FIN 6406: Financial Statement Analysis and Valuation of Lenovo

VerifiedAdded on 2023/01/16

|14

|3189

|71

Project

AI Summary

This project offers a comprehensive financial analysis of Lenovo Group Limited, examining its performance from 2014 to 2017. It begins with an overview of the company and its global operations. The analysis includes a detailed examination of financial ratios, comparing Lenovo's performance to industry averages across liquidity, solvency, asset management, and profitability metrics. The project delves into financial planning and analysis, evaluating trends and identifying strengths and weaknesses. Valuation techniques are applied, including pricing with comparables, the Capital Asset Pricing Model (CAPM) to determine the expected return, and the Weighted Average Cost of Capital (WACC). The firm's value is estimated using free cash flow analysis, incorporating a two-stage model to project future cash flows. The project concludes with recommendations based on the analysis, highlighting Lenovo's financial health and investment potential.

Running head: FINANCIAL STATEMENT ANALYSIS AND VALUAITON

Financial Statement Analysis and Valuation

Name of the Student:

Name of the University:

Author’s Note:

Financial Statement Analysis and Valuation

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL STATEMENT ANALYSIS AND VALUATION

Table of Contents

Part 1: The Company:................................................................................................................2

Part 2: Financial Planning & Analysis:......................................................................................2

Sub part 1:..............................................................................................................................2

Sub part 2:..............................................................................................................................4

Sub part 3:..............................................................................................................................5

Part 3: Pricing with Comparables..............................................................................................6

Sub part 1:..............................................................................................................................6

Sub part 2:..............................................................................................................................6

Part 4: Capital Asset Pricing Model:..........................................................................................6

Part 5: Weighted Average Cost of Capital:................................................................................7

Part 6: Estimating Firm Value:..................................................................................................8

Par 7: Strengths, Weaknesses and recommendations:...............................................................9

References and bibliography:...................................................................................................11

Table of Contents

Part 1: The Company:................................................................................................................2

Part 2: Financial Planning & Analysis:......................................................................................2

Sub part 1:..............................................................................................................................2

Sub part 2:..............................................................................................................................4

Sub part 3:..............................................................................................................................5

Part 3: Pricing with Comparables..............................................................................................6

Sub part 1:..............................................................................................................................6

Sub part 2:..............................................................................................................................6

Part 4: Capital Asset Pricing Model:..........................................................................................6

Part 5: Weighted Average Cost of Capital:................................................................................7

Part 6: Estimating Firm Value:..................................................................................................8

Par 7: Strengths, Weaknesses and recommendations:...............................................................9

References and bibliography:...................................................................................................11

2FINANCIAL STATEMENT ANALYSIS AND VALUATION

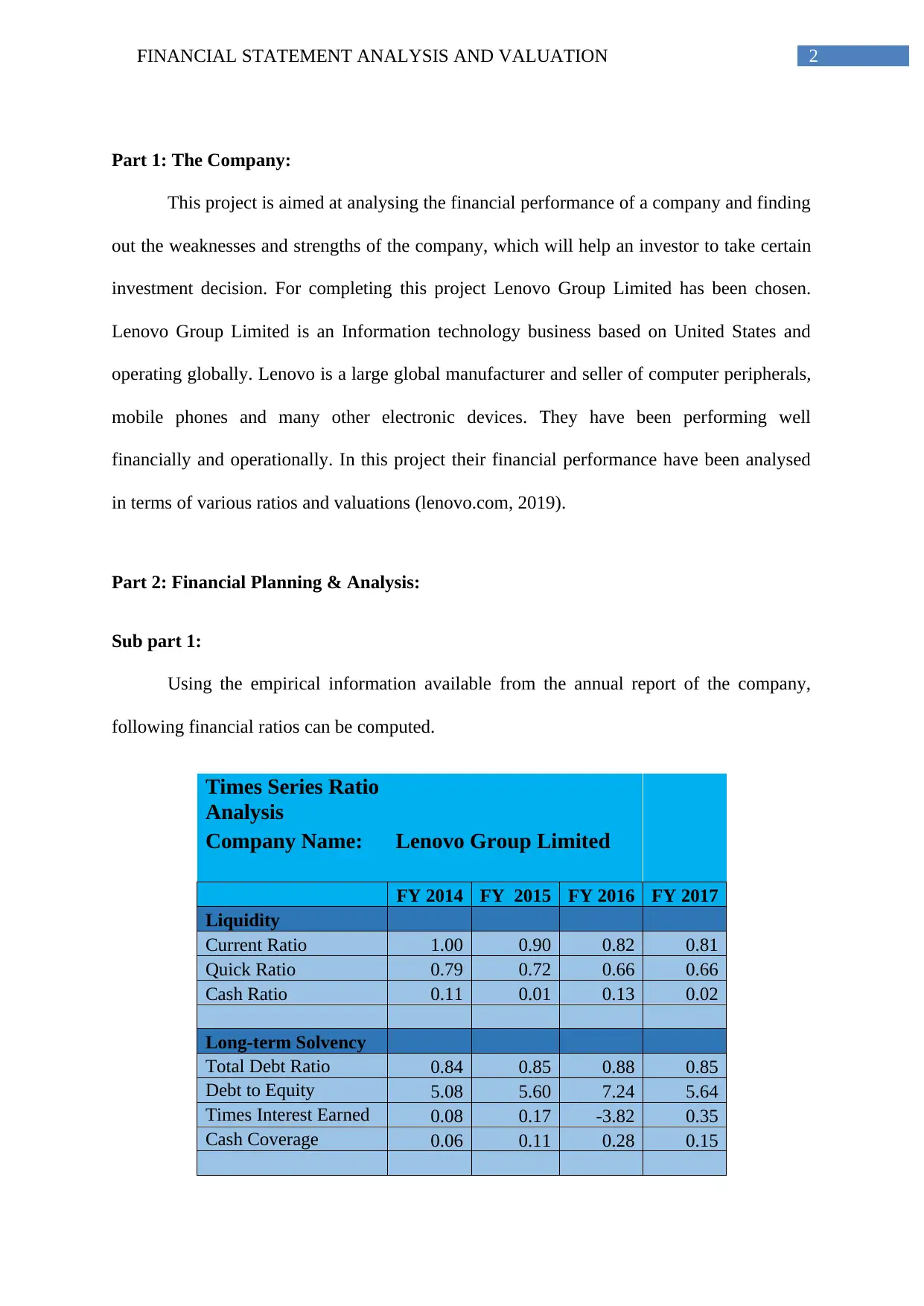

Part 1: The Company:

This project is aimed at analysing the financial performance of a company and finding

out the weaknesses and strengths of the company, which will help an investor to take certain

investment decision. For completing this project Lenovo Group Limited has been chosen.

