Financing Strategies of PPB and Kepong

VerifiedAdded on 2020/06/04

|17

|3605

|96

AI Summary

This assignment delves into the distinct financing approaches employed by two companies, PPB and Kepong. It highlights PPB's reliance on shareholder equity as its primary source of funding, contrasting it with Kepong's utilization of both long-term and short-term debt to meet investment requirements. The analysis incorporates illustrations showcasing the financial structures of each company, enabling a comparative understanding of their capital acquisition strategies.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL STATEMENT

ANALYSIS

ANALYSIS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Table of Contents

INTRODUCTION...........................................................................................................................1

1) Overview of PPB Group and Kuala Lumpur Kepong ...........................................................1

2) Sources of financing...............................................................................................................2

3) Analysis of financing activities of PPB group and Kuala Lumpur Kepong..........................3

4) Difference between the financing activities of PPB and Kuala Lumpur Kepong..................9

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

1) Overview of PPB Group and Kuala Lumpur Kepong ...........................................................1

2) Sources of financing...............................................................................................................2

3) Analysis of financing activities of PPB group and Kuala Lumpur Kepong..........................3

4) Difference between the financing activities of PPB and Kuala Lumpur Kepong..................9

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

Illustration Index

Illustration 1: Shareholder's equity of PPB......................................................................................4

Illustration 2: Long term debt of PPB..............................................................................................5

Illustration 3: Long term debt of Kepong........................................................................................6

Illustration 4: Stockholder's equity of Kepong................................................................................7

Illustration 5: Long term liabilities of Kepong................................................................................8

Illustration 6: Short term debt of Kepong........................................................................................9

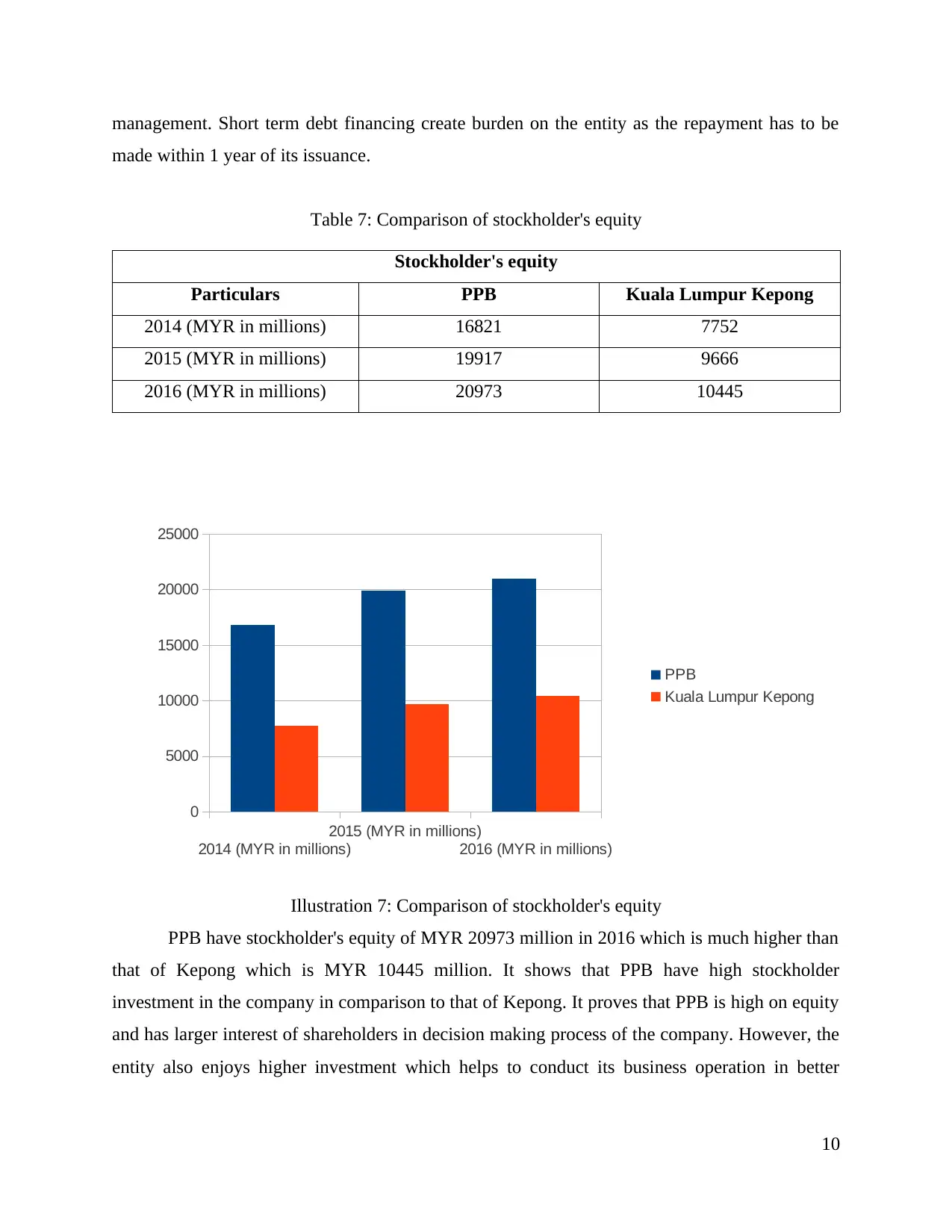

Illustration 7: Comparison of stockholder's equity........................................................................10

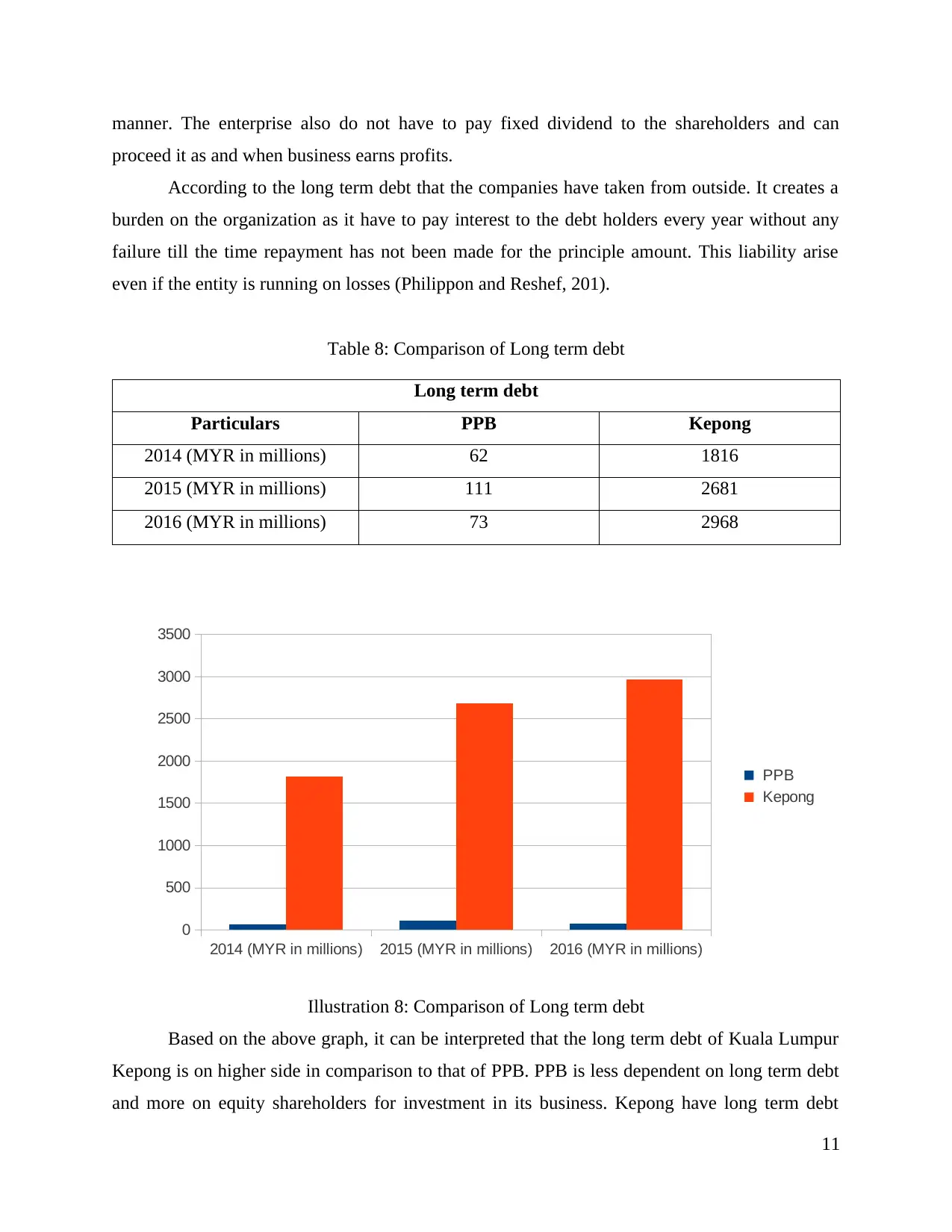

Illustration 8: Comparison of Long term debt...............................................................................11

