Financial Reporting of Macquarie Group

VerifiedAdded on 2020/06/03

|17

|2470

|56

AI Summary

This assignment delves into the financial reporting practices of Macquarie Group (MQG) for the fiscal year 2016-2017. It examines various financial statements, including the income statement, comprehensive income statement, statement of financial position, statement of changes in equity, and cash flow statement. The analysis considers reporting standards like IAS and IFRS, highlighting MQG's adherence to these frameworks. The report further assesses the effectiveness of MQG's reporting techniques in showcasing revenue generation strategies and overall financial performance, ultimately aiming to determine their impact on stakeholder investment decisions.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

FINANCIAL STATEMENT

ANALYSIS ON

DISCLOSURE

REQUIREMENTS

ANALYSIS ON

DISCLOSURE

REQUIREMENTS

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

STEP 1: Financial report of Macquarie Group Limited..................................................................1

STEP 2: Analysis of Financial reports.............................................................................................1

(a) Analysing the profit and loss statement of Macquarie Group Limited.............................1

(b) Comprehensive income statement of Macquarie Group Limited.....................................3

(c) Analysing the financial position of MQG.........................................................................4

(d) Analysing the statement of change in equity....................................................................6

(e) Analysing the Cash flow statement of MQG....................................................................8

STEP 3: Revenue analysis.............................................................................................................10

STEP 4: Financial instruments.......................................................................................................10

(a) Identifying all the categories of Financial position of MQG..........................................10

STEP 5: Income tax analysis.........................................................................................................11

(a) Income tax expenses of MQG.........................................................................................11

(b) Disclosure of deferred tax balance of MQG...................................................................12

STEP 6...........................................................................................................................................13

STEP 7...........................................................................................................................................14

(I) Relevant standard............................................................................................................14

(II) CPA module Financial reporting...................................................................................14

CONCLUSION..............................................................................................................................14

BIBLIOGRAPHY..........................................................................................................................15

INTRODUCTION...........................................................................................................................1

STEP 1: Financial report of Macquarie Group Limited..................................................................1

STEP 2: Analysis of Financial reports.............................................................................................1

(a) Analysing the profit and loss statement of Macquarie Group Limited.............................1

(b) Comprehensive income statement of Macquarie Group Limited.....................................3

(c) Analysing the financial position of MQG.........................................................................4

(d) Analysing the statement of change in equity....................................................................6

(e) Analysing the Cash flow statement of MQG....................................................................8

STEP 3: Revenue analysis.............................................................................................................10

STEP 4: Financial instruments.......................................................................................................10

(a) Identifying all the categories of Financial position of MQG..........................................10

STEP 5: Income tax analysis.........................................................................................................11

(a) Income tax expenses of MQG.........................................................................................11

(b) Disclosure of deferred tax balance of MQG...................................................................12

STEP 6...........................................................................................................................................13

STEP 7...........................................................................................................................................14

(I) Relevant standard............................................................................................................14

(II) CPA module Financial reporting...................................................................................14

CONCLUSION..............................................................................................................................14

BIBLIOGRAPHY..........................................................................................................................15

INTRODUCTION

In the present assessment, there will be discussion based on the financial reports of

Macquarie Group Limited which will be compared with various standards or framework

facilitated by IAS. Thus, the comparison based on the financial reports do meet all the criteria

which were facilitated by IAS. However, there will be analysis over comprehensive income

statements, profit and loss account, financial position, equity changes as well as firm's

profitability. Thus, such reporting will help professionals of the organisation in implementing the

fruitful changes in disclosure of such data set.

STEP 1: Financial report of Macquarie Group Limited

On the basis of Australian Security exchange, the MQG is having favourable value of its

share. Thus, it is an advisory group which normally deals as investment banking and fund

management services to various institutions or entities in Australia. Hence, the growth of this

firm in the international share market is rapidly increasing as well as it will be beneficial for the

shareholders or investors to make favourable investment planning. The internal strength of this

organisation is there are currently more than 14000 workers are performing their duties and 70

office which are located in 28 nations. However, due to these kinds of favourable growth the

business has $450 billion of Assets with it. Hence, there will be some analysis of the firm's

financial capacity in the market which can be understood through various financial reporting as

well as the criteria in meeting the standards set by IAS.

STEP 2: Analysis of Financial reports

(a) Analysing the profit and loss statement of Macquarie Group Limited

In accordance with the IAS, there are several rules and guidelines which are facilitated by

them in order to make adequate disclosure of accounts in universally accepted format. Thus, such

formatting will help the stakeholders or users of such reports belonging to various countries.

Hence, it will be fruitful for MQG to have investments from such nations or the international

investors. Thus, in accordance with IAS 1 which sets out whole needs of the financial statements

which are going to be disclosed as follows:

1

In the present assessment, there will be discussion based on the financial reports of

Macquarie Group Limited which will be compared with various standards or framework

facilitated by IAS. Thus, the comparison based on the financial reports do meet all the criteria

which were facilitated by IAS. However, there will be analysis over comprehensive income

statements, profit and loss account, financial position, equity changes as well as firm's

profitability. Thus, such reporting will help professionals of the organisation in implementing the

fruitful changes in disclosure of such data set.

STEP 1: Financial report of Macquarie Group Limited

On the basis of Australian Security exchange, the MQG is having favourable value of its

share. Thus, it is an advisory group which normally deals as investment banking and fund

management services to various institutions or entities in Australia. Hence, the growth of this

firm in the international share market is rapidly increasing as well as it will be beneficial for the

shareholders or investors to make favourable investment planning. The internal strength of this

organisation is there are currently more than 14000 workers are performing their duties and 70

office which are located in 28 nations. However, due to these kinds of favourable growth the

business has $450 billion of Assets with it. Hence, there will be some analysis of the firm's

financial capacity in the market which can be understood through various financial reporting as

well as the criteria in meeting the standards set by IAS.

STEP 2: Analysis of Financial reports

(a) Analysing the profit and loss statement of Macquarie Group Limited

In accordance with the IAS, there are several rules and guidelines which are facilitated by

them in order to make adequate disclosure of accounts in universally accepted format. Thus, such

formatting will help the stakeholders or users of such reports belonging to various countries.

