Financial Statement Analysis Report

VerifiedAdded on 2023/04/17

|18

|3460

|404

AI Summary

This report aims at analyzing and understanding the material misstatement and restatement of financial information in the financial statement of an entity. For better utilization of financial information and better decision making the accounting system should be transparent and proper disclosure principles should be followed. In this report, the case study of Avid Technologies is chosen for analysis of those schools of accounting in the view of respective GAAP and IFRSs. Lastly, the paper concludes with some affects of such restatement and possible way outs for betterment of the financial reporting system.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Running head: FINANCIAL STATEMENT ANALYSIS REPORT

Avid Technology Inc.

ADM4342M

Hassan, Ali (8467946)

Hawari, Khaled (5887702)

Oladeji, Toluwalope (8287338)

Avid Technology Inc.

ADM4342M

Hassan, Ali (8467946)

Hawari, Khaled (5887702)

Oladeji, Toluwalope (8287338)

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

1FINANCIAL STATEMENT ANALYSIS REPORT

Executive Summary:

This report aims at analyzing and understanding the material misstatement and restatement of

financial information in the financial statement of an entity. For better utilization of financial

information and better decision making the accounting system should be transparent and proper

disclosure principles should be followed. In this report, the case study of Avid Technologies is

chosen for analysis of those schools of accounting in the view of respective GAAP and IFRSs.

Lastly, the paper concludes with some affects of such restatement and possible way outs for

betterment of the financial reporting system.

Executive Summary:

This report aims at analyzing and understanding the material misstatement and restatement of

financial information in the financial statement of an entity. For better utilization of financial

information and better decision making the accounting system should be transparent and proper

disclosure principles should be followed. In this report, the case study of Avid Technologies is

chosen for analysis of those schools of accounting in the view of respective GAAP and IFRSs.

Lastly, the paper concludes with some affects of such restatement and possible way outs for

betterment of the financial reporting system.

2FINANCIAL STATEMENT ANALYSIS REPORT

Table of Contents

Introduction:....................................................................................................................................3

Brief Overview of the Company:....................................................................................................3

Case study Material Misstatement/Restatement in the financial statement:....................................3

Applicable Accounting Standards:..................................................................................................5

Stock Market Reactions:..................................................................................................................6

Accounting Failure:.........................................................................................................................9

Usefulness of accounting Information:..........................................................................................11

Agency Theory:.............................................................................................................................11

Conclusion:....................................................................................................................................12

Appendix A:...................................................................................................................................13

References:....................................................................................................................................15

Table of Contents

Introduction:....................................................................................................................................3

Brief Overview of the Company:....................................................................................................3

Case study Material Misstatement/Restatement in the financial statement:....................................3

Applicable Accounting Standards:..................................................................................................5

Stock Market Reactions:..................................................................................................................6

Accounting Failure:.........................................................................................................................9

Usefulness of accounting Information:..........................................................................................11

Agency Theory:.............................................................................................................................11

Conclusion:....................................................................................................................................12

Appendix A:...................................................................................................................................13

References:....................................................................................................................................15

3FINANCIAL STATEMENT ANALYSIS REPORT

Introduction:

Accounting helps in measuring the financial and operational performance. Financial

statement is the ultimate output of the accounting system, which helps the stakeholders to make

certain important decisions. If there are any material restatement, misstatement and manipulation

in the financial statement that will affect the decision making process of the stakeholders, which

will lead them to suffer a loss. In this report, accounting restatement and misstatement is chosen

for analysis and understanding with a chosen company Avid Technology Inc for better analysis

and discussion of the topic.

Brief Overview of the Company:

Avid Technology Inc. is the world’s leading provider of audio and video technology for

media organizations and independent professionals.1 Avid provides solutions to create, distribute

and monetize films, videos, music recordings, TV shows, live concerts and news broadcasts in

the highly competitive and rapidly changing media industry. For 25 years now, Avid led the

revolution in non-linear editing and has become the leading technology provider and trusted

strategic partner for video and audio production, broadcast, live sound, shared storage and more.

Case study Material Misstatement/Restatement in the financial statement:

In March 2013, a shareholder of Avid Technology Inc. named Nick Di Vincenzo,

represented by Robbins Arroyo LLP, had filed a complaint in the US District Court for the

District of Massachusetts against Avid’s officers and directors. The complaint was concerning

the company’s violation of the Securities Exchange Act of 1993 between the periods of April 22,

2011 and February 22, 2013, known as the “Class Period”. Shareholder Nick Di Vincenzo

1“Avid Technology, Inc. Sued by Investor,” PR Newswire. March 29, 2013, http://www.prnewswire.com/news-releases/avid-technology-inc-

sued-by-investor-200635071.html. (accessed on February 11, 2019).

Introduction:

Accounting helps in measuring the financial and operational performance. Financial

statement is the ultimate output of the accounting system, which helps the stakeholders to make

certain important decisions. If there are any material restatement, misstatement and manipulation

in the financial statement that will affect the decision making process of the stakeholders, which

will lead them to suffer a loss. In this report, accounting restatement and misstatement is chosen

for analysis and understanding with a chosen company Avid Technology Inc for better analysis

and discussion of the topic.

Brief Overview of the Company:

Avid Technology Inc. is the world’s leading provider of audio and video technology for

media organizations and independent professionals.1 Avid provides solutions to create, distribute

and monetize films, videos, music recordings, TV shows, live concerts and news broadcasts in

the highly competitive and rapidly changing media industry. For 25 years now, Avid led the

revolution in non-linear editing and has become the leading technology provider and trusted

strategic partner for video and audio production, broadcast, live sound, shared storage and more.

Case study Material Misstatement/Restatement in the financial statement:

In March 2013, a shareholder of Avid Technology Inc. named Nick Di Vincenzo,

represented by Robbins Arroyo LLP, had filed a complaint in the US District Court for the

District of Massachusetts against Avid’s officers and directors. The complaint was concerning

the company’s violation of the Securities Exchange Act of 1993 between the periods of April 22,

2011 and February 22, 2013, known as the “Class Period”. Shareholder Nick Di Vincenzo

1“Avid Technology, Inc. Sued by Investor,” PR Newswire. March 29, 2013, http://www.prnewswire.com/news-releases/avid-technology-inc-

sued-by-investor-200635071.html. (accessed on February 11, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

4FINANCIAL STATEMENT ANALYSIS REPORT

believes that Avid failed to ensure adequate controls were in place to verify that the company’s

financial statements were accurate and complies with US Generally Accepted Accounting

Principles (GAAP). The complaint says, “since at least 2010, Avid has ignored GAAP

requirements and its own internal policies by repeatedly, prematurely recognizing revenues for

certain no-cost services that were not yet provided to its customers”.2 In addition, the complaint

alleges that Avid issued a series of materially false and misleading statements to investors

regarding the company’s business and operations to erroneously inflate revenues based on the

company’s improper revenue recognition policies. Specifically, the complaint alleges that

throughout the Class Period, Avid officials failed to apply the correct accounting principles to

the treatment of bug fixes, upgrades and enhancements provided by Avid and therefore, the

company failed to account for these software update services under US GAAP.3

By September 2014, Avid Technology Inc. finally announced the financial results for

2012, 2013 and the first quarter of 2014 following a lengthy financial restatement that resulted in

the company’s delisting from NASDAQ.4 This 18 months long internal accounting audit led to

the company not being able to file financial results with securities regulators, which ultimately

resulted in Avid’s stock being delisted from the NASDAQ Stock Market on February 25, 2014.

During this time, Avid refigured its accounting to mainly comply with new rules requiring

certain types of revenue associated with product upgrades to be accounted for over the period of

time when software updates were actually provided, rather than when original purchase

transactions took place.5

2Joe Zaller, “Avid Says its 2009 - 2011 Financial Statements No Longer Reliable,” Devoncroft. May 23, 2013,

http://blog.devoncroft.com/2013/05/23/avid-says-its-2009-2011-financial-statements-no-longer-reliable/. (accessed on February 16, 2019)).