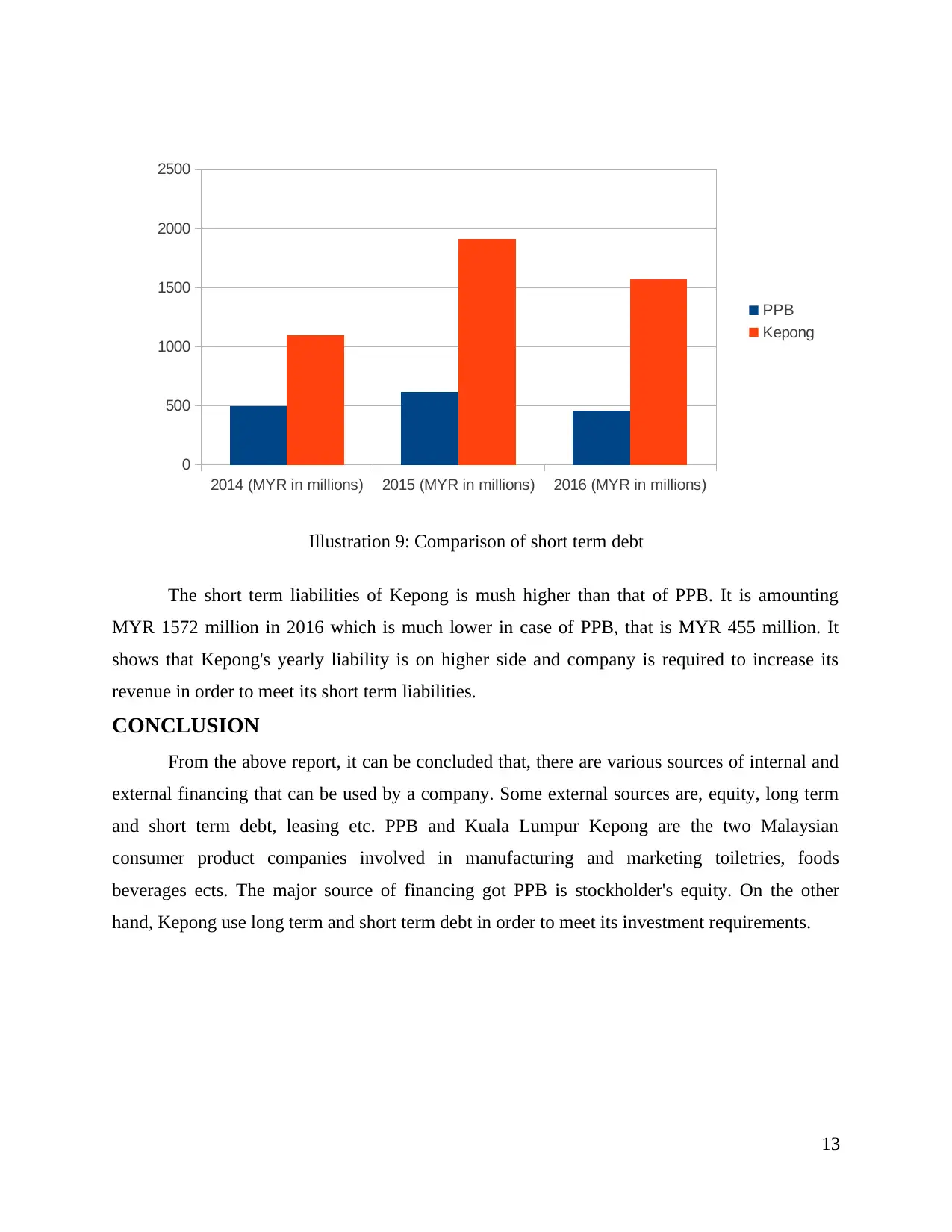

Illustration 9: Comparison of short term debt................................................................................12

Index of Tables

Table 1: Shareholder's equity of PPB..............................................................................................4

Table 2: Long term debt of PPB......................................................................................................5

Table 3: Long term debt of Kepong.................................................................................................6

Table 4: Stockholder's equity of Kepong.........................................................................................6

Table 5: Long term liabilities of Kepong.........................................................................................7

Table 6: Short term debt of Kepong................................................................................................8

Table 7: Comparison of stockholder's equity................................................................................10

Table 8: Comparison of Long term debt........................................................................................11

Table 9: Comparison of short term debt........................................................................................12

Illustration 1: Shareholder's equity of PPB......................................................................................4

Illustration 2: Long term debt of PPB..............................................................................................5

Illustration 3: Long term debt of Kepong........................................................................................6

Illustration 4: Stockholder's equity of Kepong................................................................................7

Illustration 5: Long term liabilities of Kepong................................................................................8

Illustration 6: Short term debt of Kepong........................................................................................9

Illustration 7: Comparison of stockholder's equity........................................................................10

Illustration 8: Comparison of Long term debt...............................................................................11

Illustration 9: Comparison of short term debt................................................................................12

Index of Tables

Table 1: Shareholder's equity of PPB..............................................................................................4

Table 2: Long term debt of PPB......................................................................................................5

Table 3: Long term debt of Kepong.................................................................................................6

Table 4: Stockholder's equity of Kepong.........................................................................................6

Table 5: Long term liabilities of Kepong.........................................................................................7

Table 6: Short term debt of Kepong................................................................................................8

Table 7: Comparison of stockholder's equity................................................................................10

Table 8: Comparison of Long term debt........................................................................................11

Table 9: Comparison of short term debt........................................................................................12

INTRODUCTION

Financing is a core activity performed by the companies in order to get investment to

carry out its core business activity (Brealey and et.al., 2012). PPB group and Kuala Lumpur

Kepong are the two Malaysian companies involved in manufacturing and marketing consumer

products such as, toiletries, food products etc. The report discusses various sources of financing

used by the companies such as, debt, equity etc. Further, it discusses the difference between the

financing of the companies as per the balance sheet.

1) Overview of PPB Group and Kuala Lumpur Kepong

PPB Group

PPB group is a Malaysian diversified conglomerate which engages in food production,

agriculture, waste management, film distribution, property investment and development. PPB is

also the single largest shareholder, through an 18 percent stake, in Wilmar international, one of

the leading palm oil procedures and agribusiness companies in the world.

The company was founded in 1968 as Perlis Plantations Berhad (from which derives its

current name) by Robert kuok to cultivate and mill sugar cane in the northern Malaysian state of

perlis. The company went public in 1972 and has since ventured into other industries, although it

stops the sugar business in 2009. Today its main business is the supply of four to downstream

food producers. Its subsidiary, FFM, is the largest flour miller in Malaysia. The kuok retains

control of the company with a 50.8 percent shareholder.

Vision Statement of the company

To be a market leader in the industry reputed for our sustainable quality products and

services to customer.

Kuala Lumpur Kepong

Kuala Lumpur Kepong Berhad is a Malaysian based multi national company. It has been

involved in diversified business activities such as, property development and retailing (Brown,

Martinsson and Petersen, 2012). It is also involved in plantation of oil palm and rubber with

worldwide presence. It has various group of companies involved in the development,

Manufacturing, marketing and distribution of retail items such as personal care products,

toiletries, home fragrance and fine foods. The company operates in three segments such as

manufacturing, marketing and selling of consumer goods products. The wholesale and

distribution segment is engaged in wholesale, marketing and distribution of these products. The

1

Financing is a core activity performed by the companies in order to get investment to

carry out its core business activity (Brealey and et.al., 2012). PPB group and Kuala Lumpur

Kepong are the two Malaysian companies involved in manufacturing and marketing consumer

products such as, toiletries, food products etc. The report discusses various sources of financing

used by the companies such as, debt, equity etc. Further, it discusses the difference between the

financing of the companies as per the balance sheet.