Hence, it will be fruitful for MQG to have investments from such nations or the international

investors. Thus, in accordance with IAS 1 which sets out whole needs of the financial statements

which are going to be disclosed as follows:

1

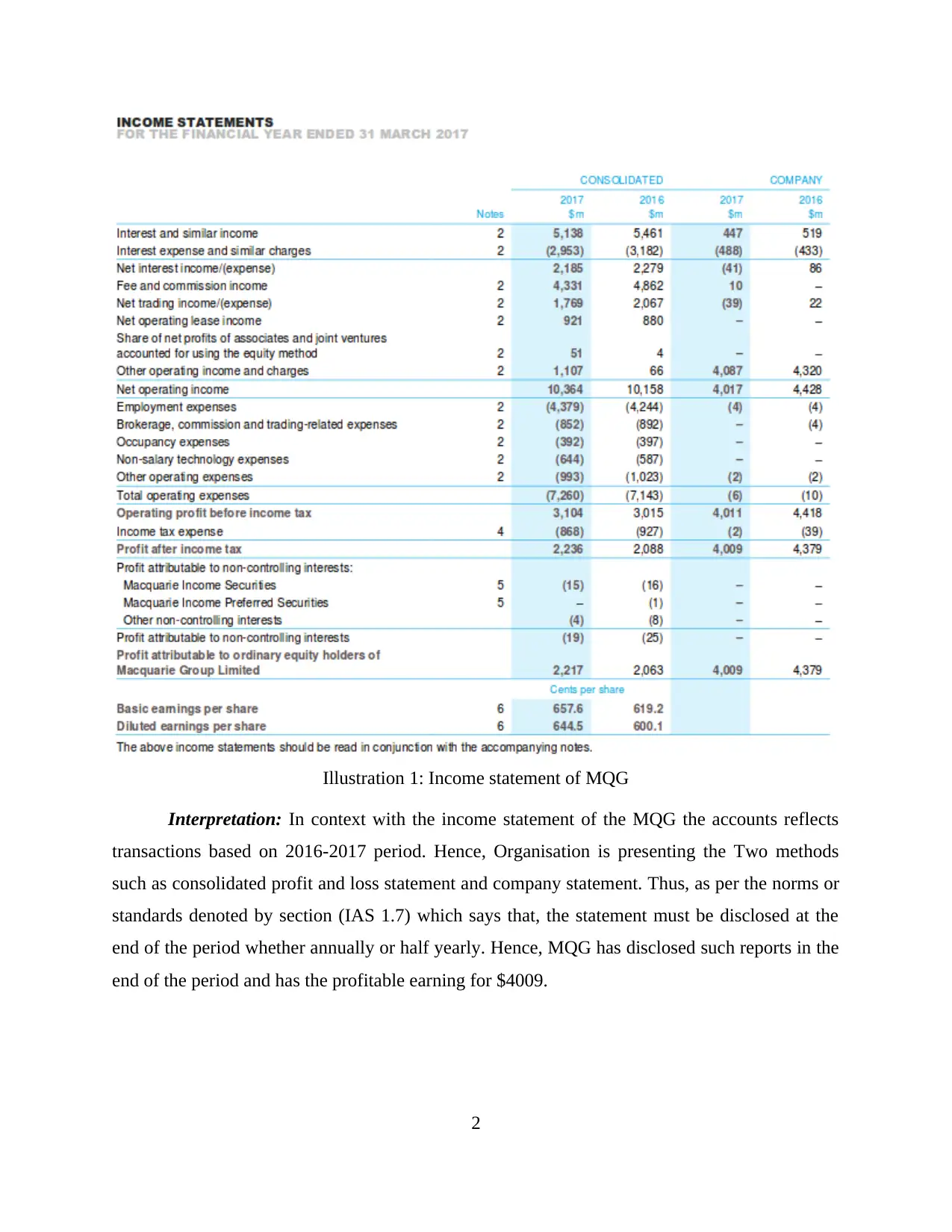

Illustration 1: Income statement of MQG

Interpretation: In context with the income statement of the MQG the accounts reflects

transactions based on 2016-2017 period. Hence, Organisation is presenting the Two methods

such as consolidated profit and loss statement and company statement. Thus, as per the norms or

standards denoted by section (IAS 1.7) which says that, the statement must be disclosed at the

end of the period whether annually or half yearly. Hence, MQG has disclosed such reports in the

end of the period and has the profitable earning for $4009.

2

Interpretation: In context with the income statement of the MQG the accounts reflects

transactions based on 2016-2017 period. Hence, Organisation is presenting the Two methods

such as consolidated profit and loss statement and company statement. Thus, as per the norms or

standards denoted by section (IAS 1.7) which says that, the statement must be disclosed at the

end of the period whether annually or half yearly. Hence, MQG has disclosed such reports in the

end of the period and has the profitable earning for $4009.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

(b) Comprehensive income statement of Macquarie Group Limited

The comprehensive income statement denotes the overall details related with the

operational transactions held in the financial year. Thus, with the help of such disclosure of

reports, firm will be able to gather maximum numbers of stakeholders or investors.

Illustration 2: Comprehensive income statement of MQG

Interpretation: As per the Statement of Comprehensive income statement of MQG the

informations are to be provided by the organisation related with the all the operational activities

held during the period. Hence, in accordance with the section (IAS 1.2) it can be said that,

Company must disclose its profit and loss statement which must be based on the period of

operating year as well as have connection with other financial reporting statements. Hence, such

3

The comprehensive income statement denotes the overall details related with the

operational transactions held in the financial year. Thus, with the help of such disclosure of

reports, firm will be able to gather maximum numbers of stakeholders or investors.

Illustration 2: Comprehensive income statement of MQG

Interpretation: As per the Statement of Comprehensive income statement of MQG the

informations are to be provided by the organisation related with the all the operational activities

held during the period. Hence, in accordance with the section (IAS 1.2) it can be said that,

Company must disclose its profit and loss statement which must be based on the period of

operating year as well as have connection with other financial reporting statements. Hence, such

3

income statement must be disclosed in the single combined report. However, as per the norms set

by IAS, MQG has presented such informations in the single report as per section (IAS 1.10).