3Joe Zaller, “Avid Says its 2009 - 2011 Financial Statements No Longer Reliable,” Devoncroft. May 23, 2013,

http://blog.devoncroft.com/2013/05/23/avid-says-its-2009-2011-financial-statements-no-longer-reliable/. (accessed on February 16, 2019)).

4Joe Zaller, “Avid Says its 2009 - 2011 Financial Statements No Longer Reliable,” Devoncroft. May 23, 2013,

http://blog.devoncroft.com/2013/05/23/avid-says-its-2009-2011-financial-statements-no-longer-reliable/. (accessed on February 18, 2019).

5Alex Lawson, “Avid Hit With Derivative Suit Over Accounting Irregularities,” Law360. June 27, 2013,

http://www.law360.com/articles/453302/avid-hit-with-derivative-suit-over-accounting-irregularities. (accessed on February 11, 2019).

believes that Avid failed to ensure adequate controls were in place to verify that the company’s

financial statements were accurate and complies with US Generally Accepted Accounting

Principles (GAAP). The complaint says, “since at least 2010, Avid has ignored GAAP

requirements and its own internal policies by repeatedly, prematurely recognizing revenues for

certain no-cost services that were not yet provided to its customers”.2 In addition, the complaint

alleges that Avid issued a series of materially false and misleading statements to investors

regarding the company’s business and operations to erroneously inflate revenues based on the

company’s improper revenue recognition policies. Specifically, the complaint alleges that

throughout the Class Period, Avid officials failed to apply the correct accounting principles to

the treatment of bug fixes, upgrades and enhancements provided by Avid and therefore, the

company failed to account for these software update services under US GAAP.3

By September 2014, Avid Technology Inc. finally announced the financial results for

2012, 2013 and the first quarter of 2014 following a lengthy financial restatement that resulted in

the company’s delisting from NASDAQ.4 This 18 months long internal accounting audit led to

the company not being able to file financial results with securities regulators, which ultimately

resulted in Avid’s stock being delisted from the NASDAQ Stock Market on February 25, 2014.

During this time, Avid refigured its accounting to mainly comply with new rules requiring

certain types of revenue associated with product upgrades to be accounted for over the period of

time when software updates were actually provided, rather than when original purchase

transactions took place.5

2Joe Zaller, “Avid Says its 2009 - 2011 Financial Statements No Longer Reliable,” Devoncroft. May 23, 2013,

http://blog.devoncroft.com/2013/05/23/avid-says-its-2009-2011-financial-statements-no-longer-reliable/. (accessed on February 16, 2019)).

3Joe Zaller, “Avid Says its 2009 - 2011 Financial Statements No Longer Reliable,” Devoncroft. May 23, 2013,

http://blog.devoncroft.com/2013/05/23/avid-says-its-2009-2011-financial-statements-no-longer-reliable/. (accessed on February 16, 2019)).

4Joe Zaller, “Avid Says its 2009 - 2011 Financial Statements No Longer Reliable,” Devoncroft. May 23, 2013,

http://blog.devoncroft.com/2013/05/23/avid-says-its-2009-2011-financial-statements-no-longer-reliable/. (accessed on February 18, 2019).

5Alex Lawson, “Avid Hit With Derivative Suit Over Accounting Irregularities,” Law360. June 27, 2013,

http://www.law360.com/articles/453302/avid-hit-with-derivative-suit-over-accounting-irregularities. (accessed on February 11, 2019).

5FINANCIAL STATEMENT ANALYSIS REPORT

Applicable Accounting Standards:

Revenue recognition is an integral part of accounting standards. The primary issue in

accounting for revenue revolves around the timing of the recognition of revenue. Avid

Technology Inc. prematurely recognized revenue for no-cost services. There are 2 set of

globally accepted standards: GAAP and IFRS. Under US GAAP, there are 2 levels of guidance:6

Level I – guidance in Concepts Statements, Concept Statement No. 6, Concept Statement

No. 5. (Level I define revenue as well as describing the basic criteria for revenue

recognition

Level II – guidance in certain industries as well as economically different transactions

The FASB defines revenues as “[…]inflows or other enhancement of assets of an entity or

settlements of its liabilities from delivering or producing goods, rendering services, or other

activities that constitute the entity's ́ s ongoing major or central operations” (2009).

On May 28, 2014, the FASB issued Accounting Update (ASU) 2014-09, Revenue from

Contracts with Customers. The standard will eliminate the “[…]transaction- and industry-

specific revenue recognition guidance under current US GAAP and replace it with a principle

based approach for determining revenue recognition”.7

The new accounting standard stipulates that to achieve the core principle, an entity should follow

these steps:8

1. Identify the contract with a customer

2. Identify the performance obligations in the contract

3. Determine the transaction price

6Hana Bohusova, “Revenue Recognition under US GAAP and IFRS Comparison,”

http://acct5183group7.wikispaces.com/file/view/revenue+recognition+-+GAAP+vs+IFRS.pdf. (accessed on February 11, 2019).

7AICPA. http://www.aicpa.org/interestareas/frc/accountingfinancialreporting/revenuerecognition/pages/revenuerecognition.aspx. (accessed on

February 12, 2019).

8AICPA. http://www.aicpa.org/interestareas/frc/accountingfinancialreporting/revenuerecognition/pages/revenuerecognition.aspx. (accessed on

February 17, 2019).

Applicable Accounting Standards:

Revenue recognition is an integral part of accounting standards. The primary issue in

accounting for revenue revolves around the timing of the recognition of revenue. Avid

Technology Inc. prematurely recognized revenue for no-cost services. There are 2 set of

globally accepted standards: GAAP and IFRS. Under US GAAP, there are 2 levels of guidance:6

Level I – guidance in Concepts Statements, Concept Statement No. 6, Concept Statement

No. 5. (Level I define revenue as well as describing the basic criteria for revenue

recognition

Level II – guidance in certain industries as well as economically different transactions

The FASB defines revenues as “[…]inflows or other enhancement of assets of an entity or

settlements of its liabilities from delivering or producing goods, rendering services, or other

activities that constitute the entity's ́ s ongoing major or central operations” (2009).

On May 28, 2014, the FASB issued Accounting Update (ASU) 2014-09, Revenue from

Contracts with Customers. The standard will eliminate the “[…]transaction- and industry-

specific revenue recognition guidance under current US GAAP and replace it with a principle

based approach for determining revenue recognition”.7

The new accounting standard stipulates that to achieve the core principle, an entity should follow

these steps:8

1. Identify the contract with a customer

2. Identify the performance obligations in the contract

3. Determine the transaction price

6Hana Bohusova, “Revenue Recognition under US GAAP and IFRS Comparison,”

http://acct5183group7.wikispaces.com/file/view/revenue+recognition+-+GAAP+vs+IFRS.pdf. (accessed on February 11, 2019).

7AICPA. http://www.aicpa.org/interestareas/frc/accountingfinancialreporting/revenuerecognition/pages/revenuerecognition.aspx. (accessed on

February 12, 2019).

8AICPA. http://www.aicpa.org/interestareas/frc/accountingfinancialreporting/revenuerecognition/pages/revenuerecognition.aspx. (accessed on

February 17, 2019).