1) Overview of PPB Group and Kuala Lumpur Kepong

PPB Group

PPB group is a Malaysian diversified conglomerate which engages in food production,

agriculture, waste management, film distribution, property investment and development. PPB is

also the single largest shareholder, through an 18 percent stake, in Wilmar international, one of

the leading palm oil procedures and agribusiness companies in the world.

The company was founded in 1968 as Perlis Plantations Berhad (from which derives its

current name) by Robert kuok to cultivate and mill sugar cane in the northern Malaysian state of

perlis. The company went public in 1972 and has since ventured into other industries, although it

stops the sugar business in 2009. Today its main business is the supply of four to downstream

food producers. Its subsidiary, FFM, is the largest flour miller in Malaysia. The kuok retains

control of the company with a 50.8 percent shareholder.

Vision Statement of the company

To be a market leader in the industry reputed for our sustainable quality products and

services to customer.

Kuala Lumpur Kepong

Kuala Lumpur Kepong Berhad is a Malaysian based multi national company. It has been

involved in diversified business activities such as, property development and retailing (Brown,

Martinsson and Petersen, 2012). It is also involved in plantation of oil palm and rubber with

worldwide presence. It has various group of companies involved in the development,

Manufacturing, marketing and distribution of retail items such as personal care products,

toiletries, home fragrance and fine foods. The company operates in three segments such as

manufacturing, marketing and selling of consumer goods products. The wholesale and

distribution segment is engaged in wholesale, marketing and distribution of these products. The

1

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

corporate segments consist of investment in retail consumer products, group properties and brand

management contract manufacturing of these goods. It provides products dossier and licensing to

a range of pharmaceuticals products. The Kepong company's products are available in 40

countries all around the world.

Vision of the company

Kuala Lumpur Kepong's vision is to provide quality products to or consumer and

diversify the business in various sectors. They also want to build an innovative business in order

to adapt to the changes that has been happening in the environment.

2) Sources of financing

Finance is the funds used for operating the business activities. It is the management of

monetary and non-monetary credentials which can be easily converted into cash. It is a simple

task of providing necessary funds needed by the business entities such as companies, firms,

individuals and others term that are most favourable in achievement of their economic goals

(Cheng, Ioannou and Serafeim, 2014).

There mainly two types of sources of Finance available for the organisations to raise the funds.

Which are as follows:

Internal sources:

These are the sources of finance which are available within the organisation for the

purpose of raising funds for the business activities (Damodaran, 2016). The term internal finance

refers to the funds which are arranged from the existing business assets and activities in the

organisation. These are various internal sources of finance available in the organisation are

mentioned below:

Retained profits : These are surplus profits of previous financial year which are retained

by the organisation for any business activity or for the purpose of raising finance in the

current financial year. Further, retained profits are those surplus gains which are not

given to the shareholders and maintained in the balance sheet of the company by

investing them back in the business (Hyman, 2014). Owner's investment : The funds which are being invested by the owner in the

organisation with the motive of starting business and continuous running of day to day

business activities. These are also called short term finance (Law and Singh, 2014).

External sources :

2

management contract manufacturing of these goods. It provides products dossier and licensing to

a range of pharmaceuticals products. The Kepong company's products are available in 40

countries all around the world.

Vision of the company

Kuala Lumpur Kepong's vision is to provide quality products to or consumer and

diversify the business in various sectors. They also want to build an innovative business in order

to adapt to the changes that has been happening in the environment.

2) Sources of financing

Finance is the funds used for operating the business activities. It is the management of

monetary and non-monetary credentials which can be easily converted into cash. It is a simple

task of providing necessary funds needed by the business entities such as companies, firms,

individuals and others term that are most favourable in achievement of their economic goals

(Cheng, Ioannou and Serafeim, 2014).

There mainly two types of sources of Finance available for the organisations to raise the funds.

Which are as follows:

Internal sources:

These are the sources of finance which are available within the organisation for the

purpose of raising funds for the business activities (Damodaran, 2016). The term internal finance

refers to the funds which are arranged from the existing business assets and activities in the

organisation. These are various internal sources of finance available in the organisation are

mentioned below:

Retained profits : These are surplus profits of previous financial year which are retained

by the organisation for any business activity or for the purpose of raising finance in the

current financial year. Further, retained profits are those surplus gains which are not

given to the shareholders and maintained in the balance sheet of the company by

investing them back in the business (Hyman, 2014). Owner's investment : The funds which are being invested by the owner in the

organisation with the motive of starting business and continuous running of day to day

business activities. These are also called short term finance (Law and Singh, 2014).

External sources :

2

In the organisation the cash flows which are generated from the outside sources or the

funds raised from the financial market are known as external sources. There are various external

sources of finance available for the organization to raise funds. Some external sources financing

areas are mentioned below:

Equity Financing : This is an external sources of finance from which funds are

generated by the issue of shares to the individuals or financial institutions in the market.

The firms should raise there funds by issuing its shares to the investors. It may include,

ordinary shares.

Debt Financing : The external source of finance in which funds are borrowed from the

financial institutions, creditors for which a fixed amount has to be made in a certain

period. Finance or the funds which are borrowed from outside the organisation. It

includes : Bank Loans, Corporate bonds, leasing, Debentures etc.

Lease financing: Assets are taken on lease rather than actually purchasing them. It is a

contract between two parties where lessor permits lessee to use an asset for a particular

duration in lieu of which it demands regular payments from the lessee. It is an effective

way of financing as it helps the enterprise to use the asset without actually purchasing it.

Overdraft: It is a facility provided by the bank where the entity is allowed to withdraw

from its bank account more than the funds it has already been there. It is a short term

financial facility provided by the bank in lieu of which it charges a certain overdraft fees

which has to paid with the amount to the bank in specific time period (Lee, Sameen and

Cowling, 2015).

Long term loans: The entity can take loans from the bank or any other licensed financial

institutions which has been approved by Bank Negara Malaysia. The entity have to pay

interest amount on regular basis till the loan has not been repaid by the enterprise.

3) Analysis of financing activities of PPB group and Kuala Lumpur Kepong

According to the balance sheet of PPB group it can be inferred that the major source of

company's finance is equity share capital. It has managed to gather equity amounting to MYR

20,973 millions in 2016. It is on the increasing phase where equity was worth MYR 19,917

millions in 2015 and MYR 16,821 millions in 2014.

3

funds raised from the financial market are known as external sources. There are various external

sources of finance available for the organization to raise funds. Some external sources financing

areas are mentioned below:

Equity Financing : This is an external sources of finance from which funds are

generated by the issue of shares to the individuals or financial institutions in the market.

The firms should raise there funds by issuing its shares to the investors. It may include,

ordinary shares.

Debt Financing : The external source of finance in which funds are borrowed from the

financial institutions, creditors for which a fixed amount has to be made in a certain

period. Finance or the funds which are borrowed from outside the organisation. It

includes : Bank Loans, Corporate bonds, leasing, Debentures etc.

Lease financing: Assets are taken on lease rather than actually purchasing them. It is a

contract between two parties where lessor permits lessee to use an asset for a particular

duration in lieu of which it demands regular payments from the lessee. It is an effective

way of financing as it helps the enterprise to use the asset without actually purchasing it.

Overdraft: It is a facility provided by the bank where the entity is allowed to withdraw

from its bank account more than the funds it has already been there. It is a short term

financial facility provided by the bank in lieu of which it charges a certain overdraft fees

which has to paid with the amount to the bank in specific time period (Lee, Sameen and

Cowling, 2015).

Long term loans: The entity can take loans from the bank or any other licensed financial

institutions which has been approved by Bank Negara Malaysia. The entity have to pay

interest amount on regular basis till the loan has not been repaid by the enterprise.

3) Analysis of financing activities of PPB group and Kuala Lumpur Kepong

According to the balance sheet of PPB group it can be inferred that the major source of

company's finance is equity share capital. It has managed to gather equity amounting to MYR

20,973 millions in 2016. It is on the increasing phase where equity was worth MYR 19,917

millions in 2015 and MYR 16,821 millions in 2014.