(c) Analysing the financial position of MQG

In accordance with analysing the financial position of the MQG where the organisation is

disclosing the statements which denotes the economic stability of the firm in the year 2015 and

2016. Hence, t will be considered that the entity is able to meet the regulatory framework defined

by IAS.

4

by IAS, MQG has presented such informations in the single report as per section (IAS 1.10).

(c) Analysing the financial position of MQG

In accordance with analysing the financial position of the MQG where the organisation is

disclosing the statements which denotes the economic stability of the firm in the year 2015 and

2016. Hence, t will be considered that the entity is able to meet the regulatory framework defined

by IAS.

4

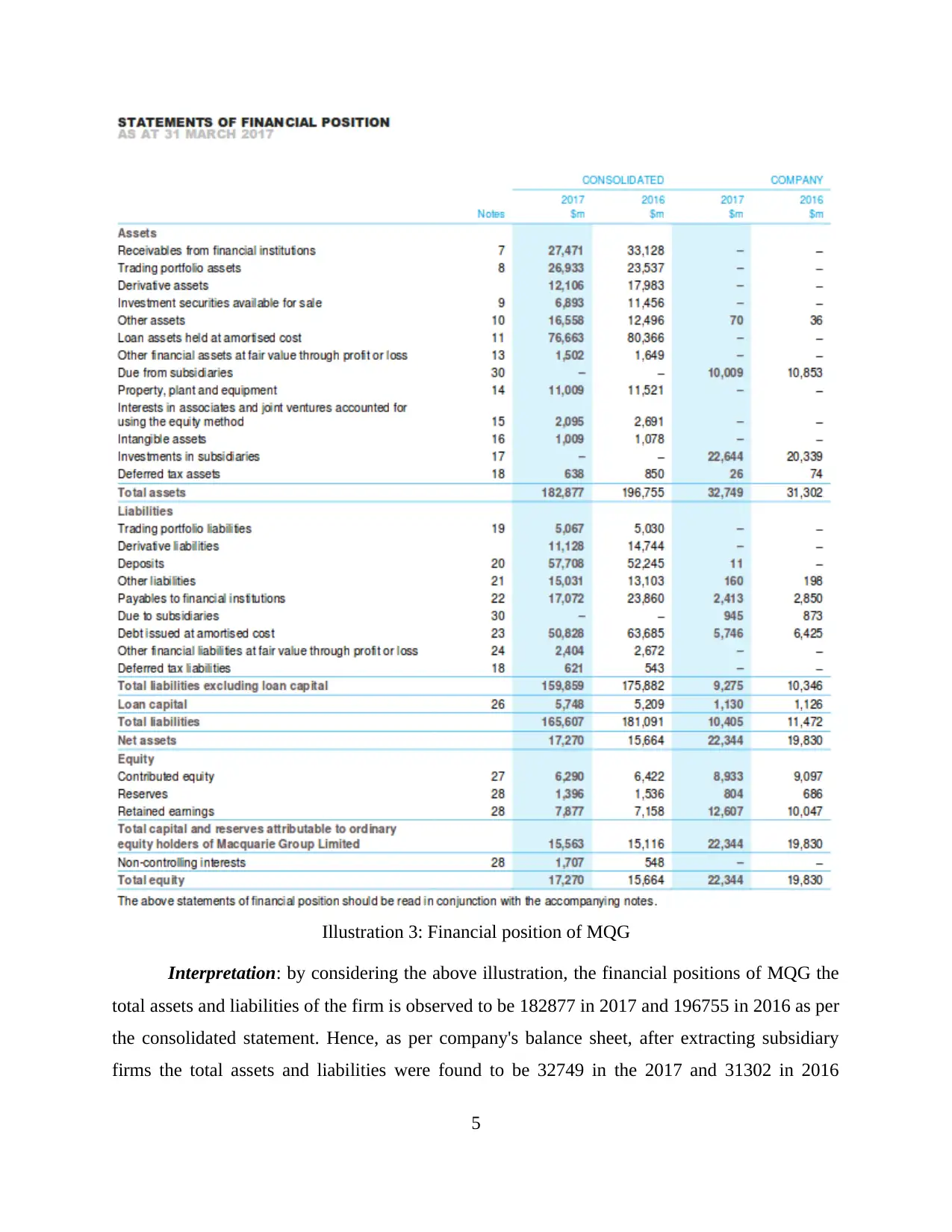

Illustration 3: Financial position of MQG

Interpretation: by considering the above illustration, the financial positions of MQG the

total assets and liabilities of the firm is observed to be 182877 in 2017 and 196755 in 2016 as per

the consolidated statement. Hence, as per company's balance sheet, after extracting subsidiary

firms the total assets and liabilities were found to be 32749 in the 2017 and 31302 in 2016

5

Interpretation: by considering the above illustration, the financial positions of MQG the

total assets and liabilities of the firm is observed to be 182877 in 2017 and 196755 in 2016 as per

the consolidated statement. Hence, as per company's balance sheet, after extracting subsidiary

firms the total assets and liabilities were found to be 32749 in the 2017 and 31302 in 2016

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

respectively. However, in accordance with the section (IAS 1.9) the financial disclosure of all the

reports must be presented in the separate statements. Thus, MQG has prepared such data set by

following such regulations.

(d) Analysing the statement of change in equity

Presentation based on the Changes in the equity capital of MQG for the year 2016 and

2017 as per the regulatory format of IAS and IFRS. Hence, it says that the presentation of the

changes in equity must be prepared for the specific period. Hence, it will enable the professionals

in the organisation to analyse the changes in their capital structure as well as they will be able to

make strategic plans which will help them in enhancing the operational efficiency.

6

reports must be presented in the separate statements. Thus, MQG has prepared such data set by

following such regulations.

(d) Analysing the statement of change in equity

Presentation based on the Changes in the equity capital of MQG for the year 2016 and

2017 as per the regulatory format of IAS and IFRS. Hence, it says that the presentation of the

changes in equity must be prepared for the specific period. Hence, it will enable the professionals

in the organisation to analyse the changes in their capital structure as well as they will be able to

make strategic plans which will help them in enhancing the operational efficiency.

