Financial Statements of Organization

VerifiedAdded on 2021/05/27

|17

|3672

|32

AI Summary

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

ALDERAN RESOURCES PVT LTD

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

INTRODUCTION OF THE REPORT

Auditing is an independent examination of financial information of an entity whether profit making or not and

irrespective of its size that is small, medium or big or its legal form whether it is a company(whether listed or

unlisted), partnership or any other body corporate and when such examination is conducted with a view to an

express an opinion thereon on the financial statements of the company. This report will describe how the

audit program in practicality is made considering all the important criteria for audit report and taking on the

bifurcated responsibility of management in construction of accounts and auditor’s responsibility to express a

qualified or an unqualified opinion. It will also help in framing an audit programme which will describe the

steps in audit of material account balanced and selected assertions and providing sufficient and appropriate

audit evidence which shall further in turn lead to expressing an opinion thereon.

TEST OF CONTROLS,SUBSTANTIVE TESTS OF TRANSACTIONS AND

SUBSTANTIVE TEST OF BALANCES

Test of controls

Test of controls are that compliance procedures to verify the designing, operation, effectiveness and

continuity of internal control system in the company. Auditor performs the audit procedure with respect to

following assertions:

1. Existence : Whether there are actually internal controls existing in the company or not.

2. Operating effectiveness: It is done to check if the internal controls exist in the company whether

they are operating effectively or not.

3. Consistency: It is also to be checked whether or not the existing internal controls are operated

through out the period.

Substantive procedure

Substantive procedure are performed to check completeness, accuracy and validity of transaction and

balances.

2

Auditing is an independent examination of financial information of an entity whether profit making or not and

irrespective of its size that is small, medium or big or its legal form whether it is a company(whether listed or

unlisted), partnership or any other body corporate and when such examination is conducted with a view to an

express an opinion thereon on the financial statements of the company. This report will describe how the

audit program in practicality is made considering all the important criteria for audit report and taking on the

bifurcated responsibility of management in construction of accounts and auditor’s responsibility to express a

qualified or an unqualified opinion. It will also help in framing an audit programme which will describe the

steps in audit of material account balanced and selected assertions and providing sufficient and appropriate

audit evidence which shall further in turn lead to expressing an opinion thereon.

TEST OF CONTROLS,SUBSTANTIVE TESTS OF TRANSACTIONS AND

SUBSTANTIVE TEST OF BALANCES

Test of controls

Test of controls are that compliance procedures to verify the designing, operation, effectiveness and

continuity of internal control system in the company. Auditor performs the audit procedure with respect to

following assertions:

1. Existence : Whether there are actually internal controls existing in the company or not.

2. Operating effectiveness: It is done to check if the internal controls exist in the company whether

they are operating effectively or not.

3. Consistency: It is also to be checked whether or not the existing internal controls are operated

through out the period.

Substantive procedure

Substantive procedure are performed to check completeness, accuracy and validity of transaction and

balances.

2

Differentiating Substantive test of transactions and substantive

test of balance

Substantive test of transactions Substantive test of balances

These tests are done for the measurement

purpose that is whether the transactions are

recorded in proper period and at proper

amount.

Whether the item is disclosed and

classified as per relevant accounting

policies and relevant statutory laws

and requirement.

Test of balances are done to check

that there is no assets and liabilities

left to be recorded.

It also verifies that event actually took

place during the relevant period.

Identifying and assessing the auditors need to perform

substantive audit procedure

The auditor shall identify and assess the risk of material misstatement at financial level and assertion level

for class of transactions.

The auditor shall identify, evaluate and assess identified risk and perform substantive audit procedure in

following cases:

a) If there is a risk of fraud.

b) Considering whether the transaction is of complex nature.

c) Whether there is transaction which gives rise to related party transaction.

d) The materiality of transactions or the subject matter.

e) When there is risk of significant unusual transaction.

Cases in which the substantive procedures only are not sufficient

The risks which are inaccurate and lead to high risk to significant account balances and where there is high

automation involved and no or minimal manual intervention. In such cases substantive procedure alone are

not sufficient.

3

test of balance

Substantive test of transactions Substantive test of balances

These tests are done for the measurement

purpose that is whether the transactions are

recorded in proper period and at proper

amount.

Whether the item is disclosed and

classified as per relevant accounting

policies and relevant statutory laws

and requirement.

Test of balances are done to check

that there is no assets and liabilities

left to be recorded.

It also verifies that event actually took

place during the relevant period.

Identifying and assessing the auditors need to perform

substantive audit procedure

The auditor shall identify and assess the risk of material misstatement at financial level and assertion level

for class of transactions.

The auditor shall identify, evaluate and assess identified risk and perform substantive audit procedure in

following cases:

a) If there is a risk of fraud.

b) Considering whether the transaction is of complex nature.

c) Whether there is transaction which gives rise to related party transaction.

d) The materiality of transactions or the subject matter.

e) When there is risk of significant unusual transaction.

Cases in which the substantive procedures only are not sufficient

The risks which are inaccurate and lead to high risk to significant account balances and where there is high

automation involved and no or minimal manual intervention. In such cases substantive procedure alone are

not sufficient.

3

Understanding relation of assertions with account balances

Relationship of assertion with respect to account balances:

Valuation: In this it shows whether the asset or liability is recorded at an appropriate value.

Existence: Whether the asset or liability exists at a given date.

Rights and duties of auditor: Whether the assets is a right of entity and liability is a duty of the

entity.

FRAMING AN AUDIT PROGRAMME

Objective of audit

PRIMARY OBJECTIVE:

Audit is conducted to express an opinion

on financial statement that is the primary

objective is reporting. Reporting on

whether the financial statement provides

true and fair view.

SECONDARY OBJECTIVE:

The secondary objective is to detect the

misstatement in financial statement and not to

frame such an opinion if the auditor is unable to

confirm or refute the risk of fraud.

NATURE OF BUSINESS ENTITY:

Business operations: Alderan resources ltd is company that is involved in natural

resources. The company is popularly known in natural resources industry for providing

metal exploration and production services.

Investments and Investments activities: Alderan resources ltd is investing and expanding

aggressively and decided to begin drilling at Accrington and Perseverance which is

company’s current high drilling program.

Financing and financing activities: Recently the company has raised $3 million through

placement of 5 million shares in which maximum are solid and reliable shareholders for

the investment purpose mentioned in above point.

Financial reporting practices: The Company follow the practice of generating quarterly

cash flow statement which shows cash generated from operating activity, investing

4

Relationship of assertion with respect to account balances:

Valuation: In this it shows whether the asset or liability is recorded at an appropriate value.

Existence: Whether the asset or liability exists at a given date.

Rights and duties of auditor: Whether the assets is a right of entity and liability is a duty of the

entity.

FRAMING AN AUDIT PROGRAMME

Objective of audit

PRIMARY OBJECTIVE:

Audit is conducted to express an opinion

on financial statement that is the primary

objective is reporting. Reporting on

whether the financial statement provides

true and fair view.

SECONDARY OBJECTIVE:

The secondary objective is to detect the

misstatement in financial statement and not to

frame such an opinion if the auditor is unable to

confirm or refute the risk of fraud.

NATURE OF BUSINESS ENTITY:

Business operations: Alderan resources ltd is company that is involved in natural

resources. The company is popularly known in natural resources industry for providing

metal exploration and production services.

Investments and Investments activities: Alderan resources ltd is investing and expanding

aggressively and decided to begin drilling at Accrington and Perseverance which is

company’s current high drilling program.

Financing and financing activities: Recently the company has raised $3 million through

placement of 5 million shares in which maximum are solid and reliable shareholders for

the investment purpose mentioned in above point.

