Financial Statement Analysis Assignment - [University Name]

VerifiedAdded on 2022/12/23

|12

|2031

|1

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial statement analysis assignment, covering a range of topics from calculating Compound Annual Growth Rate (CAGR) and analyzing dividend payout ratios to determining the quality of earnings and computing goodwill. The assignment delves into various financial concepts, including the Gordon Dividend Model, Weighted Average Cost of Capital (WACC), and different inventory valuation methods like LIFO, FIFO, and weighted average. It also includes the construction of a cash flow statement and the analysis of earnings per share (EPS). The solution provides detailed explanations and calculations for each question, offering a thorough understanding of financial statement analysis. Furthermore, the assignment explores topics like terminal value and the impact of stock splits on share prices.

FINANCIAL STATEMENT ANALYSIS

STUDENT iD:

[Pick the date]

STUDENT iD:

[Pick the date]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

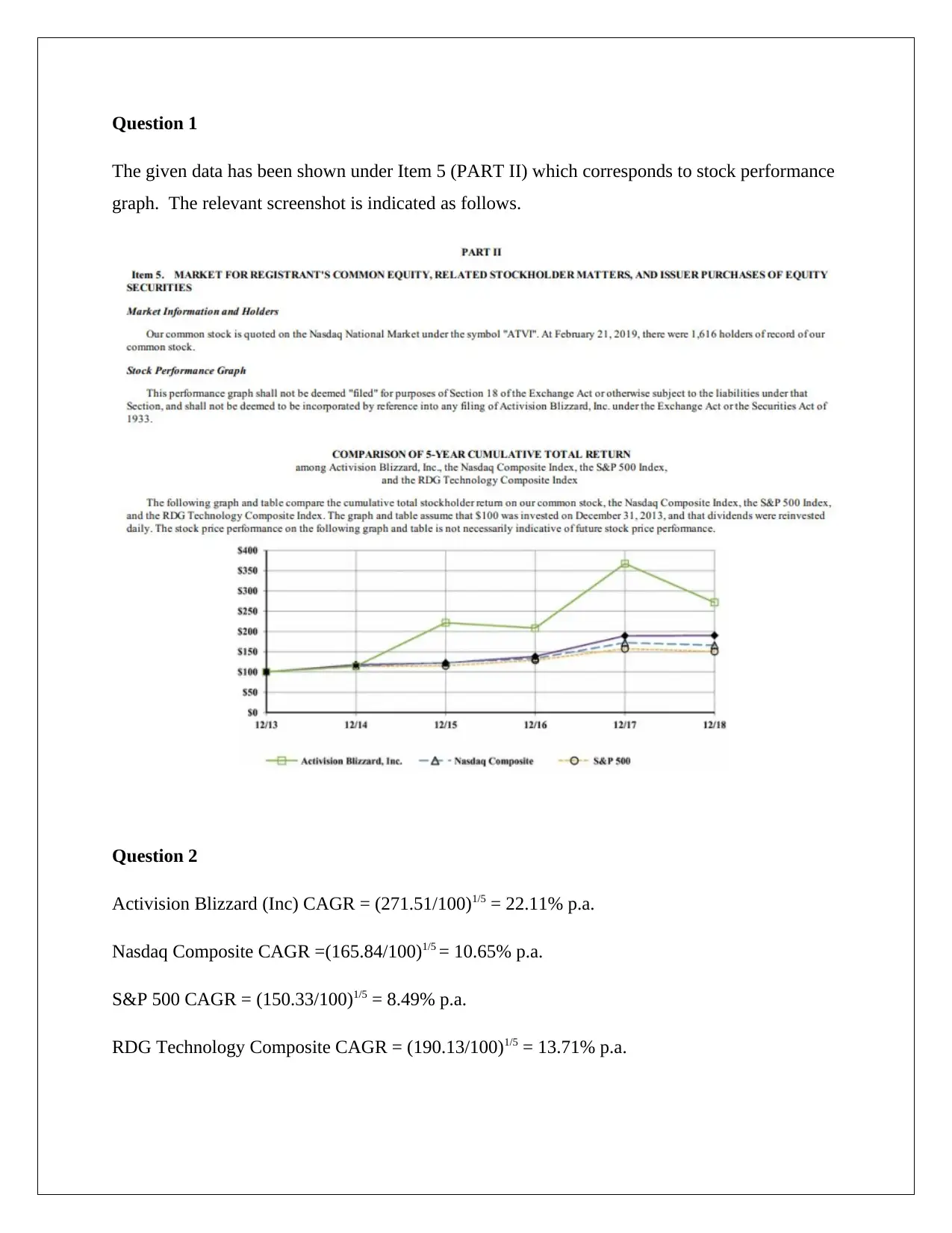

Question 1

The given data has been shown under Item 5 (PART II) which corresponds to stock performance

graph. The relevant screenshot is indicated as follows.

Question 2

Activision Blizzard (Inc) CAGR = (271.51/100)1/5 = 22.11% p.a.

Nasdaq Composite CAGR =(165.84/100)1/5 = 10.65% p.a.

S&P 500 CAGR = (150.33/100)1/5 = 8.49% p.a.

RDG Technology Composite CAGR = (190.13/100)1/5 = 13.71% p.a.

The given data has been shown under Item 5 (PART II) which corresponds to stock performance

graph. The relevant screenshot is indicated as follows.

Question 2

Activision Blizzard (Inc) CAGR = (271.51/100)1/5 = 22.11% p.a.

Nasdaq Composite CAGR =(165.84/100)1/5 = 10.65% p.a.

S&P 500 CAGR = (150.33/100)1/5 = 8.49% p.a.

RDG Technology Composite CAGR = (190.13/100)1/5 = 13.71% p.a.

Question 3

a) Topline growth in 2018 = [(7500-7017)/7017]*100 = 6.88% p.a.

b) Dividend Payout ratio (2018) = (0.34/2.38)*100 = 14.29%

c) Quality of earnings ratio = Operating cash flows/Net Income

High quality earnings are observed for 2014, 2015, 2016 & 2017 since the quality of earnings

ratio exceeds 1. However, low quality earnings are observed for 2018 since the quality of

