Financial Risk Management - Desklib

VerifiedAdded on 2023/06/16

|13

|3001

|438

AI Summary

This article discusses Financial Risk Management and covers topics such as reinvestment risk, extension risk, investment risk, diversification, covariance, R2 and volatility. It includes three case studies with calculations and analysis. The subject is relevant for finance and risk management courses in colleges and universities.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Financial Risk Management

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

CASE STUDY 1..............................................................................................................................3

A..................................................................................................................................................3

B..................................................................................................................................................4

C..................................................................................................................................................5

D .................................................................................................................................................6

CASE STUDY 2..............................................................................................................................6

(c)................................................................................................................................................6

(d)................................................................................................................................................8

CASE STUDY 3..............................................................................................................................8

a)..................................................................................................................................................8

b).................................................................................................................................................9

c)................................................................................................................................................10

d)...............................................................................................................................................11

REFERENCES..............................................................................................................................13

CASE STUDY 1..............................................................................................................................3

A..................................................................................................................................................3

B..................................................................................................................................................4

C..................................................................................................................................................5

D .................................................................................................................................................6

CASE STUDY 2..............................................................................................................................6

(c)................................................................................................................................................6

(d)................................................................................................................................................8

CASE STUDY 3..............................................................................................................................8

a)..................................................................................................................................................8

b).................................................................................................................................................9

c)................................................................................................................................................10

d)...............................................................................................................................................11

REFERENCES..............................................................................................................................13

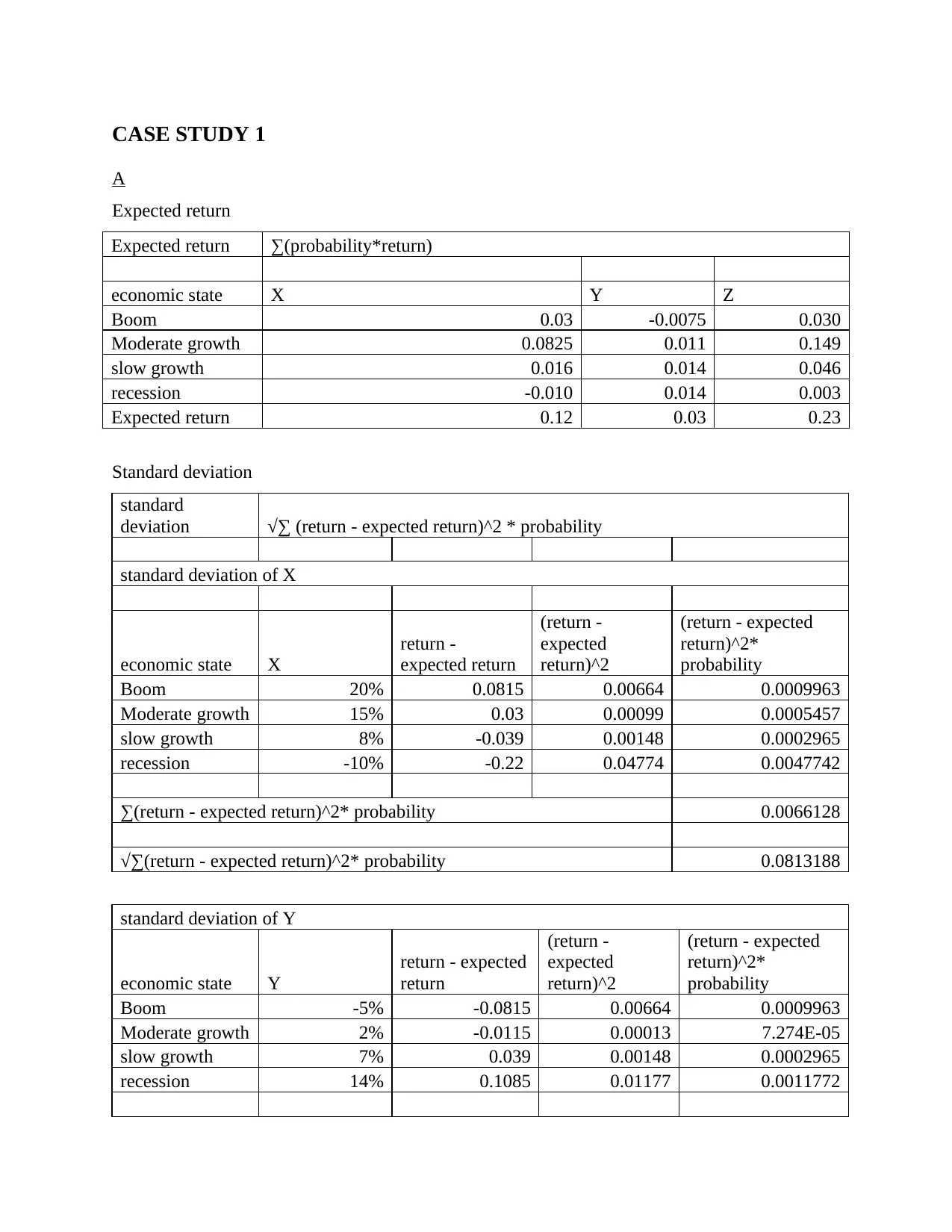

CASE STUDY 1

A

Expected return

Expected return ∑(probability*return)

economic state X Y Z

Boom 0.03 -0.0075 0.030

Moderate growth 0.0825 0.011 0.149

slow growth 0.016 0.014 0.046

recession -0.010 0.014 0.003

Expected return 0.12 0.03 0.23

Standard deviation

standard

deviation √∑ (return - expected return)^2 * probability

standard deviation of X

economic state X

return -

expected return

(return -

expected

return)^2

(return - expected

return)^2*

probability

Boom 20% 0.0815 0.00664 0.0009963

Moderate growth 15% 0.03 0.00099 0.0005457

slow growth 8% -0.039 0.00148 0.0002965

recession -10% -0.22 0.04774 0.0047742

∑(return - expected return)^2* probability 0.0066128

√∑(return - expected return)^2* probability 0.0813188

standard deviation of Y

economic state Y

return - expected

return

(return -

expected

return)^2

(return - expected

return)^2*

probability

Boom -5% -0.0815 0.00664 0.0009963

Moderate growth 2% -0.0115 0.00013 7.274E-05

slow growth 7% 0.039 0.00148 0.0002965

recession 14% 0.1085 0.01177 0.0011772

A

Expected return

Expected return ∑(probability*return)

