Financial Statistics Report: Woolworths Group Performance Analysis

VerifiedAdded on 2023/06/10

|10

|1551

|383

Report

AI Summary

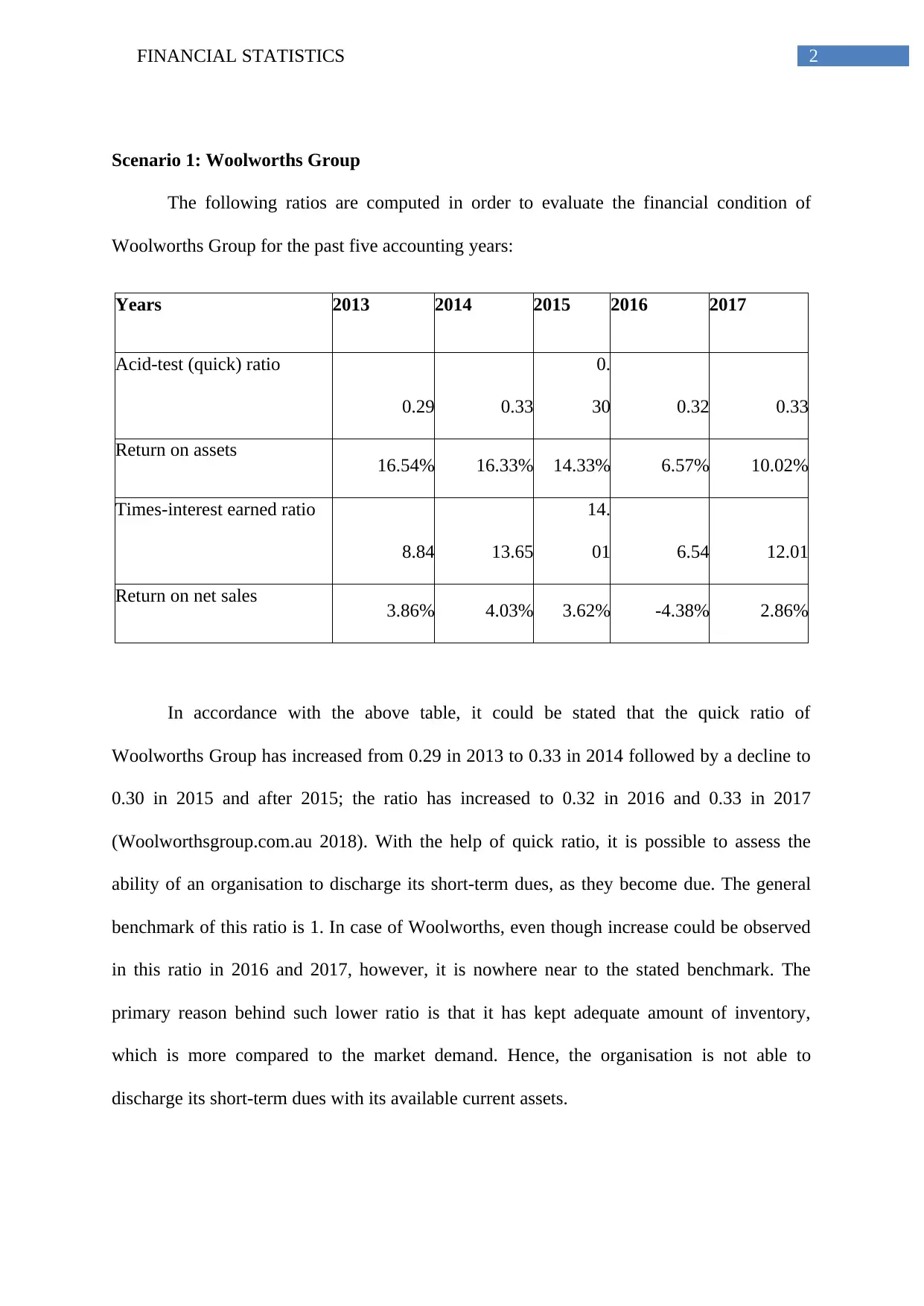

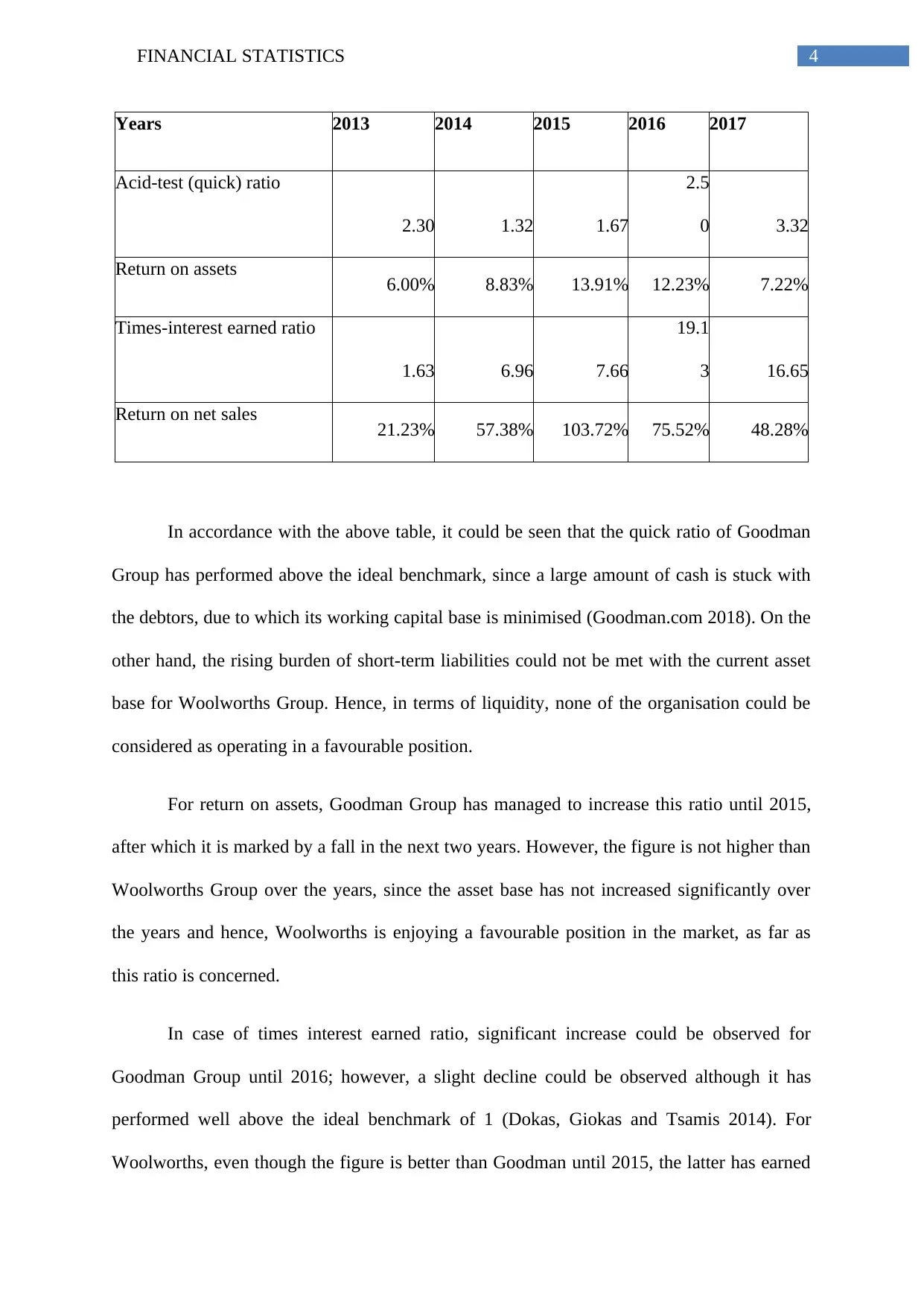

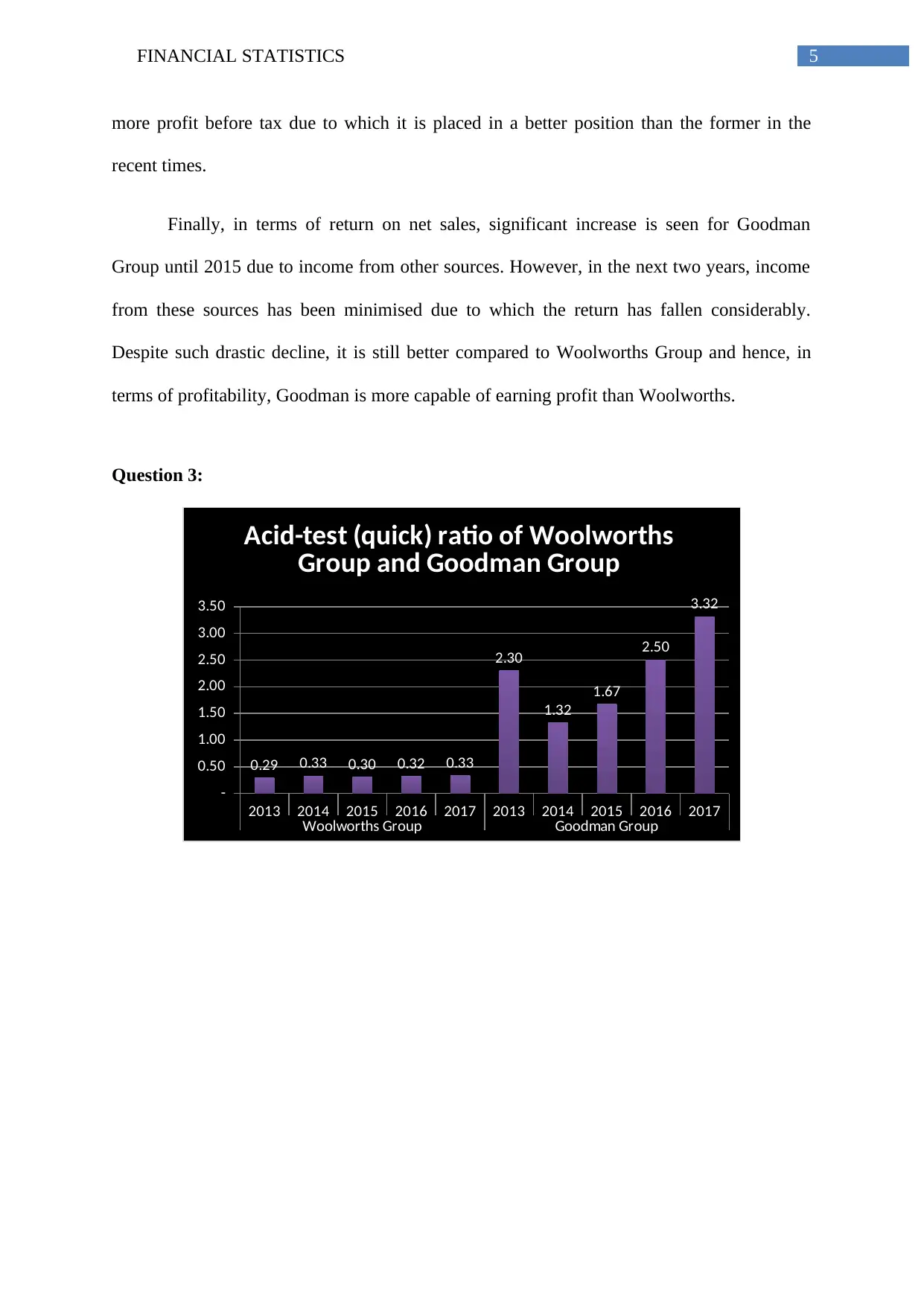