earnings ratio is lesser than 1.

d) Trailing PE = 44/Earnings per share for 2018 = 44/2.38 = 18.49

e) The given data would be found under selected financial data of PART II (Item 6).

Question 4

The following equation can be used to compute the missing data for the two companies as on

January 1, 2018.

Assets = Liabilities + common stock + additional paid-in capital + retained earnings

The following computation is for LifeZone Corp.

2900 = 1275 + 150 + additional paid-in capital + 1,150

Solving the above, additional paid-in capital for LifeZone as on January 1, 2018 = $ 325 million

The following computation is for BridgeLine LTD

2850 = 950 + 200 + 225 + Retained earnings

Solving the above, additional paid-in capital for BridgeLIne as on January 1, 2018 = $1,475

million

a) Topline growth in 2018 = [(7500-7017)/7017]*100 = 6.88% p.a.

b) Dividend Payout ratio (2018) = (0.34/2.38)*100 = 14.29%

c) Quality of earnings ratio = Operating cash flows/Net Income

High quality earnings are observed for 2014, 2015, 2016 & 2017 since the quality of earnings

ratio exceeds 1. However, low quality earnings are observed for 2018 since the quality of

earnings ratio is lesser than 1.

d) Trailing PE = 44/Earnings per share for 2018 = 44/2.38 = 18.49

e) The given data would be found under selected financial data of PART II (Item 6).

Question 4

The following equation can be used to compute the missing data for the two companies as on

January 1, 2018.

Assets = Liabilities + common stock + additional paid-in capital + retained earnings

The following computation is for LifeZone Corp.

2900 = 1275 + 150 + additional paid-in capital + 1,150

Solving the above, additional paid-in capital for LifeZone as on January 1, 2018 = $ 325 million

The following computation is for BridgeLine LTD

2850 = 950 + 200 + 225 + Retained earnings

Solving the above, additional paid-in capital for BridgeLIne as on January 1, 2018 = $1,475

million

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Market value of shares issued to acquire BridgeLIne = $ 4.8 billion

Total asset value for BridgeLIne = $ 2.85 billion

Goodwill = ($4.8 -$2.85) billion = $ 1.95 billion

Question 5

It is noteworthy that the book values for the Target Company is equal to the fair value.