6

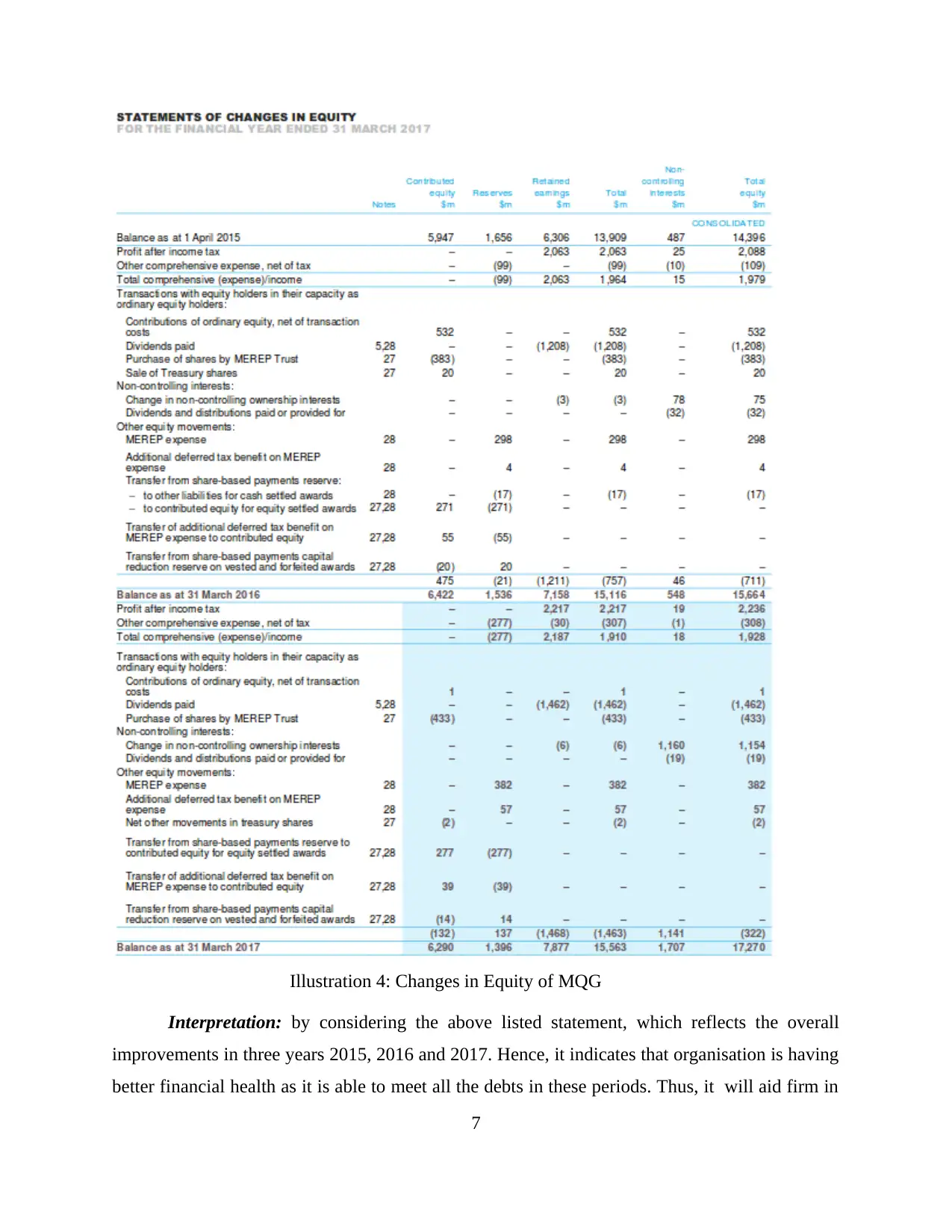

Illustration 4: Changes in Equity of MQG

Interpretation: by considering the above listed statement, which reflects the overall

improvements in three years 2015, 2016 and 2017. Hence, it indicates that organisation is having

better financial health as it is able to meet all the debts in these periods. Thus, it will aid firm in

7

Interpretation: by considering the above listed statement, which reflects the overall

improvements in three years 2015, 2016 and 2017. Hence, it indicates that organisation is having

better financial health as it is able to meet all the debts in these periods. Thus, it will aid firm in

7

attracting the maximum numbers of investors as well as increasing the market value. However,

the fair disclosure of the capital gains will be beneficial for the entity in retaining the faith of

stakeholders as well as helpful In making the fair taxation to government of Australia as per

section (IAS 1.15).

(e) Analysing the Cash flow statement of MQG

Cash Flow of MQG for the period 2016 and 2017 is based on the overall cash inflows

and outflows in context with operational functioning of the entity. Thus, such statements will

reflect the ability of firm in handling its cash credits as well as debits.

8

the fair disclosure of the capital gains will be beneficial for the entity in retaining the faith of

stakeholders as well as helpful In making the fair taxation to government of Australia as per

section (IAS 1.15).

(e) Analysing the Cash flow statement of MQG

Cash Flow of MQG for the period 2016 and 2017 is based on the overall cash inflows

and outflows in context with operational functioning of the entity. Thus, such statements will

reflect the ability of firm in handling its cash credits as well as debits.