6FINANCIAL STATEMENT ANALYSIS REPORT

4. Allocate the transaction price

5. Recognize revenue when or as the entity satisfies a performance obligation

On the other hand, IAS 18 standards deals with revenue recognition. IFRS defines

income as a concept that includes both revenues and gains. Revenue arises from the ordinary

activities that an enterprise accomplishes and is also referred to under the names of sales, fees,

interest, dividends, royalties and rent. Moreover, the recognition of revenues depends on

whether these 2 criteria are met:9

It is probable that any future economic benefit associated with the item of revenue will

flow to the entity, and

The amount of revenue can be measured with reliability. Specific rules are in place under

both GAAP and IFRS regarding treatments of complex transactions on how to properly

recognize revenue.

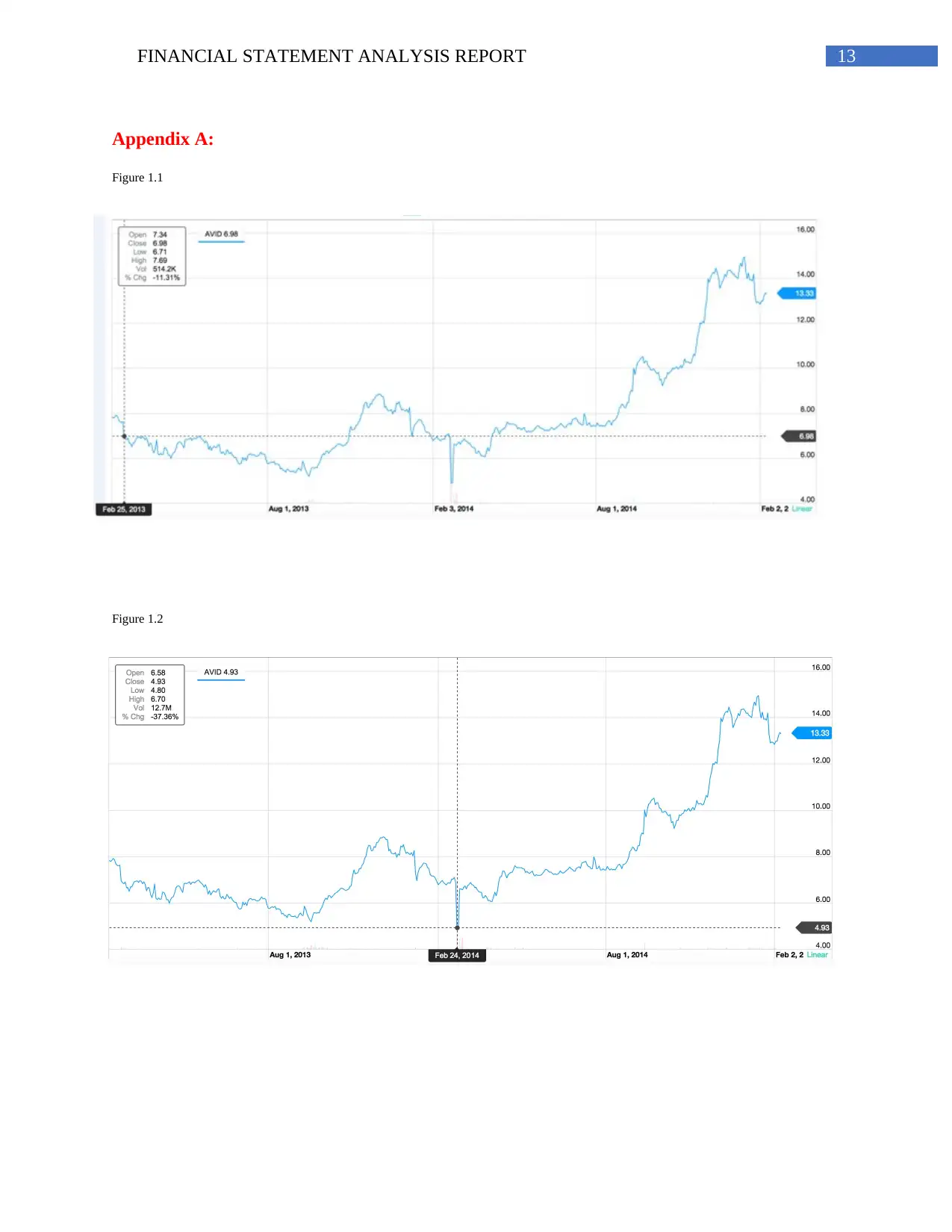

Stock Market Reactions:

On February 25, 2013, Avid Technology Inc. announced in its press release that it was

going to postpone its fourth quarter 2012 earnings release and investor conference call. The

decision to postpone was due to the company needing additional time to evaluate its current and

historical accounting treatment related to bug fixes, upgrades and enhancements to selected

products.10 An accounting treatment evaluation steamed from the company’s financial results

review for the fourth quarter for the year ended 2012. Following the release of the press

statement, Avid’s shares dropped 9 per cent, closing at $6.98 per share on February 25, 2013 as

shown in figure 1.1 in Appendix A.

9IASPlus. http://www.iasplus.com/en/standards/ias/ias18. (accessed on February 13, 2019).

10“Avid Postpones its Fourth Quarter Earnings Release,” Avid. February 25, 2011, http://ir.avid.com/releasedetail.cfm?ReleaseID=742786.

(accessed on March3, 2019).

4. Allocate the transaction price

5. Recognize revenue when or as the entity satisfies a performance obligation

On the other hand, IAS 18 standards deals with revenue recognition. IFRS defines

income as a concept that includes both revenues and gains. Revenue arises from the ordinary

activities that an enterprise accomplishes and is also referred to under the names of sales, fees,

interest, dividends, royalties and rent. Moreover, the recognition of revenues depends on

whether these 2 criteria are met:9

It is probable that any future economic benefit associated with the item of revenue will

flow to the entity, and

The amount of revenue can be measured with reliability. Specific rules are in place under

both GAAP and IFRS regarding treatments of complex transactions on how to properly

recognize revenue.

Stock Market Reactions:

On February 25, 2013, Avid Technology Inc. announced in its press release that it was

going to postpone its fourth quarter 2012 earnings release and investor conference call. The

decision to postpone was due to the company needing additional time to evaluate its current and

historical accounting treatment related to bug fixes, upgrades and enhancements to selected

products.10 An accounting treatment evaluation steamed from the company’s financial results

review for the fourth quarter for the year ended 2012. Following the release of the press

statement, Avid’s shares dropped 9 per cent, closing at $6.98 per share on February 25, 2013 as

shown in figure 1.1 in Appendix A.

9IASPlus. http://www.iasplus.com/en/standards/ias/ias18. (accessed on February 13, 2019).

10“Avid Postpones its Fourth Quarter Earnings Release,” Avid. February 25, 2011, http://ir.avid.com/releasedetail.cfm?ReleaseID=742786.

(accessed on March3, 2019).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL STATEMENT ANALYSIS REPORT

On March 21, 2013, Avid announced that due to the company being unable to file its

annual report on Form 10-K, the company received a notification letter from the NASDAQ

Listing Qualifications Department to inform the company that it was no longer in compliance

with the NASDAQ Marketplace Rule 5350(c)(1). Failure to issue financial statement in

accordance with the Securities and Exchange Commission on a timely basis could cause the

company to be delisted from the NASDAQ Global Select Market. On the same day that Avid

received the letter from NASDAQ, it informed the NASDAQ Listing Qualifications Department

that it was continuing its investigation to determine whether certain Software Updates previously

thought to be only bug fixes met the definition of post-contract customer support under US

GAAP.11 Following the release of this press statement, Avid’s shares dropped 3.81 per cent,

closing at $6.56 per share on March 22, 2013.