Amount paid for a 60% stake in Target company = $ 180 million

Net assets of the company = $ 18 million

60% of the net assets would equal (60/100)*18 million = $ 10.8 million

Hence, goodwill = $ 180 million - $ 10.8 million = $169.2 million

Also, minority interest = (60/100)*18 million = $ 10.8 million

Question 6

Basic earnings per share = (Net income – Dividends to preferred shareholders)/weighted average

common shares outstanding

Basic earnings per share for Federal Corporation (2018) = (27908-3888)/4,200 = $5.72

Diluted earnings per share = (Net income – Dividends to preferred shareholders)/weighted

average dilutive shares

Diluted earnings per share for Federal Corporation (2018) = (27908-3888)/4,620 = $5.20

Question 7

a) GMB’s average borrowing rate = 5%/(1-0.33)= 7.46% p.a.

Total asset value for BridgeLIne = $ 2.85 billion

Goodwill = ($4.8 -$2.85) billion = $ 1.95 billion

Question 5

It is noteworthy that the book values for the Target Company is equal to the fair value.

Amount paid for a 60% stake in Target company = $ 180 million

Net assets of the company = $ 18 million

60% of the net assets would equal (60/100)*18 million = $ 10.8 million

Hence, goodwill = $ 180 million - $ 10.8 million = $169.2 million

Also, minority interest = (60/100)*18 million = $ 10.8 million

Question 6

Basic earnings per share = (Net income – Dividends to preferred shareholders)/weighted average

common shares outstanding

Basic earnings per share for Federal Corporation (2018) = (27908-3888)/4,200 = $5.72

Diluted earnings per share = (Net income – Dividends to preferred shareholders)/weighted

average dilutive shares

Diluted earnings per share for Federal Corporation (2018) = (27908-3888)/4,620 = $5.20

Question 7

a) GMB’s average borrowing rate = 5%/(1-0.33)= 7.46% p.a.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

b) Market value of equity shares = 4.8 million *42 = $201.6 million

Market value of debt = $ 350 million

Weight of equity = (201.6/(201.6+350)) = 0.3655

Weight of debt = (350/(201.6+350)) = 0.6345

Cost of equity = 9.5% p.a.

Cost of debt (post tax) = 5% p.a.

Hence, weighted average cost of capital for the company = 0.3655* 9.5% + 0.6345*5% = 6.64%

p.a.

c) Cost of equity inferred = (2.8/42) *100 = 6.67% p.a.

d) Let the growth rate in dividend be g. The appropriate approach to be deployed is Gordon

Dividend Model.

Current Stock Price = Next year dividend/ (Cost of equity – Dividend growth rate)

Hence, 42 = 3.2/ (0.095-g)

Solving the above, we get g = 1.88% p.a.

Question 8

The effective tax rate for the company is given as 18%. Let the income before income tax

expense in 2016 be $ X

Then, income tax expense = 0.18X

Hence, $2,388 million = 0.18X

Solving the above, X = 13,266.67 million

Market value of debt = $ 350 million

Weight of equity = (201.6/(201.6+350)) = 0.3655

Weight of debt = (350/(201.6+350)) = 0.6345

Cost of equity = 9.5% p.a.

Cost of debt (post tax) = 5% p.a.

Hence, weighted average cost of capital for the company = 0.3655* 9.5% + 0.6345*5% = 6.64%

p.a.

c) Cost of equity inferred = (2.8/42) *100 = 6.67% p.a.

d) Let the growth rate in dividend be g. The appropriate approach to be deployed is Gordon

Dividend Model.

Current Stock Price = Next year dividend/ (Cost of equity – Dividend growth rate)

Hence, 42 = 3.2/ (0.095-g)

Solving the above, we get g = 1.88% p.a.

