Assessment 2: Financial Management Analysis of Zeta Resources Ltd.

VerifiedAdded on 2020/05/08

|12

|2249

|43

Report

AI Summary

This report provides a comprehensive financial analysis of Zeta Resources Ltd., an exempted closed-end investment company. The analysis covers debt valuation, including short-term and long-term debts, and the consistency of the company's debt structure compared to industry standards. It also includes an examination of share valuation, cost of equity (although data limitations prevented calculation), and discussions on the company's revenue, earnings, EPS, dividends, and growth expectations. The report further explores the cost of capital, specifically the weighted average cost of capital (WACC), and the impact of tax rates. It also investigates the company's capital structure and market analysis, commenting on the financial performance of Zeta Resource Ltd. and key factors influencing its operations. The report references various financial management resources to support its findings.

ASSESSMENT 2 – PART B

(FINANCIAL MANAGEMENT ANALYSIS)

1 | P a g e

(FINANCIAL MANAGEMENT ANALYSIS)

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive summary

This report provides a study on the financial statements parts of a company who is an exempted

closed-end investment company. Zeta resources Ltd. is engaged in investing the pooled funds of

the shareholders in compliance with the objective and policy of its investments. Zeta resources

Ltd. is having an aim and objective of producing and generating a return for the shareholders

with a risk level which is acceptable and attainable. The report is also to analyze the financial

performance of the company in the environment and to evaluate and analyze the conclusions

thereafter.

2 | P a g e

This report provides a study on the financial statements parts of a company who is an exempted

closed-end investment company. Zeta resources Ltd. is engaged in investing the pooled funds of

the shareholders in compliance with the objective and policy of its investments. Zeta resources

Ltd. is having an aim and objective of producing and generating a return for the shareholders

with a risk level which is acceptable and attainable. The report is also to analyze the financial

performance of the company in the environment and to evaluate and analyze the conclusions

thereafter.

2 | P a g e

Table of Contents

Executive summary.....................................................................................................................................2

(I) Debt Valuation.................................................................................................................................4

(II) Share valuation................................................................................................................................5

(III) Cost of Capital.................................................................................................................................8

(IV) Market Analysis.............................................................................................................................10

References.................................................................................................................................................11

3 | P a g e

Executive summary.....................................................................................................................................2

(I) Debt Valuation.................................................................................................................................4

(II) Share valuation................................................................................................................................5

(III) Cost of Capital.................................................................................................................................8

(IV) Market Analysis.............................................................................................................................10

References.................................................................................................................................................11

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(I) Debt Valuation

1. Short-term and long-term debts used by the firm

As such the company is not having any short-term debt in its financial statements. However, the

company is having long-term debts in the form of LT Debt excl. Capitalized Leases.

2. Consistency of Company’s debt structure

On considering the Balance Sheet of Zeta Resource Ltd, it can be identified that till June 2017

the debt amount of the company has fluctuated heavily from the year 2015 to 2017. At the same

time, it can also be significantly identified that the total debt of the company comprises of the

long-term debts and there are no short-term debts present in the company (Bodie, 2013). And if

the particular situation of the company is compared with the industry standards then it can easily

be stated that debt structure of Zeta Resource Ltd is different than the industry standards.

3. Operation of industry Zeta Resources Ltd. in affecting the part of short-term to

long-term debts of Zeta Resources Ltd.

It has been significantly identified that there is a lot of difference between the debt structure of

the Zeta Resources Ltd. and the industry. On the other hand, the financial reports of the

organization for the past 3 years are clearly stating that the company has been influenced by the

industry in the context of debt structure. In case of Zeta resource, the proportion of long-term

debts is more in the capital structure.

4. Company’s cost of debt

Neither any terms for the repayment of interest nor the interest is charged in the financials of the

Zeta Resources Ltd. For the fiscal year ended on 30 June 2017 the loan given to the Zeta energy

was impaired through gains & losses, to the company’s fair value as determined by the directors

of the company (Higgins, 2012). The boards of directors have valued the investments (listed)

held by the Zeta Resources at the market value they are listed on, at the time of determining the

fair value of Zeta Resources Ltd. The amount of loan given to Zeta Energy is showcased in AUD

to the value of $20.669 million (2016: A$20.427million). However, the interest on a loan

provided to Kumarina is showcased in AUD and is free from the interest. No terms for the fixed

repayment are provided except that no repayment is due before June of 30, 2018.