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

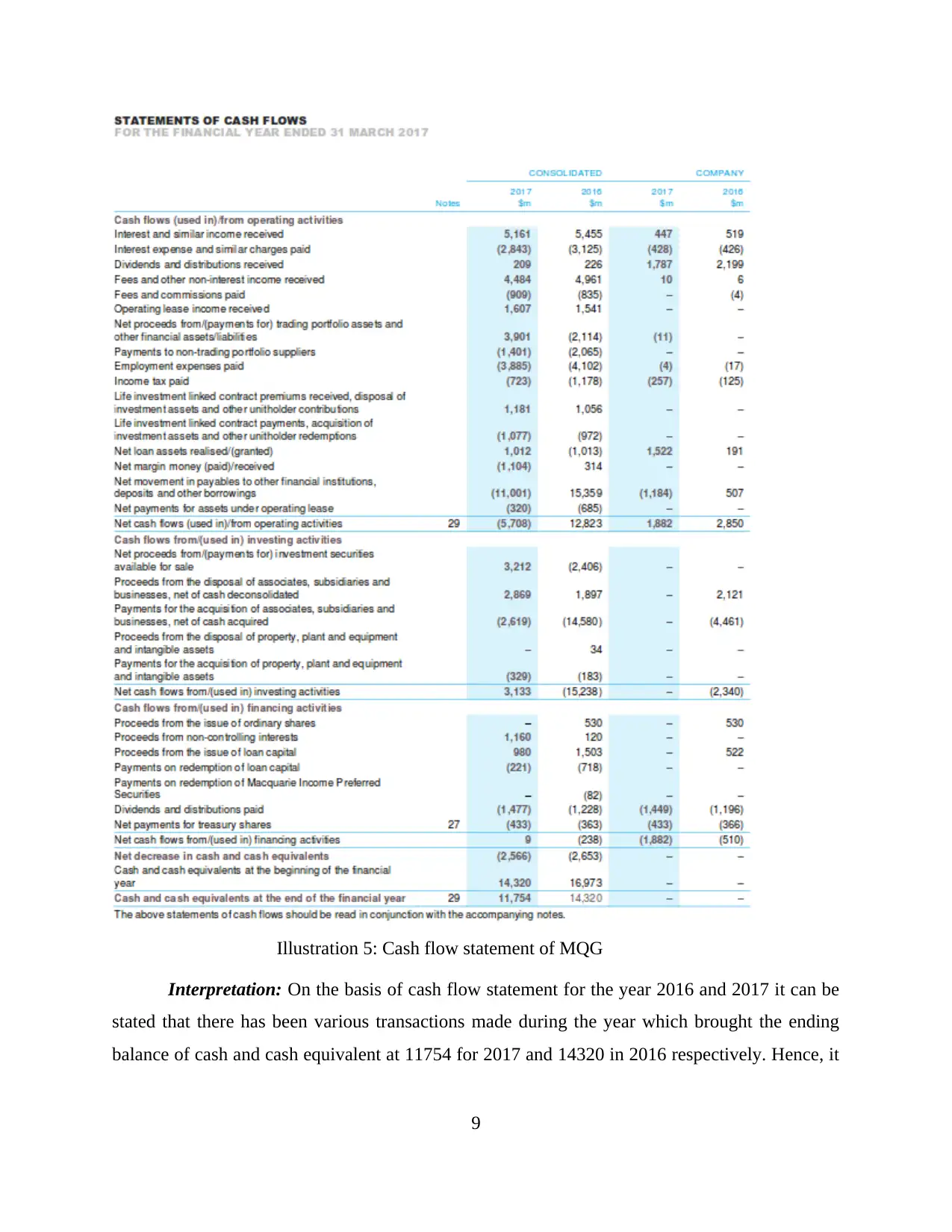

Illustration 5: Cash flow statement of MQG

Interpretation: On the basis of cash flow statement for the year 2016 and 2017 it can be

stated that there has been various transactions made during the year which brought the ending

balance of cash and cash equivalent at 11754 for 2017 and 14320 in 2016 respectively. Hence, it

9

Interpretation: On the basis of cash flow statement for the year 2016 and 2017 it can be

stated that there has been various transactions made during the year which brought the ending

balance of cash and cash equivalent at 11754 for 2017 and 14320 in 2016 respectively. Hence, it

9

can be said that the company is on the right track, as it will be able to generate favourable

amount of cash.

STEP 3: Revenue analysis

By considering the norms of AASB 151 there has been implementation of various laws

and regulations in context with making any contract with consumers. Hence, these laws can be

understood in the following aspects :

The contract must be documented in the auathorisedformat as it must be thoroughly read

and understood by the parties who are signing it. Thus, it must be developed orally,

written as well as influence of the various legal obligations.

There must be authenticated documentation of each party who are involved in it as well

as their rights and responsibilities.

It must consist of form of consideration to be awarded to the parties who are dealing in

the organisation as per section AASB 118.

The contract will be valid if there is mutual agreement from both the parties and which is

legally acceptable in norms set by Australian legislatures. Hence, it must satisfy all the

norms set in such sections of IAS (2, 16 and 38).

STEP 4: Financial instruments

(a) Identifying all the categories of Financial position of MQG

By considering the financial statement of MQG which indicates the favourable financial

growth of the entity. Thus, there has been use of various instruments which helps in making the

better disclosure such as disclosure of all current and fixed assets. Hence, the currents assets will

reflect ability of firm in meeting the short term and long-term debts. On the other side, there has

been disclosure of current liabilities of firm which indicates that, MQG is having profitability as

well as it is capable of paying dividends to shareholders.

1 Revenue from contract with consumers

10

amount of cash.

STEP 3: Revenue analysis

By considering the norms of AASB 151 there has been implementation of various laws

and regulations in context with making any contract with consumers. Hence, these laws can be

understood in the following aspects :

The contract must be documented in the auathorisedformat as it must be thoroughly read

and understood by the parties who are signing it. Thus, it must be developed orally,

written as well as influence of the various legal obligations.

There must be authenticated documentation of each party who are involved in it as well

as their rights and responsibilities.

It must consist of form of consideration to be awarded to the parties who are dealing in

the organisation as per section AASB 118.

The contract will be valid if there is mutual agreement from both the parties and which is

legally acceptable in norms set by Australian legislatures. Hence, it must satisfy all the

norms set in such sections of IAS (2, 16 and 38).

STEP 4: Financial instruments

(a) Identifying all the categories of Financial position of MQG

By considering the financial statement of MQG which indicates the favourable financial

growth of the entity. Thus, there has been use of various instruments which helps in making the

better disclosure such as disclosure of all current and fixed assets. Hence, the currents assets will

reflect ability of firm in meeting the short term and long-term debts. On the other side, there has

been disclosure of current liabilities of firm which indicates that, MQG is having profitability as

well as it is capable of paying dividends to shareholders.