Question 8

The effective tax rate for the company is given as 18%. Let the income before income tax

expense in 2016 be $ X

Then, income tax expense = 0.18X

Hence, $2,388 million = 0.18X

Solving the above, X = 13,266.67 million

Question 9

Dividends payable annually to preferred stockholders = 0.09*32*21000 = $ 60,480

Since the preferred shares are cumulative in nature, hence the dividends pending for a given year

would be paid in the future. Till the time this payment is not made, no dividend can be given to

common shareholders.

For 2010, no dividend is paid to either the preferred shareholders or the common shareholders.

For 2011, the entire amount of $ 23,000 would be paid to the preferred shareholders as there is

accrued payment of $ 60,480 to be made besides the current year dividend to preferred

shareholders.

Dividend per preferred share in 2011 = (23000/21000) = $ 1.1

No dividend would be paid to common shareholders.

For 2012 also, the entire amount of $ 19,000 would be paid to the preferred shareholders as there

is accrued payment of (60,480+60,480-23,000) or $ 97,960 payable to the preferred

shareholders.

Dividend per preferred share in 2012 = (19000/21000) = $ 1.1

No dividend would be paid to common shareholders.

For 2013 also, the entire amount of $ 88,000 would be paid to the preferred shareholders as there

is accrued payment of (60,480+60,480 +60,480-23,000-19,000) or $ 139,440 payable to the

preferred shareholders.

Dividend per preferred share in 2013 = (88000/21000) = $ 4.19

No dividend would be paid to common shareholders.

Pending dividend payable from previous years to preferred shareholders in 2014 = ($139,440+

$60,480- $88,000) =$ 111,920

Dividends payable annually to preferred stockholders = 0.09*32*21000 = $ 60,480

Since the preferred shares are cumulative in nature, hence the dividends pending for a given year

would be paid in the future. Till the time this payment is not made, no dividend can be given to

common shareholders.

For 2010, no dividend is paid to either the preferred shareholders or the common shareholders.

For 2011, the entire amount of $ 23,000 would be paid to the preferred shareholders as there is

accrued payment of $ 60,480 to be made besides the current year dividend to preferred

shareholders.

Dividend per preferred share in 2011 = (23000/21000) = $ 1.1

No dividend would be paid to common shareholders.

For 2012 also, the entire amount of $ 19,000 would be paid to the preferred shareholders as there

is accrued payment of (60,480+60,480-23,000) or $ 97,960 payable to the preferred

shareholders.

Dividend per preferred share in 2012 = (19000/21000) = $ 1.1

No dividend would be paid to common shareholders.

For 2013 also, the entire amount of $ 88,000 would be paid to the preferred shareholders as there

is accrued payment of (60,480+60,480 +60,480-23,000-19,000) or $ 139,440 payable to the

preferred shareholders.

Dividend per preferred share in 2013 = (88000/21000) = $ 4.19

No dividend would be paid to common shareholders.

Pending dividend payable from previous years to preferred shareholders in 2014 = ($139,440+