On April 22, 2013, Avid announces new Chief Financial Officer, John Federick. The

company did not mention whether former Chief Financial Officer, Ken Sexton, had a significant

role in the misstatements of financial positions.12 As stated earlier, Avid reported unable to file

Form 10-K because of a lengthy accounting treatment evaluation within the company. On May

21, 2013, Avid published the conclusions to the evaluation in a press release. The company

concluded “that certain of the no-charge Software Updates should have been accounted for as

implied post-contract customer support when recognizing revenue for the original sale of the

related product. […] the company’s unaudited interim consolidated financial statements for the

quarterly periods ended (i) September 30, 2012 and 2011, (ii) June 30, 2012 and 2011, (iii)

March 31, 2012 and 2011, as well as its audited consolidated financial statements for the three

years ended December 31, 2011, 2010, and 2009 should no longer be relied upon because of

11“Avid Announces Receipt of Anticipated NASDAQ Letter,” Avid. March 21, 2013, http://ir.avid.com/releasedetail.cfm?ReleaseID=750188.

(accessed on March 11, 2019).

12“Avid Announces New Chief Financial Officer,” Avid. April 22, 2013, http://ir.avid.com/releasedetail.cfm?ReleaseID=758125. (accessed on

March8, 2019).

On March 21, 2013, Avid announced that due to the company being unable to file its

annual report on Form 10-K, the company received a notification letter from the NASDAQ

Listing Qualifications Department to inform the company that it was no longer in compliance

with the NASDAQ Marketplace Rule 5350(c)(1). Failure to issue financial statement in

accordance with the Securities and Exchange Commission on a timely basis could cause the

company to be delisted from the NASDAQ Global Select Market. On the same day that Avid

received the letter from NASDAQ, it informed the NASDAQ Listing Qualifications Department

that it was continuing its investigation to determine whether certain Software Updates previously

thought to be only bug fixes met the definition of post-contract customer support under US

GAAP.11 Following the release of this press statement, Avid’s shares dropped 3.81 per cent,

closing at $6.56 per share on March 22, 2013.

On April 22, 2013, Avid announces new Chief Financial Officer, John Federick. The

company did not mention whether former Chief Financial Officer, Ken Sexton, had a significant

role in the misstatements of financial positions.12 As stated earlier, Avid reported unable to file

Form 10-K because of a lengthy accounting treatment evaluation within the company. On May

21, 2013, Avid published the conclusions to the evaluation in a press release. The company

concluded “that certain of the no-charge Software Updates should have been accounted for as

implied post-contract customer support when recognizing revenue for the original sale of the

related product. […] the company’s unaudited interim consolidated financial statements for the

quarterly periods ended (i) September 30, 2012 and 2011, (ii) June 30, 2012 and 2011, (iii)

March 31, 2012 and 2011, as well as its audited consolidated financial statements for the three

years ended December 31, 2011, 2010, and 2009 should no longer be relied upon because of

11“Avid Announces Receipt of Anticipated NASDAQ Letter,” Avid. March 21, 2013, http://ir.avid.com/releasedetail.cfm?ReleaseID=750188.

(accessed on March 11, 2019).

12“Avid Announces New Chief Financial Officer,” Avid. April 22, 2013, http://ir.avid.com/releasedetail.cfm?ReleaseID=758125. (accessed on

March8, 2019).

8FINANCIAL STATEMENT ANALYSIS REPORT

these errors in the application of GAAP.”13 In the same press release, Avid mentions that

although reported revenues for each period will be impacted by restatement adjustments, total

revenue to be earned, the amount of cash received or that will be received, the company’s

liquidity and prior period cash flow will not be affected.

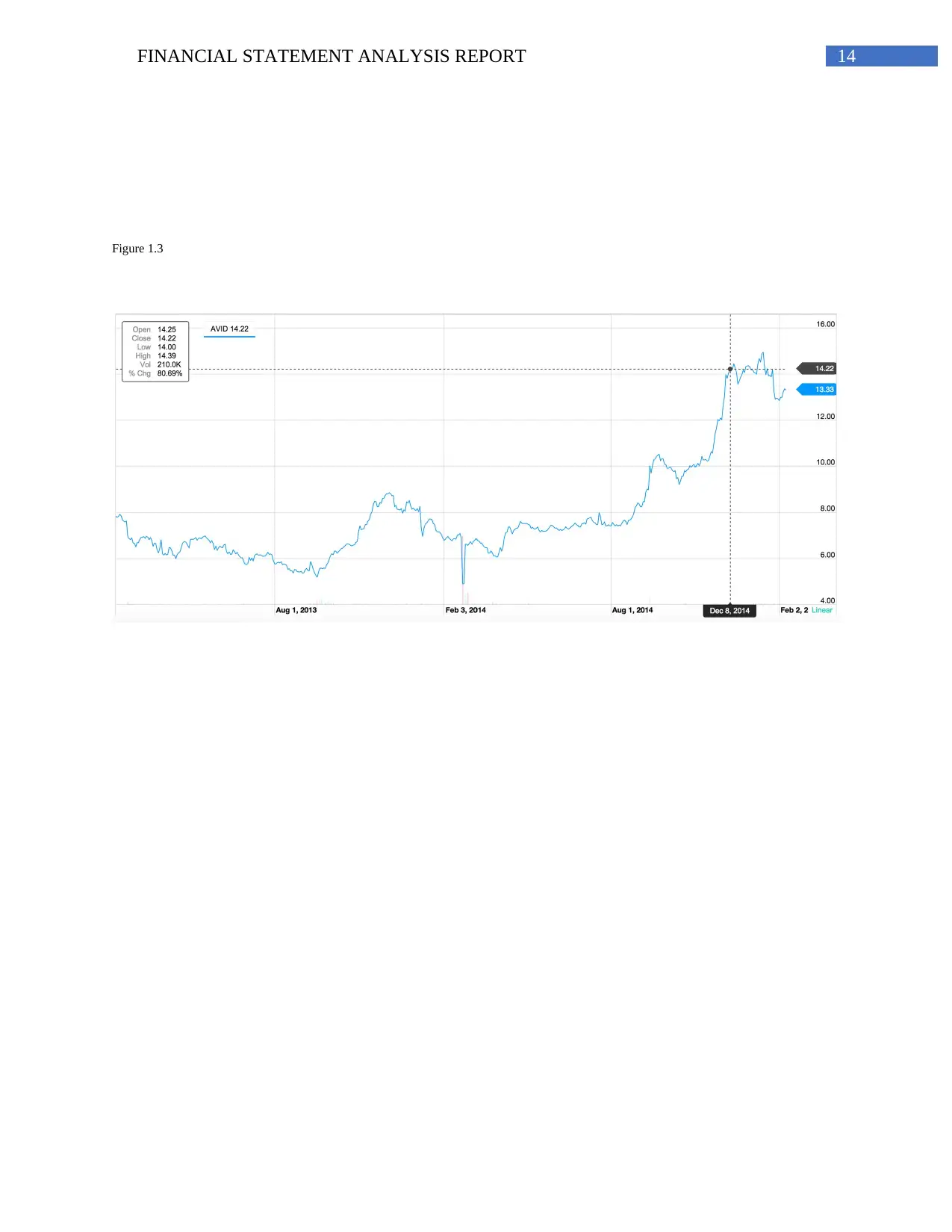

Despite Avid being granted an exception to regain compliance by the NASDAQ Listing

Qualifications Panel, the company was unable to avoid being delisted.14 On February 21, 2014,

NASDAQ delisted Avid’s shares and suspended trading, effective February 25, 2014.15 As

shown in Figure 1.2 in Appendix A, Avid’s shares were at their lowest on February 24, 2014 (the

day before the company was delisted). The company’s shares dropped 34.96%, opening at $6.58

per share and closing at $4.93. Avid had anticipated being delisted prior to receiving the

NASDAQ delist letter and were proactively taking the necessary measures to get the company

trading in the open market again.