4 | P a g e

1. Short-term and long-term debts used by the firm

As such the company is not having any short-term debt in its financial statements. However, the

company is having long-term debts in the form of LT Debt excl. Capitalized Leases.

2. Consistency of Company’s debt structure

On considering the Balance Sheet of Zeta Resource Ltd, it can be identified that till June 2017

the debt amount of the company has fluctuated heavily from the year 2015 to 2017. At the same

time, it can also be significantly identified that the total debt of the company comprises of the

long-term debts and there are no short-term debts present in the company (Bodie, 2013). And if

the particular situation of the company is compared with the industry standards then it can easily

be stated that debt structure of Zeta Resource Ltd is different than the industry standards.

3. Operation of industry Zeta Resources Ltd. in affecting the part of short-term to

long-term debts of Zeta Resources Ltd.

It has been significantly identified that there is a lot of difference between the debt structure of

the Zeta Resources Ltd. and the industry. On the other hand, the financial reports of the

organization for the past 3 years are clearly stating that the company has been influenced by the

industry in the context of debt structure. In case of Zeta resource, the proportion of long-term

debts is more in the capital structure.

4. Company’s cost of debt

Neither any terms for the repayment of interest nor the interest is charged in the financials of the

Zeta Resources Ltd. For the fiscal year ended on 30 June 2017 the loan given to the Zeta energy

was impaired through gains & losses, to the company’s fair value as determined by the directors

of the company (Higgins, 2012). The boards of directors have valued the investments (listed)

held by the Zeta Resources at the market value they are listed on, at the time of determining the

fair value of Zeta Resources Ltd. The amount of loan given to Zeta Energy is showcased in AUD

to the value of $20.669 million (2016: A$20.427million). However, the interest on a loan

provided to Kumarina is showcased in AUD and is free from the interest. No terms for the fixed

repayment are provided except that no repayment is due before June of 30, 2018.

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(II) Share valuation

1. Company’s cost of equity

Cost of equity refers to the cash flow risk to the company’s shareholders. The calculation of the

cost of equity is duly performed by adding a risk premium to the rate which is free in the long

run.

Where:

- Long-term risk-free rate

- Beta, represents the relative risk of the stock relative to the market

- Market risk premium, or

Cost of equity = (Dividend per share of the next year / Current market value of stock) + Growth

rate of dividends

Note: No dividend is provided by the period ended 30, June 2017. So it is impossible to

calculate the company’s cost of equity.

2. Discussion on Company’s revenue, earnings, EPS, dividends and growth

expectations

On considering the present and recent reports for the year 2017 of the Zeta Resource Ltd, it can

be clearly identified that revenue of the same is 11,308.9 AUD Thousand, which has increased

from the revenues of the last year (Purves, et. al., 2015). On the other hand EPS of the company

is also showing upward trend for the last 3 years. EPS of the company is 0.08 in the current year

which was (0.07) in the last year. On the other hand, it was identified that Dividend percent of

the company is has been decreased in the lasts and recent financial year which is 2017 (Brigham

and Houston, 2012).

5 | P a g e

1. Company’s cost of equity

Cost of equity refers to the cash flow risk to the company’s shareholders. The calculation of the

cost of equity is duly performed by adding a risk premium to the rate which is free in the long

run.

Where:

- Long-term risk-free rate

- Beta, represents the relative risk of the stock relative to the market

- Market risk premium, or

Cost of equity = (Dividend per share of the next year / Current market value of stock) + Growth

rate of dividends

Note: No dividend is provided by the period ended 30, June 2017. So it is impossible to

calculate the company’s cost of equity.