Lenovo Group Limited is an Information technology business based on United States and

operating globally. Lenovo is a large global manufacturer and seller of computer peripherals,

mobile phones and many other electronic devices. They have been performing well

financially and operationally. In this project their financial performance have been analysed

in terms of various ratios and valuations (lenovo.com, 2019).

Part 2: Financial Planning & Analysis:

Sub part 1:

Using the empirical information available from the annual report of the company,

following financial ratios can be computed.

Times Series Ratio

Analysis

Company Name: Lenovo Group Limited

FY 2014 FY 2015 FY 2016 FY 2017

Liquidity

Current Ratio 1.00 0.90 0.82 0.81

Quick Ratio 0.79 0.72 0.66 0.66

Cash Ratio 0.11 0.01 0.13 0.02

Long-term Solvency

Total Debt Ratio 0.84 0.85 0.88 0.85

Debt to Equity 5.08 5.60 7.24 5.64

Times Interest Earned 0.08 0.17 -3.82 0.35

Cash Coverage 0.06 0.11 0.28 0.15

Part 1: The Company:

This project is aimed at analysing the financial performance of a company and finding

out the weaknesses and strengths of the company, which will help an investor to take certain

investment decision. For completing this project Lenovo Group Limited has been chosen.

Lenovo Group Limited is an Information technology business based on United States and

operating globally. Lenovo is a large global manufacturer and seller of computer peripherals,

mobile phones and many other electronic devices. They have been performing well

financially and operationally. In this project their financial performance have been analysed

in terms of various ratios and valuations (lenovo.com, 2019).

Part 2: Financial Planning & Analysis:

Sub part 1:

Using the empirical information available from the annual report of the company,

following financial ratios can be computed.

Times Series Ratio

Analysis

Company Name: Lenovo Group Limited

FY 2014 FY 2015 FY 2016 FY 2017

Liquidity

Current Ratio 1.00 0.90 0.82 0.81

Quick Ratio 0.79 0.72 0.66 0.66

Cash Ratio 0.11 0.01 0.13 0.02

Long-term Solvency

Total Debt Ratio 0.84 0.85 0.88 0.85

Debt to Equity 5.08 5.60 7.24 5.64

Times Interest Earned 0.08 0.17 -3.82 0.35

Cash Coverage 0.06 0.11 0.28 0.15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL STATEMENT ANALYSIS AND VALUATION

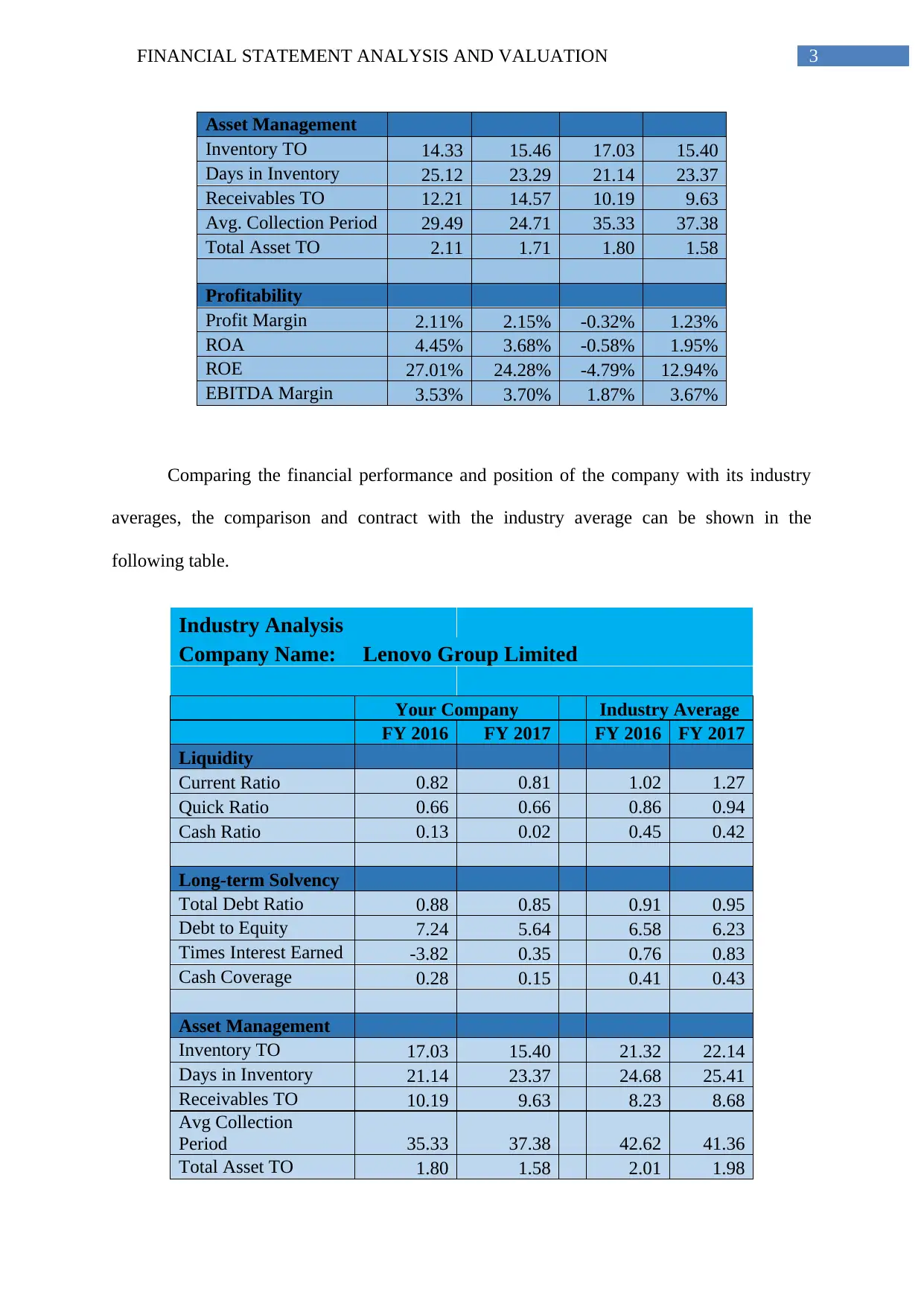

Asset Management

Inventory TO 14.33 15.46 17.03 15.40

Days in Inventory 25.12 23.29 21.14 23.37

Receivables TO 12.21 14.57 10.19 9.63

Avg. Collection Period 29.49 24.71 35.33 37.38

Total Asset TO 2.11 1.71 1.80 1.58

Profitability

Profit Margin 2.11% 2.15% -0.32% 1.23%

ROA 4.45% 3.68% -0.58% 1.95%

ROE 27.01% 24.28% -4.79% 12.94%

EBITDA Margin 3.53% 3.70% 1.87% 3.67%

Comparing the financial performance and position of the company with its industry

averages, the comparison and contract with the industry average can be shown in the

following table.

