Financial Statement Analysis: Fairfax Media Case Study - ACC510, S1

VerifiedAdded on 2023/06/12

|13

|2121

|397

Essay

AI Summary

This essay provides a comprehensive financial statement analysis of Fairfax Media, focusing on key aspects such as contingencies, provisions, leased items, and non-current assets. It examines the recognition criteria and measurement issues associated with these elements, referencing the company's 2017 annual report and relevant accounting standards like AASB 137 and AASB 16. The analysis includes a discussion of hypothetical reclassification scenarios for leased items and an evaluation of the valuation methods used for non-current assets, specifically receivables. The report concludes that Fairfax Media generally adheres to accounting standards but recommends enhanced disclosure and improved financial reporting quality. This document is available on Desklib, where students can find similar solved assignments and past papers.

Running head: FINANCIAL STATEMENTS ANALYSIS

Financial Statements Analysis

Name of the Student:

Name of the University:

Author Note

Financial Statements Analysis

Name of the Student:

Name of the University:

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL STATEMENTS ANALYSIS

Table of Contents

Introduction......................................................................................................................................2

1. Contingencies and Provisions......................................................................................................2

2. Recognition Criteria and Measurement associated with provision or contingent liability..........3

3. Contingency recorded..................................................................................................................4

4. Plant and Equipment under financial leases................................................................................5

5. Treatment of leases......................................................................................................................5

6. Reclassification of the leased item..............................................................................................7

7. Non-current asset – impairment method......................................................................................7

8. Valuation Method for Non Current Assets..................................................................................8

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

Table of Contents

Introduction......................................................................................................................................2

1. Contingencies and Provisions......................................................................................................2

2. Recognition Criteria and Measurement associated with provision or contingent liability..........3

3. Contingency recorded..................................................................................................................4

4. Plant and Equipment under financial leases................................................................................5

5. Treatment of leases......................................................................................................................5

6. Reclassification of the leased item..............................................................................................7

7. Non-current asset – impairment method......................................................................................7

8. Valuation Method for Non Current Assets..................................................................................8

Conclusion.......................................................................................................................................8

References........................................................................................................................................9

2FINANCIAL STATEMENTS ANALYSIS

Introduction:

In this particular assignment, the issues pertaining to accounting is presented in context of

Fairfax media. The analysis has been done for evaluating whether the accounting facts and

figures are presented in compliance with the prescribed accounting standard so that the financial

statements prepared are reliable for its internal as well as external users. For this purpose, data

and facts have been extracted from the annual report for year 2017.

