Financial Strategy and Policy Report: Seine Products Ltd. Analysis

VerifiedAdded on 2023/01/19

|11

|2554

|35

Report

AI Summary

This report provides a comprehensive analysis of financial strategy and policy, encompassing several key areas. Section A focuses on a six-month cash budget for Seine Products Ltd., detailing projected sales, receipts, payments, and cash flow. Section B delves into the practical problem of capital financing, evaluating three proposed financing options: issuing right shares, preference shares, and loan stock. It analyzes the features, suitability, and impact on earnings per share of each option, concluding that issuing 8% loan stock is the most suitable option. Section C calculates the weighted average cost of capital (WACC). Section D addresses the challenges and considerations for Rosdeaye Ltd., a UK manufacturing entity, in establishing overseas operations, specifically in the Caribbean. The report highlights labor market variations, political risks, and the importance of strategic planning for successful international expansion. The analysis provides insights into financial planning, cost of capital, and the implications of overseas operations.

FINANCIAL STRATEGY

AND POLICY

AND POLICY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................1

SECTION - A..................................................................................................................................1

Cash Budget............................................................................................................................1

SECTION – B..................................................................................................................................2

a) Important features of each of the three proposed financing options..................................2

b) Suitability of proposed financing option............................................................................6

SECTION – C..................................................................................................................................6

SECTION – D..................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

SECTION - A..................................................................................................................................1

Cash Budget............................................................................................................................1

SECTION – B..................................................................................................................................2

a) Important features of each of the three proposed financing options..................................2

b) Suitability of proposed financing option............................................................................6

SECTION – C..................................................................................................................................6

SECTION – D..................................................................................................................................7

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

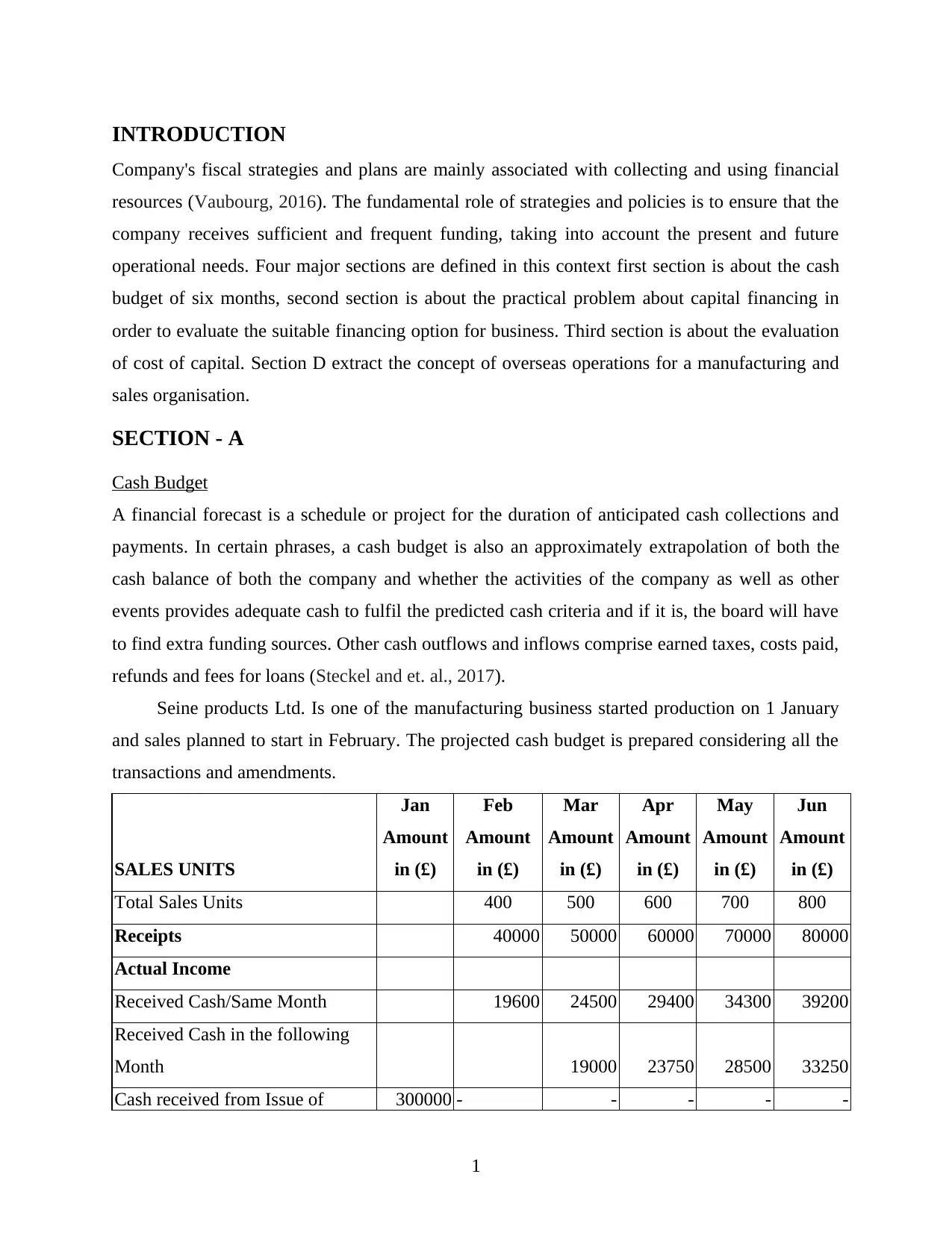

INTRODUCTION

Company's fiscal strategies and plans are mainly associated with collecting and using financial