Industry Analysis

Company Name: Lenovo Group Limited

Your Company Industry Average

FY 2016 FY 2017 FY 2016 FY 2017

Liquidity

Current Ratio 0.82 0.81 1.02 1.27

Quick Ratio 0.66 0.66 0.86 0.94

Cash Ratio 0.13 0.02 0.45 0.42

Long-term Solvency

Total Debt Ratio 0.88 0.85 0.91 0.95

Debt to Equity 7.24 5.64 6.58 6.23

Times Interest Earned -3.82 0.35 0.76 0.83

Cash Coverage 0.28 0.15 0.41 0.43

Asset Management

Inventory TO 17.03 15.40 21.32 22.14

Days in Inventory 21.14 23.37 24.68 25.41

Receivables TO 10.19 9.63 8.23 8.68

Avg Collection

Period 35.33 37.38 42.62 41.36

Total Asset TO 1.80 1.58 2.01 1.98

Asset Management

Inventory TO 14.33 15.46 17.03 15.40

Days in Inventory 25.12 23.29 21.14 23.37

Receivables TO 12.21 14.57 10.19 9.63

Avg. Collection Period 29.49 24.71 35.33 37.38

Total Asset TO 2.11 1.71 1.80 1.58

Profitability

Profit Margin 2.11% 2.15% -0.32% 1.23%

ROA 4.45% 3.68% -0.58% 1.95%

ROE 27.01% 24.28% -4.79% 12.94%

EBITDA Margin 3.53% 3.70% 1.87% 3.67%

Comparing the financial performance and position of the company with its industry

averages, the comparison and contract with the industry average can be shown in the

following table.

Industry Analysis

Company Name: Lenovo Group Limited

Your Company Industry Average

FY 2016 FY 2017 FY 2016 FY 2017

Liquidity

Current Ratio 0.82 0.81 1.02 1.27

Quick Ratio 0.66 0.66 0.86 0.94

Cash Ratio 0.13 0.02 0.45 0.42

Long-term Solvency

Total Debt Ratio 0.88 0.85 0.91 0.95

Debt to Equity 7.24 5.64 6.58 6.23

Times Interest Earned -3.82 0.35 0.76 0.83

Cash Coverage 0.28 0.15 0.41 0.43

Asset Management

Inventory TO 17.03 15.40 21.32 22.14

Days in Inventory 21.14 23.37 24.68 25.41

Receivables TO 10.19 9.63 8.23 8.68

Avg Collection

Period 35.33 37.38 42.62 41.36

Total Asset TO 1.80 1.58 2.01 1.98

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL STATEMENT ANALYSIS AND VALUATION

Profitability

Profit Margin -0.32% 1.23% 1.71% 1.74%

ROA -0.58% 1.95% 2.84% 2.31%

ROE -4.79% 12.94% 12.29% 10.95%

EBITDA Margin 1.87% 3.67% 3.15% 4.02%

Sub part 2:

Lenovo Group Limited is a US based company leading in the electronic devices and

technologies market. They generate their revenue through manufacturing and selling of

various electronic products. Form their annual reports starting from the year 2014 to 2017 a

detailed ratio analysis have been done in the above table. Various figures have been taken

from their financial statement and balance sheet. Industry averages have been taken for the

US Information Technology industry (Lenovo Group Limited Annual report 2016). It can be

observed that in all the years starting from 2014 to 2017 their liquidity measures are poor and

below the standard. Standard current ratio for a company should have been 1:2, while the

company is having lower than 1 as their current ratio for all the four years. In terms of quick

ratio also they are below the standard. Though the industry average is below the standard of

liquidity ratios, they were unable to achieve the industry average also.

In terms of long term solvency, they are having huge amount of debt through the four

years. Their assets are mostly backed by debts rather than equity. The debt to equity ratio is

much higher than the industry average; they are taking extra risk burden to earn maximum

profit. Their cash adequacy ratio is also very poor. In 2016 they were suffering a huge

amount of loss, that is why they are having a negative times interest earned ratio in 2016. To

cover the loss, they raised huge borrowings which increased their debt to equity ratio in 2015

to the highest level.

Profitability

Profit Margin -0.32% 1.23% 1.71% 1.74%

ROA -0.58% 1.95% 2.84% 2.31%

ROE -4.79% 12.94% 12.29% 10.95%

EBITDA Margin 1.87% 3.67% 3.15% 4.02%

Sub part 2:

Lenovo Group Limited is a US based company leading in the electronic devices and

technologies market. They generate their revenue through manufacturing and selling of

various electronic products. Form their annual reports starting from the year 2014 to 2017 a

detailed ratio analysis have been done in the above table. Various figures have been taken

from their financial statement and balance sheet. Industry averages have been taken for the

US Information Technology industry (Lenovo Group Limited Annual report 2016). It can be

observed that in all the years starting from 2014 to 2017 their liquidity measures are poor and

below the standard. Standard current ratio for a company should have been 1:2, while the

company is having lower than 1 as their current ratio for all the four years. In terms of quick

ratio also they are below the standard. Though the industry average is below the standard of

liquidity ratios, they were unable to achieve the industry average also.

In terms of long term solvency, they are having huge amount of debt through the four

years. Their assets are mostly backed by debts rather than equity. The debt to equity ratio is

much higher than the industry average; they are taking extra risk burden to earn maximum

profit. Their cash adequacy ratio is also very poor. In 2016 they were suffering a huge

amount of loss, that is why they are having a negative times interest earned ratio in 2016. To

cover the loss, they raised huge borrowings which increased their debt to equity ratio in 2015

to the highest level.