economic state X Y Z

Boom 0.03 -0.0075 0.030

Moderate growth 0.0825 0.011 0.149

slow growth 0.016 0.014 0.046

recession -0.010 0.014 0.003

Expected return 0.12 0.03 0.23

Standard deviation

standard

deviation √∑ (return - expected return)^2 * probability

standard deviation of X

economic state X

return -

expected return

(return -

expected

return)^2

(return - expected

return)^2*

probability

Boom 20% 0.0815 0.00664 0.0009963

Moderate growth 15% 0.03 0.00099 0.0005457

slow growth 8% -0.039 0.00148 0.0002965

recession -10% -0.22 0.04774 0.0047742

∑(return - expected return)^2* probability 0.0066128

√∑(return - expected return)^2* probability 0.0813188

standard deviation of Y

economic state Y

return - expected

return

(return -

expected

return)^2

(return - expected

return)^2*

probability

Boom -5% -0.0815 0.00664 0.0009963

Moderate growth 2% -0.0115 0.00013 7.274E-05

slow growth 7% 0.039 0.00148 0.0002965

recession 14% 0.1085 0.01177 0.0011772

∑ (return - expected return)^2* probability 0.0025428

√∑(return - expected return)^2* probability 0.0504257

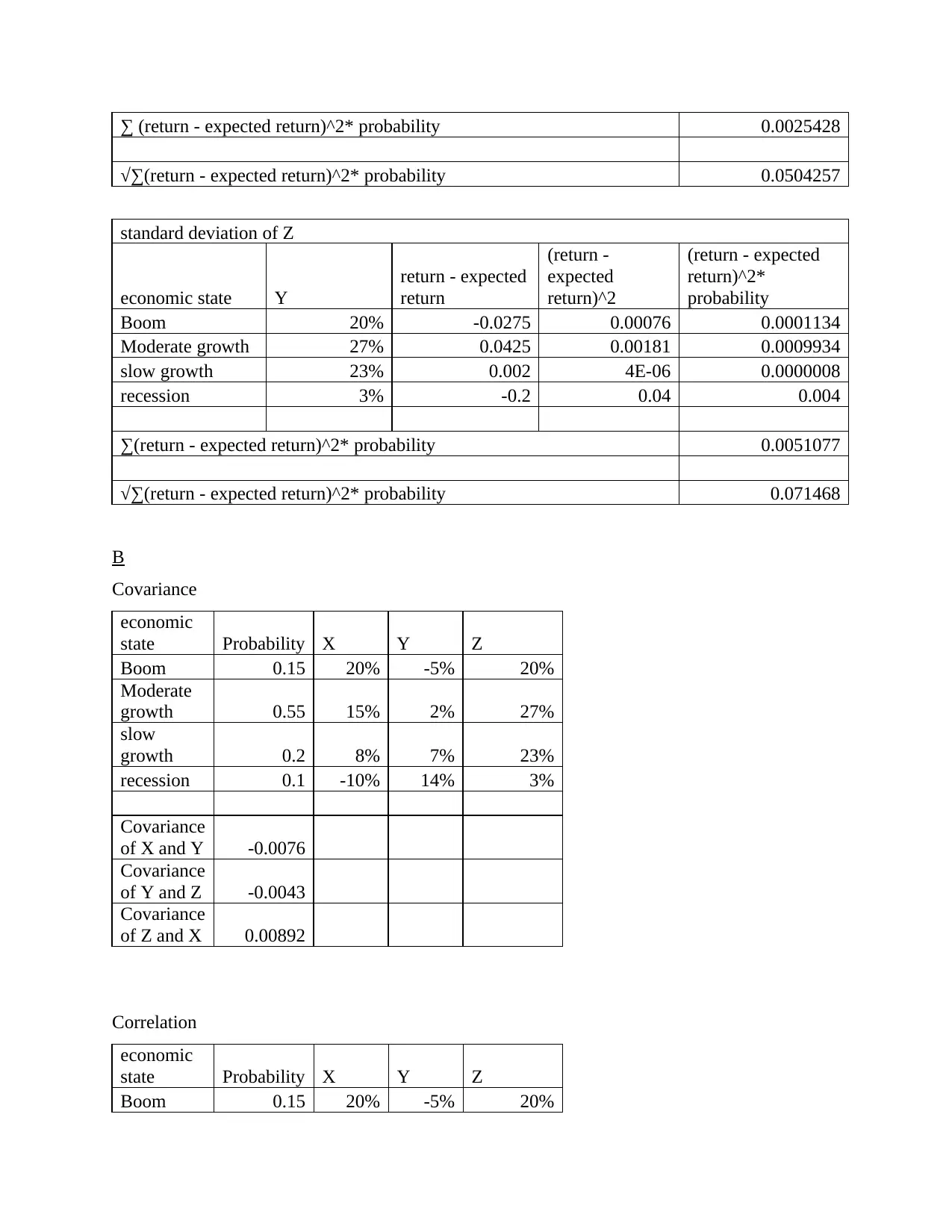

standard deviation of Z

economic state Y

return - expected

return

(return -

expected

return)^2

(return - expected

return)^2*

probability

Boom 20% -0.0275 0.00076 0.0001134

Moderate growth 27% 0.0425 0.00181 0.0009934

slow growth 23% 0.002 4E-06 0.0000008

recession 3% -0.2 0.04 0.004

∑(return - expected return)^2* probability 0.0051077

√∑(return - expected return)^2* probability 0.071468

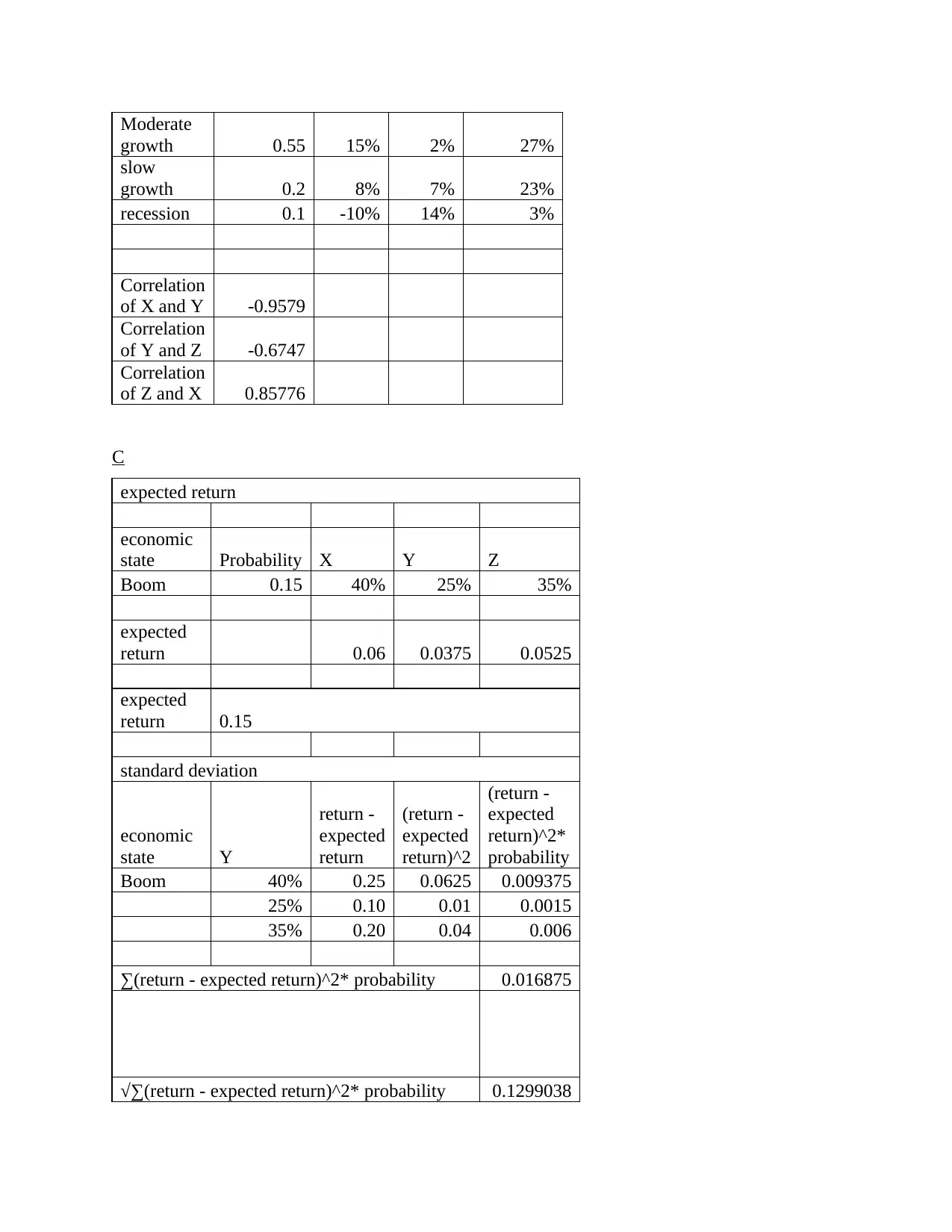

B

Covariance

economic

state Probability X Y Z

Boom 0.15 20% -5% 20%

Moderate

growth 0.55 15% 2% 27%

slow

growth 0.2 8% 7% 23%

recession 0.1 -10% 14% 3%

Covariance

of X and Y -0.0076

Covariance

of Y and Z -0.0043

Covariance

of Z and X 0.00892

Correlation

