Harvey Norman Financial Report: Accounting Theory & Ratio Analysis

VerifiedAdded on 2023/06/08

|22

|4128

|105

Report

AI Summary

This report provides a comprehensive analysis of Harvey Norman's financial statements, applying key financial ratios, accounting standards, and conceptual frameworks. It examines the company's market position, competitive forces, and adherence to AASB and IFRS standards. The analysis includes a review of contingent liabilities, corporate governance, and a competitor analysis focusing on firms like Woolworths and Myer Holdings Ltd. Ratio analysis, including current ratio, quick ratio, gearing ratio, and profit margin ratios, reveals insights into the company's profitability and liquidity. The report concludes with recommendations based on the financial analysis, offering a perspective on whether to invest in Harvey Norman based on its financial performance and market position. Desklib provides a platform for students to access similar solved assignments and past papers for academic assistance.

Running head: ACCOUNTING THEORY & CONTEMPORARY ISSUES

Accounting Theory & Contemporary Issues

University Name

Student Name

Authors’ Note

Accounting Theory & Contemporary Issues

University Name

Student Name

Authors’ Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

ACCOUNTING THEORY & CONTEMPORARY ISSUES

Executive Summary

The study critically analyses the financial statements using key financial ratio, uses of

accounting standards and conceptual framework with special orientation to the firm Harvey

Norman. Also, this study focuses on the market in which the firm operates and presents a

review of the same. Additionally, this study also elucidates in detail about the competitive

forces and competitive position of the firm. The findings of financial analysis suggests about

a favourable profitability condition of the firm as it has maintained positive trends in profit

margin. However, issues can be detected in the liquidity position that can be addressed by

means of the suggested measures discussed in the study.

ACCOUNTING THEORY & CONTEMPORARY ISSUES

Executive Summary

The study critically analyses the financial statements using key financial ratio, uses of

accounting standards and conceptual framework with special orientation to the firm Harvey

Norman. Also, this study focuses on the market in which the firm operates and presents a

review of the same. Additionally, this study also elucidates in detail about the competitive

forces and competitive position of the firm. The findings of financial analysis suggests about

a favourable profitability condition of the firm as it has maintained positive trends in profit

margin. However, issues can be detected in the liquidity position that can be addressed by

means of the suggested measures discussed in the study.

3

ACCOUNTING THEORY & CONTEMPORARY ISSUES

Table of Contents

Introduction................................................................................................................................4

Body...........................................................................................................................................4

-Current Market Analysis of the company.............................................................................4

-Accounting Standards used by the company........................................................................4

-Contingent liability of the company.....................................................................................6

-Conceptual Framework.........................................................................................................6

-Competitor Analysis of the company...................................................................................7

-Ratio Analysis of the company.............................................................................................8

Recommendations................................................................................................................13

Conclusion............................................................................................................................14

References................................................................................................................................15

Appendix..............................................................................................................................17

INCOME STATEMENT.....................................................................................................17

BALANCE SHEET.............................................................................................................18

Ratio Analysis......................................................................................................................20

ACCOUNTING THEORY & CONTEMPORARY ISSUES

Table of Contents

Introduction................................................................................................................................4

Body...........................................................................................................................................4

-Current Market Analysis of the company.............................................................................4

-Accounting Standards used by the company........................................................................4

-Contingent liability of the company.....................................................................................6

-Conceptual Framework.........................................................................................................6

-Competitor Analysis of the company...................................................................................7

-Ratio Analysis of the company.............................................................................................8

Recommendations................................................................................................................13

Conclusion............................................................................................................................14

References................................................................................................................................15

Appendix..............................................................................................................................17

INCOME STATEMENT.....................................................................................................17

BALANCE SHEET.............................................................................................................18

Ratio Analysis......................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

ACCOUNTING THEORY & CONTEMPORARY ISSUES

Introduction

The study at hand concentrates on delivering an insight regarding analysis of financial

statement using key ratio, review of accounting standards used and conceptual framework

with special reference to the company Harvey Norman. Harvey Norman, a publicly listed

firm on the Australian Stock Exchange is selected for undertaking the research on the

financial statements. Moving further, the company also presents a critical analysis of the

market in which the firm operates and further reviews the competitive forces that affect the

operations of the firm.

Body

-Current Market Analysis of the company

The company Harvey Norman Holdings Limited is primarily engaged in retailing business of

products such as furniture, electrical products, communications, bedding as well as computers

2001 (Harveynormanholdings.com.au, 2018). The business enterprise undertakes overseas

business activities that are outside Australia all the way through franchising model. In itself,

this firm gets lease payments from different franchise stores based on percentage of sales.

Currently, they own around 260 retail stores across the nation as well as franchise stores all

around the world. This publicly traded (ASX) listed company is supposed operates different

labelled department stores in different locations namely Australia, Malaysia, New Zealand

and Ireland among many others (Harvey Norman Australia, 2018). Also, this company is

regarded as largest retailer of computer hardware as well as software products in the world.

-Accounting Standards used by the company

The financial statement of the Harvey Norman Holdings Limited is a general-purpose

financial report prepared as per the regulations stipulated under the Australian Accounting

ACCOUNTING THEORY & CONTEMPORARY ISSUES

Introduction

The study at hand concentrates on delivering an insight regarding analysis of financial

statement using key ratio, review of accounting standards used and conceptual framework

with special reference to the company Harvey Norman. Harvey Norman, a publicly listed

firm on the Australian Stock Exchange is selected for undertaking the research on the

financial statements. Moving further, the company also presents a critical analysis of the

market in which the firm operates and further reviews the competitive forces that affect the

operations of the firm.