5FINANCIAL STATEMENT ANALYSIS AND VALUATION

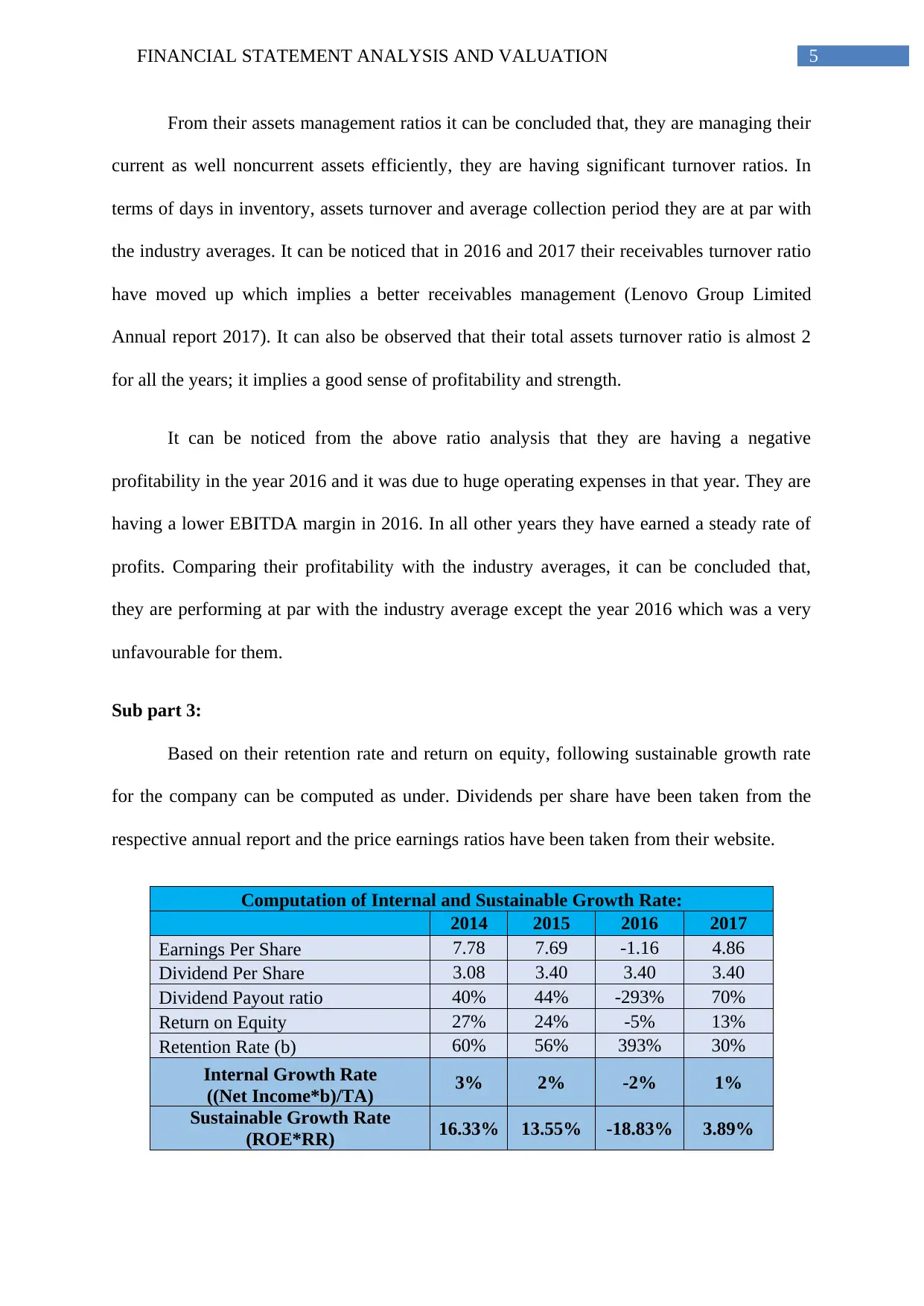

From their assets management ratios it can be concluded that, they are managing their

current as well noncurrent assets efficiently, they are having significant turnover ratios. In

terms of days in inventory, assets turnover and average collection period they are at par with

the industry averages. It can be noticed that in 2016 and 2017 their receivables turnover ratio

have moved up which implies a better receivables management (Lenovo Group Limited

Annual report 2017). It can also be observed that their total assets turnover ratio is almost 2

for all the years; it implies a good sense of profitability and strength.

It can be noticed from the above ratio analysis that they are having a negative

profitability in the year 2016 and it was due to huge operating expenses in that year. They are

having a lower EBITDA margin in 2016. In all other years they have earned a steady rate of

profits. Comparing their profitability with the industry averages, it can be concluded that,

they are performing at par with the industry average except the year 2016 which was a very

unfavourable for them.

Sub part 3:

Based on their retention rate and return on equity, following sustainable growth rate

for the company can be computed as under. Dividends per share have been taken from the

respective annual report and the price earnings ratios have been taken from their website.

Computation of Internal and Sustainable Growth Rate:

2014 2015 2016 2017

Earnings Per Share 7.78 7.69 -1.16 4.86

Dividend Per Share 3.08 3.40 3.40 3.40

Dividend Payout ratio 40% 44% -293% 70%

Return on Equity 27% 24% -5% 13%

Retention Rate (b) 60% 56% 393% 30%

Internal Growth Rate

((Net Income*b)/TA) 3% 2% -2% 1%

Sustainable Growth Rate

(ROE*RR) 16.33% 13.55% -18.83% 3.89%

From their assets management ratios it can be concluded that, they are managing their

current as well noncurrent assets efficiently, they are having significant turnover ratios. In

terms of days in inventory, assets turnover and average collection period they are at par with

the industry averages. It can be noticed that in 2016 and 2017 their receivables turnover ratio

have moved up which implies a better receivables management (Lenovo Group Limited

Annual report 2017). It can also be observed that their total assets turnover ratio is almost 2

for all the years; it implies a good sense of profitability and strength.

It can be noticed from the above ratio analysis that they are having a negative

profitability in the year 2016 and it was due to huge operating expenses in that year. They are

having a lower EBITDA margin in 2016. In all other years they have earned a steady rate of

profits. Comparing their profitability with the industry averages, it can be concluded that,

they are performing at par with the industry average except the year 2016 which was a very

unfavourable for them.

Sub part 3:

Based on their retention rate and return on equity, following sustainable growth rate

for the company can be computed as under. Dividends per share have been taken from the

respective annual report and the price earnings ratios have been taken from their website.

Computation of Internal and Sustainable Growth Rate:

2014 2015 2016 2017

Earnings Per Share 7.78 7.69 -1.16 4.86

Dividend Per Share 3.08 3.40 3.40 3.40

Dividend Payout ratio 40% 44% -293% 70%

Return on Equity 27% 24% -5% 13%

Retention Rate (b) 60% 56% 393% 30%

Internal Growth Rate

((Net Income*b)/TA) 3% 2% -2% 1%

Sustainable Growth Rate

(ROE*RR) 16.33% 13.55% -18.83% 3.89%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL STATEMENT ANALYSIS AND VALUATION

It can be said that the company is having a good sustainable growth as compared to

the industry averages, but their internal growth rate is not satisfactory.

