Financial Risk Management - PDF

VerifiedAdded on 2021/06/15

|16

|3740

|52

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL RISK MANAGEMENT

Financial Risk Management

Name of the Student:

Name of the University:

Authors Note:

Financial Risk Management

Name of the Student:

Name of the University:

Authors Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL RISK MANAGEMENT

1

Table of Contents

Section I:....................................................................................................................................2

a) Stating the specific financial risk exposure faced by Medusa Mining Ltd, which might

hamper its revenue generation capability:..................................................................................2

b) The recommendations on the hedging percentage and process that needs to be followed by

Medusa mining company:..........................................................................................................7

Section II:...................................................................................................................................8

c) Stating the recommendations on derivatives instruments for implementing the hedges:......9

d) Evaluating the recommendation regarding the 60% hedge in November and December

production of copper:...............................................................................................................10

Section III:................................................................................................................................12

e) Developing an adequate combination or option spread strategy to produce copper

minimising the negative impact from price decline:................................................................12

Reference and Bibliography:....................................................................................................14

1

Table of Contents

Section I:....................................................................................................................................2

a) Stating the specific financial risk exposure faced by Medusa Mining Ltd, which might

hamper its revenue generation capability:..................................................................................2

b) The recommendations on the hedging percentage and process that needs to be followed by

Medusa mining company:..........................................................................................................7

Section II:...................................................................................................................................8

c) Stating the recommendations on derivatives instruments for implementing the hedges:......9

d) Evaluating the recommendation regarding the 60% hedge in November and December

production of copper:...............................................................................................................10

Section III:................................................................................................................................12

e) Developing an adequate combination or option spread strategy to produce copper

minimising the negative impact from price decline:................................................................12

Reference and Bibliography:....................................................................................................14

FINANCIAL RISK MANAGEMENT

2

Section I:

a) Stating the specific financial risk exposure faced by Medusa Mining Ltd, which might

hamper its revenue generation capability:

From the evaluation of the operations of Medusa mining Limited it could be identified

that it has different levels of financial risk, which might directly impact its overall operational

capability. The company is relatively focused on producing two specific metals such as gold

and copper who is overall price in the market fluctuates adequately. from the evaluation it

could be identified that there is different level of risk such as interest rate risk, commodity

market risk, and foreign exchange risk affecting the operational capability the organization.

The thorough elaboration on the financial risk of the company is effectively depicted as

follows.

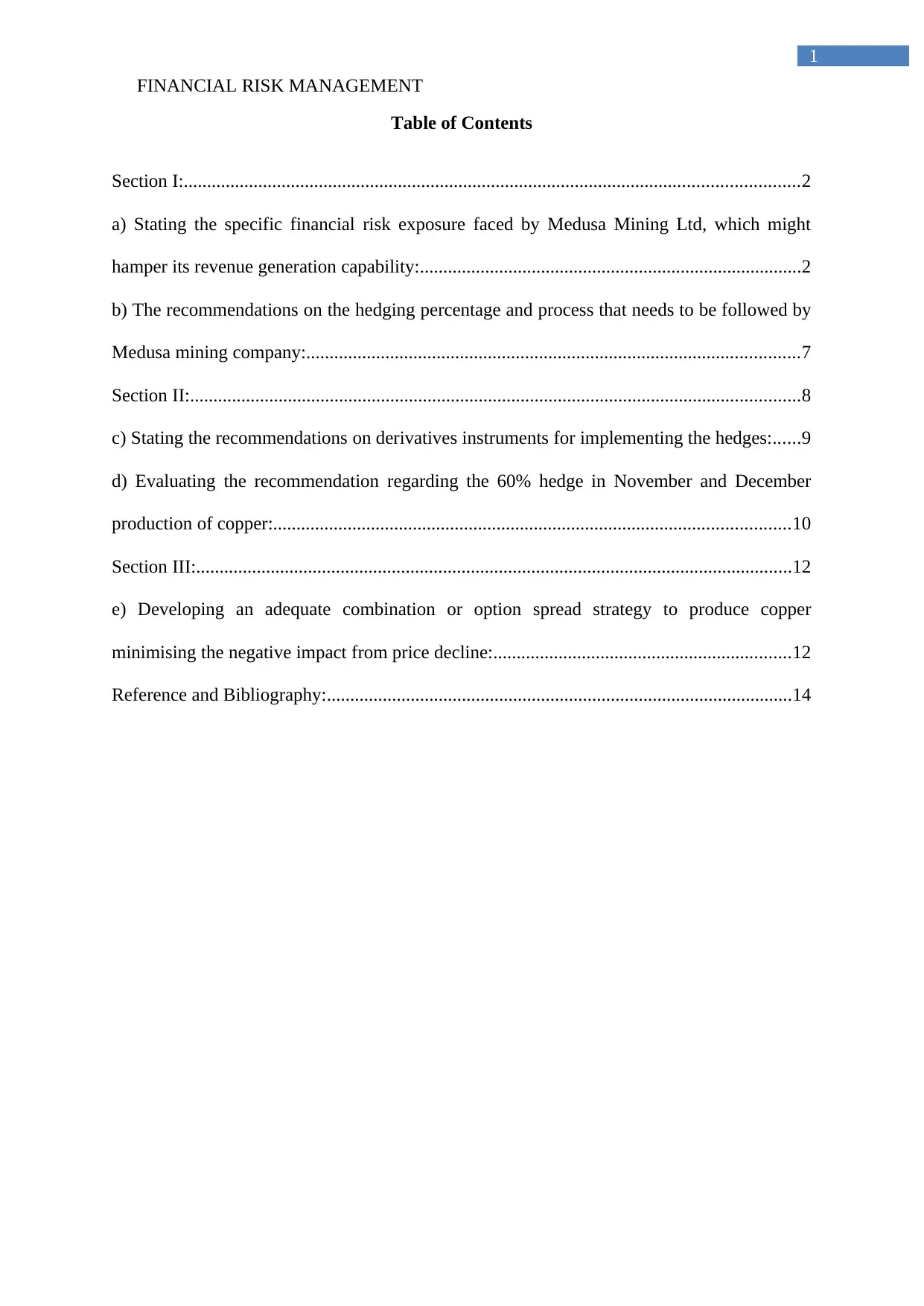

Commodity Market Risk:

Figure 1: Stating the price trend of gold

(Source: Provident Metals Online 2018)

The commodity market risk is relatively affected by the changing prices of gold

which is depicted in the above figure. The prices of gold have relatively changed during the

2

Section I:

a) Stating the specific financial risk exposure faced by Medusa Mining Ltd, which might

hamper its revenue generation capability:

From the evaluation of the operations of Medusa mining Limited it could be identified

that it has different levels of financial risk, which might directly impact its overall operational

capability. The company is relatively focused on producing two specific metals such as gold

and copper who is overall price in the market fluctuates adequately. from the evaluation it

could be identified that there is different level of risk such as interest rate risk, commodity

market risk, and foreign exchange risk affecting the operational capability the organization.

The thorough elaboration on the financial risk of the company is effectively depicted as

follows.

Commodity Market Risk:

Figure 1: Stating the price trend of gold

(Source: Provident Metals Online 2018)

The commodity market risk is relatively affected by the changing prices of gold

which is depicted in the above figure. The prices of gold have relatively changed during the

FINANCIAL RISK MANAGEMENT

3

past 1 year, as depicted in the above figure. This change and volatility in the prices of gold is

directly affecting the overall revenue generation capability of Medusa mining Limited. the

company is not able to identify a perfect price structure in which it could maximize profit

from the gold production. the continuous decline in the prices of gold can be seen from April

where a barrier is being set and the prices are not able to break a certain limit. this indicates a

down trend in the overall prices of gold, which is relatively not effective for the Medusa

mining company. the company needs to sell 14,200 ounces of gold by the end of December

as it will be producing them during July to December. Furthermore, the prices of gold is

relatively declined from the levels of $1,340 to $1,312, which indicates the overall down

trend in price of gold. Therefore, adequate hedging measure needs to be imposed by the

company for minimizing the risk from commodity price fluctuations, which might directly

impact its overall profitability. this aging procedure which is relatively fix the prices of gold

and minimizing the negative impact from reducing gold prices on its revenue generation

capacity (McNeil, Frey and Embrechts 2015).

