Analysis of Financial Statements: Shell Oman and Al Maha Companies

VerifiedAdded on 2020/01/21

|12

|2368

|49

Report

AI Summary

This report presents a financial statement analysis of Shell Oman and Al Maha, two prominent global companies. The analysis evaluates their financial performance over a four-year period, focusing on profitability, efficiency, and financial soundness. It examines revenue trends, tax burdens, interest burdens, operating margins, and financial leverage. The report includes Z-score analysis, off-balance sheet analysis, and SWOT analysis. Key findings include insights into revenue growth, profitability, liquidity, and risk management strategies. The report also highlights the companies' strengths, weaknesses, and competitive positioning within the market. The analysis draws upon financial data, industry trends, and management discussions to provide a comprehensive understanding of the companies' financial health and performance.

FINANCIAL STATEMENT ANALYSIS

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. Introduction

In association with rendering quality service, we all know that the primary concern of

every business is in the financial activities it carries out. Every company developes financial

statements for the purpose of ascertaining the financial position. Various kinds of decisions are

taken on the basis of these statements. However the information prescribed within these

statements is not adequate enough to come to a point or conclusion. Hence in order to fulfill that

different kinds of technquies are used such as ratio analysis, trend analysis, off balance sheet

analysis, z-score etc.

We have chosen to analyze the financial statements of two notable global companies—Shell

Oman and Al Maha—due to factors pointing directly at their depreciating revenue as well as the

appreciation of their net profits. Analsis of statements is made in order to evaluate the financial

performance of both the companies. This kind of evaluation will help in judging the profitability,

efficiency, profitability etc of the firms.

1.1. Limitation

The major limitation of this report is that the scope attached to it is very limited. It is

restricted to only 4 years. It is not normally enough to ascertain a company’s performance.

Objectives: This report tends to examine the financial efficiency, profitability, financial

soundness and plans of the two giant companies in the survey over a period of 4 years.

2. Trends And Analysis

The domestic consumption of Omani crude production has improved at approximately 10%

p.a. since the year 2002 with respect to the data released by the Ministry of Oil and Gas. The

In association with rendering quality service, we all know that the primary concern of

every business is in the financial activities it carries out. Every company developes financial

statements for the purpose of ascertaining the financial position. Various kinds of decisions are

taken on the basis of these statements. However the information prescribed within these

statements is not adequate enough to come to a point or conclusion. Hence in order to fulfill that

different kinds of technquies are used such as ratio analysis, trend analysis, off balance sheet

analysis, z-score etc.

We have chosen to analyze the financial statements of two notable global companies—Shell

Oman and Al Maha—due to factors pointing directly at their depreciating revenue as well as the

appreciation of their net profits. Analsis of statements is made in order to evaluate the financial

performance of both the companies. This kind of evaluation will help in judging the profitability,

efficiency, profitability etc of the firms.

1.1. Limitation

The major limitation of this report is that the scope attached to it is very limited. It is

restricted to only 4 years. It is not normally enough to ascertain a company’s performance.

Objectives: This report tends to examine the financial efficiency, profitability, financial

soundness and plans of the two giant companies in the survey over a period of 4 years.

2. Trends And Analysis

The domestic consumption of Omani crude production has improved at approximately 10%

p.a. since the year 2002 with respect to the data released by the Ministry of Oil and Gas. The

volume of exports volumes, which accounts for 83% of the total production recorded in 2012,

and was also used to garner a larger share (93%) in 2002. This rise in domestic consumption has

largely been attributed to a concerted effort made by the government to spread its dependence on

revenues from Oil firms which led to an increase in industrial, and transport patronage and use of

domestic crude to fuel industries and has consequently brought about increased usage of

automobiles. Al Maha has shown improved revenues and lower profit on a yearly basis. But with

the rebranding of filling stations in progress, and with stations functioning under the new brand,

the company’s sales growth is believed to recover in no time.

The growth in domestic consumption at a subsidized price has been in part responsible for

budgetary pressures raising the nation’s break-even oil price from $ 60/bbl in 2008 to the

expected $80/bbl in 2012, as regards the Standard. In recent developments, the government

hinted the restructuring of its subsidy bill and draft legislation with a reformation proposal has

been submitted for approval to the Council of Ministers.