Financial reporting practices: The Company follow the practice of generating quarterly

cash flow statement which shows cash generated from operating activity, investing

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

activity and financing activity. So for the quarter ending 31st march 2018 net cash and

cash equivalent was $A6, 43,000.

PERFORMING ANALYTICAL REVIEW PROCEDURE

As per ASA 520 analytical review procedure means evaluation of financial information

through analysis of relationship of both financial and non-financial data.

It includes comparing:

a) Information with prior period

b) Future results such as budgets and forecast

c) Analyzing industry information for the sake of comparing results.

d) Analyzing financial information using appropriate ratios and key areas

which may be affected due to risk of material misstatement.

This may contain either simple comparison policies or complex analysis that

advanced automated or statistical techniques.

Performing substantive procedure shall involve:

1) Considering suitability of substantive analytical procedure that is

determining suitability of such procedures for a particular item.

2) These procedures are usually used for those events or transactions

which are tend to be predictable that is which may regularly occur at

regular intervals. It can be used to estimate or compare ratios such as

gross profit ratio and other profit related ratios.

3) Reliability of data also plays an important role in performing analytical

procedure for example information obtained from external source shall

be more reliable than information obtained from internal source as it

may be modified or filtered by the management or internal

personnel’s.

4) Such procedures are also influenced by measuring comparability of

information available that is whether the information available is

comparable or not.

5) The information available for performing such procedures shall be

relevant. For example profit ratios for nonprofit organizations.

6) It involves developing expectation for recorded values and such

expectations should be accurate and precise so that many

misstatements can be easily accessed and identified.

Key ratios which can help in analyzing financial performance and financial position of last

5

cash equivalent was $A6, 43,000.

PERFORMING ANALYTICAL REVIEW PROCEDURE

As per ASA 520 analytical review procedure means evaluation of financial information

through analysis of relationship of both financial and non-financial data.

It includes comparing:

a) Information with prior period

b) Future results such as budgets and forecast

c) Analyzing industry information for the sake of comparing results.

d) Analyzing financial information using appropriate ratios and key areas

which may be affected due to risk of material misstatement.

This may contain either simple comparison policies or complex analysis that

advanced automated or statistical techniques.

Performing substantive procedure shall involve:

1) Considering suitability of substantive analytical procedure that is

determining suitability of such procedures for a particular item.

2) These procedures are usually used for those events or transactions

which are tend to be predictable that is which may regularly occur at

regular intervals. It can be used to estimate or compare ratios such as

gross profit ratio and other profit related ratios.

3) Reliability of data also plays an important role in performing analytical

procedure for example information obtained from external source shall

be more reliable than information obtained from internal source as it

may be modified or filtered by the management or internal

personnel’s.

4) Such procedures are also influenced by measuring comparability of

information available that is whether the information available is

comparable or not.

5) The information available for performing such procedures shall be

relevant. For example profit ratios for nonprofit organizations.

6) It involves developing expectation for recorded values and such

expectations should be accurate and precise so that many

misstatements can be easily accessed and identified.

Key ratios which can help in analyzing financial performance and financial position of last

5

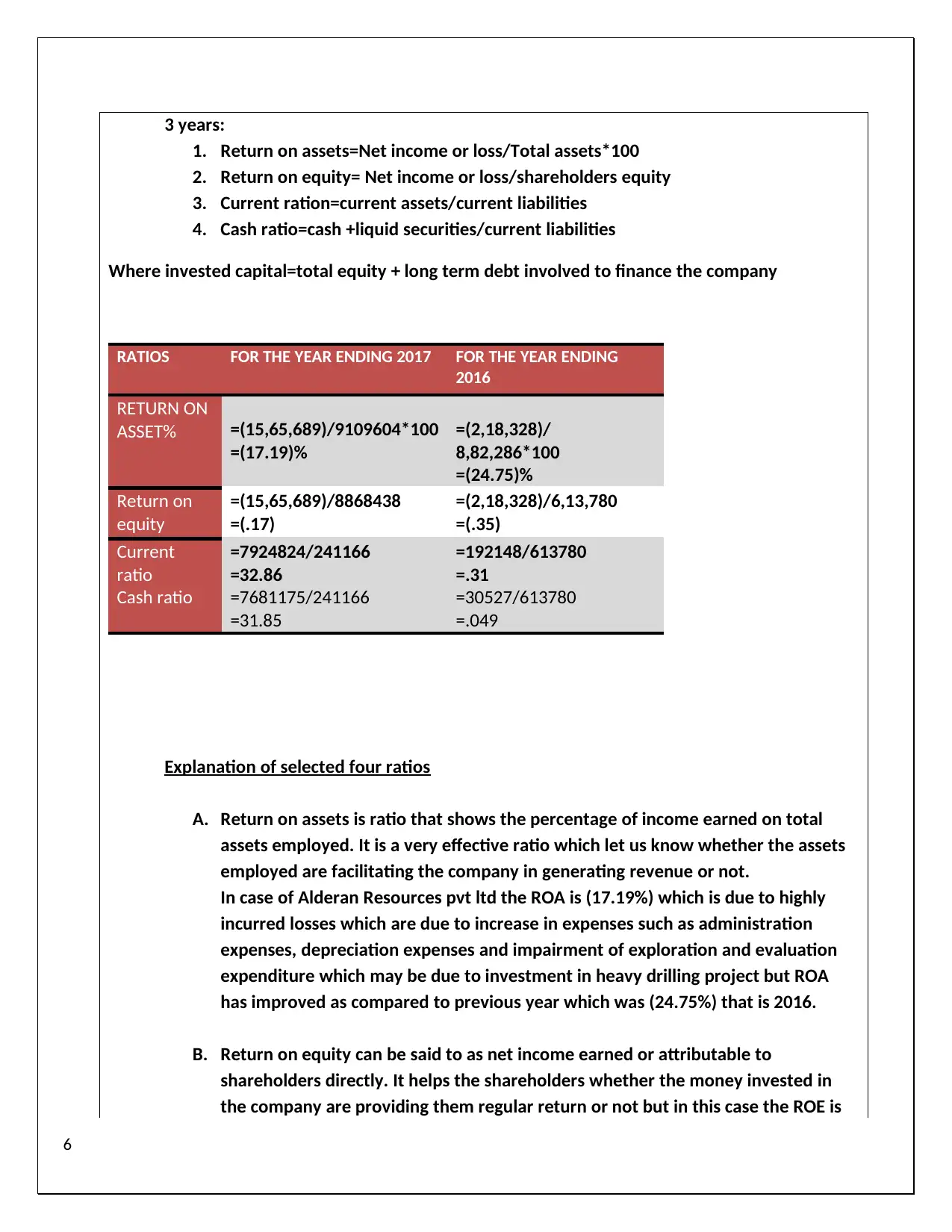

3 years:

1. Return on assets=Net income or loss/Total assets*100

2. Return on equity= Net income or loss/shareholders equity

3. Current ration=current assets/current liabilities

4. Cash ratio=cash +liquid securities/current liabilities

Where invested capital=total equity + long term debt involved to finance the company

RATIOS FOR THE YEAR ENDING 2017 FOR THE YEAR ENDING

2016

RETURN ON

ASSET% =(15,65,689)/9109604*100

=(17.19)%

=(2,18,328)/

8,82,286*100

=(24.75)%

Return on

equity

=(15,65,689)/8868438

=(.17)

=(2,18,328)/6,13,780

=(.35)

Current

ratio

Cash ratio

=7924824/241166

=32.86

=7681175/241166

=31.85

=192148/613780

=.31

=30527/613780

=.049

Explanation of selected four ratios

A. Return on assets is ratio that shows the percentage of income earned on total

assets employed. It is a very effective ratio which let us know whether the assets

employed are facilitating the company in generating revenue or not.