It can be said that the company is having a good sustainable growth as compared to

the industry averages, but their internal growth rate is not satisfactory.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL STATEMENT ANALYSIS AND VALUATION

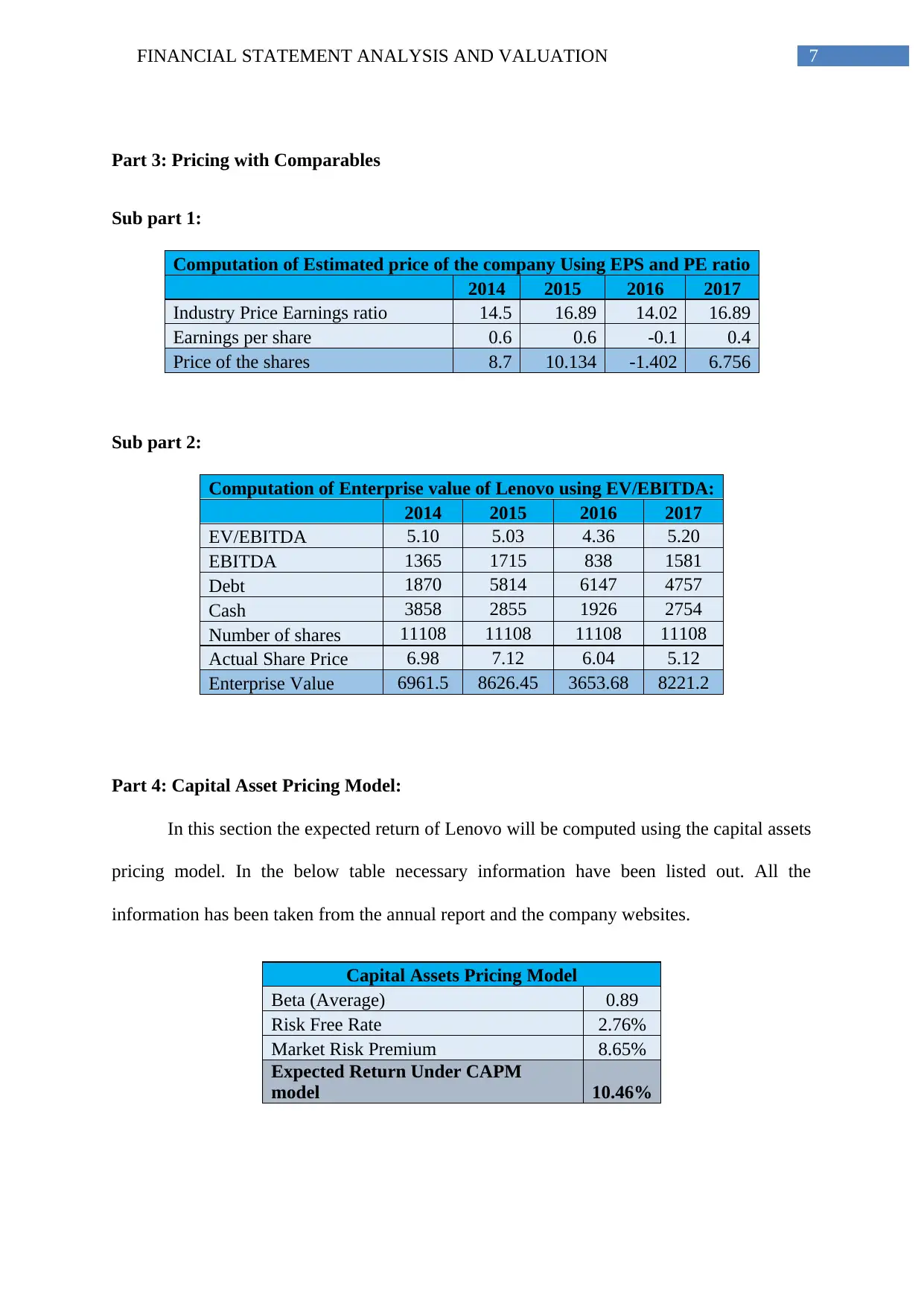

Part 3: Pricing with Comparables

Sub part 1:

Computation of Estimated price of the company Using EPS and PE ratio

2014 2015 2016 2017

Industry Price Earnings ratio 14.5 16.89 14.02 16.89

Earnings per share 0.6 0.6 -0.1 0.4

Price of the shares 8.7 10.134 -1.402 6.756

Sub part 2:

Computation of Enterprise value of Lenovo using EV/EBITDA:

2014 2015 2016 2017

EV/EBITDA 5.10 5.03 4.36 5.20

EBITDA 1365 1715 838 1581

Debt 1870 5814 6147 4757

Cash 3858 2855 1926 2754

Number of shares 11108 11108 11108 11108

Actual Share Price 6.98 7.12 6.04 5.12

Enterprise Value 6961.5 8626.45 3653.68 8221.2

Part 4: Capital Asset Pricing Model:

In this section the expected return of Lenovo will be computed using the capital assets

pricing model. In the below table necessary information have been listed out. All the

information has been taken from the annual report and the company websites.

Capital Assets Pricing Model

Beta (Average) 0.89

Risk Free Rate 2.76%

Market Risk Premium 8.65%

Expected Return Under CAPM

model 10.46%

Part 3: Pricing with Comparables

Sub part 1:

Computation of Estimated price of the company Using EPS and PE ratio

2014 2015 2016 2017

Industry Price Earnings ratio 14.5 16.89 14.02 16.89

Earnings per share 0.6 0.6 -0.1 0.4

Price of the shares 8.7 10.134 -1.402 6.756

Sub part 2:

Computation of Enterprise value of Lenovo using EV/EBITDA:

2014 2015 2016 2017

EV/EBITDA 5.10 5.03 4.36 5.20

EBITDA 1365 1715 838 1581

Debt 1870 5814 6147 4757

Cash 3858 2855 1926 2754

Number of shares 11108 11108 11108 11108

Actual Share Price 6.98 7.12 6.04 5.12

Enterprise Value 6961.5 8626.45 3653.68 8221.2

Part 4: Capital Asset Pricing Model:

In this section the expected return of Lenovo will be computed using the capital assets

pricing model. In the below table necessary information have been listed out. All the

information has been taken from the annual report and the company websites.