3

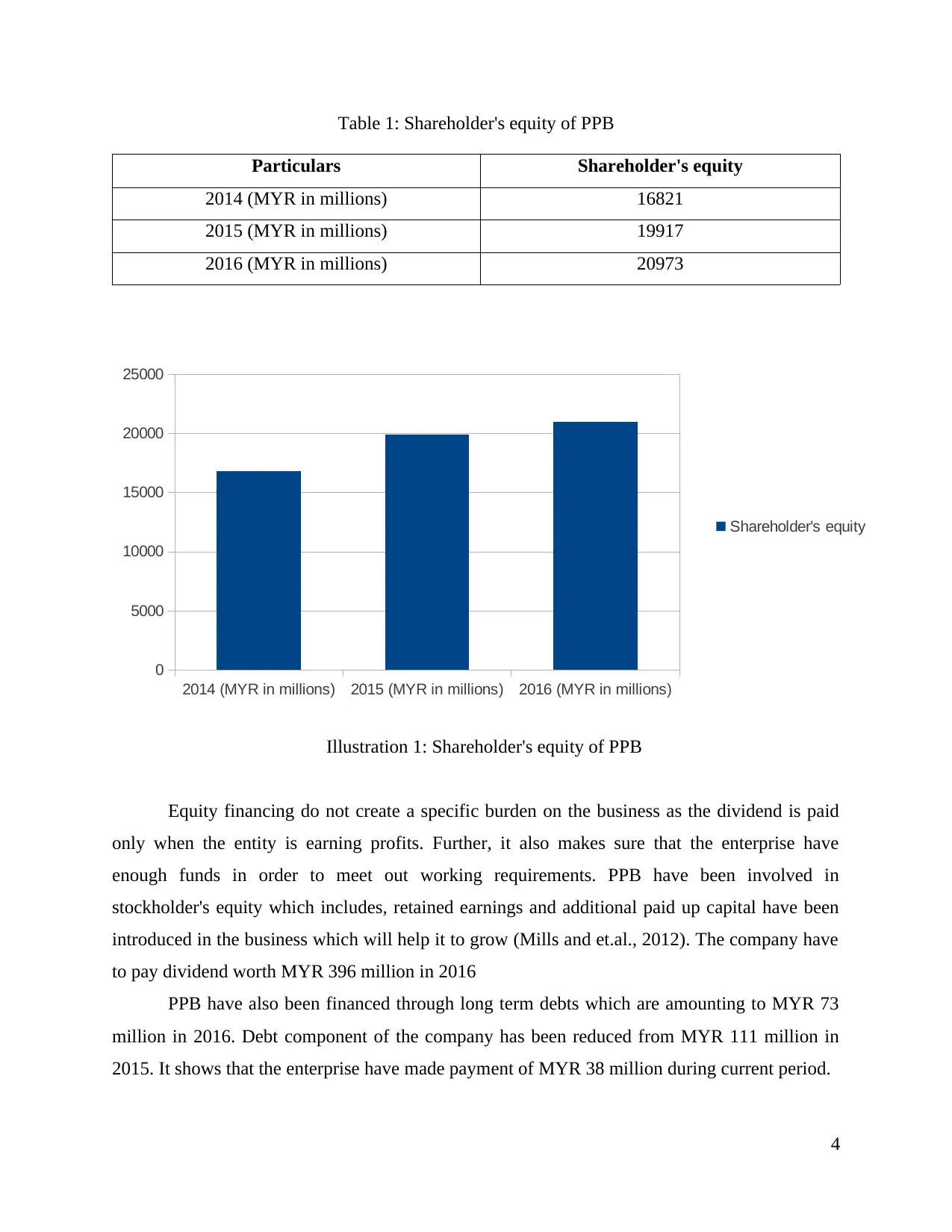

Table 1: Shareholder's equity of PPB

Particulars Shareholder's equity

2014 (MYR in millions) 16821

2015 (MYR in millions) 19917

2016 (MYR in millions) 20973

Equity financing do not create a specific burden on the business as the dividend is paid

only when the entity is earning profits. Further, it also makes sure that the enterprise have

enough funds in order to meet out working requirements. PPB have been involved in

stockholder's equity which includes, retained earnings and additional paid up capital have been

introduced in the business which will help it to grow (Mills and et.al., 2012). The company have

to pay dividend worth MYR 396 million in 2016

PPB have also been financed through long term debts which are amounting to MYR 73

million in 2016. Debt component of the company has been reduced from MYR 111 million in

2015. It shows that the enterprise have made payment of MYR 38 million during current period.

4

2014 (MYR in millions) 2015 (MYR in millions) 2016 (MYR in millions)

0

5000

10000

15000

20000

25000

Shareholder's equity

Illustration 1: Shareholder's equity of PPB

Particulars Shareholder's equity

2014 (MYR in millions) 16821

2015 (MYR in millions) 19917

2016 (MYR in millions) 20973

Equity financing do not create a specific burden on the business as the dividend is paid

only when the entity is earning profits. Further, it also makes sure that the enterprise have

enough funds in order to meet out working requirements. PPB have been involved in

stockholder's equity which includes, retained earnings and additional paid up capital have been

introduced in the business which will help it to grow (Mills and et.al., 2012). The company have

to pay dividend worth MYR 396 million in 2016

PPB have also been financed through long term debts which are amounting to MYR 73

million in 2016. Debt component of the company has been reduced from MYR 111 million in

2015. It shows that the enterprise have made payment of MYR 38 million during current period.

4

2014 (MYR in millions) 2015 (MYR in millions) 2016 (MYR in millions)

0

5000

10000

15000

20000

25000

Shareholder's equity

Illustration 1: Shareholder's equity of PPB

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

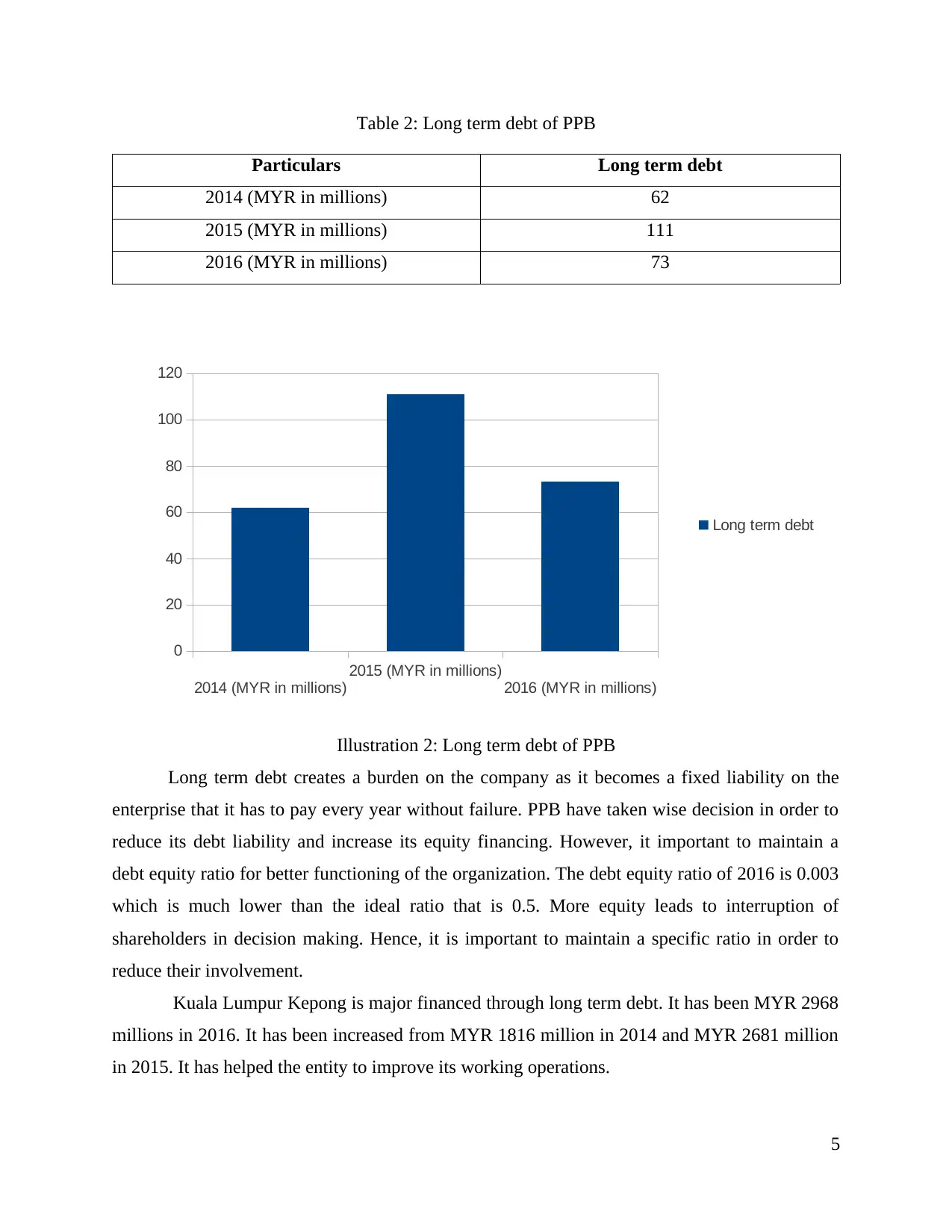

Table 2: Long term debt of PPB

Particulars Long term debt

2014 (MYR in millions) 62

2015 (MYR in millions) 111

2016 (MYR in millions) 73

Long term debt creates a burden on the company as it becomes a fixed liability on the

