Financial Statement Analysis, Budgeting, and Ratio Calculation Report

VerifiedAdded on 2023/06/08

|14

|3355

|252

Report

AI Summary

This report provides a detailed analysis of financial statements and budgetary control. It examines the purpose of accounting functions within an organization, describing ethical rules and regulations. The report includes the preparation of financial statements for various business structures, calculation of financial ratios, and comparison of company performance over time. A cash budget is prepared, and the advantages and disadvantages of budgets and budgetary planning are discussed. The report utilizes examples from 'Moore Kingston Smith' and 'Village-Wide Catering Company' to illustrate key concepts and financial analysis techniques. Overall, the report offers a comprehensive overview of financial accounting and its practical application in business settings.

FINANCIAL

STATEMENTS AND

BUDGETARY

CONTROL

STATEMENTS AND

BUDGETARY

CONTROL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

P1. Examine the purpose of the accounting function of an organisation ...................................3

P2. Describe the various functions of accounting established inside the company which is

related to its various ethical rules and regulations. ....................................................................4

P3. Compose the financial statements with the help of the provided trial balance for sole

traders, partnerships and not-for-profit organisations, to join the accounting principles,

conventions and standards..........................................................................................................6

P4. Calculate the different types of financial ratios using final accounts of Village – Wide

Catering Company......................................................................................................................8

P5. Perform a Comparison of the presentation of the company over time while using the

financial ratios...........................................................................................................................10

P6. Prepare a cash budget from given data for an organisation using a spreadsheet................12

P7. The advantages and disadvantages of budgets and budgetary planning and control for an

organisation...............................................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

P1. Examine the purpose of the accounting function of an organisation ...................................3

P2. Describe the various functions of accounting established inside the company which is

related to its various ethical rules and regulations. ....................................................................4

P3. Compose the financial statements with the help of the provided trial balance for sole

traders, partnerships and not-for-profit organisations, to join the accounting principles,

conventions and standards..........................................................................................................6

P4. Calculate the different types of financial ratios using final accounts of Village – Wide

Catering Company......................................................................................................................8

P5. Perform a Comparison of the presentation of the company over time while using the

financial ratios...........................................................................................................................10

P6. Prepare a cash budget from given data for an organisation using a spreadsheet................12

P7. The advantages and disadvantages of budgets and budgetary planning and control for an

organisation...............................................................................................................................12

CONCLUSION .............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

The primary purpose of the financial statements is to provide the financial information to

the user of those informations in making financial decision. They do not provide non-financial

information to the user whether they are relevant for making economic decision. Financial

statements are prepared on the basis of going concern assumption. Financial statements contain

Balance sheet, Profit and loss and cash flow statement. All the elements of the financial

statements are related each other because they show various aspects of same transaction.

Budgetary control is managing income and expenditure. It is prepared for future on the basis of

past data. It is a control technique where budgeted results are compared with actual results. In

this report, a detailed analysis has been performed on the accounting function of 'Moore

Kingston Smith' which is a leading UK based firm. Further in this report preparation of financial

statements of Village Wide Catering Company and also calculated of financial ratios and

comparison of the organisation performance using financial ratio. Further in this report

preparation of cash budget and discuss the benefits and limitation of budgets and budgetary

planning (Cannizzaro and et.al, 2018).

MAIN BODY

P1. Examine the purpose of the accounting function of an organisation

Accounting functions means the tracking, recording, storing and summarising of a

company's financial transactions. The company maintains a systematic record of transaction so

that they can make accessible for audits. These financial statements help management in

decision-making. The company can use financial statements to identify the weakness and

strength of the organisation.

The main objective of the accounting is to providing the information to the owners and

management so that they will take better decision of the business entity. The entity can use

reports, budget and cost data for increased profits and reducing cost (Bruno, and Lapsley, 2018).

The basic function of the accounting they are as follow-

1. To keeping records- It is the basic of the accounting. The accounting is helped to

maintain day to day transaction such as sales, purchase, receipts and payments.

The primary purpose of the financial statements is to provide the financial information to

the user of those informations in making financial decision. They do not provide non-financial

information to the user whether they are relevant for making economic decision. Financial

statements are prepared on the basis of going concern assumption. Financial statements contain

Balance sheet, Profit and loss and cash flow statement. All the elements of the financial

statements are related each other because they show various aspects of same transaction.

Budgetary control is managing income and expenditure. It is prepared for future on the basis of

past data. It is a control technique where budgeted results are compared with actual results. In

this report, a detailed analysis has been performed on the accounting function of 'Moore

Kingston Smith' which is a leading UK based firm. Further in this report preparation of financial

statements of Village Wide Catering Company and also calculated of financial ratios and

comparison of the organisation performance using financial ratio. Further in this report

preparation of cash budget and discuss the benefits and limitation of budgets and budgetary

planning (Cannizzaro and et.al, 2018).

MAIN BODY

P1. Examine the purpose of the accounting function of an organisation

Accounting functions means the tracking, recording, storing and summarising of a

company's financial transactions. The company maintains a systematic record of transaction so

that they can make accessible for audits. These financial statements help management in

decision-making. The company can use financial statements to identify the weakness and

strength of the organisation.

The main objective of the accounting is to providing the information to the owners and

management so that they will take better decision of the business entity. The entity can use

reports, budget and cost data for increased profits and reducing cost (Bruno, and Lapsley, 2018).

The basic function of the accounting they are as follow-

1. To keeping records- It is the basic of the accounting. The accounting is helped to

maintain day to day transaction such as sales, purchase, receipts and payments.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Preparing budgets- The company prepares the budget to determine the difference

between actual results and budgeted results.