$60,480- $88,000) =$ 111,920

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

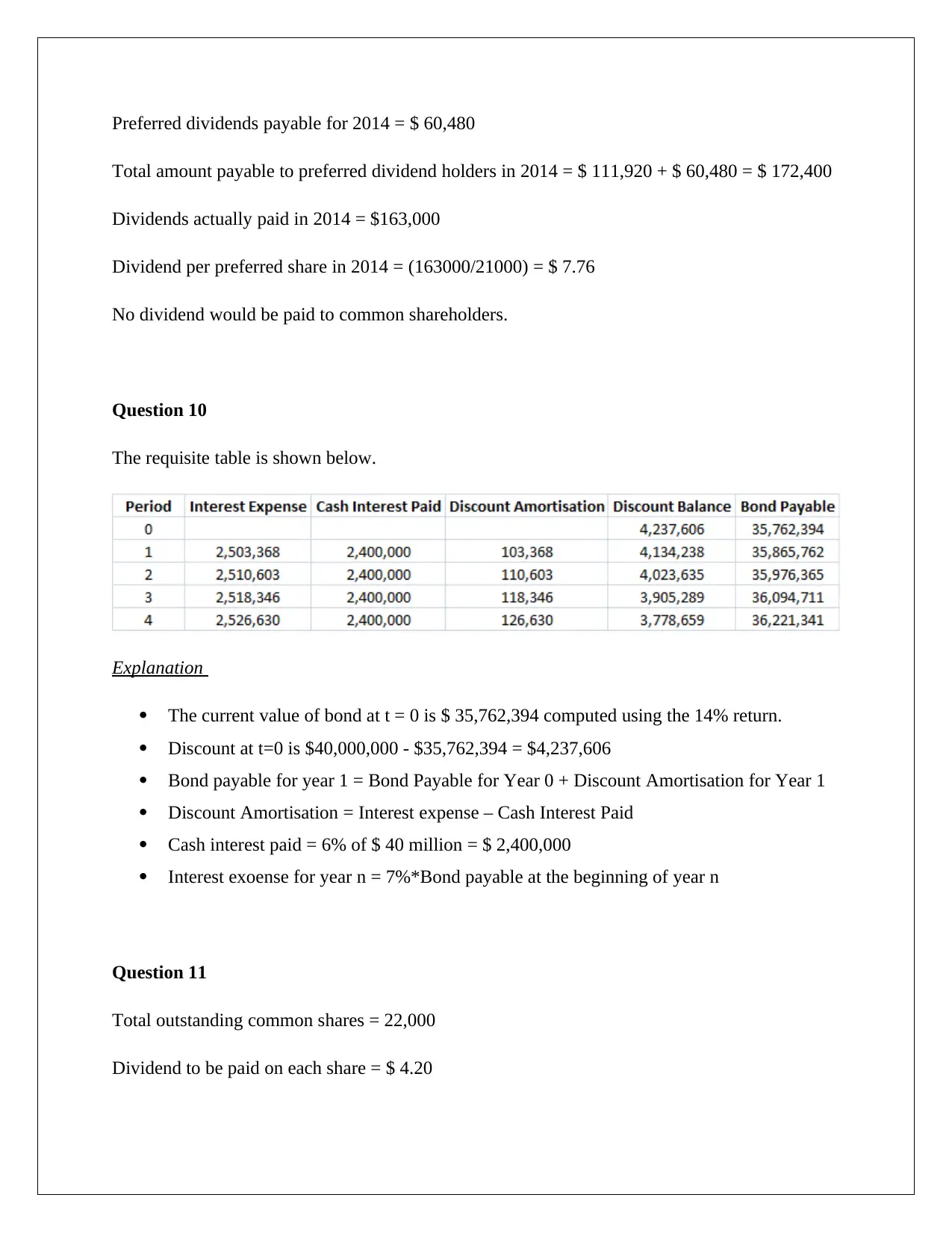

Preferred dividends payable for 2014 = $ 60,480

Total amount payable to preferred dividend holders in 2014 = $ 111,920 + $ 60,480 = $ 172,400

Dividends actually paid in 2014 = $163,000

Dividend per preferred share in 2014 = (163000/21000) = $ 7.76

No dividend would be paid to common shareholders.

Question 10

The requisite table is shown below.

Explanation

The current value of bond at t = 0 is $ 35,762,394 computed using the 14% return.

Discount at t=0 is $40,000,000 - $35,762,394 = $4,237,606

Bond payable for year 1 = Bond Payable for Year 0 + Discount Amortisation for Year 1

Discount Amortisation = Interest expense – Cash Interest Paid

Cash interest paid = 6% of $ 40 million = $ 2,400,000

Interest exoense for year n = 7%*Bond payable at the beginning of year n

Question 11

Total outstanding common shares = 22,000

Dividend to be paid on each share = $ 4.20

Total amount payable to preferred dividend holders in 2014 = $ 111,920 + $ 60,480 = $ 172,400

Dividends actually paid in 2014 = $163,000

Dividend per preferred share in 2014 = (163000/21000) = $ 7.76

No dividend would be paid to common shareholders.

Question 10

The requisite table is shown below.

Explanation

The current value of bond at t = 0 is $ 35,762,394 computed using the 14% return.