Both companies participate and compete fiercely in all sectors of the economy. In retail,

they can only contend on service, like presence and branding due to Government Directive of the

retail price. In all the other sectors, the companies have room to compete on price. Although,

Shell Oman has a separate benefit in the lubricant sector as it is the only company in Oman that

has a blending plant to itself.

and was also used to garner a larger share (93%) in 2002. This rise in domestic consumption has

largely been attributed to a concerted effort made by the government to spread its dependence on

revenues from Oil firms which led to an increase in industrial, and transport patronage and use of

domestic crude to fuel industries and has consequently brought about increased usage of

automobiles. Al Maha has shown improved revenues and lower profit on a yearly basis. But with

the rebranding of filling stations in progress, and with stations functioning under the new brand,

the company’s sales growth is believed to recover in no time.

The growth in domestic consumption at a subsidized price has been in part responsible for

budgetary pressures raising the nation’s break-even oil price from $ 60/bbl in 2008 to the

expected $80/bbl in 2012, as regards the Standard. In recent developments, the government

hinted the restructuring of its subsidy bill and draft legislation with a reformation proposal has

been submitted for approval to the Council of Ministers.

Both companies participate and compete fiercely in all sectors of the economy. In retail,

they can only contend on service, like presence and branding due to Government Directive of the

retail price. In all the other sectors, the companies have room to compete on price. Although,

Shell Oman has a separate benefit in the lubricant sector as it is the only company in Oman that

has a blending plant to itself.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1