2. Discussion on Company’s revenue, earnings, EPS, dividends and growth

expectations

On considering the present and recent reports for the year 2017 of the Zeta Resource Ltd, it can

be clearly identified that revenue of the same is 11,308.9 AUD Thousand, which has increased

from the revenues of the last year (Purves, et. al., 2015). On the other hand EPS of the company

is also showing upward trend for the last 3 years. EPS of the company is 0.08 in the current year

which was (0.07) in the last year. On the other hand, it was identified that Dividend percent of

the company is has been decreased in the lasts and recent financial year which is 2017 (Brigham

and Houston, 2012).

5 | P a g e

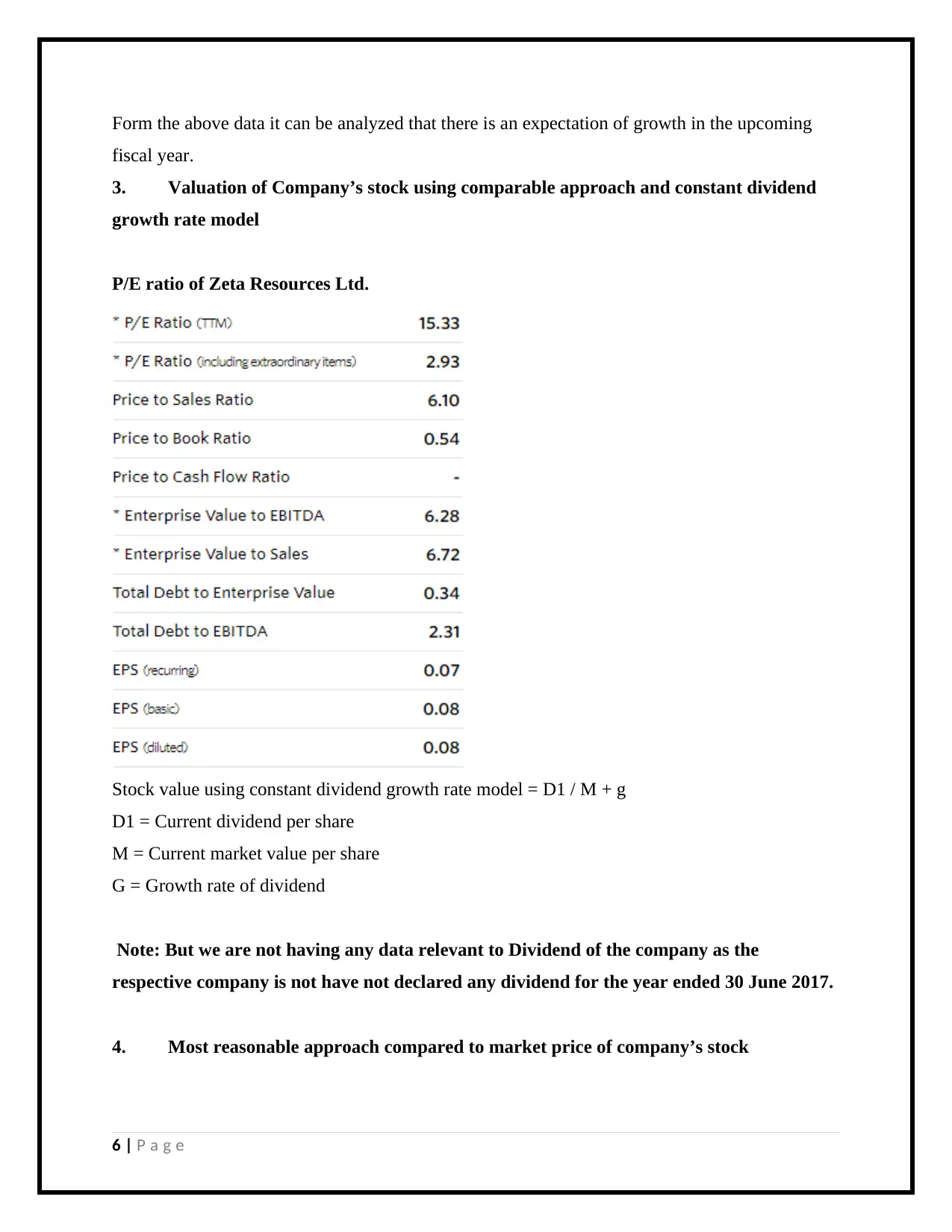

Form the above data it can be analyzed that there is an expectation of growth in the upcoming

fiscal year.