In case of Alderan Resources pvt ltd the ROA is (17.19%) which is due to highly

incurred losses which are due to increase in expenses such as administration

expenses, depreciation expenses and impairment of exploration and evaluation

expenditure which may be due to investment in heavy drilling project but ROA

has improved as compared to previous year which was (24.75%) that is 2016.

B. Return on equity can be said to as net income earned or attributable to

shareholders directly. It helps the shareholders whether the money invested in

the company are providing them regular return or not but in this case the ROE is

6

1. Return on assets=Net income or loss/Total assets*100

2. Return on equity= Net income or loss/shareholders equity

3. Current ration=current assets/current liabilities

4. Cash ratio=cash +liquid securities/current liabilities

Where invested capital=total equity + long term debt involved to finance the company

RATIOS FOR THE YEAR ENDING 2017 FOR THE YEAR ENDING

2016

RETURN ON

ASSET% =(15,65,689)/9109604*100

=(17.19)%

=(2,18,328)/

8,82,286*100

=(24.75)%

Return on

equity

=(15,65,689)/8868438

=(.17)

=(2,18,328)/6,13,780

=(.35)

Current

ratio

Cash ratio

=7924824/241166

=32.86

=7681175/241166

=31.85

=192148/613780

=.31

=30527/613780

=.049

Explanation of selected four ratios

A. Return on assets is ratio that shows the percentage of income earned on total

assets employed. It is a very effective ratio which let us know whether the assets

employed are facilitating the company in generating revenue or not.

In case of Alderan Resources pvt ltd the ROA is (17.19%) which is due to highly

incurred losses which are due to increase in expenses such as administration

expenses, depreciation expenses and impairment of exploration and evaluation

expenditure which may be due to investment in heavy drilling project but ROA

has improved as compared to previous year which was (24.75%) that is 2016.

B. Return on equity can be said to as net income earned or attributable to

shareholders directly. It helps the shareholders whether the money invested in

the company are providing them regular return or not but in this case the ROE is

6

(.17) which means that there are no profits and in turn means that zero dividend

payout ratio.

C. Current ratio is liquid ratio which shows that current asset will be sufficient to pay

off the current liabilities. Most appropriate current ratio is 2:1 but Alderan

resources ltd has 32.85 which is more than satisfying for a loss incurring company

and which is mostly due to humongous cash and cash equivalent.

D. Cash Ratio is the ratio that identifies whether the current cash and cash

equivalent is able to repay short term liabilities. As discussed above the cash

available is more than sufficient to repay short term debt and long term debt to

some extent.

If compared with previous year(2016) the cash and cash equivalent has increased

and short term liabilities have decreased concluding high cash ratio as compared

to previous year.

PERFORMING ANALYTICAL PROCEDURE FOR FINANCIAL STATEMENT AND

FINANCIAL PERFORMANCE

Following are the procedures to be performed:

INSPECTION: This step incorporates examining of records,

documents and also the tangible assets. Analytical procedure

consist of obtaining documentary evidence originating from third

party and also which are remained with third party which is usually

called the External evidence which is far more reliable than internal

evidence.

It also contains documentary evidence from the entity and also

contained with entity which is usually known as internal evidence.

Inspection also includes documentary evidence which originates

from third party and which can be founded with entity and vice

versa.

Observation: Next step in performing analytical procedures to

analyze the financial performance and financial statement is

observing the process and workings performed by others. Example

being overseeing the counting of stock done by management or the

stock department head.

Inquiry/Confirmation : It consist of enquiring or obtaining accurate

and appropriate information from a knowledgeable advisor who

may provide appropriate advice and on the basis of such response

further actions may be taken. For example applying ASA 505

external confirmation and asking for confirmation from debtors for

7

payout ratio.

C. Current ratio is liquid ratio which shows that current asset will be sufficient to pay

off the current liabilities. Most appropriate current ratio is 2:1 but Alderan

resources ltd has 32.85 which is more than satisfying for a loss incurring company

and which is mostly due to humongous cash and cash equivalent.

D. Cash Ratio is the ratio that identifies whether the current cash and cash

equivalent is able to repay short term liabilities. As discussed above the cash

available is more than sufficient to repay short term debt and long term debt to

some extent.

If compared with previous year(2016) the cash and cash equivalent has increased

and short term liabilities have decreased concluding high cash ratio as compared

to previous year.

PERFORMING ANALYTICAL PROCEDURE FOR FINANCIAL STATEMENT AND

FINANCIAL PERFORMANCE

Following are the procedures to be performed:

INSPECTION: This step incorporates examining of records,

documents and also the tangible assets. Analytical procedure

consist of obtaining documentary evidence originating from third

party and also which are remained with third party which is usually

called the External evidence which is far more reliable than internal

evidence.

It also contains documentary evidence from the entity and also

contained with entity which is usually known as internal evidence.

Inspection also includes documentary evidence which originates

from third party and which can be founded with entity and vice

versa.

Observation: Next step in performing analytical procedures to

analyze the financial performance and financial statement is

observing the process and workings performed by others. Example

being overseeing the counting of stock done by management or the

stock department head.

Inquiry/Confirmation : It consist of enquiring or obtaining accurate

and appropriate information from a knowledgeable advisor who

may provide appropriate advice and on the basis of such response

further actions may be taken. For example applying ASA 505

external confirmation and asking for confirmation from debtors for

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

balance statement or obtaining copies of balance in the books of

debtor/suppliers.

Calculation/workings: This step consists of verifying mathematical

or statistical accuracy of accounts and calculation solely done by

employees or professional in a company.

Reviewing analysis : This step of analytical procedure involves

reviewing the significant trends, ratios and comparing such trends

and ratios and performing further procedures for any unusual event

or transaction occurred during the review process.

Re-Performing the work done: Last step of this procedure is redo

the work which is performed by the management and the

company’s personnel’s so that the auditor shall get the idea of how

the work is performed in the company and if there is any fraud or

any misstatement is to be detected or need to be assessed or

communicated to the top management.

Concept of materiality of account balances as per ASA 320

Materiality: Material account balances are those which may affect the judgment of users of

financial statements. For e.g. for equity shareholders net profit attributable to equity

shareholders is of utmost importance as their dividend payment is dependent on such profits.

Usually percentage is used as benchmark for some material balances.

For e.g. any expense exceeding 2% of total revenue shall be disclosed separately rather than

shown as some additional information.

Determination of account balances which are material for planning purposes

As per ASA 320 Misstatement can be found in components of financial report or statement such

as assets , liabilities, equity , revenue or expenses.

Also it states that whether there are any items whether there are any items or account balances

which require attention of users of financial statement(such as sudden rise in profits and

consistent negative losses.

So if statement of financial statements is considered there are many expenses which can be

considered material for planning purpose which are administration expenses, employee benefit

8

debtor/suppliers.

Calculation/workings: This step consists of verifying mathematical

or statistical accuracy of accounts and calculation solely done by

employees or professional in a company.

Reviewing analysis : This step of analytical procedure involves

reviewing the significant trends, ratios and comparing such trends

and ratios and performing further procedures for any unusual event

or transaction occurred during the review process.

Re-Performing the work done: Last step of this procedure is redo

the work which is performed by the management and the

company’s personnel’s so that the auditor shall get the idea of how

the work is performed in the company and if there is any fraud or

any misstatement is to be detected or need to be assessed or

communicated to the top management.