2

3

4

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

403,552 430,570

361,511

336,015

304,760,786 318,498,270

368,939

349,414

Revenues

Shell Oman Al Maha

Years

Amount

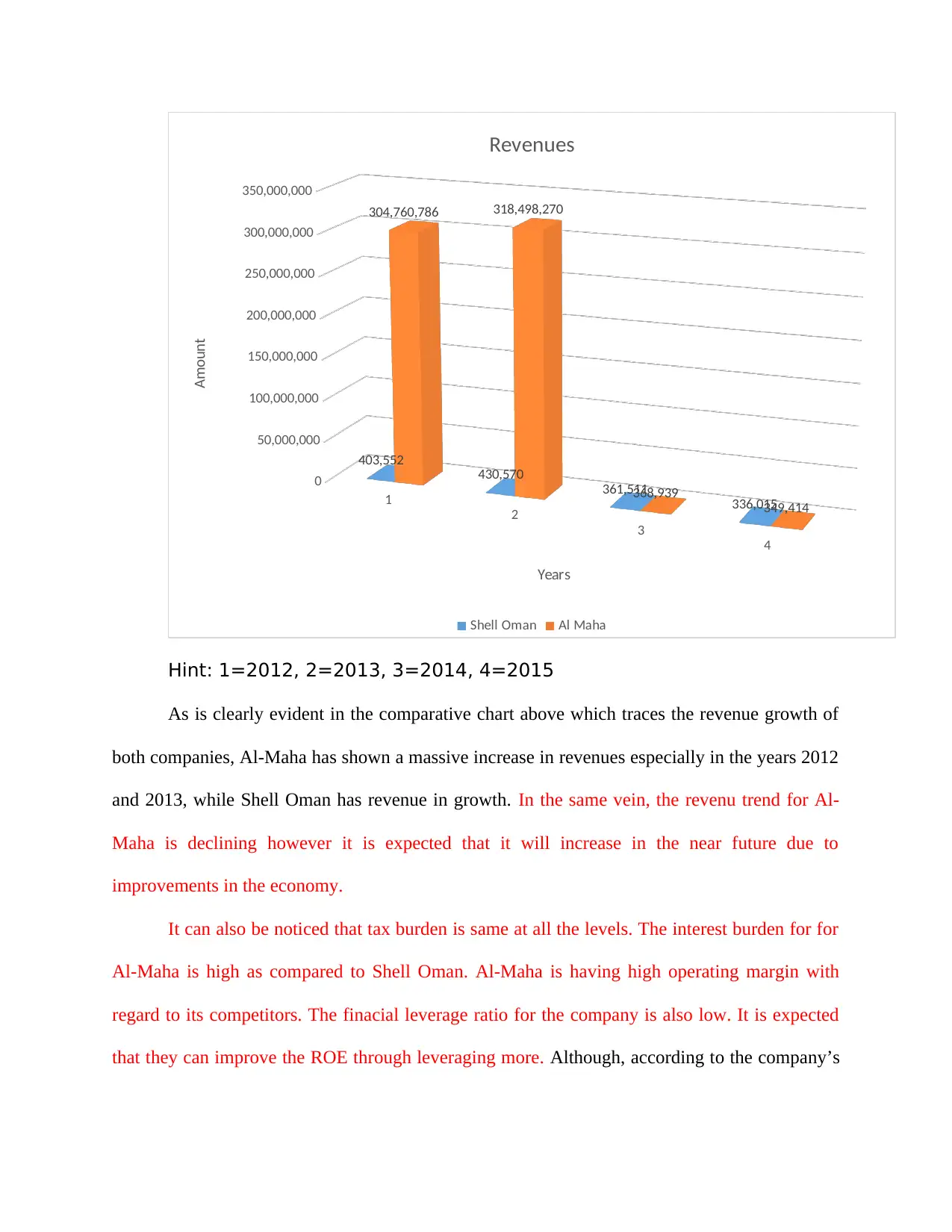

Hint: 1=2012, 2=2013, 3=2014, 4=2015

As is clearly evident in the comparative chart above which traces the revenue growth of

both companies, Al-Maha has shown a massive increase in revenues especially in the years 2012

and 2013, while Shell Oman has revenue in growth. In the same vein, the revenu trend for Al-

Maha is declining however it is expected that it will increase in the near future due to

improvements in the economy.

It can also be noticed that tax burden is same at all the levels. The interest burden for for

Al-Maha is high as compared to Shell Oman. Al-Maha is having high operating margin with

regard to its competitors. The finacial leverage ratio for the company is also low. It is expected

that they can improve the ROE through leveraging more. Although, according to the company’s

2

3

4

0

50,000,000

100,000,000

150,000,000

200,000,000

250,000,000

300,000,000

350,000,000

403,552 430,570

361,511

336,015

304,760,786 318,498,270

368,939

349,414

Revenues

Shell Oman Al Maha

Years

Amount

Hint: 1=2012, 2=2013, 3=2014, 4=2015

As is clearly evident in the comparative chart above which traces the revenue growth of

both companies, Al-Maha has shown a massive increase in revenues especially in the years 2012

and 2013, while Shell Oman has revenue in growth. In the same vein, the revenu trend for Al-

Maha is declining however it is expected that it will increase in the near future due to

improvements in the economy.

It can also be noticed that tax burden is same at all the levels. The interest burden for for

Al-Maha is high as compared to Shell Oman. Al-Maha is having high operating margin with

regard to its competitors. The finacial leverage ratio for the company is also low. It is expected

that they can improve the ROE through leveraging more. Although, according to the company’s

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

management, this is a strategic step taken by top management officials to have a conventional

tactic to business by leveraging very minimal.

In the year 2014, the Shell Oman blending plant produced and delivered around 53

million liters of finished lubricants to both local and foreign markets, which was 4% higher than

the 2013 level of production. The successful functioning and material cost savings plans for 2014

supported the plant in reducing the effect of base oil price increase during the first 3-quarters of

the year. Despite the instability in the regional export markets, Shell maintained around the same

export volumes as in 2013.

In 2014, the Shell Omani achieved a good success in the retail and commercial sector.

This sector is mainly empowered by investment in new sites, operational excellence and many

more. The lubricant potential were at the same level as it was in 2013. On the other hand, the

bitumen capacities was reduced as several projects were discarded.

At the end of the year 2014, revenes were around RO361.5 million. The figure was 16%

lower as compared to the previous tear. This was mainly due to the assumption of the Oman Aire

Contract and two major government fuel contracts. Steady growth was witnessed in retail and

commercial fleet due to the result of strategic growth investments. The net profit for 2014 was

RO12.28 MILLION as compared to the 2013 year. The simple earning per share is 1.5% higher

as compared to 2013. The revenues were low because there was reduction in the operatin costs

and due to revision to the decline rates. Focus on high business margin opportunities was also

one of the factor behind such trend. Net cash generated from operating activities was

RO20.9million, 7.6% more than what was obtainable in 2013. This was due to a release of

working capital previously devoted to supporting some of the commercial contracts that ended in

early 2014 (Management Discussion Analysis, financial performance Pg 10).

tactic to business by leveraging very minimal.

In the year 2014, the Shell Oman blending plant produced and delivered around 53

million liters of finished lubricants to both local and foreign markets, which was 4% higher than

the 2013 level of production. The successful functioning and material cost savings plans for 2014

supported the plant in reducing the effect of base oil price increase during the first 3-quarters of

the year. Despite the instability in the regional export markets, Shell maintained around the same

export volumes as in 2013.

In 2014, the Shell Omani achieved a good success in the retail and commercial sector.

This sector is mainly empowered by investment in new sites, operational excellence and many

more. The lubricant potential were at the same level as it was in 2013. On the other hand, the

bitumen capacities was reduced as several projects were discarded.

