Comprehensive Financial Analysis Report of Big Bang Pty Ltd

VerifiedAdded on 2024/06/28

|14

|1727

|479

Report

AI Summary

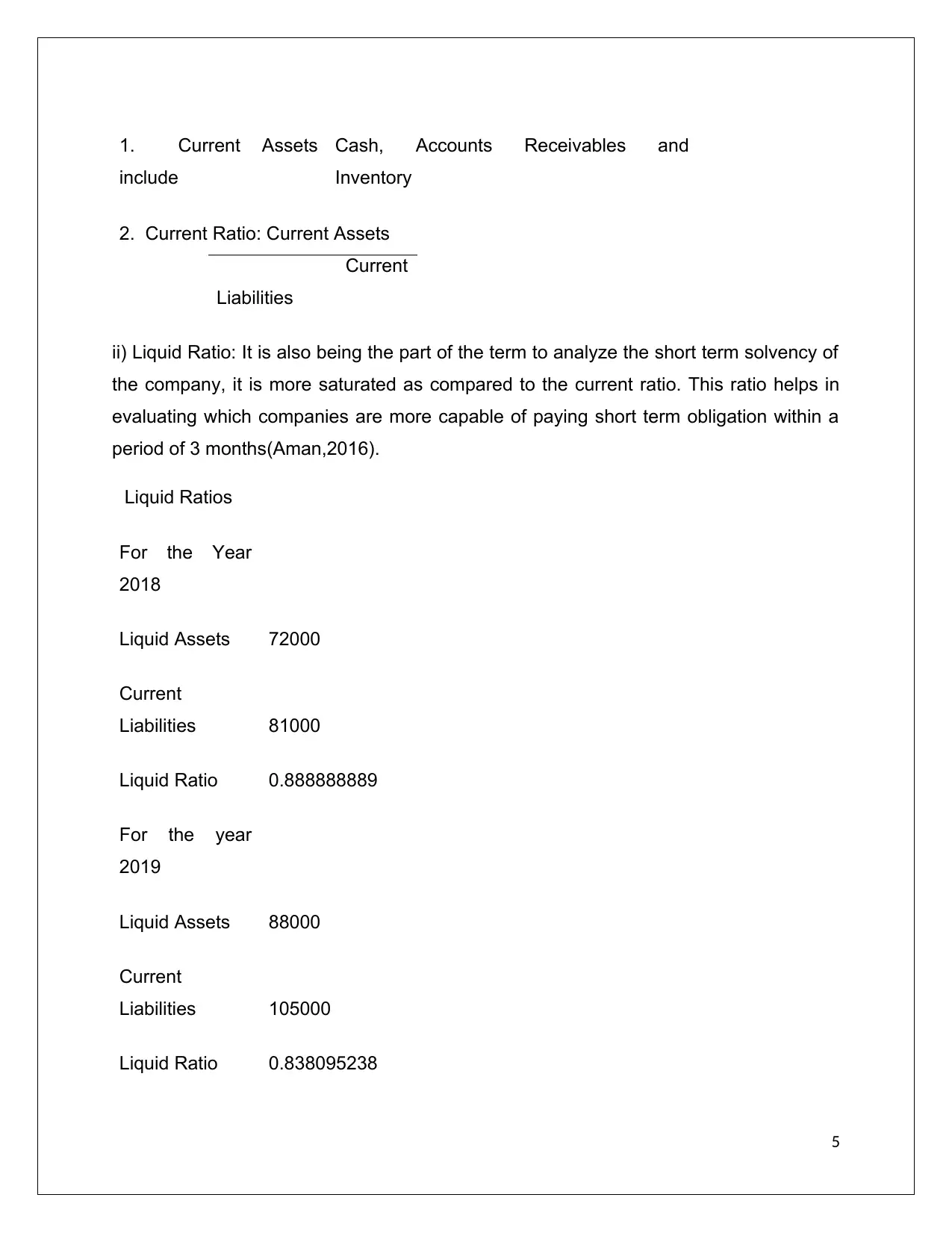

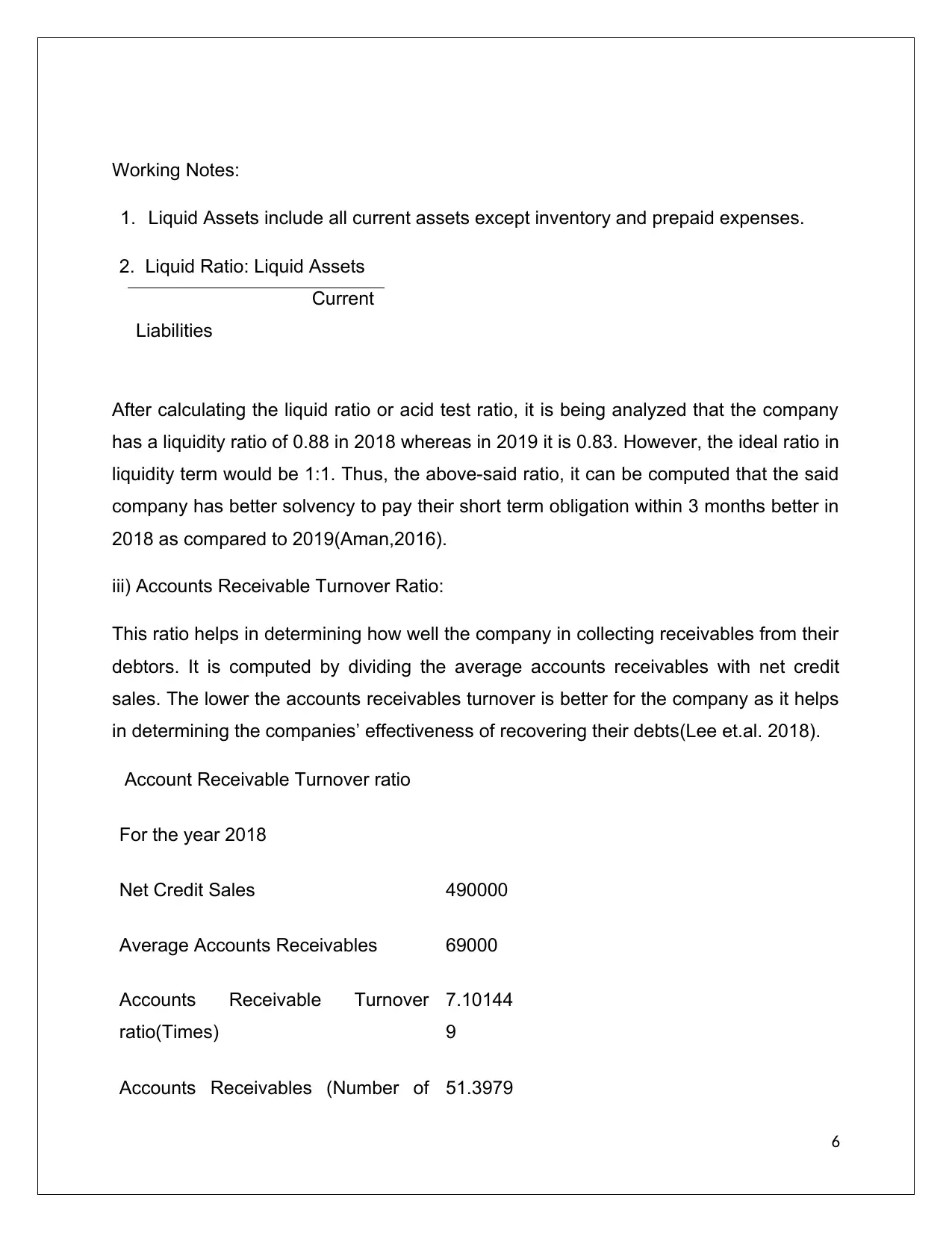

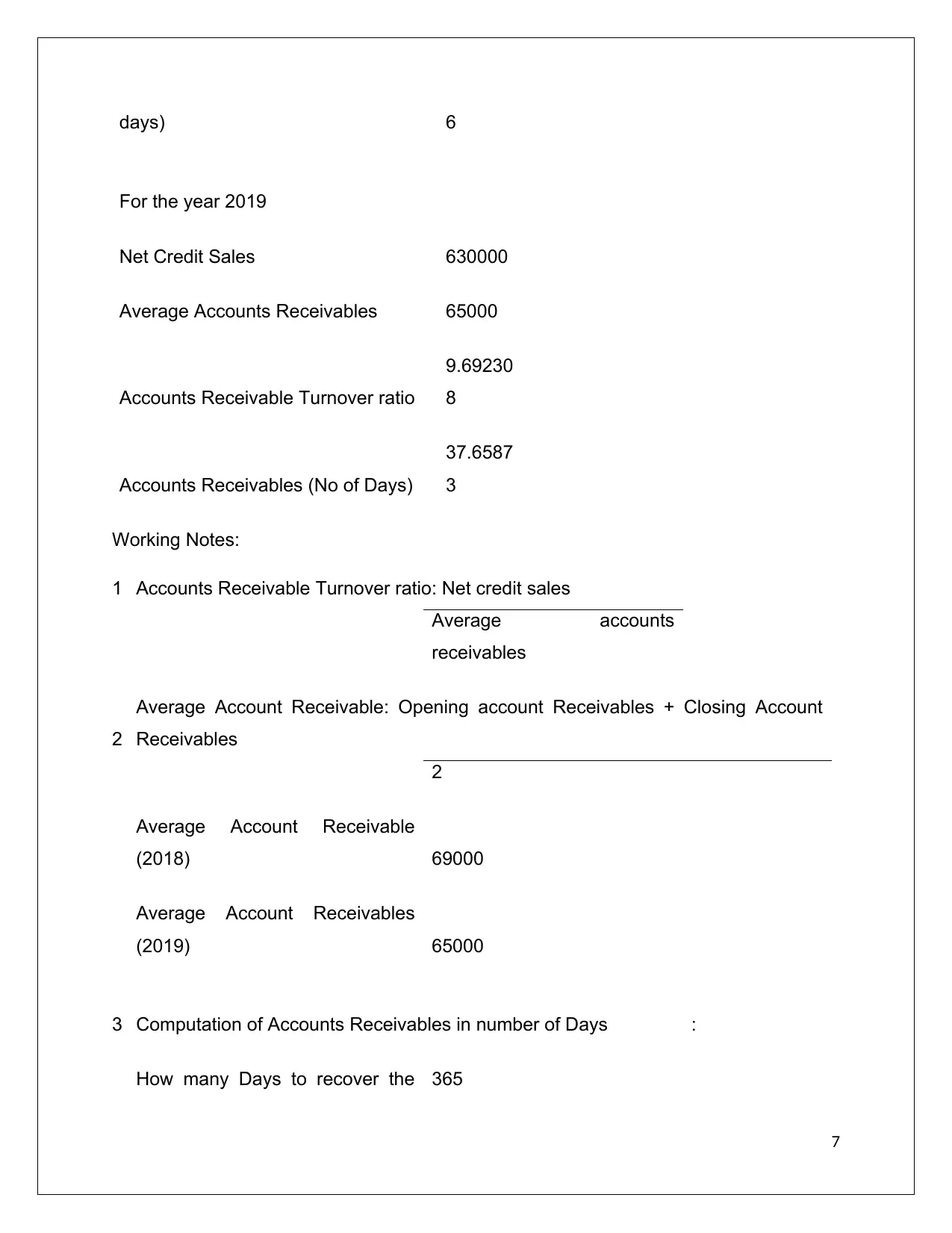