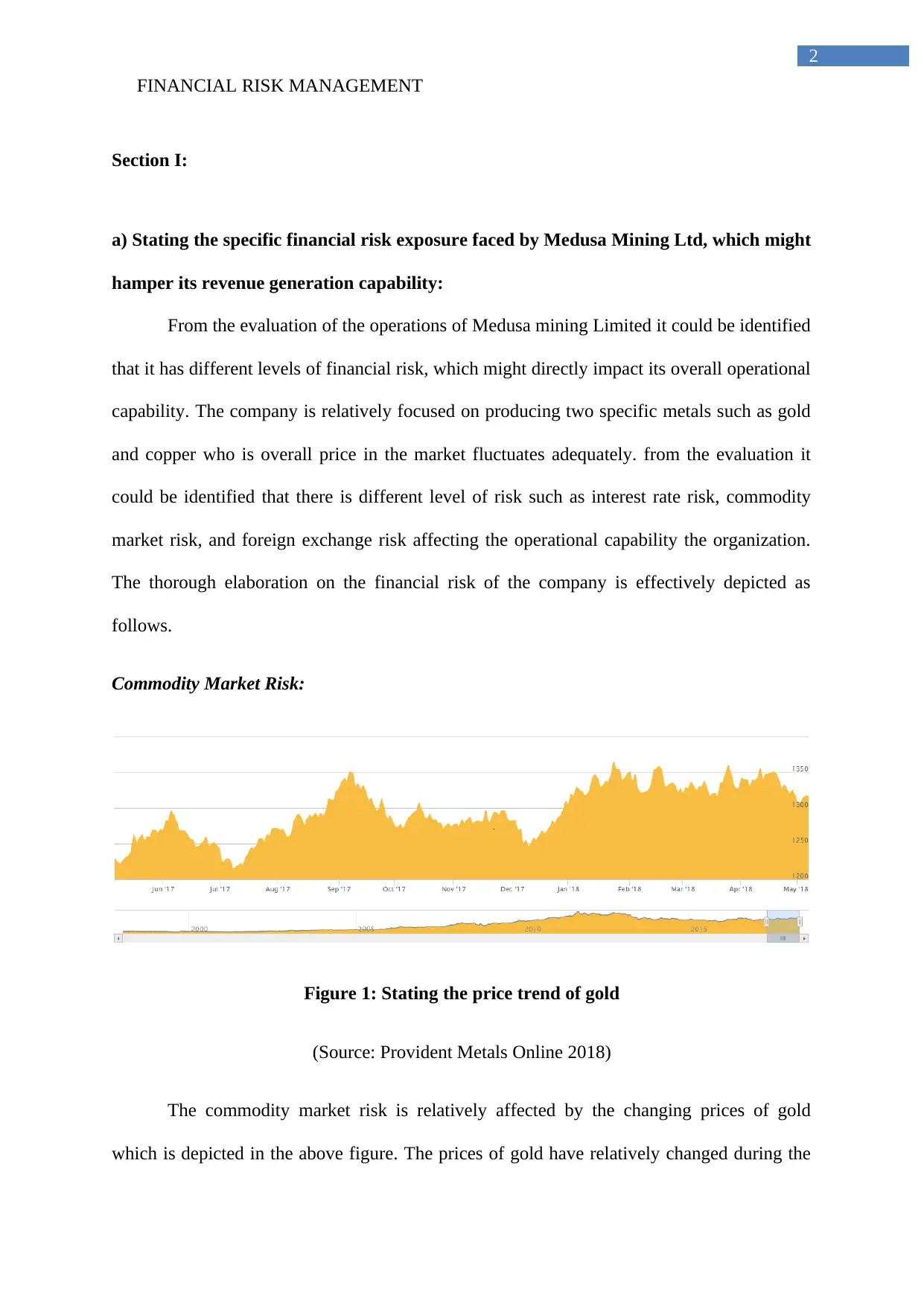

Figure 2: Stating the price trend of Copper

(Source: Provident Metals Online 2018)

The above figure relatively States the overall changes in price of copper, which is

relatively produced by Medusa mining company during July to December. the price changes

in copper is relatively detected from the above figure, which could directly affect the revenue

3

past 1 year, as depicted in the above figure. This change and volatility in the prices of gold is

directly affecting the overall revenue generation capability of Medusa mining Limited. the

company is not able to identify a perfect price structure in which it could maximize profit

from the gold production. the continuous decline in the prices of gold can be seen from April

where a barrier is being set and the prices are not able to break a certain limit. this indicates a

down trend in the overall prices of gold, which is relatively not effective for the Medusa

mining company. the company needs to sell 14,200 ounces of gold by the end of December

as it will be producing them during July to December. Furthermore, the prices of gold is

relatively declined from the levels of $1,340 to $1,312, which indicates the overall down

trend in price of gold. Therefore, adequate hedging measure needs to be imposed by the

company for minimizing the risk from commodity price fluctuations, which might directly

impact its overall profitability. this aging procedure which is relatively fix the prices of gold

and minimizing the negative impact from reducing gold prices on its revenue generation

capacity (McNeil, Frey and Embrechts 2015).

Figure 2: Stating the price trend of Copper

(Source: Provident Metals Online 2018)

The above figure relatively States the overall changes in price of copper, which is

relatively produced by Medusa mining company during July to December. the price changes

in copper is relatively detected from the above figure, which could directly affect the revenue

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL RISK MANAGEMENT

4

generation capability of the company. the declining prices of copper would reduce its revenue

while the cost will remain same, which will directly hamper its overall profits from operation.

The evaluation also indicate that the prices of copper has been declining since January of

2018, which is not a good sign for the Medusa mining company, as it produces lots of copper

from its operations. This would directly impact its revenue generation capacity, while

hampering the overall profit that could be obtained from investment. The company is

relatively producing 3,800,000 pounds of copper from July to December, which is directly

affecting the overall revenue generation capability of the company due to the fluctuations in

copper price. Further decline in the, price would directly affect its profits, as the cost of

producing the copper remains constant. hence the use of hedging measure would eventually

help the organization to minimize the negative impact from commodity market risk and

maintain its profitability (Titman, Keown and Martin 2017).