3. Complying rules and regulation- Accounting helps that the company follows proper rules

and regulations which is related to taxation and financial reporting.

4. To deduct fraud and error- The accountant helps to deduct fraud and error and

determined no wastage of money occur in the company.

5. Performance reviewing- Accounting reviews daily financial performance and reducing

wastage and increase overall performance of an organisation (Aobdia, 2019).

'Moore Kingston Smith' which is leading in UK, the accounting team provides a full details

of business, rules and regulation to their customers so that they can take better in the business.

The main function of this organisation to providing valuable services, the customers can change

the world. It is used two forms of accounting:

1. Managerial Accounting- This accounting is used for the purpose of controlling the

internal function of the organisation. To use of managerial accounting, the owner can

save the future and take the better decision.

2. Financial Accounting- To analysis the past data with the objective of determining the

organisation value. Shareholders use this information and determined the value of an

organisation.

P2. Describe the various functions of accounting established inside the company which is related

to its various ethical rules and regulations.

Accounting ethics includes the following particular rules and guidelines fixed by the

governing institutions which must be followed by each and every individual who is associated

with accounting as a subject to prevent and preclude the misuse of the financial data, information

or the administrative or managerial position. There are various ethical rules and regulations

established in accounting to prevent any misuse of the authority and managerial positions or any

unethical constraints that may occur in the normal working of the society (Abdullayev and et.al,

2019). Access to Data and Privacy Issues: An accountant has very high access to a lot of

information and subject matters that are heavily confidential to the respective parties,

which is very necessary to be protected at all costs. Failing to protect such necessary

informations and not keeping such data confidential for the purpose of taking benefit of

between actual results and budgeted results.

3. Complying rules and regulation- Accounting helps that the company follows proper rules

and regulations which is related to taxation and financial reporting.

4. To deduct fraud and error- The accountant helps to deduct fraud and error and

determined no wastage of money occur in the company.

5. Performance reviewing- Accounting reviews daily financial performance and reducing

wastage and increase overall performance of an organisation (Aobdia, 2019).

'Moore Kingston Smith' which is leading in UK, the accounting team provides a full details

of business, rules and regulation to their customers so that they can take better in the business.

The main function of this organisation to providing valuable services, the customers can change

the world. It is used two forms of accounting:

1. Managerial Accounting- This accounting is used for the purpose of controlling the

internal function of the organisation. To use of managerial accounting, the owner can

save the future and take the better decision.

2. Financial Accounting- To analysis the past data with the objective of determining the

organisation value. Shareholders use this information and determined the value of an

organisation.

P2. Describe the various functions of accounting established inside the company which is related

to its various ethical rules and regulations.

Accounting ethics includes the following particular rules and guidelines fixed by the

governing institutions which must be followed by each and every individual who is associated

with accounting as a subject to prevent and preclude the misuse of the financial data, information

or the administrative or managerial position. There are various ethical rules and regulations

established in accounting to prevent any misuse of the authority and managerial positions or any

unethical constraints that may occur in the normal working of the society (Abdullayev and et.al,

2019). Access to Data and Privacy Issues: An accountant has very high access to a lot of

information and subject matters that are heavily confidential to the respective parties,

which is very necessary to be protected at all costs. Failing to protect such necessary

informations and not keeping such data confidential for the purpose of taking benefit of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

any future development or drop in the company's valueis among the major issues faced in

accounting. Communicating and distributing any such information which is related to the

company to any outsider or making it realizable for the competitors to steal or purchase

company's data or confidential information through neglect is also an ethical issues

(Elghaish and et.al, 2020).

Conflicts of Interests : This is a very prevalent and common ethical issue in almost all

the organisations in today's times. For example: if the higher authorities of the

organisation receive their appraisals based on the stock prices of the company that prevail

in the market, it is very possible that all the stock decisions that are made by the higher

authorities are dependent on the base to favour those decisions which increase the value

of company's stocks. They will favour and try for this situation even if the increase in

these stock prices is not good or not in favour of the company and its financial health.

This clearly builds for the biases that keep building in the culture of the company and it

creates a bulk of problem that keep occurring with time (Jia and et.al, 2020).

accounting. Communicating and distributing any such information which is related to the

company to any outsider or making it realizable for the competitors to steal or purchase

company's data or confidential information through neglect is also an ethical issues

(Elghaish and et.al, 2020).

Conflicts of Interests : This is a very prevalent and common ethical issue in almost all

the organisations in today's times. For example: if the higher authorities of the

organisation receive their appraisals based on the stock prices of the company that prevail

in the market, it is very possible that all the stock decisions that are made by the higher

authorities are dependent on the base to favour those decisions which increase the value

of company's stocks. They will favour and try for this situation even if the increase in

these stock prices is not good or not in favour of the company and its financial health.

This clearly builds for the biases that keep building in the culture of the company and it

creates a bulk of problem that keep occurring with time (Jia and et.al, 2020).