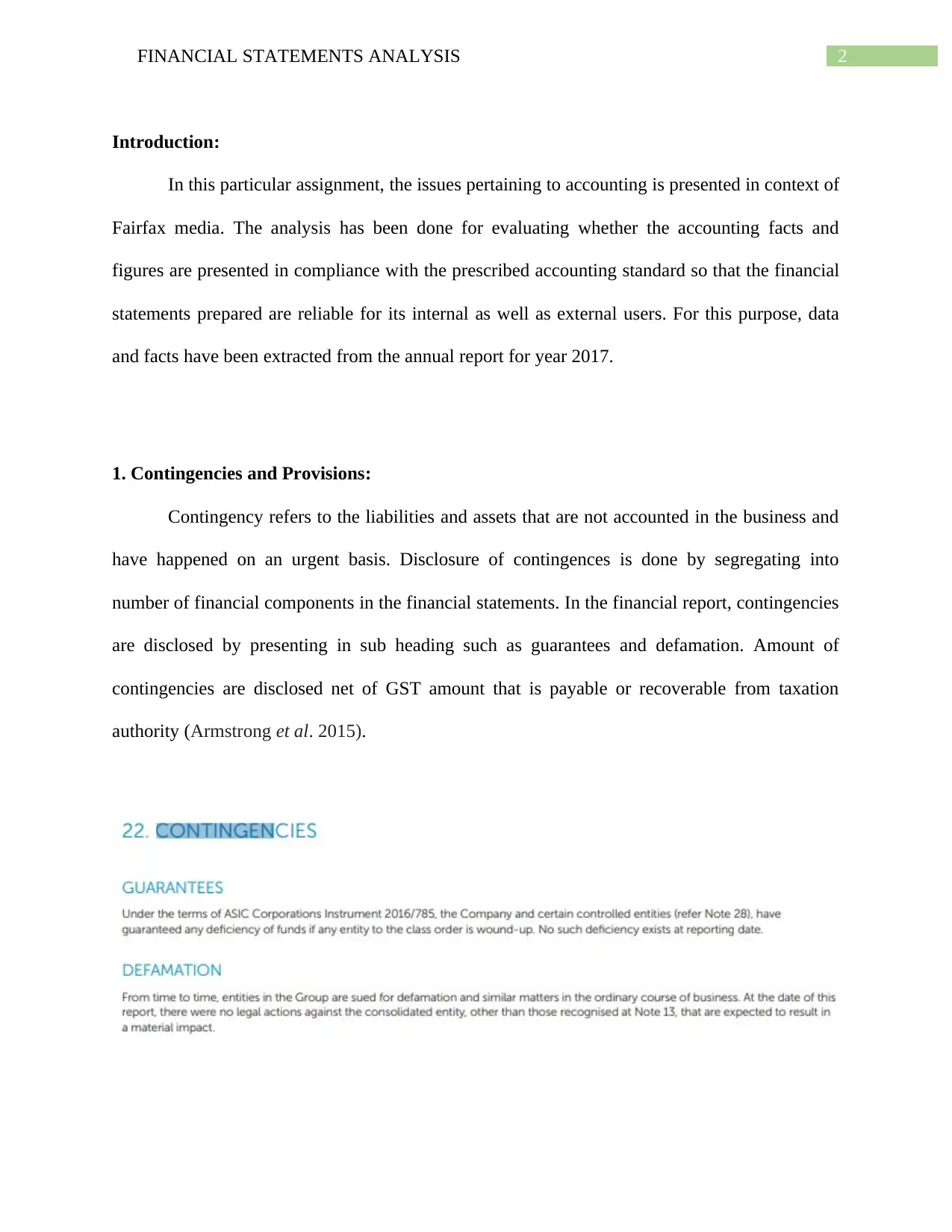

1. Contingencies and Provisions:

Contingency refers to the liabilities and assets that are not accounted in the business and

have happened on an urgent basis. Disclosure of contingences is done by segregating into

number of financial components in the financial statements. In the financial report, contingencies

are disclosed by presenting in sub heading such as guarantees and defamation. Amount of

contingencies are disclosed net of GST amount that is payable or recoverable from taxation

authority (Armstrong et al. 2015).

Introduction:

In this particular assignment, the issues pertaining to accounting is presented in context of

Fairfax media. The analysis has been done for evaluating whether the accounting facts and

figures are presented in compliance with the prescribed accounting standard so that the financial

statements prepared are reliable for its internal as well as external users. For this purpose, data

and facts have been extracted from the annual report for year 2017.

1. Contingencies and Provisions:

Contingency refers to the liabilities and assets that are not accounted in the business and

have happened on an urgent basis. Disclosure of contingences is done by segregating into

number of financial components in the financial statements. In the financial report, contingencies

are disclosed by presenting in sub heading such as guarantees and defamation. Amount of

contingencies are disclosed net of GST amount that is payable or recoverable from taxation

authority (Armstrong et al. 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL STATEMENTS ANALYSIS