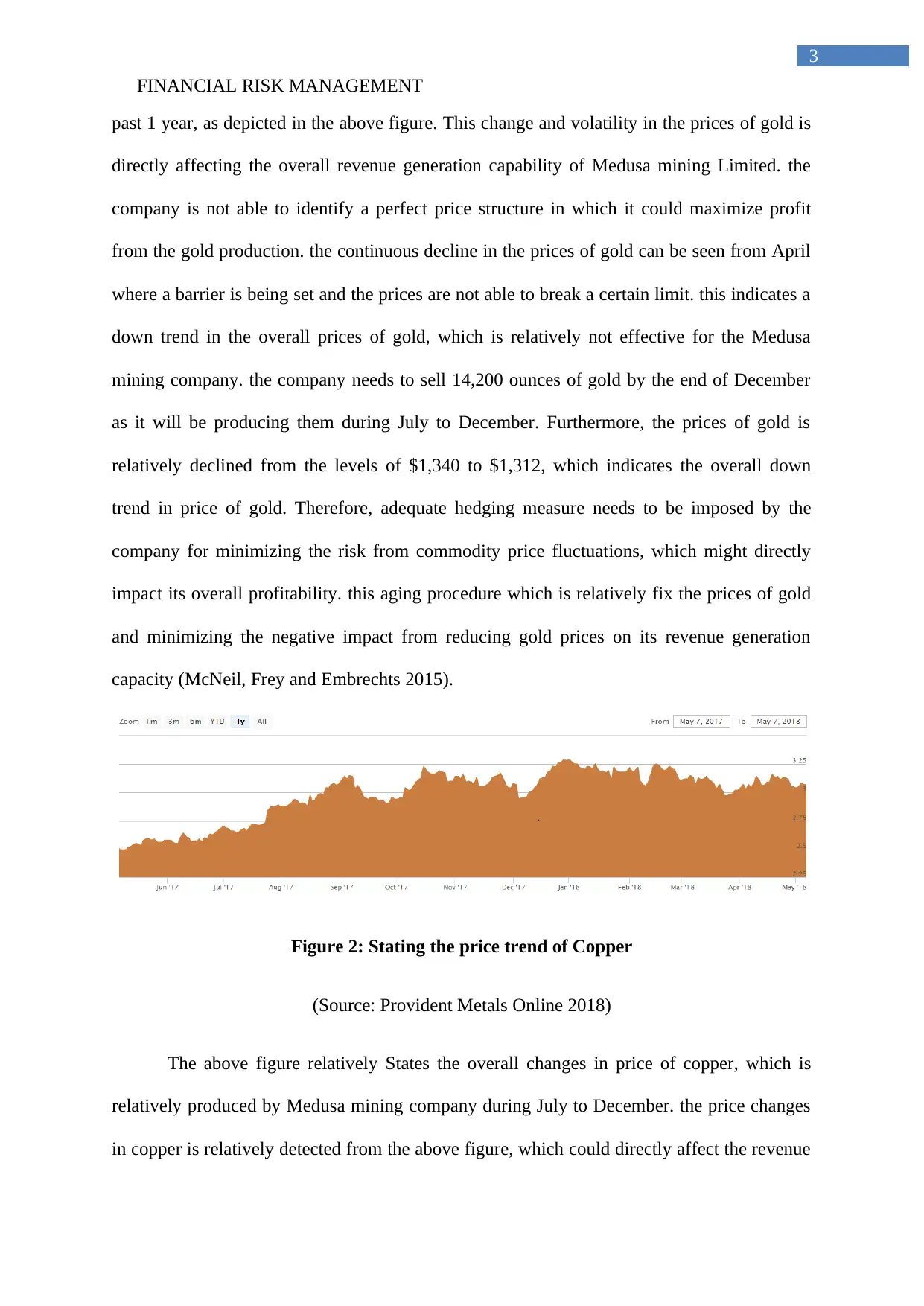

Interest Rate Risk:

Figure 3: Stating the change in US Dollar Libor Rate

(Source: Tradingeconomics.com 2018)

4

generation capability of the company. the declining prices of copper would reduce its revenue

while the cost will remain same, which will directly hamper its overall profits from operation.

The evaluation also indicate that the prices of copper has been declining since January of

2018, which is not a good sign for the Medusa mining company, as it produces lots of copper

from its operations. This would directly impact its revenue generation capacity, while

hampering the overall profit that could be obtained from investment. The company is

relatively producing 3,800,000 pounds of copper from July to December, which is directly

affecting the overall revenue generation capability of the company due to the fluctuations in

copper price. Further decline in the, price would directly affect its profits, as the cost of

producing the copper remains constant. hence the use of hedging measure would eventually

help the organization to minimize the negative impact from commodity market risk and

maintain its profitability (Titman, Keown and Martin 2017).

Interest Rate Risk:

Figure 3: Stating the change in US Dollar Libor Rate

(Source: Tradingeconomics.com 2018)

FINANCIAL RISK MANAGEMENT

5

The change in US dollar LIBOR rate can be identified from the above figure, which

has constantly increased over the period of 2 years. This mainly indicates the change in the

overall interest rates of banks regarding the different types of loans provided to companies.

the Medusa mining company has relatively accumulated loans from US bank, who is overall

interest rates changes with the change in US dollar LIBOR rate. The changes in the overall

bank interest rate would directly affect interest payments over the period of 12 months, where

the high volatility in the US dollar LIBOR rate would increase the cash outflow of the

organization, as interest payments. the company has taken a loan of $600 million for

supporting its operations in the mind field, where the price fluctuations is affecting its

profitability and this increment interest rate would hamper the maintenance of adequate

profits. Therefore, using the adequate hedging measure will reduce the risk from rising

interest rate that would minimize risk and improve profitability of the organization (Olson

and Wu 2017).

Foreign Exchange Risk:

Figure 4: Stating the change in AUD/EUR value

(Source: Xe.com 2018)

5

The change in US dollar LIBOR rate can be identified from the above figure, which

has constantly increased over the period of 2 years. This mainly indicates the change in the

overall interest rates of banks regarding the different types of loans provided to companies.

the Medusa mining company has relatively accumulated loans from US bank, who is overall

interest rates changes with the change in US dollar LIBOR rate. The changes in the overall

bank interest rate would directly affect interest payments over the period of 12 months, where

the high volatility in the US dollar LIBOR rate would increase the cash outflow of the

organization, as interest payments. the company has taken a loan of $600 million for

supporting its operations in the mind field, where the price fluctuations is affecting its

profitability and this increment interest rate would hamper the maintenance of adequate

profits. Therefore, using the adequate hedging measure will reduce the risk from rising

interest rate that would minimize risk and improve profitability of the organization (Olson

and Wu 2017).

Foreign Exchange Risk:

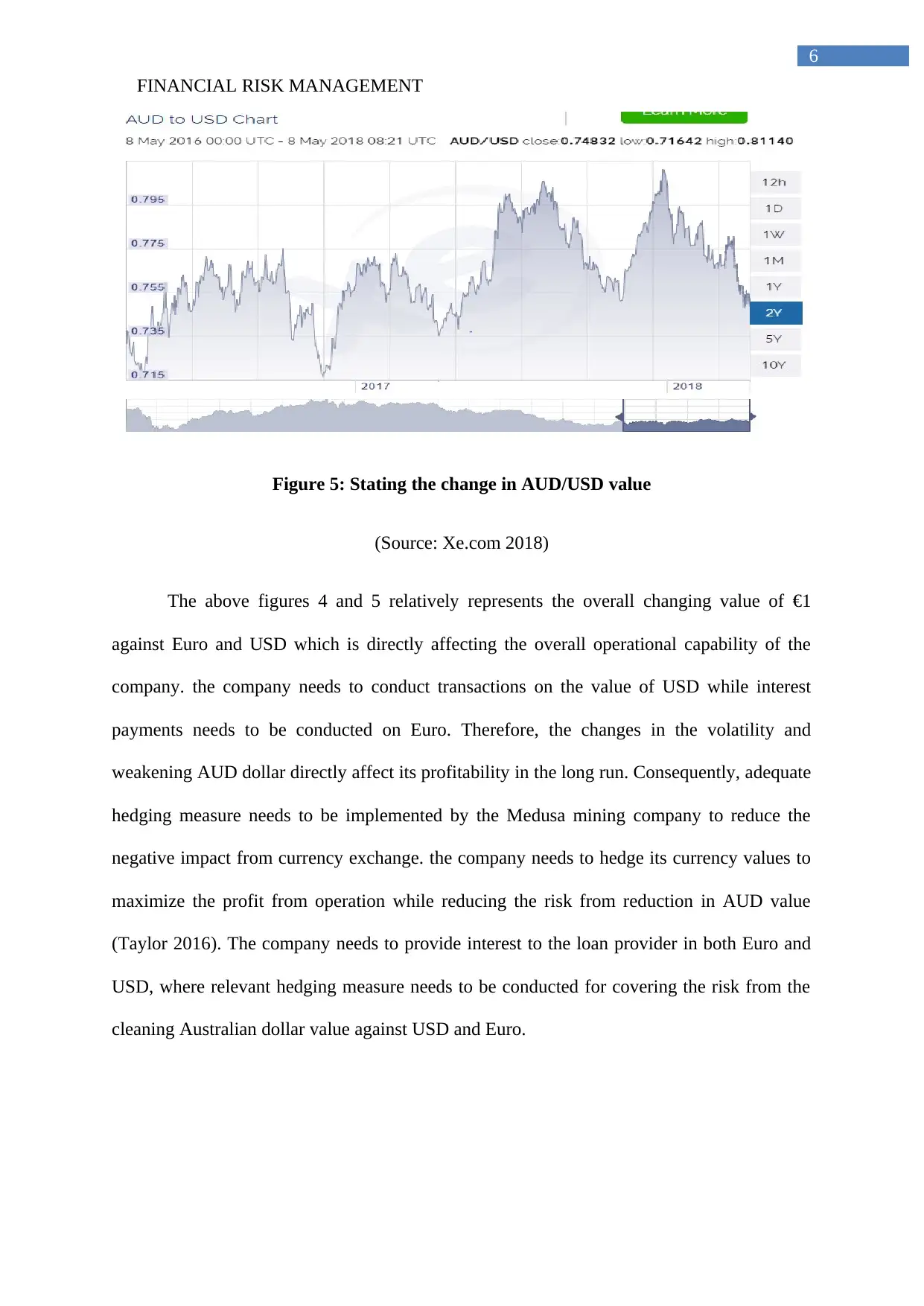

Figure 4: Stating the change in AUD/EUR value

(Source: Xe.com 2018)