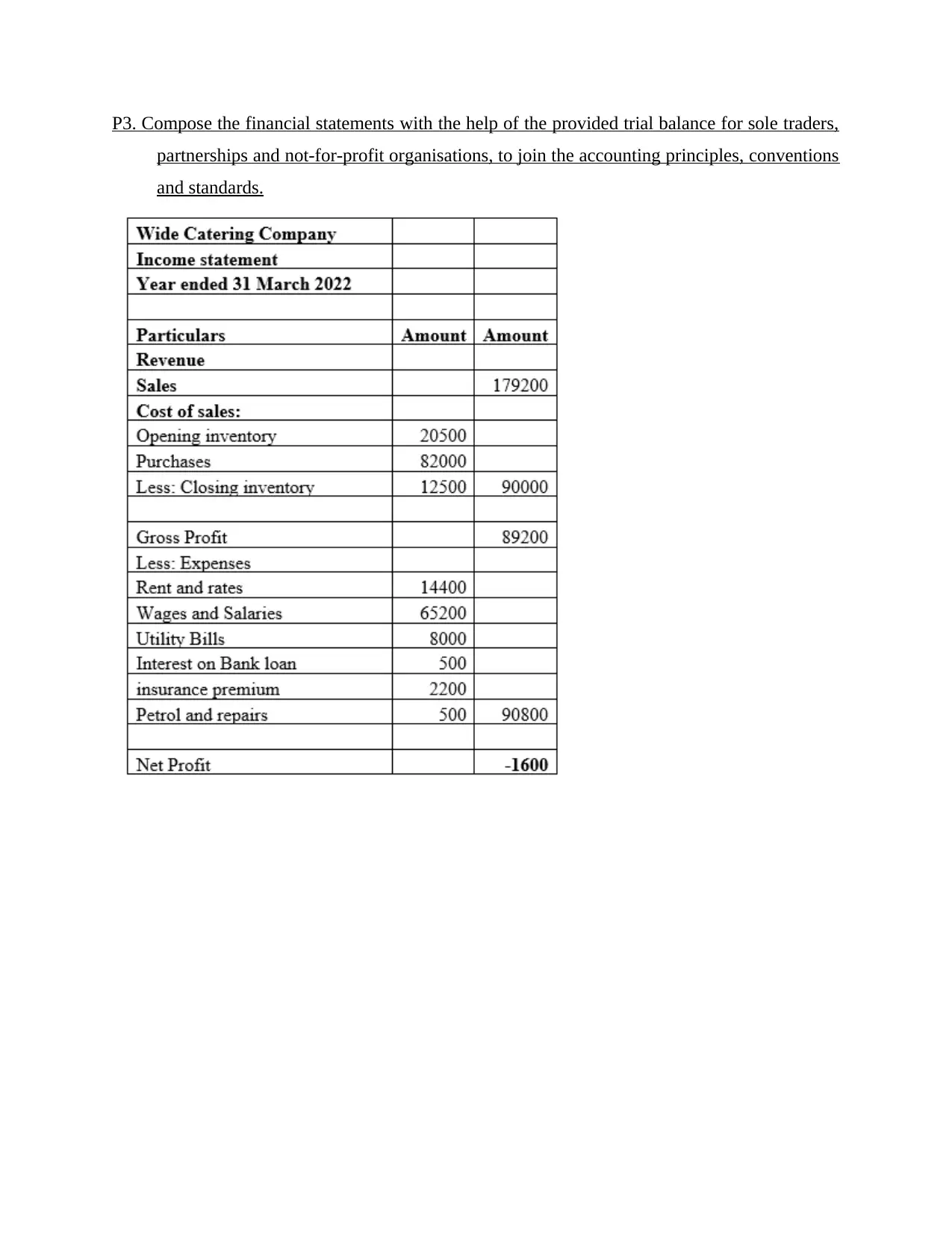

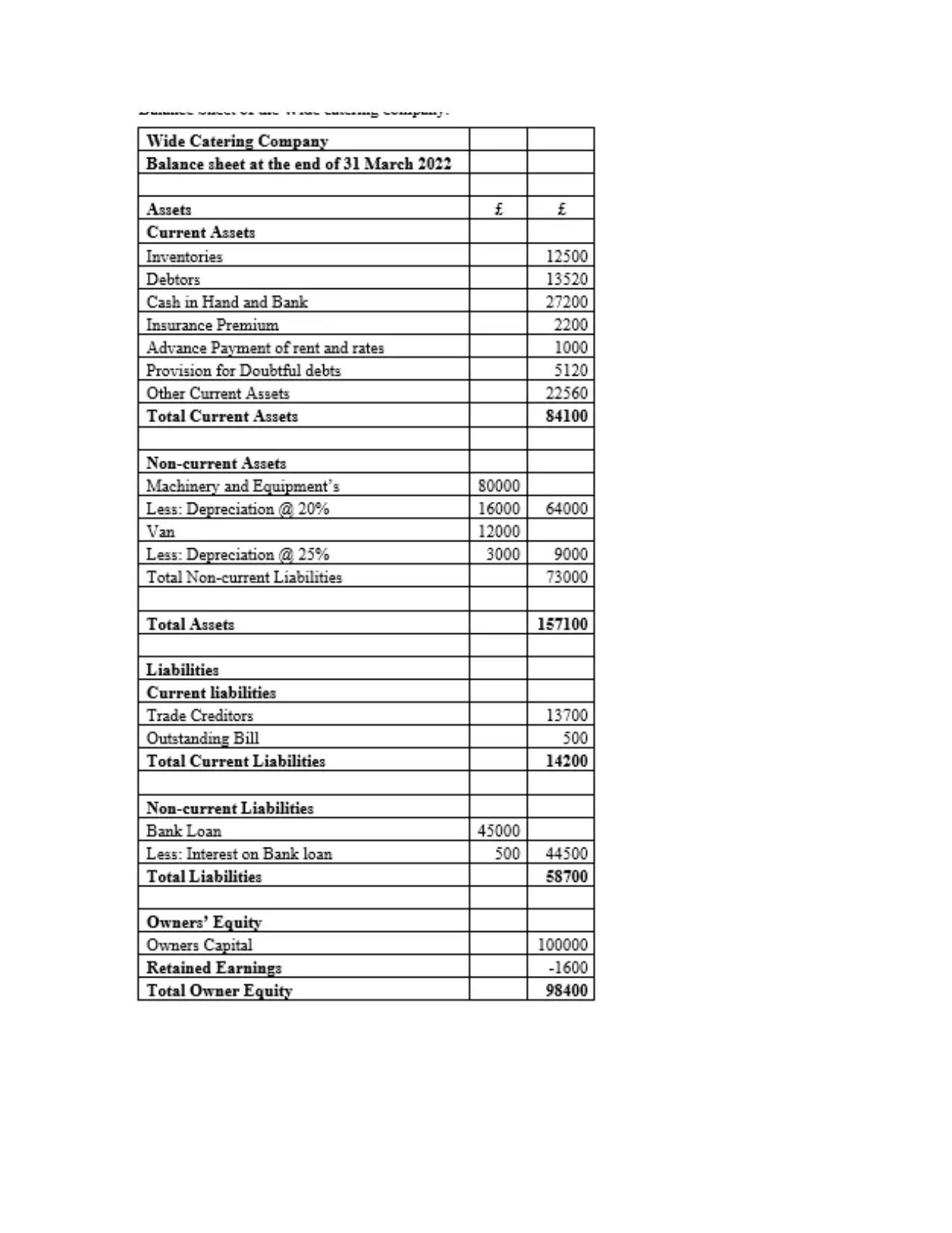

P3. Compose the financial statements with the help of the provided trial balance for sole traders,

partnerships and not-for-profit organisations, to join the accounting principles, conventions

and standards.

partnerships and not-for-profit organisations, to join the accounting principles, conventions

and standards.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

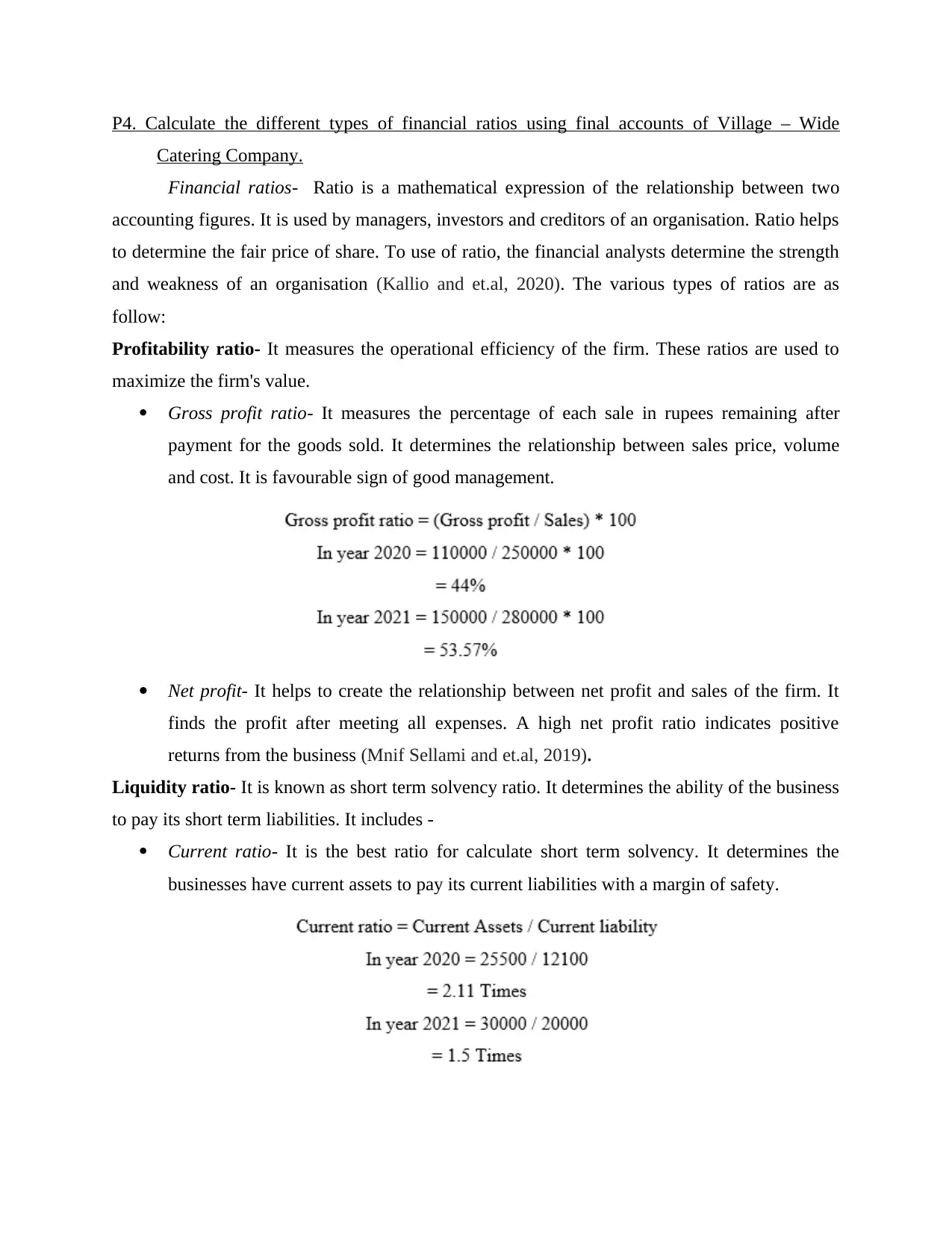

P4. Calculate the different types of financial ratios using final accounts of Village – Wide

Catering Company.

Financial ratios- Ratio is a mathematical expression of the relationship between two

accounting figures. It is used by managers, investors and creditors of an organisation. Ratio helps

to determine the fair price of share. To use of ratio, the financial analysts determine the strength

and weakness of an organisation (Kallio and et.al, 2020). The various types of ratios are as

follow:

Profitability ratio- It measures the operational efficiency of the firm. These ratios are used to

maximize the firm's value.