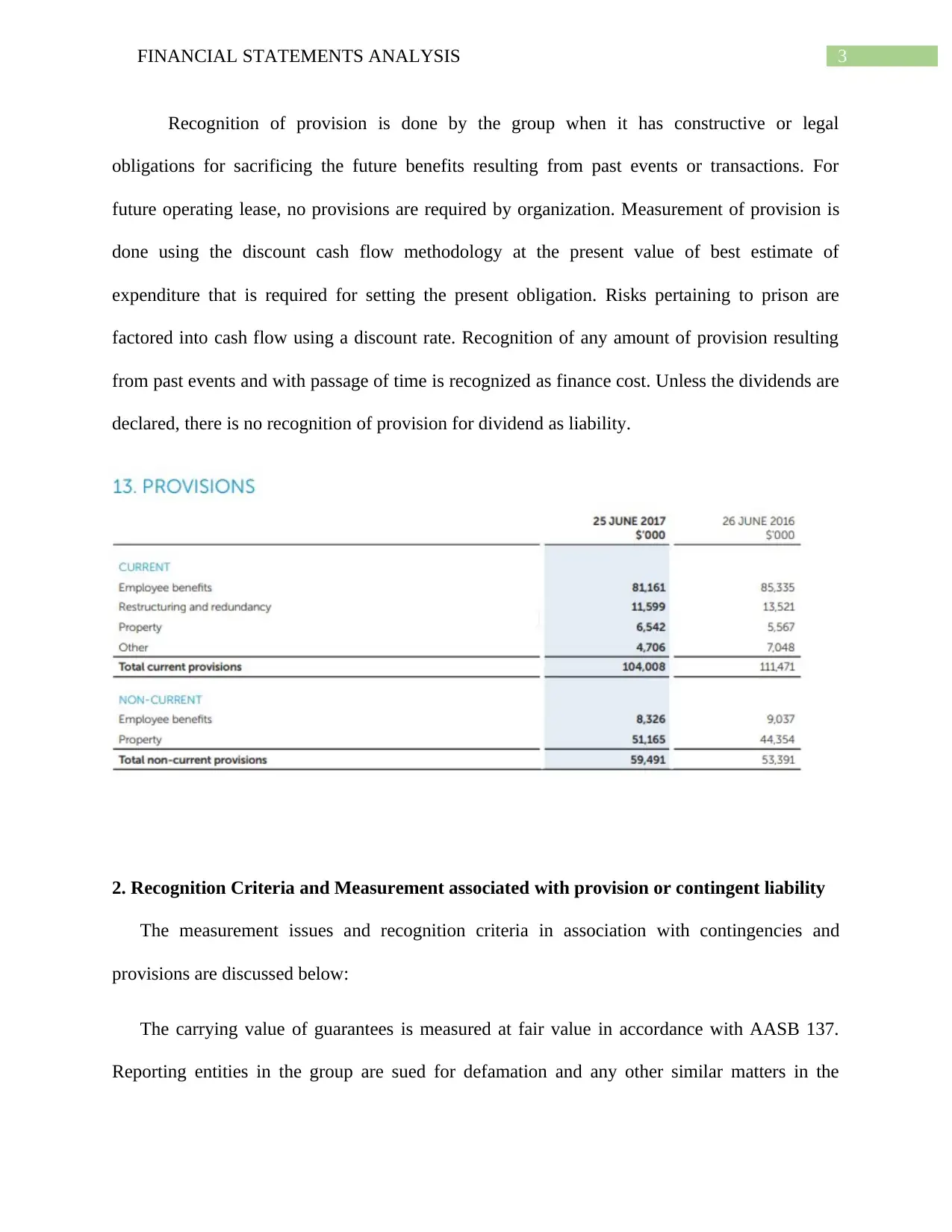

Recognition of provision is done by the group when it has constructive or legal

obligations for sacrificing the future benefits resulting from past events or transactions. For

future operating lease, no provisions are required by organization. Measurement of provision is

done using the discount cash flow methodology at the present value of best estimate of

expenditure that is required for setting the present obligation. Risks pertaining to prison are

factored into cash flow using a discount rate. Recognition of any amount of provision resulting

from past events and with passage of time is recognized as finance cost. Unless the dividends are

declared, there is no recognition of provision for dividend as liability.

2. Recognition Criteria and Measurement associated with provision or contingent liability

The measurement issues and recognition criteria in association with contingencies and

provisions are discussed below:

The carrying value of guarantees is measured at fair value in accordance with AASB 137.

Reporting entities in the group are sued for defamation and any other similar matters in the

Recognition of provision is done by the group when it has constructive or legal

obligations for sacrificing the future benefits resulting from past events or transactions. For

future operating lease, no provisions are required by organization. Measurement of provision is

done using the discount cash flow methodology at the present value of best estimate of

expenditure that is required for setting the present obligation. Risks pertaining to prison are

factored into cash flow using a discount rate. Recognition of any amount of provision resulting

from past events and with passage of time is recognized as finance cost. Unless the dividends are

declared, there is no recognition of provision for dividend as liability.

2. Recognition Criteria and Measurement associated with provision or contingent liability

The measurement issues and recognition criteria in association with contingencies and

provisions are discussed below:

The carrying value of guarantees is measured at fair value in accordance with AASB 137.

Reporting entities in the group are sued for defamation and any other similar matters in the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL STATEMENTS ANALYSIS

ordinary course of business. In regard to any undrawn letter, entity recognized the letter of credit

that is not limited to insurance or leases.

Measurement of provisions is based on estimates that will be used for setting the obligations

at the current reporting period. Current assessment of market situation and other associated risks

is reflected in the discount rate that is used for determining the present value of pre tax rate.

3. Contingency recorded

The contingencies that are disclosed in the annual report of Fairfax limited can be

referred to defamation and guaranteed. Any deficiency of funds is guaranteed by certain

controlled entities and the company in the event when entity to class order is wound up. At the

reporting date, there foes not exists any such deficiency. Defamation is about to sue entities from

time to time in event of any defamation. There was no legal action at the reporting date against

the consolidated entity except some of the items that have a material impact and is mentioned in

the notes to financial statements. In event of acquisition, any contingent consideration is

recognized at fair value and is transferred by the acquirer. Any change in the fair value of

consideration that is deemed to be liability is recognized in the income statement according to

AASB 139.