On January 7, 2014, prior to being delisted, Avid announced that Deloitte &Touche LLP will be

its new auditor firm to succeed Ernst & Young LLP.16 This was a necessary transition to reassure

the public that the company was making an effort to strengthen their management control

system. On August 13, 2014, the company announced its plans to file Form 10-K for the fiscal

year ended 2013 within the following four weeks.17 The company was able to accomplish this

and was well-rewarded. On December 4, 2014, received a notice that the company will be listed

13“Avid Announces Receipt of Second Anticipated NASDAQ Letter and Initial Determinations of its Accounting Evaluation,” Avid. May 21,

2013, http://ir.avid.com/releasedetail.cfm?ReleaseID=766370. (accessed on March 9, 2019).

14“Delisting of Avid Stock Stayed Through NASDAQ Hearing Process,” Avid. September 18, 2013, http://ir.avid.com/releasedetail.cfm?

ReleaseID=791591. (accessed on March 11, 2019).

15Avid Receives Anticipated NASDAQ Delist Letter,” Avid. February 24, 2014, http://ir.avid.com/releasedetail.cfm?ReleaseID=827707.

(accessed on February 11, 2015).

16 “Avid Announces Appointment of Deloitte &Touche as New Audit Firm,” Avid. January 7, 2014, http://ir.avid.com/releasedetail.cfm?

ReleaseID=817675. (accessed on March 11, 2019).

17 “Avid Announces New Timeline for Restatement,” Avid. August 13, 2014, http://ir.avid.com/releasedetail.cfm?ReleaseID=866020.

(accessed on March 11, 2019).

these errors in the application of GAAP.”13 In the same press release, Avid mentions that

although reported revenues for each period will be impacted by restatement adjustments, total

revenue to be earned, the amount of cash received or that will be received, the company’s

liquidity and prior period cash flow will not be affected.

Despite Avid being granted an exception to regain compliance by the NASDAQ Listing

Qualifications Panel, the company was unable to avoid being delisted.14 On February 21, 2014,

NASDAQ delisted Avid’s shares and suspended trading, effective February 25, 2014.15 As

shown in Figure 1.2 in Appendix A, Avid’s shares were at their lowest on February 24, 2014 (the

day before the company was delisted). The company’s shares dropped 34.96%, opening at $6.58

per share and closing at $4.93. Avid had anticipated being delisted prior to receiving the

NASDAQ delist letter and were proactively taking the necessary measures to get the company

trading in the open market again.

On January 7, 2014, prior to being delisted, Avid announced that Deloitte &Touche LLP will be

its new auditor firm to succeed Ernst & Young LLP.16 This was a necessary transition to reassure

the public that the company was making an effort to strengthen their management control

system. On August 13, 2014, the company announced its plans to file Form 10-K for the fiscal

year ended 2013 within the following four weeks.17 The company was able to accomplish this

and was well-rewarded. On December 4, 2014, received a notice that the company will be listed

13“Avid Announces Receipt of Second Anticipated NASDAQ Letter and Initial Determinations of its Accounting Evaluation,” Avid. May 21,

2013, http://ir.avid.com/releasedetail.cfm?ReleaseID=766370. (accessed on March 9, 2019).

14“Delisting of Avid Stock Stayed Through NASDAQ Hearing Process,” Avid. September 18, 2013, http://ir.avid.com/releasedetail.cfm?

ReleaseID=791591. (accessed on March 11, 2019).

15Avid Receives Anticipated NASDAQ Delist Letter,” Avid. February 24, 2014, http://ir.avid.com/releasedetail.cfm?ReleaseID=827707.

(accessed on February 11, 2015).

16 “Avid Announces Appointment of Deloitte &Touche as New Audit Firm,” Avid. January 7, 2014, http://ir.avid.com/releasedetail.cfm?

ReleaseID=817675. (accessed on March 11, 2019).

17 “Avid Announces New Timeline for Restatement,” Avid. August 13, 2014, http://ir.avid.com/releasedetail.cfm?ReleaseID=866020.

(accessed on March 11, 2019).

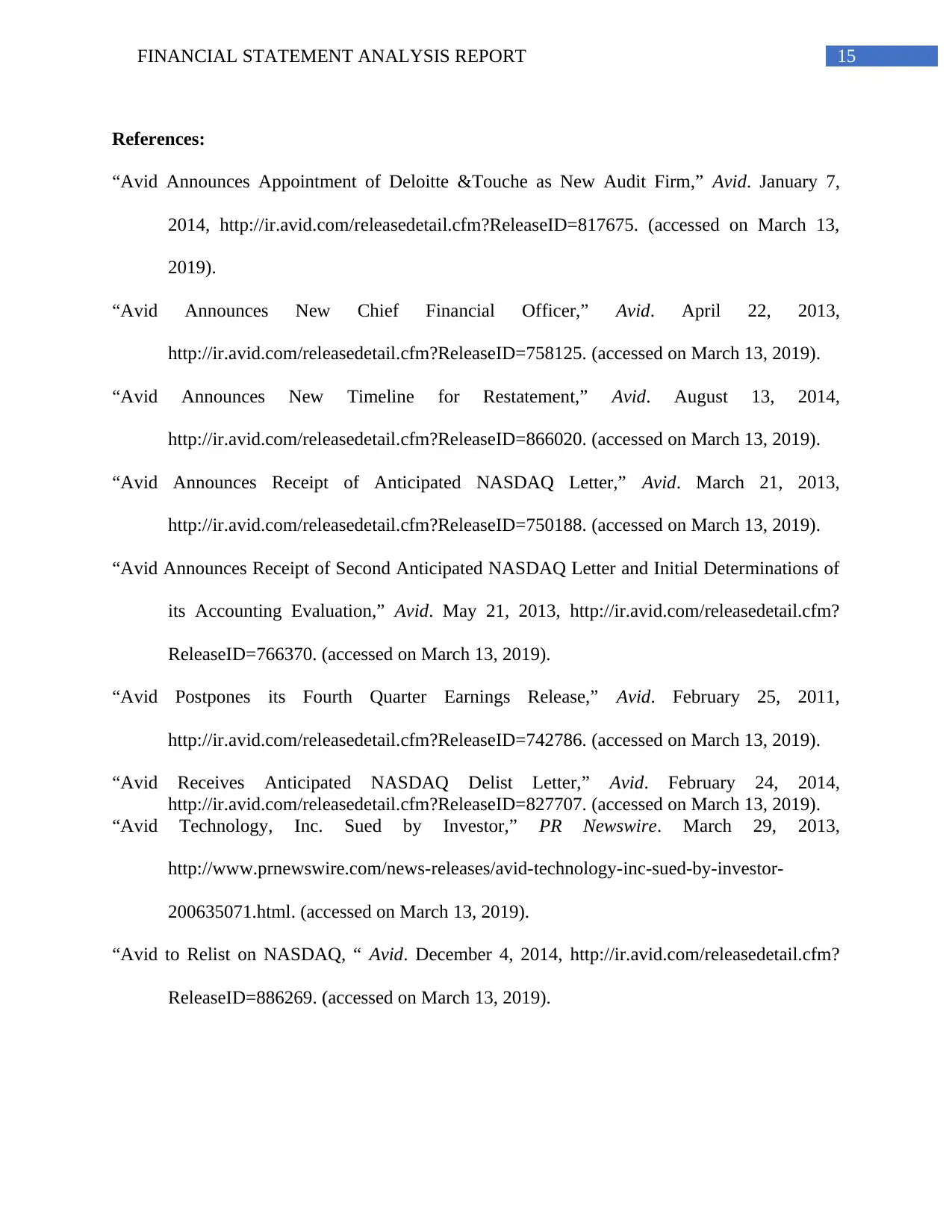

9FINANCIAL STATEMENT ANALYSIS REPORT

on the NASDAQ Stock Market effective with the open of trading on December 8, 2014.18 On

December 8, 2014, Avid opened at $13.39 per share, the company’s shares were not worth this

much since early July of 2011 (refer to Figure 1.3 in Appendix A).