Body

-Current Market Analysis of the company

The company Harvey Norman Holdings Limited is primarily engaged in retailing business of

products such as furniture, electrical products, communications, bedding as well as computers

2001 (Harveynormanholdings.com.au, 2018). The business enterprise undertakes overseas

business activities that are outside Australia all the way through franchising model. In itself,

this firm gets lease payments from different franchise stores based on percentage of sales.

Currently, they own around 260 retail stores across the nation as well as franchise stores all

around the world. This publicly traded (ASX) listed company is supposed operates different

labelled department stores in different locations namely Australia, Malaysia, New Zealand

and Ireland among many others (Harvey Norman Australia, 2018). Also, this company is

regarded as largest retailer of computer hardware as well as software products in the world.

-Accounting Standards used by the company

The financial statement of the Harvey Norman Holdings Limited is a general-purpose

financial report prepared as per the regulations stipulated under the Australian Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

ACCOUNTING THEORY & CONTEMPORARY ISSUES

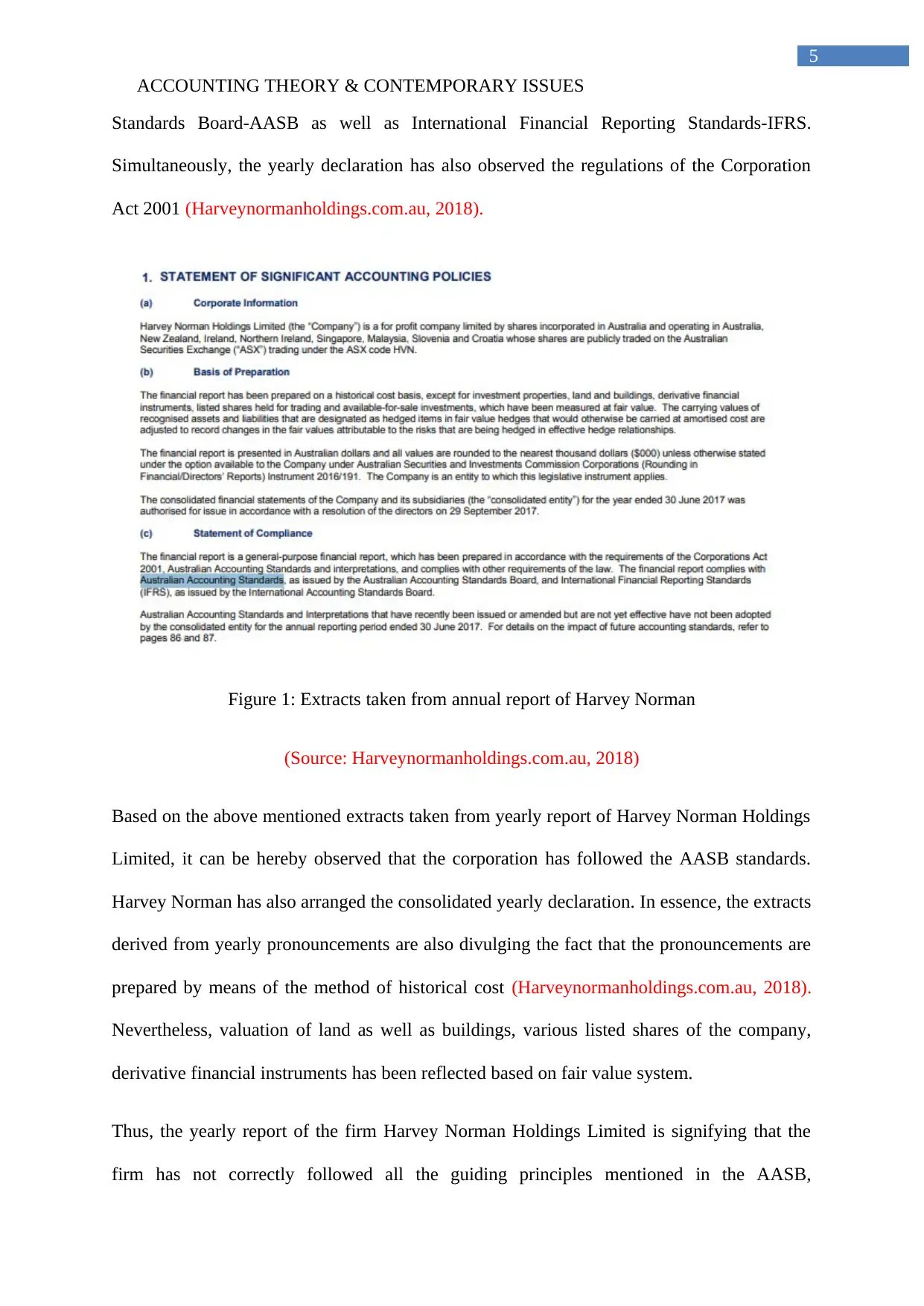

Standards Board-AASB as well as International Financial Reporting Standards-IFRS.

Simultaneously, the yearly declaration has also observed the regulations of the Corporation

Act 2001 (Harveynormanholdings.com.au, 2018).

Figure 1: Extracts taken from annual report of Harvey Norman

(Source: Harveynormanholdings.com.au, 2018)

Based on the above mentioned extracts taken from yearly report of Harvey Norman Holdings

Limited, it can be hereby observed that the corporation has followed the AASB standards.

Harvey Norman has also arranged the consolidated yearly declaration. In essence, the extracts

derived from yearly pronouncements are also divulging the fact that the pronouncements are

prepared by means of the method of historical cost (Harveynormanholdings.com.au, 2018).

Nevertheless, valuation of land as well as buildings, various listed shares of the company,

derivative financial instruments has been reflected based on fair value system.