At the end of the year 2014, revenes were around RO361.5 million. The figure was 16%

lower as compared to the previous tear. This was mainly due to the assumption of the Oman Aire

Contract and two major government fuel contracts. Steady growth was witnessed in retail and

commercial fleet due to the result of strategic growth investments. The net profit for 2014 was

RO12.28 MILLION as compared to the 2013 year. The simple earning per share is 1.5% higher

as compared to 2013. The revenues were low because there was reduction in the operatin costs

and due to revision to the decline rates. Focus on high business margin opportunities was also

one of the factor behind such trend. Net cash generated from operating activities was

RO20.9million, 7.6% more than what was obtainable in 2013. This was due to a release of

working capital previously devoted to supporting some of the commercial contracts that ended in

early 2014 (Management Discussion Analysis, financial performance Pg 10).

3. Analysis of cash flows

By May 13, 2016, the consensus prediction amongst two polled asset analysts covering Al

Maha Petroleum Products Marketing Co. counsels. Investors were required to hold their

respective position withion the organization. This has been the consensus forecast since the

emotion of investment analysts deteriorated on Jan 26, 2015. The previous consensus prediction

advised that Al Maha Petroleum Products Marketing Co. would outperform the market. The

analyst proposing a 12-month price target expects Al Maha Petroleum Products Marketing Co.

share price to increase to 1.70 in the next year from the previous price of 1.55. 2014 net profit for

Shell Oman Oil was RO12.28 million compared to RO12.09 million in 2013.

By Jul 23, 2014, Al Maha Petroleum Products Marketing Co. announced 2nd quarter 2014

earnings of 0.045 per share. This figures undermined the 0.12 expectation of the company’s

analyst but exceeded the previous year's 2nd quarter results by 8.43%. Al Maha Petroleum

Products Marketing Co. reported 2012 annual earnings of 0.1454 per share on Jan 27, 2013. The

Al Maha Company’s SAOG had as at the 1st quarter 2016 revenues of 84.40m. This defied the

101.00m evaluation of the company’s analyst.

By May 13, 2016, the consensus prediction amongst two polled asset analysts covering Al

Maha Petroleum Products Marketing Co. counsels. Investors were required to hold their

respective position withion the organization. This has been the consensus forecast since the

emotion of investment analysts deteriorated on Jan 26, 2015. The previous consensus prediction

advised that Al Maha Petroleum Products Marketing Co. would outperform the market. The

analyst proposing a 12-month price target expects Al Maha Petroleum Products Marketing Co.

share price to increase to 1.70 in the next year from the previous price of 1.55. 2014 net profit for

Shell Oman Oil was RO12.28 million compared to RO12.09 million in 2013.

By Jul 23, 2014, Al Maha Petroleum Products Marketing Co. announced 2nd quarter 2014

earnings of 0.045 per share. This figures undermined the 0.12 expectation of the company’s

analyst but exceeded the previous year's 2nd quarter results by 8.43%. Al Maha Petroleum

Products Marketing Co. reported 2012 annual earnings of 0.1454 per share on Jan 27, 2013. The

Al Maha Company’s SAOG had as at the 1st quarter 2016 revenues of 84.40m. This defied the

101.00m evaluation of the company’s analyst.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