Discount at t=0 is $40,000,000 - $35,762,394 = $4,237,606

Bond payable for year 1 = Bond Payable for Year 0 + Discount Amortisation for Year 1

Discount Amortisation = Interest expense – Cash Interest Paid

Cash interest paid = 6% of $ 40 million = $ 2,400,000

Interest exoense for year n = 7%*Bond payable at the beginning of year n

Question 11

Total outstanding common shares = 22,000

Dividend to be paid on each share = $ 4.20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Hence, total dividend size required = 22,000*4.20 = $ 92,400

Question 12

Income reported by the company for 2018 = Basic earnings per share * weighted average basic

shares outstanding = 2.84*5,098 million = $14,478.32 million

Question 13

a) Number of shares issued at May 31, 2018 = 175,000 – 15,000 = 160,000

b) Average issue price of shares = (85,500+680,000)/175,000 = $4.37

c) Average cost of purchase of treasury shares = (160,000/15000) = $10.67

Question 14

a) A 4 for 1 stock split would indicate that 1 stock would be split into 4 stocks and hence for

each stock that the current shareholder has, the shareholder would get this split into 4 shares.

b) Companies such as North Forest would opt for stock split so as to increase bettr price

realization and higher liquidity in trading of shares. As evident, the price before split is $ 412

which is very large owing to which only limited share trading would be done. Through

splitting of the stock, the price of each stock would become significantly lower and would

result in greater participation from shareholders.

c) Shares outstanding when split was announced = (26.6million/4) = 6.65 million

Question 15

Beginning balance of equity investment = $ 12 million

Net amount for the shareholders of Glasgow = Net income- Dividends = $1,800,000 - $400,000

= $ 1.4 million

Question 12

Income reported by the company for 2018 = Basic earnings per share * weighted average basic

shares outstanding = 2.84*5,098 million = $14,478.32 million

Question 13

a) Number of shares issued at May 31, 2018 = 175,000 – 15,000 = 160,000

b) Average issue price of shares = (85,500+680,000)/175,000 = $4.37

c) Average cost of purchase of treasury shares = (160,000/15000) = $10.67

Question 14

a) A 4 for 1 stock split would indicate that 1 stock would be split into 4 stocks and hence for

each stock that the current shareholder has, the shareholder would get this split into 4 shares.

b) Companies such as North Forest would opt for stock split so as to increase bettr price

realization and higher liquidity in trading of shares. As evident, the price before split is $ 412

which is very large owing to which only limited share trading would be done. Through

splitting of the stock, the price of each stock would become significantly lower and would

result in greater participation from shareholders.

c) Shares outstanding when split was announced = (26.6million/4) = 6.65 million

Question 15

Beginning balance of equity investment = $ 12 million

Net amount for the shareholders of Glasgow = Net income- Dividends = $1,800,000 - $400,000

= $ 1.4 million

Since the stake in Glasgow is 42%, hence amount attributed to Hopkins Corporation =

(42/100)*1.4 million = $ 0.59 million

Hence, closing balance of equity investment = $ 12 million + $ 0.59 million = $ 12.59 million

Question 16

Amount of interest accrued = 200,000*(8/36500)*15 = $ 657.53

Question 17

Periodic interest payment = $300,000*(8%/2) = $ 12,000 every six months

Question 18

Let the retained earnings for Ranbaxy as on December 31, 2013 be $ X

Retained earnings change during 2014 = Net income for 2014 – Cash dividends for 2014 =

$90,050 - $39,600 = $ 50,450

Retained earnings for Ranbaxy as on December 31, 2014 is $308,002

X + $50,450 = $308,002

Solving the above, X = $257,552

Question 19

Total units bought = 6,400

Total units sold = 6,000

Ending inventory = 6,400 – 6,000 = 400 units

(42/100)*1.4 million = $ 0.59 million

Hence, closing balance of equity investment = $ 12 million + $ 0.59 million = $ 12.59 million

Question 16

Amount of interest accrued = 200,000*(8/36500)*15 = $ 657.53

Question 17

Periodic interest payment = $300,000*(8%/2) = $ 12,000 every six months

Question 18

Let the retained earnings for Ranbaxy as on December 31, 2013 be $ X

Retained earnings change during 2014 = Net income for 2014 – Cash dividends for 2014 =

