Detailed Financial Performance Analysis of Myer for ACCT3013

VerifiedAdded on 2023/01/11

|9

|1454

|44

Report

AI Summary

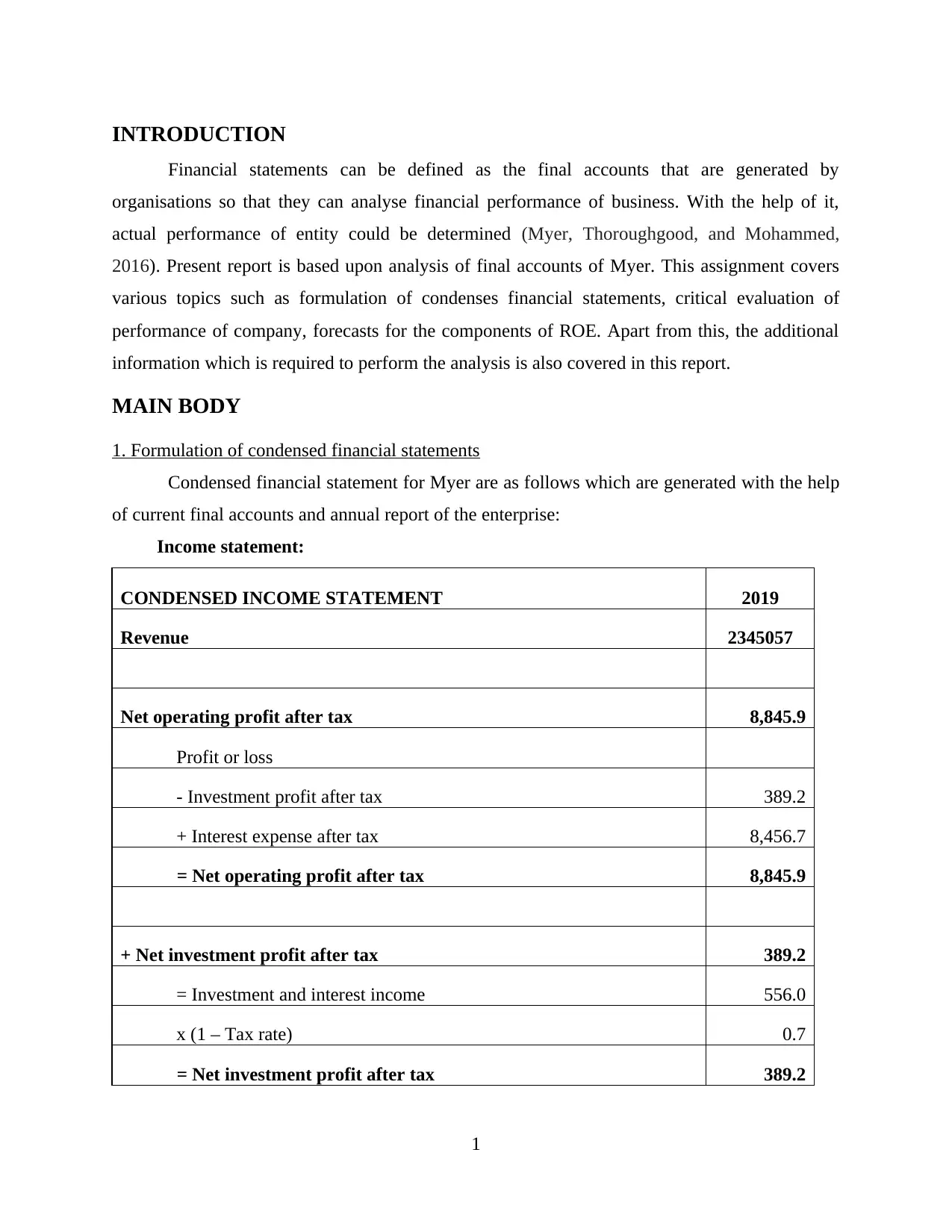

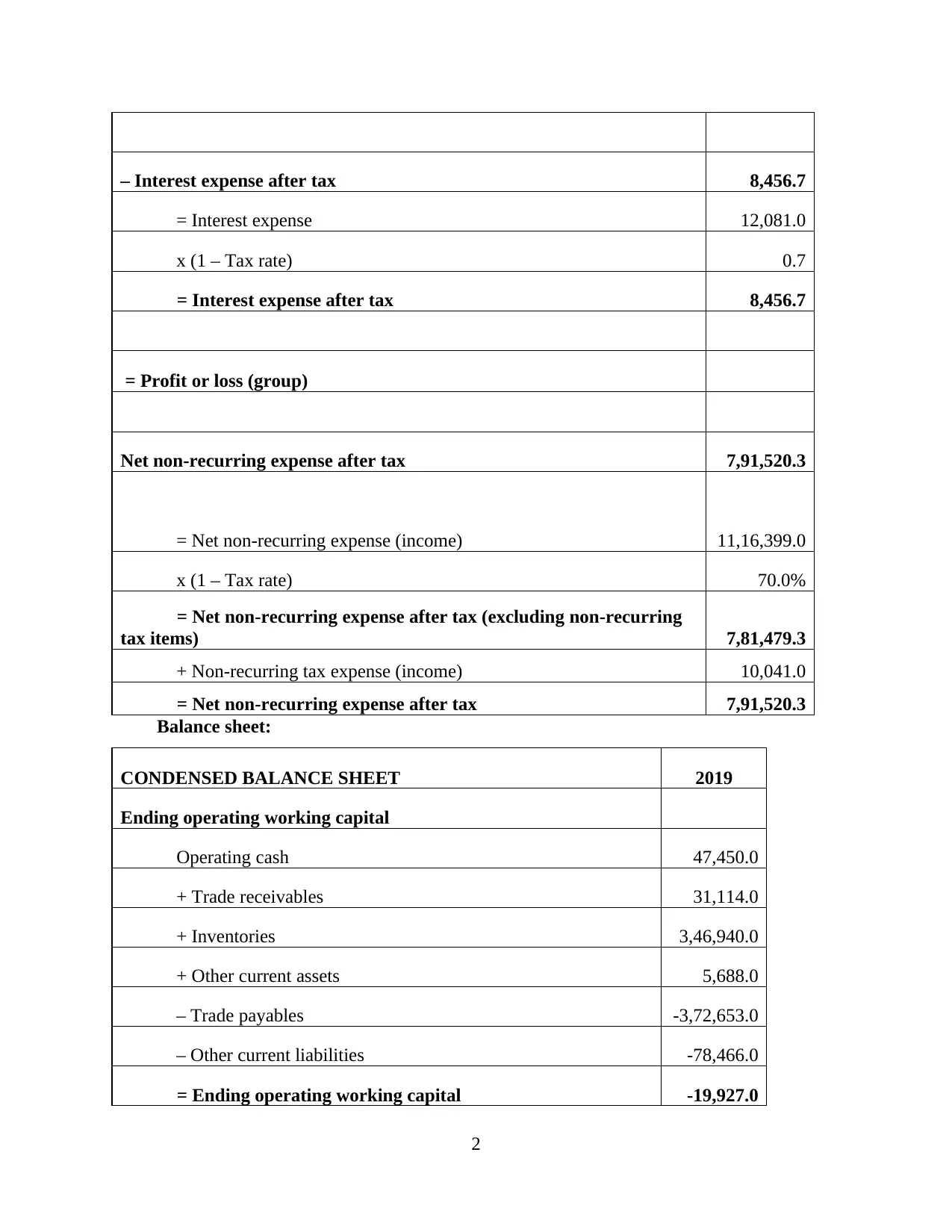