economic

state Probability X Y Z

Boom 0.15 20% -5% 20%

√∑(return - expected return)^2* probability 0.0504257

standard deviation of Z

economic state Y

return - expected

return

(return -

expected

return)^2

(return - expected

return)^2*

probability

Boom 20% -0.0275 0.00076 0.0001134

Moderate growth 27% 0.0425 0.00181 0.0009934

slow growth 23% 0.002 4E-06 0.0000008

recession 3% -0.2 0.04 0.004

∑(return - expected return)^2* probability 0.0051077

√∑(return - expected return)^2* probability 0.071468

B

Covariance

economic

state Probability X Y Z

Boom 0.15 20% -5% 20%

Moderate

growth 0.55 15% 2% 27%

slow

growth 0.2 8% 7% 23%

recession 0.1 -10% 14% 3%

Covariance

of X and Y -0.0076

Covariance

of Y and Z -0.0043

Covariance

of Z and X 0.00892

Correlation

economic

state Probability X Y Z

Boom 0.15 20% -5% 20%

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Moderate

growth 0.55 15% 2% 27%

slow

growth 0.2 8% 7% 23%

recession 0.1 -10% 14% 3%

Correlation

of X and Y -0.9579

Correlation

of Y and Z -0.6747

Correlation

of Z and X 0.85776

C

expected return

economic

state Probability X Y Z

Boom 0.15 40% 25% 35%

expected

return 0.06 0.0375 0.0525

expected

return 0.15

standard deviation

economic

state Y

return -

expected

return

(return -

expected

return)^2

(return -

expected

return)^2*

probability

Boom 40% 0.25 0.0625 0.009375

25% 0.10 0.01 0.0015

35% 0.20 0.04 0.006

∑(return - expected return)^2* probability 0.016875

√∑(return - expected return)^2* probability 0.1299038

growth 0.55 15% 2% 27%

slow

growth 0.2 8% 7% 23%

recession 0.1 -10% 14% 3%

Correlation

of X and Y -0.9579

Correlation

of Y and Z -0.6747

Correlation

of Z and X 0.85776

C

expected return

economic

state Probability X Y Z

Boom 0.15 40% 25% 35%

expected

return 0.06 0.0375 0.0525

expected