Thus, the yearly report of the firm Harvey Norman Holdings Limited is signifying that the

firm has not correctly followed all the guiding principles mentioned in the AASB,

ACCOUNTING THEORY & CONTEMPORARY ISSUES

Standards Board-AASB as well as International Financial Reporting Standards-IFRS.

Simultaneously, the yearly declaration has also observed the regulations of the Corporation

Act 2001 (Harveynormanholdings.com.au, 2018).

Figure 1: Extracts taken from annual report of Harvey Norman

(Source: Harveynormanholdings.com.au, 2018)

Based on the above mentioned extracts taken from yearly report of Harvey Norman Holdings

Limited, it can be hereby observed that the corporation has followed the AASB standards.

Harvey Norman has also arranged the consolidated yearly declaration. In essence, the extracts

derived from yearly pronouncements are also divulging the fact that the pronouncements are

prepared by means of the method of historical cost (Harveynormanholdings.com.au, 2018).

Nevertheless, valuation of land as well as buildings, various listed shares of the company,

derivative financial instruments has been reflected based on fair value system.

Thus, the yearly report of the firm Harvey Norman Holdings Limited is signifying that the

firm has not correctly followed all the guiding principles mentioned in the AASB,

6

ACCOUNTING THEORY & CONTEMPORARY ISSUES

particularly for enumerations of different financial values barring certain assets. Again, in

case of the yearly statement of the firm it has been stated that corporate governance of the

company is essentially good, although nothing has been stated to uphold that the corporate

governance status is at a satisfactory level. Basically, the report presented by the director of

the Harvey Norman declared that the firm has pursued diverse principles and doctrines of

good corporate governance but the principles that the firm has followed has not been stated in

the declaration (Harveynormanholdings.com.au, 2018).

-Contingent liability of the company

According to AASB 137, a business entity is supposed to reveal contingent liabilities in case

if it regards itself to be liable towards the community. Nevertheless, analysis of the yearly

declaration of the firm Harvey Norman Holdings Limited reveals that the company has

divulged about the contingent liabilities clearly in the report (Harveynormanholdings.com.au,

2018). As per report for the period of June 30, 2017, this consolidated business entity does

not necessarily have contingent liabilities at all. According to reports, the contingent liability

registered as on June 30 of the year 2016 was $10.30 million associated to “guarantee” for

presentation of joint venture unit that had entered into a specific loan facility together with

many other parties (Harveynormanholdings.com.au, 2018).

-Conceptual Framework

Harvey Norman intends to commit towards attainment of sustainability in the upcoming

period. This necessarily gives an explanation for socio-economic, environmental influence of

diverse operations carried out for the purpose of analysis of future period. This necessarily

concentrates on presenting best outcomes that can reap benefits for the society and carry

positive business necessarily in an effectual manner. Fundamentally, this makes sure

developing on reputation and helps in placing as first-rate corporate citizen in the future

period. So far as the notion of conceptual framework is concerned, this necessarily takes into

ACCOUNTING THEORY & CONTEMPORARY ISSUES

particularly for enumerations of different financial values barring certain assets. Again, in

case of the yearly statement of the firm it has been stated that corporate governance of the

company is essentially good, although nothing has been stated to uphold that the corporate

governance status is at a satisfactory level. Basically, the report presented by the director of

the Harvey Norman declared that the firm has pursued diverse principles and doctrines of

good corporate governance but the principles that the firm has followed has not been stated in

the declaration (Harveynormanholdings.com.au, 2018).

-Contingent liability of the company

According to AASB 137, a business entity is supposed to reveal contingent liabilities in case

if it regards itself to be liable towards the community. Nevertheless, analysis of the yearly

declaration of the firm Harvey Norman Holdings Limited reveals that the company has

divulged about the contingent liabilities clearly in the report (Harveynormanholdings.com.au,

2018). As per report for the period of June 30, 2017, this consolidated business entity does

not necessarily have contingent liabilities at all. According to reports, the contingent liability

registered as on June 30 of the year 2016 was $10.30 million associated to “guarantee” for

presentation of joint venture unit that had entered into a specific loan facility together with

many other parties (Harveynormanholdings.com.au, 2018).

-Conceptual Framework

Harvey Norman intends to commit towards attainment of sustainability in the upcoming

period. This necessarily gives an explanation for socio-economic, environmental influence of

diverse operations carried out for the purpose of analysis of future period. This necessarily

concentrates on presenting best outcomes that can reap benefits for the society and carry

positive business necessarily in an effectual manner. Fundamentally, this makes sure

developing on reputation and helps in placing as first-rate corporate citizen in the future

period. So far as the notion of conceptual framework is concerned, this necessarily takes into

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

ACCOUNTING THEORY & CONTEMPORARY ISSUES

consideration explanation of different objectives present in the process of arrangement and

preparation of GPFR (general purpose of financial reporting)

(Harveynormanholdings.com.au, 2018). Essentially, this can be considered as one of the

realistic tools that support and help the Board in the process of arrangement and preparation

of reports as per regulations stipulated under IFRS standards. As such, it concentrates

primarily on preparation of financial accounting for the purpose of developing a variety of

accounting strategies simultaneously (Mohanram, et al., 2018). Fundamentally, there exists

no definite IFRS standard that assists the overall process of preparation of financial assertions

of firms. Robinson, et al. (2015) suggests that it facilitates the process of comprehension

along with interpretation of financial assertion on the whole. According to Robinson, et al.