enterprise that it has to pay every year without failure. PPB have taken wise decision in order to

reduce its debt liability and increase its equity financing. However, it important to maintain a

debt equity ratio for better functioning of the organization. The debt equity ratio of 2016 is 0.003

which is much lower than the ideal ratio that is 0.5. More equity leads to interruption of

shareholders in decision making. Hence, it is important to maintain a specific ratio in order to

reduce their involvement.

Kuala Lumpur Kepong is major financed through long term debt. It has been MYR 2968

millions in 2016. It has been increased from MYR 1816 million in 2014 and MYR 2681 million

in 2015. It has helped the entity to improve its working operations.

5

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

20

40

60

80

100

120

Long term debt

Illustration 2: Long term debt of PPB

Particulars Long term debt

2014 (MYR in millions) 62

2015 (MYR in millions) 111

2016 (MYR in millions) 73

Long term debt creates a burden on the company as it becomes a fixed liability on the

enterprise that it has to pay every year without failure. PPB have taken wise decision in order to

reduce its debt liability and increase its equity financing. However, it important to maintain a

debt equity ratio for better functioning of the organization. The debt equity ratio of 2016 is 0.003

which is much lower than the ideal ratio that is 0.5. More equity leads to interruption of

shareholders in decision making. Hence, it is important to maintain a specific ratio in order to

reduce their involvement.

Kuala Lumpur Kepong is major financed through long term debt. It has been MYR 2968

millions in 2016. It has been increased from MYR 1816 million in 2014 and MYR 2681 million

in 2015. It has helped the entity to improve its working operations.

5

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

20

40

60

80

100

120

Long term debt

Illustration 2: Long term debt of PPB

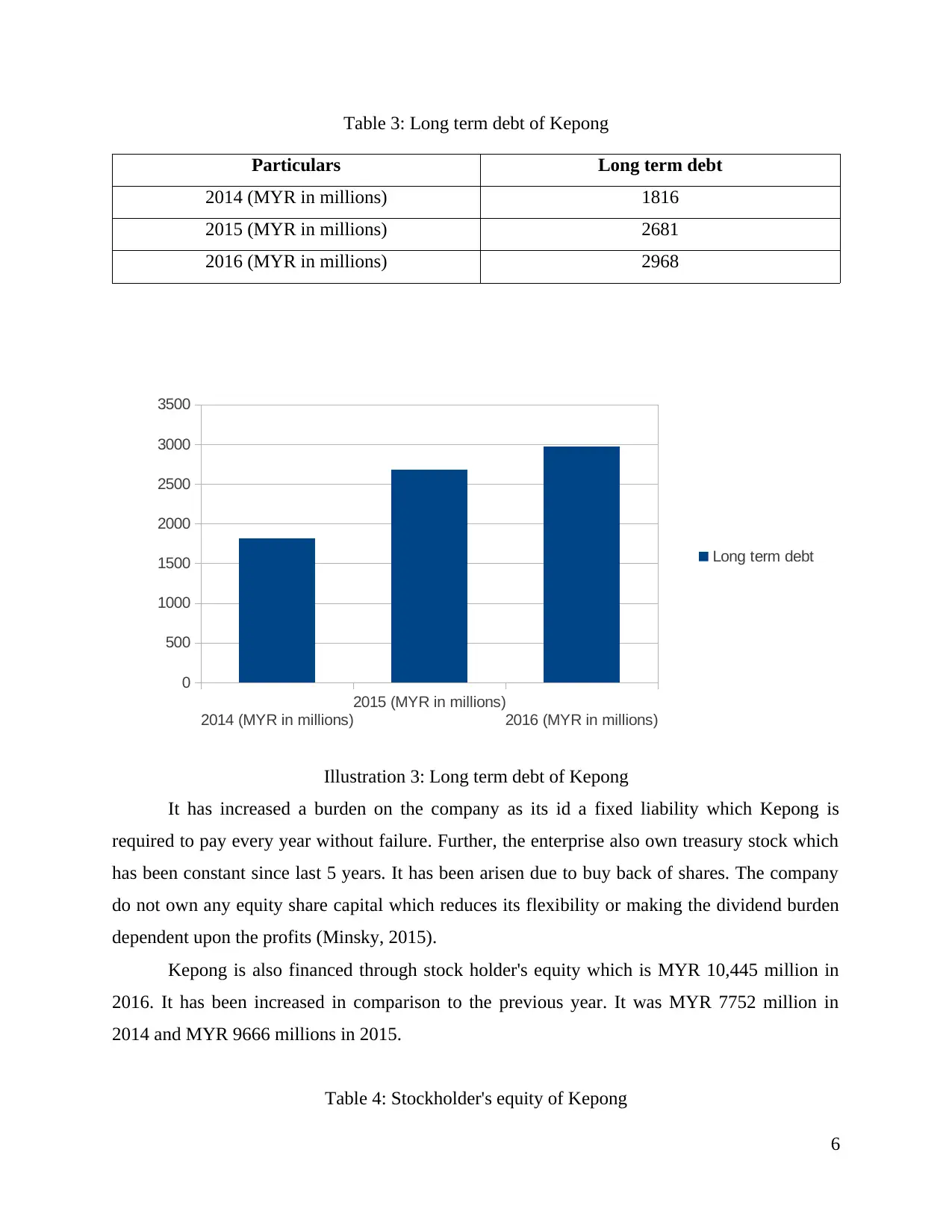

Table 3: Long term debt of Kepong

Particulars Long term debt

2014 (MYR in millions) 1816

2015 (MYR in millions) 2681

2016 (MYR in millions) 2968

It has increased a burden on the company as its id a fixed liability which Kepong is

required to pay every year without failure. Further, the enterprise also own treasury stock which

has been constant since last 5 years. It has been arisen due to buy back of shares. The company

do not own any equity share capital which reduces its flexibility or making the dividend burden

dependent upon the profits (Minsky, 2015).

Kepong is also financed through stock holder's equity which is MYR 10,445 million in

2016. It has been increased in comparison to the previous year. It was MYR 7752 million in

2014 and MYR 9666 millions in 2015.

Table 4: Stockholder's equity of Kepong

6

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

500

1000

1500

2000

2500

3000

3500

Long term debt

Illustration 3: Long term debt of Kepong

Particulars Long term debt

2014 (MYR in millions) 1816

2015 (MYR in millions) 2681

2016 (MYR in millions) 2968

It has increased a burden on the company as its id a fixed liability which Kepong is

required to pay every year without failure. Further, the enterprise also own treasury stock which

has been constant since last 5 years. It has been arisen due to buy back of shares. The company

do not own any equity share capital which reduces its flexibility or making the dividend burden

dependent upon the profits (Minsky, 2015).

Kepong is also financed through stock holder's equity which is MYR 10,445 million in

2016. It has been increased in comparison to the previous year. It was MYR 7752 million in

2014 and MYR 9666 millions in 2015.