return 0.15

standard deviation

economic

state Y

return -

expected

return

(return -

expected

return)^2

(return -

expected

return)^2*

probability

Boom 40% 0.25 0.0625 0.009375

25% 0.10 0.01 0.0015

35% 0.20 0.04 0.006

∑(return - expected return)^2* probability 0.016875

√∑(return - expected return)^2* probability 0.1299038

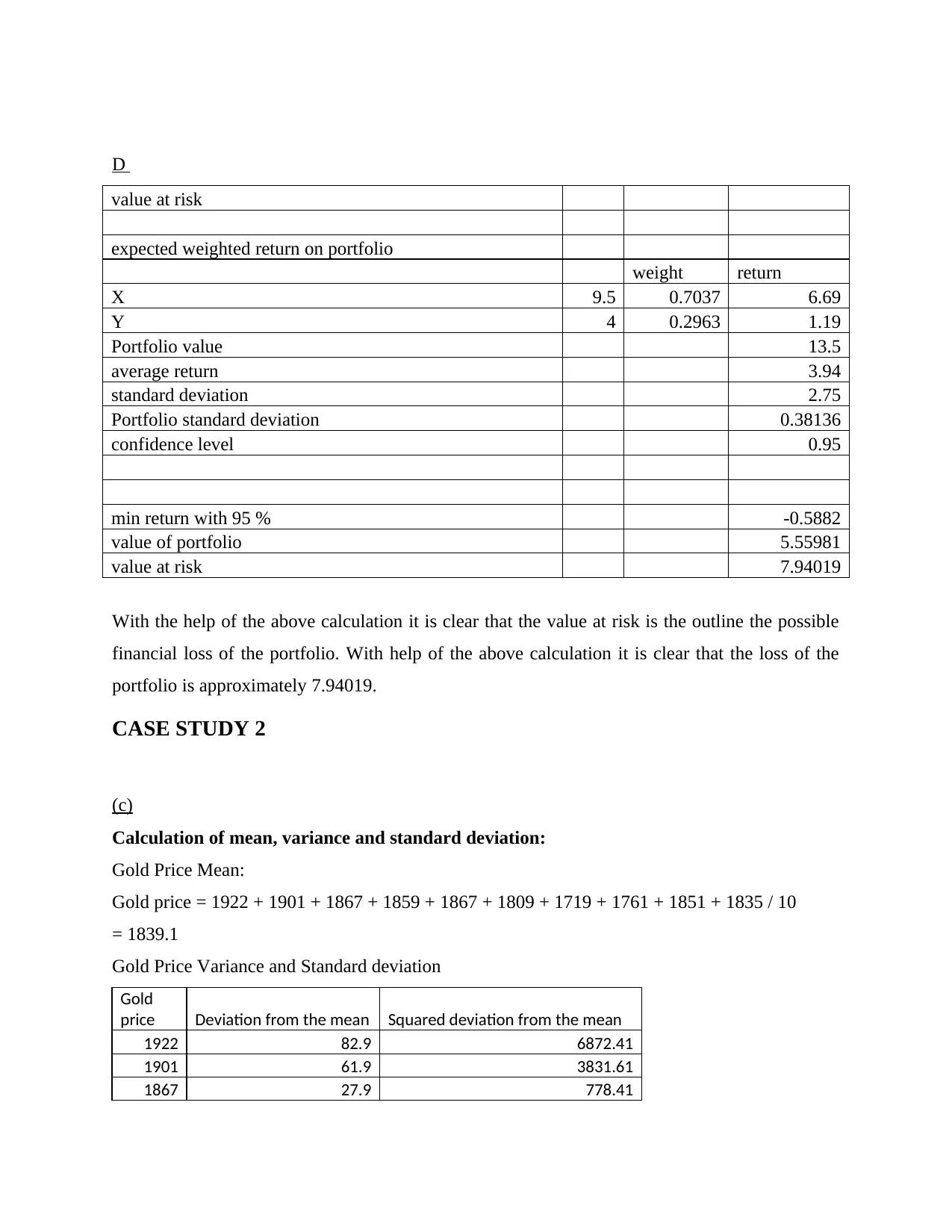

D

value at risk

expected weighted return on portfolio

weight return

X 9.5 0.7037 6.69

Y 4 0.2963 1.19

Portfolio value 13.5

average return 3.94

standard deviation 2.75

Portfolio standard deviation 0.38136

confidence level 0.95

min return with 95 % -0.5882

value of portfolio 5.55981

value at risk 7.94019

With the help of the above calculation it is clear that the value at risk is the outline the possible

financial loss of the portfolio. With help of the above calculation it is clear that the loss of the

portfolio is approximately 7.94019.

CASE STUDY 2

(c)

Calculation of mean, variance and standard deviation:

Gold Price Mean:

Gold price = 1922 + 1901 + 1867 + 1859 + 1867 + 1809 + 1719 + 1761 + 1851 + 1835 / 10

= 1839.1

Gold Price Variance and Standard deviation

Gold

price Deviation from the mean Squared deviation from the mean

1922 82.9 6872.41

1901 61.9 3831.61

1867 27.9 778.41

value at risk

expected weighted return on portfolio

weight return

X 9.5 0.7037 6.69

Y 4 0.2963 1.19

Portfolio value 13.5

average return 3.94

standard deviation 2.75

Portfolio standard deviation 0.38136

confidence level 0.95

min return with 95 % -0.5882

value of portfolio 5.55981

value at risk 7.94019

With the help of the above calculation it is clear that the value at risk is the outline the possible

financial loss of the portfolio. With help of the above calculation it is clear that the loss of the

portfolio is approximately 7.94019.

