Financial Statement Analysis of JB Hi-Fi Limited

VerifiedAdded on 2023/04/21

|13

|3289

|429

AI Summary

This report contains detailed analysis of financial statement of JB Hi-Fi Limited. JB Hi-Fi is a large Australian consumer goods retailer operating through numerous retail outlets and through online platform. They have been performing well since its imitation and as compared to their competitors. In this report, their financial and operational performance of JB Hi-Fi Limited is analysed based on the information available in their 2014 annual report. Lastly, the paper concludes with outlining some key success factors for their financial and operational Excellencies.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL STATEMENT ANALYSIS OF JB HIFI LIMITED

Financial Statement Analysis of JB Hi-Fi Limited

Name of the Student:

Name of the University:

Author’s Note:

Financial Statement Analysis of JB Hi-Fi Limited

Name of the Student:

Name of the University:

Author’s Note:

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

Executive Summary:

This report contains detailed analysis of financial statement of JB Hi-Fi Limited. JB Hi-Fi is a

large Australian consumer goods retailer operating through numerous retail outlets and through

online platform. They have been performing well since its imitation and as compared to their

competitors. In this report, their financial and operational performance of JB Hi-Fi Limited is

analysed based on the information available in their 2014 annual report. Lastly, the paper

concludes with outlining some key success factors for their financial and operational

Excellencies.

Executive Summary:

This report contains detailed analysis of financial statement of JB Hi-Fi Limited. JB Hi-Fi is a

large Australian consumer goods retailer operating through numerous retail outlets and through

online platform. They have been performing well since its imitation and as compared to their

competitors. In this report, their financial and operational performance of JB Hi-Fi Limited is

analysed based on the information available in their 2014 annual report. Lastly, the paper

concludes with outlining some key success factors for their financial and operational

Excellencies.

2FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

Table of Contents

Introduction:....................................................................................................................................4

Part A:..............................................................................................................................................4

1. Financial performance and financial position parameters based on 2014 Annual report of JB

Hi-Fi:............................................................................................................................................4

2. Normal balance of above accounts and effects for decrease in balance:.................................5

Part B:..............................................................................................................................................7

1. Different types of revenues generated by consolidated group of JB Hi-Fi:............................7

2. Assets classification of JB Hi-Fi:............................................................................................7

3. Categories of JB Hi-Fi group’s equity and number of ordinary shares:..................................8

4. Current Liability for dividends and dividend calculations:.....................................................8

5. Comparison of dividend per share with earnings per share:....................................................9

Part C:............................................................................................................................................10

Requirement 1:...........................................................................................................................10

Requirement 2:...........................................................................................................................11

Conclusion:....................................................................................................................................11

Bibliography:.................................................................................................................................12

Table of Contents

Introduction:....................................................................................................................................4

Part A:..............................................................................................................................................4

1. Financial performance and financial position parameters based on 2014 Annual report of JB

Hi-Fi:............................................................................................................................................4

2. Normal balance of above accounts and effects for decrease in balance:.................................5

Part B:..............................................................................................................................................7

1. Different types of revenues generated by consolidated group of JB Hi-Fi:............................7

2. Assets classification of JB Hi-Fi:............................................................................................7

3. Categories of JB Hi-Fi group’s equity and number of ordinary shares:..................................8

4. Current Liability for dividends and dividend calculations:.....................................................8

5. Comparison of dividend per share with earnings per share:....................................................9

Part C:............................................................................................................................................10

Requirement 1:...........................................................................................................................10

Requirement 2:...........................................................................................................................11

Conclusion:....................................................................................................................................11

Bibliography:.................................................................................................................................12

3FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

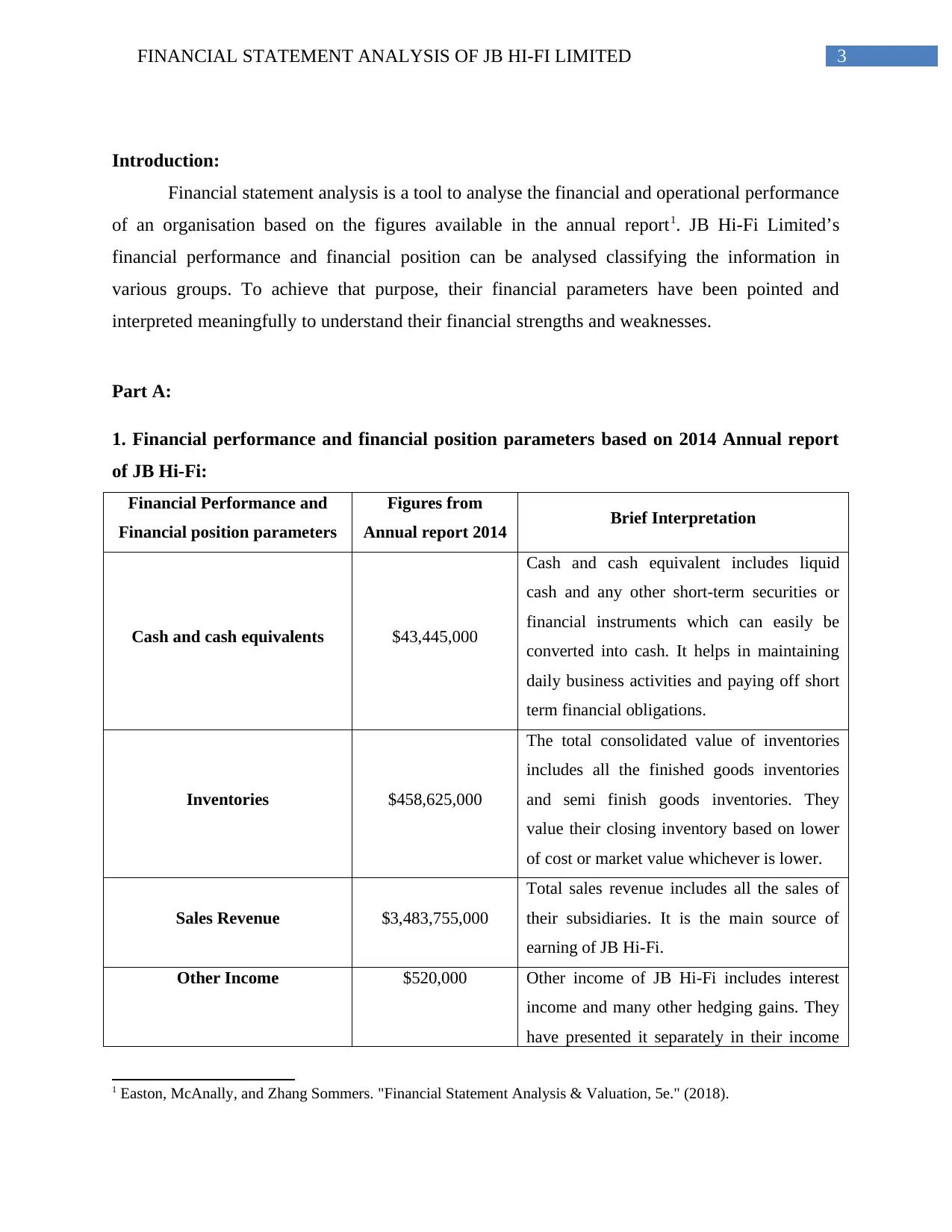

Introduction:

Financial statement analysis is a tool to analyse the financial and operational performance

of an organisation based on the figures available in the annual report1. JB Hi-Fi Limited’s

financial performance and financial position can be analysed classifying the information in

various groups. To achieve that purpose, their financial parameters have been pointed and

interpreted meaningfully to understand their financial strengths and weaknesses.