(2015), conceptual framework aids in the process of enhancing ways in particularly the

system of economic reporting. Thus, it attains the objectives concerning present conceptual

framework by the members of the Board. Moving further, it has the intention to update and

improve the “conceptual framework” in modified form. However, conceptual framework also

appropriately defines overall nature and rationale of accounting principles in unison, makes

certain tackling theoretical along with conceptual concerns in compliance with business

actions (Griffin, 2015). Also, it has the need to make certain that system of financial reporting

can bring rational and reliable information in the most suitable manner. Essentially, this

intends to underpin developments of accounting standards.

-Competitor Analysis of the company

There are quite a number of firms that act as competitive forces to the firm Harvey Norman.

It can be hereby observed that that the United States exerts a huge threat. In essence,

packaged software corporate is associated to technical know-how as well as savvy marketing

exercises. In essence, the economy of U.S. exerts influence on business spending for diverse

ACCOUNTING THEORY & CONTEMPORARY ISSUES

consideration explanation of different objectives present in the process of arrangement and

preparation of GPFR (general purpose of financial reporting)

(Harveynormanholdings.com.au, 2018). Essentially, this can be considered as one of the

realistic tools that support and help the Board in the process of arrangement and preparation

of reports as per regulations stipulated under IFRS standards. As such, it concentrates

primarily on preparation of financial accounting for the purpose of developing a variety of

accounting strategies simultaneously (Mohanram, et al., 2018). Fundamentally, there exists

no definite IFRS standard that assists the overall process of preparation of financial assertions

of firms. Robinson, et al. (2015) suggests that it facilitates the process of comprehension

along with interpretation of financial assertion on the whole. According to Robinson, et al.

(2015), conceptual framework aids in the process of enhancing ways in particularly the

system of economic reporting. Thus, it attains the objectives concerning present conceptual

framework by the members of the Board. Moving further, it has the intention to update and

improve the “conceptual framework” in modified form. However, conceptual framework also

appropriately defines overall nature and rationale of accounting principles in unison, makes

certain tackling theoretical along with conceptual concerns in compliance with business

actions (Griffin, 2015). Also, it has the need to make certain that system of financial reporting

can bring rational and reliable information in the most suitable manner. Essentially, this

intends to underpin developments of accounting standards.

-Competitor Analysis of the company

There are quite a number of firms that act as competitive forces to the firm Harvey Norman.

It can be hereby observed that that the United States exerts a huge threat. In essence,

packaged software corporate is associated to technical know-how as well as savvy marketing

exercises. In essence, the economy of U.S. exerts influence on business spending for diverse

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

ACCOUNTING THEORY & CONTEMPORARY ISSUES

software products and overall accomplishment of programming. For this the firms relies

strongly on technology as well as technical know-how (Harveynormanholdings.com.au,

2018). However, small sized software corporations compete to a large extent by means of

development of packaged goods in different petite niche areas or else manufacture custom

products for particularly individuals. There are certain small sized corporation that present

alliances with larger business in a bid to promote their wares. Whilst Harvey Norman

competes in this specific segment, it too competes in different other segments as well. In

general, key competitors of the firm Harvey Norman are Woolworths Myer Holdings Ltd as

well as David Jones Limited (Harveynormanholdings.com.au, 2018).