$90,050 - $39,600 = $ 50,450

Retained earnings for Ranbaxy as on December 31, 2014 is $308,002

X + $50,450 = $308,002

Solving the above, X = $257,552

Question 19

Total units bought = 6,400

Total units sold = 6,000

Ending inventory = 6,400 – 6,000 = 400 units

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

LIFO Method

Total sales = 6000*60 = $ 360,000

Ending inventory = 400*38 = $ 15,200

Cost of goods sold =$260,800 - $ 15,200 = $ 245,600

Gross profit = Total sales – Cost ofgoods sold = $360,000 - $245,600 = $ 114,400

Gross margin = (Gross profit/Total Sales)*100 = (114400/360000)*100 = 31.78%

FIFO Method

Total sales = 6000*60 = $ 360,000

Ending inventory = 400*44 = $ 17,600

Cost of goods sold =$260,800 - $ 17,600 = $ 243,200

Gross profit = Total sales – Cost ofgoods sold = $360,000 - $243,200 = $ 116,800

Gross margin = (Gross profit/Total Sales)*100 = (116800/360000)*100 = 32.44%

Weighted Average Method

Total sales = 6000*60 = $ 360,000

Ending inventory = 400*(260,800/6,400) = $ 16,300

Cost of goods sold =$260,800 - $ 16,300 = $ 244,500

Gross profit = Total sales – Cost ofgoods sold = $360,000 - $244,500 = $ 115,500

Gross margin = (Gross profit/Total Sales)*100 = (115500/360000)*100 = 32.08%

Question 20

Total sales = 6000*60 = $ 360,000

Ending inventory = 400*38 = $ 15,200

Cost of goods sold =$260,800 - $ 15,200 = $ 245,600

Gross profit = Total sales – Cost ofgoods sold = $360,000 - $245,600 = $ 114,400

Gross margin = (Gross profit/Total Sales)*100 = (114400/360000)*100 = 31.78%

FIFO Method

Total sales = 6000*60 = $ 360,000

Ending inventory = 400*44 = $ 17,600

Cost of goods sold =$260,800 - $ 17,600 = $ 243,200

Gross profit = Total sales – Cost ofgoods sold = $360,000 - $243,200 = $ 116,800

Gross margin = (Gross profit/Total Sales)*100 = (116800/360000)*100 = 32.44%

Weighted Average Method

Total sales = 6000*60 = $ 360,000

Ending inventory = 400*(260,800/6,400) = $ 16,300

Cost of goods sold =$260,800 - $ 16,300 = $ 244,500

Gross profit = Total sales – Cost ofgoods sold = $360,000 - $244,500 = $ 115,500

Gross margin = (Gross profit/Total Sales)*100 = (115500/360000)*100 = 32.08%

Question 20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Terminal value refers to the cumulative value of the cash flows associated with the firm orproject

considering a particular growth rate and given cost of capital. Typically, some form of Gordon

dividend model is used for the computation of terminal value which is then discounted to convert

into present value terms. The terminal value of the business is determined for all the years after a

given year n and reflects the value of the future cash flows associated with the business or

project at time period n only.

Question 21

The topline growth assumptions for the next 10 years can be worked out as follows.

Assumed growth rate of the industry in which the company operates

Assumed growth rate of economy in the primary market of operation for the company

Determine whether the company would have topline growth in excess of the peers or not.

Determine if the company is planning to pursue any opportunities for any acquisition and

the tentative size of the same.