Part A:

1. Financial performance and financial position parameters based on 2014 Annual report

of JB Hi-Fi:

Financial Performance and

Financial position parameters

Figures from

Annual report 2014 Brief Interpretation

Cash and cash equivalents $43,445,000

Cash and cash equivalent includes liquid

cash and any other short-term securities or

financial instruments which can easily be

converted into cash. It helps in maintaining

daily business activities and paying off short

term financial obligations.

Inventories $458,625,000

The total consolidated value of inventories

includes all the finished goods inventories

and semi finish goods inventories. They

value their closing inventory based on lower

of cost or market value whichever is lower.

Sales Revenue $3,483,755,000

Total sales revenue includes all the sales of

their subsidiaries. It is the main source of

earning of JB Hi-Fi.

Other Income $520,000 Other income of JB Hi-Fi includes interest

income and many other hedging gains. They

have presented it separately in their income

1 Easton, McAnally, and Zhang Sommers. "Financial Statement Analysis & Valuation, 5e." (2018).

Introduction:

Financial statement analysis is a tool to analyse the financial and operational performance

of an organisation based on the figures available in the annual report1. JB Hi-Fi Limited’s

financial performance and financial position can be analysed classifying the information in

various groups. To achieve that purpose, their financial parameters have been pointed and

interpreted meaningfully to understand their financial strengths and weaknesses.

Part A:

1. Financial performance and financial position parameters based on 2014 Annual report

of JB Hi-Fi:

Financial Performance and

Financial position parameters

Figures from

Annual report 2014 Brief Interpretation

Cash and cash equivalents $43,445,000

Cash and cash equivalent includes liquid

cash and any other short-term securities or

financial instruments which can easily be

converted into cash. It helps in maintaining

daily business activities and paying off short

term financial obligations.

Inventories $458,625,000

The total consolidated value of inventories

includes all the finished goods inventories

and semi finish goods inventories. They

value their closing inventory based on lower

of cost or market value whichever is lower.

Sales Revenue $3,483,755,000

Total sales revenue includes all the sales of

their subsidiaries. It is the main source of

earning of JB Hi-Fi.

Other Income $520,000 Other income of JB Hi-Fi includes interest

income and many other hedging gains. They

have presented it separately in their income

1 Easton, McAnally, and Zhang Sommers. "Financial Statement Analysis & Valuation, 5e." (2018).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

statement and a respective foot not

explaining the details also included in the

notes.

Plant and Equipment $181,564,000

They have reported their total plant and

equipment in their annual report 2014 with a

detailed breakup of the block of assets

including accumulated depreciation. They

have shown their plant and equipment netted

with accumulated depreciation.

Interest Expenses (Finance

Costs) $8,845,000

They have reported their total finance costs

or the Interest expense in their annual report

with a note explaining the components of

their net finance costs.

Sales and Marketing Expense $365,694,000

They have reported a significant amount of

sales and marketing expenses in their 2014

annual report, which implies they have spent

a huge amount in the sales promotional

activities.

Occupancy Expenses $148,969,000

It includes expenses relating to occupying a

office or building. Expenses such as Rent,

Rates and taxes are included in It.

Trade and other payables $302,979,000

They have stated their trade and other

payables at amortised costs. Their trade and

other payables include, trade payables, GST

payables, other credits and accruals and

deferred incomes.

Borrowings (Non-current) $179,653,000

Their noncurrent borrowing mainly includes

unsecured bank loans. They are having a

significant amount of long-term borrowings

to finance their long-term financial needs.

2. Normal balance of above accounts and effects for decrease in balance:

Name of Accounts Normal Balance Effect of decrease in normal balance

statement and a respective foot not

explaining the details also included in the

notes.

Plant and Equipment $181,564,000

They have reported their total plant and

equipment in their annual report 2014 with a

detailed breakup of the block of assets

including accumulated depreciation. They

have shown their plant and equipment netted

with accumulated depreciation.

Interest Expenses (Finance

Costs) $8,845,000

They have reported their total finance costs

or the Interest expense in their annual report

with a note explaining the components of

their net finance costs.

Sales and Marketing Expense $365,694,000

They have reported a significant amount of

sales and marketing expenses in their 2014

annual report, which implies they have spent

a huge amount in the sales promotional

activities.

Occupancy Expenses $148,969,000

It includes expenses relating to occupying a

office or building. Expenses such as Rent,

Rates and taxes are included in It.

Trade and other payables $302,979,000

They have stated their trade and other

payables at amortised costs. Their trade and

other payables include, trade payables, GST

payables, other credits and accruals and

deferred incomes.

Borrowings (Non-current) $179,653,000

Their noncurrent borrowing mainly includes

unsecured bank loans. They are having a

significant amount of long-term borrowings

to finance their long-term financial needs.