Gross profit ratio- It measures the percentage of each sale in rupees remaining after

payment for the goods sold. It determines the relationship between sales price, volume

and cost. It is favourable sign of good management.

Net profit- It helps to create the relationship between net profit and sales of the firm. It

finds the profit after meeting all expenses. A high net profit ratio indicates positive

returns from the business (Mnif Sellami and et.al, 2019).

Liquidity ratio- It is known as short term solvency ratio. It determines the ability of the business

to pay its short term liabilities. It includes -

Current ratio- It is the best ratio for calculate short term solvency. It determines the

businesses have current assets to pay its current liabilities with a margin of safety.

Catering Company.

Financial ratios- Ratio is a mathematical expression of the relationship between two

accounting figures. It is used by managers, investors and creditors of an organisation. Ratio helps

to determine the fair price of share. To use of ratio, the financial analysts determine the strength

and weakness of an organisation (Kallio and et.al, 2020). The various types of ratios are as

follow:

Profitability ratio- It measures the operational efficiency of the firm. These ratios are used to

maximize the firm's value.

Gross profit ratio- It measures the percentage of each sale in rupees remaining after

payment for the goods sold. It determines the relationship between sales price, volume

and cost. It is favourable sign of good management.

Net profit- It helps to create the relationship between net profit and sales of the firm. It

finds the profit after meeting all expenses. A high net profit ratio indicates positive

returns from the business (Mnif Sellami and et.al, 2019).

Liquidity ratio- It is known as short term solvency ratio. It determines the ability of the business

to pay its short term liabilities. It includes -

Current ratio- It is the best ratio for calculate short term solvency. It determines the

businesses have current assets to pay its current liabilities with a margin of safety.

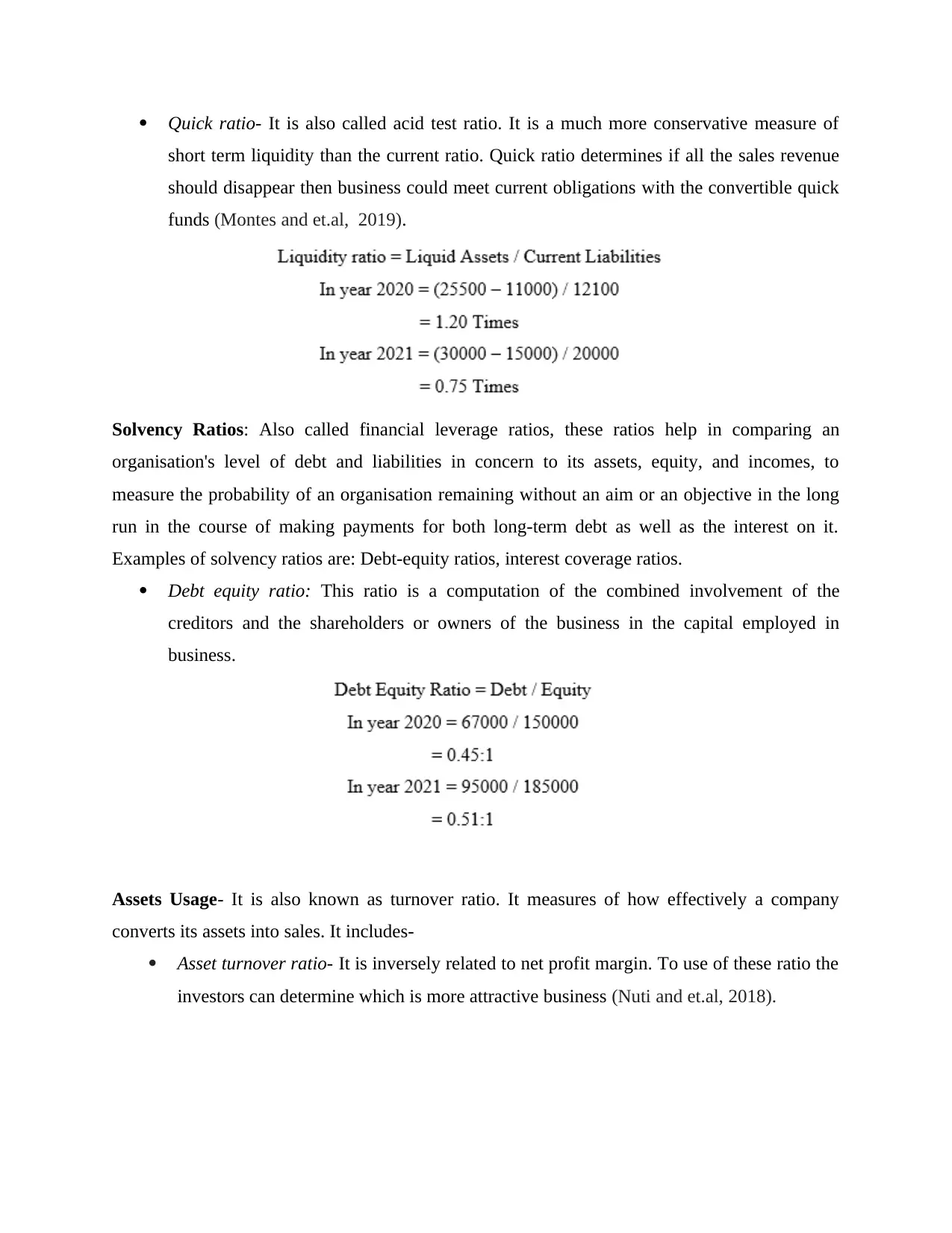

Quick ratio- It is also called acid test ratio. It is a much more conservative measure of

short term liquidity than the current ratio. Quick ratio determines if all the sales revenue

should disappear then business could meet current obligations with the convertible quick

funds (Montes and et.al, 2019).