FINANCIAL RISK MANAGEMENT

6

Figure 5: Stating the change in AUD/USD value

(Source: Xe.com 2018)

The above figures 4 and 5 relatively represents the overall changing value of €1

against Euro and USD which is directly affecting the overall operational capability of the

company. the company needs to conduct transactions on the value of USD while interest

payments needs to be conducted on Euro. Therefore, the changes in the volatility and

weakening AUD dollar directly affect its profitability in the long run. Consequently, adequate

hedging measure needs to be implemented by the Medusa mining company to reduce the

negative impact from currency exchange. the company needs to hedge its currency values to

maximize the profit from operation while reducing the risk from reduction in AUD value

(Taylor 2016). The company needs to provide interest to the loan provider in both Euro and

USD, where relevant hedging measure needs to be conducted for covering the risk from the

cleaning Australian dollar value against USD and Euro.

6

Figure 5: Stating the change in AUD/USD value

(Source: Xe.com 2018)

The above figures 4 and 5 relatively represents the overall changing value of €1

against Euro and USD which is directly affecting the overall operational capability of the

company. the company needs to conduct transactions on the value of USD while interest

payments needs to be conducted on Euro. Therefore, the changes in the volatility and

weakening AUD dollar directly affect its profitability in the long run. Consequently, adequate

hedging measure needs to be implemented by the Medusa mining company to reduce the

negative impact from currency exchange. the company needs to hedge its currency values to

maximize the profit from operation while reducing the risk from reduction in AUD value

(Taylor 2016). The company needs to provide interest to the loan provider in both Euro and

USD, where relevant hedging measure needs to be conducted for covering the risk from the

cleaning Australian dollar value against USD and Euro.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL RISK MANAGEMENT

7

b) The recommendations on the hedging percentage and process that needs to be

followed by Medusa mining company:

From the evaluation of the overall changes in gold prices adequate hedging measure

needs to be implemented by Medusa mining company. However, the current price levels of

Gold are adequate for the mining company, which needs to be hatched for minimizing its

impact on future price changes. The company needs to hedge its gold exposure by 75%,

which will fix the overall Prices for gold and the remaining 25% could be used for tapping on

the opportunities of rising gold price. this overall measure would eventually help Medusa

mining company to minimize the risk from volatile gold prices and maximize their profits in

future. the production level can be continued by Medusa mining company as the exposure of

gold prices has been hedged adequately for maximizing the profits even if the prices of gold

the clients in future (Wolke 2017).

The changes in price volatility of copper also indicates that the organization needs to

conduct and hedging procedure where the security of profits from copper production is

maintain. The company directly needs to Hedge 60% of the overall copper values to

effectively minimize the negative impact from changes of copper price. This would

eventually provide the organization with adequate heading provisions to minimize the risk

from arising copper prices. The Other 40% of the copper value is not, as the rising prices of

copper could allow the organization to tap into the new profit that would be generated from

positive value.

Moreover, the interest payment rates conducted by the company needs to be held fully

for reducing the negative impact rising LIBOR rates. hatching the whole interest repayment

of 3-month US dollar LIBOR that would eventually help the management to minimize the

possibility of extra interest payments by the organization.

7

b) The recommendations on the hedging percentage and process that needs to be

followed by Medusa mining company:

From the evaluation of the overall changes in gold prices adequate hedging measure

needs to be implemented by Medusa mining company. However, the current price levels of

Gold are adequate for the mining company, which needs to be hatched for minimizing its

impact on future price changes. The company needs to hedge its gold exposure by 75%,

which will fix the overall Prices for gold and the remaining 25% could be used for tapping on

the opportunities of rising gold price. this overall measure would eventually help Medusa

mining company to minimize the risk from volatile gold prices and maximize their profits in

future. the production level can be continued by Medusa mining company as the exposure of

gold prices has been hedged adequately for maximizing the profits even if the prices of gold

the clients in future (Wolke 2017).

The changes in price volatility of copper also indicates that the organization needs to

conduct and hedging procedure where the security of profits from copper production is

maintain. The company directly needs to Hedge 60% of the overall copper values to

effectively minimize the negative impact from changes of copper price. This would

eventually provide the organization with adequate heading provisions to minimize the risk

from arising copper prices. The Other 40% of the copper value is not, as the rising prices of

copper could allow the organization to tap into the new profit that would be generated from

positive value.

Moreover, the interest payment rates conducted by the company needs to be held fully

for reducing the negative impact rising LIBOR rates. hatching the whole interest repayment

of 3-month US dollar LIBOR that would eventually help the management to minimize the

possibility of extra interest payments by the organization.

FINANCIAL RISK MANAGEMENT

8

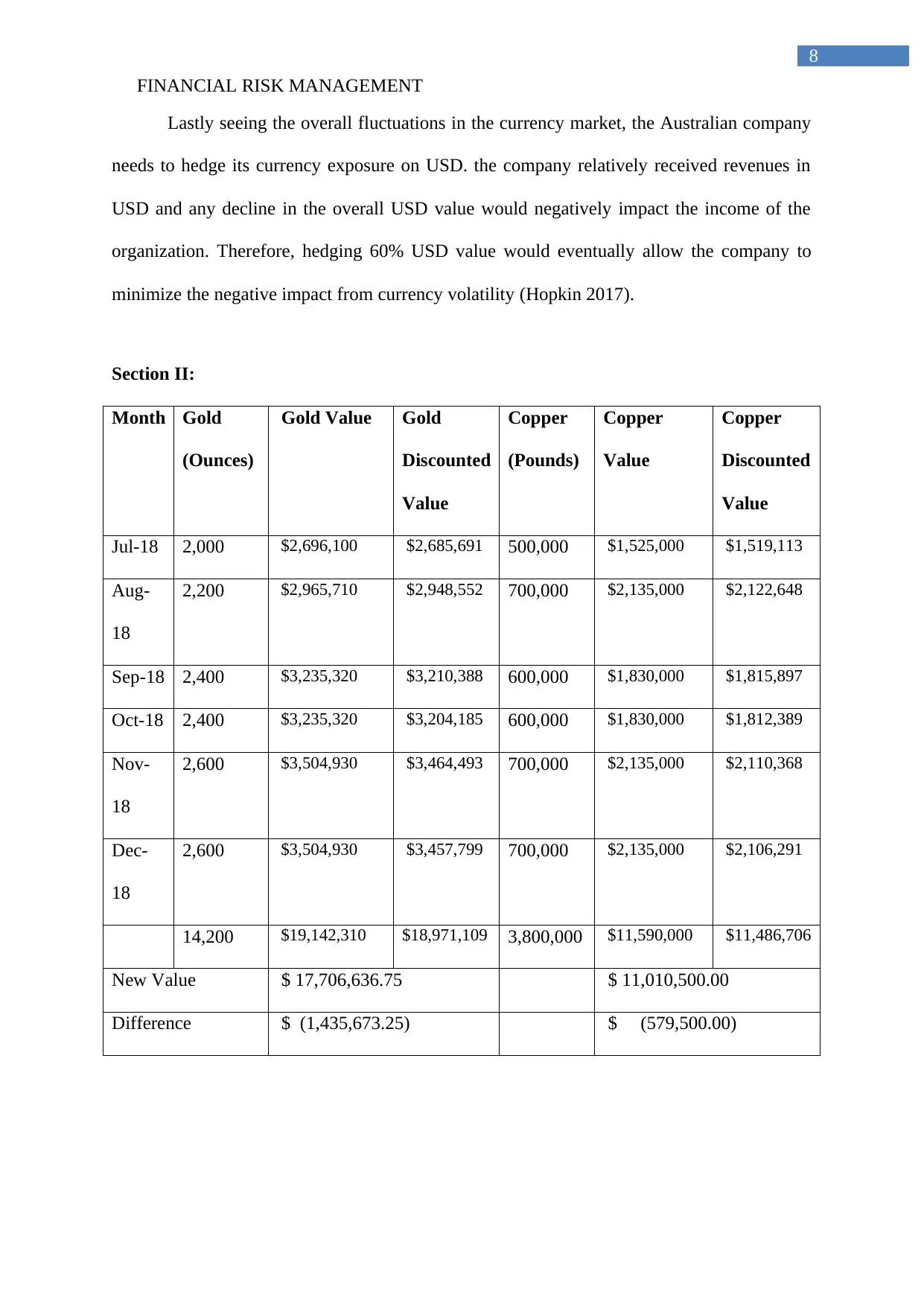

Lastly seeing the overall fluctuations in the currency market, the Australian company

needs to hedge its currency exposure on USD. the company relatively received revenues in

USD and any decline in the overall USD value would negatively impact the income of the

organization. Therefore, hedging 60% USD value would eventually allow the company to

minimize the negative impact from currency volatility (Hopkin 2017).