2. Normal balance of above accounts and effects for decrease in balance:

Name of Accounts Normal Balance Effect of decrease in normal balance

5FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

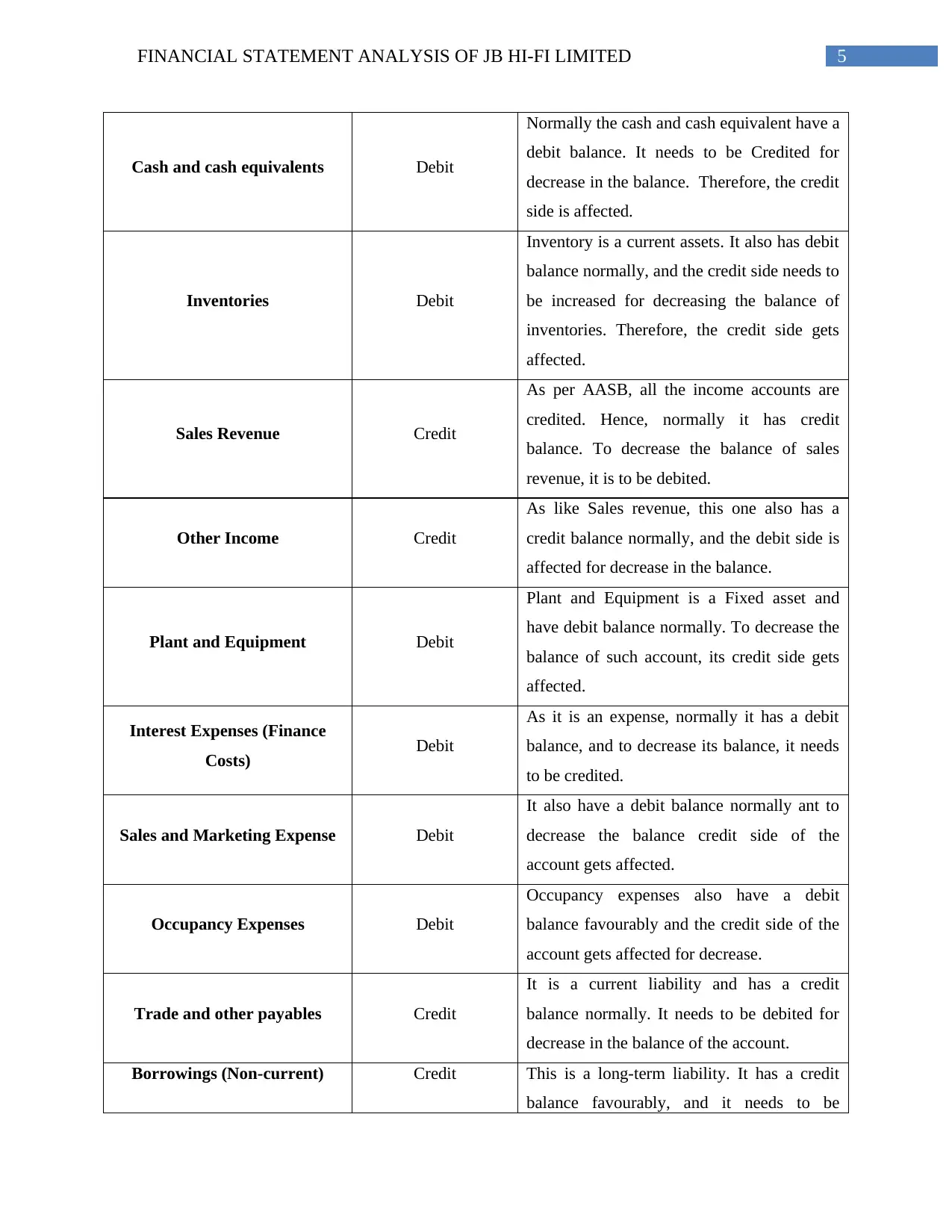

Cash and cash equivalents Debit

Normally the cash and cash equivalent have a

debit balance. It needs to be Credited for

decrease in the balance. Therefore, the credit

side is affected.

Inventories Debit

Inventory is a current assets. It also has debit

balance normally, and the credit side needs to

be increased for decreasing the balance of

inventories. Therefore, the credit side gets

affected.

Sales Revenue Credit

As per AASB, all the income accounts are

credited. Hence, normally it has credit

balance. To decrease the balance of sales

revenue, it is to be debited.

Other Income Credit

As like Sales revenue, this one also has a

credit balance normally, and the debit side is

affected for decrease in the balance.

Plant and Equipment Debit

Plant and Equipment is a Fixed asset and

have debit balance normally. To decrease the

balance of such account, its credit side gets

affected.

Interest Expenses (Finance

Costs) Debit

As it is an expense, normally it has a debit

balance, and to decrease its balance, it needs

to be credited.

Sales and Marketing Expense Debit

It also have a debit balance normally ant to

decrease the balance credit side of the

account gets affected.

Occupancy Expenses Debit

Occupancy expenses also have a debit

balance favourably and the credit side of the

account gets affected for decrease.

Trade and other payables Credit

It is a current liability and has a credit

balance normally. It needs to be debited for

decrease in the balance of the account.

Borrowings (Non-current) Credit This is a long-term liability. It has a credit

balance favourably, and it needs to be

Cash and cash equivalents Debit

Normally the cash and cash equivalent have a

debit balance. It needs to be Credited for

decrease in the balance. Therefore, the credit

side is affected.

Inventories Debit

Inventory is a current assets. It also has debit

balance normally, and the credit side needs to

be increased for decreasing the balance of

inventories. Therefore, the credit side gets

affected.

Sales Revenue Credit

As per AASB, all the income accounts are

credited. Hence, normally it has credit

balance. To decrease the balance of sales

revenue, it is to be debited.

Other Income Credit

As like Sales revenue, this one also has a

credit balance normally, and the debit side is

affected for decrease in the balance.

Plant and Equipment Debit

Plant and Equipment is a Fixed asset and

have debit balance normally. To decrease the

balance of such account, its credit side gets

affected.

Interest Expenses (Finance

Costs) Debit

As it is an expense, normally it has a debit

balance, and to decrease its balance, it needs

to be credited.

Sales and Marketing Expense Debit

It also have a debit balance normally ant to

decrease the balance credit side of the

account gets affected.

Occupancy Expenses Debit

Occupancy expenses also have a debit

balance favourably and the credit side of the

account gets affected for decrease.

Trade and other payables Credit

It is a current liability and has a credit

balance normally. It needs to be debited for

decrease in the balance of the account.

Borrowings (Non-current) Credit This is a long-term liability. It has a credit

balance favourably, and it needs to be

6FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

debited for decreasing the balance.

Part B:

1. Different types of revenues generated by consolidated group of JB Hi-Fi:

JB Hi-Fi is having various subsidiaries operating in different business segments. Their

retail segment earns revenue from retail sale of goods through retail outlets and online stores.

Some of their subsidiary acts as a subsidiary to other companies and they earn commission as the

revenue from those services2. They are also rendering various services to their clients and

customers and they earn service revenue from there. Some of their subsidiaries provide various

such services where from they earn subscription revenue. Their total revenue also includes some

interest income and dividend income from some deposits and investments.

Therefore, it can be concluded that they have generated their total revenue from retail

selling of various consumer goods and rendering of various services and it also includes some

interest and investment incomes.

2. Assets classification of JB Hi-Fi:

JB Hi-Fi reported $859,841,000 of total assets in their balance sheet. They have presented

their total assets classifying in two broad heads, Current assets and Noncurrent assts. Again they

have classified their assets in various groups and sub groups for better and clear presentation of

their financial position. Their total current assets include, cash and cash equivalent, trade and

other receivables, inventories and other current assets. Their total noncurrent assets include,

financial assets, plant and equipment, deferred tax assets and intangible assets, which includes

goodwill. They have reported sufficient amount of information in the notes of the financial

statement to explain the components of their assets3.