Determine if the company plans to diversify geographically or through product lines

Question 22

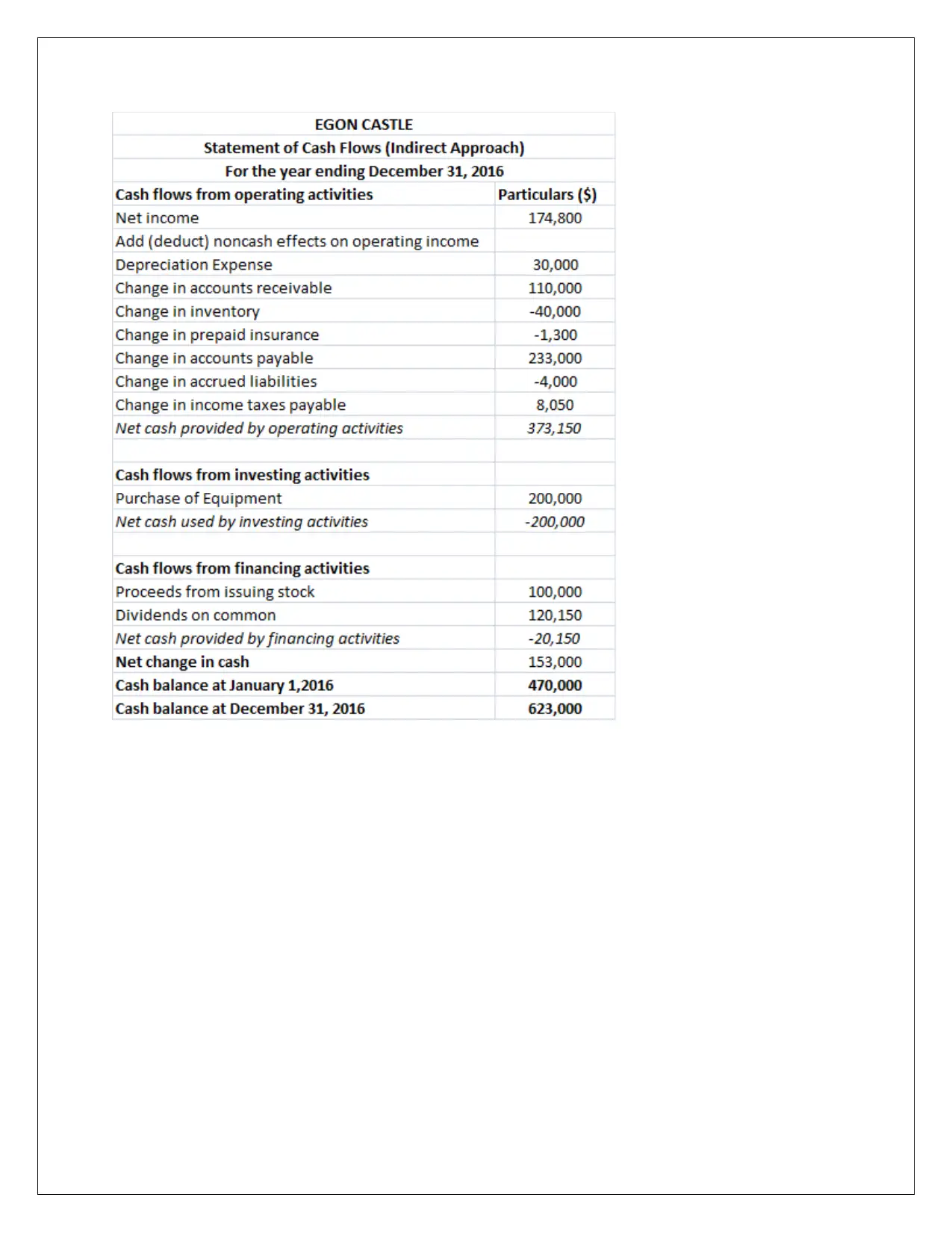

The requisite cash flow statement for the company is shown below.

considering a particular growth rate and given cost of capital. Typically, some form of Gordon

dividend model is used for the computation of terminal value which is then discounted to convert

into present value terms. The terminal value of the business is determined for all the years after a

given year n and reflects the value of the future cash flows associated with the business or

project at time period n only.

Question 21

The topline growth assumptions for the next 10 years can be worked out as follows.

Assumed growth rate of the industry in which the company operates

Assumed growth rate of economy in the primary market of operation for the company

Determine whether the company would have topline growth in excess of the peers or not.

Determine if the company is planning to pursue any opportunities for any acquisition and

the tentative size of the same.

Determine if the company plans to diversify geographically or through product lines

Question 22

The requisite cash flow statement for the company is shown below.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.