Concept of materiality of account balances as per ASA 320

Materiality: Material account balances are those which may affect the judgment of users of

financial statements. For e.g. for equity shareholders net profit attributable to equity

shareholders is of utmost importance as their dividend payment is dependent on such profits.

Usually percentage is used as benchmark for some material balances.

For e.g. any expense exceeding 2% of total revenue shall be disclosed separately rather than

shown as some additional information.

Determination of account balances which are material for planning purposes

As per ASA 320 Misstatement can be found in components of financial report or statement such

as assets , liabilities, equity , revenue or expenses.

Also it states that whether there are any items whether there are any items or account balances

which require attention of users of financial statement(such as sudden rise in profits and

consistent negative losses.

So if statement of financial statements is considered there are many expenses which can be

considered material for planning purpose which are administration expenses, employee benefit

8

expense and also share based payments.

These components are considered material because there is quite a high increase in such

expenses if compared with previous year that is the year ending 30th June 2016.

Most important of them all is share based payment which is maximum of all and was not at all

opted by employees during the previous year. Here it is assessed that due to such consistent

losses the users of financial statement shall put their attention on such negative losses and

expenses which are giving rise to such consistent losses.

Capital structure also plays an important role in determining the materiality of account balances

in planning, in other words whether the company is financed by long term debt or shareholders

equity. If the company is financed by long term debt it may give rise to uncertainty of repayment

which may lead to company going into bankruptcy. But the Alderan Resources ltd is solely

financed with shareholders equity which includes mainly the shares issued through seed capital

raising that is $10,50,000 in which the money is raised from friends and family which may give

rise to related party transaction in future.

ASSETS ASSERTIONS EXPLAINATIO

9

These components are considered material because there is quite a high increase in such

expenses if compared with previous year that is the year ending 30th June 2016.

Most important of them all is share based payment which is maximum of all and was not at all

opted by employees during the previous year. Here it is assessed that due to such consistent

losses the users of financial statement shall put their attention on such negative losses and

expenses which are giving rise to such consistent losses.

Capital structure also plays an important role in determining the materiality of account balances

in planning, in other words whether the company is financed by long term debt or shareholders

equity. If the company is financed by long term debt it may give rise to uncertainty of repayment

which may lead to company going into bankruptcy. But the Alderan Resources ltd is solely

financed with shareholders equity which includes mainly the shares issued through seed capital

raising that is $10,50,000 in which the money is raised from friends and family which may give

rise to related party transaction in future.

ASSETS ASSERTIONS EXPLAINATIO

9

NS

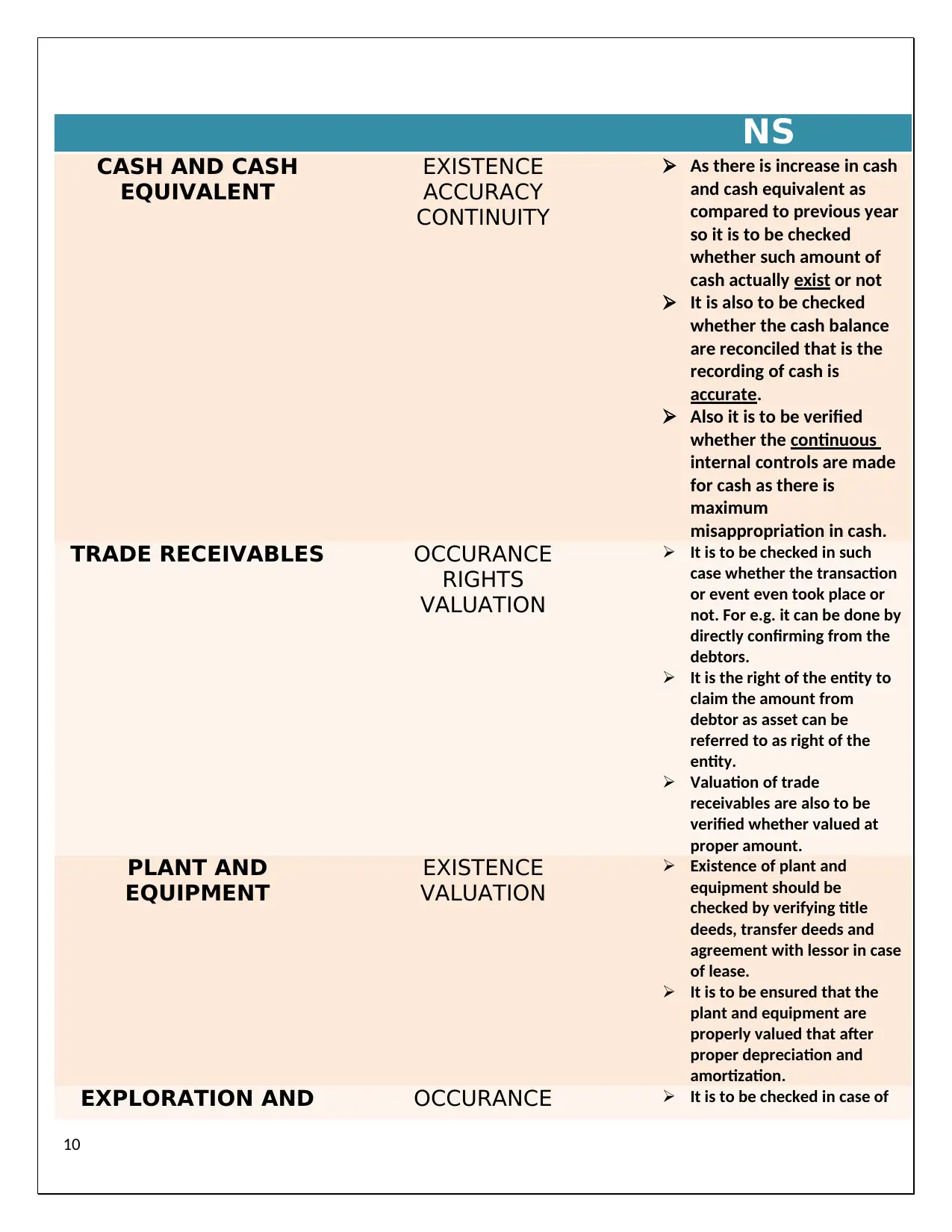

CASH AND CASH

EQUIVALENT

EXISTENCE

ACCURACY

CONTINUITY

As there is increase in cash

and cash equivalent as

compared to previous year

so it is to be checked

whether such amount of

cash actually exist or not

It is also to be checked

whether the cash balance

are reconciled that is the

recording of cash is

accurate.

Also it is to be verified

whether the continuous

internal controls are made

for cash as there is

maximum

misappropriation in cash.

