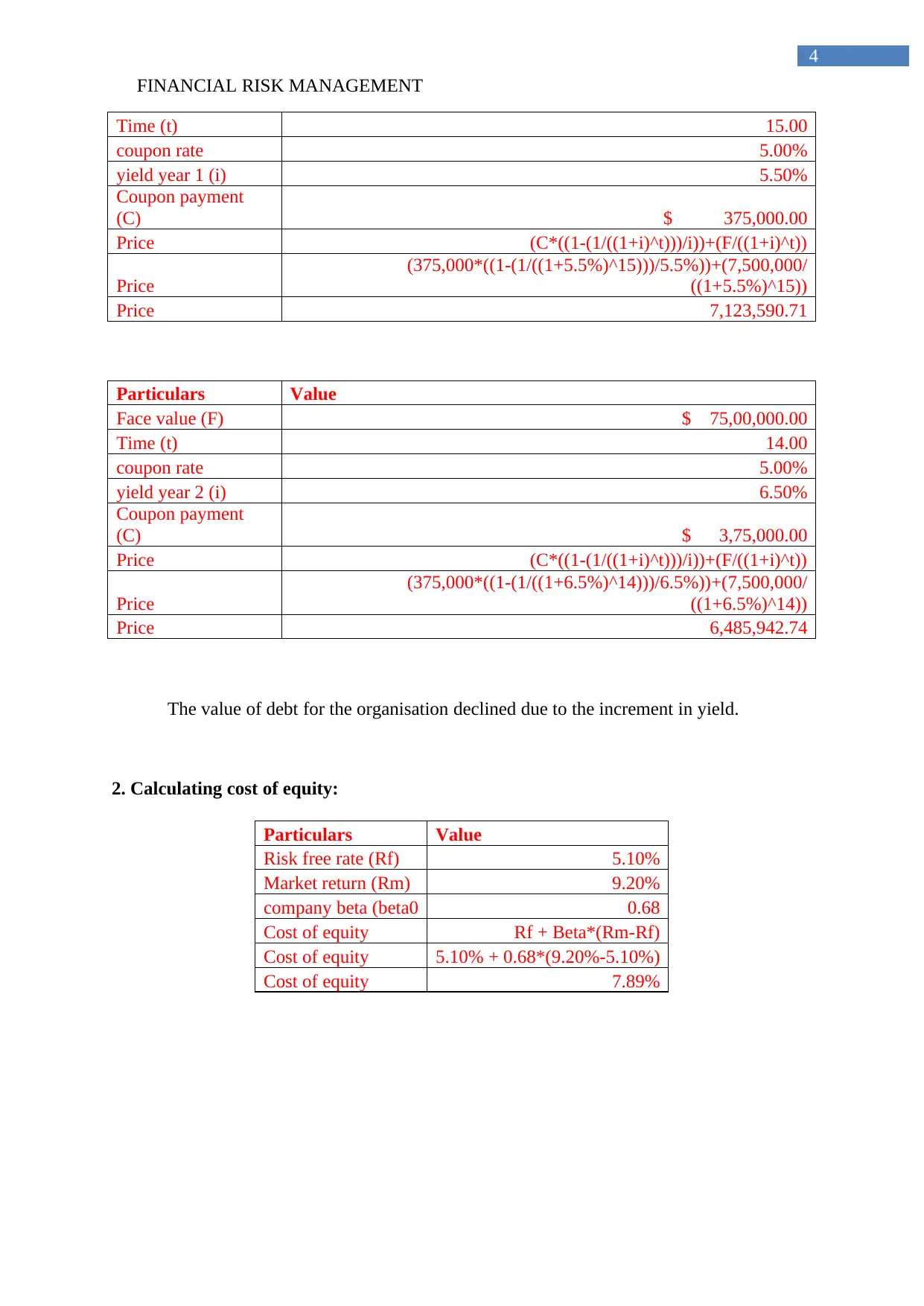

Time (t) 15.00

coupon rate 5.00%

yield year 1 (i) 5.50%

Coupon payment

(C) $ 375,000.00

Price (C*((1-(1/((1+i)^t)))/i))+(F/((1+i)^t))

Price

(375,000*((1-(1/((1+5.5%)^15)))/5.5%))+(7,500,000/

((1+5.5%)^15))

Price 7,123,590.71

Particulars Value

Face value (F) $ 75,00,000.00

Time (t) 14.00

coupon rate 5.00%

yield year 2 (i) 6.50%

Coupon payment

(C) $ 3,75,000.00

Price (C*((1-(1/((1+i)^t)))/i))+(F/((1+i)^t))

Price

(375,000*((1-(1/((1+6.5%)^14)))/6.5%))+(7,500,000/

((1+6.5%)^14))

Price 6,485,942.74

The value of debt for the organisation declined due to the increment in yield.

2. Calculating cost of equity:

Particulars Value

Risk free rate (Rf) 5.10%

Market return (Rm) 9.20%

company beta (beta0 0.68

Cost of equity Rf + Beta*(Rm-Rf)

Cost of equity 5.10% + 0.68*(9.20%-5.10%)

Cost of equity 7.89%

4

Time (t) 15.00

coupon rate 5.00%

yield year 1 (i) 5.50%

Coupon payment

(C) $ 375,000.00

Price (C*((1-(1/((1+i)^t)))/i))+(F/((1+i)^t))

Price

(375,000*((1-(1/((1+5.5%)^15)))/5.5%))+(7,500,000/

((1+5.5%)^15))

Price 7,123,590.71

Particulars Value

Face value (F) $ 75,00,000.00

Time (t) 14.00

coupon rate 5.00%

yield year 2 (i) 6.50%

Coupon payment

(C) $ 3,75,000.00

Price (C*((1-(1/((1+i)^t)))/i))+(F/((1+i)^t))

Price

(375,000*((1-(1/((1+6.5%)^14)))/6.5%))+(7,500,000/

((1+6.5%)^14))

Price 6,485,942.74

The value of debt for the organisation declined due to the increment in yield.