Section II:

Month Gold

(Ounces)

Gold Value Gold

Discounted

Value

Copper

(Pounds)

Copper

Value

Copper

Discounted

Value

Jul-18 2,000 $2,696,100 $2,685,691 500,000 $1,525,000 $1,519,113

Aug-

18

2,200 $2,965,710 $2,948,552 700,000 $2,135,000 $2,122,648

Sep-18 2,400 $3,235,320 $3,210,388 600,000 $1,830,000 $1,815,897

Oct-18 2,400 $3,235,320 $3,204,185 600,000 $1,830,000 $1,812,389

Nov-

18

2,600 $3,504,930 $3,464,493 700,000 $2,135,000 $2,110,368

Dec-

18

2,600 $3,504,930 $3,457,799 700,000 $2,135,000 $2,106,291

14,200 $19,142,310 $18,971,109 3,800,000 $11,590,000 $11,486,706

New Value $ 17,706,636.75 $ 11,010,500.00

Difference $ (1,435,673.25) $ (579,500.00)

8

Lastly seeing the overall fluctuations in the currency market, the Australian company

needs to hedge its currency exposure on USD. the company relatively received revenues in

USD and any decline in the overall USD value would negatively impact the income of the

organization. Therefore, hedging 60% USD value would eventually allow the company to

minimize the negative impact from currency volatility (Hopkin 2017).

Section II:

Month Gold

(Ounces)

Gold Value Gold

Discounted

Value

Copper

(Pounds)

Copper

Value

Copper

Discounted

Value

Jul-18 2,000 $2,696,100 $2,685,691 500,000 $1,525,000 $1,519,113

Aug-

18

2,200 $2,965,710 $2,948,552 700,000 $2,135,000 $2,122,648

Sep-18 2,400 $3,235,320 $3,210,388 600,000 $1,830,000 $1,815,897

Oct-18 2,400 $3,235,320 $3,204,185 600,000 $1,830,000 $1,812,389

Nov-

18

2,600 $3,504,930 $3,464,493 700,000 $2,135,000 $2,110,368

Dec-

18

2,600 $3,504,930 $3,457,799 700,000 $2,135,000 $2,106,291

14,200 $19,142,310 $18,971,109 3,800,000 $11,590,000 $11,486,706

New Value $ 17,706,636.75 $ 11,010,500.00

Difference $ (1,435,673.25) $ (579,500.00)

FINANCIAL RISK MANAGEMENT

9

c) Stating the recommendations on derivatives instruments for implementing the

hedges:

From the valuation of above risk identified for Medusa mining company Adequate

hedging procedure needs to be conducted with the help of derivative instruments. these

derivative instruments would eventually help in minimizing the negative impact from

changing prices and improve profitability of the organization. The first hedging measure that

need to be implemented by Medusa mining company is on gold. where shorting the future

contracts of gold consisting of 75% of the overall production would eventually help to fixate

the selling price of the product. This would eventually help the organization to mitigate any

kind of risk from future declining prices of gold. The other 25% of the of the gold value is to

tap into the rising prices of gold and improve profitability of the organization. The future

contracts of gold need to be sold by Medusa mining company for effectively controlling its

hedging measure and minimize any risk from volatile commodity market (Ho et al. 2015).

Moreover, advertising measure on copper prices needs to be conducted by Medusa

mining company for effectively improving the level of profit from operations. The company

directly needs to hedge copper value by 60% of the total production that will be conducted

from July to December. The declining prices of copper needs to be hedged by shorting the

future contract, where the overall prices of copper will be fixated, while minimizing the risk

from overall operation. The remaining 40% of the overall copper value will not be hedged, as

the organization needs to tap into the rising prices of copper in future. This would eventually

allow the organization to minimize the negative impact of declining prices while improving

the level of profits that could be generated from copper production.

Medusa mining company also needs to hedge adequately in the Australian dollars

where its volatility is it directly affecting its capability to generate revenue from operation.

the volatile Australian currency value is directly affecting the ability of the organization to

9

c) Stating the recommendations on derivatives instruments for implementing the

hedges:

From the valuation of above risk identified for Medusa mining company Adequate

hedging procedure needs to be conducted with the help of derivative instruments. these

derivative instruments would eventually help in minimizing the negative impact from

changing prices and improve profitability of the organization. The first hedging measure that

need to be implemented by Medusa mining company is on gold. where shorting the future

contracts of gold consisting of 75% of the overall production would eventually help to fixate

the selling price of the product. This would eventually help the organization to mitigate any

kind of risk from future declining prices of gold. The other 25% of the of the gold value is to

tap into the rising prices of gold and improve profitability of the organization. The future

contracts of gold need to be sold by Medusa mining company for effectively controlling its

hedging measure and minimize any risk from volatile commodity market (Ho et al. 2015).

Moreover, advertising measure on copper prices needs to be conducted by Medusa

mining company for effectively improving the level of profit from operations. The company

directly needs to hedge copper value by 60% of the total production that will be conducted

from July to December. The declining prices of copper needs to be hedged by shorting the

future contract, where the overall prices of copper will be fixated, while minimizing the risk

from overall operation. The remaining 40% of the overall copper value will not be hedged, as

the organization needs to tap into the rising prices of copper in future. This would eventually

allow the organization to minimize the negative impact of declining prices while improving

the level of profits that could be generated from copper production.

Medusa mining company also needs to hedge adequately in the Australian dollars

where its volatility is it directly affecting its capability to generate revenue from operation.

the volatile Australian currency value is directly affecting the ability of the organization to

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

FINANCIAL RISK MANAGEMENT

10

acquire the required revenue by selling gold and copper in the commodity market.

Furthermore, 50% of the overall currency value that will be converted from USD needs to be

hedged by Medusa mining companies using put options where the strengthening of

Australian dollars would directly affect its operations. Therefore, any kind of increment in the

values of AUD negatively affecting the USD would be hedged and the organization would

you receive adequate payment from its export. In this context, Chance and Brooks (2015)

stated that with the use of adequate hedging measure organizations are able to minimize the

risk from operation and maximize the profit that could be generated in future.