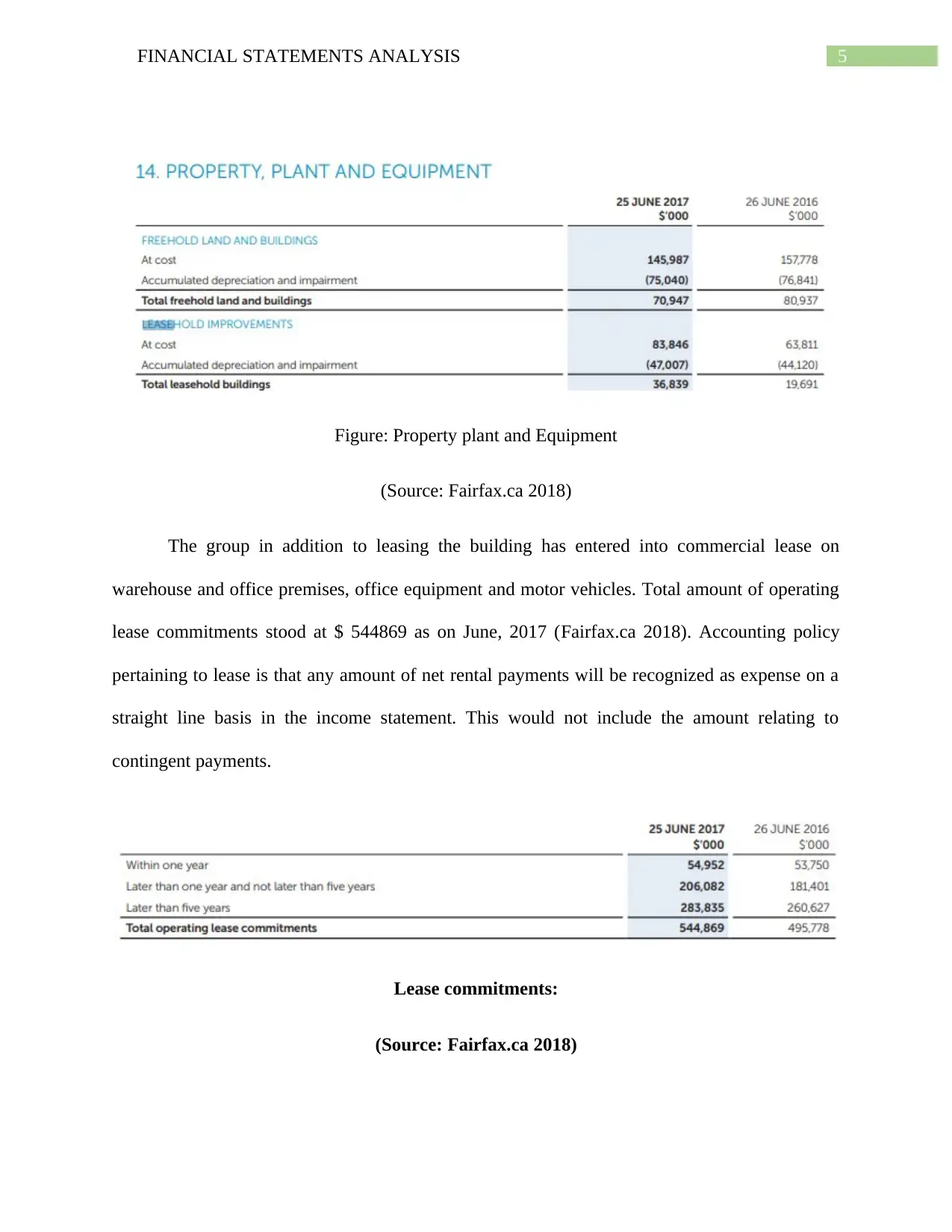

4. Plant and Equipment under financial leases

It is indicated by the image below that plant and equipment are under the finance lease

with total value of leasehold building at $ 36839 in year 2017.

ordinary course of business. In regard to any undrawn letter, entity recognized the letter of credit

that is not limited to insurance or leases.

Measurement of provisions is based on estimates that will be used for setting the obligations

at the current reporting period. Current assessment of market situation and other associated risks

is reflected in the discount rate that is used for determining the present value of pre tax rate.

3. Contingency recorded

The contingencies that are disclosed in the annual report of Fairfax limited can be

referred to defamation and guaranteed. Any deficiency of funds is guaranteed by certain

controlled entities and the company in the event when entity to class order is wound up. At the

reporting date, there foes not exists any such deficiency. Defamation is about to sue entities from

time to time in event of any defamation. There was no legal action at the reporting date against

the consolidated entity except some of the items that have a material impact and is mentioned in

the notes to financial statements. In event of acquisition, any contingent consideration is

recognized at fair value and is transferred by the acquirer. Any change in the fair value of

consideration that is deemed to be liability is recognized in the income statement according to

AASB 139.

4. Plant and Equipment under financial leases

It is indicated by the image below that plant and equipment are under the finance lease

with total value of leasehold building at $ 36839 in year 2017.

5FINANCIAL STATEMENTS ANALYSIS

Figure: Property plant and Equipment

(Source: Fairfax.ca 2018)

The group in addition to leasing the building has entered into commercial lease on

warehouse and office premises, office equipment and motor vehicles. Total amount of operating

lease commitments stood at $ 544869 as on June, 2017 (Fairfax.ca 2018). Accounting policy

pertaining to lease is that any amount of net rental payments will be recognized as expense on a

straight line basis in the income statement. This would not include the amount relating to

contingent payments.