2. Calculating cost of equity:

Particulars Value

Risk free rate (Rf) 5.10%

Market return (Rm) 9.20%

company beta (beta0 0.68

Cost of equity Rf + Beta*(Rm-Rf)

Cost of equity 5.10% + 0.68*(9.20%-5.10%)

Cost of equity 7.89%

FINANCIAL RISK MANAGEMENT

5

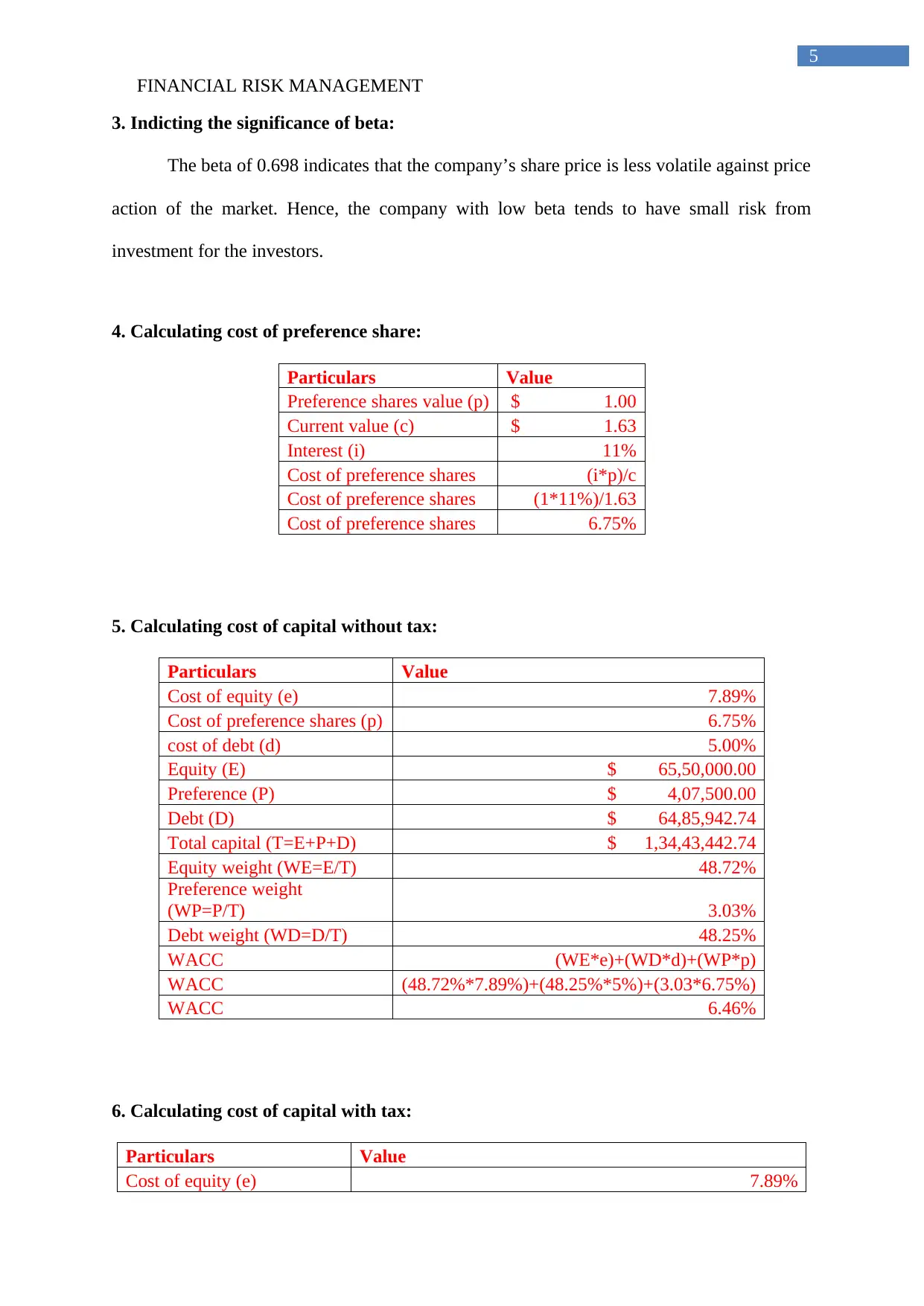

3. Indicting the significance of beta:

The beta of 0.698 indicates that the company’s share price is less volatile against price

action of the market. Hence, the company with low beta tends to have small risk from

investment for the investors.

4. Calculating cost of preference share:

Particulars Value

Preference shares value (p) $ 1.00

Current value (c) $ 1.63

Interest (i) 11%

Cost of preference shares (i*p)/c

Cost of preference shares (1*11%)/1.63

Cost of preference shares 6.75%

5. Calculating cost of capital without tax:

Particulars Value

Cost of equity (e) 7.89%

Cost of preference shares (p) 6.75%

cost of debt (d) 5.00%

Equity (E) $ 65,50,000.00

Preference (P) $ 4,07,500.00

Debt (D) $ 64,85,942.74

Total capital (T=E+P+D) $ 1,34,43,442.74

Equity weight (WE=E/T) 48.72%

Preference weight

(WP=P/T) 3.03%

Debt weight (WD=D/T) 48.25%

WACC (WE*e)+(WD*d)+(WP*p)

WACC (48.72%*7.89%)+(48.25%*5%)+(3.03*6.75%)

WACC 6.46%

6. Calculating cost of capital with tax:

Particulars Value

Cost of equity (e) 7.89%

5

3. Indicting the significance of beta:

The beta of 0.698 indicates that the company’s share price is less volatile against price

action of the market. Hence, the company with low beta tends to have small risk from

investment for the investors.

4. Calculating cost of preference share:

Particulars Value

Preference shares value (p) $ 1.00

Current value (c) $ 1.63

Interest (i) 11%

Cost of preference shares (i*p)/c

Cost of preference shares (1*11%)/1.63

Cost of preference shares 6.75%

5. Calculating cost of capital without tax:

Particulars Value

Cost of equity (e) 7.89%

Cost of preference shares (p) 6.75%

cost of debt (d) 5.00%

Equity (E) $ 65,50,000.00

Preference (P) $ 4,07,500.00

Debt (D) $ 64,85,942.74

Total capital (T=E+P+D) $ 1,34,43,442.74

Equity weight (WE=E/T) 48.72%

Preference weight

(WP=P/T) 3.03%

Debt weight (WD=D/T) 48.25%

WACC (WE*e)+(WD*d)+(WP*p)

WACC (48.72%*7.89%)+(48.25%*5%)+(3.03*6.75%)

WACC 6.46%

6. Calculating cost of capital with tax:

Particulars Value

Cost of equity (e) 7.89%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL RISK MANAGEMENT