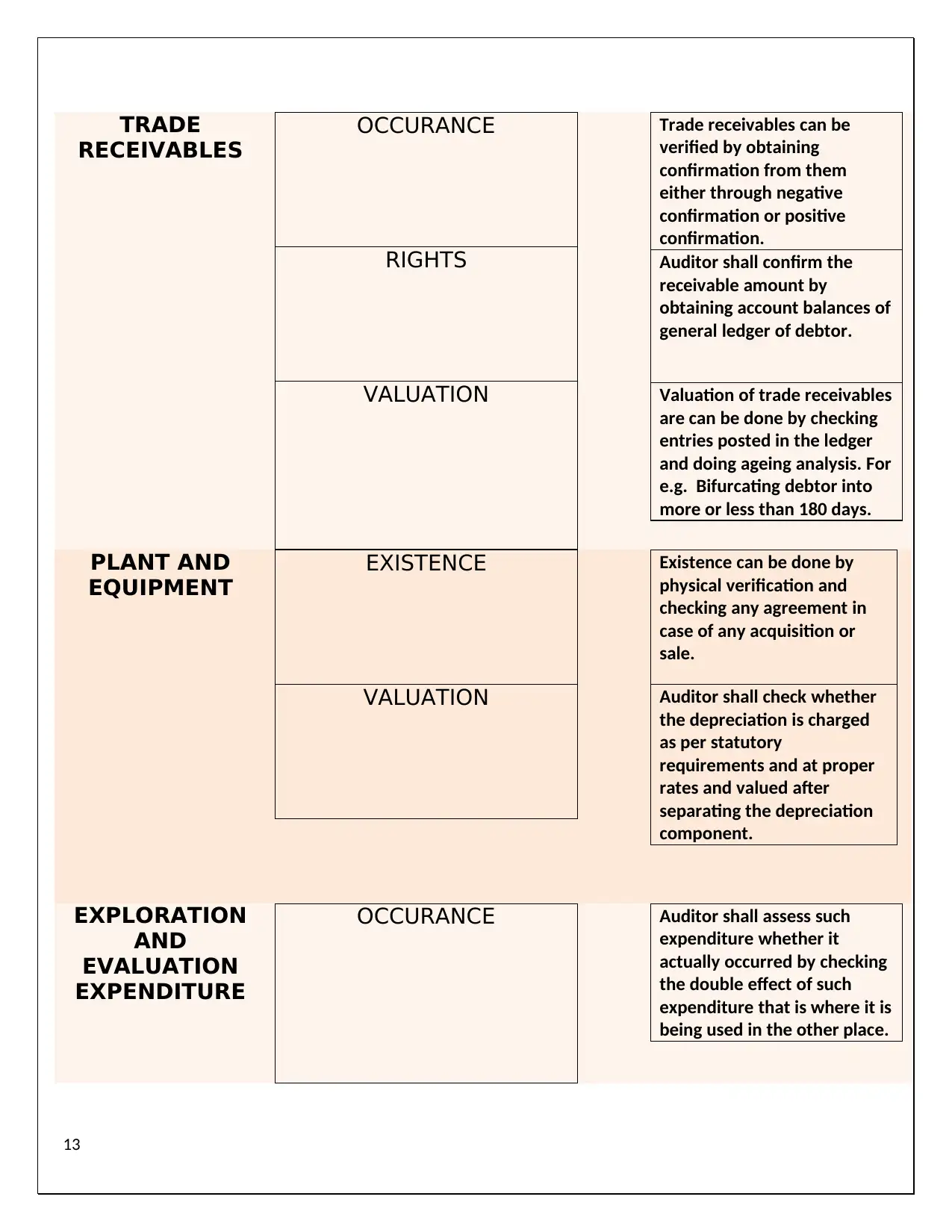

TRADE RECEIVABLES OCCURANCE

RIGHTS

VALUATION

It is to be checked in such

case whether the transaction

or event even took place or

not. For e.g. it can be done by

directly confirming from the

debtors.

It is the right of the entity to

claim the amount from

debtor as asset can be

referred to as right of the

entity.

Valuation of trade

receivables are also to be

verified whether valued at

proper amount.

PLANT AND

EQUIPMENT

EXISTENCE

VALUATION

Existence of plant and

equipment should be

checked by verifying title

deeds, transfer deeds and

agreement with lessor in case

of lease.

It is to be ensured that the

plant and equipment are

properly valued that after

proper depreciation and

amortization.

EXPLORATION AND OCCURANCE It is to be checked in case of

10

CASH AND CASH

EQUIVALENT

EXISTENCE

ACCURACY

CONTINUITY

As there is increase in cash

and cash equivalent as

compared to previous year

so it is to be checked

whether such amount of

cash actually exist or not

It is also to be checked

whether the cash balance

are reconciled that is the

recording of cash is

accurate.

Also it is to be verified

whether the continuous

internal controls are made

for cash as there is

maximum

misappropriation in cash.

TRADE RECEIVABLES OCCURANCE

RIGHTS

VALUATION

It is to be checked in such

case whether the transaction

or event even took place or

not. For e.g. it can be done by

directly confirming from the

debtors.

It is the right of the entity to

claim the amount from

debtor as asset can be

referred to as right of the

entity.

Valuation of trade

receivables are also to be

verified whether valued at

proper amount.

PLANT AND

EQUIPMENT

EXISTENCE

VALUATION

Existence of plant and

equipment should be

checked by verifying title

deeds, transfer deeds and

agreement with lessor in case

of lease.

It is to be ensured that the

plant and equipment are

properly valued that after

proper depreciation and

amortization.

EXPLORATION AND OCCURANCE It is to be checked in case of

10

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

EVALUATION

EXPENDITURE

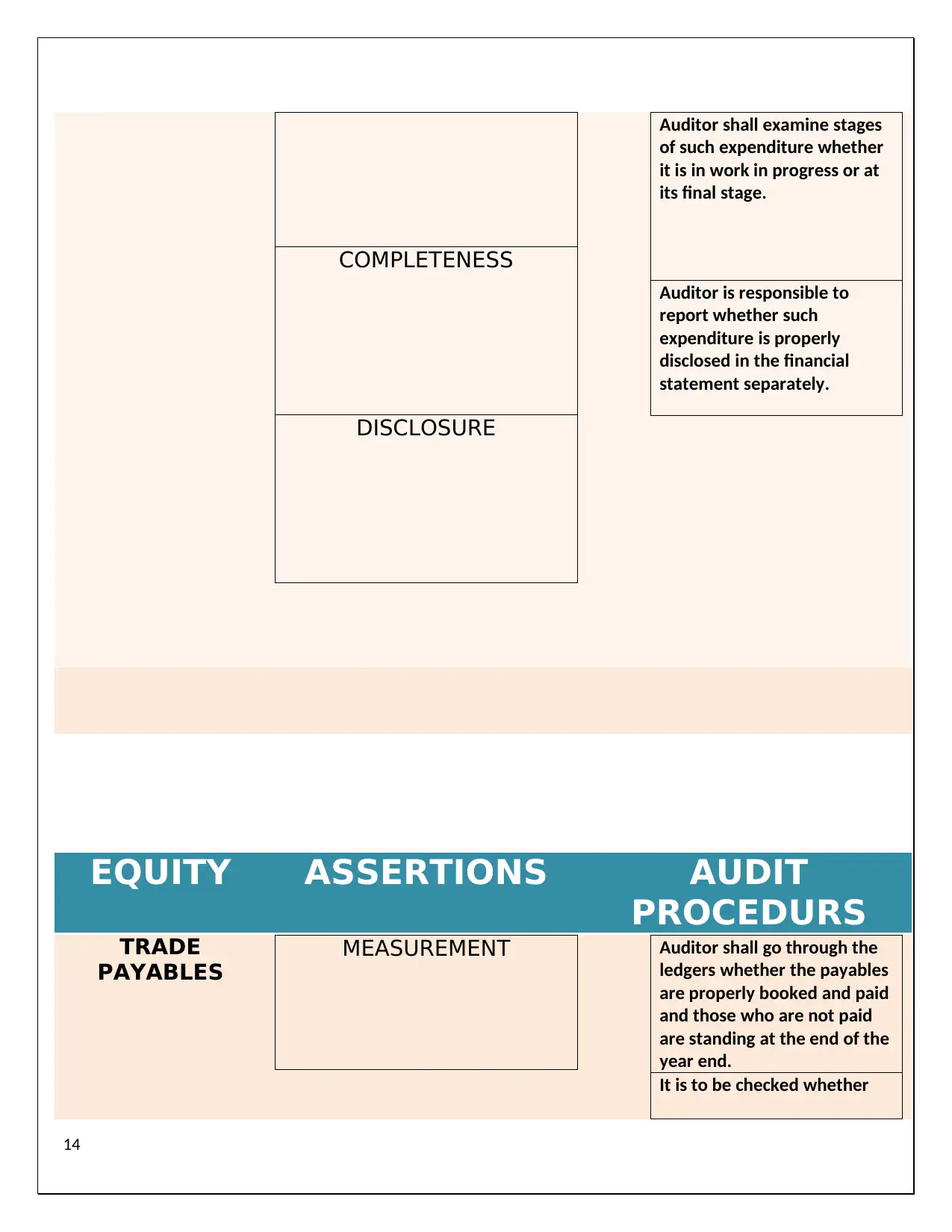

COMPLETENESS

DISCLOSURE

such expenditure whether

such expenditure took place

and for what purpose it took

place.