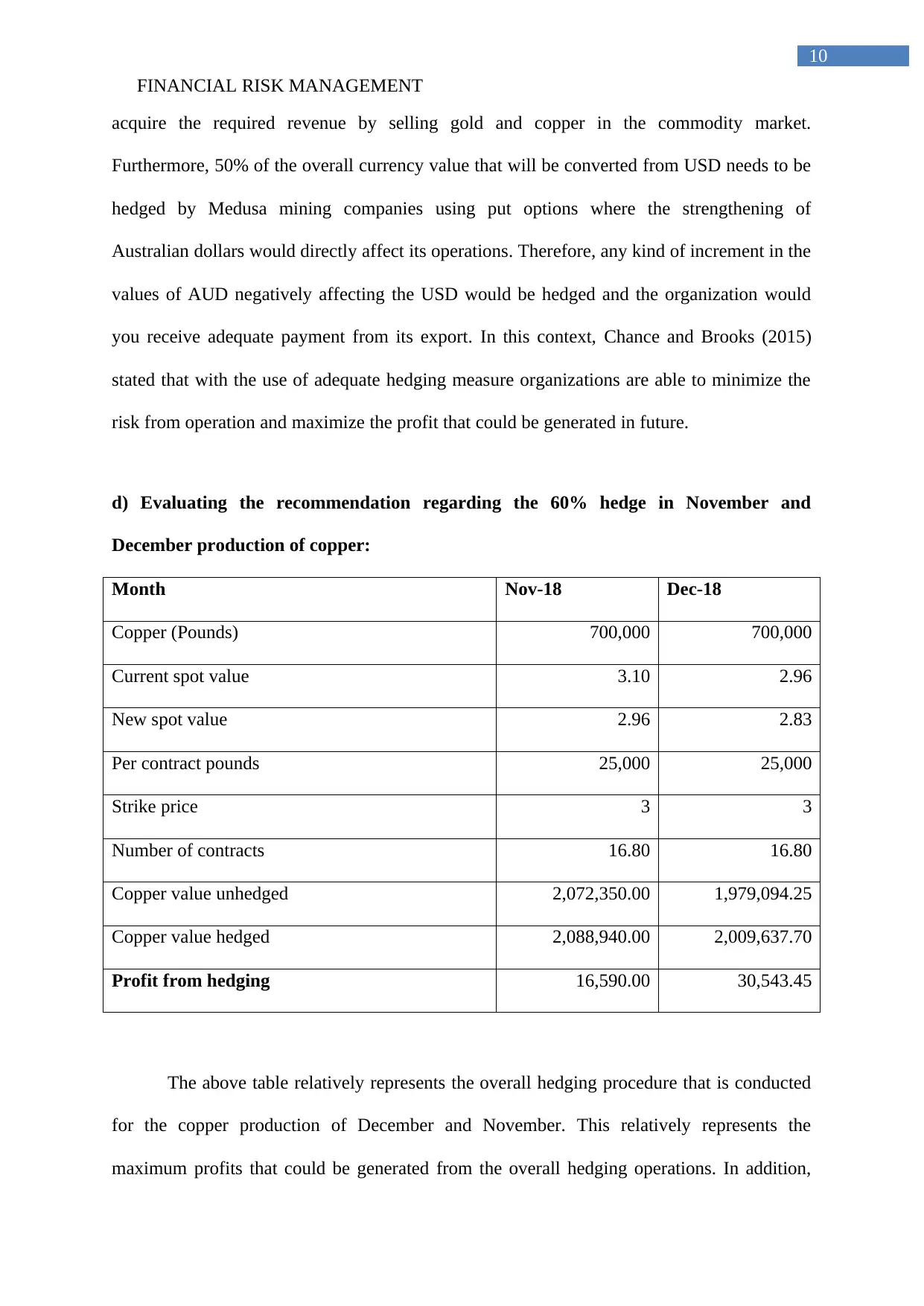

d) Evaluating the recommendation regarding the 60% hedge in November and

December production of copper:

Month Nov-18 Dec-18

Copper (Pounds) 700,000 700,000

Current spot value 3.10 2.96

New spot value 2.96 2.83

Per contract pounds 25,000 25,000

Strike price 3 3

Number of contracts 16.80 16.80

Copper value unhedged 2,072,350.00 1,979,094.25

Copper value hedged 2,088,940.00 2,009,637.70

Profit from hedging 16,590.00 30,543.45

The above table relatively represents the overall hedging procedure that is conducted

for the copper production of December and November. This relatively represents the

maximum profits that could be generated from the overall hedging operations. In addition,

10

acquire the required revenue by selling gold and copper in the commodity market.

Furthermore, 50% of the overall currency value that will be converted from USD needs to be

hedged by Medusa mining companies using put options where the strengthening of

Australian dollars would directly affect its operations. Therefore, any kind of increment in the

values of AUD negatively affecting the USD would be hedged and the organization would

you receive adequate payment from its export. In this context, Chance and Brooks (2015)

stated that with the use of adequate hedging measure organizations are able to minimize the

risk from operation and maximize the profit that could be generated in future.

d) Evaluating the recommendation regarding the 60% hedge in November and

December production of copper:

Month Nov-18 Dec-18

Copper (Pounds) 700,000 700,000

Current spot value 3.10 2.96

New spot value 2.96 2.83

Per contract pounds 25,000 25,000

Strike price 3 3

Number of contracts 16.80 16.80

Copper value unhedged 2,072,350.00 1,979,094.25

Copper value hedged 2,088,940.00 2,009,637.70

Profit from hedging 16,590.00 30,543.45

The above table relatively represents the overall hedging procedure that is conducted

for the copper production of December and November. This relatively represents the

maximum profits that could be generated from the overall hedging operations. In addition,

FINANCIAL RISK MANAGEMENT

11

the prophets that is generated relatively reduces the overall of that might and if the company

did not use any kind of hedging procedures for their copper production. DeAngelo and Stulz

(2015) mention that with the help of nursing procedures companies are able to minimize risk

from volatile prices while increasing returns from investment. Hence, with the help of above

hedging measure the overall profit from the operations of copper can be conducted, as there is

an anticipation of copper prices to decline in future. Therefore, the hedging process would

eventually help Medusa mining company to maximize the profits that could be generated

from its operations by minimizing the negative impact of declining copper prices.

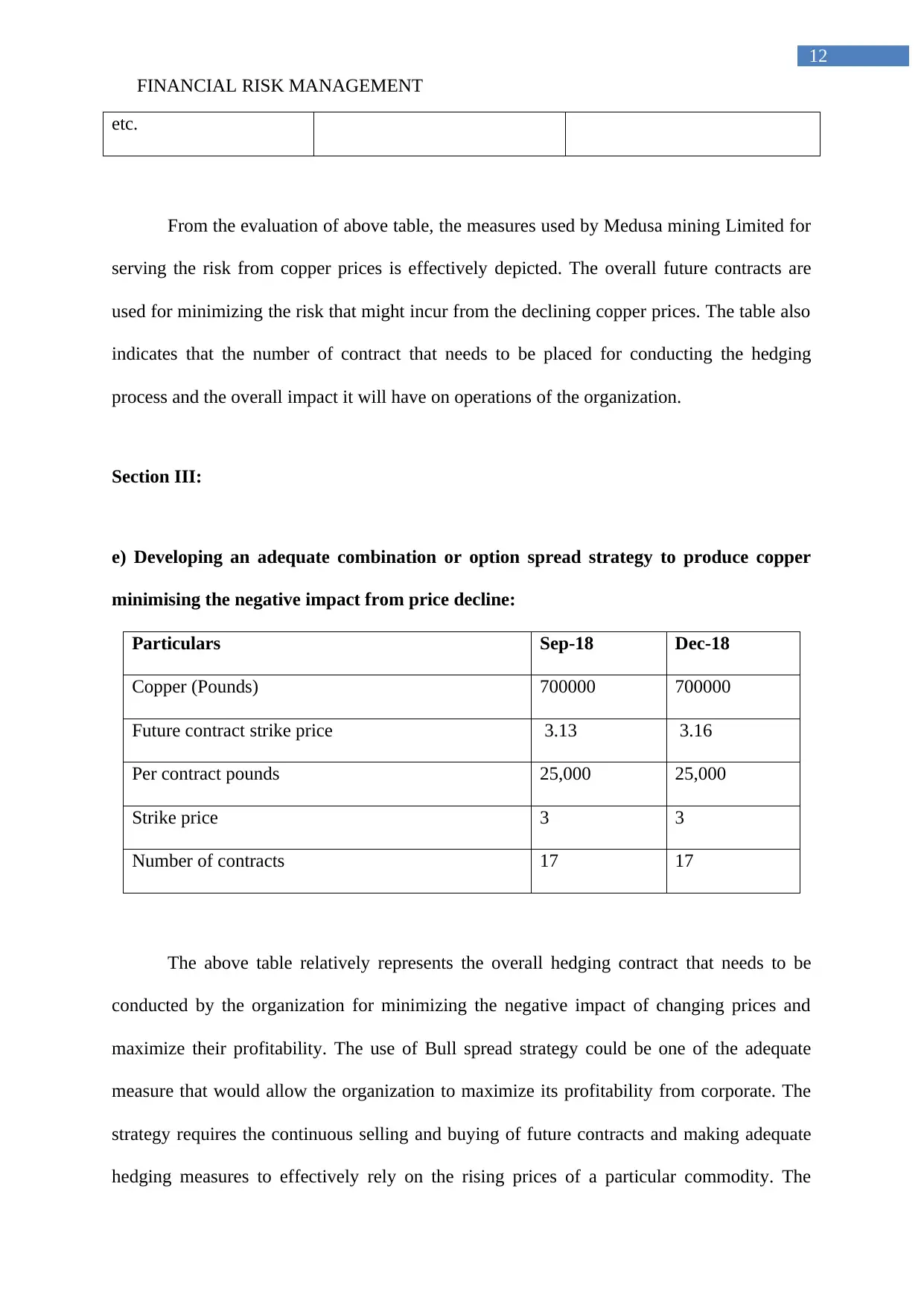

Type of Risk Price Change risk Price Change risk

Exposure to be hedged 700,000 700,000

Proportion of the

exposure to be hedged

420,000 420,000

Derivatives i.e.