2 JB Hi-Fi Limited. (2014). JB Hi-Fi Annual report 2014 [Ebook]. Auustralia. Retrieved from http://Feltham, Gerald

A., and James A. Ohlson. "Valuation and clean surplus accounting for operating and financial activities."

Contemporary accounting research 11.2 (1995): 689-731.

3 JB Hi-Fi Limited. (2014). JB Hi-Fi Annual report 2014 [Ebook]. Auustralia. Retrieved from http://Feltham, Gerald

A., and James A. Ohlson. "Valuation and clean surplus accounting for operating and financial activities."

Contemporary accounting research 11.2 (1995): 689-731.

debited for decreasing the balance.

Part B:

1. Different types of revenues generated by consolidated group of JB Hi-Fi:

JB Hi-Fi is having various subsidiaries operating in different business segments. Their

retail segment earns revenue from retail sale of goods through retail outlets and online stores.

Some of their subsidiary acts as a subsidiary to other companies and they earn commission as the

revenue from those services2. They are also rendering various services to their clients and

customers and they earn service revenue from there. Some of their subsidiaries provide various

such services where from they earn subscription revenue. Their total revenue also includes some

interest income and dividend income from some deposits and investments.

Therefore, it can be concluded that they have generated their total revenue from retail

selling of various consumer goods and rendering of various services and it also includes some

interest and investment incomes.

2. Assets classification of JB Hi-Fi:

JB Hi-Fi reported $859,841,000 of total assets in their balance sheet. They have presented

their total assets classifying in two broad heads, Current assets and Noncurrent assts. Again they

have classified their assets in various groups and sub groups for better and clear presentation of

their financial position. Their total current assets include, cash and cash equivalent, trade and

other receivables, inventories and other current assets. Their total noncurrent assets include,

financial assets, plant and equipment, deferred tax assets and intangible assets, which includes

goodwill. They have reported sufficient amount of information in the notes of the financial

statement to explain the components of their assets3.

2 JB Hi-Fi Limited. (2014). JB Hi-Fi Annual report 2014 [Ebook]. Auustralia. Retrieved from http://Feltham, Gerald

A., and James A. Ohlson. "Valuation and clean surplus accounting for operating and financial activities."

Contemporary accounting research 11.2 (1995): 689-731.

3 JB Hi-Fi Limited. (2014). JB Hi-Fi Annual report 2014 [Ebook]. Auustralia. Retrieved from http://Feltham, Gerald

A., and James A. Ohlson. "Valuation and clean surplus accounting for operating and financial activities."

Contemporary accounting research 11.2 (1995): 689-731.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

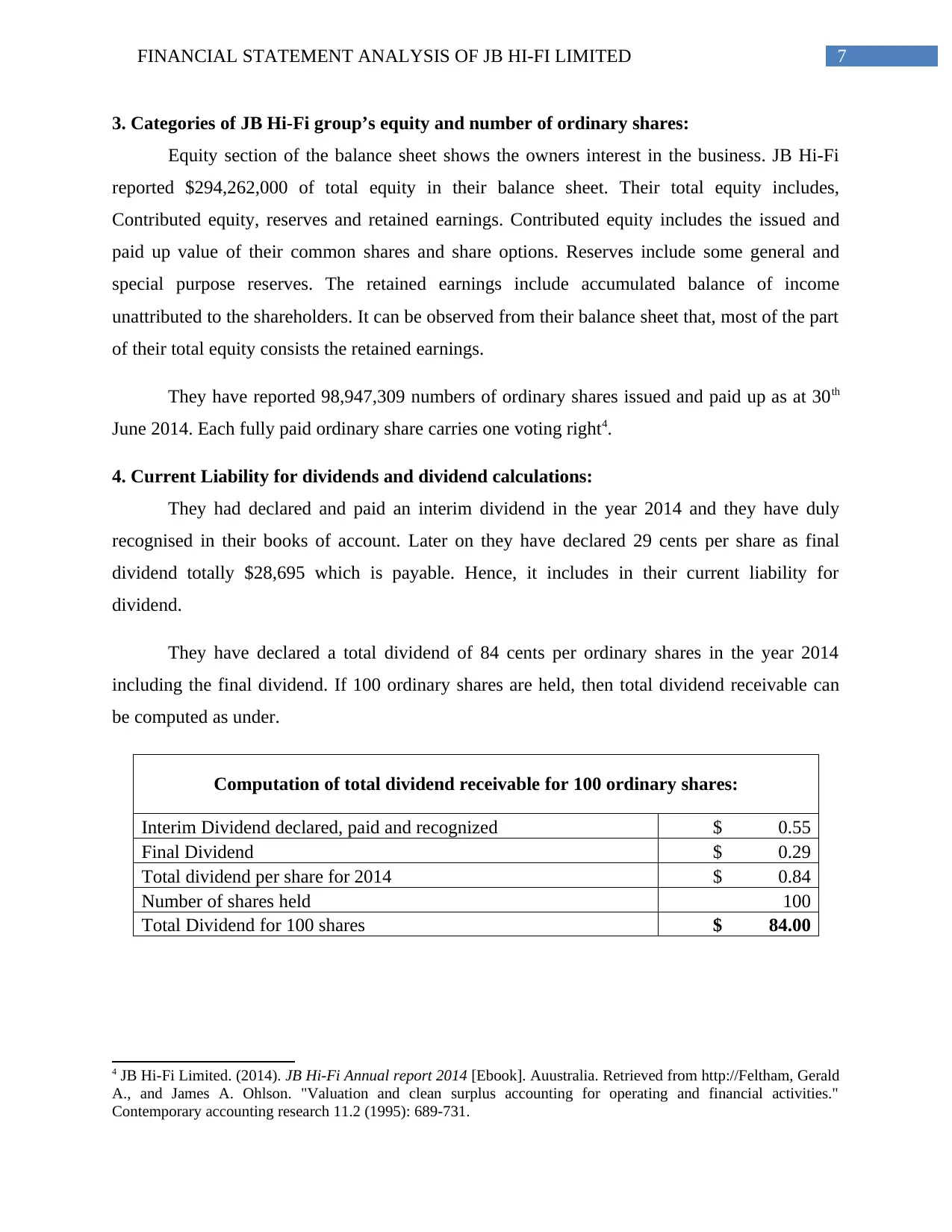

3. Categories of JB Hi-Fi group’s equity and number of ordinary shares:

Equity section of the balance sheet shows the owners interest in the business. JB Hi-Fi

reported $294,262,000 of total equity in their balance sheet. Their total equity includes,

Contributed equity, reserves and retained earnings. Contributed equity includes the issued and

paid up value of their common shares and share options. Reserves include some general and

special purpose reserves. The retained earnings include accumulated balance of income

unattributed to the shareholders. It can be observed from their balance sheet that, most of the part

of their total equity consists the retained earnings.