3. Valuation of Company’s stock using comparable approach and constant dividend

growth rate model

P/E ratio of Zeta Resources Ltd.

Stock value using constant dividend growth rate model = D1 / M + g

D1 = Current dividend per share

M = Current market value per share

G = Growth rate of dividend

Note: But we are not having any data relevant to Dividend of the company as the

respective company is not have not declared any dividend for the year ended 30 June 2017.

4. Most reasonable approach compared to market price of company’s stock

6 | P a g e

fiscal year.

3. Valuation of Company’s stock using comparable approach and constant dividend

growth rate model

P/E ratio of Zeta Resources Ltd.

Stock value using constant dividend growth rate model = D1 / M + g

D1 = Current dividend per share

M = Current market value per share

G = Growth rate of dividend

Note: But we are not having any data relevant to Dividend of the company as the

respective company is not have not declared any dividend for the year ended 30 June 2017.

4. Most reasonable approach compared to market price of company’s stock

6 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Value of stock can be identified by formulating the dividend growth rate model and it will

generally showcase the most reasonable value of the company’s stock when compared to the

market price per share (Thella, et. al., 2011). This is simply because of the reason that the value

of the stock in this model has been determined by considering the dividend growth percent of the

company.

5. Additional data and information preferring for valuing the stock of the company

The beta value of the company's stock and Earnings growth of the company could be used for

valuing the company’s stock. It is because of the simple reason the earnings growth of the share

of the company could assist to understand the share performance in the last few years.

7 | P a g e

generally showcase the most reasonable value of the company’s stock when compared to the

market price per share (Thella, et. al., 2011). This is simply because of the reason that the value

of the stock in this model has been determined by considering the dividend growth percent of the

company.

5. Additional data and information preferring for valuing the stock of the company

The beta value of the company's stock and Earnings growth of the company could be used for

valuing the company’s stock. It is because of the simple reason the earnings growth of the share

of the company could assist to understand the share performance in the last few years.