Futures/or Options etc.

Futures Futures

Explain the choice of

derivative

instrument/strategy

The future contract will fix the

selling price of copper and

allow the organisation to

minimise the negative impact

from price volatility

The future contract will fix the

selling price of copper and

allow the organisation to

minimise the negative impact

from price volatility

No. of Contracts 420,000 / 25000 = 17 420,000 / 25000 = 17

Contract months Nov-18 Dec-18

Long/short/ Put/Call Short Short

Strike Prices,

premiums/Futures prices

3 3

11

the prophets that is generated relatively reduces the overall of that might and if the company

did not use any kind of hedging procedures for their copper production. DeAngelo and Stulz

(2015) mention that with the help of nursing procedures companies are able to minimize risk

from volatile prices while increasing returns from investment. Hence, with the help of above

hedging measure the overall profit from the operations of copper can be conducted, as there is

an anticipation of copper prices to decline in future. Therefore, the hedging process would

eventually help Medusa mining company to maximize the profits that could be generated

from its operations by minimizing the negative impact of declining copper prices.

Type of Risk Price Change risk Price Change risk

Exposure to be hedged 700,000 700,000

Proportion of the

exposure to be hedged

420,000 420,000

Derivatives i.e.

Futures/or Options etc.

Futures Futures

Explain the choice of

derivative

instrument/strategy

The future contract will fix the

selling price of copper and

allow the organisation to

minimise the negative impact

from price volatility

The future contract will fix the

selling price of copper and

allow the organisation to

minimise the negative impact

from price volatility

No. of Contracts 420,000 / 25000 = 17 420,000 / 25000 = 17

Contract months Nov-18 Dec-18

Long/short/ Put/Call Short Short

Strike Prices,

premiums/Futures prices

3 3

FINANCIAL RISK MANAGEMENT

12

etc.

From the evaluation of above table, the measures used by Medusa mining Limited for

serving the risk from copper prices is effectively depicted. The overall future contracts are

used for minimizing the risk that might incur from the declining copper prices. The table also

indicates that the number of contract that needs to be placed for conducting the hedging

process and the overall impact it will have on operations of the organization.

Section III:

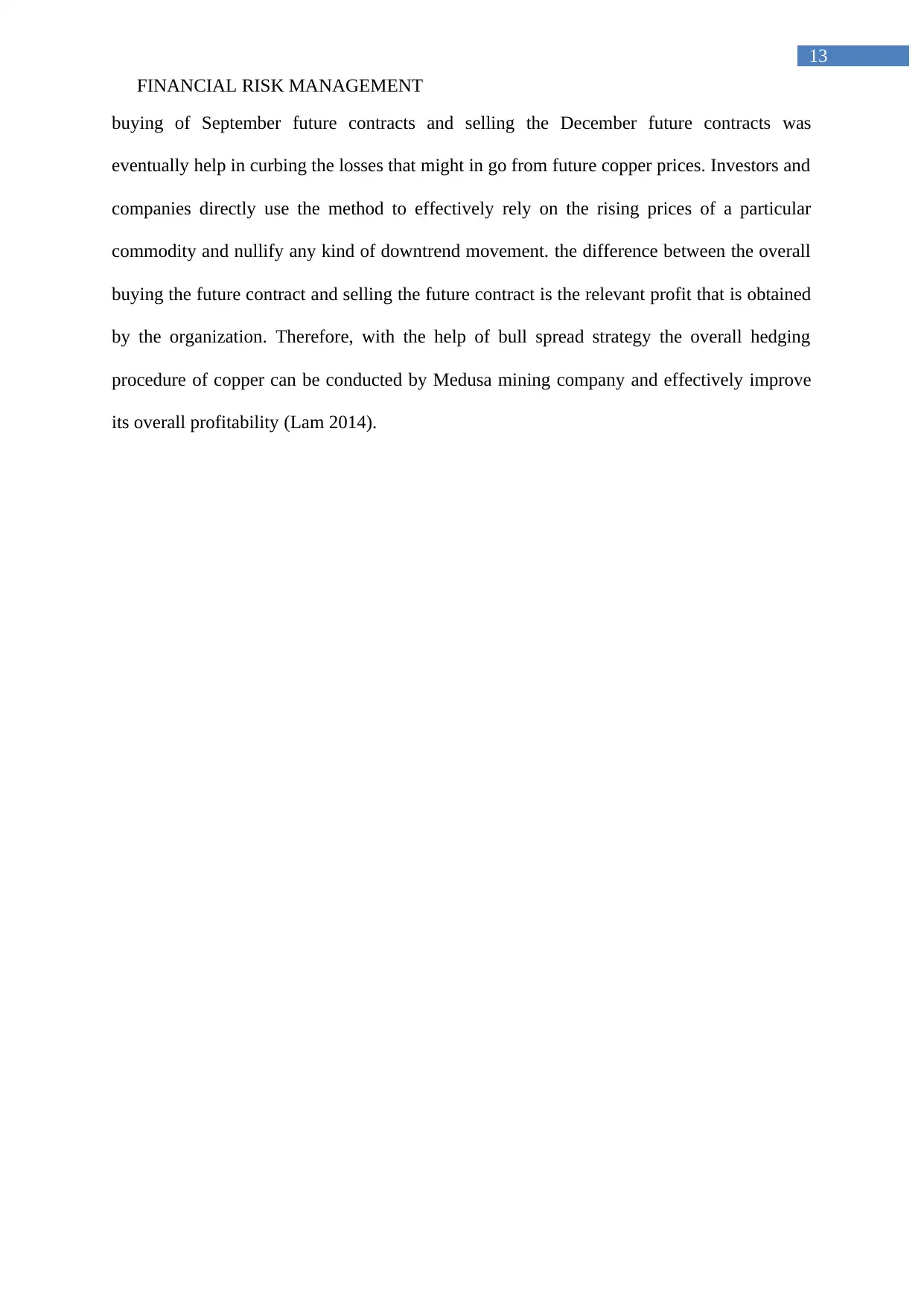

e) Developing an adequate combination or option spread strategy to produce copper

minimising the negative impact from price decline:

Particulars Sep-18 Dec-18

Copper (Pounds) 700000 700000

Future contract strike price 3.13 3.16

Per contract pounds 25,000 25,000

Strike price 3 3

Number of contracts 17 17

The above table relatively represents the overall hedging contract that needs to be

conducted by the organization for minimizing the negative impact of changing prices and

maximize their profitability. The use of Bull spread strategy could be one of the adequate

measure that would allow the organization to maximize its profitability from corporate. The

strategy requires the continuous selling and buying of future contracts and making adequate

hedging measures to effectively rely on the rising prices of a particular commodity. The

12

etc.

From the evaluation of above table, the measures used by Medusa mining Limited for

serving the risk from copper prices is effectively depicted. The overall future contracts are

used for minimizing the risk that might incur from the declining copper prices. The table also

indicates that the number of contract that needs to be placed for conducting the hedging

process and the overall impact it will have on operations of the organization.

