Financial Statement Disclosures

Added on 2023-01-04

6 Pages1111 Words71 Views

Financial Statement Disclosures

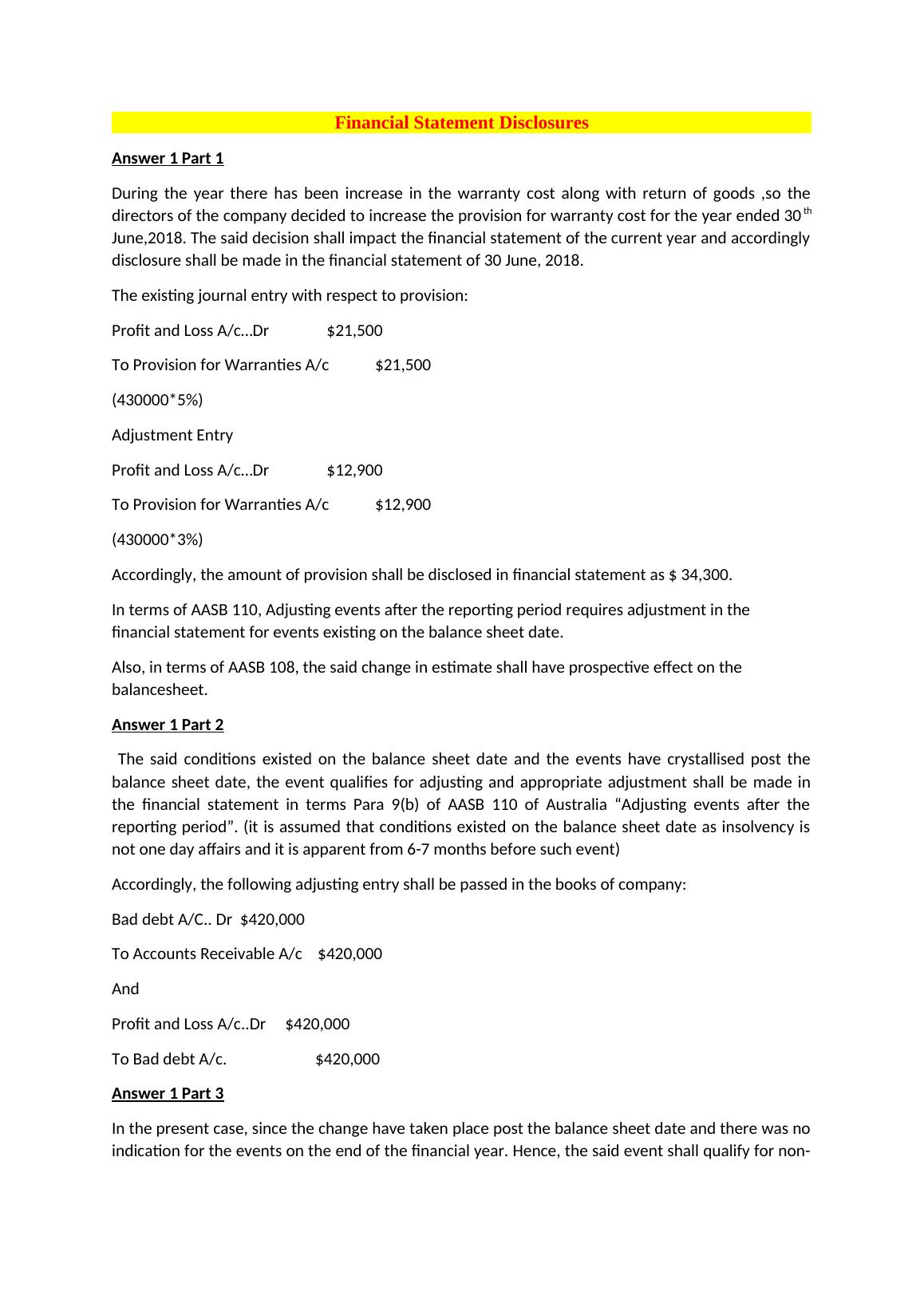

Answer 1 Part 1

During the year there has been increase in the warranty cost along with return of

goods ,so the directors of the company decided to increase the provision for

warranty cost for the year ended 30th June,2018. The said decision shall impact

the financial statement of the current year and accordingly disclosure shall be

made in the financial statement of 30 June, 2018.