CASE STUDY 2

(c)

Calculation of mean, variance and standard deviation:

Gold Price Mean:

Gold price = 1922 + 1901 + 1867 + 1859 + 1867 + 1809 + 1719 + 1761 + 1851 + 1835 / 10

= 1839.1

Gold Price Variance and Standard deviation

Gold

price Deviation from the mean Squared deviation from the mean

1922 82.9 6872.41

1901 61.9 3831.61

1867 27.9 778.41

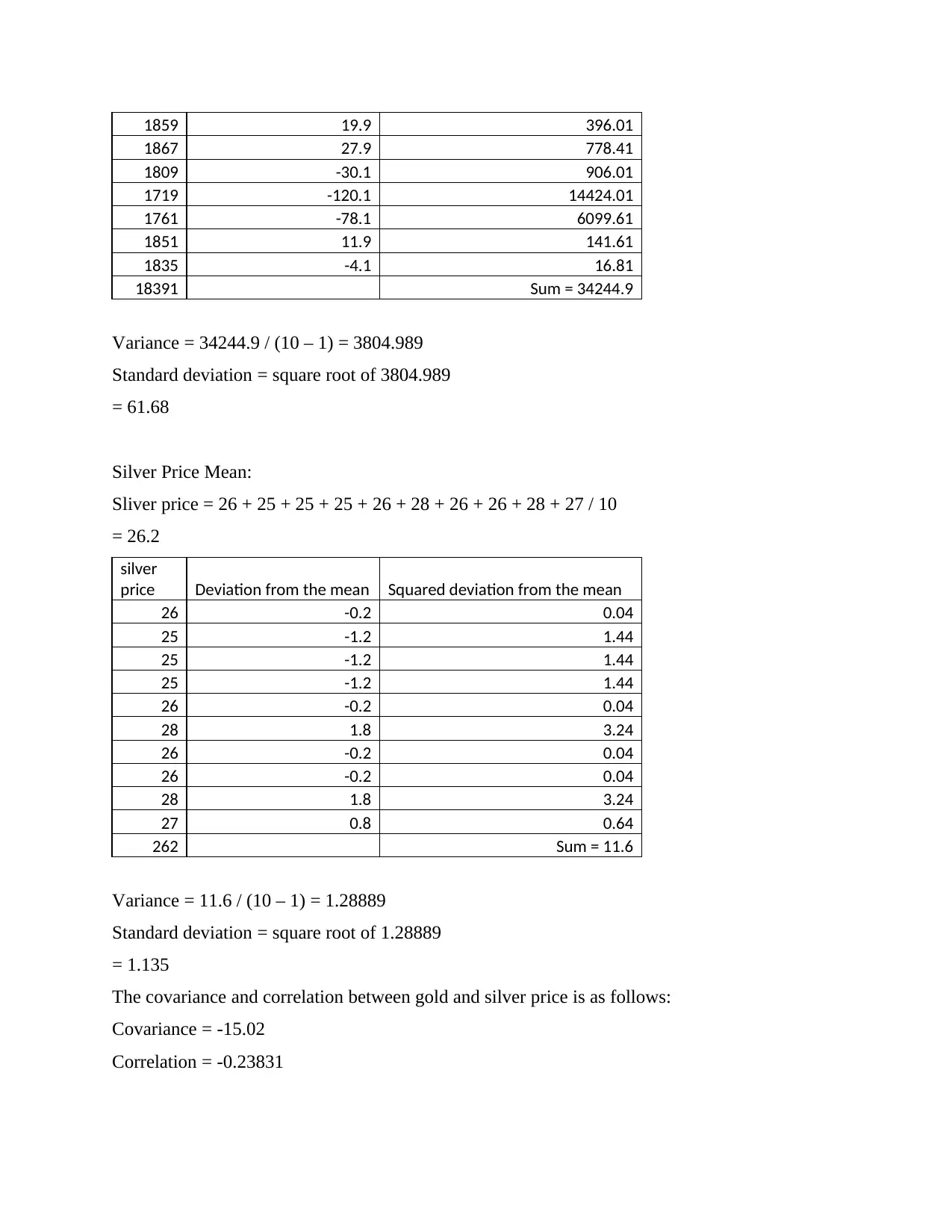

1859 19.9 396.01

1867 27.9 778.41

1809 -30.1 906.01

1719 -120.1 14424.01

1761 -78.1 6099.61

1851 11.9 141.61

1835 -4.1 16.81

18391 Sum = 34244.9

Variance = 34244.9 / (10 – 1) = 3804.989

Standard deviation = square root of 3804.989

= 61.68

Silver Price Mean:

Sliver price = 26 + 25 + 25 + 25 + 26 + 28 + 26 + 26 + 28 + 27 / 10

= 26.2

silver

price Deviation from the mean Squared deviation from the mean

26 -0.2 0.04

25 -1.2 1.44

25 -1.2 1.44

25 -1.2 1.44

26 -0.2 0.04

28 1.8 3.24

26 -0.2 0.04

26 -0.2 0.04

28 1.8 3.24

27 0.8 0.64

262 Sum = 11.6

Variance = 11.6 / (10 – 1) = 1.28889

Standard deviation = square root of 1.28889

= 1.135

The covariance and correlation between gold and silver price is as follows:

Covariance = -15.02

Correlation = -0.23831

1867 27.9 778.41

1809 -30.1 906.01

1719 -120.1 14424.01

1761 -78.1 6099.61

1851 11.9 141.61

1835 -4.1 16.81

18391 Sum = 34244.9

Variance = 34244.9 / (10 – 1) = 3804.989

Standard deviation = square root of 3804.989

= 61.68

Silver Price Mean:

Sliver price = 26 + 25 + 25 + 25 + 26 + 28 + 26 + 26 + 28 + 27 / 10

= 26.2

silver

price Deviation from the mean Squared deviation from the mean

26 -0.2 0.04

25 -1.2 1.44

25 -1.2 1.44

25 -1.2 1.44

26 -0.2 0.04

28 1.8 3.24

26 -0.2 0.04

26 -0.2 0.04

28 1.8 3.24

27 0.8 0.64

262 Sum = 11.6

Variance = 11.6 / (10 – 1) = 1.28889

Standard deviation = square root of 1.28889

= 1.135

The covariance and correlation between gold and silver price is as follows:

Covariance = -15.02

Correlation = -0.23831

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Calculation of annualized standard deviation of return:

Formula = Standard deviation of monthly return * square root of 12 months

Gold Price = 61.68 * 3.46 = 213.4128

Silver Price = 1.135 * 3.46 = 3.9271

(d)

Yes, in order to manage the risk attached with the price of the commodity such as metal

mining, the company should hedge their sales revenue. This is because the price of the industrial

products get changes over the span of time. So, hedging the sales revenue of the commodity

helps the industrial companies in limits the loses to the great extent. It is also good for the

company to increase liquidity as it facilitates investors to invest in various assets classes (Peng

and et.al., 2018). Thus, it is advisable to the companies that they have to use hedge technique to

protect their sales revenue by setting the lower margin outlay. This will help the company

especially industrial in protecting their sales revenue from the changes taken place in external

environment.