They have reported 98,947,309 numbers of ordinary shares issued and paid up as at 30th

June 2014. Each fully paid ordinary share carries one voting right4.

4. Current Liability for dividends and dividend calculations:

They had declared and paid an interim dividend in the year 2014 and they have duly

recognised in their books of account. Later on they have declared 29 cents per share as final

dividend totally $28,695 which is payable. Hence, it includes in their current liability for

dividend.

They have declared a total dividend of 84 cents per ordinary shares in the year 2014

including the final dividend. If 100 ordinary shares are held, then total dividend receivable can

be computed as under.

Computation of total dividend receivable for 100 ordinary shares:

Interim Dividend declared, paid and recognized $ 0.55

Final Dividend $ 0.29

Total dividend per share for 2014 $ 0.84

Number of shares held 100

Total Dividend for 100 shares $ 84.00

4 JB Hi-Fi Limited. (2014). JB Hi-Fi Annual report 2014 [Ebook]. Auustralia. Retrieved from http://Feltham, Gerald

A., and James A. Ohlson. "Valuation and clean surplus accounting for operating and financial activities."

Contemporary accounting research 11.2 (1995): 689-731.

3. Categories of JB Hi-Fi group’s equity and number of ordinary shares:

Equity section of the balance sheet shows the owners interest in the business. JB Hi-Fi

reported $294,262,000 of total equity in their balance sheet. Their total equity includes,

Contributed equity, reserves and retained earnings. Contributed equity includes the issued and

paid up value of their common shares and share options. Reserves include some general and

special purpose reserves. The retained earnings include accumulated balance of income

unattributed to the shareholders. It can be observed from their balance sheet that, most of the part

of their total equity consists the retained earnings.

They have reported 98,947,309 numbers of ordinary shares issued and paid up as at 30th

June 2014. Each fully paid ordinary share carries one voting right4.

4. Current Liability for dividends and dividend calculations:

They had declared and paid an interim dividend in the year 2014 and they have duly

recognised in their books of account. Later on they have declared 29 cents per share as final

dividend totally $28,695 which is payable. Hence, it includes in their current liability for

dividend.

They have declared a total dividend of 84 cents per ordinary shares in the year 2014

including the final dividend. If 100 ordinary shares are held, then total dividend receivable can

be computed as under.

Computation of total dividend receivable for 100 ordinary shares:

Interim Dividend declared, paid and recognized $ 0.55

Final Dividend $ 0.29

Total dividend per share for 2014 $ 0.84

Number of shares held 100

Total Dividend for 100 shares $ 84.00

4 JB Hi-Fi Limited. (2014). JB Hi-Fi Annual report 2014 [Ebook]. Auustralia. Retrieved from http://Feltham, Gerald

A., and James A. Ohlson. "Valuation and clean surplus accounting for operating and financial activities."

Contemporary accounting research 11.2 (1995): 689-731.

8FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

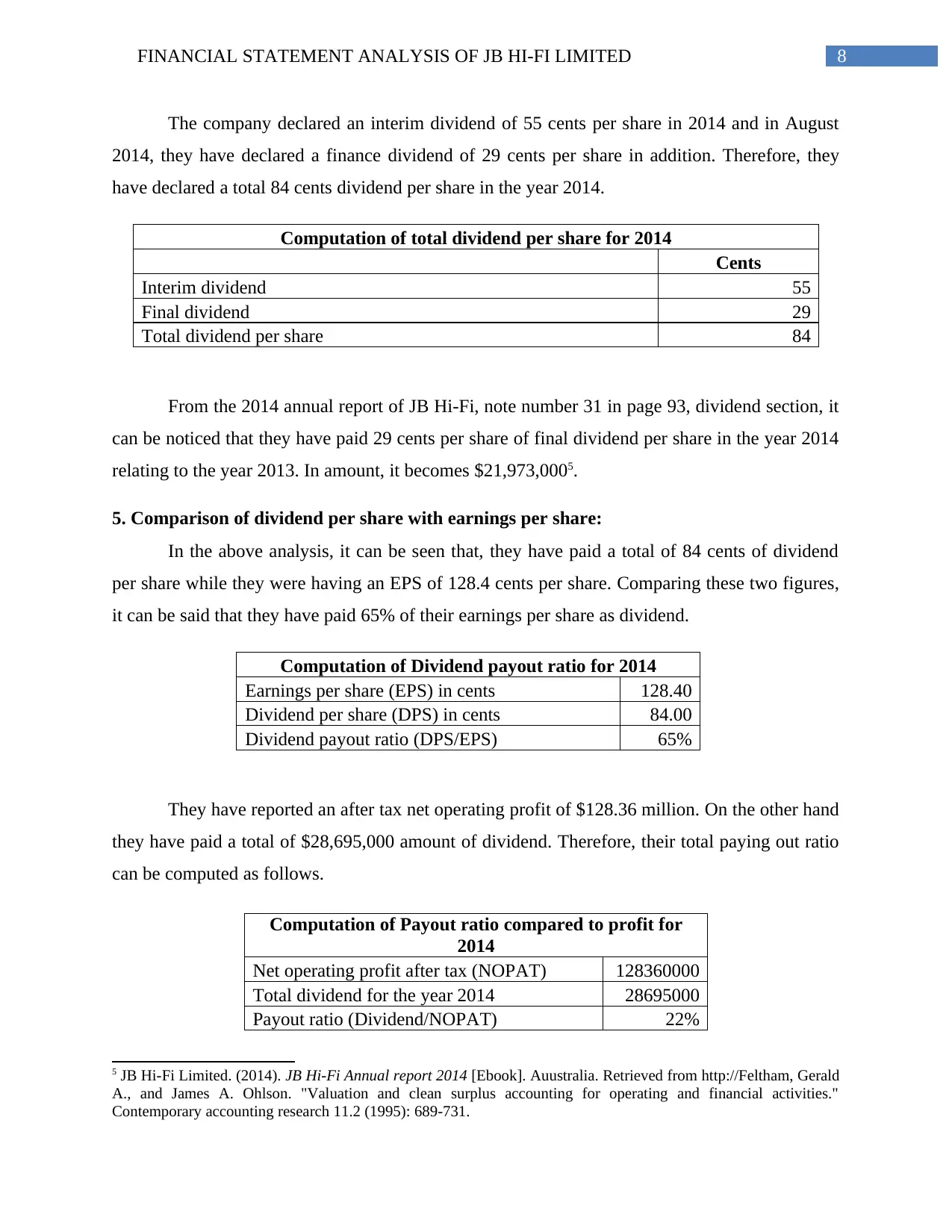

The company declared an interim dividend of 55 cents per share in 2014 and in August

2014, they have declared a finance dividend of 29 cents per share in addition. Therefore, they

have declared a total 84 cents dividend per share in the year 2014.