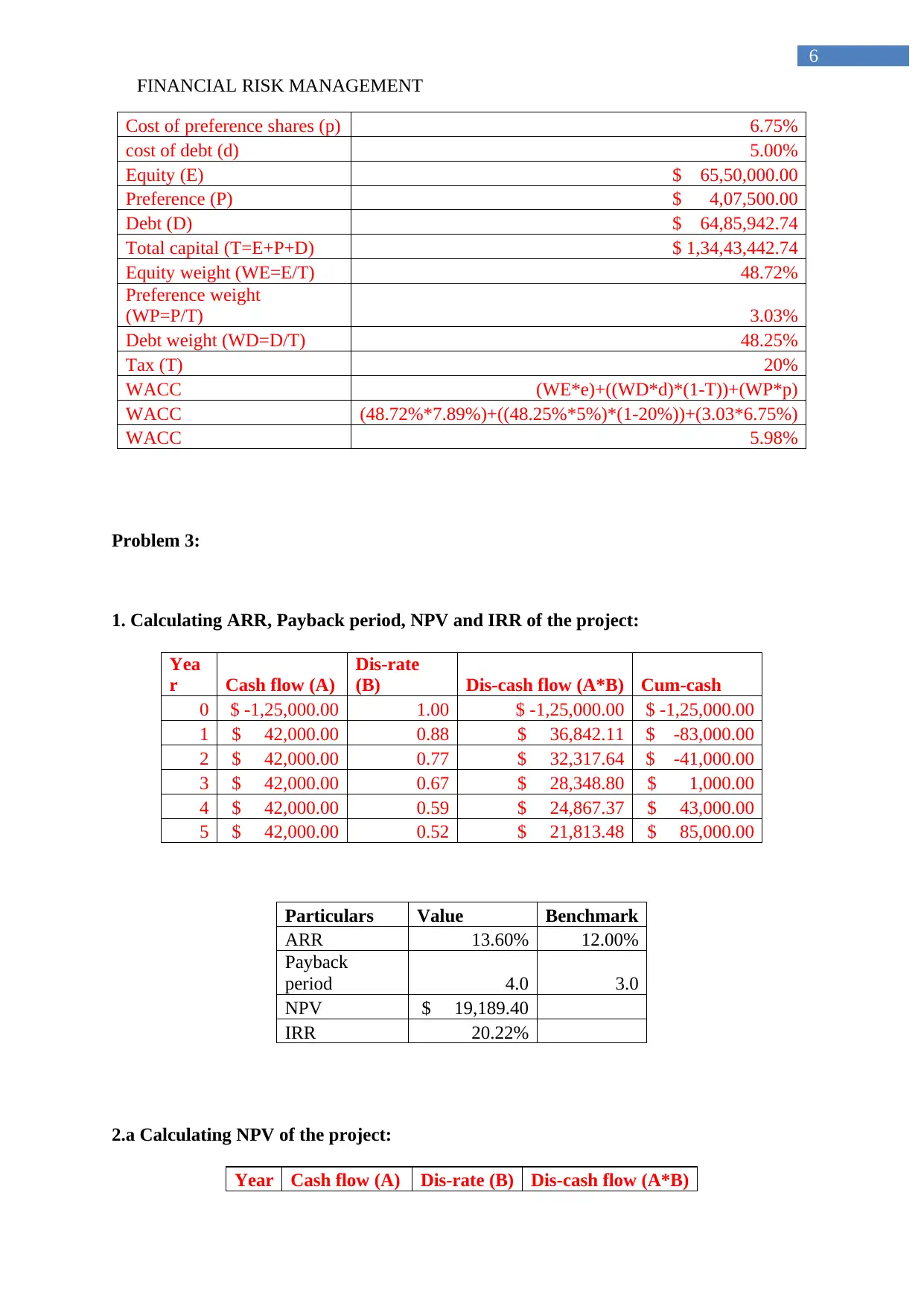

6

Cost of preference shares (p) 6.75%

cost of debt (d) 5.00%

Equity (E) $ 65,50,000.00

Preference (P) $ 4,07,500.00

Debt (D) $ 64,85,942.74

Total capital (T=E+P+D) $ 1,34,43,442.74

Equity weight (WE=E/T) 48.72%

Preference weight

(WP=P/T) 3.03%

Debt weight (WD=D/T) 48.25%

Tax (T) 20%

WACC (WE*e)+((WD*d)*(1-T))+(WP*p)

WACC (48.72%*7.89%)+((48.25%*5%)*(1-20%))+(3.03*6.75%)

WACC 5.98%

Problem 3:

1. Calculating ARR, Payback period, NPV and IRR of the project:

Yea

r Cash flow (A)

Dis-rate

(B) Dis-cash flow (A*B) Cum-cash

0 $ -1,25,000.00 1.00 $ -1,25,000.00 $ -1,25,000.00

1 $ 42,000.00 0.88 $ 36,842.11 $ -83,000.00

2 $ 42,000.00 0.77 $ 32,317.64 $ -41,000.00

3 $ 42,000.00 0.67 $ 28,348.80 $ 1,000.00

4 $ 42,000.00 0.59 $ 24,867.37 $ 43,000.00

5 $ 42,000.00 0.52 $ 21,813.48 $ 85,000.00

Particulars Value Benchmark

ARR 13.60% 12.00%

Payback

period 4.0 3.0

NPV $ 19,189.40

IRR 20.22%

2.a Calculating NPV of the project:

Year Cash flow (A) Dis-rate (B) Dis-cash flow (A*B)

6

Cost of preference shares (p) 6.75%

cost of debt (d) 5.00%

Equity (E) $ 65,50,000.00

Preference (P) $ 4,07,500.00

Debt (D) $ 64,85,942.74

Total capital (T=E+P+D) $ 1,34,43,442.74

Equity weight (WE=E/T) 48.72%

Preference weight

(WP=P/T) 3.03%

Debt weight (WD=D/T) 48.25%

Tax (T) 20%

WACC (WE*e)+((WD*d)*(1-T))+(WP*p)

WACC (48.72%*7.89%)+((48.25%*5%)*(1-20%))+(3.03*6.75%)

WACC 5.98%

Problem 3:

1. Calculating ARR, Payback period, NPV and IRR of the project:

Yea

r Cash flow (A)