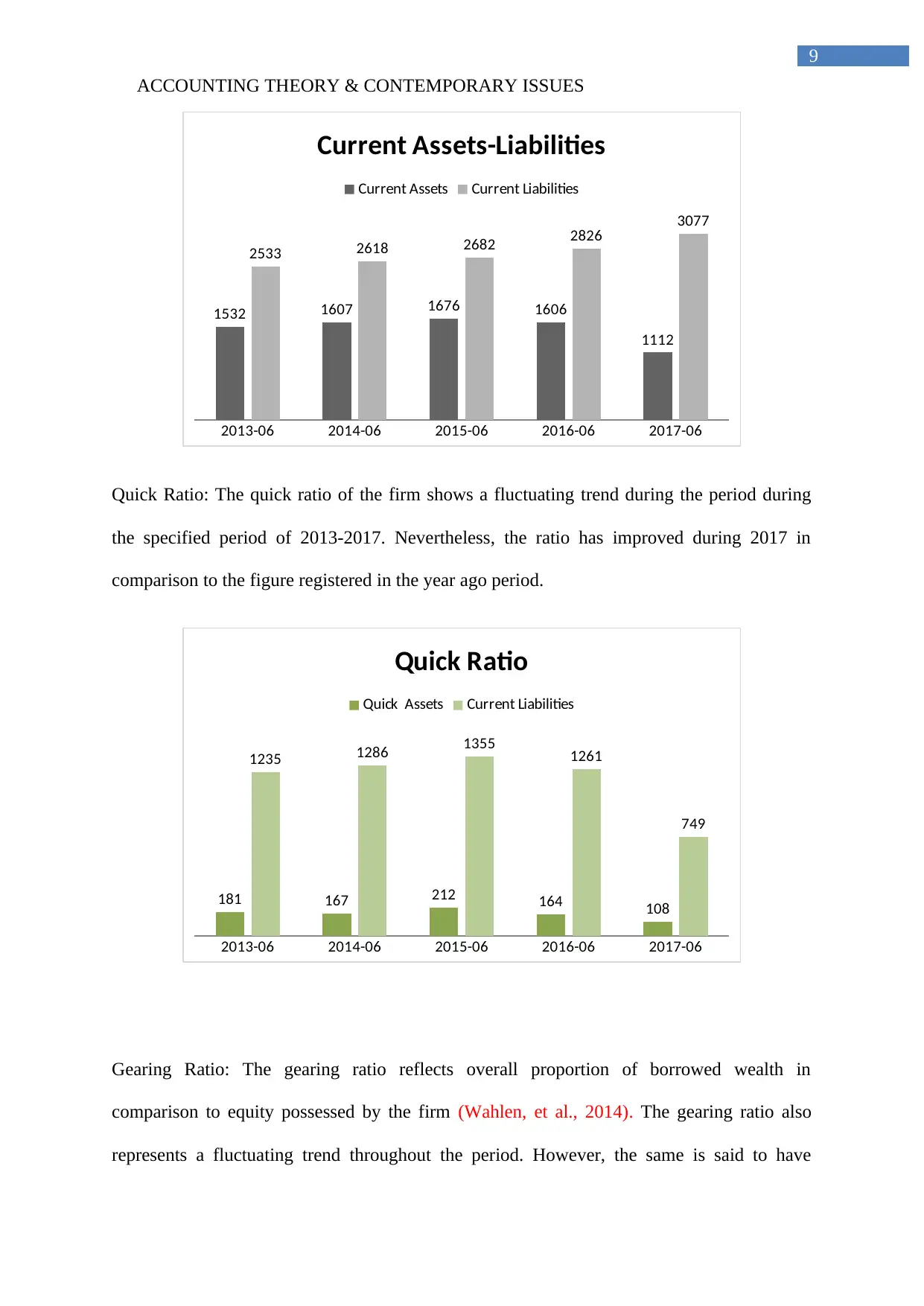

-Ratio Analysis of the company

Based on the results of the ratio analysis of the firm for the period 2013-2017 (refer to table 1

presented in appendix) it is possible to analyse the condition of the financial health of the

firm. The findings of the key ratios are hereby analysed one by one:

Current ratio: The current ratio calculated for the period 2013 to 2017 shows a declining

trend. This shows that the potency of the firm to pay off different short term debts has

declined considerably, reflecting unfavourable financial condition (Drake, et al., 2017). Also,

the current ratio is not even close to the industry standard of 2:1 that means a firm possessing

double assets in comparison to that of liabilities, reflecting greater potency of paying back

debts (Grant, 2016).

ACCOUNTING THEORY & CONTEMPORARY ISSUES

software products and overall accomplishment of programming. For this the firms relies

strongly on technology as well as technical know-how (Harveynormanholdings.com.au,

2018). However, small sized software corporations compete to a large extent by means of

development of packaged goods in different petite niche areas or else manufacture custom

products for particularly individuals. There are certain small sized corporation that present

alliances with larger business in a bid to promote their wares. Whilst Harvey Norman

competes in this specific segment, it too competes in different other segments as well. In

general, key competitors of the firm Harvey Norman are Woolworths Myer Holdings Ltd as

well as David Jones Limited (Harveynormanholdings.com.au, 2018).

-Ratio Analysis of the company

Based on the results of the ratio analysis of the firm for the period 2013-2017 (refer to table 1

presented in appendix) it is possible to analyse the condition of the financial health of the

firm. The findings of the key ratios are hereby analysed one by one:

Current ratio: The current ratio calculated for the period 2013 to 2017 shows a declining

trend. This shows that the potency of the firm to pay off different short term debts has

declined considerably, reflecting unfavourable financial condition (Drake, et al., 2017). Also,

the current ratio is not even close to the industry standard of 2:1 that means a firm possessing

double assets in comparison to that of liabilities, reflecting greater potency of paying back

debts (Grant, 2016).

9

ACCOUNTING THEORY & CONTEMPORARY ISSUES

2013-06 2014-06 2015-06 2016-06 2017-06

1532 1607 1676 1606

1112

2533 2618 2682 2826 3077

Current Assets-Liabilities

Current Assets Current Liabilities

Quick Ratio: The quick ratio of the firm shows a fluctuating trend during the period during

the specified period of 2013-2017. Nevertheless, the ratio has improved during 2017 in

comparison to the figure registered in the year ago period.