Computation of total dividend per share for 2014

Cents

Interim dividend 55

Final dividend 29

Total dividend per share 84

From the 2014 annual report of JB Hi-Fi, note number 31 in page 93, dividend section, it

can be noticed that they have paid 29 cents per share of final dividend per share in the year 2014

relating to the year 2013. In amount, it becomes $21,973,0005.

5. Comparison of dividend per share with earnings per share:

In the above analysis, it can be seen that, they have paid a total of 84 cents of dividend

per share while they were having an EPS of 128.4 cents per share. Comparing these two figures,

it can be said that they have paid 65% of their earnings per share as dividend.

Computation of Dividend payout ratio for 2014

Earnings per share (EPS) in cents 128.40

Dividend per share (DPS) in cents 84.00

Dividend payout ratio (DPS/EPS) 65%

They have reported an after tax net operating profit of $128.36 million. On the other hand

they have paid a total of $28,695,000 amount of dividend. Therefore, their total paying out ratio

can be computed as follows.

5 JB Hi-Fi Limited. (2014). JB Hi-Fi Annual report 2014 [Ebook]. Auustralia. Retrieved from http://Feltham, Gerald

A., and James A. Ohlson. "Valuation and clean surplus accounting for operating and financial activities."

Contemporary accounting research 11.2 (1995): 689-731.

Computation of Payout ratio compared to profit for

2014

Net operating profit after tax (NOPAT) 128360000

Total dividend for the year 2014 28695000

Payout ratio (Dividend/NOPAT) 22%

The company declared an interim dividend of 55 cents per share in 2014 and in August

2014, they have declared a finance dividend of 29 cents per share in addition. Therefore, they

have declared a total 84 cents dividend per share in the year 2014.

Computation of total dividend per share for 2014

Cents

Interim dividend 55

Final dividend 29

Total dividend per share 84

From the 2014 annual report of JB Hi-Fi, note number 31 in page 93, dividend section, it

can be noticed that they have paid 29 cents per share of final dividend per share in the year 2014

relating to the year 2013. In amount, it becomes $21,973,0005.

5. Comparison of dividend per share with earnings per share:

In the above analysis, it can be seen that, they have paid a total of 84 cents of dividend

per share while they were having an EPS of 128.4 cents per share. Comparing these two figures,

it can be said that they have paid 65% of their earnings per share as dividend.

Computation of Dividend payout ratio for 2014

Earnings per share (EPS) in cents 128.40

Dividend per share (DPS) in cents 84.00

Dividend payout ratio (DPS/EPS) 65%

They have reported an after tax net operating profit of $128.36 million. On the other hand

they have paid a total of $28,695,000 amount of dividend. Therefore, their total paying out ratio

can be computed as follows.

5 JB Hi-Fi Limited. (2014). JB Hi-Fi Annual report 2014 [Ebook]. Auustralia. Retrieved from http://Feltham, Gerald

A., and James A. Ohlson. "Valuation and clean surplus accounting for operating and financial activities."

Contemporary accounting research 11.2 (1995): 689-731.

Computation of Payout ratio compared to profit for

2014

Net operating profit after tax (NOPAT) 128360000

Total dividend for the year 2014 28695000

Payout ratio (Dividend/NOPAT) 22%

9FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

Part C:

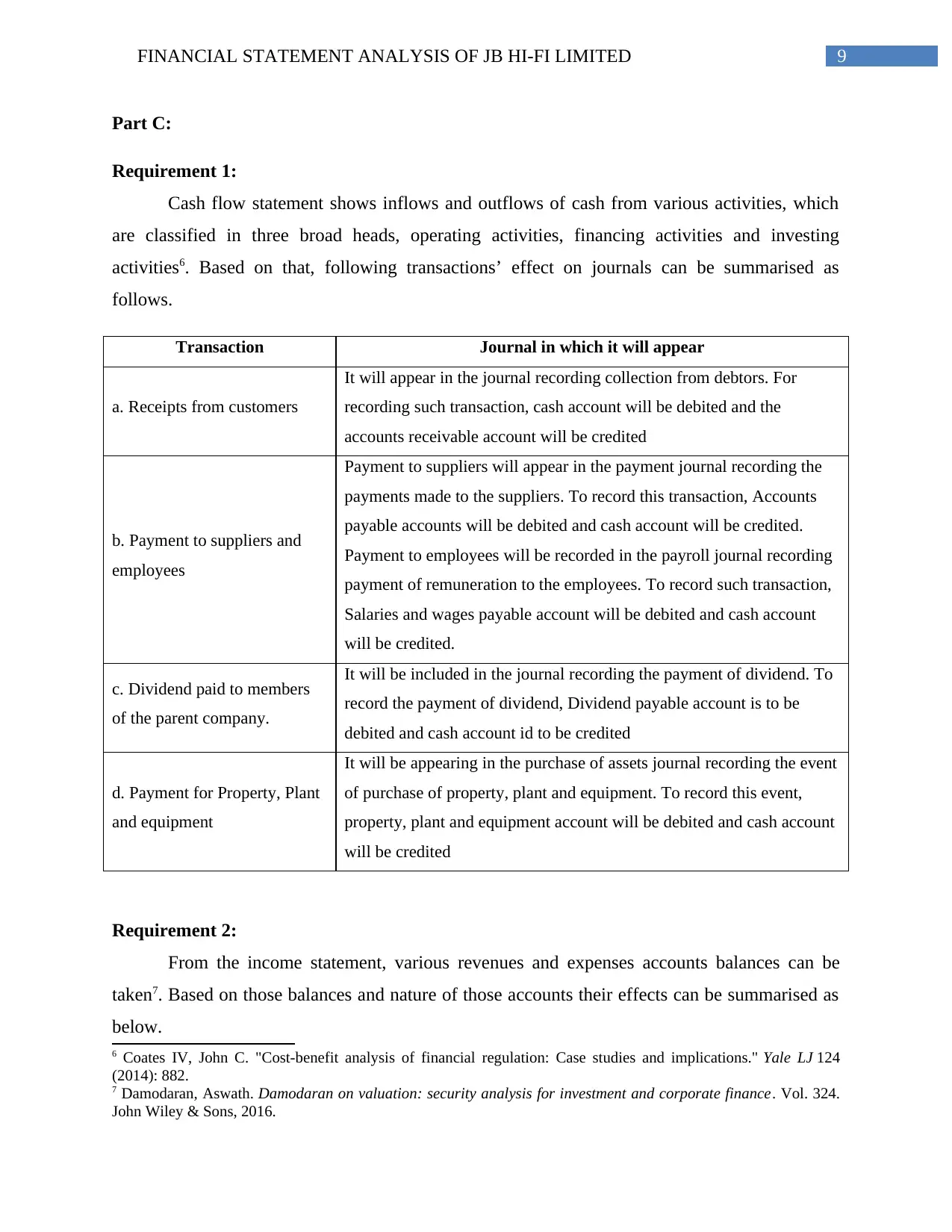

Requirement 1:

Cash flow statement shows inflows and outflows of cash from various activities, which

are classified in three broad heads, operating activities, financing activities and investing

activities6. Based on that, following transactions’ effect on journals can be summarised as

follows.