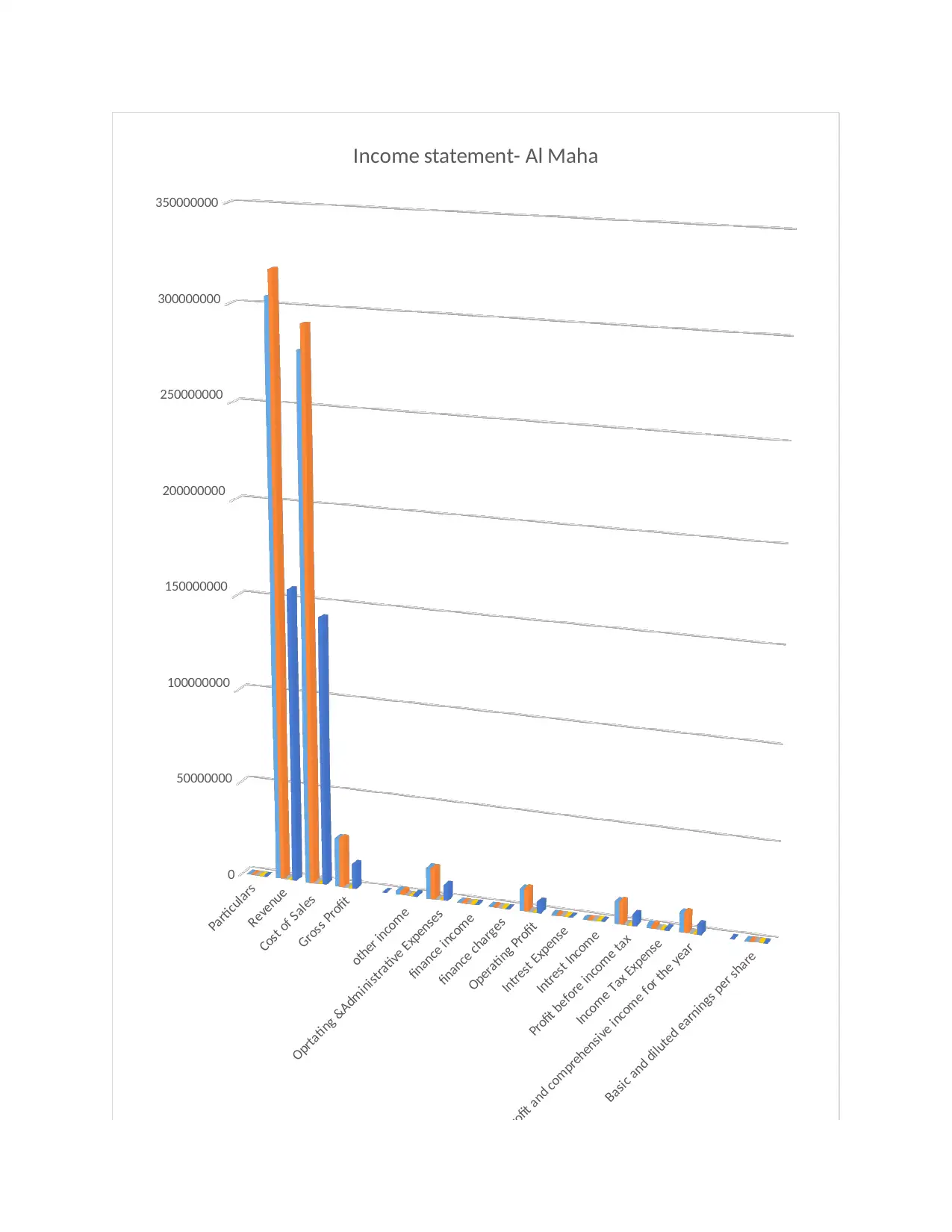

Particulars

Revenue

Cost of Sales

Gross Profit

other income

Oprtating &Administrative Expenses

finance income

finance charges

Operating Profit

Intrest Expense

Intrest Income

Profit before income tax

Income Tax Expense

Profit and comprehensive income for the year

Basic and diluted earnings per share

0

50000000

100000000

150000000

200000000

250000000

300000000

350000000

Income statement- Al Maha

Years Series2 Series3 Series4 Series5

Revenue

Cost of Sales

Gross Profit

other income

Oprtating &Administrative Expenses

finance income

finance charges

Operating Profit

Intrest Expense

Intrest Income

Profit before income tax

Income Tax Expense

Profit and comprehensive income for the year

Basic and diluted earnings per share

0

50000000

100000000

150000000

200000000

250000000

300000000

350000000

Income statement- Al Maha

Years Series2 Series3 Series4 Series5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