CASE STUDY 3

a)

Reinvestment risk refers to inability of investor to get the cash flow from the investment for

further investment. In the case of UK banking chances that cash flow received from the

investment will be less than the amount invested. The one of the crucial vulnerable to reinvest is

found to be in callable bonds. In the banking system reinvestment risk refers to declining rate

which leads to affect the liquidity and position of the banking institution. Extension risk is

mostly refers to having differ repayments due to market condition. It is mostly concerned with

the secondary credit market.

In the UK banking system there is rise in prices of products which is leading to result in

inflation situation system (Gonçalves, 2021). The mentioned kinds of risk is resulting in having

bank to pay higher level of focus on rate of risk which can decrease the prevailing threats. The

structure of UK banking institutions are formulated in such manner which can incline its ability

to manage and monitor the prevailing situation in turn higher competitive advantages can be

derived. The impact of reinvestment risk incline in banks for bonds with longer maturities &

Formula = Standard deviation of monthly return * square root of 12 months

Gold Price = 61.68 * 3.46 = 213.4128

Silver Price = 1.135 * 3.46 = 3.9271

(d)

Yes, in order to manage the risk attached with the price of the commodity such as metal

mining, the company should hedge their sales revenue. This is because the price of the industrial

products get changes over the span of time. So, hedging the sales revenue of the commodity

helps the industrial companies in limits the loses to the great extent. It is also good for the

company to increase liquidity as it facilitates investors to invest in various assets classes (Peng

and et.al., 2018). Thus, it is advisable to the companies that they have to use hedge technique to

protect their sales revenue by setting the lower margin outlay. This will help the company

especially industrial in protecting their sales revenue from the changes taken place in external

environment.

CASE STUDY 3

a)

Reinvestment risk refers to inability of investor to get the cash flow from the investment for

further investment. In the case of UK banking chances that cash flow received from the

investment will be less than the amount invested. The one of the crucial vulnerable to reinvest is

found to be in callable bonds. In the banking system reinvestment risk refers to declining rate

which leads to affect the liquidity and position of the banking institution. Extension risk is

mostly refers to having differ repayments due to market condition. It is mostly concerned with

the secondary credit market.

In the UK banking system there is rise in prices of products which is leading to result in

inflation situation system (Gonçalves, 2021). The mentioned kinds of risk is resulting in having

bank to pay higher level of focus on rate of risk which can decrease the prevailing threats. The

structure of UK banking institutions are formulated in such manner which can incline its ability

to manage and monitor the prevailing situation in turn higher competitive advantages can be

derived. The impact of reinvestment risk incline in banks for bonds with longer maturities &

higher coupon payment that can decrease h with shorter maturities. In addition to this, it can be

specified that Barclays is one of the larger bank that highly contribute in economic growth h &

development. In order to manage reinvestment risk the much emphasis is provided on application

of different kinds of practices. It includes using non callable bonds, zero coupon instruments,

bond ladders, activity managed funds and long term securities.

Extension risk has adverse impact on the processing of banking function. In addition to this, the

major impact that can arise due to presence of this particular risk includes lowering the

secondary market value via incline in rate (Grundke and Kühn, 2020). In addition to this, it can

be specified that the banking institutions in UK get highly affect which influence its ability to

manage liquidity & efficiency this is basically monitored by these firm through focusing on

involving avoidance, loss prevention, separation, duplication & diversification. This can

contribute in overcoming situation which has adverse impact on the processing of specified

sector. On the basis of this, it can be interpreted that controlling this both kinds of risk in turn

smooth functioning can be derived.

b)

Investment risk is associated with possibilities of losses which can occur due to changes in

expected return within particular period. Investors largely pay attention on measuring investment

risk through giving focus on distinct elements which can lead in arising of risk. There are

different kinds of approaches which can be utilized by investors for mitigating or eliminating

related risk with particular investment.

Diversification refers to making portfolio of investment by involving distinct feature

comprising which can decline risk. It is the practice of spreading investment around so that

exposure to nay particular type of asset is kept to be limited (Duan and et.al., 2018). In order to

mitigate the risk it is highly crucial for an individual to adopt the technique of diversification in

turn having appropriate level of balance in declining possibilities of loss can be done. It aids in

managing volatility of possessing portfolio so that inclining opportunity of deriving profitability

can be achieved.

Covariance measures the e directional relationship between tow variables. In case of

investment risk, covariance is helpful in measuring that directional relationship between two

assets in which positive indicate assets turnover move together. In case of negative be covariance

which indicates inverse relationship. It is basically a statistical tool that contribute in ascertaining

specified that Barclays is one of the larger bank that highly contribute in economic growth h &

development. In order to manage reinvestment risk the much emphasis is provided on application

of different kinds of practices. It includes using non callable bonds, zero coupon instruments,

bond ladders, activity managed funds and long term securities.

Extension risk has adverse impact on the processing of banking function. In addition to this, the

major impact that can arise due to presence of this particular risk includes lowering the

secondary market value via incline in rate (Grundke and Kühn, 2020). In addition to this, it can

be specified that the banking institutions in UK get highly affect which influence its ability to

manage liquidity & efficiency this is basically monitored by these firm through focusing on

involving avoidance, loss prevention, separation, duplication & diversification. This can

contribute in overcoming situation which has adverse impact on the processing of specified

sector. On the basis of this, it can be interpreted that controlling this both kinds of risk in turn

smooth functioning can be derived.

b)

Investment risk is associated with possibilities of losses which can occur due to changes in

expected return within particular period. Investors largely pay attention on measuring investment

risk through giving focus on distinct elements which can lead in arising of risk. There are

different kinds of approaches which can be utilized by investors for mitigating or eliminating

related risk with particular investment.