Solvency Ratios: Also called financial leverage ratios, these ratios help in comparing an

organisation's level of debt and liabilities in concern to its assets, equity, and incomes, to

measure the probability of an organisation remaining without an aim or an objective in the long

run in the course of making payments for both long-term debt as well as the interest on it.

Examples of solvency ratios are: Debt-equity ratios, interest coverage ratios.

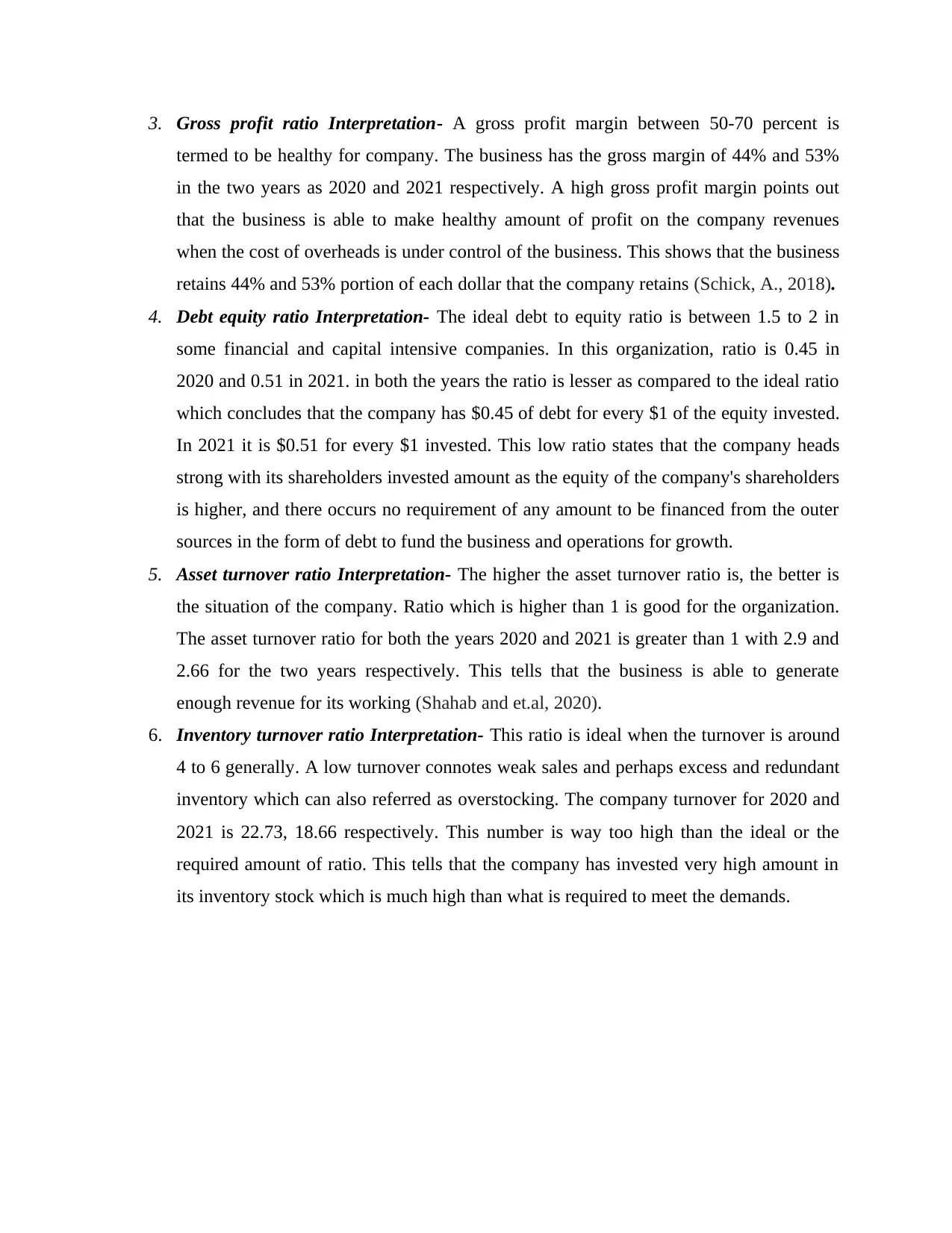

Debt equity ratio: This ratio is a computation of the combined involvement of the

creditors and the shareholders or owners of the business in the capital employed in

business.

Assets Usage- It is also known as turnover ratio. It measures of how effectively a company

converts its assets into sales. It includes-

Asset turnover ratio- It is inversely related to net profit margin. To use of these ratio the

investors can determine which is more attractive business (Nuti and et.al, 2018).

short term liquidity than the current ratio. Quick ratio determines if all the sales revenue

should disappear then business could meet current obligations with the convertible quick

funds (Montes and et.al, 2019).

Solvency Ratios: Also called financial leverage ratios, these ratios help in comparing an

organisation's level of debt and liabilities in concern to its assets, equity, and incomes, to

measure the probability of an organisation remaining without an aim or an objective in the long

run in the course of making payments for both long-term debt as well as the interest on it.

Examples of solvency ratios are: Debt-equity ratios, interest coverage ratios.

Debt equity ratio: This ratio is a computation of the combined involvement of the

creditors and the shareholders or owners of the business in the capital employed in

business.