Dis-rate

(B) Dis-cash flow (A*B) Cum-cash

0 $ -1,25,000.00 1.00 $ -1,25,000.00 $ -1,25,000.00

1 $ 42,000.00 0.88 $ 36,842.11 $ -83,000.00

2 $ 42,000.00 0.77 $ 32,317.64 $ -41,000.00

3 $ 42,000.00 0.67 $ 28,348.80 $ 1,000.00

4 $ 42,000.00 0.59 $ 24,867.37 $ 43,000.00

5 $ 42,000.00 0.52 $ 21,813.48 $ 85,000.00

Particulars Value Benchmark

ARR 13.60% 12.00%

Payback

period 4.0 3.0

NPV $ 19,189.40

IRR 20.22%

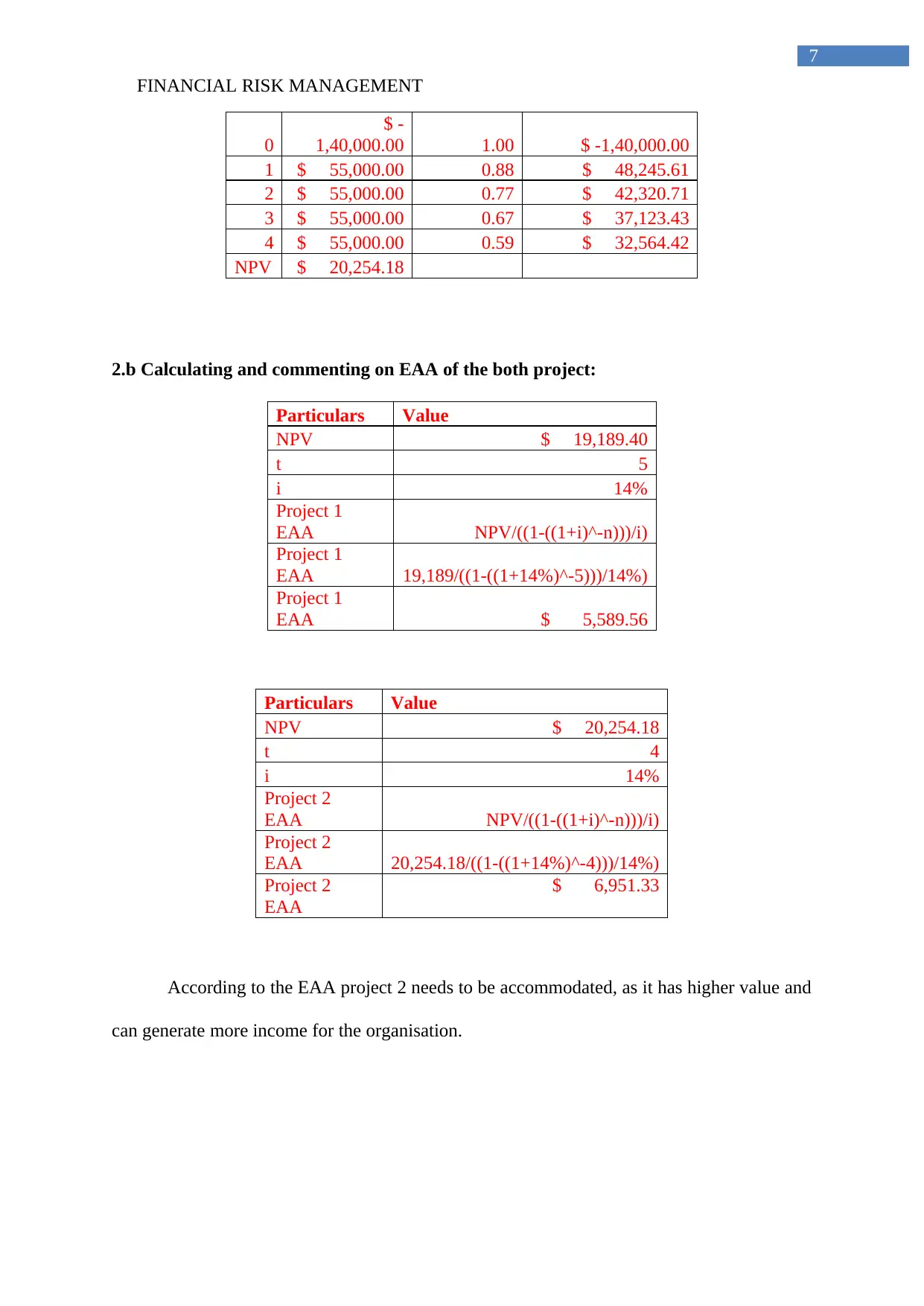

2.a Calculating NPV of the project:

Year Cash flow (A) Dis-rate (B) Dis-cash flow (A*B)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL RISK MANAGEMENT

7

0

$ -

1,40,000.00 1.00 $ -1,40,000.00

1 $ 55,000.00 0.88 $ 48,245.61

2 $ 55,000.00 0.77 $ 42,320.71

3 $ 55,000.00 0.67 $ 37,123.43

4 $ 55,000.00 0.59 $ 32,564.42

NPV $ 20,254.18

2.b Calculating and commenting on EAA of the both project:

Particulars Value

NPV $ 19,189.40

t 5

i 14%

Project 1

EAA NPV/((1-((1+i)^-n)))/i)

Project 1

EAA 19,189/((1-((1+14%)^-5)))/14%)

Project 1

EAA $ 5,589.56

Particulars Value

NPV $ 20,254.18

t 4

i 14%

Project 2

EAA NPV/((1-((1+i)^-n)))/i)

Project 2

EAA 20,254.18/((1-((1+14%)^-4)))/14%)

Project 2

EAA

$ 6,951.33

According to the EAA project 2 needs to be accommodated, as it has higher value and

can generate more income for the organisation.

7

0

$ -

1,40,000.00 1.00 $ -1,40,000.00

1 $ 55,000.00 0.88 $ 48,245.61

2 $ 55,000.00 0.77 $ 42,320.71

3 $ 55,000.00 0.67 $ 37,123.43

4 $ 55,000.00 0.59 $ 32,564.42

NPV $ 20,254.18

2.b Calculating and commenting on EAA of the both project:

Particulars Value

NPV $ 19,189.40

t 5

i 14%

Project 1

EAA NPV/((1-((1+i)^-n)))/i)

Project 1

EAA 19,189/((1-((1+14%)^-5)))/14%)

Project 1

EAA $ 5,589.56

Particulars Value

NPV $ 20,254.18

t 4

i 14%

Project 2

EAA NPV/((1-((1+i)^-n)))/i)

Project 2

EAA 20,254.18/((1-((1+14%)^-4)))/14%)

Project 2

EAA

$ 6,951.33

According to the EAA project 2 needs to be accommodated, as it has higher value and

can generate more income for the organisation.