Table 4: Stockholder's equity of Kepong

6

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

500

1000

1500

2000

2500

3000

3500

Long term debt

Illustration 3: Long term debt of Kepong

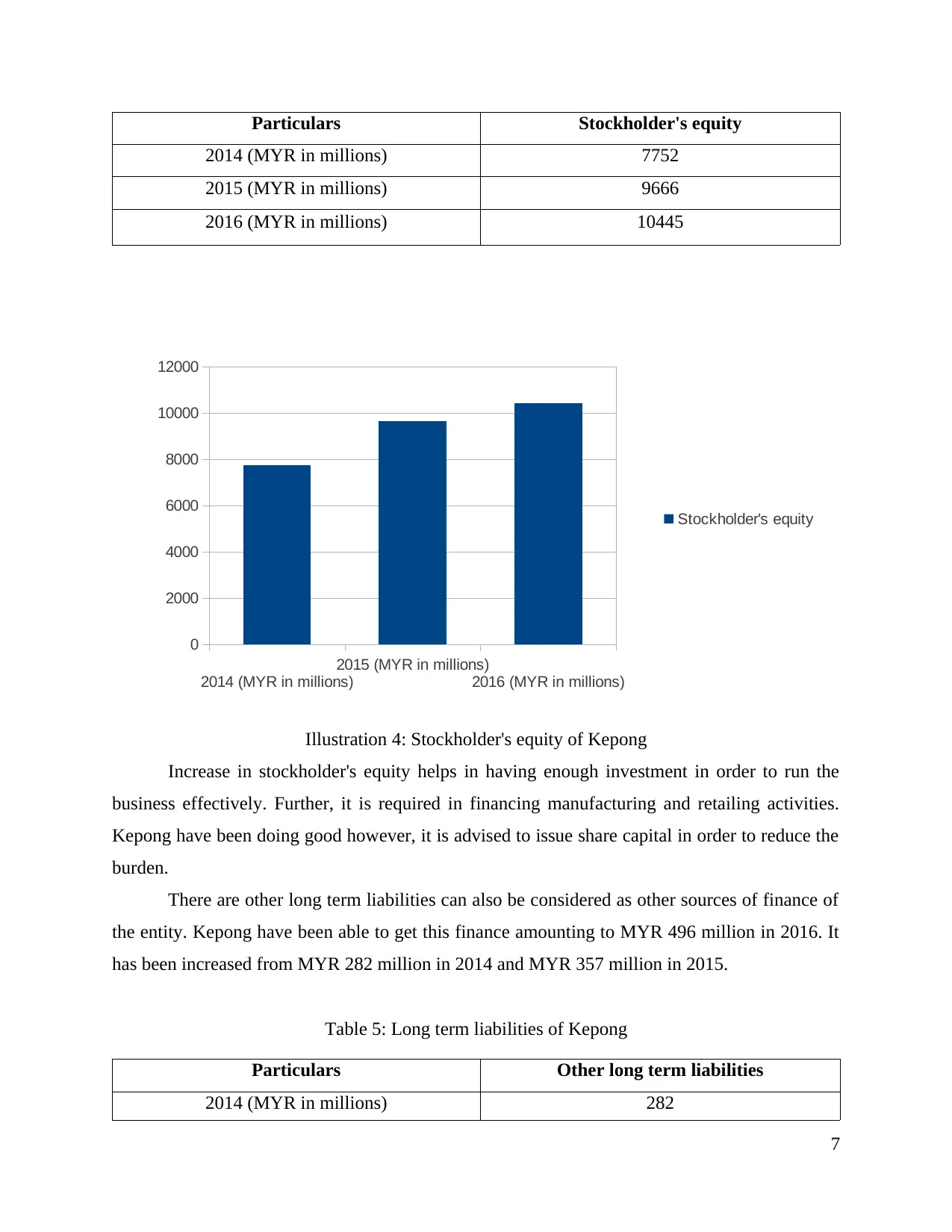

Particulars Stockholder's equity

2014 (MYR in millions) 7752

2015 (MYR in millions) 9666

2016 (MYR in millions) 10445

Increase in stockholder's equity helps in having enough investment in order to run the

business effectively. Further, it is required in financing manufacturing and retailing activities.

Kepong have been doing good however, it is advised to issue share capital in order to reduce the

burden.

There are other long term liabilities can also be considered as other sources of finance of

the entity. Kepong have been able to get this finance amounting to MYR 496 million in 2016. It

has been increased from MYR 282 million in 2014 and MYR 357 million in 2015.

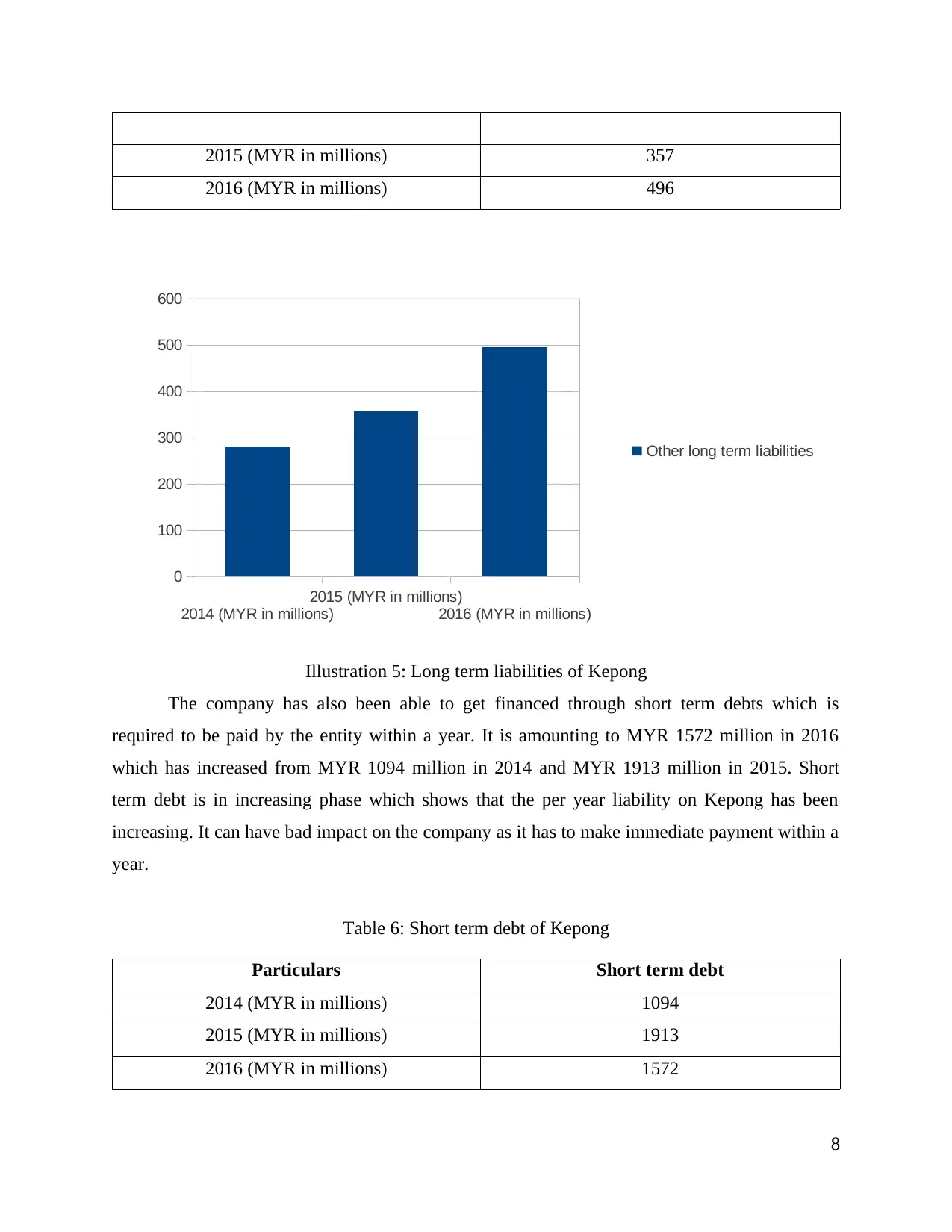

Table 5: Long term liabilities of Kepong

Particulars Other long term liabilities

2014 (MYR in millions) 282

7

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

2000

4000

6000

8000

10000

12000

Stockholder's equity

Illustration 4: Stockholder's equity of Kepong

2014 (MYR in millions) 7752

2015 (MYR in millions) 9666

2016 (MYR in millions) 10445

Increase in stockholder's equity helps in having enough investment in order to run the

business effectively. Further, it is required in financing manufacturing and retailing activities.

Kepong have been doing good however, it is advised to issue share capital in order to reduce the

burden.