Lease commitments:

(Source: Fairfax.ca 2018)

Figure: Property plant and Equipment

(Source: Fairfax.ca 2018)

The group in addition to leasing the building has entered into commercial lease on

warehouse and office premises, office equipment and motor vehicles. Total amount of operating

lease commitments stood at $ 544869 as on June, 2017 (Fairfax.ca 2018). Accounting policy

pertaining to lease is that any amount of net rental payments will be recognized as expense on a

straight line basis in the income statement. This would not include the amount relating to

contingent payments.

Lease commitments:

(Source: Fairfax.ca 2018)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL STATEMENTS ANALYSIS

5. Treatment of leases

Leases of organization are treated according to the accounting standard AASB 16

that is effective from January, 2013. With reference to these particular lease standards, all the

items of lease having a term of over 12 years are recognized in the balance sheet. The

measurement of liabilities for leased payment and any corresponding right to use assets is done

at present value of the amounts that is expected to be paid over time. In addition to this, the

classification of lease as operating or financial lease will form the basis of cost recognition of

such leases in the income statement. Operating lease cost over the lease term will be recognized

as single operating expense on straight line basis and financing lease on other hand is recognized

both as an interest and operating expenses after disaggregating such lease.

5. Treatment of leases

Leases of organization are treated according to the accounting standard AASB 16

that is effective from January, 2013. With reference to these particular lease standards, all the

items of lease having a term of over 12 years are recognized in the balance sheet. The

measurement of liabilities for leased payment and any corresponding right to use assets is done

at present value of the amounts that is expected to be paid over time. In addition to this, the

classification of lease as operating or financial lease will form the basis of cost recognition of

such leases in the income statement. Operating lease cost over the lease term will be recognized

as single operating expense on straight line basis and financing lease on other hand is recognized

both as an interest and operating expenses after disaggregating such lease.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL STATEMENTS ANALYSIS