Accounting Failure:

Avid Technology Inc. failed to report its bug fixes, enhancements and software updates

that it provided to customers in the correct fashion.19 This lead to accounting misstatements in

Avid’s revenue account and subsequently Avid needed to restate its reports comprising its value

on the stock market and its legitimacy in following reporting standards. Financial statements

from 2009 until 2011 were no longer to be relied upon because of these accounting errors

committed by Avid.20 The issue that was the main concern of Avid’s statements was “whether

software updates previously made available by the company to certain of its customers at no-

charge included upgrades, enhancements or compatibility extensions and if so, whether such

upgrades, enhancements or compatibility extensions met the definition of post-contract customer

support (PCS) under U.S. Generally Accepted Accounting Principles (“GAAP”).”21 The

adjustments that were needed to be made not only affected the revenue account and when

revenue should be recognized but also, would have an impact on income taxes.22 In essence,

Avid was claiming revenue for non-cost services that had not yet been provided to customers.23

This lead to revenue consistently being overstated.

18“Avid to Relist on NASDAQ, “ Avid. December 4, 2014, http://ir.avid.com/releasedetail.cfm?ReleaseID=886269. (accessed on March 11,

2019)

19Avid. http://www.avid.com/US/about.html. (accessed onMarch 13, 2019).

20Alex Lawson, “Avid Hit With Derivative Suit Over Accounting Irregularities,” Law360. June 27, 2013,

http://www.law360.com/articles/453302/avid-hit-with-derivative-suit-over-accounting-irregularities. (accessed on February 11, 2019).

21“Avid Technology, Inc. Sued by Investor,” PR Newswire. March 29, 2013, http://www.prnewswire.com/news-releases/avid-technology-inc-

sued-by-investor-200635071.html. (accessed on March 13, 2019).

22Bryant Frazer, “Avid Talks Growth Strategy As It Completes Financial Restatement,” StudioDaily. September 24, 2014,

http://www.studiodaily.com/2014/09/avid-talks-growth-strategy-as-it-completes-financial-restatement/. (accessed on March 13, 2019).

23Bryant Frazer, “Avid Talks Growth Strategy As It Completes Financial Restatement,” StudioDaily. September 24, 2014,

http://www.studiodaily.com/2014/09/avid-talks-growth-strategy-as-it-completes-financial-restatement/. (accessed on March 13, 2019).

on the NASDAQ Stock Market effective with the open of trading on December 8, 2014.18 On

December 8, 2014, Avid opened at $13.39 per share, the company’s shares were not worth this

much since early July of 2011 (refer to Figure 1.3 in Appendix A).

Accounting Failure:

Avid Technology Inc. failed to report its bug fixes, enhancements and software updates

that it provided to customers in the correct fashion.19 This lead to accounting misstatements in

Avid’s revenue account and subsequently Avid needed to restate its reports comprising its value

on the stock market and its legitimacy in following reporting standards. Financial statements

from 2009 until 2011 were no longer to be relied upon because of these accounting errors

committed by Avid.20 The issue that was the main concern of Avid’s statements was “whether

software updates previously made available by the company to certain of its customers at no-

charge included upgrades, enhancements or compatibility extensions and if so, whether such

upgrades, enhancements or compatibility extensions met the definition of post-contract customer

support (PCS) under U.S. Generally Accepted Accounting Principles (“GAAP”).”21 The

adjustments that were needed to be made not only affected the revenue account and when

revenue should be recognized but also, would have an impact on income taxes.22 In essence,

Avid was claiming revenue for non-cost services that had not yet been provided to customers.23

This lead to revenue consistently being overstated.

18“Avid to Relist on NASDAQ, “ Avid. December 4, 2014, http://ir.avid.com/releasedetail.cfm?ReleaseID=886269. (accessed on March 11,

2019)

19Avid. http://www.avid.com/US/about.html. (accessed onMarch 13, 2019).

20Alex Lawson, “Avid Hit With Derivative Suit Over Accounting Irregularities,” Law360. June 27, 2013,

http://www.law360.com/articles/453302/avid-hit-with-derivative-suit-over-accounting-irregularities. (accessed on February 11, 2019).

21“Avid Technology, Inc. Sued by Investor,” PR Newswire. March 29, 2013, http://www.prnewswire.com/news-releases/avid-technology-inc-

sued-by-investor-200635071.html. (accessed on March 13, 2019).

22Bryant Frazer, “Avid Talks Growth Strategy As It Completes Financial Restatement,” StudioDaily. September 24, 2014,

http://www.studiodaily.com/2014/09/avid-talks-growth-strategy-as-it-completes-financial-restatement/. (accessed on March 13, 2019).

23Bryant Frazer, “Avid Talks Growth Strategy As It Completes Financial Restatement,” StudioDaily. September 24, 2014,

http://www.studiodaily.com/2014/09/avid-talks-growth-strategy-as-it-completes-financial-restatement/. (accessed on March 13, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

10FINANCIAL STATEMENT ANALYSIS REPORT

According to IFRS / ASPE revenue for PCS should not be recognized immediately after

the sale is made.24 This is due to revenue timing issues, the PCS will be provided over the life of

the contract and henceforth it would be viewed as inappropriate to be claiming the revenue from

such service before it has actually been performed. If a recognized fair value for the PCS exists

then the company should be using such value when determining how much revenue it should not

yet be claiming.25If a transaction for $2000 occurs for a software license and the PCS is offered

separately on the market for external purchase for $300 then the company should only be

recognizing $1700 in revenue for that sale.26If a transaction for $2000 occurs for a software

license and the PCS is not offered separately on the market then reasonable and reliable

estimates need to be made in order to determine how much revenue can actually be claimed for

that period.27In this case the company would need to wait until evidence exists to revise its

estimate or determine the fair value of the software sold as a standalone option without any PCS.

Avid ignored one of the basic fundamentals of revenue recognition which is timing and as such it

resulted in an accounting failure.

Usefulness of accounting Information:

The result of the whole accounting system is some meaningful accounting information. It

is prepared for the users of financial information who will be using it for various important

decisions making. In this context, the usefulness of accounting information is very important. If

the information are meaningless or includes any material misstatement or restatement, it will lead

the users in wrong interpretation of financial performance and position of the business and faulty

24Hana Bohusova, “Revenue Recognition Under US GAAP and IFRS Comparison,”

http://acct5183group7.wikispaces.com/file/view/revenue+recognition+-+GAAP+vs+IFRS.pdf. (accessed on March 13, 2019).

25“Expert Access Seminar Series: Revenue Recognition,” PriceWaterHouseCooper.

http://www.pwc.com/ca/en/emerging-company/publications/pwc-revenue-recognition-2012-04-en.pdf. (accessed on March 13, 2019).

26“Expert Access Seminar Series: Revenue Recognition,” PriceWaterHouseCooper.

http://www.pwc.com/ca/en/emerging-company/publications/pwc-revenue-recognition-2012-04-en.pdf. (accessed on March 13, 2019).

27“Expert Access Seminar Series: Revenue Recognition,” PriceWaterHouseCooper.

http://www.pwc.com/ca/en/emerging-company/publications/pwc-revenue-recognition-2012-04-en.pdf. (accessed on March 13, 2019).

According to IFRS / ASPE revenue for PCS should not be recognized immediately after

the sale is made.24 This is due to revenue timing issues, the PCS will be provided over the life of

the contract and henceforth it would be viewed as inappropriate to be claiming the revenue from

such service before it has actually been performed. If a recognized fair value for the PCS exists

then the company should be using such value when determining how much revenue it should not

yet be claiming.25If a transaction for $2000 occurs for a software license and the PCS is offered

separately on the market for external purchase for $300 then the company should only be

recognizing $1700 in revenue for that sale.26If a transaction for $2000 occurs for a software

license and the PCS is not offered separately on the market then reasonable and reliable

estimates need to be made in order to determine how much revenue can actually be claimed for

that period.27In this case the company would need to wait until evidence exists to revise its

estimate or determine the fair value of the software sold as a standalone option without any PCS.