The existing journal entry with respect to provision:

Profit and Loss A/c...Dr $21,500

To Provision for Warranties A/c $21,500

(430000*5%)

Adjustment Entry

Profit and Loss A/c...Dr $12,900

To Provision for Warranties A/c $12,900

(430000*3%)

Accordingly, the amount of provision shall be disclosed in financial statement as

$ 34,300.

In terms of AASB 110, Adjusting events after the reporting period requires

adjustment in the financial statement for events existing on the balance sheet

date.

Also, in terms of AASB 108, the said change in estimate shall have prospective

effect on the balancesheet.

Answer 1 Part 2

The said conditions existed on the balance sheet date and the events have

crystallised post the balance sheet date, the event qualifies for adjusting and

appropriate adjustment shall be made in the financial statement in terms Para

9(b) of AASB 110 of Australia “Adjusting events after the reporting period”. (it is

assumed that conditions existed on the balance sheet date as insolvency is not

one day affairs and it is apparent from 6-7 months before such event)

Accordingly, the following adjusting entry shall be passed in the books of

company:

Bad debt A/C.. Dr $420,000

To Accounts Receivable A/c $420,000

And

Profit and Loss A/c..Dr $420,000

To Bad debt A/c. $420,000

Answer 1 Part 3

Answer 1 Part 1

During the year there has been increase in the warranty cost along with return of

goods ,so the directors of the company decided to increase the provision for

warranty cost for the year ended 30th June,2018. The said decision shall impact

the financial statement of the current year and accordingly disclosure shall be

made in the financial statement of 30 June, 2018.

The existing journal entry with respect to provision:

Profit and Loss A/c...Dr $21,500

To Provision for Warranties A/c $21,500

(430000*5%)

Adjustment Entry

Profit and Loss A/c...Dr $12,900

To Provision for Warranties A/c $12,900

(430000*3%)

Accordingly, the amount of provision shall be disclosed in financial statement as

$ 34,300.

In terms of AASB 110, Adjusting events after the reporting period requires

adjustment in the financial statement for events existing on the balance sheet

date.

Also, in terms of AASB 108, the said change in estimate shall have prospective

effect on the balancesheet.

Answer 1 Part 2

The said conditions existed on the balance sheet date and the events have

crystallised post the balance sheet date, the event qualifies for adjusting and

appropriate adjustment shall be made in the financial statement in terms Para

9(b) of AASB 110 of Australia “Adjusting events after the reporting period”. (it is

assumed that conditions existed on the balance sheet date as insolvency is not

one day affairs and it is apparent from 6-7 months before such event)

Accordingly, the following adjusting entry shall be passed in the books of

company:

Bad debt A/C.. Dr $420,000

To Accounts Receivable A/c $420,000

And

Profit and Loss A/c..Dr $420,000

To Bad debt A/c. $420,000

Answer 1 Part 3

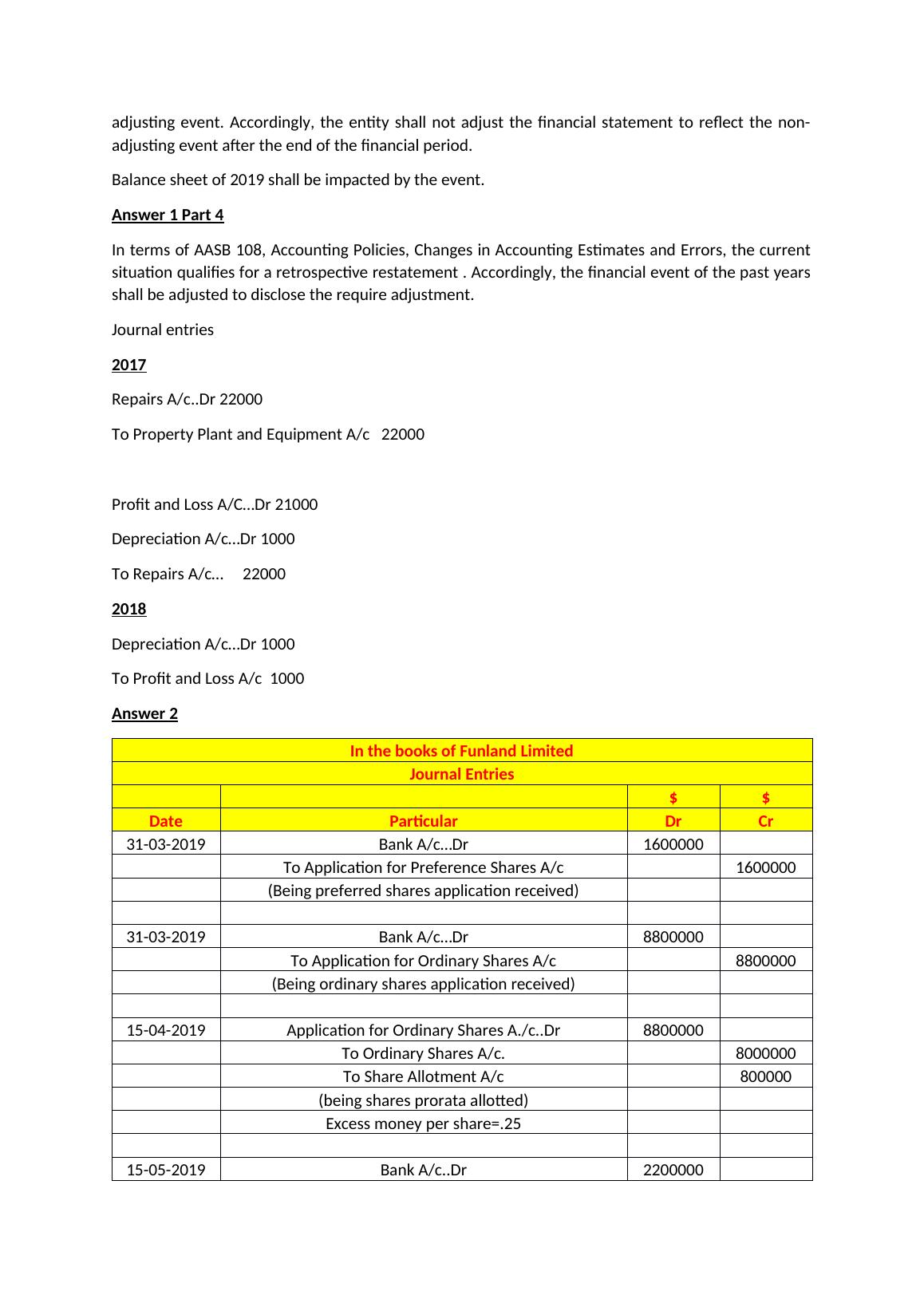

In the present case, since the change have taken place post the balance sheet

date and there was no indication for the events on the end of the financial year.

Hence, the said event shall qualify for non-adjusting event. Accordingly, the

entity shall not adjust the financial statement to reflect the non-adjusting event

after the end of the financial period.

Balance sheet of 2019 shall be impacted by the event.

Answer 1 Part 4

In terms of AASB 108, Accounting Policies, Changes in Accounting Estimates and

Errors, the current situation qualifies for a retrospective restatement .

Accordingly, the financial event of the past years shall be adjusted to disclose

the require adjustment.

Journal entries

2017

Repairs A/c..Dr 22000

To Property Plant and Equipment A/c 22000

Profit and Loss A/C...Dr 21000

Depreciation A/c...Dr 1000

To Repairs A/c... 22000

2018

Depreciation A/c...Dr 1000

To Profit and Loss A/c 1000

Answer 2

In the books of Funland Limited

Journal Entries

$ $

Date Particular Dr Cr

31-03-

2019 Bank A/c...Dr 1600000

To Application for Preference Shares A/c 1600000

(Being preferred shares application received)

31-03-

2019 Bank A/c...Dr 8800000

To Application for Ordinary Shares A/c 8800000

(Being ordinary shares application received)

15-04-

2019 Application for Ordinary Shares A./c..Dr 8800000

To Ordinary Shares A/c. 8000000

date and there was no indication for the events on the end of the financial year.