Capital Assets Pricing Model

Beta (Average) 0.89

Risk Free Rate 2.76%

Market Risk Premium 8.65%

Expected Return Under CAPM

model 10.46%

8FINANCIAL STATEMENT ANALYSIS AND VALUATION

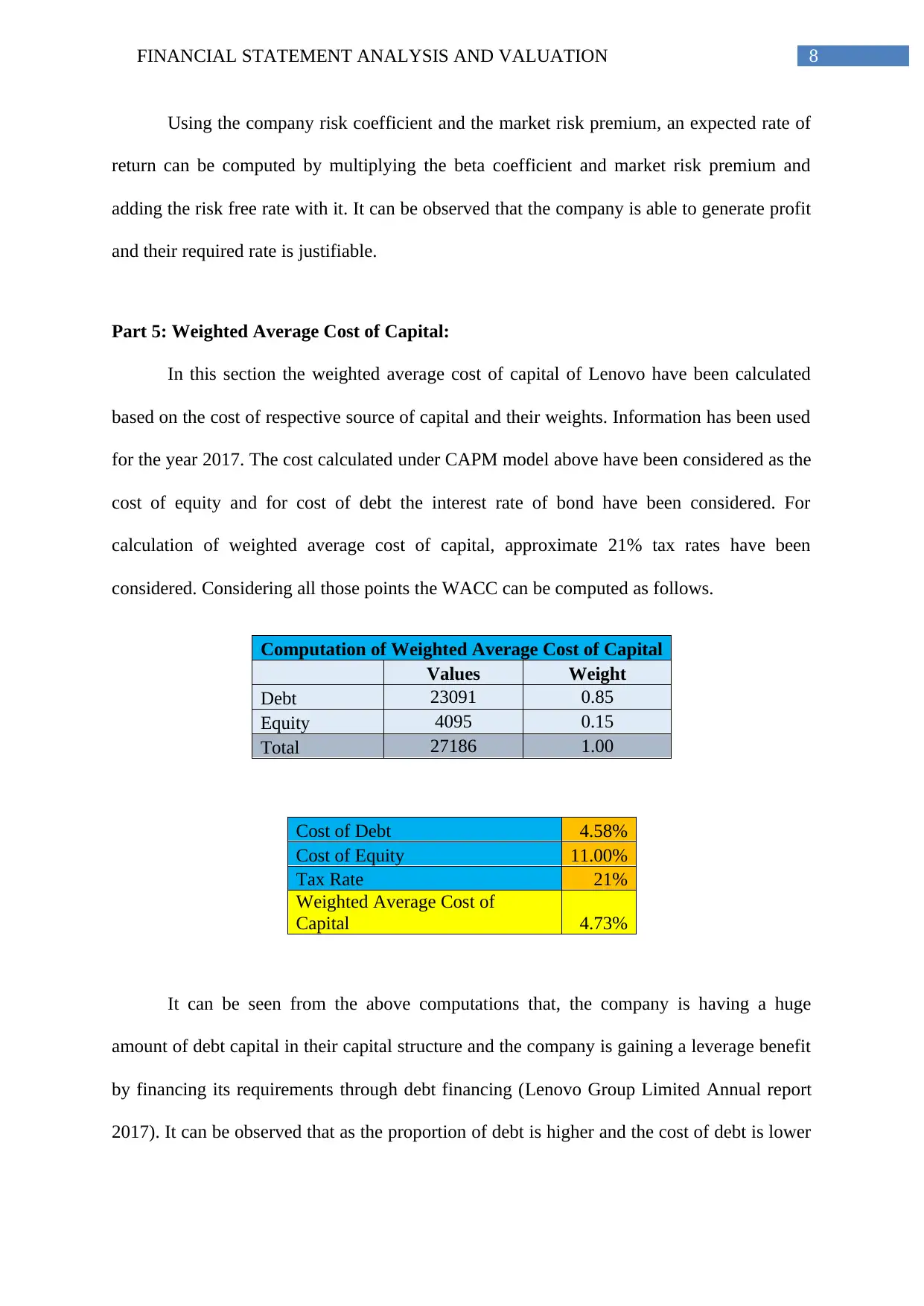

Using the company risk coefficient and the market risk premium, an expected rate of

return can be computed by multiplying the beta coefficient and market risk premium and

adding the risk free rate with it. It can be observed that the company is able to generate profit

and their required rate is justifiable.

Part 5: Weighted Average Cost of Capital:

In this section the weighted average cost of capital of Lenovo have been calculated

based on the cost of respective source of capital and their weights. Information has been used

for the year 2017. The cost calculated under CAPM model above have been considered as the

cost of equity and for cost of debt the interest rate of bond have been considered. For

calculation of weighted average cost of capital, approximate 21% tax rates have been

considered. Considering all those points the WACC can be computed as follows.

Computation of Weighted Average Cost of Capital

Values Weight

Debt 23091 0.85

Equity 4095 0.15

Total 27186 1.00

Cost of Debt 4.58%

Cost of Equity 11.00%

Tax Rate 21%

Weighted Average Cost of

Capital 4.73%

It can be seen from the above computations that, the company is having a huge

amount of debt capital in their capital structure and the company is gaining a leverage benefit

by financing its requirements through debt financing (Lenovo Group Limited Annual report

2017). It can be observed that as the proportion of debt is higher and the cost of debt is lower

Using the company risk coefficient and the market risk premium, an expected rate of

return can be computed by multiplying the beta coefficient and market risk premium and

adding the risk free rate with it. It can be observed that the company is able to generate profit

and their required rate is justifiable.

Part 5: Weighted Average Cost of Capital:

In this section the weighted average cost of capital of Lenovo have been calculated

based on the cost of respective source of capital and their weights. Information has been used

for the year 2017. The cost calculated under CAPM model above have been considered as the

cost of equity and for cost of debt the interest rate of bond have been considered. For

calculation of weighted average cost of capital, approximate 21% tax rates have been

considered. Considering all those points the WACC can be computed as follows.

Computation of Weighted Average Cost of Capital

Values Weight

Debt 23091 0.85

Equity 4095 0.15

Total 27186 1.00

Cost of Debt 4.58%

Cost of Equity 11.00%

Tax Rate 21%

Weighted Average Cost of

Capital 4.73%

It can be seen from the above computations that, the company is having a huge

amount of debt capital in their capital structure and the company is gaining a leverage benefit

by financing its requirements through debt financing (Lenovo Group Limited Annual report

2017). It can be observed that as the proportion of debt is higher and the cost of debt is lower

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL STATEMENT ANALYSIS AND VALUATION

than the cost of equity, their weighted average cost of capital comes to 4.61% only. It implies

their efficient capital management strategies.