2013-06 2014-06 2015-06 2016-06 2017-06

181 167 212 164 108

1235 1286 1355 1261

749

Quick Ratio

Quick Assets Current Liabilities

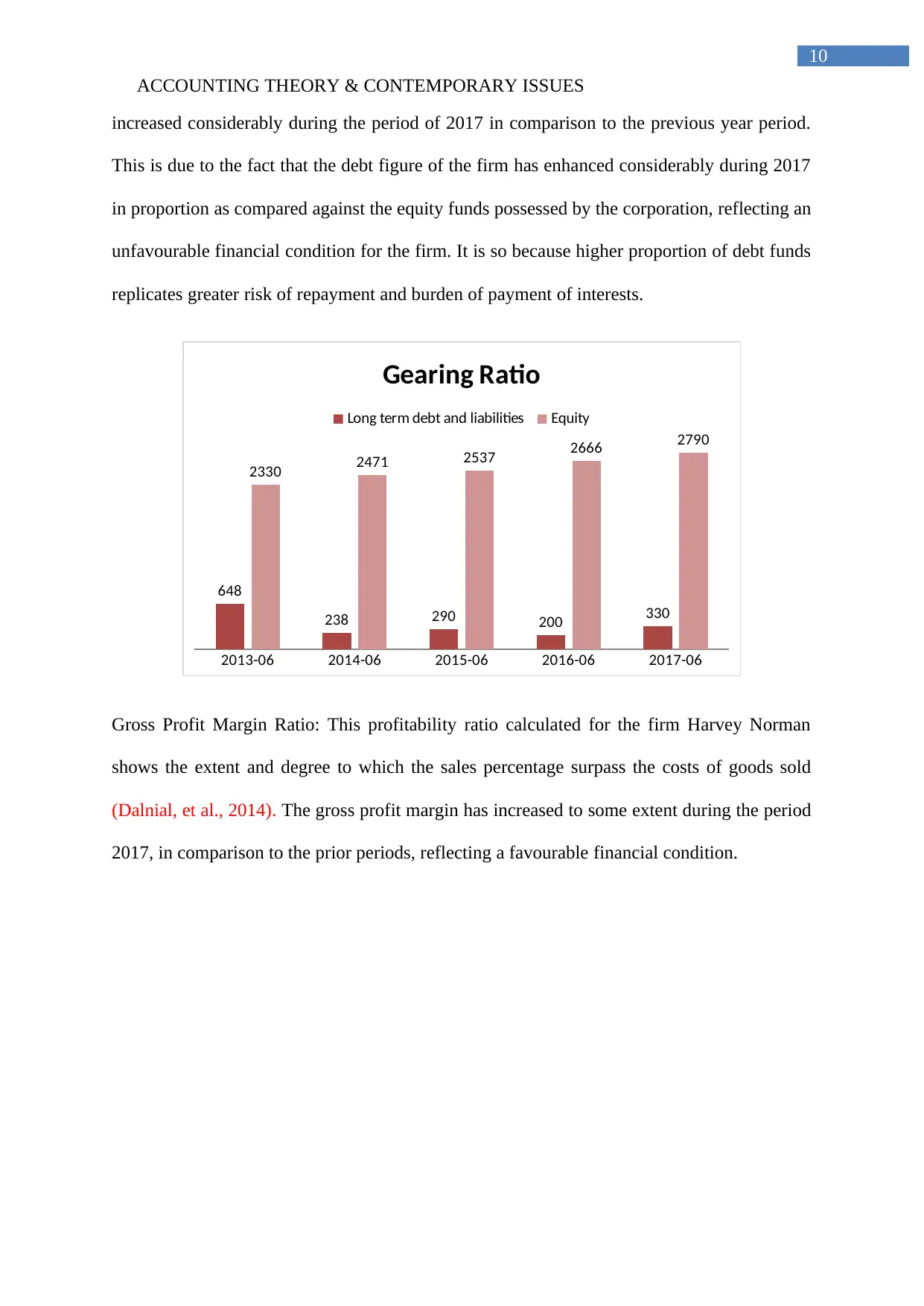

Gearing Ratio: The gearing ratio reflects overall proportion of borrowed wealth in

comparison to equity possessed by the firm (Wahlen, et al., 2014). The gearing ratio also

represents a fluctuating trend throughout the period. However, the same is said to have

ACCOUNTING THEORY & CONTEMPORARY ISSUES

2013-06 2014-06 2015-06 2016-06 2017-06

1532 1607 1676 1606

1112

2533 2618 2682 2826 3077

Current Assets-Liabilities

Current Assets Current Liabilities

Quick Ratio: The quick ratio of the firm shows a fluctuating trend during the period during

the specified period of 2013-2017. Nevertheless, the ratio has improved during 2017 in

comparison to the figure registered in the year ago period.

2013-06 2014-06 2015-06 2016-06 2017-06

181 167 212 164 108

1235 1286 1355 1261

749

Quick Ratio

Quick Assets Current Liabilities

Gearing Ratio: The gearing ratio reflects overall proportion of borrowed wealth in

comparison to equity possessed by the firm (Wahlen, et al., 2014). The gearing ratio also

represents a fluctuating trend throughout the period. However, the same is said to have

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

ACCOUNTING THEORY & CONTEMPORARY ISSUES

increased considerably during the period of 2017 in comparison to the previous year period.

This is due to the fact that the debt figure of the firm has enhanced considerably during 2017

in proportion as compared against the equity funds possessed by the corporation, reflecting an

unfavourable financial condition for the firm. It is so because higher proportion of debt funds

replicates greater risk of repayment and burden of payment of interests.