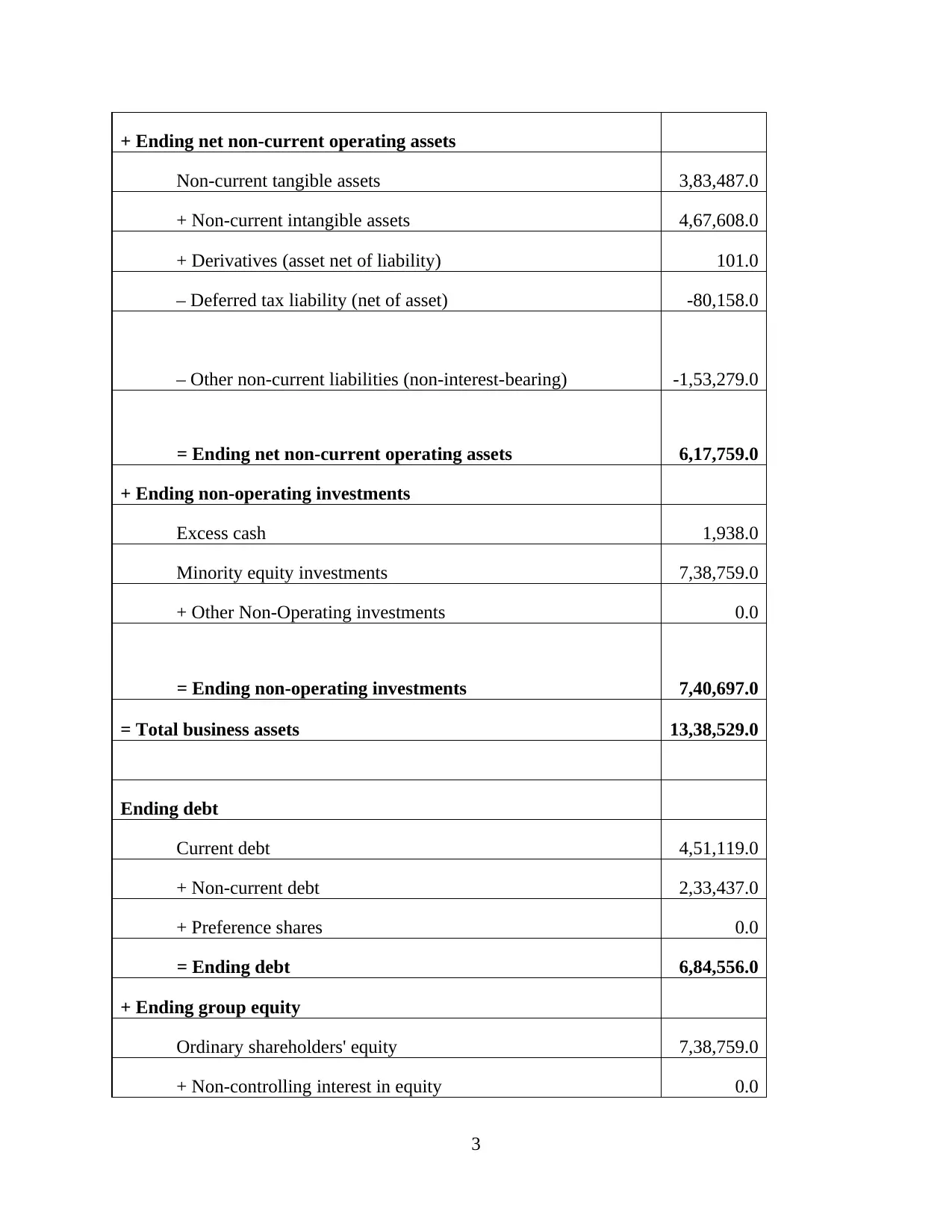

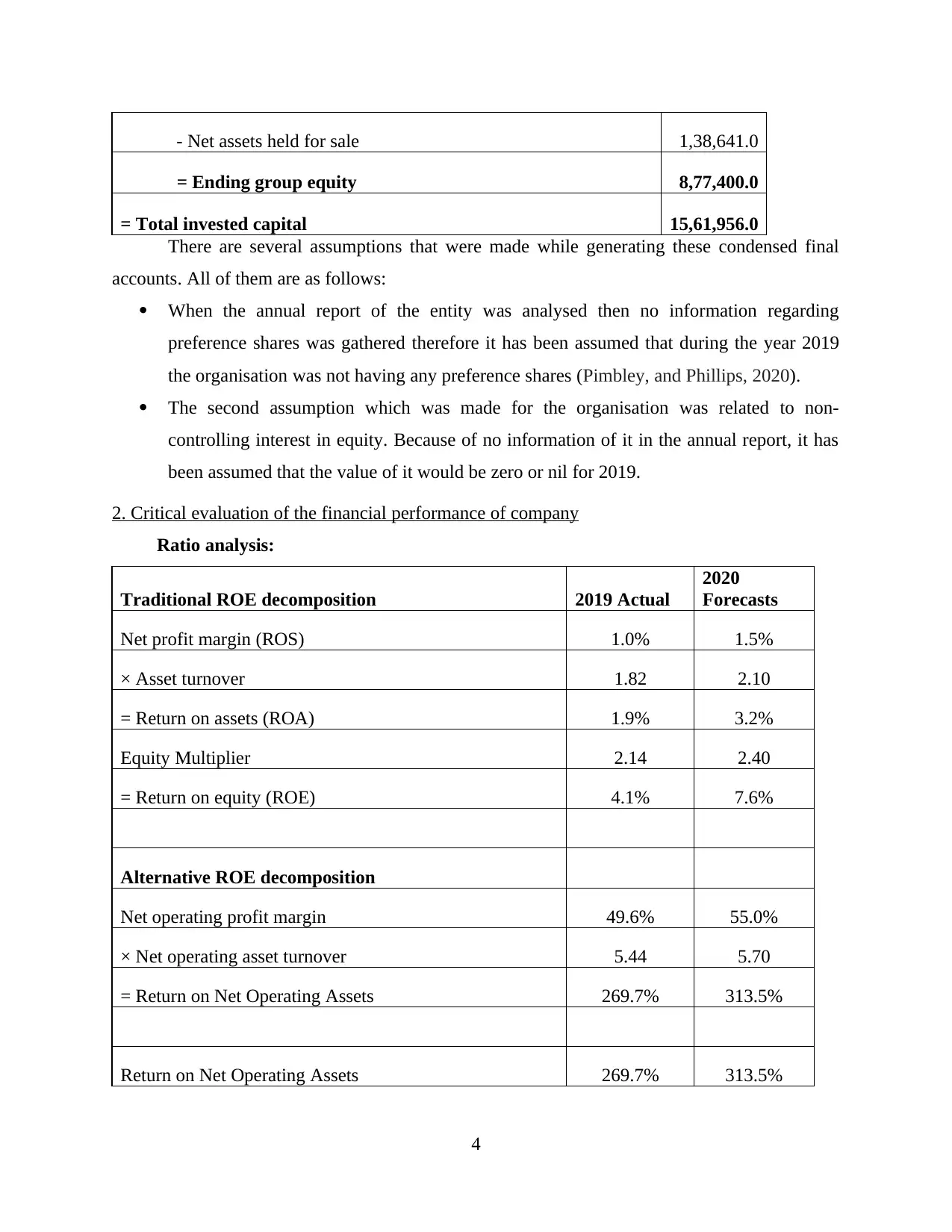

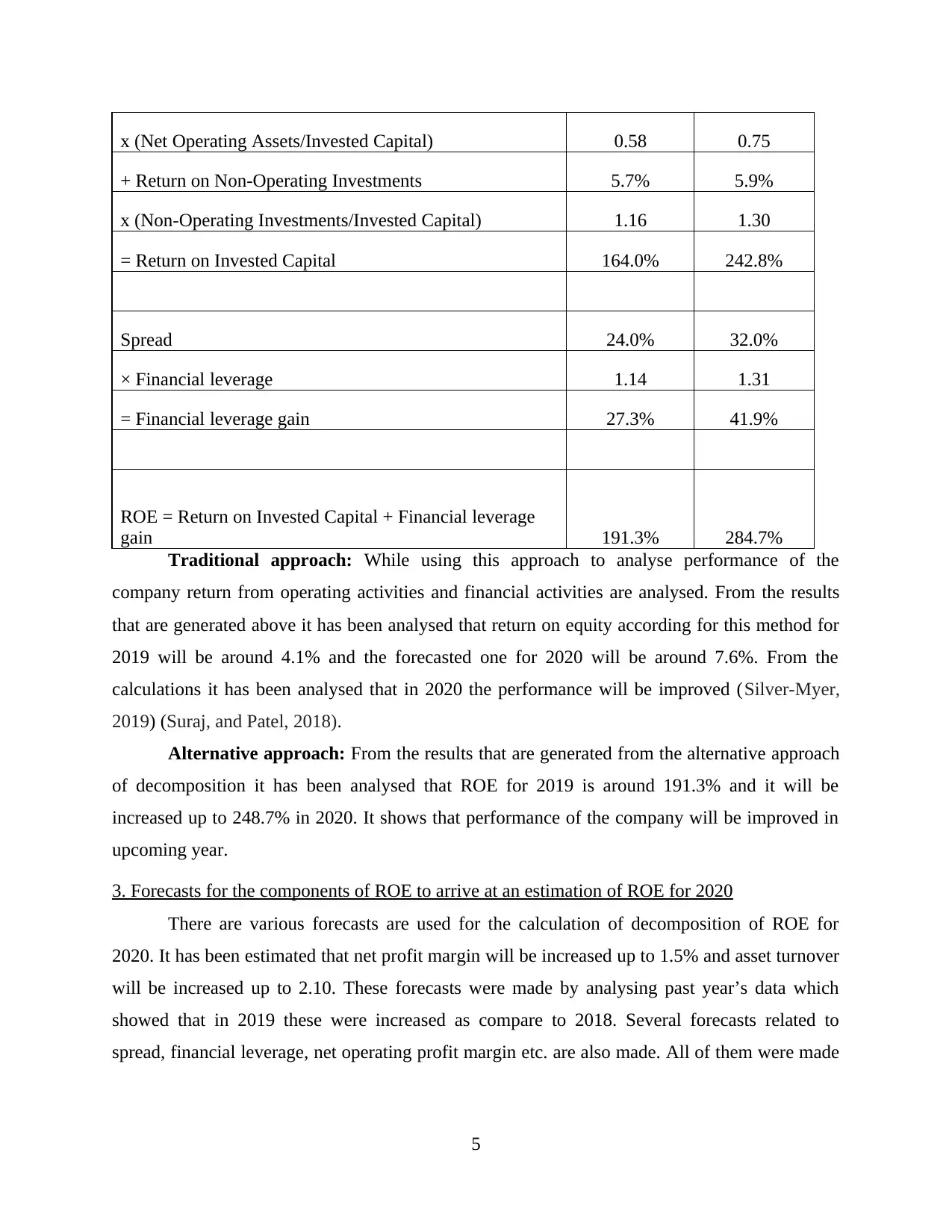

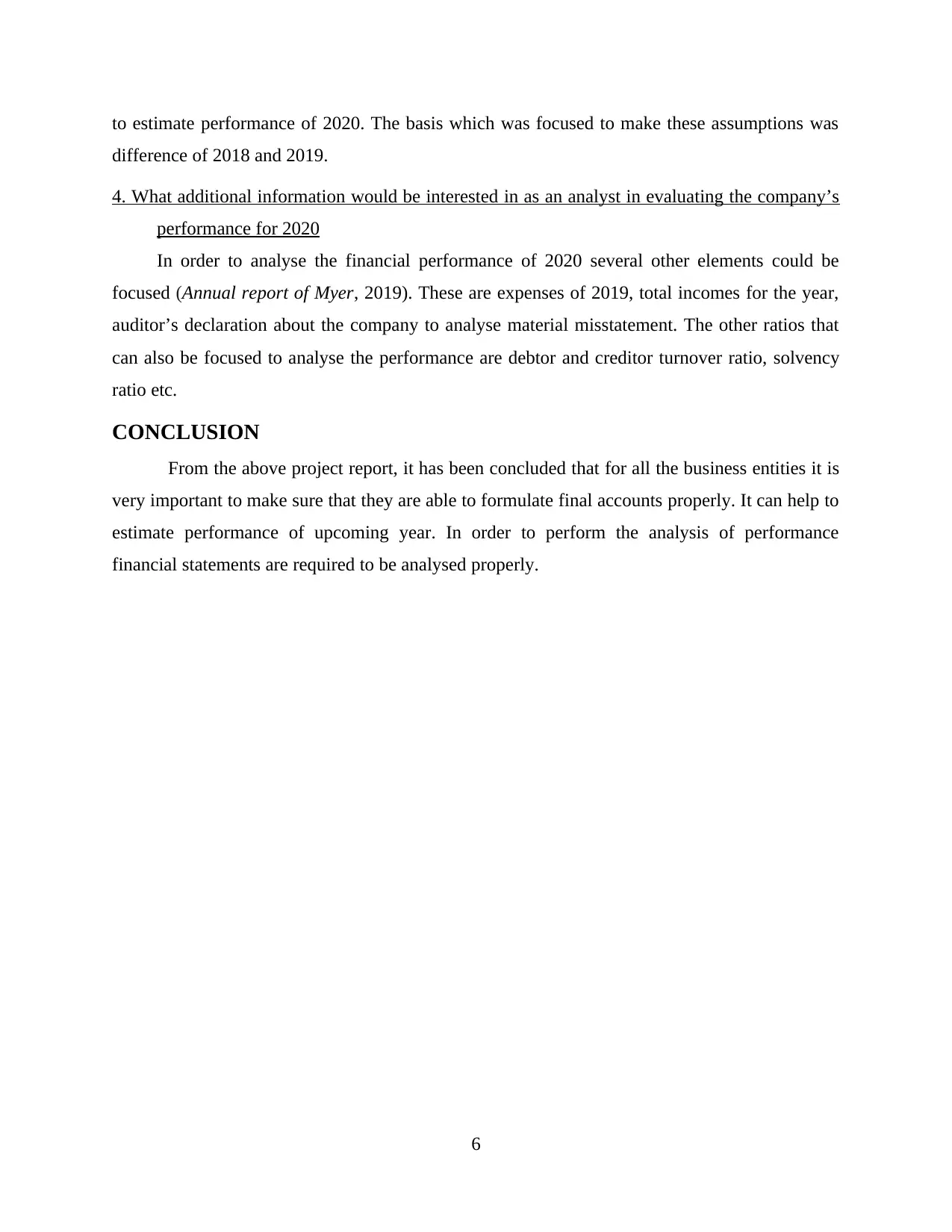

This report provides a financial statement analysis of Myer, focusing on the company's performance and financial position. It begins with the formulation of condensed financial statements, including an income statement and balance sheet for 2019, along with the assumptions made during their generation. The report then critically evaluates Myer's financial performance using ratio analysis, comparing actual figures from 2019 with forecasts for 2020. It decomposes the Return on Equity (ROE) using both traditional and alternative approaches. The analysis includes forecasts for the components of ROE to estimate the 2020 ROE. Finally, the report identifies additional information an analyst would find valuable in evaluating Myer's performance for 2020, such as expenses, incomes, and auditor's declaration. The report concludes by emphasizing the importance of accurate financial statement formulation for business performance assessment.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.