There are other long term liabilities can also be considered as other sources of finance of

the entity. Kepong have been able to get this finance amounting to MYR 496 million in 2016. It

has been increased from MYR 282 million in 2014 and MYR 357 million in 2015.

Table 5: Long term liabilities of Kepong

Particulars Other long term liabilities

2014 (MYR in millions) 282

7

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

2000

4000

6000

8000

10000

12000

Stockholder's equity

Illustration 4: Stockholder's equity of Kepong

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

2015 (MYR in millions) 357

2016 (MYR in millions) 496

The company has also been able to get financed through short term debts which is

required to be paid by the entity within a year. It is amounting to MYR 1572 million in 2016

which has increased from MYR 1094 million in 2014 and MYR 1913 million in 2015. Short

term debt is in increasing phase which shows that the per year liability on Kepong has been

increasing. It can have bad impact on the company as it has to make immediate payment within a

year.

Table 6: Short term debt of Kepong

Particulars Short term debt

2014 (MYR in millions) 1094

2015 (MYR in millions) 1913

2016 (MYR in millions) 1572

8

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

100

200

300

400

500

600

Other long term liabilities

Illustration 5: Long term liabilities of Kepong

2016 (MYR in millions) 496

The company has also been able to get financed through short term debts which is

required to be paid by the entity within a year. It is amounting to MYR 1572 million in 2016

which has increased from MYR 1094 million in 2014 and MYR 1913 million in 2015. Short

term debt is in increasing phase which shows that the per year liability on Kepong has been

increasing. It can have bad impact on the company as it has to make immediate payment within a

year.

Table 6: Short term debt of Kepong

Particulars Short term debt

2014 (MYR in millions) 1094

2015 (MYR in millions) 1913

2016 (MYR in millions) 1572

8

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

100

200

300

400

500

600

Other long term liabilities

Illustration 5: Long term liabilities of Kepong

Sources of financing helps the company to get enough investment that is helpful in

performing core activities of the business. The two companies have been able to get their

business financed through equity, long term debt and other sources as well. PPB and Kepong are

also financed through short term debt financing which they are required to pay within one year

time.

4) Difference between the financing activities of PPB and Kuala Lumpur Kepong

The sources of used by PPB and Kuala Lumpur Kepong are short term and long term

debt, equity shareholders, Retained earnings, additional capital invested by the owner etc.

However there is a difference between priorities that has been given to different sources of

financing. PPB is dependent more on its equity shareholders in order to get investment in daily

operations. However, Kuala Lumpur Kepong has been dependent on long term debts and

stockholder;'s equity to get finance to conduct its business.

It is important to have a perfect ratio of debt and capital because more debt content can

lead the company into fixed burden and more equity interrupts in decision making of the

9

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

500

1000

1500

2000

2500

Short term debt

Illustration 6: Short term debt of Kepong

performing core activities of the business. The two companies have been able to get their

business financed through equity, long term debt and other sources as well. PPB and Kepong are

also financed through short term debt financing which they are required to pay within one year

time.

4) Difference between the financing activities of PPB and Kuala Lumpur Kepong

The sources of used by PPB and Kuala Lumpur Kepong are short term and long term

debt, equity shareholders, Retained earnings, additional capital invested by the owner etc.

However there is a difference between priorities that has been given to different sources of

financing. PPB is dependent more on its equity shareholders in order to get investment in daily

operations. However, Kuala Lumpur Kepong has been dependent on long term debts and

stockholder;'s equity to get finance to conduct its business.

It is important to have a perfect ratio of debt and capital because more debt content can

lead the company into fixed burden and more equity interrupts in decision making of the

9

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

500

1000

1500

2000

2500

Short term debt

Illustration 6: Short term debt of Kepong

management. Short term debt financing create burden on the entity as the repayment has to be

made within 1 year of its issuance.

Table 7: Comparison of stockholder's equity

Stockholder's equity

Particulars PPB Kuala Lumpur Kepong

2014 (MYR in millions) 16821 7752

2015 (MYR in millions) 19917 9666

2016 (MYR in millions) 20973 10445

PPB have stockholder's equity of MYR 20973 million in 2016 which is much higher than

that of Kepong which is MYR 10445 million. It shows that PPB have high stockholder

investment in the company in comparison to that of Kepong. It proves that PPB is high on equity

and has larger interest of shareholders in decision making process of the company. However, the

entity also enjoys higher investment which helps to conduct its business operation in better

10

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

5000

10000

15000

20000

25000

PPB

Kuala Lumpur Kepong

Illustration 7: Comparison of stockholder's equity

made within 1 year of its issuance.

Table 7: Comparison of stockholder's equity

Stockholder's equity

Particulars PPB Kuala Lumpur Kepong

2014 (MYR in millions) 16821 7752

2015 (MYR in millions) 19917 9666

2016 (MYR in millions) 20973 10445

PPB have stockholder's equity of MYR 20973 million in 2016 which is much higher than

that of Kepong which is MYR 10445 million. It shows that PPB have high stockholder

investment in the company in comparison to that of Kepong. It proves that PPB is high on equity

and has larger interest of shareholders in decision making process of the company. However, the

entity also enjoys higher investment which helps to conduct its business operation in better

10

2014 (MYR in millions)

2015 (MYR in millions)

2016 (MYR in millions)

0

5000

10000

15000

20000

25000

PPB

Kuala Lumpur Kepong

Illustration 7: Comparison of stockholder's equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

manner. The enterprise also do not have to pay fixed dividend to the shareholders and can

proceed it as and when business earns profits.

According to the long term debt that the companies have taken from outside. It creates a

burden on the organization as it have to pay interest to the debt holders every year without any

failure till the time repayment has not been made for the principle amount. This liability arise

even if the entity is running on losses (Philippon and Reshef, 201).

