Financial Reports: Income Statement and Balance Sheet Analysis

VerifiedAdded on 2021/02/19

|10

|2084

|109

Report

AI Summary

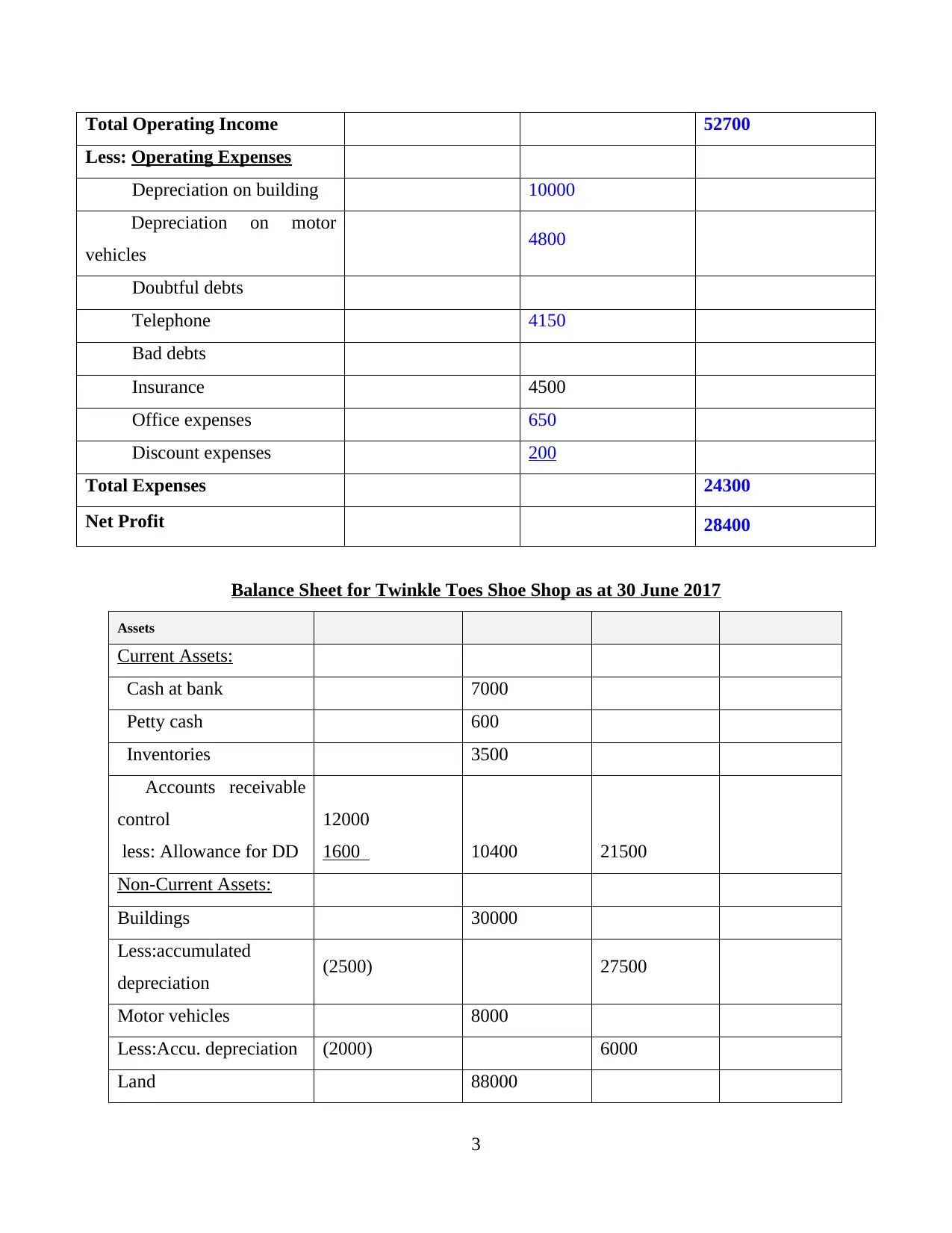

This report delves into the preparation and analysis of financial statements, crucial for understanding a company's financial performance. It covers the creation of income statements, balance sheets, and cash flow statements, essential components for assessing a company's profitability, financial position, and cash flow activities. The report includes practical examples from Twinkle Toes Shoe Shop and Brisbane Camping World, demonstrating the application of accounting principles and the interpretation of financial data. It explores key financial concepts such as assets, liabilities, owner's equity, and the use of general ledgers. The report emphasizes the importance of financial statement analysis for predicting future performance, identifying potential issues, and making informed business decisions, supported by references to relevant academic literature.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.