2013-06 2014-06 2015-06 2016-06 2017-06

648

238 290 200 330

2330 2471 2537 2666 2790

Gearing Ratio

Long term debt and liabilities Equity

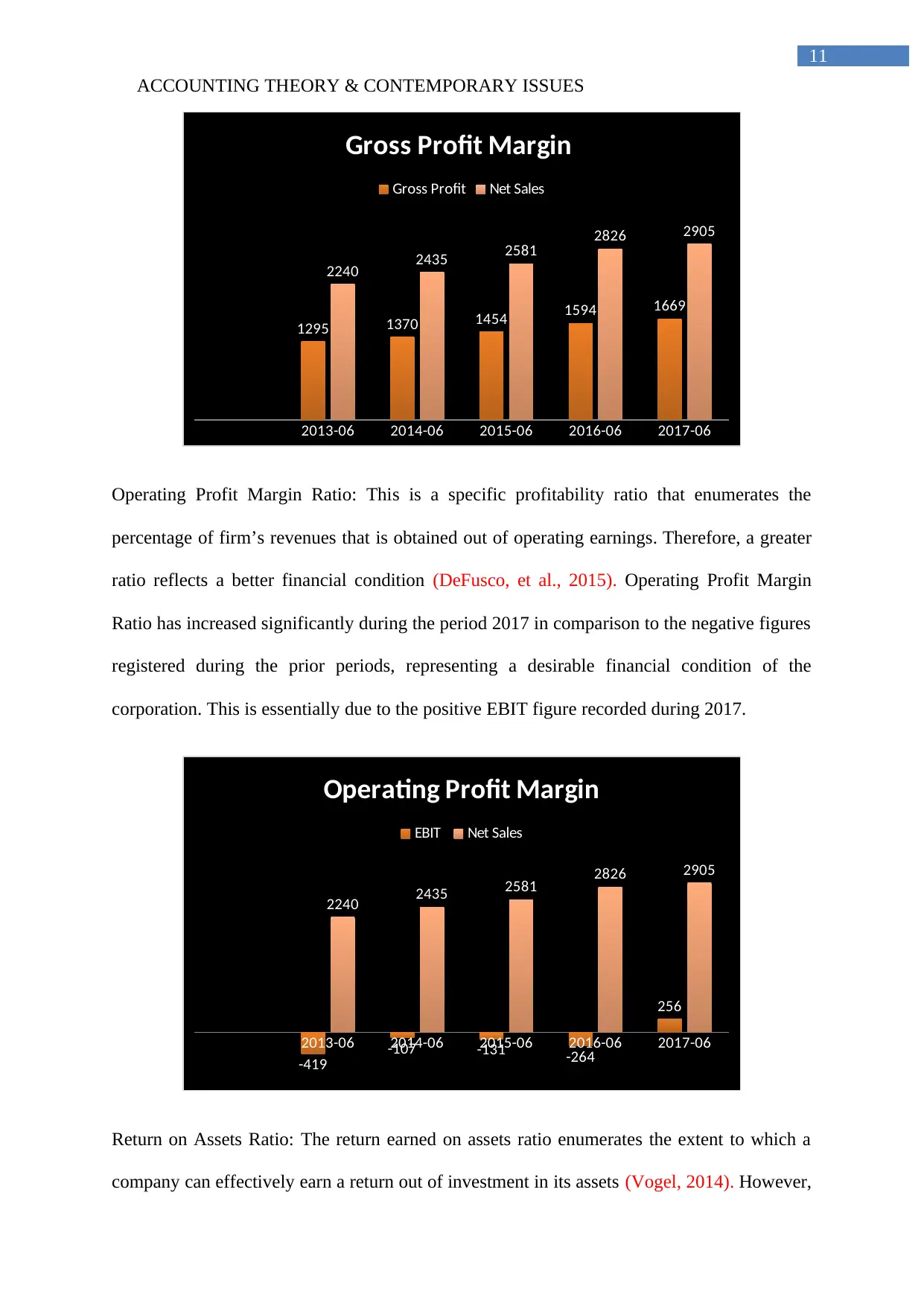

Gross Profit Margin Ratio: This profitability ratio calculated for the firm Harvey Norman

shows the extent and degree to which the sales percentage surpass the costs of goods sold

(Dalnial, et al., 2014). The gross profit margin has increased to some extent during the period

2017, in comparison to the prior periods, reflecting a favourable financial condition.

ACCOUNTING THEORY & CONTEMPORARY ISSUES

increased considerably during the period of 2017 in comparison to the previous year period.

This is due to the fact that the debt figure of the firm has enhanced considerably during 2017

in proportion as compared against the equity funds possessed by the corporation, reflecting an

unfavourable financial condition for the firm. It is so because higher proportion of debt funds

replicates greater risk of repayment and burden of payment of interests.

2013-06 2014-06 2015-06 2016-06 2017-06

648

238 290 200 330

2330 2471 2537 2666 2790

Gearing Ratio

Long term debt and liabilities Equity

Gross Profit Margin Ratio: This profitability ratio calculated for the firm Harvey Norman

shows the extent and degree to which the sales percentage surpass the costs of goods sold

(Dalnial, et al., 2014). The gross profit margin has increased to some extent during the period

2017, in comparison to the prior periods, reflecting a favourable financial condition.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

ACCOUNTING THEORY & CONTEMPORARY ISSUES

2013-06 2014-06 2015-06 2016-06 2017-06

1295 1370 1454 1594 1669

2240 2435 2581 2826 2905

Gross Profit Margin

Gross Profit Net Sales

Operating Profit Margin Ratio: This is a specific profitability ratio that enumerates the

percentage of firm’s revenues that is obtained out of operating earnings. Therefore, a greater

ratio reflects a better financial condition (DeFusco, et al., 2015). Operating Profit Margin

Ratio has increased significantly during the period 2017 in comparison to the negative figures

registered during the prior periods, representing a desirable financial condition of the

corporation. This is essentially due to the positive EBIT figure recorded during 2017.