1 Revenue from contract with consumers

10

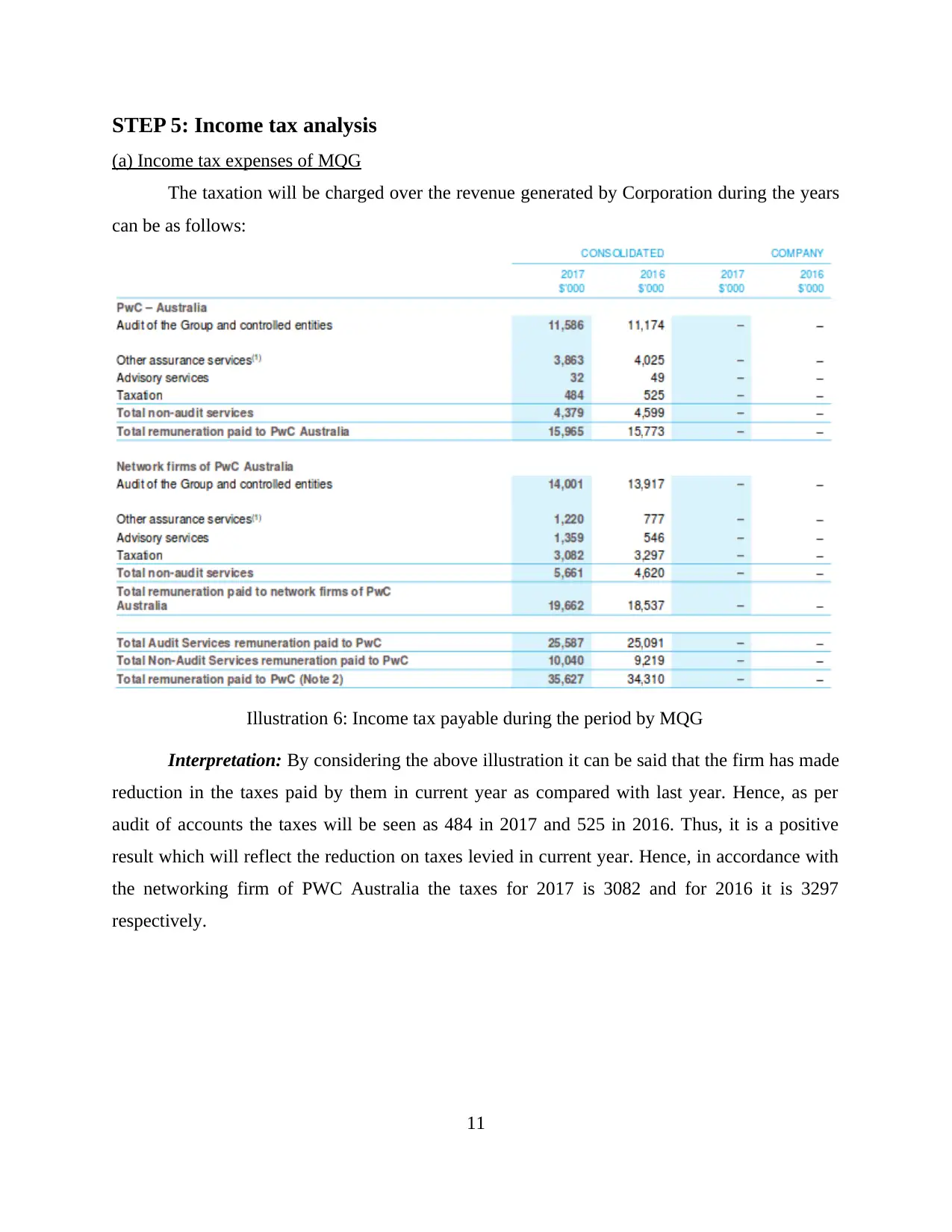

STEP 5: Income tax analysis

(a) Income tax expenses of MQG

The taxation will be charged over the revenue generated by Corporation during the years

can be as follows:

Illustration 6: Income tax payable during the period by MQG

Interpretation: By considering the above illustration it can be said that the firm has made

reduction in the taxes paid by them in current year as compared with last year. Hence, as per

audit of accounts the taxes will be seen as 484 in 2017 and 525 in 2016. Thus, it is a positive

result which will reflect the reduction on taxes levied in current year. Hence, in accordance with

the networking firm of PWC Australia the taxes for 2017 is 3082 and for 2016 it is 3297

respectively.

11

(a) Income tax expenses of MQG

The taxation will be charged over the revenue generated by Corporation during the years

can be as follows:

Illustration 6: Income tax payable during the period by MQG

Interpretation: By considering the above illustration it can be said that the firm has made

reduction in the taxes paid by them in current year as compared with last year. Hence, as per

audit of accounts the taxes will be seen as 484 in 2017 and 525 in 2016. Thus, it is a positive

result which will reflect the reduction on taxes levied in current year. Hence, in accordance with

the networking firm of PWC Australia the taxes for 2017 is 3082 and for 2016 it is 3297

respectively.