7 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(III) Cost of Capital

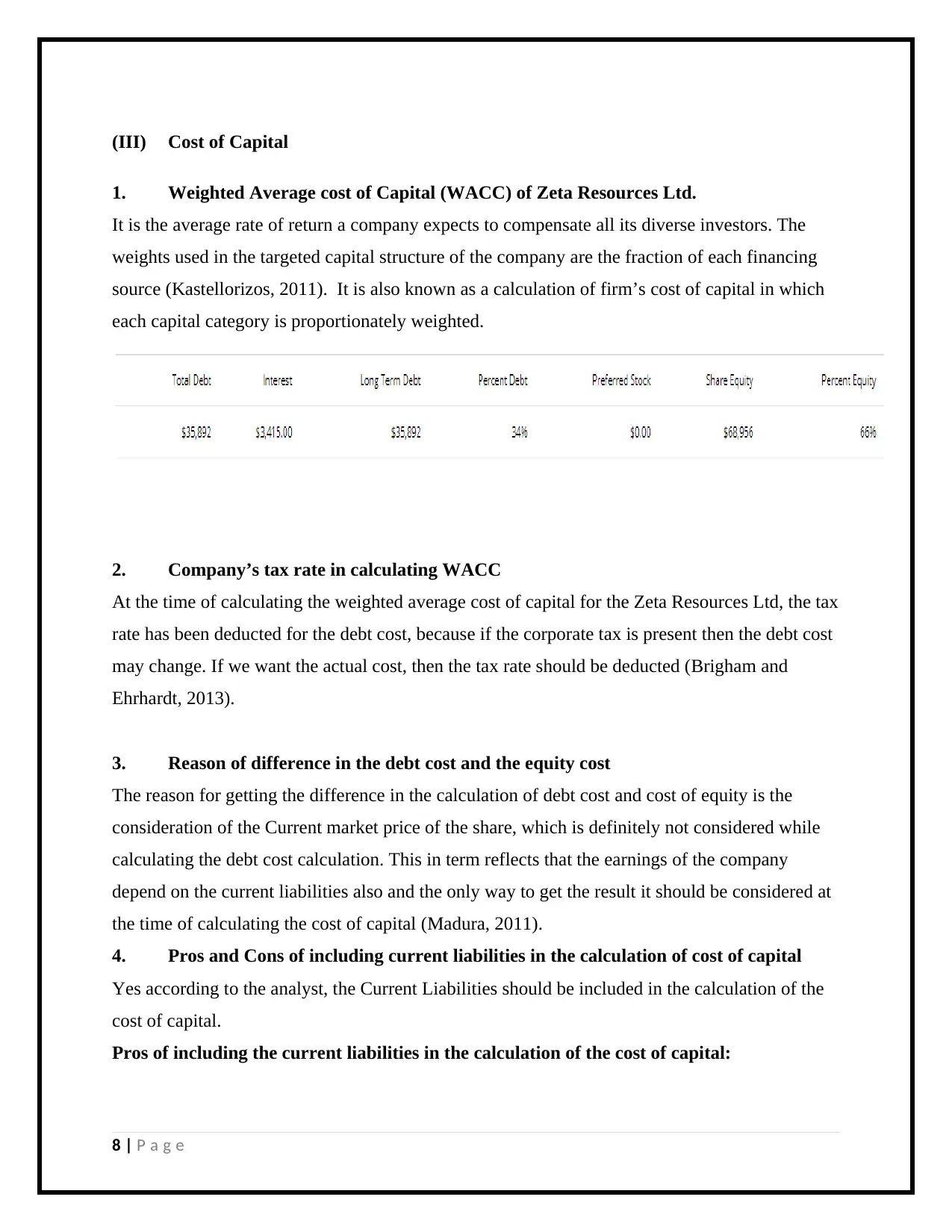

1. Weighted Average cost of Capital (WACC) of Zeta Resources Ltd.

It is the average rate of return a company expects to compensate all its diverse investors. The

weights used in the targeted capital structure of the company are the fraction of each financing

source (Kastellorizos, 2011). It is also known as a calculation of firm’s cost of capital in which

each capital category is proportionately weighted.

2. Company’s tax rate in calculating WACC

At the time of calculating the weighted average cost of capital for the Zeta Resources Ltd, the tax

rate has been deducted for the debt cost, because if the corporate tax is present then the debt cost

may change. If we want the actual cost, then the tax rate should be deducted (Brigham and

Ehrhardt, 2013).

3. Reason of difference in the debt cost and the equity cost

The reason for getting the difference in the calculation of debt cost and cost of equity is the

consideration of the Current market price of the share, which is definitely not considered while

calculating the debt cost calculation. This in term reflects that the earnings of the company

depend on the current liabilities also and the only way to get the result it should be considered at

the time of calculating the cost of capital (Madura, 2011).

4. Pros and Cons of including current liabilities in the calculation of cost of capital

Yes according to the analyst, the Current Liabilities should be included in the calculation of the

cost of capital.

Pros of including the current liabilities in the calculation of the cost of capital:

8 | P a g e

1. Weighted Average cost of Capital (WACC) of Zeta Resources Ltd.

It is the average rate of return a company expects to compensate all its diverse investors. The

weights used in the targeted capital structure of the company are the fraction of each financing

source (Kastellorizos, 2011). It is also known as a calculation of firm’s cost of capital in which

each capital category is proportionately weighted.

2. Company’s tax rate in calculating WACC

At the time of calculating the weighted average cost of capital for the Zeta Resources Ltd, the tax

rate has been deducted for the debt cost, because if the corporate tax is present then the debt cost

may change. If we want the actual cost, then the tax rate should be deducted (Brigham and

Ehrhardt, 2013).