2013-06 2014-06 2015-06 2016-06 2017-06

-419

-107 -131 -264

256

2240 2435 2581 2826 2905

Operating Profit Margin

EBIT Net Sales

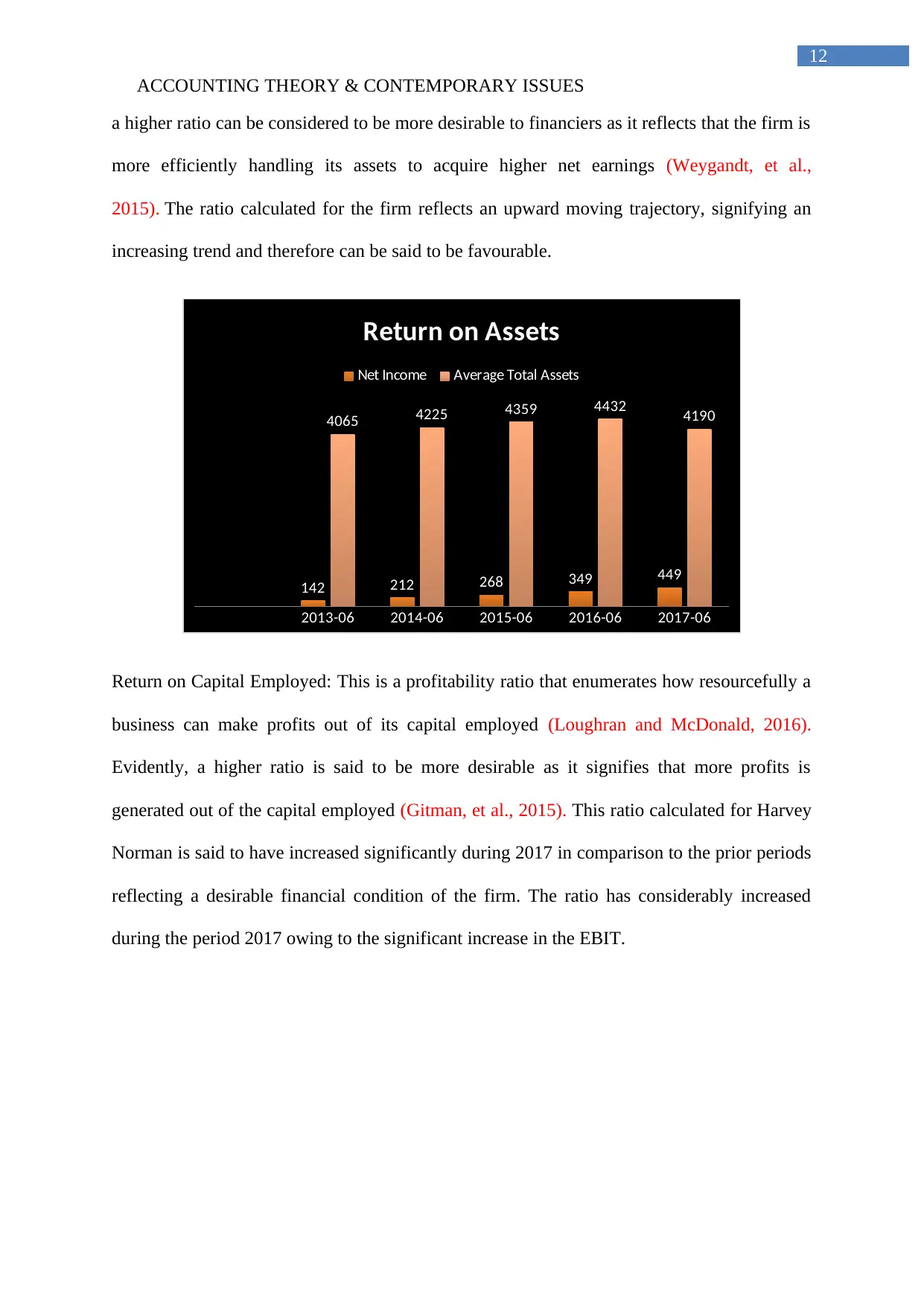

Return on Assets Ratio: The return earned on assets ratio enumerates the extent to which a

company can effectively earn a return out of investment in its assets (Vogel, 2014). However,

ACCOUNTING THEORY & CONTEMPORARY ISSUES

2013-06 2014-06 2015-06 2016-06 2017-06

1295 1370 1454 1594 1669

2240 2435 2581 2826 2905

Gross Profit Margin

Gross Profit Net Sales

Operating Profit Margin Ratio: This is a specific profitability ratio that enumerates the

percentage of firm’s revenues that is obtained out of operating earnings. Therefore, a greater

ratio reflects a better financial condition (DeFusco, et al., 2015). Operating Profit Margin

Ratio has increased significantly during the period 2017 in comparison to the negative figures

registered during the prior periods, representing a desirable financial condition of the

corporation. This is essentially due to the positive EBIT figure recorded during 2017.

2013-06 2014-06 2015-06 2016-06 2017-06

-419

-107 -131 -264

256

2240 2435 2581 2826 2905

Operating Profit Margin

EBIT Net Sales

Return on Assets Ratio: The return earned on assets ratio enumerates the extent to which a

company can effectively earn a return out of investment in its assets (Vogel, 2014). However,

12

ACCOUNTING THEORY & CONTEMPORARY ISSUES

a higher ratio can be considered to be more desirable to financiers as it reflects that the firm is

more efficiently handling its assets to acquire higher net earnings (Weygandt, et al.,

2015). The ratio calculated for the firm reflects an upward moving trajectory, signifying an

increasing trend and therefore can be said to be favourable.

2013-06 2014-06 2015-06 2016-06 2017-06

142 212 268 349 449

4065 4225 4359 4432 4190

Return on Assets

Net Income Average Total Assets

Return on Capital Employed: This is a profitability ratio that enumerates how resourcefully a

business can make profits out of its capital employed (Loughran and McDonald, 2016).

Evidently, a higher ratio is said to be more desirable as it signifies that more profits is

generated out of the capital employed (Gitman, et al., 2015). This ratio calculated for Harvey

Norman is said to have increased significantly during 2017 in comparison to the prior periods

reflecting a desirable financial condition of the firm. The ratio has considerably increased

during the period 2017 owing to the significant increase in the EBIT.

ACCOUNTING THEORY & CONTEMPORARY ISSUES

a higher ratio can be considered to be more desirable to financiers as it reflects that the firm is

more efficiently handling its assets to acquire higher net earnings (Weygandt, et al.,

2015). The ratio calculated for the firm reflects an upward moving trajectory, signifying an

increasing trend and therefore can be said to be favourable.

2013-06 2014-06 2015-06 2016-06 2017-06

142 212 268 349 449

4065 4225 4359 4432 4190

Return on Assets

Net Income Average Total Assets

Return on Capital Employed: This is a profitability ratio that enumerates how resourcefully a

business can make profits out of its capital employed (Loughran and McDonald, 2016).

Evidently, a higher ratio is said to be more desirable as it signifies that more profits is

generated out of the capital employed (Gitman, et al., 2015). This ratio calculated for Harvey

Norman is said to have increased significantly during 2017 in comparison to the prior periods

reflecting a desirable financial condition of the firm. The ratio has considerably increased

during the period 2017 owing to the significant increase in the EBIT.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.