11

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

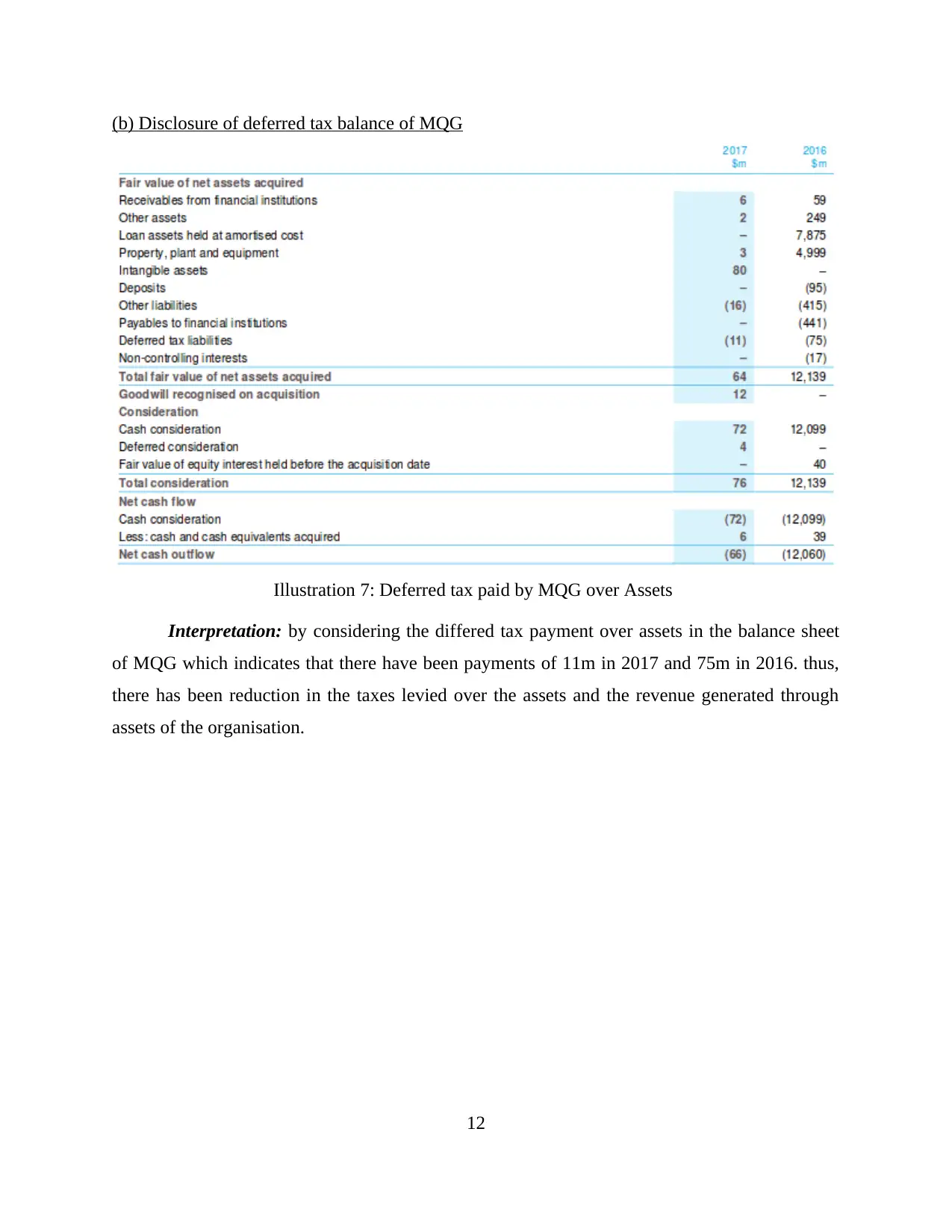

(b) Disclosure of deferred tax balance of MQG

Illustration 7: Deferred tax paid by MQG over Assets

Interpretation: by considering the differed tax payment over assets in the balance sheet

of MQG which indicates that there have been payments of 11m in 2017 and 75m in 2016. thus,

there has been reduction in the taxes levied over the assets and the revenue generated through

assets of the organisation.

12

Illustration 7: Deferred tax paid by MQG over Assets

Interpretation: by considering the differed tax payment over assets in the balance sheet

of MQG which indicates that there have been payments of 11m in 2017 and 75m in 2016. thus,

there has been reduction in the taxes levied over the assets and the revenue generated through

assets of the organisation.

12

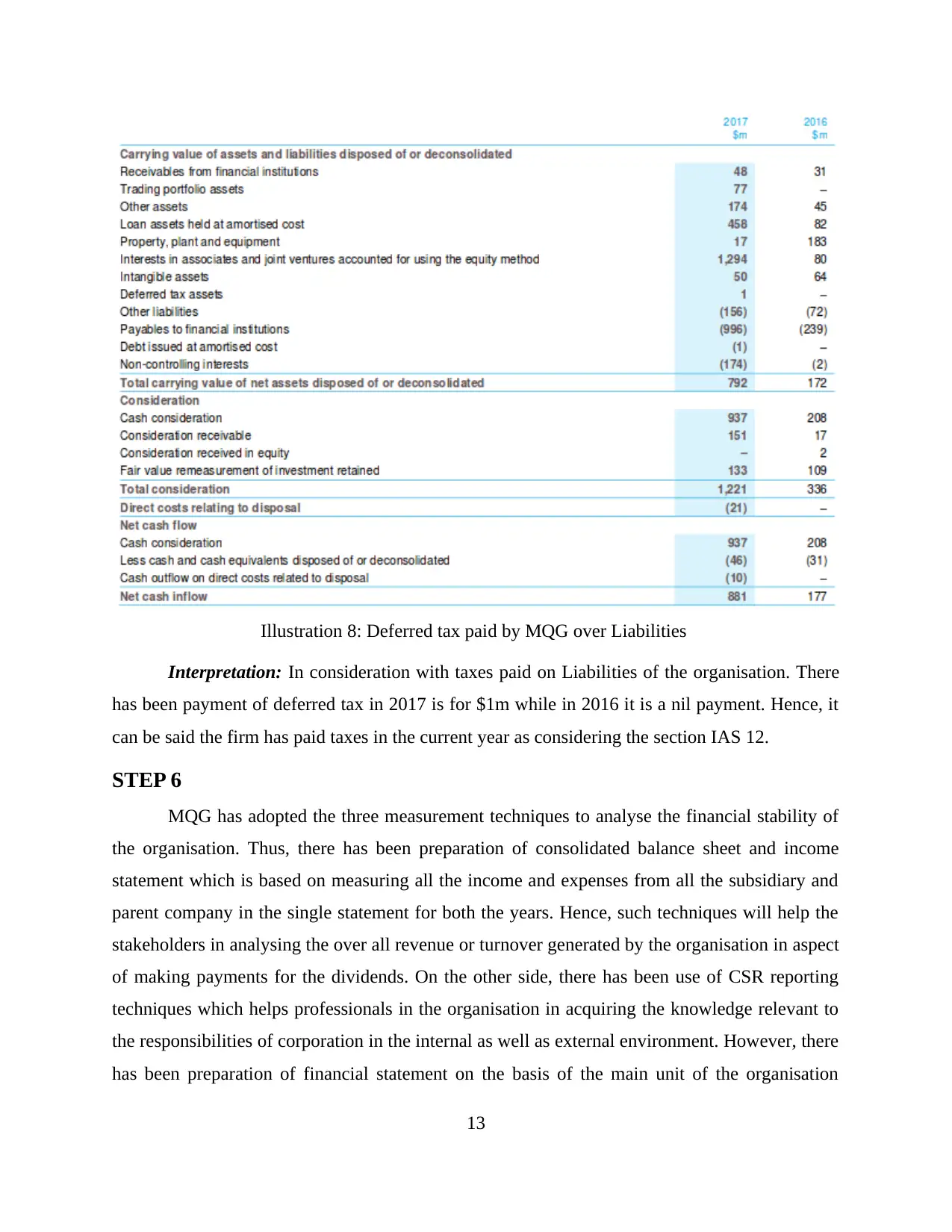

Illustration 8: Deferred tax paid by MQG over Liabilities

Interpretation: In consideration with taxes paid on Liabilities of the organisation. There

has been payment of deferred tax in 2017 is for $1m while in 2016 it is a nil payment. Hence, it

can be said the firm has paid taxes in the current year as considering the section IAS 12.