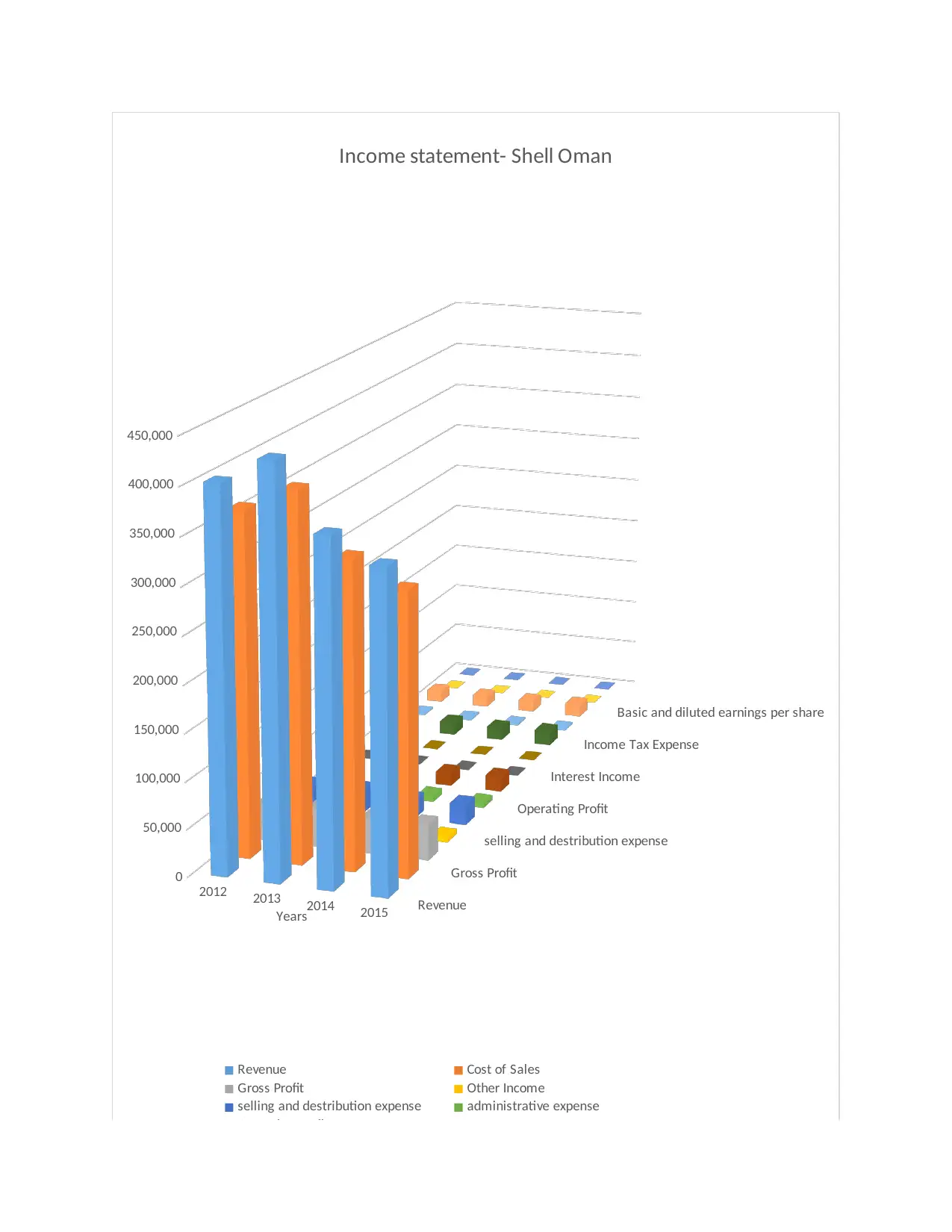

2012 2013 2014 2015Years

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Revenue

Gross Profit

selling and destribution expense

Operating Profit

Interest Income

Income Tax Expense

Basic and diluted earnings per share

Income statement- Shell Oman

Revenue Cost of Sales

Gross Profit Other Income

selling and destribution expense administrative expense

Operating Profit Interest Expenses

Interest Income Profit before income tax

Income Tax Expense Profit and comprehensive income for the year

Basic and diluted earnings per share Dividend Per Share

0

50,000

100,000

150,000

200,000

250,000

300,000

350,000

400,000

450,000

Revenue

Gross Profit

selling and destribution expense

Operating Profit

Interest Income

Income Tax Expense

Basic and diluted earnings per share

Income statement- Shell Oman

Revenue Cost of Sales

Gross Profit Other Income

selling and destribution expense administrative expense

Operating Profit Interest Expenses

Interest Income Profit before income tax

Income Tax Expense Profit and comprehensive income for the year

Basic and diluted earnings per share Dividend Per Share

4. Z-Score Analysis

According to the Z-score model, firms which are havng a score of above 3 are regarded as

safe and healthy. There are no chances of getting bankcrupt in the coming future. It is expected

that firms with a scoe of 1.8 to 3 are likely to become banckcrupt in the upcoming 2 years. The

Altman z-score for the two companies suggest that Sell Oman is having low score as compared

to AlMaha Oil. It can be seen that financial position of the Shell Oman is also good and is also

performing well. The retained earnings are showing an upward trend and there are adequate cash

balances. Hence this shows that both the firms are having enough finance for the operations.

5. Off-Balance Sheet Analysis

Oman Oil and Shell Oman follows International Financial Reporting Standards. The

formation of the financial statements comprise of estimates and assumptions which are likely to

affect the balance sheet. This will affect at the time of preparation and changes in the fair value.

The estimates and assumptions are based on different factors related to the firms. Three different

types of risks are faced by both the companies which includes Market Risk, Credit Risk and

Liquidty risk. Management is of the opinion that none of the risk could have an material impact.