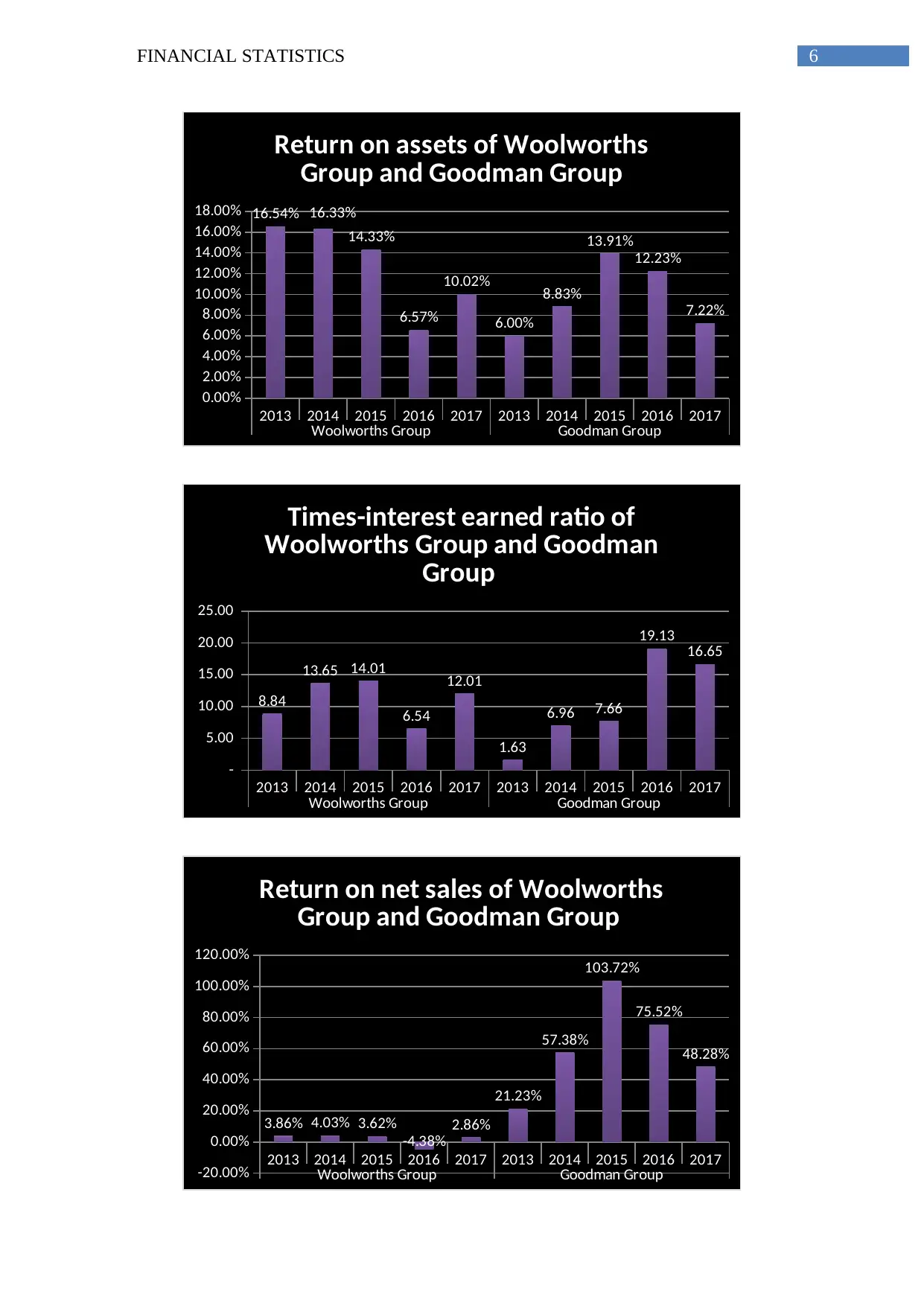

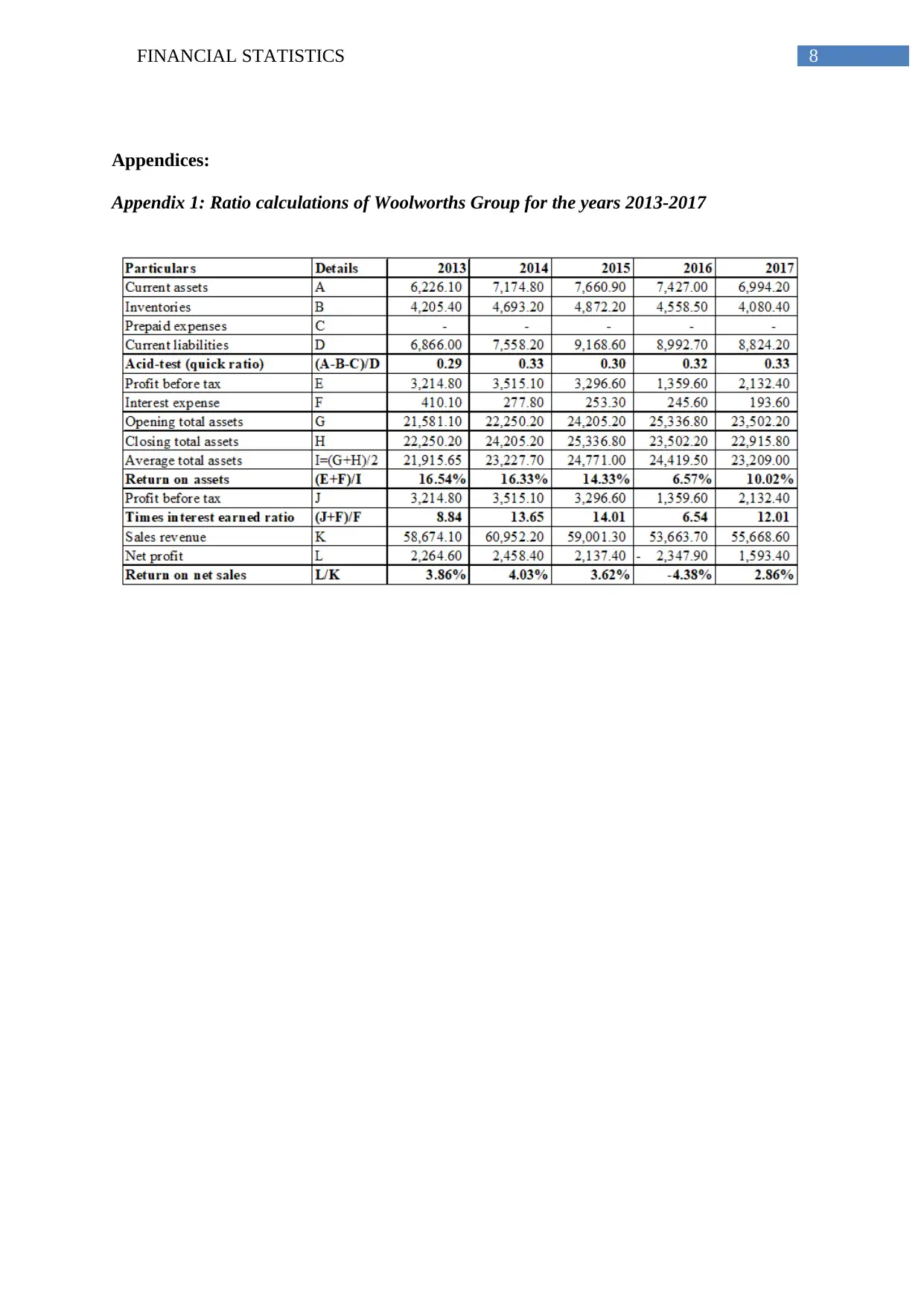

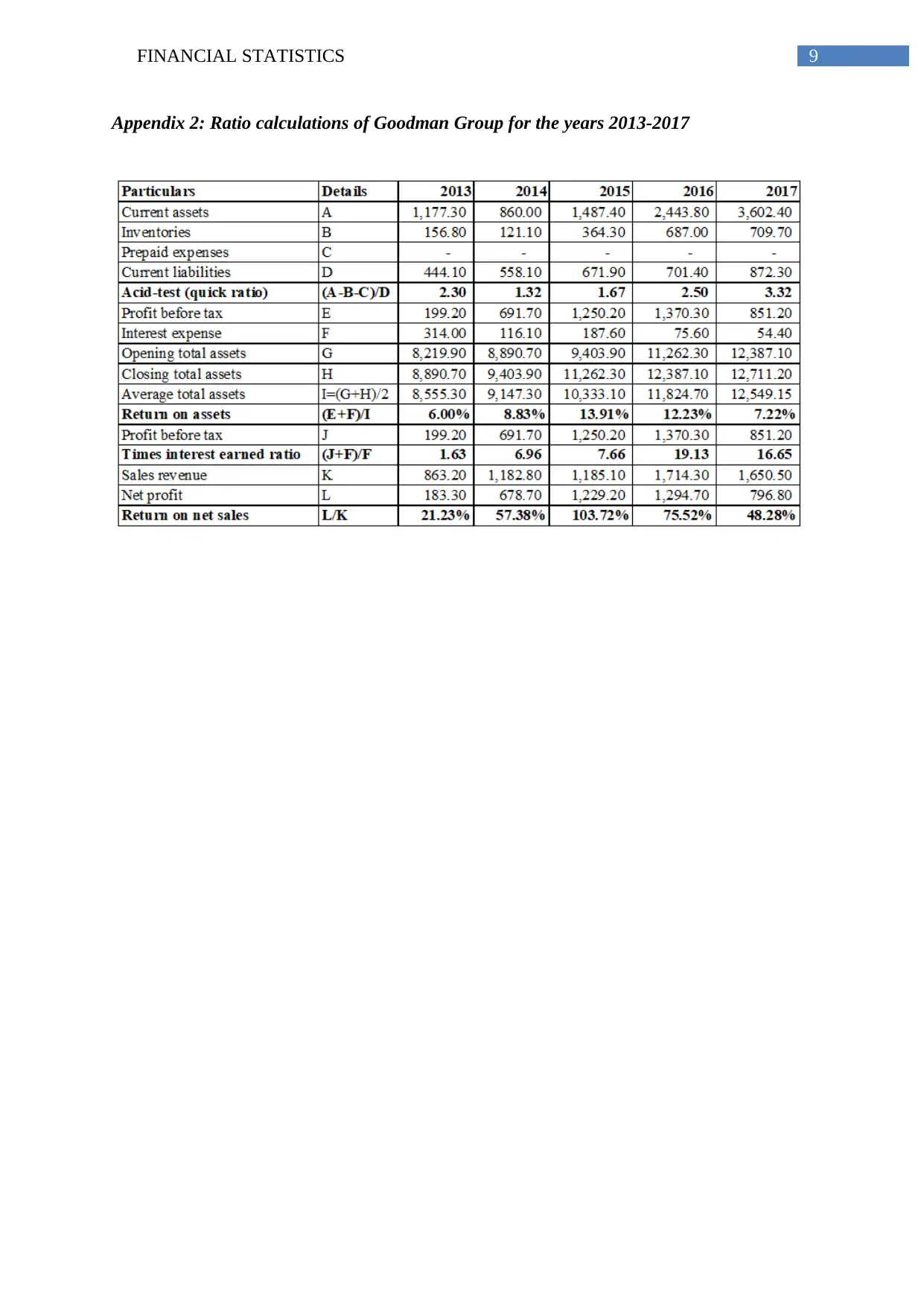

This report presents a financial analysis of Woolworths Group, evaluating its performance from 2013 to 2017 using key financial ratios. The analysis includes the quick ratio, return on assets, times interest earned ratio, and return on net sales. The report examines the trends in each ratio over the five-year period, assessing whether the company's performance is improving or worsening. The quick ratio indicates an increasing trend, though remaining below the benchmark. Return on assets initially declined but improved in later years. The times-interest-earned ratio fluctuated but generally remained above the ideal standard. Return on net sales showed fluctuations, including a negative value in 2016, with improvement in 2017. The report attributes these trends to factors like inventory management, profitability, and market demand. Furthermore, the report compares Woolworths' performance with Goodman Group, highlighting differences in liquidity, profitability, and solvency based on the calculated ratios. Graphs are used to visually compare the performance of both companies.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.