Case Study: Financial Statement Analysis & Accounting Concepts

VerifiedAdded on 2023/06/10

|6

|865

|140

Case Study

AI Summary

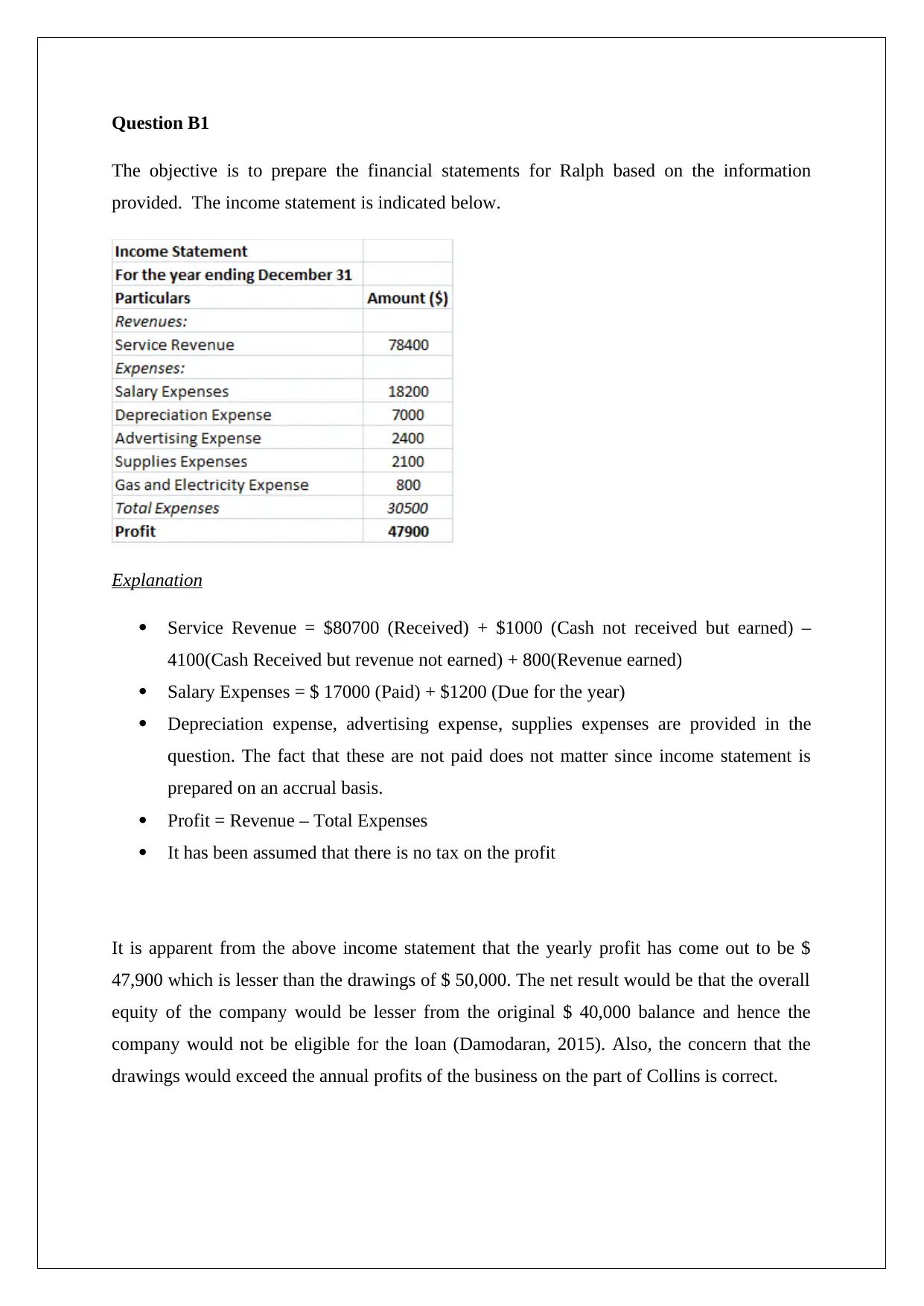

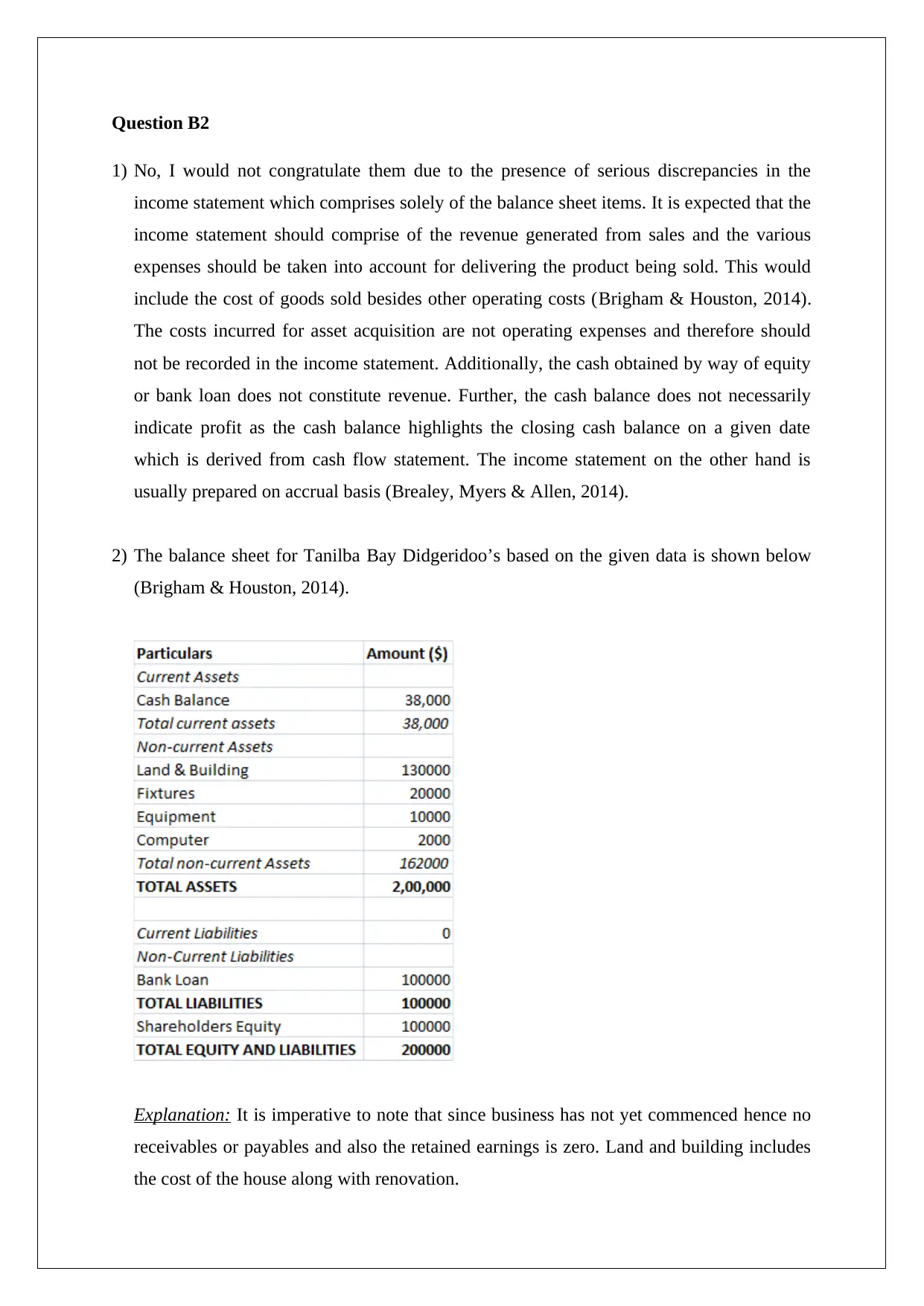

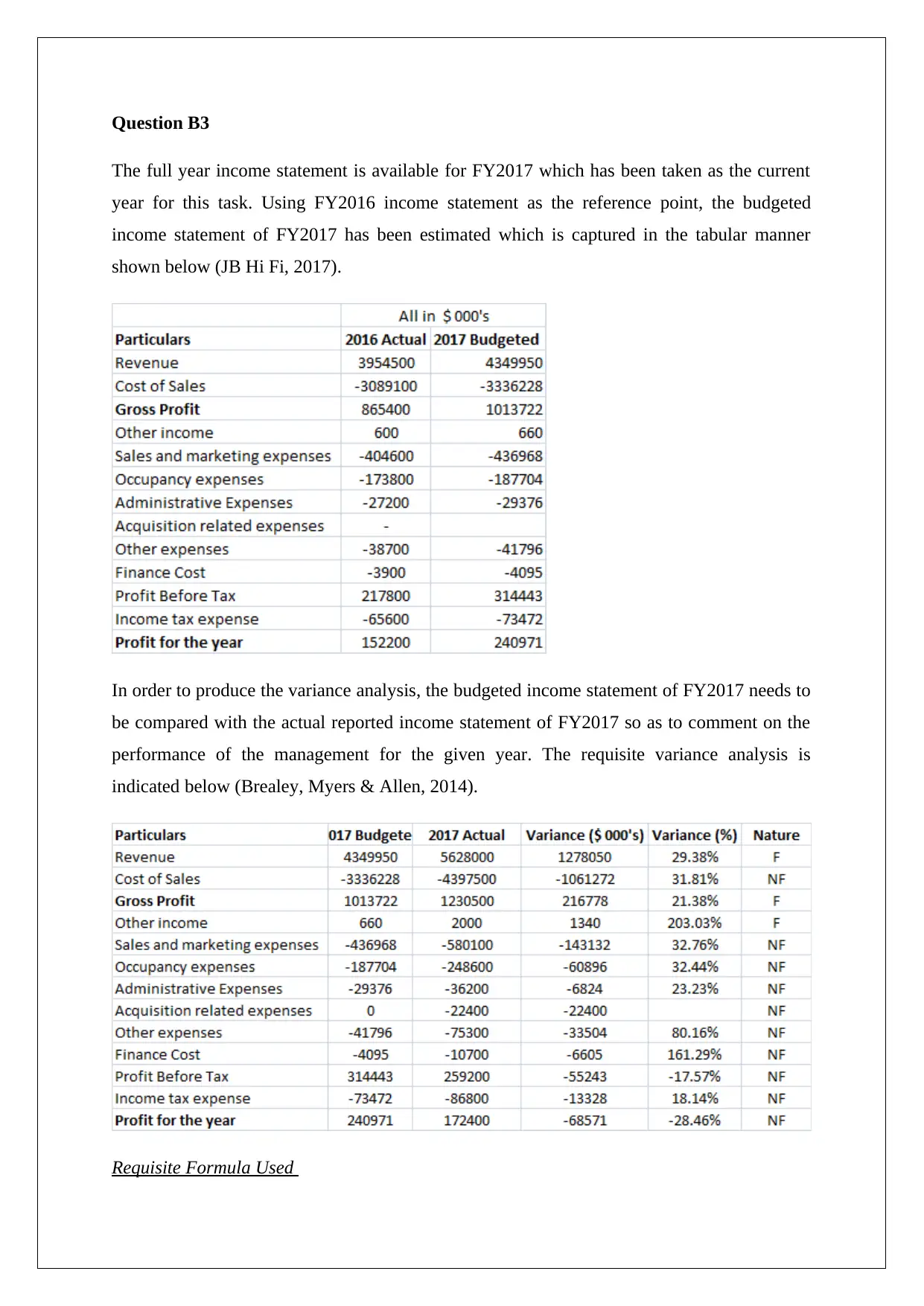

This assignment presents a case study involving financial statement analysis and accounting principles. It includes preparing an income statement for Collins Consignment Sales, identifying discrepancies in a provided income statement, creating a balance sheet for Tanilba Bay Didgeridoo’s, and conducting a variance analysis for JB Hi-Fi's FY2017 income statement. The analysis involves comparing budgeted and actual figures to assess management performance, highlighting the impact of acquisitions on revenue and costs. The document also includes references to relevant finance and accounting literature.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.