STEP 6

MQG has adopted the three measurement techniques to analyse the financial stability of

the organisation. Thus, there has been preparation of consolidated balance sheet and income

statement which is based on measuring all the income and expenses from all the subsidiary and

parent company in the single statement for both the years. Hence, such techniques will help the

stakeholders in analysing the over all revenue or turnover generated by the organisation in aspect

of making payments for the dividends. On the other side, there has been use of CSR reporting

techniques which helps professionals in the organisation in acquiring the knowledge relevant to

the responsibilities of corporation in the internal as well as external environment. However, there

has been preparation of financial statement on the basis of the main unit of the organisation

13

Interpretation: In consideration with taxes paid on Liabilities of the organisation. There

has been payment of deferred tax in 2017 is for $1m while in 2016 it is a nil payment. Hence, it

can be said the firm has paid taxes in the current year as considering the section IAS 12.

STEP 6

MQG has adopted the three measurement techniques to analyse the financial stability of

the organisation. Thus, there has been preparation of consolidated balance sheet and income

statement which is based on measuring all the income and expenses from all the subsidiary and

parent company in the single statement for both the years. Hence, such techniques will help the

stakeholders in analysing the over all revenue or turnover generated by the organisation in aspect

of making payments for the dividends. On the other side, there has been use of CSR reporting

techniques which helps professionals in the organisation in acquiring the knowledge relevant to

the responsibilities of corporation in the internal as well as external environment. However, there

has been preparation of financial statement on the basis of the main unit of the organisation

13

which provides detailed information regarding transaction held in the main firm during such

years.

STEP 7

(I) Relevant standard

There has been use of IFRS of IAS standards which are beneficial for the professionals in

preparing the relevant statements. Thus, it can be said that, with the help of such standards there

will be facilities of proper guidance as well as adequate framework which are universally

accepted by the accountant and auditors. Hence, such reporting techniques will be fruitful for the

shareholders in which they will be able to make the better judgement regarding investments and

dividends benefits from MQG.

(II) CPA module Financial reporting

By considering the CPA module the course tends to focus on the various categories in

context with preparation of financial statements such as:

Proper taxation

Reporting

Finance or funds

financial accounting

CONCLUSION

On the basis of above report there has been use of various kinds of techniques in

presenting the Financial reports of MQG for the period 2016-2017. Hence, as per the framework

and guidance facilitated by IAS and IFRS, professionals at MQG has prepared reports in

accordance with the same. Further, it can be said, while analysing the cash flow statement,

financial position as well as profit and loss report of the entity, it indicates the favourable

revenue gathering techniques. Thus, it can be said that such reporting techniques are beneficial

for the firm in having profitable growth as well as attracting the large numbers of stakeholders.

14

years.

STEP 7

(I) Relevant standard

There has been use of IFRS of IAS standards which are beneficial for the professionals in

preparing the relevant statements. Thus, it can be said that, with the help of such standards there

will be facilities of proper guidance as well as adequate framework which are universally

accepted by the accountant and auditors. Hence, such reporting techniques will be fruitful for the

shareholders in which they will be able to make the better judgement regarding investments and

dividends benefits from MQG.

(II) CPA module Financial reporting

By considering the CPA module the course tends to focus on the various categories in

context with preparation of financial statements such as:

Proper taxation

Reporting

Finance or funds

financial accounting

CONCLUSION

On the basis of above report there has been use of various kinds of techniques in

presenting the Financial reports of MQG for the period 2016-2017. Hence, as per the framework

and guidance facilitated by IAS and IFRS, professionals at MQG has prepared reports in

accordance with the same. Further, it can be said, while analysing the cash flow statement,

financial position as well as profit and loss report of the entity, it indicates the favourable

revenue gathering techniques. Thus, it can be said that such reporting techniques are beneficial

for the firm in having profitable growth as well as attracting the large numbers of stakeholders.

14

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

BIBLIOGRAPHY

https://static.macquarie.com/dafiles/Internet/mgl/global/shared/about/investors/results/2017/

Macquarie-Group-FY17-Annual-Report.pdf?v=2

http://www.ifrs.org/issued-standards/list-of-standards/ias-1-presentation-of-financial-statements/

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/professional-resources/

ifrs-factsheets/factsheet-ifrs15-revenue-from-contracts-with-customers.pdf?la=en

http://www.aasb.gov.au/admin/file/content105/c9/AASB15_12-14.pdf

http://www.ifrs.org/issued-standards/list-of-standards/ias-12-income-taxes/

https://www.cpacanada.ca/en/become-a-cpa/cpa-professional-education-program-becoming-a-

cpa/cpa-professional-education-program-core-modules/cpa-pep-core-1-module

15

https://static.macquarie.com/dafiles/Internet/mgl/global/shared/about/investors/results/2017/

Macquarie-Group-FY17-Annual-Report.pdf?v=2

http://www.ifrs.org/issued-standards/list-of-standards/ias-1-presentation-of-financial-statements/

https://www.cpaaustralia.com.au/~/media/corporate/allfiles/document/professional-resources/

ifrs-factsheets/factsheet-ifrs15-revenue-from-contracts-with-customers.pdf?la=en

http://www.aasb.gov.au/admin/file/content105/c9/AASB15_12-14.pdf

http://www.ifrs.org/issued-standards/list-of-standards/ias-12-income-taxes/

https://www.cpacanada.ca/en/become-a-cpa/cpa-professional-education-program-becoming-a-

cpa/cpa-professional-education-program-core-modules/cpa-pep-core-1-module

15

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.