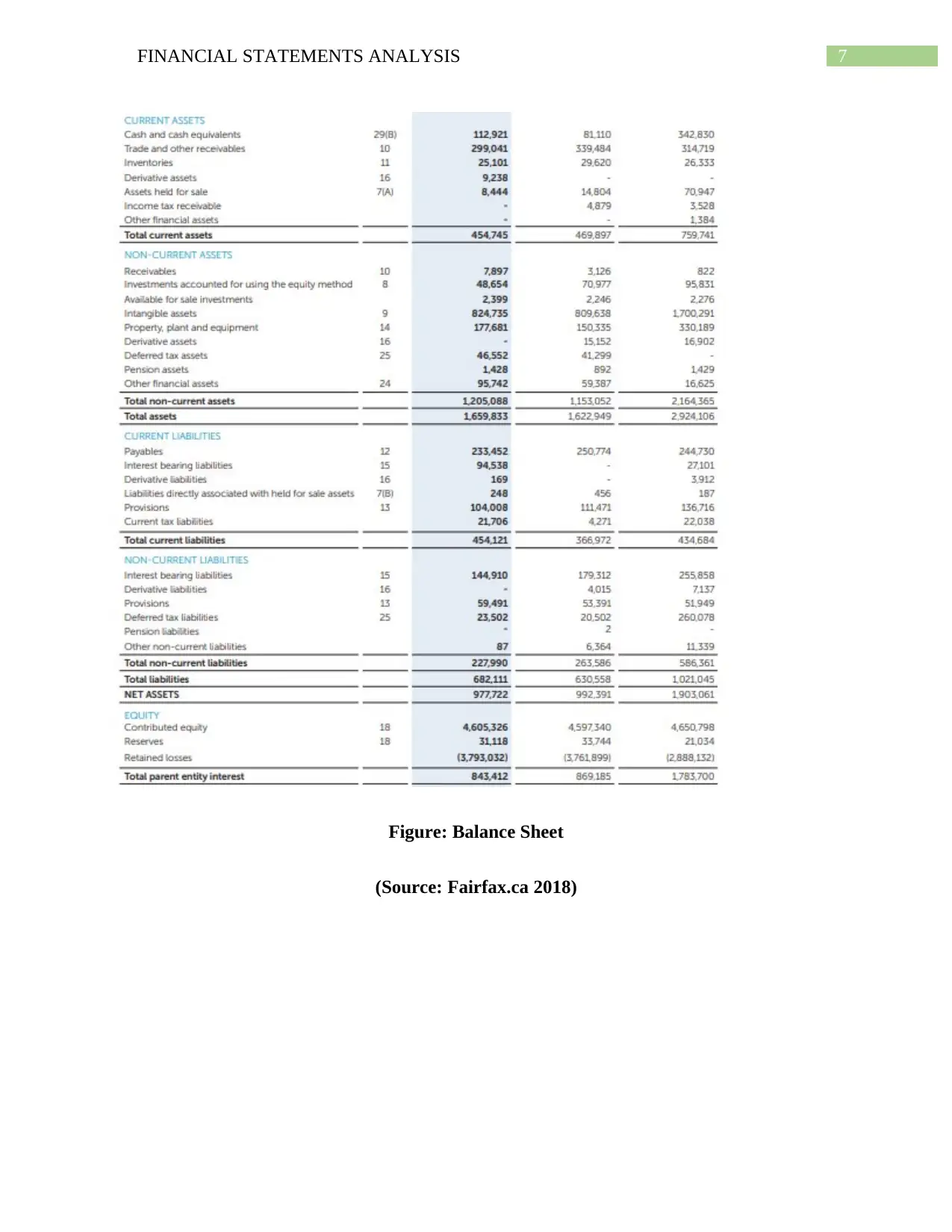

Figure: Balance Sheet

(Source: Fairfax.ca 2018)

Figure: Balance Sheet

(Source: Fairfax.ca 2018)

8FINANCIAL STATEMENTS ANALYSIS

6. Reclassification of the leased item

The hypothetical situation where reclassification of leased items would be required can

be explained by presenting the issue. Some of the examples depicting the situation of leased

items reclassification are listed below:

It is experienced by lease to have the option of purchasing the assets at a price that is

below the fair value o assets and it is at an expected price.

It is resulted by lessors to have the ownership of assets transferred to the lease by the end

of lease term.

Leases are enabled as indicated by the nature of leased assets to perform the

incorporation without making any major modifications.

7. Non-current asset – impairment method

In this particular question, details of particular noncurrent assets have been asked to

evaluate along with explaining the valuation of the same. The particular asset that has been

selected from the statement of financial position under the heading in current assets is

receivables. Receivables are the amounts that are yet to be received from debtors of company.

Total amount of receivables that have been recorded in the statement stood at $ 7897 in year

2017 compared to $ 3126 in year 2016 indicating that there is considerable increase in total

amount of receivables attributable to company (Fairfax.ca 2018).

The statement of financial position of group as on 25th June, 2017 involves a non current

asset relating to party loan receivable that is due from equity investee that is Stan entertainment

6. Reclassification of the leased item

The hypothetical situation where reclassification of leased items would be required can

be explained by presenting the issue. Some of the examples depicting the situation of leased

items reclassification are listed below:

It is experienced by lease to have the option of purchasing the assets at a price that is

below the fair value o assets and it is at an expected price.

It is resulted by lessors to have the ownership of assets transferred to the lease by the end

of lease term.

Leases are enabled as indicated by the nature of leased assets to perform the

incorporation without making any major modifications.

7. Non-current asset – impairment method

In this particular question, details of particular noncurrent assets have been asked to

evaluate along with explaining the valuation of the same. The particular asset that has been

selected from the statement of financial position under the heading in current assets is

receivables. Receivables are the amounts that are yet to be received from debtors of company.

Total amount of receivables that have been recorded in the statement stood at $ 7897 in year

2017 compared to $ 3126 in year 2016 indicating that there is considerable increase in total

amount of receivables attributable to company (Fairfax.ca 2018).

The statement of financial position of group as on 25th June, 2017 involves a non current

asset relating to party loan receivable that is due from equity investee that is Stan entertainment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL STATEMENTS ANALYSIS