Assets Usage- It is also known as turnover ratio. It measures of how effectively a company

converts its assets into sales. It includes-

Asset turnover ratio- It is inversely related to net profit margin. To use of these ratio the

investors can determine which is more attractive business (Nuti and et.al, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory turnover ratio: It helps to calculate how many number of times the stock is

sold or utilised in a fixed time period. It is computed to assess and check the amount of

excessive inventory that is present in the company as compared to its sales level (Payne

and et.al, 2018).

P5. Perform a Comparison of the presentation of the company over time while using the financial

ratios.

1. Current ratio Interpretation- The ideal current ratio for organisations is 2:1. From the

ratio calculations made above, it can be concluded that the current ratio of the company

for year 2020 is 2.11 which shows excess of current assets over the current liabilities. In

2021 it is 1.5 which shows that in this year, the amount of current assets with the

company reduced with a significant number and it needs to work on increasing the

current assets with the company so that there is no shortages of such cash and cash

equivalents with the company in the future period (Roussy and et.al, 2018).

2. Quick ratio Interpretation- From the above computation of quick ratio for the two years

in comparison to the ideal ratio of 1:1, it can be seen that in 2020 the company had

better positioning with respect to its liquid assets. Although in 2021 the company fell

short of the liquid assets and the current liabilities also increased and the ratio fell down

as compared to the ideal ratio.

sold or utilised in a fixed time period. It is computed to assess and check the amount of

excessive inventory that is present in the company as compared to its sales level (Payne

and et.al, 2018).

P5. Perform a Comparison of the presentation of the company over time while using the financial

ratios.

1. Current ratio Interpretation- The ideal current ratio for organisations is 2:1. From the

ratio calculations made above, it can be concluded that the current ratio of the company

for year 2020 is 2.11 which shows excess of current assets over the current liabilities. In

2021 it is 1.5 which shows that in this year, the amount of current assets with the

company reduced with a significant number and it needs to work on increasing the

current assets with the company so that there is no shortages of such cash and cash

equivalents with the company in the future period (Roussy and et.al, 2018).

2. Quick ratio Interpretation- From the above computation of quick ratio for the two years

in comparison to the ideal ratio of 1:1, it can be seen that in 2020 the company had

better positioning with respect to its liquid assets. Although in 2021 the company fell

short of the liquid assets and the current liabilities also increased and the ratio fell down

as compared to the ideal ratio.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Gross profit ratio Interpretation- A gross profit margin between 50-70 percent is

termed to be healthy for company. The business has the gross margin of 44% and 53%

in the two years as 2020 and 2021 respectively. A high gross profit margin points out

that the business is able to make healthy amount of profit on the company revenues

when the cost of overheads is under control of the business. This shows that the business

retains 44% and 53% portion of each dollar that the company retains (Schick, A., 2018).

4. Debt equity ratio Interpretation- The ideal debt to equity ratio is between 1.5 to 2 in

some financial and capital intensive companies. In this organization, ratio is 0.45 in

2020 and 0.51 in 2021. in both the years the ratio is lesser as compared to the ideal ratio

which concludes that the company has $0.45 of debt for every $1 of the equity invested.

In 2021 it is $0.51 for every $1 invested. This low ratio states that the company heads

strong with its shareholders invested amount as the equity of the company's shareholders

is higher, and there occurs no requirement of any amount to be financed from the outer

sources in the form of debt to fund the business and operations for growth.

5. Asset turnover ratio Interpretation- The higher the asset turnover ratio is, the better is

the situation of the company. Ratio which is higher than 1 is good for the organization.

The asset turnover ratio for both the years 2020 and 2021 is greater than 1 with 2.9 and

2.66 for the two years respectively. This tells that the business is able to generate

enough revenue for its working (Shahab and et.al, 2020).

6. Inventory turnover ratio Interpretation- This ratio is ideal when the turnover is around

4 to 6 generally. A low turnover connotes weak sales and perhaps excess and redundant

inventory which can also referred as overstocking. The company turnover for 2020 and

2021 is 22.73, 18.66 respectively. This number is way too high than the ideal or the

required amount of ratio. This tells that the company has invested very high amount in

its inventory stock which is much high than what is required to meet the demands.

termed to be healthy for company. The business has the gross margin of 44% and 53%

in the two years as 2020 and 2021 respectively. A high gross profit margin points out

that the business is able to make healthy amount of profit on the company revenues

when the cost of overheads is under control of the business. This shows that the business

retains 44% and 53% portion of each dollar that the company retains (Schick, A., 2018).

4. Debt equity ratio Interpretation- The ideal debt to equity ratio is between 1.5 to 2 in

some financial and capital intensive companies. In this organization, ratio is 0.45 in

2020 and 0.51 in 2021. in both the years the ratio is lesser as compared to the ideal ratio

which concludes that the company has $0.45 of debt for every $1 of the equity invested.

In 2021 it is $0.51 for every $1 invested. This low ratio states that the company heads

strong with its shareholders invested amount as the equity of the company's shareholders

is higher, and there occurs no requirement of any amount to be financed from the outer

sources in the form of debt to fund the business and operations for growth.

5. Asset turnover ratio Interpretation- The higher the asset turnover ratio is, the better is

the situation of the company. Ratio which is higher than 1 is good for the organization.

The asset turnover ratio for both the years 2020 and 2021 is greater than 1 with 2.9 and

2.66 for the two years respectively. This tells that the business is able to generate

enough revenue for its working (Shahab and et.al, 2020).

6. Inventory turnover ratio Interpretation- This ratio is ideal when the turnover is around

4 to 6 generally. A low turnover connotes weak sales and perhaps excess and redundant

inventory which can also referred as overstocking. The company turnover for 2020 and

2021 is 22.73, 18.66 respectively. This number is way too high than the ideal or the

required amount of ratio. This tells that the company has invested very high amount in

its inventory stock which is much high than what is required to meet the demands.