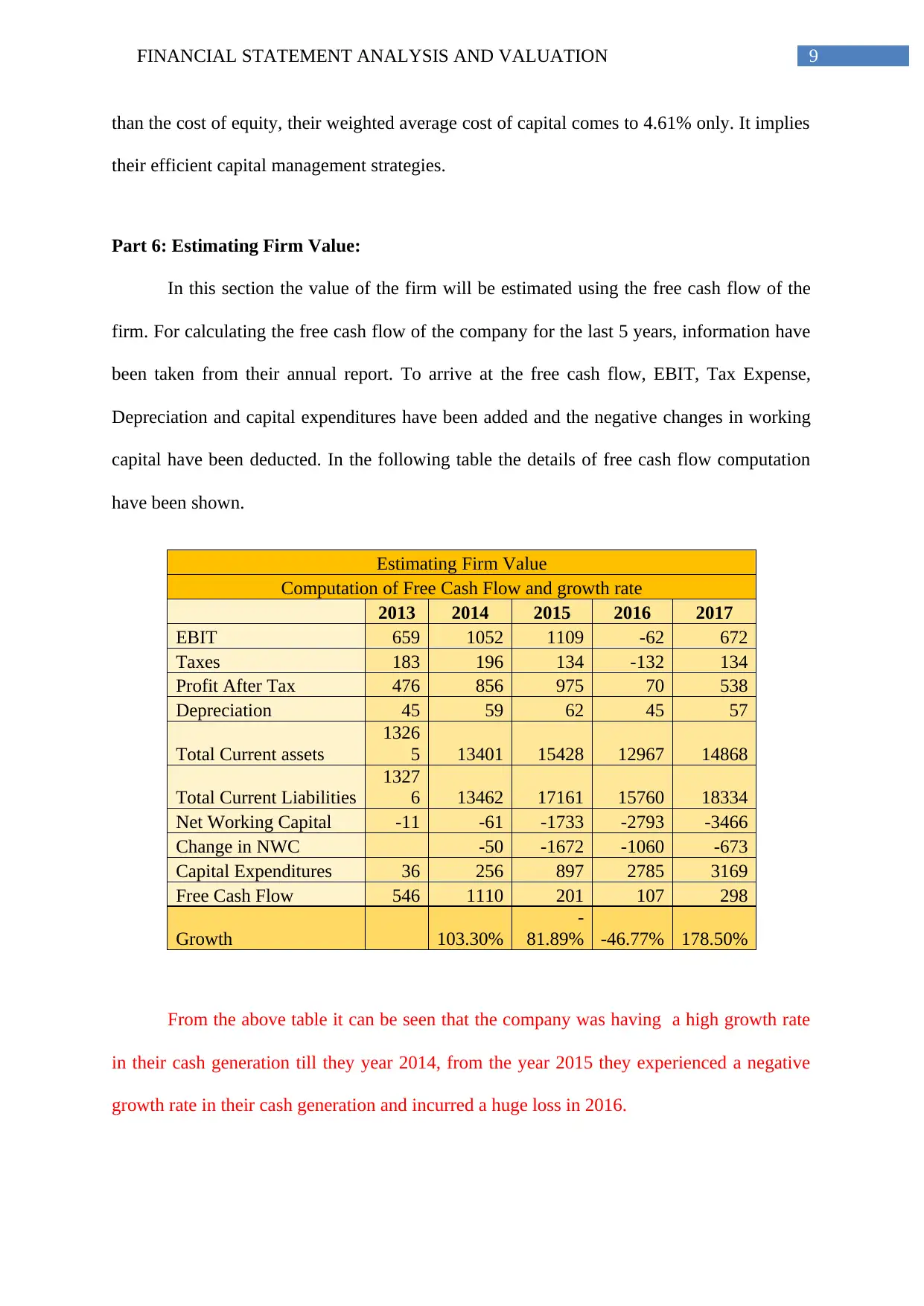

Part 6: Estimating Firm Value:

In this section the value of the firm will be estimated using the free cash flow of the

firm. For calculating the free cash flow of the company for the last 5 years, information have

been taken from their annual report. To arrive at the free cash flow, EBIT, Tax Expense,

Depreciation and capital expenditures have been added and the negative changes in working

capital have been deducted. In the following table the details of free cash flow computation

have been shown.

Estimating Firm Value

Computation of Free Cash Flow and growth rate

2013 2014 2015 2016 2017

EBIT 659 1052 1109 -62 672

Taxes 183 196 134 -132 134

Profit After Tax 476 856 975 70 538

Depreciation 45 59 62 45 57

Total Current assets

1326

5 13401 15428 12967 14868

Total Current Liabilities

1327

6 13462 17161 15760 18334

Net Working Capital -11 -61 -1733 -2793 -3466

Change in NWC -50 -1672 -1060 -673

Capital Expenditures 36 256 897 2785 3169

Free Cash Flow 546 1110 201 107 298

Growth 103.30%

-

81.89% -46.77% 178.50%

From the above table it can be seen that the company was having a high growth rate

in their cash generation till they year 2014, from the year 2015 they experienced a negative

growth rate in their cash generation and incurred a huge loss in 2016.

than the cost of equity, their weighted average cost of capital comes to 4.61% only. It implies

their efficient capital management strategies.

Part 6: Estimating Firm Value:

In this section the value of the firm will be estimated using the free cash flow of the

firm. For calculating the free cash flow of the company for the last 5 years, information have

been taken from their annual report. To arrive at the free cash flow, EBIT, Tax Expense,

Depreciation and capital expenditures have been added and the negative changes in working

capital have been deducted. In the following table the details of free cash flow computation

have been shown.

Estimating Firm Value

Computation of Free Cash Flow and growth rate

2013 2014 2015 2016 2017

EBIT 659 1052 1109 -62 672

Taxes 183 196 134 -132 134

Profit After Tax 476 856 975 70 538

Depreciation 45 59 62 45 57

Total Current assets

1326

5 13401 15428 12967 14868

Total Current Liabilities

1327

6 13462 17161 15760 18334

Net Working Capital -11 -61 -1733 -2793 -3466

Change in NWC -50 -1672 -1060 -673

Capital Expenditures 36 256 897 2785 3169

Free Cash Flow 546 1110 201 107 298

Growth 103.30%

-

81.89% -46.77% 178.50%

From the above table it can be seen that the company was having a high growth rate

in their cash generation till they year 2014, from the year 2015 they experienced a negative

growth rate in their cash generation and incurred a huge loss in 2016.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL STATEMENT ANALYSIS AND VALUATION