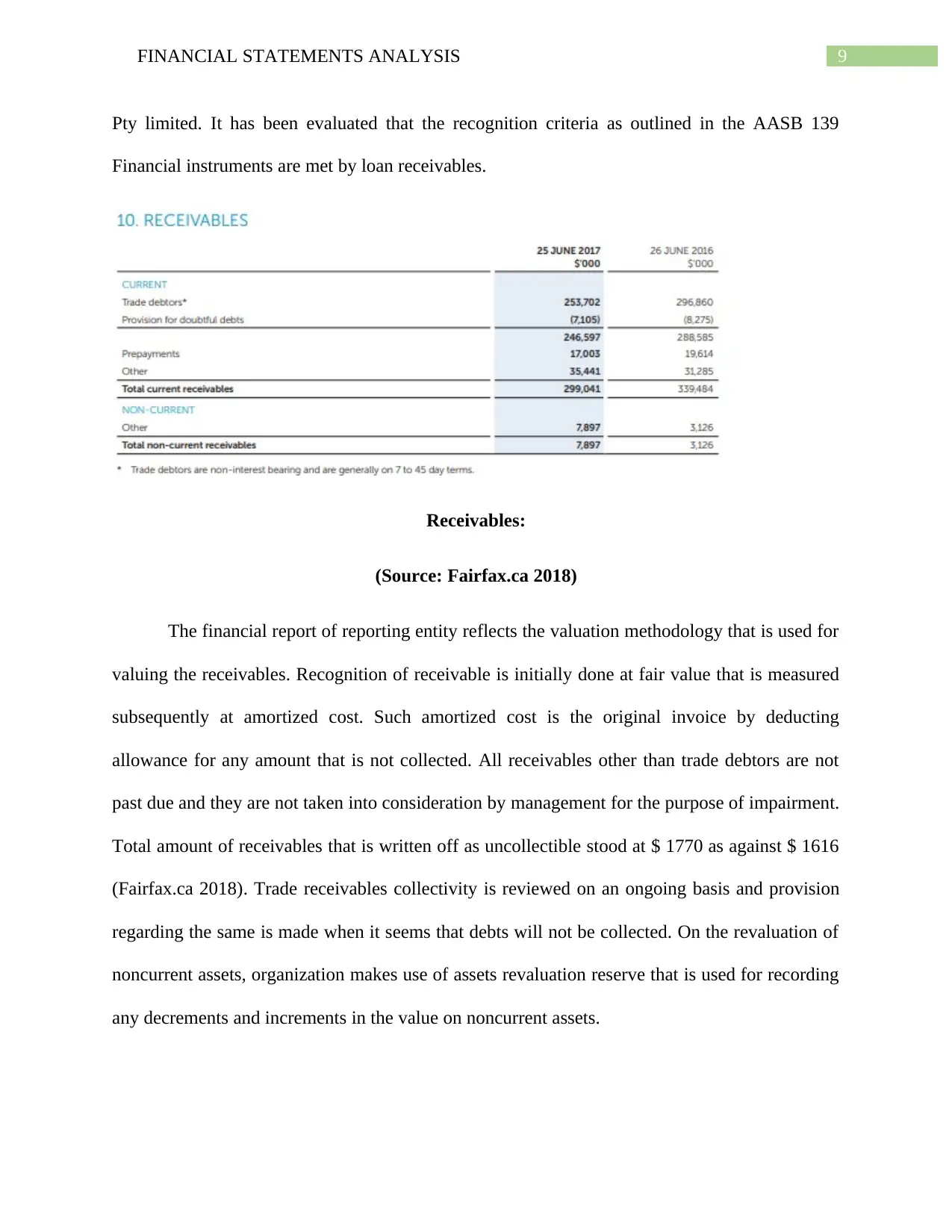

Pty limited. It has been evaluated that the recognition criteria as outlined in the AASB 139

Financial instruments are met by loan receivables.

Receivables:

(Source: Fairfax.ca 2018)

The financial report of reporting entity reflects the valuation methodology that is used for

valuing the receivables. Recognition of receivable is initially done at fair value that is measured

subsequently at amortized cost. Such amortized cost is the original invoice by deducting

allowance for any amount that is not collected. All receivables other than trade debtors are not

past due and they are not taken into consideration by management for the purpose of impairment.

Total amount of receivables that is written off as uncollectible stood at $ 1770 as against $ 1616

(Fairfax.ca 2018). Trade receivables collectivity is reviewed on an ongoing basis and provision

regarding the same is made when it seems that debts will not be collected. On the revaluation of

noncurrent assets, organization makes use of assets revaluation reserve that is used for recording

any decrements and increments in the value on noncurrent assets.

Pty limited. It has been evaluated that the recognition criteria as outlined in the AASB 139

Financial instruments are met by loan receivables.

Receivables:

(Source: Fairfax.ca 2018)

The financial report of reporting entity reflects the valuation methodology that is used for

valuing the receivables. Recognition of receivable is initially done at fair value that is measured

subsequently at amortized cost. Such amortized cost is the original invoice by deducting

allowance for any amount that is not collected. All receivables other than trade debtors are not

past due and they are not taken into consideration by management for the purpose of impairment.

Total amount of receivables that is written off as uncollectible stood at $ 1770 as against $ 1616

(Fairfax.ca 2018). Trade receivables collectivity is reviewed on an ongoing basis and provision

regarding the same is made when it seems that debts will not be collected. On the revaluation of

noncurrent assets, organization makes use of assets revaluation reserve that is used for recording

any decrements and increments in the value on noncurrent assets.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL STATEMENTS ANALYSIS

8. Valuation Method for Non Current Assets

An alternative method that can be used for valuing the noncurrent assets with reference to

the qualitative characteristics would be the valuation using historical cost or taking into account

fair value methodology. Implementation of these two measures that is fair value and historical

cost, would have the consequence of increasing the valuation of any specific account that would

be impacted negatively. However, it would be suitable to use the technique of fair value

compared to valuation using the historical cost. It is due to this particular fact that the accounting

board refers organization to employ the method of fair valuation for measuring the noncurrent

assets.