FINANCIAL RISK MANAGEMENT

8

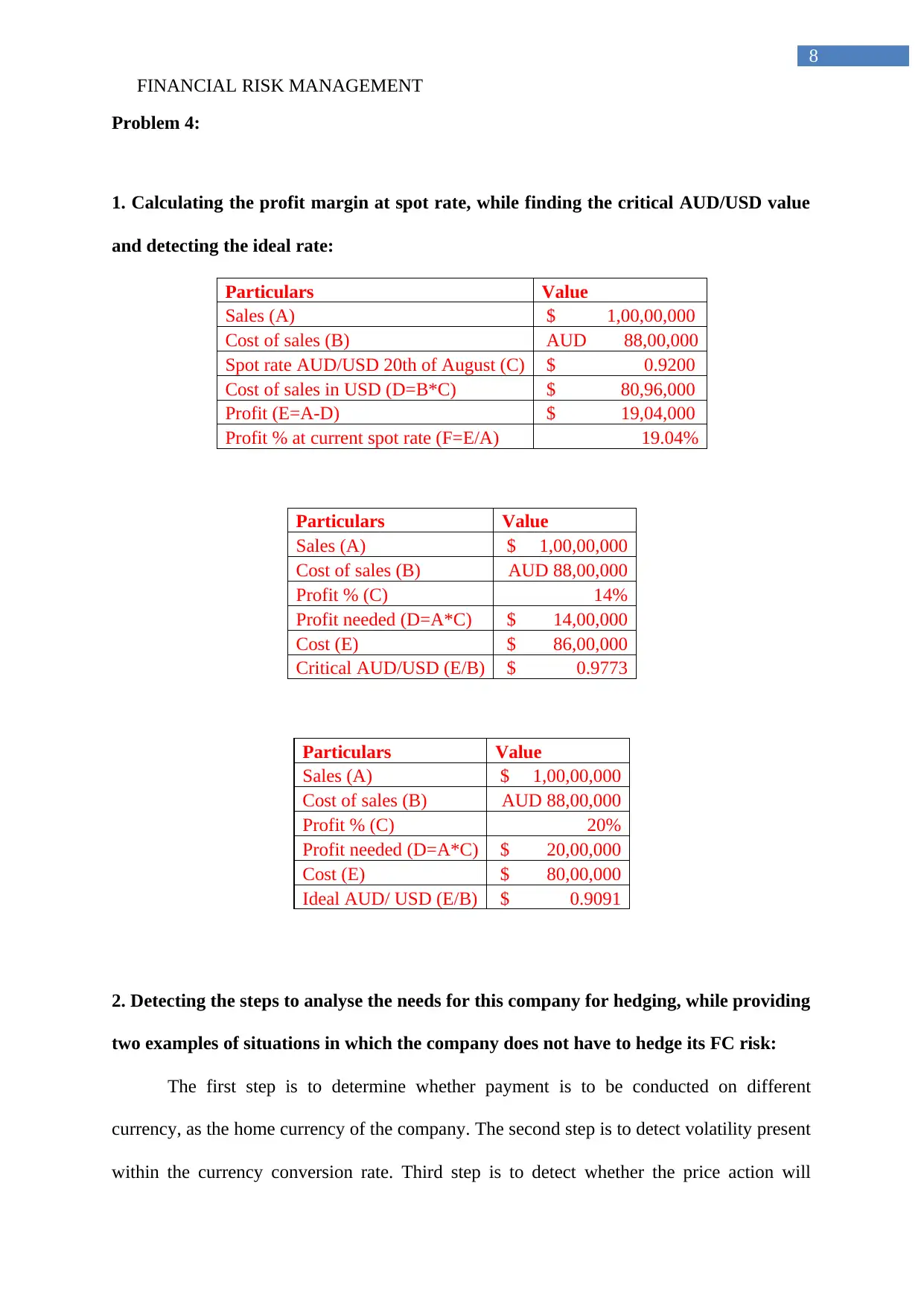

Problem 4:

1. Calculating the profit margin at spot rate, while finding the critical AUD/USD value

and detecting the ideal rate:

Particulars Value

Sales (A) $ 1,00,00,000

Cost of sales (B) AUD 88,00,000

Spot rate AUD/USD 20th of August (C) $ 0.9200

Cost of sales in USD (D=B*C) $ 80,96,000

Profit (E=A-D) $ 19,04,000

Profit % at current spot rate (F=E/A) 19.04%

Particulars Value

Sales (A) $ 1,00,00,000

Cost of sales (B) AUD 88,00,000

Profit % (C) 14%

Profit needed (D=A*C) $ 14,00,000

Cost (E) $ 86,00,000

Critical AUD/USD (E/B) $ 0.9773

Particulars Value

Sales (A) $ 1,00,00,000

Cost of sales (B) AUD 88,00,000

Profit % (C) 20%

Profit needed (D=A*C) $ 20,00,000

Cost (E) $ 80,00,000

Ideal AUD/ USD (E/B) $ 0.9091

2. Detecting the steps to analyse the needs for this company for hedging, while providing

two examples of situations in which the company does not have to hedge its FC risk:

The first step is to determine whether payment is to be conducted on different

currency, as the home currency of the company. The second step is to detect volatility present

within the currency conversion rate. Third step is to detect whether the price action will

8

Problem 4:

1. Calculating the profit margin at spot rate, while finding the critical AUD/USD value

and detecting the ideal rate:

Particulars Value

Sales (A) $ 1,00,00,000

Cost of sales (B) AUD 88,00,000

Spot rate AUD/USD 20th of August (C) $ 0.9200

Cost of sales in USD (D=B*C) $ 80,96,000

Profit (E=A-D) $ 19,04,000

Profit % at current spot rate (F=E/A) 19.04%

Particulars Value

Sales (A) $ 1,00,00,000

Cost of sales (B) AUD 88,00,000

Profit % (C) 14%

Profit needed (D=A*C) $ 14,00,000

Cost (E) $ 86,00,000

Critical AUD/USD (E/B) $ 0.9773

Particulars Value

Sales (A) $ 1,00,00,000

Cost of sales (B) AUD 88,00,000

Profit % (C) 20%

Profit needed (D=A*C) $ 20,00,000

Cost (E) $ 80,00,000

Ideal AUD/ USD (E/B) $ 0.9091

2. Detecting the steps to analyse the needs for this company for hedging, while providing

two examples of situations in which the company does not have to hedge its FC risk:

The first step is to determine whether payment is to be conducted on different

currency, as the home currency of the company. The second step is to detect volatility present

within the currency conversion rate. Third step is to detect whether the price action will

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCIAL RISK MANAGEMENT

9

benefit or harm the currency conversion value. The two examples in which hedging are not

needed is that when the government fixes the currency exchange rate. The second example is

when the payments in not made in foreign currency, where the risk from volatile currency

market does not affect the company (Clark & Judge, 2017).