Diversification refers to making portfolio of investment by involving distinct feature

comprising which can decline risk. It is the practice of spreading investment around so that

exposure to nay particular type of asset is kept to be limited (Duan and et.al., 2018). In order to

mitigate the risk it is highly crucial for an individual to adopt the technique of diversification in

turn having appropriate level of balance in declining possibilities of loss can be done. It aids in

managing volatility of possessing portfolio so that inclining opportunity of deriving profitability

can be achieved.

Covariance measures the e directional relationship between tow variables. In case of

investment risk, covariance is helpful in measuring that directional relationship between two

assets in which positive indicate assets turnover move together. In case of negative be covariance

which indicates inverse relationship. It is basically a statistical tool that contribute in ascertaining

the mentioned kind of relationship so that estimating particular level of risk which lead to profit

or loss can be identified.

R2 is taken into practice as the bench marking for measuring the percentage of an asset.

It is one of the crucial function that provides assistance in interpreting relevant information

regarding movements of security. The combination of diversification, covariance and R2 can be

utilized by organization for having depth insights in turn having relevant ability to mitigate

prevailing level of risk can become possible (Taghizadeh-Hesary and Yoshino, 2019). To get

significant mixture can assist in having proper extent of ability to identify directional movement,

possibilities of losses, performance of assets as compared to standard bench marking. From the

evaluation it can be articulated that having appropriate extent of capabilities to manage the e

prevailing circumstances' int turn avoiding situation that can lead to loss. On the basis of this, it

can be interpreted that investment risk can be properly managed by applying diversification,

covariance and R2.

c)

Volatility refers to rapid change in rate due to which prices of stock increases or declines over

particular duration. In case of higher stock prices there is availability of greater risk which are

required to be taken to be consideration. This contributes in estimating higher level of ability to

understand the prevailing situation. Understanding fluctuation through tending to rapid &

extreme alteration which results in incing or declining stock price which can be measured by

beta coefficient. The volatility is helpful in decreasing security experience period of

unpredictable so that decision regarding investment can be done. There are different kinds of

method available which can taken into consideration for estimating volatility. The one of the

significant approach that is widely used for ascertaining fluctuation involves calculation of

standard deviation. It is highly used method as provides concise details of fluctuation that is easy

to interpret in turn crucial evaluation regarding investment can be done. The specified method

gives emphasis on having relevant measure of market volatility which can be appropriately

analyzed SD.

or loss can be identified.

R2 is taken into practice as the bench marking for measuring the percentage of an asset.

It is one of the crucial function that provides assistance in interpreting relevant information

regarding movements of security. The combination of diversification, covariance and R2 can be

utilized by organization for having depth insights in turn having relevant ability to mitigate

prevailing level of risk can become possible (Taghizadeh-Hesary and Yoshino, 2019). To get

significant mixture can assist in having proper extent of ability to identify directional movement,

possibilities of losses, performance of assets as compared to standard bench marking. From the

evaluation it can be articulated that having appropriate extent of capabilities to manage the e

prevailing circumstances' int turn avoiding situation that can lead to loss. On the basis of this, it

can be interpreted that investment risk can be properly managed by applying diversification,

covariance and R2.

c)

Volatility refers to rapid change in rate due to which prices of stock increases or declines over

particular duration. In case of higher stock prices there is availability of greater risk which are

required to be taken to be consideration. This contributes in estimating higher level of ability to

understand the prevailing situation. Understanding fluctuation through tending to rapid &

extreme alteration which results in incing or declining stock price which can be measured by

beta coefficient. The volatility is helpful in decreasing security experience period of

unpredictable so that decision regarding investment can be done. There are different kinds of

method available which can taken into consideration for estimating volatility. The one of the

significant approach that is widely used for ascertaining fluctuation involves calculation of

standard deviation. It is highly used method as provides concise details of fluctuation that is easy

to interpret in turn crucial evaluation regarding investment can be done. The specified method

gives emphasis on having relevant measure of market volatility which can be appropriately

analyzed SD.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Maximum downward is another approach which contribute in estimating relevant

information regarding price fluctuations. It aids in estimating that how much it has fell or

inclined in turn formulating appropriate course of action for making decision can become

possible. In addition to this it is used by large number of investors, analyst, etc so that

speculating assets locators and growth investors for the purpose to limit losses (Peng and et.al.,

2018). It aids in predicting the pattern of losses so that formulation of relevant functioning in

turn higher productive result providing outcome can be achieved.

Beta is included as one of the crucial method that can be included to have to measure

stock market. It provides assistance in evaluating relevant risk of stocks In addition to this,

determining diversification of assets through enabling organization to have measure fluctuations

in turn making appropriate decision can become possible. Beta has the values of less than 1

reflecting their lower volatility and vice versa. It gives proper specification regarding extent of

fluctuation in turn making relevant and appropriate decision to avoiding loss occurring situation.

With help of such kinds of method it becomes possible to estimate distinct types of volatility

which involves historical, implied and future realized which larger contribute in making

appropriate decision.

d)

Interest rate risk is considered with having potential change in the overall interest rates which

will decline the value of bond or other fixed rate investment. The rise in interest rate risk decline

the price value of bind and other fixed rate risk. The main cause behind interest rate risk is

associated with incline in equity fall which can paying out more interest. It leads to impact the

credit risk of company which is forces the lender to raise interest rates for potential borrowings.

Organization faces higher interest rate when the proportion of debt in the capital structure. The

different kinds of interest risk involve repricing, yield curve, basis and optionality. It is highly

essential to pay attention on having information regarding the main sources of interest risk which

involve difference in risk of default & over dues, liquidity of debt, term to maturity and leaders

cost of serving loans.

There are several causes which are required to be taken into considerations as it leads to rise in

arriving of interest rate risk. The one of the main source which result in arriving of interest risk

which is re pricing. The re pricing is concerned with changes of interest rate at the time of

financial contract rate is reset it leads to result in arising risk if the interest rates are settled on

information regarding price fluctuations. It aids in estimating that how much it has fell or

inclined in turn formulating appropriate course of action for making decision can become

possible. In addition to this it is used by large number of investors, analyst, etc so that

speculating assets locators and growth investors for the purpose to limit losses (Peng and et.al.,

2018). It aids in predicting the pattern of losses so that formulation of relevant functioning in

turn higher productive result providing outcome can be achieved.