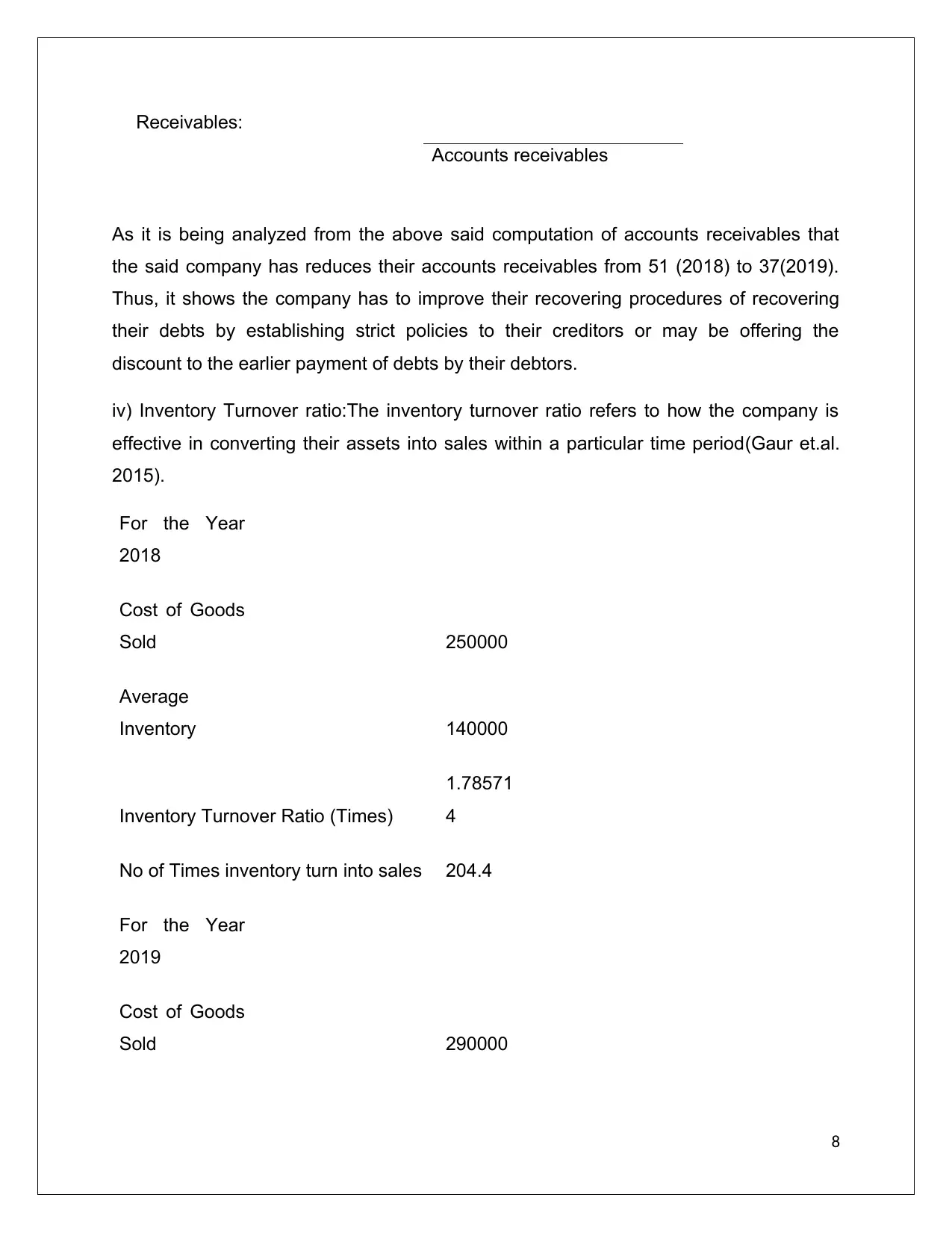

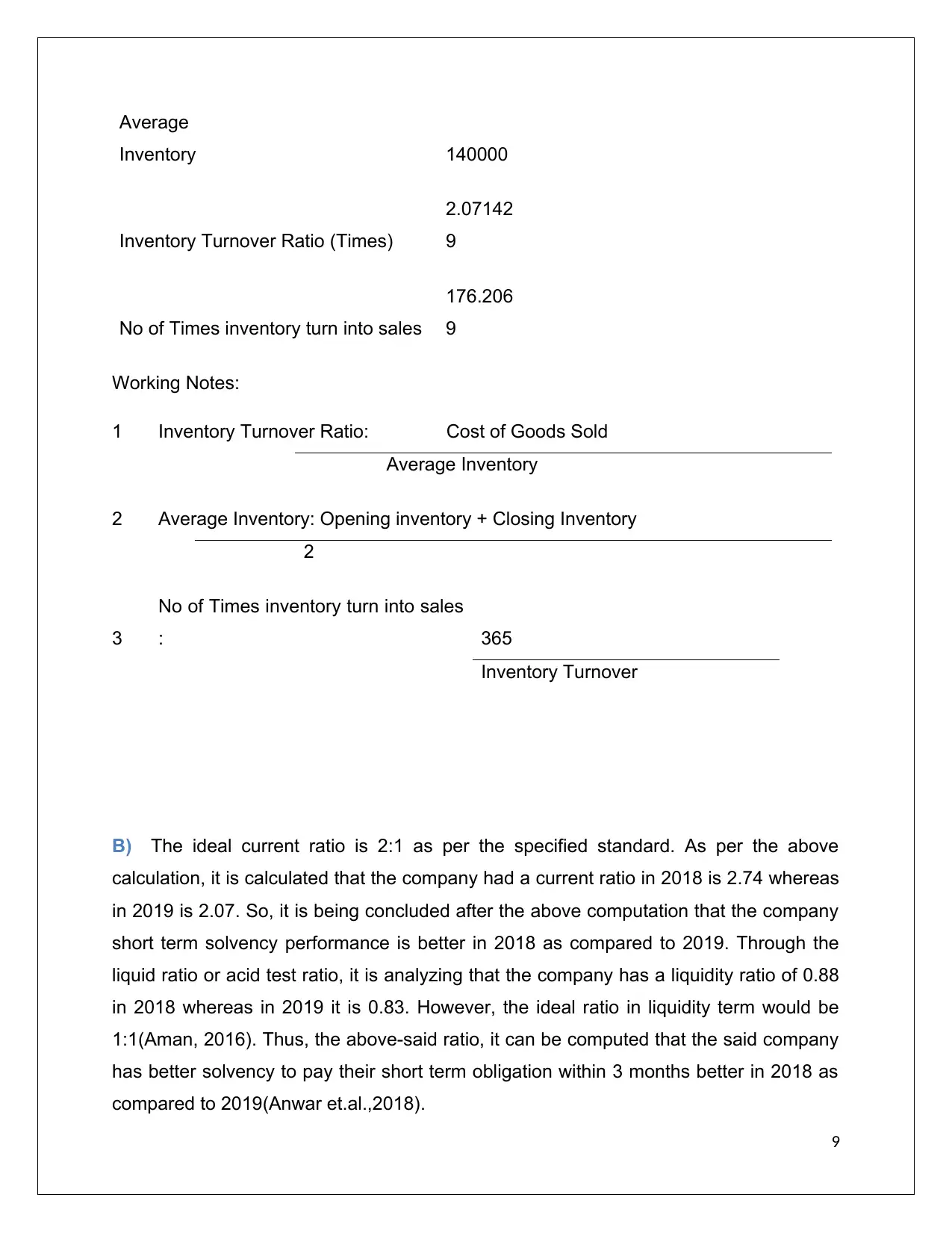

This report provides a detailed financial statement analysis of Big Bang Pty Ltd, focusing on key financial ratios such as current ratio, quick ratio, and turnover ratios. The analysis assesses the company's ability to meet its short-term obligations, comparing its performance in 2018 and 2019. Additionally, the report discusses the financial transactions of Green Apple Limited to identify income and revenue streams, and evaluates the short-term solvency of ABC Company and XYZ Company for a loan application, using net asset value method for company valuation. The findings indicate the importance of maintaining optimal financial ratios to ensure short-term solvency and attract potential investors or lenders. Desklib offers a range of similar financial analysis reports and study tools for students.

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.