3. Identifying the risk associated with future contracts:

The future contract is for January, while the actual payment will be conducted on

February, which indicates the risk from volatile currency market is high, as adequate hedging

will not be conducted for the last month. The future contract with a tenure will 20 February

would be beneficial for reducing the risk attributes of the currency market, while the current

contract cannot nullify the risk involved in currency conversion (Do & Vu, 2018).

4.I Hedge 100 % of the revenues with a forward contract:

100% Hedged with forward contract

Particulars Value Value

Sales (A) $ 1,00,00,000 $ 1,00,00,000

Expected forward rate of AUD/USD $ 0.9173 $ 0.9173

Expected forward rate of USD/AUD 1/$ 0.9173 1/$ 0.9173

Expected forward rate of USD/AUD

(B) AUD 1.09 AUD 1.09

Sale (FC=A*B) AUD 1,09,01,351.01 AUD 1,09,01,351.01

Cost of sales (D) AUD 88,00,000 AUD 88,00,000

Profit % from hedge (S-D)/S 19.3% 19.3%

4.II Hedge 50 % of the revenues with a forward contract and leave the other 50 %

unhedged:

50% Hedged with forward contract

Particulars Value Value

Sales (A) $ 1,00,00,000 $ 1,00,00,000

Spot rate AUD/USD 20th of February $1.05 $ 0.85

Spot rate USD/AUD 20th of February 1/ 1.05 1/0.85

9

benefit or harm the currency conversion value. The two examples in which hedging are not

needed is that when the government fixes the currency exchange rate. The second example is

when the payments in not made in foreign currency, where the risk from volatile currency

market does not affect the company (Clark & Judge, 2017).

3. Identifying the risk associated with future contracts:

The future contract is for January, while the actual payment will be conducted on

February, which indicates the risk from volatile currency market is high, as adequate hedging

will not be conducted for the last month. The future contract with a tenure will 20 February

would be beneficial for reducing the risk attributes of the currency market, while the current

contract cannot nullify the risk involved in currency conversion (Do & Vu, 2018).

4.I Hedge 100 % of the revenues with a forward contract:

100% Hedged with forward contract

Particulars Value Value

Sales (A) $ 1,00,00,000 $ 1,00,00,000

Expected forward rate of AUD/USD $ 0.9173 $ 0.9173

Expected forward rate of USD/AUD 1/$ 0.9173 1/$ 0.9173

Expected forward rate of USD/AUD

(B) AUD 1.09 AUD 1.09

Sale (FC=A*B) AUD 1,09,01,351.01 AUD 1,09,01,351.01

Cost of sales (D) AUD 88,00,000 AUD 88,00,000

Profit % from hedge (S-D)/S 19.3% 19.3%

4.II Hedge 50 % of the revenues with a forward contract and leave the other 50 %

unhedged:

50% Hedged with forward contract

Particulars Value Value

Sales (A) $ 1,00,00,000 $ 1,00,00,000

Spot rate AUD/USD 20th of February $1.05 $ 0.85

Spot rate USD/AUD 20th of February 1/ 1.05 1/0.85

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL RISK MANAGEMENT

10

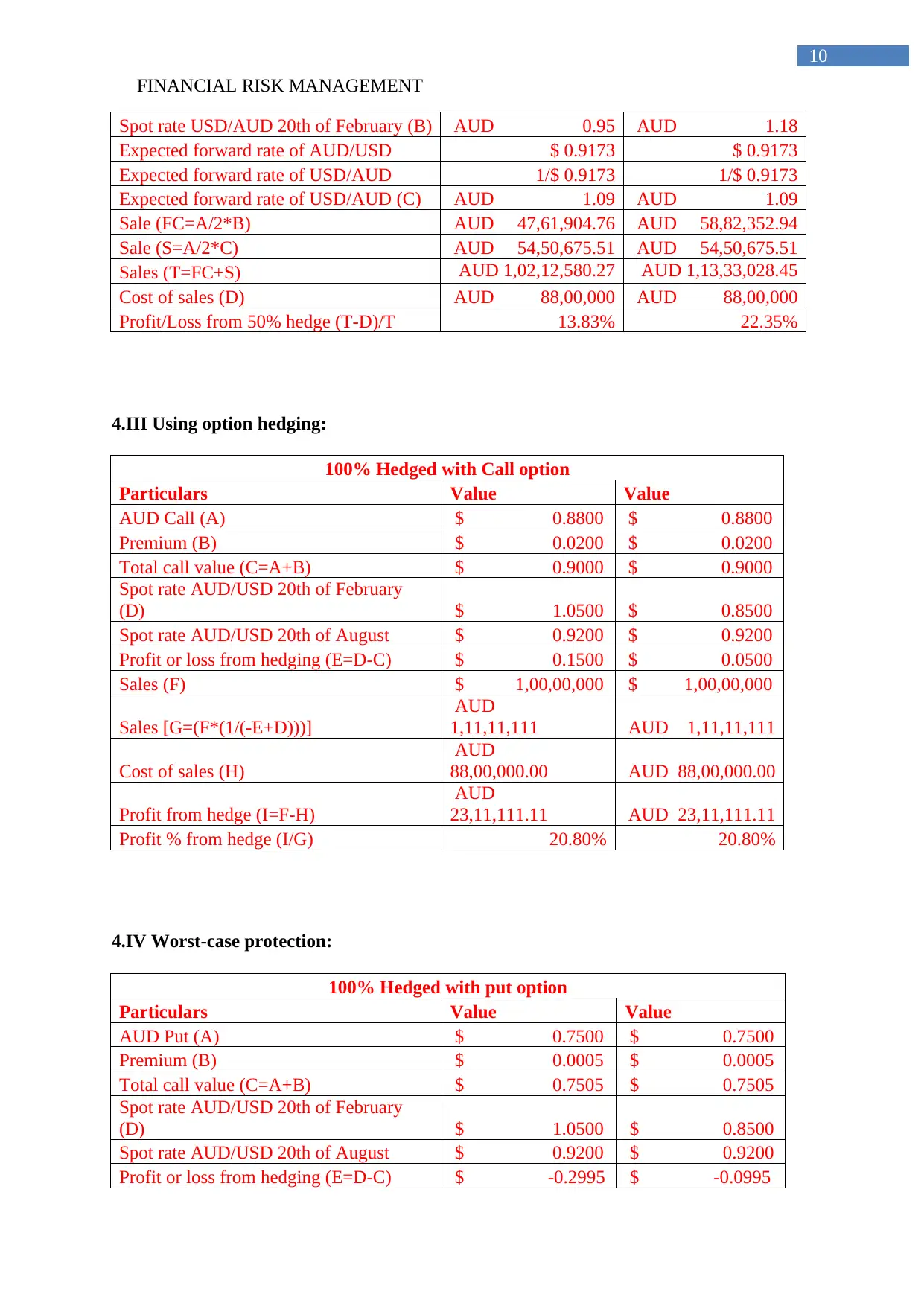

Spot rate USD/AUD 20th of February (B) AUD 0.95 AUD 1.18

Expected forward rate of AUD/USD $ 0.9173 $ 0.9173

Expected forward rate of USD/AUD 1/$ 0.9173 1/$ 0.9173

Expected forward rate of USD/AUD (C) AUD 1.09 AUD 1.09

Sale (FC=A/2*B) AUD 47,61,904.76 AUD 58,82,352.94

Sale (S=A/2*C) AUD 54,50,675.51 AUD 54,50,675.51

Sales (T=FC+S) AUD 1,02,12,580.27 AUD 1,13,33,028.45

Cost of sales (D) AUD 88,00,000 AUD 88,00,000

Profit/Loss from 50% hedge (T-D)/T 13.83% 22.35%

4.III Using option hedging:

100% Hedged with Call option

Particulars Value Value

AUD Call (A) $ 0.8800 $ 0.8800

Premium (B) $ 0.0200 $ 0.0200

Total call value (C=A+B) $ 0.9000 $ 0.9000

Spot rate AUD/USD 20th of February

(D) $ 1.0500 $ 0.8500

Spot rate AUD/USD 20th of August $ 0.9200 $ 0.9200

Profit or loss from hedging (E=D-C) $ 0.1500 $ 0.0500

Sales (F) $ 1,00,00,000 $ 1,00,00,000

Sales [G=(F*(1/(-E+D)))]

AUD

1,11,11,111 AUD 1,11,11,111

Cost of sales (H)

AUD

88,00,000.00 AUD 88,00,000.00

Profit from hedge (I=F-H)

AUD

23,11,111.11 AUD 23,11,111.11

Profit % from hedge (I/G) 20.80% 20.80%

4.IV Worst-case protection:

100% Hedged with put option

Particulars Value Value

AUD Put (A) $ 0.7500 $ 0.7500

Premium (B) $ 0.0005 $ 0.0005

Total call value (C=A+B) $ 0.7505 $ 0.7505

Spot rate AUD/USD 20th of February

(D) $ 1.0500 $ 0.8500

Spot rate AUD/USD 20th of August $ 0.9200 $ 0.9200

Profit or loss from hedging (E=D-C) $ -0.2995 $ -0.0995

10

Spot rate USD/AUD 20th of February (B) AUD 0.95 AUD 1.18

Expected forward rate of AUD/USD $ 0.9173 $ 0.9173

Expected forward rate of USD/AUD 1/$ 0.9173 1/$ 0.9173

Expected forward rate of USD/AUD (C) AUD 1.09 AUD 1.09

Sale (FC=A/2*B) AUD 47,61,904.76 AUD 58,82,352.94

Sale (S=A/2*C) AUD 54,50,675.51 AUD 54,50,675.51

Sales (T=FC+S) AUD 1,02,12,580.27 AUD 1,13,33,028.45

Cost of sales (D) AUD 88,00,000 AUD 88,00,000

Profit/Loss from 50% hedge (T-D)/T 13.83% 22.35%

4.III Using option hedging:

100% Hedged with Call option

Particulars Value Value

AUD Call (A) $ 0.8800 $ 0.8800

Premium (B) $ 0.0200 $ 0.0200

Total call value (C=A+B) $ 0.9000 $ 0.9000

Spot rate AUD/USD 20th of February

(D) $ 1.0500 $ 0.8500

Spot rate AUD/USD 20th of August $ 0.9200 $ 0.9200

Profit or loss from hedging (E=D-C) $ 0.1500 $ 0.0500

Sales (F) $ 1,00,00,000 $ 1,00,00,000

Sales [G=(F*(1/(-E+D)))]

AUD

1,11,11,111 AUD 1,11,11,111

Cost of sales (H)

AUD

88,00,000.00 AUD 88,00,000.00

Profit from hedge (I=F-H)

AUD

23,11,111.11 AUD 23,11,111.11

Profit % from hedge (I/G) 20.80% 20.80%

4.IV Worst-case protection:

100% Hedged with put option

Particulars Value Value

AUD Put (A) $ 0.7500 $ 0.7500

Premium (B) $ 0.0005 $ 0.0005

Total call value (C=A+B) $ 0.7505 $ 0.7505

Spot rate AUD/USD 20th of February

(D) $ 1.0500 $ 0.8500

Spot rate AUD/USD 20th of August $ 0.9200 $ 0.9200

Profit or loss from hedging (E=D-C) $ -0.2995 $ -0.0995

FINANCIAL RISK MANAGEMENT

11

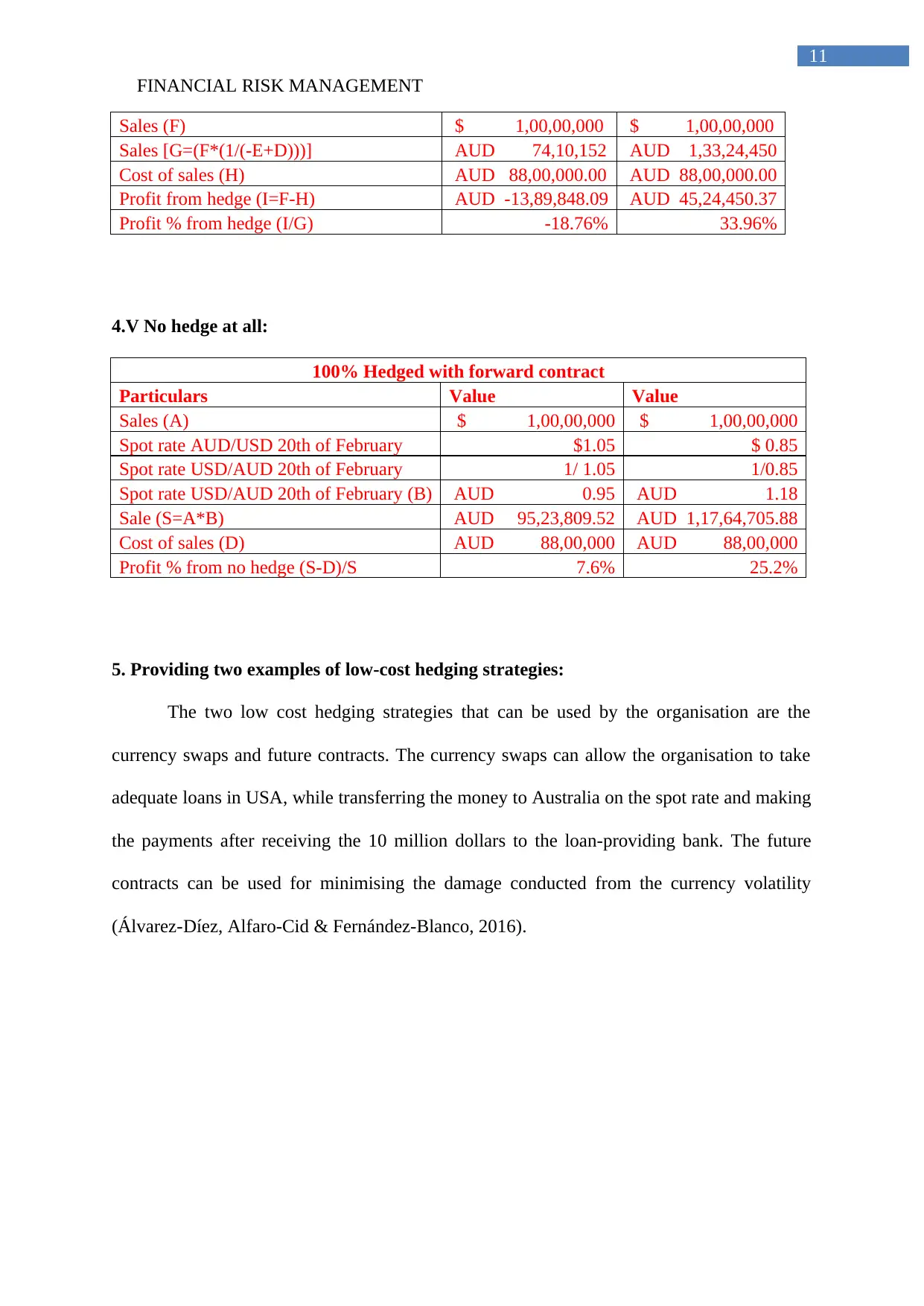

Sales (F) $ 1,00,00,000 $ 1,00,00,000

Sales [G=(F*(1/(-E+D)))] AUD 74,10,152 AUD 1,33,24,450

Cost of sales (H) AUD 88,00,000.00 AUD 88,00,000.00

Profit from hedge (I=F-H) AUD -13,89,848.09 AUD 45,24,450.37

Profit % from hedge (I/G) -18.76% 33.96%

4.V No hedge at all:

100% Hedged with forward contract

Particulars Value Value

Sales (A) $ 1,00,00,000 $ 1,00,00,000

Spot rate AUD/USD 20th of February $1.05 $ 0.85

Spot rate USD/AUD 20th of February 1/ 1.05 1/0.85

Spot rate USD/AUD 20th of February (B) AUD 0.95 AUD 1.18

Sale (S=A*B) AUD 95,23,809.52 AUD 1,17,64,705.88

Cost of sales (D) AUD 88,00,000 AUD 88,00,000

Profit % from no hedge (S-D)/S 7.6% 25.2%

5. Providing two examples of low-cost hedging strategies:

The two low cost hedging strategies that can be used by the organisation are the

currency swaps and future contracts. The currency swaps can allow the organisation to take

adequate loans in USA, while transferring the money to Australia on the spot rate and making

the payments after receiving the 10 million dollars to the loan-providing bank. The future

contracts can be used for minimising the damage conducted from the currency volatility

(Álvarez-Díez, Alfaro-Cid & Fernández-Blanco, 2016).

11

Sales (F) $ 1,00,00,000 $ 1,00,00,000

Sales [G=(F*(1/(-E+D)))] AUD 74,10,152 AUD 1,33,24,450

Cost of sales (H) AUD 88,00,000.00 AUD 88,00,000.00

Profit from hedge (I=F-H) AUD -13,89,848.09 AUD 45,24,450.37

Profit % from hedge (I/G) -18.76% 33.96%

4.V No hedge at all:

100% Hedged with forward contract

Particulars Value Value

Sales (A) $ 1,00,00,000 $ 1,00,00,000

Spot rate AUD/USD 20th of February $1.05 $ 0.85

Spot rate USD/AUD 20th of February 1/ 1.05 1/0.85

Spot rate USD/AUD 20th of February (B) AUD 0.95 AUD 1.18

Sale (S=A*B) AUD 95,23,809.52 AUD 1,17,64,705.88

Cost of sales (D) AUD 88,00,000 AUD 88,00,000

Profit % from no hedge (S-D)/S 7.6% 25.2%

5. Providing two examples of low-cost hedging strategies:

The two low cost hedging strategies that can be used by the organisation are the

currency swaps and future contracts. The currency swaps can allow the organisation to take

adequate loans in USA, while transferring the money to Australia on the spot rate and making

the payments after receiving the 10 million dollars to the loan-providing bank. The future

contracts can be used for minimising the damage conducted from the currency volatility

(Álvarez-Díez, Alfaro-Cid & Fernández-Blanco, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.