Hence, the said event shall qualify for non-adjusting event. Accordingly, the

entity shall not adjust the financial statement to reflect the non-adjusting event

after the end of the financial period.

Balance sheet of 2019 shall be impacted by the event.

Answer 1 Part 4

In terms of AASB 108, Accounting Policies, Changes in Accounting Estimates and

Errors, the current situation qualifies for a retrospective restatement .

Accordingly, the financial event of the past years shall be adjusted to disclose

the require adjustment.

Journal entries

2017

Repairs A/c..Dr 22000

To Property Plant and Equipment A/c 22000

Profit and Loss A/C...Dr 21000

Depreciation A/c...Dr 1000

To Repairs A/c... 22000

2018

Depreciation A/c...Dr 1000

To Profit and Loss A/c 1000

Answer 2

In the books of Funland Limited

Journal Entries

$ $

Date Particular Dr Cr

31-03-

2019 Bank A/c...Dr 1600000

To Application for Preference Shares A/c 1600000

(Being preferred shares application received)

31-03-

2019 Bank A/c...Dr 8800000

To Application for Ordinary Shares A/c 8800000

(Being ordinary shares application received)

15-04-

2019 Application for Ordinary Shares A./c..Dr 8800000

To Ordinary Shares A/c. 8000000

In the books of Funland Limited

Journal Entries

$ $

Date Particular Dr Cr

To Share Allotment A/c 800000

(being shares prorata allotted)

Excess money per share=.25

15-05-

2019 Bank A/c..Dr 2200000

To Share Allotment A/c 2200000

(Being Balance amount received)

(2000000*1.5-800000)

15-05-

2019 Share Allotment A/c..Dr 3000000

To Ordinary Shares A/c. 3000000

(Being shares allotted)

01-09-

2019 Bank A/c..Dr 980000

To call on Shares A/c 980000

1960000*.5

(Being call on shares made)

Answer 3

Computation of Taxable Income

For Splash Limited

For Year ended 30 June 2018

$ $

Sl

No Particulars Amount Amount

1 Profit as per Profit and Loss A/c 714000

2 Add

Annual Leave Expense 13200

Doubtful Expense 22800

Depreciation as per books of Account- Plant 48750

Depreciation as per books of Account- Motor 30000

Insurance expense 23000

Impairment Loss 14000

Warranty Expense 37400

Entertainment Expense 3500 192650

3 Less

Royalties 15000

Depreciation as per Act- Plant 65000

Journal Entries

$ $

Date Particular Dr Cr

To Share Allotment A/c 800000

(being shares prorata allotted)

Excess money per share=.25

15-05-

2019 Bank A/c..Dr 2200000

To Share Allotment A/c 2200000

(Being Balance amount received)

(2000000*1.5-800000)

15-05-

2019 Share Allotment A/c..Dr 3000000

To Ordinary Shares A/c. 3000000

(Being shares allotted)

01-09-

2019 Bank A/c..Dr 980000

To call on Shares A/c 980000

1960000*.5

(Being call on shares made)

Answer 3

Computation of Taxable Income

For Splash Limited

For Year ended 30 June 2018

$ $

Sl

No Particulars Amount Amount

1 Profit as per Profit and Loss A/c 714000

2 Add

Annual Leave Expense 13200

Doubtful Expense 22800

Depreciation as per books of Account- Plant 48750

Depreciation as per books of Account- Motor 30000

Insurance expense 23000

Impairment Loss 14000

Warranty Expense 37400

Entertainment Expense 3500 192650

3 Less

Royalties 15000

Depreciation as per Act- Plant 65000

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

Accounting and Financial Reportinglg...

|17

|1146

|85

Accounting Standards and Transactions: Provision of Journal Entries and Deferred Tax Assets and Liabilitieslg...

|11

|2563

|62

Accounting: Provision, Change in Accounting Estimate, Income Taxes, Fixed Assetslg...

|29

|2847

|478

Intermediate Financial Accountinglg...

|11

|1720

|199

Management Accounting Case Study 2022lg...

|46

|2247

|14

Financial Management: Case Study Analysis and Solutionslg...

|13

|1858

|443