Both the firms had maintained a provision for environmental remediation cost on the basis of

assessments. Contigent liabilities of Rials 894,045 and Rials 4,965,923 can be witnessed. It has

been anticipated that these would not create any material impact on the earnings. The Oman Oil

faced the charge of Rials 332,419 because of the difference in the prices. It has not been

considered since it’s not probable based on the legal opinion. Shell Oman has also faced the

litigation from an ex-employee for the charge of illegal termination. Further a provition of

According to the Z-score model, firms which are havng a score of above 3 are regarded as

safe and healthy. There are no chances of getting bankcrupt in the coming future. It is expected

that firms with a scoe of 1.8 to 3 are likely to become banckcrupt in the upcoming 2 years. The

Altman z-score for the two companies suggest that Sell Oman is having low score as compared

to AlMaha Oil. It can be seen that financial position of the Shell Oman is also good and is also

performing well. The retained earnings are showing an upward trend and there are adequate cash

balances. Hence this shows that both the firms are having enough finance for the operations.

5. Off-Balance Sheet Analysis

Oman Oil and Shell Oman follows International Financial Reporting Standards. The

formation of the financial statements comprise of estimates and assumptions which are likely to

affect the balance sheet. This will affect at the time of preparation and changes in the fair value.

The estimates and assumptions are based on different factors related to the firms. Three different

types of risks are faced by both the companies which includes Market Risk, Credit Risk and

Liquidty risk. Management is of the opinion that none of the risk could have an material impact.

Both the firms had maintained a provision for environmental remediation cost on the basis of

assessments. Contigent liabilities of Rials 894,045 and Rials 4,965,923 can be witnessed. It has

been anticipated that these would not create any material impact on the earnings. The Oman Oil

faced the charge of Rials 332,419 because of the difference in the prices. It has not been

considered since it’s not probable based on the legal opinion. Shell Oman has also faced the

litigation from an ex-employee for the charge of illegal termination. Further a provition of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

compensation for injury during the job has also been charged. However it is unlikely to have an

material impact. However no provision had been made in the financial statements.

6. SWOT ANALYSIS:

Strength

Vertically integrated operations –

Shell operates into the energy sector and seres into three major markets which are Asia,

Europe and North America. The company is involved in activity of acquition of buying

out competition. A vertical integration approach is followed. It includes acquiring and

making mergers with the other entities. The Shell and Saudi Aramco agreed to enter into

a partnership within the category of refining and marketing. A joint venture named

Motiva Enterprises was established in the year 1998. It was a limited liability company

which was headquartered in Texas. In the year 2004, revenue of $24bn was gained. It is

the largest refinery and is having a capacity of 740,000 barrels per day. This has

increased the market power and it can also help in reducing the competiion. The growth

of the company is based on two strategies. It includes integrated gas and deep water.

Hence it will help in meting the global demand for the energy (Nowlin, 2014).

Weaknesses

Issues such as human rights and environmental problems can spoil the goodwill of the

company. There are differences in the regulatory regimes and policies. For example,

Sheel was faced extreme criticization over the issue of Niger Delta Oil. Other companies

material impact. However no provision had been made in the financial statements.

6. SWOT ANALYSIS:

Strength

Vertically integrated operations –

Shell operates into the energy sector and seres into three major markets which are Asia,

Europe and North America. The company is involved in activity of acquition of buying

out competition. A vertical integration approach is followed. It includes acquiring and

making mergers with the other entities. The Shell and Saudi Aramco agreed to enter into

a partnership within the category of refining and marketing. A joint venture named

Motiva Enterprises was established in the year 1998. It was a limited liability company

which was headquartered in Texas. In the year 2004, revenue of $24bn was gained. It is

the largest refinery and is having a capacity of 740,000 barrels per day. This has

increased the market power and it can also help in reducing the competiion. The growth

of the company is based on two strategies. It includes integrated gas and deep water.

Hence it will help in meting the global demand for the energy (Nowlin, 2014).

Weaknesses

Issues such as human rights and environmental problems can spoil the goodwill of the

company. There are differences in the regulatory regimes and policies. For example,

Sheel was faced extreme criticization over the issue of Niger Delta Oil. Other companies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

had accused Shell of abusing the position in Nigeria (Gaughran, 2013). It was noticed

that company has polluted the environment in Ogoniland, Niger Delta. Nigeria.