Table 8: Comparison of Long term debt

Long term debt

Particulars PPB Kepong

2014 (MYR in millions) 62 1816

2015 (MYR in millions) 111 2681

2016 (MYR in millions) 73 2968

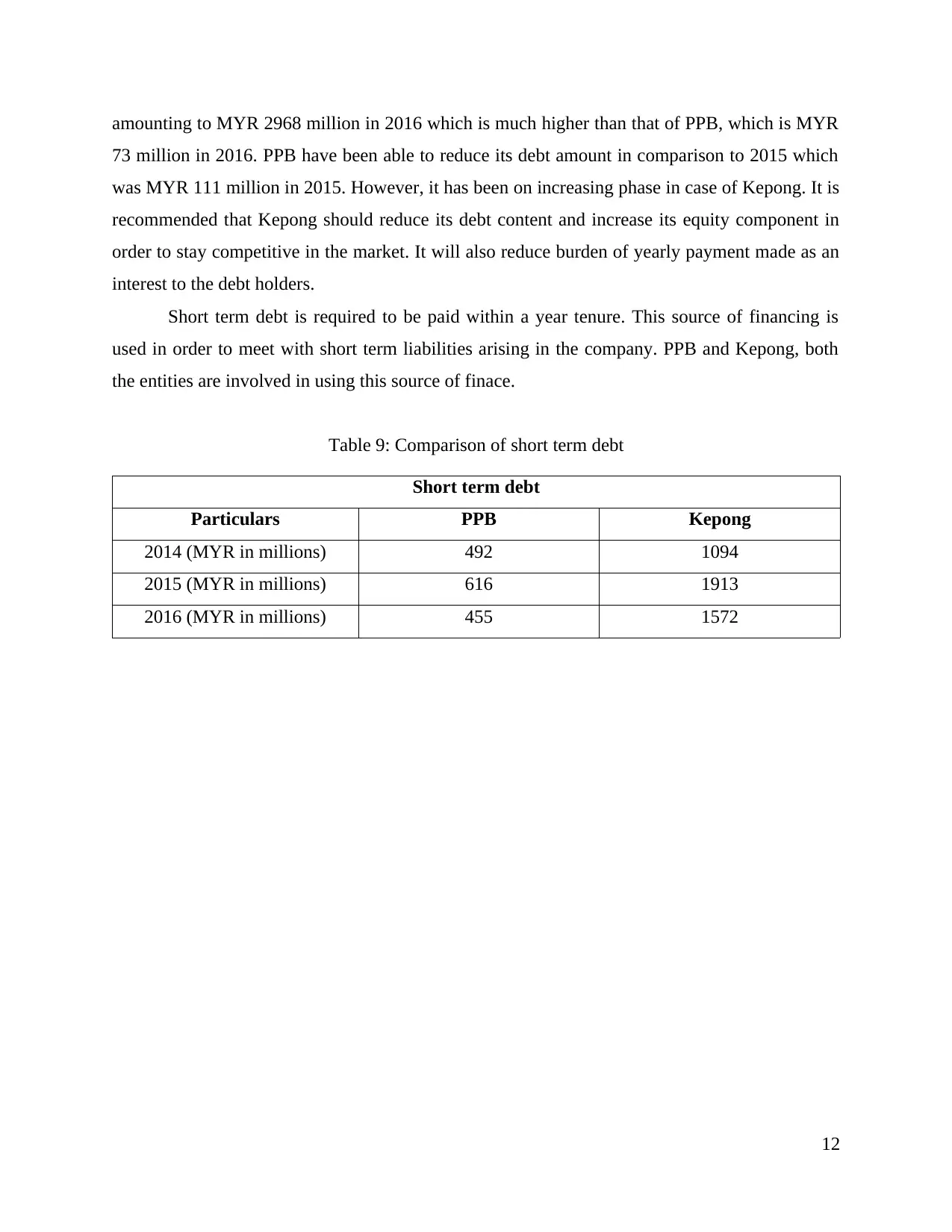

Based on the above graph, it can be interpreted that the long term debt of Kuala Lumpur

Kepong is on higher side in comparison to that of PPB. PPB is less dependent on long term debt

and more on equity shareholders for investment in its business. Kepong have long term debt

11

2014 (MYR in millions) 2015 (MYR in millions) 2016 (MYR in millions)

0

500

1000

1500

2000

2500

3000

3500

PPB

Kepong

Illustration 8: Comparison of Long term debt

proceed it as and when business earns profits.

According to the long term debt that the companies have taken from outside. It creates a

burden on the organization as it have to pay interest to the debt holders every year without any

failure till the time repayment has not been made for the principle amount. This liability arise

even if the entity is running on losses (Philippon and Reshef, 201).

Table 8: Comparison of Long term debt

Long term debt

Particulars PPB Kepong

2014 (MYR in millions) 62 1816

2015 (MYR in millions) 111 2681

2016 (MYR in millions) 73 2968

Based on the above graph, it can be interpreted that the long term debt of Kuala Lumpur

Kepong is on higher side in comparison to that of PPB. PPB is less dependent on long term debt

and more on equity shareholders for investment in its business. Kepong have long term debt

11

2014 (MYR in millions) 2015 (MYR in millions) 2016 (MYR in millions)

0

500

1000

1500

2000

2500

3000

3500

PPB

Kepong

Illustration 8: Comparison of Long term debt

amounting to MYR 2968 million in 2016 which is much higher than that of PPB, which is MYR

73 million in 2016. PPB have been able to reduce its debt amount in comparison to 2015 which

was MYR 111 million in 2015. However, it has been on increasing phase in case of Kepong. It is

recommended that Kepong should reduce its debt content and increase its equity component in

order to stay competitive in the market. It will also reduce burden of yearly payment made as an

interest to the debt holders.

Short term debt is required to be paid within a year tenure. This source of financing is

used in order to meet with short term liabilities arising in the company. PPB and Kepong, both

the entities are involved in using this source of finace.

Table 9: Comparison of short term debt

Short term debt

Particulars PPB Kepong

2014 (MYR in millions) 492 1094

2015 (MYR in millions) 616 1913

2016 (MYR in millions) 455 1572

12

73 million in 2016. PPB have been able to reduce its debt amount in comparison to 2015 which

was MYR 111 million in 2015. However, it has been on increasing phase in case of Kepong. It is

recommended that Kepong should reduce its debt content and increase its equity component in

order to stay competitive in the market. It will also reduce burden of yearly payment made as an

interest to the debt holders.

Short term debt is required to be paid within a year tenure. This source of financing is

used in order to meet with short term liabilities arising in the company. PPB and Kepong, both

the entities are involved in using this source of finace.

Table 9: Comparison of short term debt

Short term debt

Particulars PPB Kepong

2014 (MYR in millions) 492 1094

2015 (MYR in millions) 616 1913

2016 (MYR in millions) 455 1572

12

The short term liabilities of Kepong is mush higher than that of PPB. It is amounting

MYR 1572 million in 2016 which is much lower in case of PPB, that is MYR 455 million. It

shows that Kepong's yearly liability is on higher side and company is required to increase its

revenue in order to meet its short term liabilities.

CONCLUSION

From the above report, it can be concluded that, there are various sources of internal and

external financing that can be used by a company. Some external sources are, equity, long term

and short term debt, leasing etc. PPB and Kuala Lumpur Kepong are the two Malaysian

consumer product companies involved in manufacturing and marketing toiletries, foods

beverages ects. The major source of financing got PPB is stockholder's equity. On the other

hand, Kepong use long term and short term debt in order to meet its investment requirements.

13

2014 (MYR in millions) 2015 (MYR in millions) 2016 (MYR in millions)

0

500

1000

1500

2000

2500

PPB

Kepong

Illustration 9: Comparison of short term debt

MYR 1572 million in 2016 which is much lower in case of PPB, that is MYR 455 million. It

shows that Kepong's yearly liability is on higher side and company is required to increase its

revenue in order to meet its short term liabilities.

CONCLUSION

From the above report, it can be concluded that, there are various sources of internal and

external financing that can be used by a company. Some external sources are, equity, long term

and short term debt, leasing etc. PPB and Kuala Lumpur Kepong are the two Malaysian

consumer product companies involved in manufacturing and marketing toiletries, foods

beverages ects. The major source of financing got PPB is stockholder's equity. On the other

hand, Kepong use long term and short term debt in order to meet its investment requirements.

13

2014 (MYR in millions) 2015 (MYR in millions) 2016 (MYR in millions)

0

500

1000

1500

2000

2500

PPB

Kepong

Illustration 9: Comparison of short term debt

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

REFERENCES

Brealey, R. A. and et.al., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Brown, J. R., Martinsson, G. and Petersen, B. C., 2012. Do financing constraints matter for

R&D?. European Economic Review. 56(8). pp.1512-1529.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic Management Journal. 35(1). pp.1-23.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Hyman, D. N., 2014. Public finance: A contemporary application of theory to policy. Cengage

Learning.

Law, S. H. and Singh, N., 2014. Does too much finance harm economic growth?. Journal of

Banking & Finance. 41. pp.36-44.

Lee, N., Sameen, H. and Cowling, M., 2015. Access to finance for innovative SMEs since the

financial crisis. Research policy. 44(2). pp.370-380.

Mills, A. and et.al., 2012. Equity in financing and use of health care in Ghana, South Africa, and

Tanzania: implications for paths to universal coverage. The Lancet. 380(9837). pp.126-

133.

Minsky, H. P., 2015. Can" it" happen again?: essays on instability and finance. Routledge.

Philippon, T. and Reshef, A., 2013. An international look at the growth of modern finance. The

Journal of Economic Perspectives. 27(2). pp.73-96.

14

Brealey, R. A. and et.al., 2012. Principles of corporate finance. Tata McGraw-Hill Education.

Brown, J. R., Martinsson, G. and Petersen, B. C., 2012. Do financing constraints matter for

R&D?. European Economic Review. 56(8). pp.1512-1529.

Cheng, B., Ioannou, I. and Serafeim, G., 2014. Corporate social responsibility and access to

finance. Strategic Management Journal. 35(1). pp.1-23.

Damodaran, A., 2016. Damodaran on valuation: security analysis for investment and corporate

finance (Vol. 324). John Wiley & Sons.

Hyman, D. N., 2014. Public finance: A contemporary application of theory to policy. Cengage

Learning.

Law, S. H. and Singh, N., 2014. Does too much finance harm economic growth?. Journal of

Banking & Finance. 41. pp.36-44.

Lee, N., Sameen, H. and Cowling, M., 2015. Access to finance for innovative SMEs since the

financial crisis. Research policy. 44(2). pp.370-380.

Mills, A. and et.al., 2012. Equity in financing and use of health care in Ghana, South Africa, and

Tanzania: implications for paths to universal coverage. The Lancet. 380(9837). pp.126-

133.

Minsky, H. P., 2015. Can" it" happen again?: essays on instability and finance. Routledge.

Philippon, T. and Reshef, A., 2013. An international look at the growth of modern finance. The

Journal of Economic Perspectives. 27(2). pp.73-96.

14

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.