Conclusion:

A detailed analysis of various accounts to financial statements of Fairfax limited has been

presented in the report by referring to the annual report. Evaluation of several accounts such as

contingencies, provisions, noncurrent assets and valuation methodology has been discussed and

based on findings, conclusions have been drawn. It can be inferred from the above analysis that

reporting entity has more or less adhered to several accounting standards when evaluating

accounts as recommended by the accounting standard board. It is indicative of the fact that

accounting statements have been prepared with due care and diligence. However, it has also been

ascertained that there are not detailed disclosure regarding the valuation technique of some

noncurrent assets and proper disclosure in relation to contingencies. It is therefore recommended

to enhance the disclosure and make further improvement in quality of financial reporting.

8. Valuation Method for Non Current Assets

An alternative method that can be used for valuing the noncurrent assets with reference to

the qualitative characteristics would be the valuation using historical cost or taking into account

fair value methodology. Implementation of these two measures that is fair value and historical

cost, would have the consequence of increasing the valuation of any specific account that would

be impacted negatively. However, it would be suitable to use the technique of fair value

compared to valuation using the historical cost. It is due to this particular fact that the accounting

board refers organization to employ the method of fair valuation for measuring the noncurrent

assets.

Conclusion:

A detailed analysis of various accounts to financial statements of Fairfax limited has been

presented in the report by referring to the annual report. Evaluation of several accounts such as

contingencies, provisions, noncurrent assets and valuation methodology has been discussed and

based on findings, conclusions have been drawn. It can be inferred from the above analysis that

reporting entity has more or less adhered to several accounting standards when evaluating

accounts as recommended by the accounting standard board. It is indicative of the fact that

accounting statements have been prepared with due care and diligence. However, it has also been

ascertained that there are not detailed disclosure regarding the valuation technique of some

noncurrent assets and proper disclosure in relation to contingencies. It is therefore recommended

to enhance the disclosure and make further improvement in quality of financial reporting.

11FINANCIAL STATEMENTS ANALYSIS

References list:

Armstrong, C., Guay, W.R., Mehran, H. and Weber, J., 2015. The role of information and

financial reporting in corporate governance: A review of the evidence and the implications for

banking firms and the financial services industry.

Beck, M.J., Glendening, M. and Hogan, C.E., 2016. Financial Statement Disaggregation,

Auditor Effort and Financial Reporting Quality. working paper, Michigan State University.

Dye, R.A., 2017. Some recent advances in the theory of financial reporting and

disclosures. Accounting Horizons, 31(3), pp.39-54.

Fairfax.ca. (2018). Fairfax - Financials - Annual Reports . [online] Available at:

https://www.fairfax.ca/financials/annual-reports/default.aspx [Accessed 21 May 2018].

Feng, M., Li, C., McVay, S.E. and Skaife, H., 2014. Does ineffective internal control over

financial reporting affect a firm's operations? Evidence from firms' inventory management. The

Accounting Review, 90(2), pp.529-557.

Martínez‐Ferrero, J., Garcia‐Sanchez, I.M. and Cuadrado‐Ballesteros, B., 2015. Effect of

financial reporting quality on sustainability information disclosure. Corporate Social

Responsibility and Environmental Management, 22(1), pp.45-64.

Naranjo, P., Saavedra, D. and Verdi, R., 2017. Financial reporting regulation and financing

decisions.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Patelli, L. and Pedrini, M., 2015. Is tone at the top associated with financial reporting

aggressiveness?. Journal of Business Ethics, 126(1), pp.3-19.

References list:

Armstrong, C., Guay, W.R., Mehran, H. and Weber, J., 2015. The role of information and

financial reporting in corporate governance: A review of the evidence and the implications for

banking firms and the financial services industry.

Beck, M.J., Glendening, M. and Hogan, C.E., 2016. Financial Statement Disaggregation,

Auditor Effort and Financial Reporting Quality. working paper, Michigan State University.

Dye, R.A., 2017. Some recent advances in the theory of financial reporting and

disclosures. Accounting Horizons, 31(3), pp.39-54.

Fairfax.ca. (2018). Fairfax - Financials - Annual Reports . [online] Available at:

https://www.fairfax.ca/financials/annual-reports/default.aspx [Accessed 21 May 2018].

Feng, M., Li, C., McVay, S.E. and Skaife, H., 2014. Does ineffective internal control over

financial reporting affect a firm's operations? Evidence from firms' inventory management. The

Accounting Review, 90(2), pp.529-557.

Martínez‐Ferrero, J., Garcia‐Sanchez, I.M. and Cuadrado‐Ballesteros, B., 2015. Effect of

financial reporting quality on sustainability information disclosure. Corporate Social

Responsibility and Environmental Management, 22(1), pp.45-64.

Naranjo, P., Saavedra, D. and Verdi, R., 2017. Financial reporting regulation and financing

decisions.

Nobes, C., 2014. International Classification of Financial Reporting 3e. Routledge.

Patelli, L. and Pedrini, M., 2015. Is tone at the top associated with financial reporting

aggressiveness?. Journal of Business Ethics, 126(1), pp.3-19.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.