Avid ignored one of the basic fundamentals of revenue recognition which is timing and as such it

resulted in an accounting failure.

Usefulness of accounting Information:

The result of the whole accounting system is some meaningful accounting information. It

is prepared for the users of financial information who will be using it for various important

decisions making. In this context, the usefulness of accounting information is very important. If

the information are meaningless or includes any material misstatement or restatement, it will lead

the users in wrong interpretation of financial performance and position of the business and faulty

24Hana Bohusova, “Revenue Recognition Under US GAAP and IFRS Comparison,”

http://acct5183group7.wikispaces.com/file/view/revenue+recognition+-+GAAP+vs+IFRS.pdf. (accessed on March 13, 2019).

25“Expert Access Seminar Series: Revenue Recognition,” PriceWaterHouseCooper.

http://www.pwc.com/ca/en/emerging-company/publications/pwc-revenue-recognition-2012-04-en.pdf. (accessed on March 13, 2019).

26“Expert Access Seminar Series: Revenue Recognition,” PriceWaterHouseCooper.

http://www.pwc.com/ca/en/emerging-company/publications/pwc-revenue-recognition-2012-04-en.pdf. (accessed on March 13, 2019).

27“Expert Access Seminar Series: Revenue Recognition,” PriceWaterHouseCooper.

http://www.pwc.com/ca/en/emerging-company/publications/pwc-revenue-recognition-2012-04-en.pdf. (accessed on March 13, 2019).

11FINANCIAL STATEMENT ANALYSIS REPORT

decision based on such a wrong interpretation. In the case study of Avid Technology Inc, such an

instance can be found, where they have materially misstated certain financial information in their

financial statement.

Agency Theory:

Agency theory in corporate governance, describes the principal and agent relationship

between the management of an organisation and the owners of the organisation. Shareholders are

the real owner of the business, but not all of them can participate in the operation and

management of the business. On behalf of the owners, management manages the whole

operations of the business and strive to achieve the overall organisational goal. The management

works as the agent to the owners of the business, they need to protect the shareholders’ interest

with their efficient performance and transparent accounting and reporting policies. If the

management makes any manipulation or misstatement in the financial statement of the company

then the shareholders’ interest gets affected.

decision based on such a wrong interpretation. In the case study of Avid Technology Inc, such an

instance can be found, where they have materially misstated certain financial information in their

financial statement.

Agency Theory:

Agency theory in corporate governance, describes the principal and agent relationship

between the management of an organisation and the owners of the organisation. Shareholders are

the real owner of the business, but not all of them can participate in the operation and

management of the business. On behalf of the owners, management manages the whole

operations of the business and strive to achieve the overall organisational goal. The management

works as the agent to the owners of the business, they need to protect the shareholders’ interest

with their efficient performance and transparent accounting and reporting policies. If the

management makes any manipulation or misstatement in the financial statement of the company

then the shareholders’ interest gets affected.

12FINANCIAL STATEMENT ANALYSIS REPORT

Conclusion:

From the above discussion, it can be concluded that, financial information should be free

from material misstatement or restatement it must be presented to the users of information in a

meaningful way. Material misstatement in the financial statement can led the investors and the

business itself to a financial failure and disaster. For better utilization of financial statement

information, it must be prepared in compliance with the relevant accounting standards and

statutory guidelines.

Conclusion:

From the above discussion, it can be concluded that, financial information should be free

from material misstatement or restatement it must be presented to the users of information in a

meaningful way. Material misstatement in the financial statement can led the investors and the

business itself to a financial failure and disaster. For better utilization of financial statement

information, it must be prepared in compliance with the relevant accounting standards and

statutory guidelines.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

13FINANCIAL STATEMENT ANALYSIS REPORT

Appendix A:

Figure 1.1

Figure 1.2

Appendix A:

Figure 1.1

Figure 1.2

14FINANCIAL STATEMENT ANALYSIS REPORT

Figure 1.3

Figure 1.3

15FINANCIAL STATEMENT ANALYSIS REPORT

References:

“Avid Announces Appointment of Deloitte &Touche as New Audit Firm,” Avid. January 7,

2014, http://ir.avid.com/releasedetail.cfm?ReleaseID=817675. (accessed on March 13,

2019).

“Avid Announces New Chief Financial Officer,” Avid. April 22, 2013,

http://ir.avid.com/releasedetail.cfm?ReleaseID=758125. (accessed on March 13, 2019).

“Avid Announces New Timeline for Restatement,” Avid. August 13, 2014,

http://ir.avid.com/releasedetail.cfm?ReleaseID=866020. (accessed on March 13, 2019).

“Avid Announces Receipt of Anticipated NASDAQ Letter,” Avid. March 21, 2013,

http://ir.avid.com/releasedetail.cfm?ReleaseID=750188. (accessed on March 13, 2019).

“Avid Announces Receipt of Second Anticipated NASDAQ Letter and Initial Determinations of

its Accounting Evaluation,” Avid. May 21, 2013, http://ir.avid.com/releasedetail.cfm?

ReleaseID=766370. (accessed on March 13, 2019).

“Avid Postpones its Fourth Quarter Earnings Release,” Avid. February 25, 2011,

http://ir.avid.com/releasedetail.cfm?ReleaseID=742786. (accessed on March 13, 2019).

“Avid Receives Anticipated NASDAQ Delist Letter,” Avid. February 24, 2014,

http://ir.avid.com/releasedetail.cfm?ReleaseID=827707. (accessed on March 13, 2019).

“Avid Technology, Inc. Sued by Investor,” PR Newswire. March 29, 2013,

http://www.prnewswire.com/news-releases/avid-technology-inc-sued-by-investor-

200635071.html. (accessed on March 13, 2019).

“Avid to Relist on NASDAQ, “ Avid. December 4, 2014, http://ir.avid.com/releasedetail.cfm?

ReleaseID=886269. (accessed on March 13, 2019).

References:

“Avid Announces Appointment of Deloitte &Touche as New Audit Firm,” Avid. January 7,

2014, http://ir.avid.com/releasedetail.cfm?ReleaseID=817675. (accessed on March 13,

2019).

“Avid Announces New Chief Financial Officer,” Avid. April 22, 2013,

http://ir.avid.com/releasedetail.cfm?ReleaseID=758125. (accessed on March 13, 2019).

“Avid Announces New Timeline for Restatement,” Avid. August 13, 2014,

http://ir.avid.com/releasedetail.cfm?ReleaseID=866020. (accessed on March 13, 2019).

“Avid Announces Receipt of Anticipated NASDAQ Letter,” Avid. March 21, 2013,

http://ir.avid.com/releasedetail.cfm?ReleaseID=750188. (accessed on March 13, 2019).

“Avid Announces Receipt of Second Anticipated NASDAQ Letter and Initial Determinations of

its Accounting Evaluation,” Avid. May 21, 2013, http://ir.avid.com/releasedetail.cfm?

ReleaseID=766370. (accessed on March 13, 2019).

“Avid Postpones its Fourth Quarter Earnings Release,” Avid. February 25, 2011,

http://ir.avid.com/releasedetail.cfm?ReleaseID=742786. (accessed on March 13, 2019).

“Avid Receives Anticipated NASDAQ Delist Letter,” Avid. February 24, 2014,

http://ir.avid.com/releasedetail.cfm?ReleaseID=827707. (accessed on March 13, 2019).