resources (Vaubourg, 2016). The fundamental role of strategies and policies is to ensure that the

company receives sufficient and frequent funding, taking into account the present and future

operational needs. Four major sections are defined in this context first section is about the cash

budget of six months, second section is about the practical problem about capital financing in

order to evaluate the suitable financing option for business. Third section is about the evaluation

of cost of capital. Section D extract the concept of overseas operations for a manufacturing and

sales organisation.

SECTION - A

Cash Budget

A financial forecast is a schedule or project for the duration of anticipated cash collections and

payments. In certain phrases, a cash budget is also an approximately extrapolation of both the

cash balance of both the company and whether the activities of the company as well as other

events provides adequate cash to fulfil the predicted cash criteria and if it is, the board will have

to find extra funding sources. Other cash outflows and inflows comprise earned taxes, costs paid,

refunds and fees for loans (Steckel and et. al., 2017).

Seine products Ltd. Is one of the manufacturing business started production on 1 January

and sales planned to start in February. The projected cash budget is prepared considering all the

transactions and amendments.

SALES UNITS

Jan

Amount

in (£)

Feb

Amount

in (£)

Mar

Amount

in (£)

Apr

Amount

in (£)

May

Amount

in (£)

Jun

Amount

in (£)

Total Sales Units 400 500 600 700 800

Receipts 40000 50000 60000 70000 80000

Actual Income

Received Cash/Same Month 19600 24500 29400 34300 39200

Received Cash in the following

Month 19000 23750 28500 33250

Cash received from Issue of 300000 - - - - -

1

Company's fiscal strategies and plans are mainly associated with collecting and using financial

resources (Vaubourg, 2016). The fundamental role of strategies and policies is to ensure that the

company receives sufficient and frequent funding, taking into account the present and future

operational needs. Four major sections are defined in this context first section is about the cash

budget of six months, second section is about the practical problem about capital financing in

order to evaluate the suitable financing option for business. Third section is about the evaluation

of cost of capital. Section D extract the concept of overseas operations for a manufacturing and

sales organisation.

SECTION - A

Cash Budget

A financial forecast is a schedule or project for the duration of anticipated cash collections and

payments. In certain phrases, a cash budget is also an approximately extrapolation of both the

cash balance of both the company and whether the activities of the company as well as other

events provides adequate cash to fulfil the predicted cash criteria and if it is, the board will have

to find extra funding sources. Other cash outflows and inflows comprise earned taxes, costs paid,

refunds and fees for loans (Steckel and et. al., 2017).

Seine products Ltd. Is one of the manufacturing business started production on 1 January

and sales planned to start in February. The projected cash budget is prepared considering all the

transactions and amendments.

SALES UNITS

Jan

Amount

in (£)

Feb

Amount

in (£)

Mar

Amount

in (£)

Apr

Amount

in (£)

May

Amount

in (£)

Jun

Amount

in (£)