Also the completeness of the

expenditure is to be checked

whether all the expenditure

are complete or not.

It is also to be examined

whether the such

expenditure has been

properly presented and

disclosed as per proper

standards and requirements.

EQUITY ASSERTIONS EXPLAINATIO

NS

TRADE PAYABLES MEASUREMENT

OBLIGATION

In trade payables it is very

important that the payables

are recorded in proper period

and at proper amount.

It is to be ensured that the

payables are liability of an

entity that is they are an

obligation to be paid at an

given date.

LOAN PAYABLES EXISTENCE

VALUATION

OBLIGATION

It is to be examined whether

such long term loans exist

during the year or not.

Valuation of such loan

payable should be at proper

amount as it may influence

the decision of users of

financial statement.

It is to be made sure that

company has acknowledged

their obligation to be paid to

11

EXPENDITURE

COMPLETENESS

DISCLOSURE

such expenditure whether

such expenditure took place

and for what purpose it took

place.

Also the completeness of the

expenditure is to be checked

whether all the expenditure

are complete or not.

It is also to be examined

whether the such

expenditure has been

properly presented and

disclosed as per proper

standards and requirements.

EQUITY ASSERTIONS EXPLAINATIO

NS

TRADE PAYABLES MEASUREMENT

OBLIGATION

In trade payables it is very

important that the payables

are recorded in proper period

and at proper amount.

It is to be ensured that the

payables are liability of an

entity that is they are an

obligation to be paid at an

given date.

LOAN PAYABLES EXISTENCE

VALUATION

OBLIGATION

It is to be examined whether

such long term loans exist

during the year or not.

Valuation of such loan

payable should be at proper

amount as it may influence

the decision of users of

financial statement.

It is to be made sure that

company has acknowledged

their obligation to be paid to

11

other party from which the

loans has been raised.

AUDIT WORKSTEPS ADDRESSING SELECTED ASSERTIONS FOR

MATERIAL ACCOUNT BALANCES

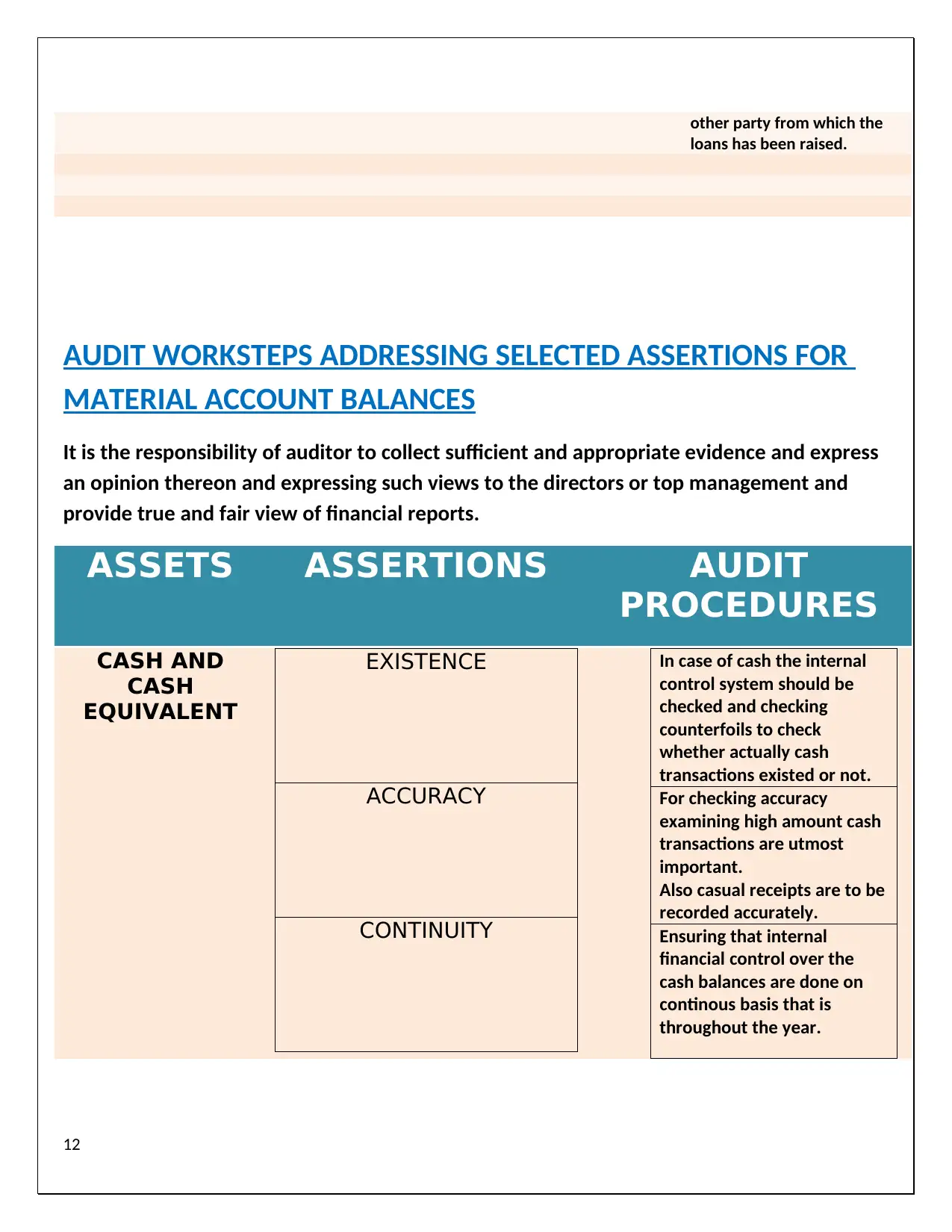

It is the responsibility of auditor to collect sufficient and appropriate evidence and express

an opinion thereon and expressing such views to the directors or top management and

provide true and fair view of financial reports.

ASSETS ASSERTIONS AUDIT

PROCEDURES

CASH AND

CASH

EQUIVALENT

EXISTENCE

ACCURACY

CONTINUITY

In case of cash the internal

control system should be

checked and checking

counterfoils to check

whether actually cash

transactions existed or not.

For checking accuracy

examining high amount cash

transactions are utmost

important.

Also casual receipts are to be

recorded accurately.

Ensuring that internal

financial control over the

cash balances are done on

continous basis that is

throughout the year.

12

loans has been raised.

AUDIT WORKSTEPS ADDRESSING SELECTED ASSERTIONS FOR

MATERIAL ACCOUNT BALANCES

It is the responsibility of auditor to collect sufficient and appropriate evidence and express

an opinion thereon and expressing such views to the directors or top management and

provide true and fair view of financial reports.