Transaction Journal in which it will appear

a. Receipts from customers

It will appear in the journal recording collection from debtors. For

recording such transaction, cash account will be debited and the

accounts receivable account will be credited

b. Payment to suppliers and

employees

Payment to suppliers will appear in the payment journal recording the

payments made to the suppliers. To record this transaction, Accounts

payable accounts will be debited and cash account will be credited.

Payment to employees will be recorded in the payroll journal recording

payment of remuneration to the employees. To record such transaction,

Salaries and wages payable account will be debited and cash account

will be credited.

c. Dividend paid to members

of the parent company.

It will be included in the journal recording the payment of dividend. To

record the payment of dividend, Dividend payable account is to be

debited and cash account id to be credited

d. Payment for Property, Plant

and equipment

It will be appearing in the purchase of assets journal recording the event

of purchase of property, plant and equipment. To record this event,

property, plant and equipment account will be debited and cash account

will be credited

Requirement 2:

From the income statement, various revenues and expenses accounts balances can be

taken7. Based on those balances and nature of those accounts their effects can be summarised as

below.

6 Coates IV, John C. "Cost-benefit analysis of financial regulation: Case studies and implications." Yale LJ 124

(2014): 882.

7 Damodaran, Aswath. Damodaran on valuation: security analysis for investment and corporate finance. Vol. 324.

John Wiley & Sons, 2016.

Part C:

Requirement 1:

Cash flow statement shows inflows and outflows of cash from various activities, which

are classified in three broad heads, operating activities, financing activities and investing

activities6. Based on that, following transactions’ effect on journals can be summarised as

follows.

Transaction Journal in which it will appear

a. Receipts from customers

It will appear in the journal recording collection from debtors. For

recording such transaction, cash account will be debited and the

accounts receivable account will be credited

b. Payment to suppliers and

employees

Payment to suppliers will appear in the payment journal recording the

payments made to the suppliers. To record this transaction, Accounts

payable accounts will be debited and cash account will be credited.

Payment to employees will be recorded in the payroll journal recording

payment of remuneration to the employees. To record such transaction,

Salaries and wages payable account will be debited and cash account

will be credited.

c. Dividend paid to members

of the parent company.

It will be included in the journal recording the payment of dividend. To

record the payment of dividend, Dividend payable account is to be

debited and cash account id to be credited

d. Payment for Property, Plant

and equipment

It will be appearing in the purchase of assets journal recording the event

of purchase of property, plant and equipment. To record this event,

property, plant and equipment account will be debited and cash account

will be credited

Requirement 2:

From the income statement, various revenues and expenses accounts balances can be

taken7. Based on those balances and nature of those accounts their effects can be summarised as

below.

6 Coates IV, John C. "Cost-benefit analysis of financial regulation: Case studies and implications." Yale LJ 124

(2014): 882.

7 Damodaran, Aswath. Damodaran on valuation: security analysis for investment and corporate finance. Vol. 324.

John Wiley & Sons, 2016.

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

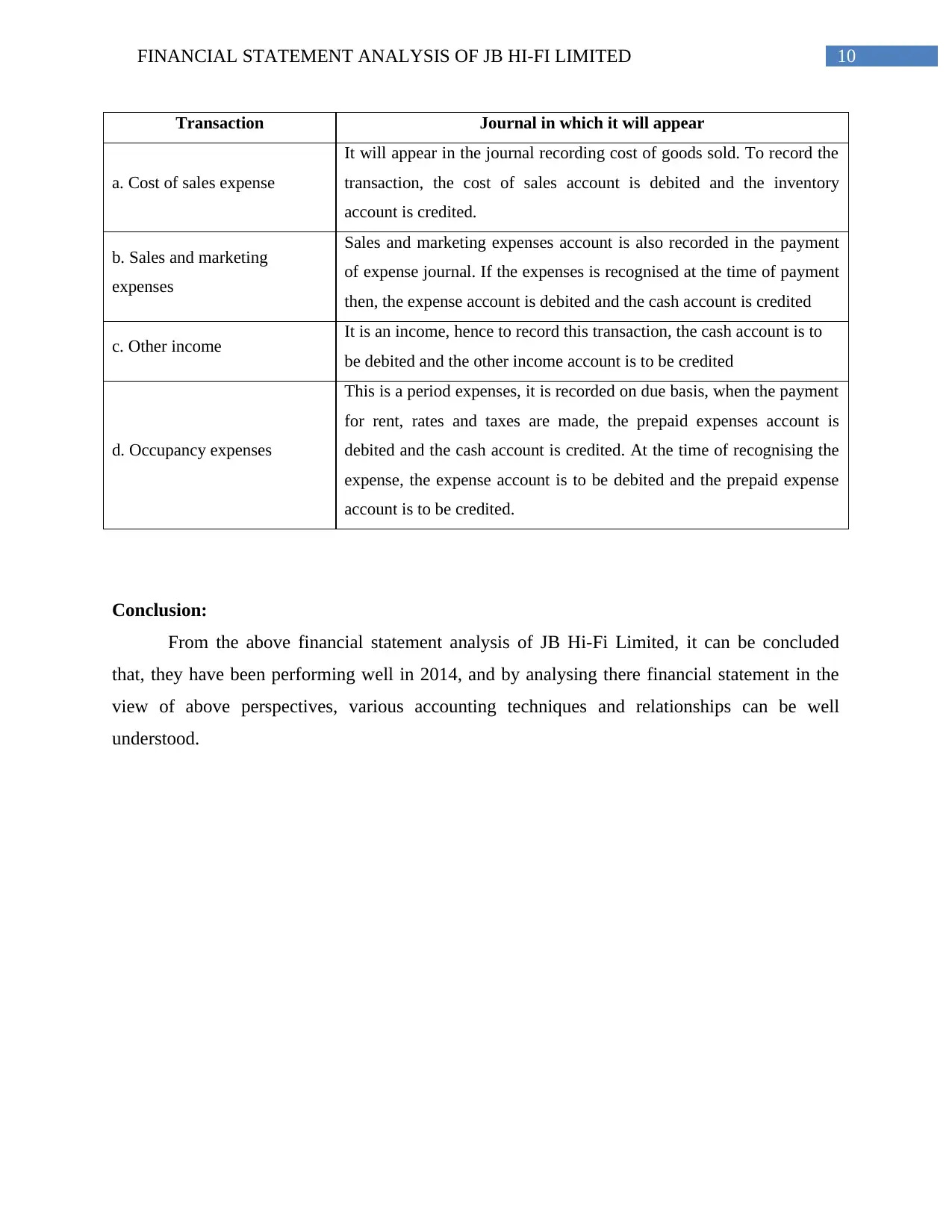

Transaction Journal in which it will appear

a. Cost of sales expense

It will appear in the journal recording cost of goods sold. To record the

transaction, the cost of sales account is debited and the inventory

account is credited.