Section III:

e) Developing an adequate combination or option spread strategy to produce copper

minimising the negative impact from price decline:

Particulars Sep-18 Dec-18

Copper (Pounds) 700000 700000

Future contract strike price 3.13 3.16

Per contract pounds 25,000 25,000

Strike price 3 3

Number of contracts 17 17

The above table relatively represents the overall hedging contract that needs to be

conducted by the organization for minimizing the negative impact of changing prices and

maximize their profitability. The use of Bull spread strategy could be one of the adequate

measure that would allow the organization to maximize its profitability from corporate. The

strategy requires the continuous selling and buying of future contracts and making adequate

hedging measures to effectively rely on the rising prices of a particular commodity. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL RISK MANAGEMENT

13

buying of September future contracts and selling the December future contracts was

eventually help in curbing the losses that might in go from future copper prices. Investors and

companies directly use the method to effectively rely on the rising prices of a particular

commodity and nullify any kind of downtrend movement. the difference between the overall

buying the future contract and selling the future contract is the relevant profit that is obtained

by the organization. Therefore, with the help of bull spread strategy the overall hedging

procedure of copper can be conducted by Medusa mining company and effectively improve

its overall profitability (Lam 2014).

13

buying of September future contracts and selling the December future contracts was

eventually help in curbing the losses that might in go from future copper prices. Investors and

companies directly use the method to effectively rely on the rising prices of a particular

commodity and nullify any kind of downtrend movement. the difference between the overall

buying the future contract and selling the future contract is the relevant profit that is obtained

by the organization. Therefore, with the help of bull spread strategy the overall hedging

procedure of copper can be conducted by Medusa mining company and effectively improve

its overall profitability (Lam 2014).

FINANCIAL RISK MANAGEMENT

14

Reference and Bibliography:

Ahmed, S., Elsholkami, M., Elkamel, A., Du, J., Ydstie, E.B. and Douglas, P.L., 2014.

Financial risk management for new technology integration in energy planning under

uncertainty. Applied Energy, 128, pp.75-81.

Al-Tamimi, H., Miniaoui, H. and Elkelish, W.W., 2015. Financial Risk and Islamic Banks’

Performance in the Gulf Cooperation Council Countries. The International Journal of

Business and Finance Research, 9(5), pp.103-112.

Bookstaber, R.M., Glasserman, P., Iyengar, G., Luo, Y., Venkatasubramanian, V. and Zhang,

Z., 2015. Process systems engineering as a modeling paradigm for analyzing systemic risk in

financial networks.

Cerchiello, P. and Giudici, P., 2016. Big data analysis for financial risk management. Journal

of Big Data, 3(1), p.18.

Chance, D.M. and Brooks, R., 2015. Introduction to derivatives and risk management.

Cengage Learning.

Cole, S., Giné, X. and Vickery, J., 2017. How does risk management influence production

decisions? Evidence from a field experiment. The Review of Financial Studies, 30(6),

pp.1935-1970.

DeAngelo, H. and Stulz, R.M., 2015. Liquid-claim production, risk management, and bank

capital structure: Why high leverage is optimal for banks. Journal of Financial

Economics, 116(2), pp.219-236.

Giannakis, M. and Papadopoulos, T., 2016. Supply chain sustainability: A risk management

approach. International Journal of Production Economics, 171, pp.455-470.

14

Reference and Bibliography:

Ahmed, S., Elsholkami, M., Elkamel, A., Du, J., Ydstie, E.B. and Douglas, P.L., 2014.

Financial risk management for new technology integration in energy planning under

uncertainty. Applied Energy, 128, pp.75-81.

Al-Tamimi, H., Miniaoui, H. and Elkelish, W.W., 2015. Financial Risk and Islamic Banks’

Performance in the Gulf Cooperation Council Countries. The International Journal of

Business and Finance Research, 9(5), pp.103-112.

Bookstaber, R.M., Glasserman, P., Iyengar, G., Luo, Y., Venkatasubramanian, V. and Zhang,

Z., 2015. Process systems engineering as a modeling paradigm for analyzing systemic risk in

financial networks.

Cerchiello, P. and Giudici, P., 2016. Big data analysis for financial risk management. Journal

of Big Data, 3(1), p.18.

Chance, D.M. and Brooks, R., 2015. Introduction to derivatives and risk management.

Cengage Learning.

Cole, S., Giné, X. and Vickery, J., 2017. How does risk management influence production

decisions? Evidence from a field experiment. The Review of Financial Studies, 30(6),

pp.1935-1970.

DeAngelo, H. and Stulz, R.M., 2015. Liquid-claim production, risk management, and bank

capital structure: Why high leverage is optimal for banks. Journal of Financial

Economics, 116(2), pp.219-236.

Giannakis, M. and Papadopoulos, T., 2016. Supply chain sustainability: A risk management

approach. International Journal of Production Economics, 171, pp.455-470.

FINANCIAL RISK MANAGEMENT

15

Ho, W., Zheng, T., Yildiz, H. and Talluri, S., 2015. Supply chain risk management: a

literature review. International Journal of Production Research, 53(16), pp.5031-5069.

Hopkin, P., 2017. Fundamentals of risk management: understanding, evaluating and

implementing effective risk management. Kogan Page Publishers.

Kou, G., Peng, Y. and Wang, G., 2014. Evaluation of clustering algorithms for financial risk

analysis using MCDM methods. Information Sciences, 275, pp.1-12.

Lam, J., 2014. Enterprise risk management: from incentives to controls. John Wiley & Sons.

McNeil, A.J., Frey, R. and Embrechts, P., 2015. Quantitative risk management: Concepts,

techniques and tools. Princeton university press.

Olson, D.L. and Wu, D.D., 2017. Data Mining Models and Enterprise Risk Management.

In Enterprise Risk Management Models (pp. 119-132). Springer, Berlin, Heidelberg.

Provident Metals Online. (2018). Today's Copper Price: Copper Spot & Historical Prices.

[online] Available at: https://www.providentmetals.com/spot-price/chart/copper/ [Accessed

11 May 2018].

Renz, D.O. and Herman, R.D. eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Sadgrove, K., 2016. The complete guide to business risk management. Routledge.

Skoglund, J. and Chen, W., 2015. Financial risk management: Applications in market, credit,

asset and liability management and firmwide risk. John Wiley & Sons.

Taylor, J.W. and Yu, K., 2016. Using auto‐regressive logit models to forecast the exceedance

probability for financial risk management. Journal of the Royal Statistical Society: Series A

(Statistics in Society), 179(4), pp.1069-1092.

15

Ho, W., Zheng, T., Yildiz, H. and Talluri, S., 2015. Supply chain risk management: a

literature review. International Journal of Production Research, 53(16), pp.5031-5069.

Hopkin, P., 2017. Fundamentals of risk management: understanding, evaluating and

implementing effective risk management. Kogan Page Publishers.

Kou, G., Peng, Y. and Wang, G., 2014. Evaluation of clustering algorithms for financial risk

analysis using MCDM methods. Information Sciences, 275, pp.1-12.

Lam, J., 2014. Enterprise risk management: from incentives to controls. John Wiley & Sons.

McNeil, A.J., Frey, R. and Embrechts, P., 2015. Quantitative risk management: Concepts,

techniques and tools. Princeton university press.

Olson, D.L. and Wu, D.D., 2017. Data Mining Models and Enterprise Risk Management.

In Enterprise Risk Management Models (pp. 119-132). Springer, Berlin, Heidelberg.

Provident Metals Online. (2018). Today's Copper Price: Copper Spot & Historical Prices.

[online] Available at: https://www.providentmetals.com/spot-price/chart/copper/ [Accessed

11 May 2018].

Renz, D.O. and Herman, R.D. eds., 2016. The Jossey-Bass handbook of nonprofit leadership

and management. John Wiley & Sons.

Sadgrove, K., 2016. The complete guide to business risk management. Routledge.

Skoglund, J. and Chen, W., 2015. Financial risk management: Applications in market, credit,

asset and liability management and firmwide risk. John Wiley & Sons.

Taylor, J.W. and Yu, K., 2016. Using auto‐regressive logit models to forecast the exceedance

probability for financial risk management. Journal of the Royal Statistical Society: Series A

(Statistics in Society), 179(4), pp.1069-1092.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.