ASSETS ASSERTIONS AUDIT

PROCEDURES

CASH AND

CASH

EQUIVALENT

EXISTENCE

ACCURACY

CONTINUITY

In case of cash the internal

control system should be

checked and checking

counterfoils to check

whether actually cash

transactions existed or not.

For checking accuracy

examining high amount cash

transactions are utmost

important.

Also casual receipts are to be

recorded accurately.

Ensuring that internal

financial control over the

cash balances are done on

continous basis that is

throughout the year.

12

TRADE

RECEIVABLES

OCCURANCE

RIGHTS

VALUATION

Trade receivables can be

verified by obtaining

confirmation from them

either through negative

confirmation or positive

confirmation.

Auditor shall confirm the

receivable amount by

obtaining account balances of

general ledger of debtor.

Valuation of trade receivables

are can be done by checking

entries posted in the ledger

and doing ageing analysis. For

e.g. Bifurcating debtor into

more or less than 180 days.

PLANT AND

EQUIPMENT

EXISTENCE

VALUATION

Existence can be done by

physical verification and

checking any agreement in

case of any acquisition or

sale.

Auditor shall check whether

the depreciation is charged

as per statutory

requirements and at proper

rates and valued after

separating the depreciation

component.

EXPLORATION

AND

EVALUATION

EXPENDITURE

OCCURANCE Auditor shall assess such

expenditure whether it

actually occurred by checking

the double effect of such

expenditure that is where it is

being used in the other place.

13

RECEIVABLES

OCCURANCE

RIGHTS

VALUATION

Trade receivables can be

verified by obtaining

confirmation from them

either through negative

confirmation or positive

confirmation.

Auditor shall confirm the

receivable amount by

obtaining account balances of

general ledger of debtor.

Valuation of trade receivables

are can be done by checking

entries posted in the ledger

and doing ageing analysis. For

e.g. Bifurcating debtor into

more or less than 180 days.

PLANT AND

EQUIPMENT

EXISTENCE

VALUATION

Existence can be done by

physical verification and

checking any agreement in

case of any acquisition or

sale.

Auditor shall check whether

the depreciation is charged

as per statutory

requirements and at proper

rates and valued after

separating the depreciation

component.

EXPLORATION

AND

EVALUATION

EXPENDITURE

OCCURANCE Auditor shall assess such

expenditure whether it

actually occurred by checking

the double effect of such

expenditure that is where it is

being used in the other place.

13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COMPLETENESS

DISCLOSURE

Auditor shall examine stages

of such expenditure whether

it is in work in progress or at

its final stage.

Auditor is responsible to

report whether such

expenditure is properly

disclosed in the financial

statement separately.

EQUITY ASSERTIONS AUDIT

PROCEDURS

TRADE

PAYABLES

MEASUREMENT Auditor shall go through the

ledgers whether the payables

are properly booked and paid

and those who are not paid

are standing at the end of the

year end.

It is to be checked whether

14

DISCLOSURE

Auditor shall examine stages

of such expenditure whether

it is in work in progress or at

its final stage.

Auditor is responsible to

report whether such

expenditure is properly

disclosed in the financial

statement separately.

EQUITY ASSERTIONS AUDIT

PROCEDURS

TRADE

PAYABLES

MEASUREMENT Auditor shall go through the

ledgers whether the payables

are properly booked and paid

and those who are not paid

are standing at the end of the

year end.

It is to be checked whether

14

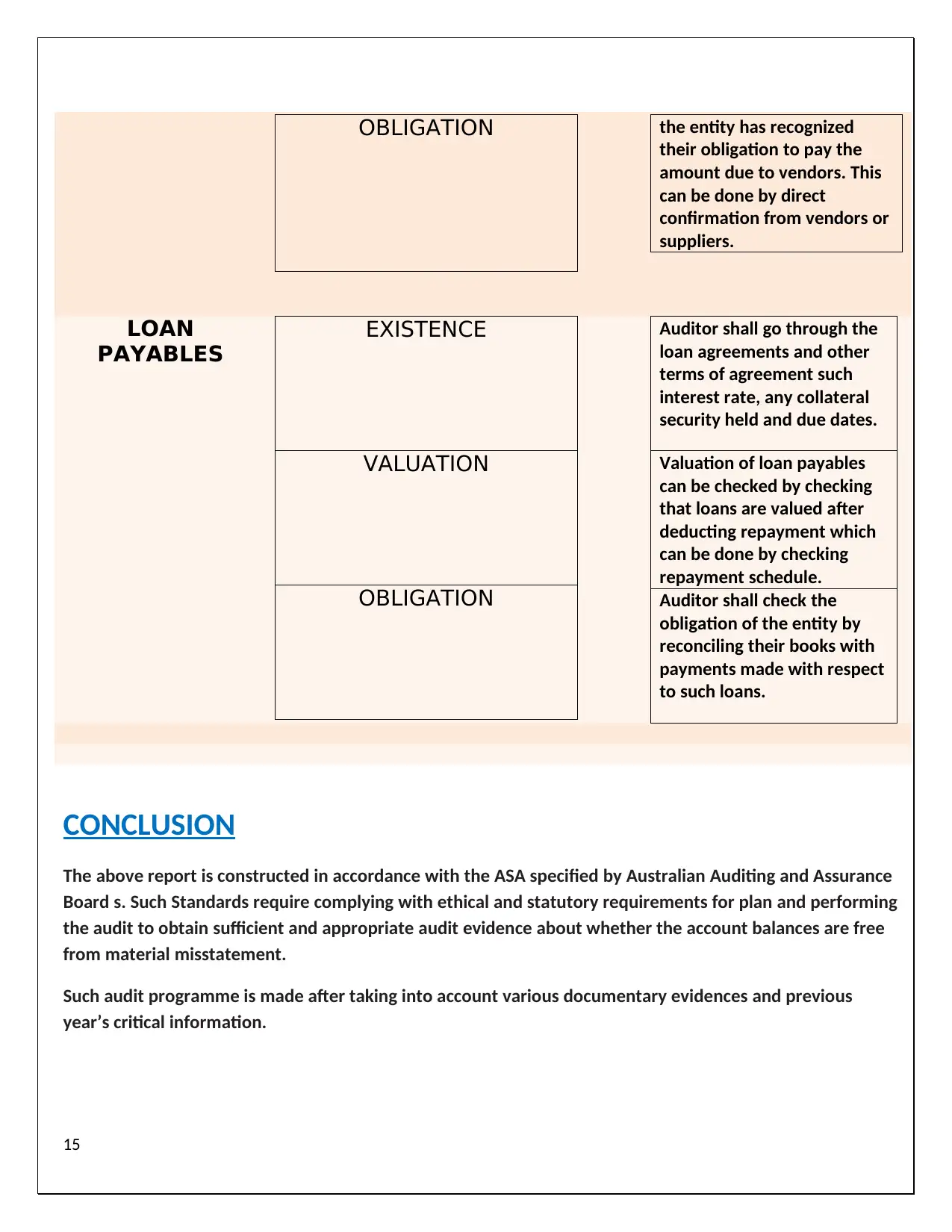

OBLIGATION the entity has recognized

their obligation to pay the

amount due to vendors. This

can be done by direct

confirmation from vendors or

suppliers.

LOAN

PAYABLES

EXISTENCE

VALUATION

OBLIGATION

Auditor shall go through the

loan agreements and other

terms of agreement such

interest rate, any collateral

security held and due dates.

Valuation of loan payables

can be checked by checking

that loans are valued after

deducting repayment which

can be done by checking

repayment schedule.