3. Reason of difference in the debt cost and the equity cost

The reason for getting the difference in the calculation of debt cost and cost of equity is the

consideration of the Current market price of the share, which is definitely not considered while

calculating the debt cost calculation. This in term reflects that the earnings of the company

depend on the current liabilities also and the only way to get the result it should be considered at

the time of calculating the cost of capital (Madura, 2011).

4. Pros and Cons of including current liabilities in the calculation of cost of capital

Yes according to the analyst, the Current Liabilities should be included in the calculation of the

cost of capital.

Pros of including the current liabilities in the calculation of the cost of capital:

8 | P a g e

The company can easily identify the actual and reasonable cost of its capital because of the much

high cost of current liabilities.

Cons of including the current liabilities in the calculus of cost of capital:

By including the current liabilities in the cost of capital, the cost of capital of the company

increases.

5. The major value of calculation of WACC for Zeta Resources Ltd.

Cost of debt is the major value of WACC. The company’s management of can understands that whether

they should borrow money or not from the external sources of the market for investment just by simply

considering the cost of debt.

6. Examples of recently used WACC in the Zeta Resources Ltd.

Calculation of Economic Value added:

Economic value added is calculated by deducting the cost of capital from the net revenues of the

Zeta Resources Ltd. In calculating the Economic value added, WACC helps as the company’s

cost of capital. Exactly that’s how the WACC can also be called a tool for the creation of value.

7. The capital structure of Zeta Resources Ltd.

On referencing the financial statements of the company, the analyst analyzed that company has

long-term debts only and the company is not having any proportion of short-term debts in its

capital structure. On comparing this with the industrial norms, it can be conveyed that it is

entirely different from the standards of the industry.

8. Optimal capital structure

That portion of equity and debt capital which creates the highest value for the company and at

the same time having the capital cost at its lowest point. It can be differentiated if the rate of

interest in the economy changes or rate of economic inflation changes.

9 | P a g e

high cost of current liabilities.

Cons of including the current liabilities in the calculus of cost of capital:

By including the current liabilities in the cost of capital, the cost of capital of the company

increases.

5. The major value of calculation of WACC for Zeta Resources Ltd.

Cost of debt is the major value of WACC. The company’s management of can understands that whether

they should borrow money or not from the external sources of the market for investment just by simply

considering the cost of debt.

6. Examples of recently used WACC in the Zeta Resources Ltd.

Calculation of Economic Value added:

Economic value added is calculated by deducting the cost of capital from the net revenues of the

Zeta Resources Ltd. In calculating the Economic value added, WACC helps as the company’s

cost of capital. Exactly that’s how the WACC can also be called a tool for the creation of value.

7. The capital structure of Zeta Resources Ltd.

On referencing the financial statements of the company, the analyst analyzed that company has

long-term debts only and the company is not having any proportion of short-term debts in its

capital structure. On comparing this with the industrial norms, it can be conveyed that it is

entirely different from the standards of the industry.

8. Optimal capital structure

That portion of equity and debt capital which creates the highest value for the company and at

the same time having the capital cost at its lowest point. It can be differentiated if the rate of

interest in the economy changes or rate of economic inflation changes.

9 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6.

(IV) Market Analysis

1. Comment on the financial performance of Zeta Resource Ltd

In the above-detailed study, it has been identified that Zeta Resource Ltd. is one of the topmost

and leading investments company, investing the pooled funds of its shareholders simply in

accordance with its investments policy and objectives (Healy and Palepu, 2012). The company s

having an aim and objective of producing and generating returns for the shareholders with an

acceptable risk level.

2. Literature search on the company

If we consider the financial report of the company, it can be easily identified that the financial

reports of the company have provided the true and fair view of the performance of the company

(Michalski, 2013). It is simply because of the reason that the company’s earnings have

frequently increased in some of the last recent years and along with that, there has been an

increase in the company’s revenues also.

3. Comment on any other item that is important or different about the company

Cash inflow is a very important tool for any organization to determine the financial position of

the company (WORSE, 2013). Rise in the flow of liquid cash of the company which frequently

states that the working capital of the company is using in the daily operations and activities of

the business. This flow of liquid cash showcases that the company will not face any difficulty in

facing the short-term liabilities of the company (Gill, et. al., 2010).