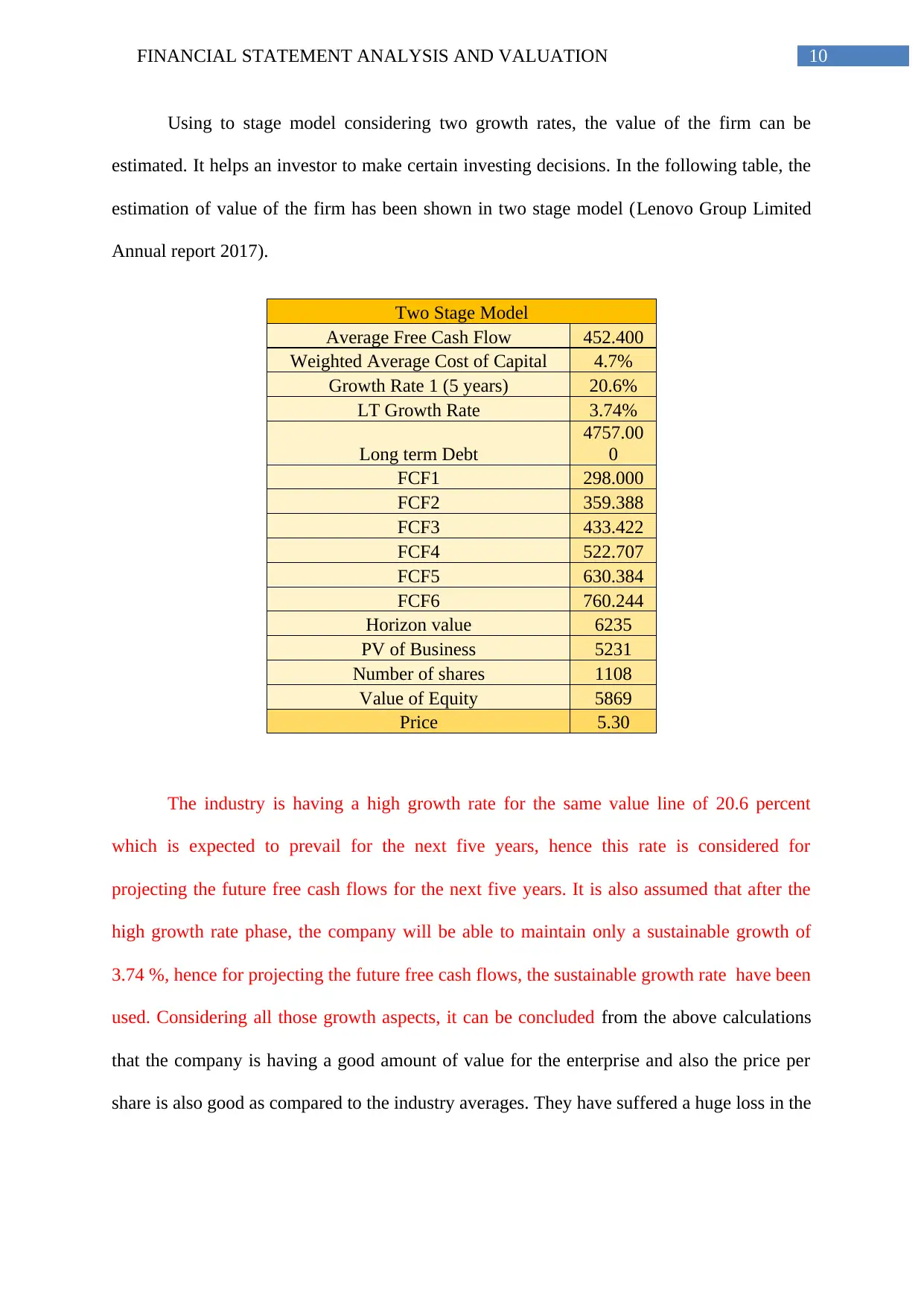

Using to stage model considering two growth rates, the value of the firm can be

estimated. It helps an investor to make certain investing decisions. In the following table, the

estimation of value of the firm has been shown in two stage model (Lenovo Group Limited

Annual report 2017).

Two Stage Model

Average Free Cash Flow 452.400

Weighted Average Cost of Capital 4.7%

Growth Rate 1 (5 years) 20.6%

LT Growth Rate 3.74%

Long term Debt

4757.00

0

FCF1 298.000

FCF2 359.388

FCF3 433.422

FCF4 522.707

FCF5 630.384

FCF6 760.244

Horizon value 6235

PV of Business 5231

Number of shares 1108

Value of Equity 5869

Price 5.30

The industry is having a high growth rate for the same value line of 20.6 percent

which is expected to prevail for the next five years, hence this rate is considered for

projecting the future free cash flows for the next five years. It is also assumed that after the

high growth rate phase, the company will be able to maintain only a sustainable growth of

3.74 %, hence for projecting the future free cash flows, the sustainable growth rate have been

used. Considering all those growth aspects, it can be concluded from the above calculations

that the company is having a good amount of value for the enterprise and also the price per

share is also good as compared to the industry averages. They have suffered a huge loss in the

Using to stage model considering two growth rates, the value of the firm can be

estimated. It helps an investor to make certain investing decisions. In the following table, the

estimation of value of the firm has been shown in two stage model (Lenovo Group Limited

Annual report 2017).

Two Stage Model

Average Free Cash Flow 452.400

Weighted Average Cost of Capital 4.7%

Growth Rate 1 (5 years) 20.6%

LT Growth Rate 3.74%

Long term Debt

4757.00

0

FCF1 298.000

FCF2 359.388

FCF3 433.422

FCF4 522.707

FCF5 630.384

FCF6 760.244

Horizon value 6235

PV of Business 5231

Number of shares 1108

Value of Equity 5869

Price 5.30

The industry is having a high growth rate for the same value line of 20.6 percent

which is expected to prevail for the next five years, hence this rate is considered for

projecting the future free cash flows for the next five years. It is also assumed that after the

high growth rate phase, the company will be able to maintain only a sustainable growth of

3.74 %, hence for projecting the future free cash flows, the sustainable growth rate have been

used. Considering all those growth aspects, it can be concluded from the above calculations

that the company is having a good amount of value for the enterprise and also the price per

share is also good as compared to the industry averages. They have suffered a huge loss in the

11FINANCIAL STATEMENT ANALYSIS AND VALUATION

year 2016 but later on they have overcome the situation and having a good growth rate again

(Lenovo Group Limited Annual report 2017).

Par 7: Strengths, Weaknesses and recommendations:

From the above valuations, and analysis it can be concluded that the company is a

leading company in the respective industry, they have been performing financially and

operationally well for a long period of time. They are one of the global exporters of the

computers and electronic devices. Though their short term and long term liquidity is not so

good, but they are efficiently managing their assets to continue their business and to keep

maintaining the adequacy of working capital for meeting their cash requirements.

From the profitability point of view, they have been performing well till the year

2015, in 2016 they have experienced a worse situation in their situation thereby incurring a

huge amount of loss, but their efficient business strategies helped them to overcome the

situation and to make significant amount of profit again. If the value of the firm and the

estimated share price is considered, it can be recommended for a potential investor that the

company is a well established and old company, and their strength is their efficient assets

management and debt financing, gaining a huge amount of leverage benefit, which can

increase the shareholders wealth in the future. As the company have overcome the loss

making situation and again a growth rate in their revenue and profit can be seen, it will be

good option to invest in.

year 2016 but later on they have overcome the situation and having a good growth rate again

(Lenovo Group Limited Annual report 2017).

Par 7: Strengths, Weaknesses and recommendations:

From the above valuations, and analysis it can be concluded that the company is a

leading company in the respective industry, they have been performing financially and

operationally well for a long period of time. They are one of the global exporters of the

computers and electronic devices. Though their short term and long term liquidity is not so

good, but they are efficiently managing their assets to continue their business and to keep

maintaining the adequacy of working capital for meeting their cash requirements.

From the profitability point of view, they have been performing well till the year

2015, in 2016 they have experienced a worse situation in their situation thereby incurring a

huge amount of loss, but their efficient business strategies helped them to overcome the

situation and to make significant amount of profit again. If the value of the firm and the

estimated share price is considered, it can be recommended for a potential investor that the

company is a well established and old company, and their strength is their efficient assets

management and debt financing, gaining a huge amount of leverage benefit, which can

increase the shareholders wealth in the future. As the company have overcome the loss

making situation and again a growth rate in their revenue and profit can be seen, it will be

good option to invest in.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.