Beta is included as one of the crucial method that can be included to have to measure

stock market. It provides assistance in evaluating relevant risk of stocks In addition to this,

determining diversification of assets through enabling organization to have measure fluctuations

in turn making appropriate decision can become possible. Beta has the values of less than 1

reflecting their lower volatility and vice versa. It gives proper specification regarding extent of

fluctuation in turn making relevant and appropriate decision to avoiding loss occurring situation.

With help of such kinds of method it becomes possible to estimate distinct types of volatility

which involves historical, implied and future realized which larger contribute in making

appropriate decision.

d)

Interest rate risk is considered with having potential change in the overall interest rates which

will decline the value of bond or other fixed rate investment. The rise in interest rate risk decline

the price value of bind and other fixed rate risk. The main cause behind interest rate risk is

associated with incline in equity fall which can paying out more interest. It leads to impact the

credit risk of company which is forces the lender to raise interest rates for potential borrowings.

Organization faces higher interest rate when the proportion of debt in the capital structure. The

different kinds of interest risk involve repricing, yield curve, basis and optionality. It is highly

essential to pay attention on having information regarding the main sources of interest risk which

involve difference in risk of default & over dues, liquidity of debt, term to maturity and leaders

cost of serving loans.

There are several causes which are required to be taken into considerations as it leads to rise in

arriving of interest rate risk. The one of the main source which result in arriving of interest risk

which is re pricing. The re pricing is concerned with changes of interest rate at the time of

financial contract rate is reset it leads to result in arising risk if the interest rates are settled on

liabilities for the period which differs from those on offsetting assets (Kiley and Roberts, 2017).

It occurs when company retires employee stock option that has lower strike price. In addition to

this, company can effectively replace when keep top managers.

Yield curve risk is another source which aids in experiencing an adverse shift in market h

interest aster associated with investing in fixed income instrument. The performance of fixed rate

possessing instrument get affected from this (Brunnermeier and Koby, 2018). The shorter term

changes in this yield may lead to have higher level of impact on prevailing circumstances and

results in change of rate.

Basis risk arise in case of mismatch of the position of hedged. In addition to this, interest rate

risk come into existence due to imperfect hedge which results in losses in investment. It is one of

the significant source of risk which majorly affect the investment by inclining rate of interest.

Optionality risk is considered to be one of the crucial threat for the investors. It arises due to

change in time or scope of monetary instruments that brings cash flow sdue to alteration in the

interest. The main reason for their occurrence is having options embedded in corporate assets,

liabilities, etc. on the basis of the provided information it can be specified that these are main

sources of interest rate risk.

It occurs when company retires employee stock option that has lower strike price. In addition to

this, company can effectively replace when keep top managers.

Yield curve risk is another source which aids in experiencing an adverse shift in market h

interest aster associated with investing in fixed income instrument. The performance of fixed rate

possessing instrument get affected from this (Brunnermeier and Koby, 2018). The shorter term

changes in this yield may lead to have higher level of impact on prevailing circumstances and

results in change of rate.

Basis risk arise in case of mismatch of the position of hedged. In addition to this, interest rate

risk come into existence due to imperfect hedge which results in losses in investment. It is one of

the significant source of risk which majorly affect the investment by inclining rate of interest.

Optionality risk is considered to be one of the crucial threat for the investors. It arises due to

change in time or scope of monetary instruments that brings cash flow sdue to alteration in the

interest. The main reason for their occurrence is having options embedded in corporate assets,

liabilities, etc. on the basis of the provided information it can be specified that these are main

sources of interest rate risk.

REFERENCES

Books and Journals

Brunnermeier, M.K. and Koby, Y., 2018. The reversal interest rate (No. w25406). National

Bureau of Economic Research.

Duan, F. and et.al., 2018. Energy investment risk assessment for nations along China’s Belt &

Road Initiative. Journal of Cleaner Production. 170. pp.535-547.

Gonçalves, A.S., 2021. Reinvestment risk and the equity term structure. The Journal of Finance.

Grundke, P. and Kühn, A., 2020. The impact of the Basel III liquidity ratios on banks: Evidence

from a simulation study. The Quarterly Review of Economics and Finance. 75. pp.167-

190.

Kiley, M.T. and Roberts, J.M., 2017. Monetary policy in a low interest rate world. Brookings

Papers on Economic Activity. 2017(1). pp.317-396.

Peng, Y. and et.al., 2018. The best of two worlds: Forecasting high frequency volatility for

cryptocurrencies and traditional currencies with Support Vector Regression. Expert

Systems with Applications . 97. pp.177-192.

Taghizadeh-Hesary, F. and Yoshino, N., 2019. The way to induce private participation in green

finance and investment. Finance Research Letters. 31. pp.98-103.

Books and Journals

Brunnermeier, M.K. and Koby, Y., 2018. The reversal interest rate (No. w25406). National

Bureau of Economic Research.

Duan, F. and et.al., 2018. Energy investment risk assessment for nations along China’s Belt &

Road Initiative. Journal of Cleaner Production. 170. pp.535-547.

Gonçalves, A.S., 2021. Reinvestment risk and the equity term structure. The Journal of Finance.

Grundke, P. and Kühn, A., 2020. The impact of the Basel III liquidity ratios on banks: Evidence

from a simulation study. The Quarterly Review of Economics and Finance. 75. pp.167-

190.

Kiley, M.T. and Roberts, J.M., 2017. Monetary policy in a low interest rate world. Brookings

Papers on Economic Activity. 2017(1). pp.317-396.

Peng, Y. and et.al., 2018. The best of two worlds: Forecasting high frequency volatility for

cryptocurrencies and traditional currencies with Support Vector Regression. Expert

Systems with Applications . 97. pp.177-192.

Taghizadeh-Hesary, F. and Yoshino, N., 2019. The way to induce private participation in green

finance and investment. Finance Research Letters. 31. pp.98-103.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.