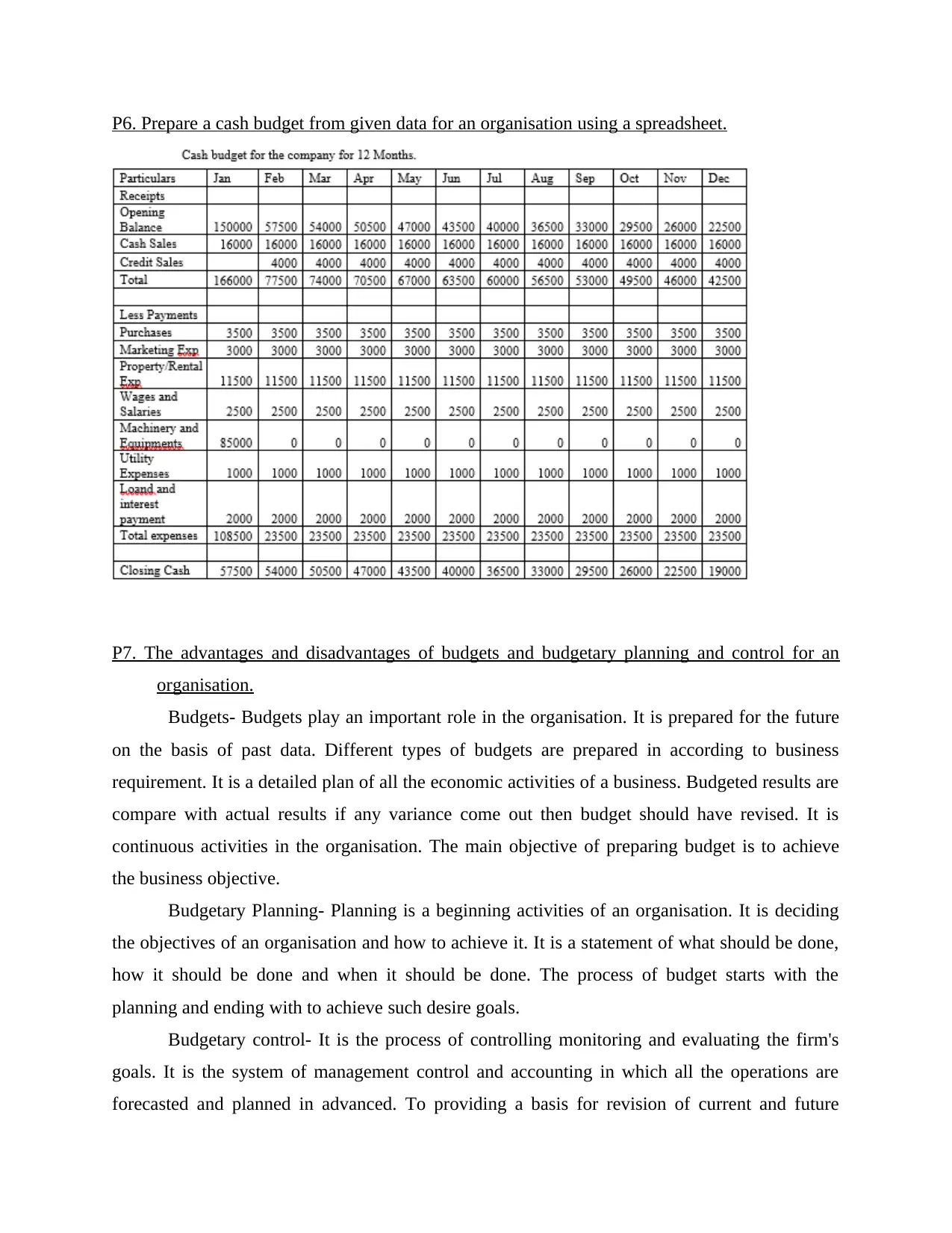

P6. Prepare a cash budget from given data for an organisation using a spreadsheet.

P7. The advantages and disadvantages of budgets and budgetary planning and control for an

organisation.

Budgets- Budgets play an important role in the organisation. It is prepared for the future

on the basis of past data. Different types of budgets are prepared in according to business

requirement. It is a detailed plan of all the economic activities of a business. Budgeted results are

compare with actual results if any variance come out then budget should have revised. It is

continuous activities in the organisation. The main objective of preparing budget is to achieve

the business objective.

Budgetary Planning- Planning is a beginning activities of an organisation. It is deciding

the objectives of an organisation and how to achieve it. It is a statement of what should be done,

how it should be done and when it should be done. The process of budget starts with the

planning and ending with to achieve such desire goals.

Budgetary control- It is the process of controlling monitoring and evaluating the firm's

goals. It is the system of management control and accounting in which all the operations are

forecasted and planned in advanced. To providing a basis for revision of current and future

P7. The advantages and disadvantages of budgets and budgetary planning and control for an

organisation.

Budgets- Budgets play an important role in the organisation. It is prepared for the future

on the basis of past data. Different types of budgets are prepared in according to business

requirement. It is a detailed plan of all the economic activities of a business. Budgeted results are

compare with actual results if any variance come out then budget should have revised. It is

continuous activities in the organisation. The main objective of preparing budget is to achieve

the business objective.

Budgetary Planning- Planning is a beginning activities of an organisation. It is deciding

the objectives of an organisation and how to achieve it. It is a statement of what should be done,

how it should be done and when it should be done. The process of budget starts with the

planning and ending with to achieve such desire goals.

Budgetary control- It is the process of controlling monitoring and evaluating the firm's

goals. It is the system of management control and accounting in which all the operations are

forecasted and planned in advanced. To providing a basis for revision of current and future

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.