b. Sales and marketing

expenses

Sales and marketing expenses account is also recorded in the payment

of expense journal. If the expenses is recognised at the time of payment

then, the expense account is debited and the cash account is credited

c. Other income It is an income, hence to record this transaction, the cash account is to

be debited and the other income account is to be credited

d. Occupancy expenses

This is a period expenses, it is recorded on due basis, when the payment

for rent, rates and taxes are made, the prepaid expenses account is

debited and the cash account is credited. At the time of recognising the

expense, the expense account is to be debited and the prepaid expense

account is to be credited.

Conclusion:

From the above financial statement analysis of JB Hi-Fi Limited, it can be concluded

that, they have been performing well in 2014, and by analysing there financial statement in the

view of above perspectives, various accounting techniques and relationships can be well

understood.

Transaction Journal in which it will appear

a. Cost of sales expense

It will appear in the journal recording cost of goods sold. To record the

transaction, the cost of sales account is debited and the inventory

account is credited.

b. Sales and marketing

expenses

Sales and marketing expenses account is also recorded in the payment

of expense journal. If the expenses is recognised at the time of payment

then, the expense account is debited and the cash account is credited

c. Other income It is an income, hence to record this transaction, the cash account is to

be debited and the other income account is to be credited

d. Occupancy expenses

This is a period expenses, it is recorded on due basis, when the payment

for rent, rates and taxes are made, the prepaid expenses account is

debited and the cash account is credited. At the time of recognising the

expense, the expense account is to be debited and the prepaid expense

account is to be credited.

Conclusion:

From the above financial statement analysis of JB Hi-Fi Limited, it can be concluded

that, they have been performing well in 2014, and by analysing there financial statement in the

view of above perspectives, various accounting techniques and relationships can be well

understood.

11FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

Bibliography:

Baños-Caballero, Sonia, Pedro J. García-Teruel, and Pedro Martínez-Solano. "Working capital

management, corporate performance, and financial constraints." Journal of Business

Research 67.3 (2014): 332-338.

Berk, Jonathon, et al. Fundamentals of corporate finance. Pearson Higher Education AU, 2013.

Carter, Michael M. "Engine, system and method of providing cloud-based business valuation and

associated services." U.S. Patent No. 8,666,851. 4 Mar. 2014.

Coates IV, John C. "Cost-benefit analysis of financial regulation: Case studies and

implications." Yale LJ 124 (2014): 882.

Damodaran, Aswath. Damodaran on valuation: security analysis for investment and corporate

finance. Vol. 324. John Wiley & Sons, 2016.

Easton, McAnally, and Zhang Sommers. "Financial Statement Analysis & Valuation, 5e."

(2018).

Feltham, Gerald A., and James A. Ohlson. "Valuation and clean surplus accounting for operating

and financial activities." Contemporary accounting research 11.2 (1995): 689-731.

Fracassi, Cesare. "Corporate finance policies and social networks." Management Science 63.8

(2016): 2420-2438.

Healy, Paul M., and Krishna G. Palepu. Business analysis valuation: Using financial statements.

Cengage Learning, 2012.

Idowu, Samuel O., et al. Encyclopedia of corporate social responsibility. Vol. 21. New York:

Springer, 2013.

JB Hi-Fi Limited. (2014). JB Hi-Fi Annual report 2014 [Ebook]. Auustralia. Retrieved from

http://Feltham, Gerald A., and James A. Ohlson. "Valuation and clean surplus accounting for

operating and financial activities." Contemporary accounting research 11.2 (1995): 689-731.

Bibliography:

Baños-Caballero, Sonia, Pedro J. García-Teruel, and Pedro Martínez-Solano. "Working capital

management, corporate performance, and financial constraints." Journal of Business

Research 67.3 (2014): 332-338.

Berk, Jonathon, et al. Fundamentals of corporate finance. Pearson Higher Education AU, 2013.

Carter, Michael M. "Engine, system and method of providing cloud-based business valuation and

associated services." U.S. Patent No. 8,666,851. 4 Mar. 2014.

Coates IV, John C. "Cost-benefit analysis of financial regulation: Case studies and

implications." Yale LJ 124 (2014): 882.

Damodaran, Aswath. Damodaran on valuation: security analysis for investment and corporate

finance. Vol. 324. John Wiley & Sons, 2016.

Easton, McAnally, and Zhang Sommers. "Financial Statement Analysis & Valuation, 5e."

(2018).

Feltham, Gerald A., and James A. Ohlson. "Valuation and clean surplus accounting for operating

and financial activities." Contemporary accounting research 11.2 (1995): 689-731.

Fracassi, Cesare. "Corporate finance policies and social networks." Management Science 63.8

(2016): 2420-2438.

Healy, Paul M., and Krishna G. Palepu. Business analysis valuation: Using financial statements.

Cengage Learning, 2012.

Idowu, Samuel O., et al. Encyclopedia of corporate social responsibility. Vol. 21. New York:

Springer, 2013.

JB Hi-Fi Limited. (2014). JB Hi-Fi Annual report 2014 [Ebook]. Auustralia. Retrieved from

http://Feltham, Gerald A., and James A. Ohlson. "Valuation and clean surplus accounting for

operating and financial activities." Contemporary accounting research 11.2 (1995): 689-731.

12FINANCIAL STATEMENT ANALYSIS OF JB HI-FI LIMITED

Mathuva, David. "The Influence of working capital management components on corporate

profitability." (2015).

Mathuva, David. "The Influence of working capital management components on corporate

profitability." (2015).

Ross, Stephen A., et al. Corporate finance. McGraw-Hill/Irwin, 2013.

Trugman. Understanding business valuation: A practical guide to valuing small to medium sized

businesses. John Wiley & Sons, 2016.

Mathuva, David. "The Influence of working capital management components on corporate

profitability." (2015).

Mathuva, David. "The Influence of working capital management components on corporate

profitability." (2015).

Ross, Stephen A., et al. Corporate finance. McGraw-Hill/Irwin, 2013.

Trugman. Understanding business valuation: A practical guide to valuing small to medium sized

businesses. John Wiley & Sons, 2016.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.