“Avid Technology, Inc. Sued by Investor,” PR Newswire. March 29, 2013,

http://www.prnewswire.com/news-releases/avid-technology-inc-sued-by-investor-

200635071.html. (accessed on March 13, 2019).

“Avid to Relist on NASDAQ, “ Avid. December 4, 2014, http://ir.avid.com/releasedetail.cfm?

ReleaseID=886269. (accessed on March 13, 2019).

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

16FINANCIAL STATEMENT ANALYSIS REPORT

“Delisting of Avid Stock Stayed Through NASDAQ Hearing Process,” Avid. September 18,

2013, http://ir.avid.com/releasedetail.cfm?ReleaseID=791591. (accessed on March 13,

2019).

“Expert Access Seminar Series: Revenue Recognition,” PriceWaterHouseCooper.

http://www.pwc.com/ca/en/emerging-company/publications/pwc-revenue-recognition-

2012-04-en.pdf. (accessed February 11, 2015).

“IFRS and US GAAP: Similarities and Differences,” PriceWaterHouseCooper.

http://www.pwc.com/en_US/us/issues/ifrs-reporting/publications/assets/ifrs-and-us-gaap-

similarities-and-differences-2012.pdf. (accessed February 11, 2015).

AICPA. http://www.aicpa.org/interestareas/frc/accountingfinancialrep

orting/revenuerecognition/pages/revenuerecognition.aspx. (accessed on March 13, 2019).

Amiram, D., Bozanic, Z., & Rouen, E. (2015). Financial statement errors: Evidence from the

distributional properties of financial statement numbers. Review of Accounting

Studies, 20(4), 1540-1593.

Avid. http://ir.avid.com/releases.cfm?view=all. (accessed on March 13, 2019).

Avid. http://www.avid.com/US/about.html. (accessed on March 13, 2019).

Bohusova, Hana. “Revenue Recognition Under US GAAP and IFRS Comparison,”

http://acct5183group7.wikispaces.com/file/view/revenue+recognition+-

+GAAP+vs+IFRS.pdf. (accessed on March 13, 2019).

Churet, C., & Eccles, R. G. (2014). Integrated reporting, quality of management, and financial

performance. Journal of Applied Corporate Finance, 26(1), 56-64.

“Delisting of Avid Stock Stayed Through NASDAQ Hearing Process,” Avid. September 18,

2013, http://ir.avid.com/releasedetail.cfm?ReleaseID=791591. (accessed on March 13,

2019).

“Expert Access Seminar Series: Revenue Recognition,” PriceWaterHouseCooper.

http://www.pwc.com/ca/en/emerging-company/publications/pwc-revenue-recognition-

2012-04-en.pdf. (accessed February 11, 2015).

“IFRS and US GAAP: Similarities and Differences,” PriceWaterHouseCooper.

http://www.pwc.com/en_US/us/issues/ifrs-reporting/publications/assets/ifrs-and-us-gaap-

similarities-and-differences-2012.pdf. (accessed February 11, 2015).

AICPA. http://www.aicpa.org/interestareas/frc/accountingfinancialrep

orting/revenuerecognition/pages/revenuerecognition.aspx. (accessed on March 13, 2019).

Amiram, D., Bozanic, Z., & Rouen, E. (2015). Financial statement errors: Evidence from the

distributional properties of financial statement numbers. Review of Accounting

Studies, 20(4), 1540-1593.

Avid. http://ir.avid.com/releases.cfm?view=all. (accessed on March 13, 2019).

Avid. http://www.avid.com/US/about.html. (accessed on March 13, 2019).

Bohusova, Hana. “Revenue Recognition Under US GAAP and IFRS Comparison,”

http://acct5183group7.wikispaces.com/file/view/revenue+recognition+-

+GAAP+vs+IFRS.pdf. (accessed on March 13, 2019).

Churet, C., & Eccles, R. G. (2014). Integrated reporting, quality of management, and financial

performance. Journal of Applied Corporate Finance, 26(1), 56-64.

17FINANCIAL STATEMENT ANALYSIS REPORT

Dalnial, H., Kamaluddin, A., Sanusi, Z. M., & Khairuddin, K. S. (2014). Detecting fraudulent

financial reporting through financial statement analysis. Journal of Advanced

Management Science, 2(1).

Frazer, Bryant. “Avid Talks Growth Strategy As It Completes Financial Restatement,”

StudioDaily. September 24, 2014, http://www.studiodaily.com/2014/09/avid-talks-

growth-strategy-as-it-completes-financial-restatement/. (accessed on March 13, 2019).

Gomariz, M. F. C., & Ballesta, J. P. S. (2014). Financial reporting quality, debt maturity and

investment efficiency. Journal of Banking & Finance, 40, 494-506.

Gray, G.L. and Debreceny, R.S., 2014. A taxonomy to guide research on the application of data

mining to fraud detection in financial statement audits. International Journal of

Accounting Information Systems, 15(4), pp.357-380.

IASPlus. http://www.iasplus.com/en/standards/ias/ias18. (accessed on March 13, 2019).

Lawson, Alex. “Avid Hit With Derivative Suit Over Accounting Irregularities,” Law360. June

27, 2013, http://www.law360.com/articles/453302/avid-hit-with-derivative-suit-over-

accounting-irregularities. (accessed on March 13, 2019)

Wahlen, J., Baginski, S., & Bradshaw, M. (2014). Financial reporting, financial statement

analysis and valuation. Nelson Education.

Yahoo Finance. http://finance.yahoo.com/echarts?s=AVID+Interactive#%7B%22range%22%3A

%222y%22%2C%22scale%22%3A%22linear%22%7D(accessed on March 13, 2019).

Zaller, Joe. “Avid Says its 2009 - 2011 Financial Statements No Longer Reliable,” Devoncroft.

May 23, 2013, http://blog.devoncroft.com/2013/05/23/avid-says-its-2009-2011-financial-

statements-no-longer-reliable/. (accessed on March 13, 2019)

Dalnial, H., Kamaluddin, A., Sanusi, Z. M., & Khairuddin, K. S. (2014). Detecting fraudulent

financial reporting through financial statement analysis. Journal of Advanced

Management Science, 2(1).

Frazer, Bryant. “Avid Talks Growth Strategy As It Completes Financial Restatement,”

StudioDaily. September 24, 2014, http://www.studiodaily.com/2014/09/avid-talks-

growth-strategy-as-it-completes-financial-restatement/. (accessed on March 13, 2019).

Gomariz, M. F. C., & Ballesta, J. P. S. (2014). Financial reporting quality, debt maturity and

investment efficiency. Journal of Banking & Finance, 40, 494-506.

Gray, G.L. and Debreceny, R.S., 2014. A taxonomy to guide research on the application of data

mining to fraud detection in financial statement audits. International Journal of

Accounting Information Systems, 15(4), pp.357-380.

IASPlus. http://www.iasplus.com/en/standards/ias/ias18. (accessed on March 13, 2019).

Lawson, Alex. “Avid Hit With Derivative Suit Over Accounting Irregularities,” Law360. June

27, 2013, http://www.law360.com/articles/453302/avid-hit-with-derivative-suit-over-

accounting-irregularities. (accessed on March 13, 2019)

Wahlen, J., Baginski, S., & Bradshaw, M. (2014). Financial reporting, financial statement

analysis and valuation. Nelson Education.

Yahoo Finance. http://finance.yahoo.com/echarts?s=AVID+Interactive#%7B%22range%22%3A

%222y%22%2C%22scale%22%3A%22linear%22%7D(accessed on March 13, 2019).

Zaller, Joe. “Avid Says its 2009 - 2011 Financial Statements No Longer Reliable,” Devoncroft.

May 23, 2013, http://blog.devoncroft.com/2013/05/23/avid-says-its-2009-2011-financial-

statements-no-longer-reliable/. (accessed on March 13, 2019)

1 out of 18

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.