Auditor shall check the

obligation of the entity by

reconciling their books with

payments made with respect

to such loans.

CONCLUSION

The above report is constructed in accordance with the ASA specified by Australian Auditing and Assurance

Board s. Such Standards require complying with ethical and statutory requirements for plan and performing

the audit to obtain sufficient and appropriate audit evidence about whether the account balances are free

from material misstatement.

Such audit programme is made after taking into account various documentary evidences and previous

year’s critical information.

15

their obligation to pay the

amount due to vendors. This

can be done by direct

confirmation from vendors or

suppliers.

LOAN

PAYABLES

EXISTENCE

VALUATION

OBLIGATION

Auditor shall go through the

loan agreements and other

terms of agreement such

interest rate, any collateral

security held and due dates.

Valuation of loan payables

can be checked by checking

that loans are valued after

deducting repayment which

can be done by checking

repayment schedule.

Auditor shall check the

obligation of the entity by

reconciling their books with

payments made with respect

to such loans.

CONCLUSION

The above report is constructed in accordance with the ASA specified by Australian Auditing and Assurance

Board s. Such Standards require complying with ethical and statutory requirements for plan and performing

the audit to obtain sufficient and appropriate audit evidence about whether the account balances are free

from material misstatement.

Such audit programme is made after taking into account various documentary evidences and previous

year’s critical information.

15

REFERENCES

Bibliography

A.Benge, V., n.d. Assertions proven by accounts receivable. [Online]

Available at: http://smallbusiness.chron.com/assertions-proven-accounts-receivable-confirmations-35833.html

[Accessed 23 may 2018].

ACCA, n.d. Audit procedures. SA TECHINICAL, pp. 1-5.

Anon., 2017. Ratio valuation of Alderan Resources. [Online]

Available at: https://www.infrontanalytics.com/fe-EN/40737AA/ALDERAN-RESOURCES/financial-ratios

[Accessed 22 may 2018].

Anon., 2018. bloomberg-key statistics. [Online]

Available at: https://www.bloomberg.com/quote/AL8:AU

[Accessed 23 may 2018].

Anon., n.d. Audit readiness-Propert,plant and equipment. [Online]

Available at: https://www2.deloitte.com/ng/en/pages/audit/articles/financial-reporting/audit-readiness-4-property-

plant-and-equipment.html

[Accessed 21 may 2018].

BASU, S., 2017. fundamentals of auditing. s.l.:Pearson.

board, A. a. a., 2009. ASA 505. AUDITING STANDARD ASA 505 EXTERNAL CONFIRMATION, pp. 1-20.

board, A. a. a. s., 2009. ASA 320. Auditing standard ASA 320, pp. 1-7.

board, A. a. a. s., 2009. ASA 520. AUDITING STANDARD ASA 520 ANALYTICAL PROCEDURES, pp. 1-16.

board, A. a. A. s., 2009. Auditors response to assessed risk. ASA 330, pp. 1-34.

BOARD, A. R., 2018. March 2018 Quarterly activities report. ALDERAN RESOURCES, p. 7.

hall, c., 2017. Fraud test for auditors. [Online]

Available at: https://cpa-scribo.com/receipt-fraud-tests-auditors/

[Accessed 22 may 2018].

Hall, C., n.d. Auditing accounts payable and expenses. [Online]

Available at: https://cpa-scribo.com/auditing-payables-expenses/

[Accessed 22nd may 2018].

16

Bibliography

A.Benge, V., n.d. Assertions proven by accounts receivable. [Online]

Available at: http://smallbusiness.chron.com/assertions-proven-accounts-receivable-confirmations-35833.html

[Accessed 23 may 2018].

ACCA, n.d. Audit procedures. SA TECHINICAL, pp. 1-5.

Anon., 2017. Ratio valuation of Alderan Resources. [Online]

Available at: https://www.infrontanalytics.com/fe-EN/40737AA/ALDERAN-RESOURCES/financial-ratios

[Accessed 22 may 2018].

Anon., 2018. bloomberg-key statistics. [Online]

Available at: https://www.bloomberg.com/quote/AL8:AU

[Accessed 23 may 2018].

Anon., n.d. Audit readiness-Propert,plant and equipment. [Online]

Available at: https://www2.deloitte.com/ng/en/pages/audit/articles/financial-reporting/audit-readiness-4-property-

plant-and-equipment.html

[Accessed 21 may 2018].

BASU, S., 2017. fundamentals of auditing. s.l.:Pearson.

board, A. a. a., 2009. ASA 505. AUDITING STANDARD ASA 505 EXTERNAL CONFIRMATION, pp. 1-20.

board, A. a. a. s., 2009. ASA 320. Auditing standard ASA 320, pp. 1-7.

board, A. a. a. s., 2009. ASA 520. AUDITING STANDARD ASA 520 ANALYTICAL PROCEDURES, pp. 1-16.

board, A. a. A. s., 2009. Auditors response to assessed risk. ASA 330, pp. 1-34.

BOARD, A. R., 2018. March 2018 Quarterly activities report. ALDERAN RESOURCES, p. 7.

hall, c., 2017. Fraud test for auditors. [Online]

Available at: https://cpa-scribo.com/receipt-fraud-tests-auditors/

[Accessed 22 may 2018].

Hall, C., n.d. Auditing accounts payable and expenses. [Online]

Available at: https://cpa-scribo.com/auditing-payables-expenses/

[Accessed 22nd may 2018].

16

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

ICAEW, n.d. Materiality in the audit of financial statement. International Accounting , Auditing and ethics audit and

assurance faculty, pp. 7-34.

India, I. o. C. A. o., 2016. Auditing and Assurance. s.l.:ICAI.

institute, c. f., n.d. Audit asserions. [Online]

Available at: https://corporatefinanceinstitute.com/resources/knowledge/accounting/audit-assertions/

[Accessed 21 may 2018].

LTD, A. R., 2017. ANNUAL CONSOLIDATED FINANCIAL REPORT, West Perth,AUSTRALIA: s.n.

Maverick, J., 2016. Financial statement assertions. [Online]

Available at: https://www.investopedia.com/articles/financial-analysis/063016/what-are-financial-statement-

assertions.asp

[Accessed 22 may 2018].

PERRY, L., 2014. Auditing special purpose framework. [Online]

Available at: https://www.accountingweb.com/aa/auditing/auditing-special-purpose-frameworks-auditing-cash-

classifications-part-1

[Accessed 22nd may 2018].

stewardship, T., 2016. AUDIT PROGRAM OBJECTIVE AND METHODOLOGY. p. 1.

17

assurance faculty, pp. 7-34.

India, I. o. C. A. o., 2016. Auditing and Assurance. s.l.:ICAI.

institute, c. f., n.d. Audit asserions. [Online]

Available at: https://corporatefinanceinstitute.com/resources/knowledge/accounting/audit-assertions/

[Accessed 21 may 2018].

LTD, A. R., 2017. ANNUAL CONSOLIDATED FINANCIAL REPORT, West Perth,AUSTRALIA: s.n.

Maverick, J., 2016. Financial statement assertions. [Online]

Available at: https://www.investopedia.com/articles/financial-analysis/063016/what-are-financial-statement-

assertions.asp

[Accessed 22 may 2018].

PERRY, L., 2014. Auditing special purpose framework. [Online]

Available at: https://www.accountingweb.com/aa/auditing/auditing-special-purpose-frameworks-auditing-cash-

classifications-part-1

[Accessed 22nd may 2018].

stewardship, T., 2016. AUDIT PROGRAM OBJECTIVE AND METHODOLOGY. p. 1.

17

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.