10 | P a g e

(IV) Market Analysis

1. Comment on the financial performance of Zeta Resource Ltd

In the above-detailed study, it has been identified that Zeta Resource Ltd. is one of the topmost

and leading investments company, investing the pooled funds of its shareholders simply in

accordance with its investments policy and objectives (Healy and Palepu, 2012). The company s

having an aim and objective of producing and generating returns for the shareholders with an

acceptable risk level.

2. Literature search on the company

If we consider the financial report of the company, it can be easily identified that the financial

reports of the company have provided the true and fair view of the performance of the company

(Michalski, 2013). It is simply because of the reason that the company’s earnings have

frequently increased in some of the last recent years and along with that, there has been an

increase in the company’s revenues also.

3. Comment on any other item that is important or different about the company

Cash inflow is a very important tool for any organization to determine the financial position of

the company (WORSE, 2013). Rise in the flow of liquid cash of the company which frequently

states that the working capital of the company is using in the daily operations and activities of

the business. This flow of liquid cash showcases that the company will not face any difficulty in

facing the short-term liabilities of the company (Gill, et. al., 2010).

10 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

References

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Brigham, E.F. and Houston, J.F., 2012. Fundamentals of financial management. Cengage

Learning.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Madura, J., 2011. International financial management. Cengage Learning.

Healy, P.M. and Palepu, K.G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Gill, A., Biger, N. and Mathur, N., 2010. The relationship between working capital management

and profitability: Evidence from the United States. Business and Economics Journal, 10(1), pp.1-

9.

Michalski, G., 2013. Portfolio management approach in trade credit decision making. arXiv

preprint arXiv:1301.3823.

WORSE, I., Class of 2013 ASX Minerals IPOs: Funding at a Decadal Low.

Kastellorizos, P., 2011. Third Annual report on Zeta Project.

Thella, J.S., Manna, M., Mukherjee, A.K. and Banerjee, P.K., 2011. Zeta potential: holistic

approach to control electro-kinetics in dispersion-selective flocculation systems. In MPT-2011:

XII International Conference on Mineral Processing Technology.

Purves, N., Niblock, S.J. and Sloan, K., 2015. On the relationship between financial and non-

financial factors: A case study analysis of financial failure predictors of agribusiness firms in

Australia. Agricultural Finance Review, 75(2), pp.282-300.

11 | P a g e

Higgins, R.C., 2012. Analysis for financial management. McGraw-Hill/Irwin.

Brigham, E.F. and Houston, J.F., 2012. Fundamentals of financial management. Cengage

Learning.

Brigham, E.F. and Ehrhardt, M.C., 2013. Financial management: Theory & practice. Cengage

Learning.

Madura, J., 2011. International financial management. Cengage Learning.

Healy, P.M. and Palepu, K.G., 2012. Business analysis valuation: Using financial statements.

Cengage Learning.

Gill, A., Biger, N. and Mathur, N., 2010. The relationship between working capital management

and profitability: Evidence from the United States. Business and Economics Journal, 10(1), pp.1-

9.

Michalski, G., 2013. Portfolio management approach in trade credit decision making. arXiv

preprint arXiv:1301.3823.

WORSE, I., Class of 2013 ASX Minerals IPOs: Funding at a Decadal Low.

Kastellorizos, P., 2011. Third Annual report on Zeta Project.

Thella, J.S., Manna, M., Mukherjee, A.K. and Banerjee, P.K., 2011. Zeta potential: holistic

approach to control electro-kinetics in dispersion-selective flocculation systems. In MPT-2011:

XII International Conference on Mineral Processing Technology.

Purves, N., Niblock, S.J. and Sloan, K., 2015. On the relationship between financial and non-

financial factors: A case study analysis of financial failure predictors of agribusiness firms in

Australia. Agricultural Finance Review, 75(2), pp.282-300.

11 | P a g e

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.