7. Conclusion

The analysis of this research has brought us to a conclusion that the financial efficiency,

profitability, financial soundness and plans of the two giant companies is guaranteed if they can

efficiently manage their finances. Financial stability can be seen highly in the Shell Oman. The

company is having better profitability and liquidity. The collection policy of the firms is good

but not adequate enough. No increase can be seen in the receivables. This has affected the

productivity. Analysis of financial statements suggests that both the companies are doing well in

their respective operations. Diversification & management of risk is done in better manner by the

Shell Oman.

that company has polluted the environment in Ogoniland, Niger Delta. Nigeria.

7. Conclusion

The analysis of this research has brought us to a conclusion that the financial efficiency,

profitability, financial soundness and plans of the two giant companies is guaranteed if they can

efficiently manage their finances. Financial stability can be seen highly in the Shell Oman. The

company is having better profitability and liquidity. The collection policy of the firms is good

but not adequate enough. No increase can be seen in the receivables. This has affected the

productivity. Analysis of financial statements suggests that both the companies are doing well in

their respective operations. Diversification & management of risk is done in better manner by the

Shell Oman.

References

1. Biais, B. and C. Gollier. (1997). ‘‘Trade Credit and Credit Rationing.’’ The Review of

Financial Studies 10, 903–937.

2. Fama, E. and K. French. (1998). ‘‘Taxes, Financing Decisions, and Firm Value.’’ Journal

of Finance 53, 819–843.

3. Feltham, J. and J. Ohlson. (1995). ‘‘Valuation and Clean Surplus Accounting for

Operating and Financing Activities.’’ Contemporary Accounting Research 11, 689–731.

4. Harris, M. and A. Raviv. (1991). ‘‘The Theory of Capital Structure.’’ Journal of Finance

46, 297–355.

5. Kemsley, D. and D. Nissim. (2002). ‘‘Valuation of the Debt-tax Shield.’’ Journal of

Finance 57, 2045–2074.

6. Mian, S. and C. Smith, Jr. (1992). ‘‘Accounts Receivable Management Policy: Theory

and Evidence.’’ Journal of Finance 47, 169–200.

7. Modigliani, F. and M. Miller. (1958). ‘‘The Cost of Capital, Corporation Finance, and the

Theory of Investment.’’ American Economic Review 46, 261–297.

8. Penman, S. (2004). Financial Statement Analysis, Security Valuation 2nd ed. New York:

Irwin/McGraw-Hill.

9. Petersen, M. and R. Rajan. (1997). ‘‘Trade Credit: Theories and Evidence.’’ The Review

of Financial Studies 10, 661–691.

10. Ross. S. (1977). ‘‘The Determination of Financial Structure: The Incentive-Signaling

Approach.’’ Bell Journal of Economics 8, 23–40.

11. Schwartz, R. (1974). ‘‘An Economic Model of Trade Credit.’’ Journal of Financial,

Quantitative Analysis 9, 643–657.

1. Biais, B. and C. Gollier. (1997). ‘‘Trade Credit and Credit Rationing.’’ The Review of

Financial Studies 10, 903–937.

2. Fama, E. and K. French. (1998). ‘‘Taxes, Financing Decisions, and Firm Value.’’ Journal

of Finance 53, 819–843.

3. Feltham, J. and J. Ohlson. (1995). ‘‘Valuation and Clean Surplus Accounting for

Operating and Financing Activities.’’ Contemporary Accounting Research 11, 689–731.

4. Harris, M. and A. Raviv. (1991). ‘‘The Theory of Capital Structure.’’ Journal of Finance

46, 297–355.

5. Kemsley, D. and D. Nissim. (2002). ‘‘Valuation of the Debt-tax Shield.’’ Journal of

Finance 57, 2045–2074.

6. Mian, S. and C. Smith, Jr. (1992). ‘‘Accounts Receivable Management Policy: Theory

and Evidence.’’ Journal of Finance 47, 169–200.

7. Modigliani, F. and M. Miller. (1958). ‘‘The Cost of Capital, Corporation Finance, and the

Theory of Investment.’’ American Economic Review 46, 261–297.

8. Penman, S. (2004). Financial Statement Analysis, Security Valuation 2nd ed. New York:

Irwin/McGraw-Hill.

9. Petersen, M. and R. Rajan. (1997). ‘‘Trade Credit: Theories and Evidence.’’ The Review

of Financial Studies 10, 661–691.

10. Ross. S. (1977). ‘‘The Determination of Financial Structure: The Incentive-Signaling

Approach.’’ Bell Journal of Economics 8, 23–40.

11. Schwartz, R. (1974). ‘‘An Economic Model of Trade Credit.’’ Journal of Financial,

Quantitative Analysis 9, 643–657.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.