Total Sales Units 400 500 600 700 800

Receipts 40000 50000 60000 70000 80000

Actual Income

Received Cash/Same Month 19600 24500 29400 34300 39200

Received Cash in the following

Month 19000 23750 28500 33250

Cash received from Issue of 300000 - - - - -

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

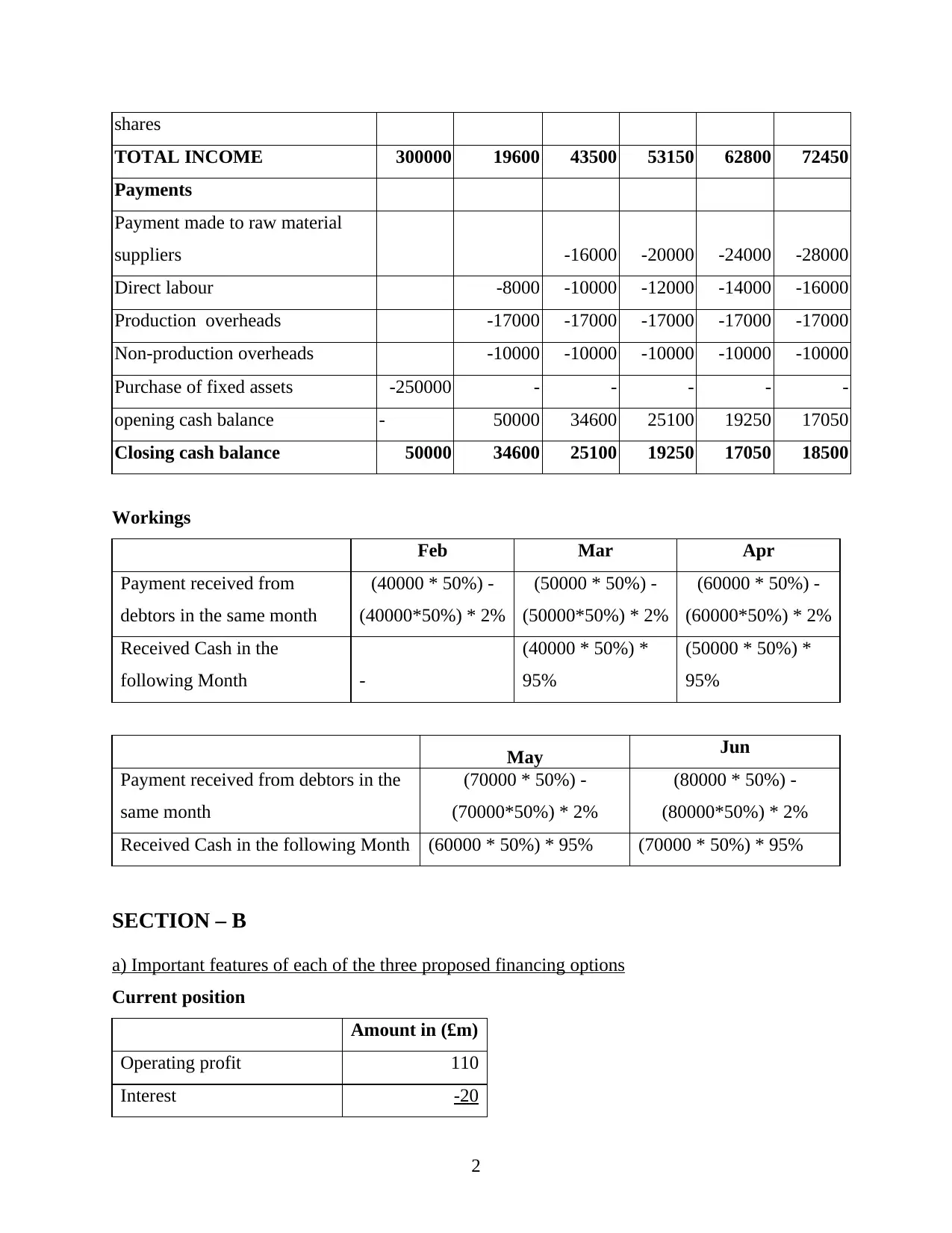

shares

TOTAL INCOME 300000 19600 43500 53150 62800 72450

Payments

Payment made to raw material

suppliers -16000 -20000 -24000 -28000

Direct labour -8000 -10000 -12000 -14000 -16000

Production overheads -17000 -17000 -17000 -17000 -17000

Non-production overheads -10000 -10000 -10000 -10000 -10000

Purchase of fixed assets -250000 - - - - -

opening cash balance - 50000 34600 25100 19250 17050

Closing cash balance 50000 34600 25100 19250 17050 18500

Workings

Feb Mar Apr

Payment received from

debtors in the same month

(40000 * 50%) -

(40000*50%) * 2%

(50000 * 50%) -

(50000*50%) * 2%

(60000 * 50%) -

(60000*50%) * 2%

Received Cash in the

following Month -

(40000 * 50%) *

95%

(50000 * 50%) *

95%

May Jun

Payment received from debtors in the

same month

(70000 * 50%) -

(70000*50%) * 2%

(80000 * 50%) -

(80000*50%) * 2%

Received Cash in the following Month (60000 * 50%) * 95% (70000 * 50%) * 95%

SECTION – B

a) Important features of each of the three proposed financing options

Current position

Amount in (£m)

Operating profit 110

Interest -20

2

TOTAL INCOME 300000 19600 43500 53150 62800 72450

Payments

Payment made to raw material

suppliers -16000 -20000 -24000 -28000

Direct labour -8000 -10000 -12000 -14000 -16000

Production overheads -17000 -17000 -17000 -17000 -17000

Non-production overheads -10000 -10000 -10000 -10000 -10000

Purchase of fixed assets -250000 - - - - -

opening cash balance - 50000 34600 25100 19250 17050

Closing cash balance 50000 34600 25100 19250 17050 18500

Workings

Feb Mar Apr

Payment received from

debtors in the same month

(40000 * 50%) -

(40000*50%) * 2%

(50000 * 50%) -

(50000*50%) * 2%

(60000 * 50%) -

(60000*50%) * 2%

Received Cash in the

following Month -

(40000 * 50%) *

95%

(50000 * 50%) *

95%

May Jun

Payment received from debtors in the

same month

(70000 * 50%) -

(70000*50%) * 2%

(80000 * 50%) -

(80000*50%) * 2%

Received Cash in the following Month (60000 * 50%) * 95% (70000 * 50%) * 95%

SECTION – B

a) Important features of each of the three proposed financing options

Current position

Amount in (£m)

Operating profit 110

Interest -20

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

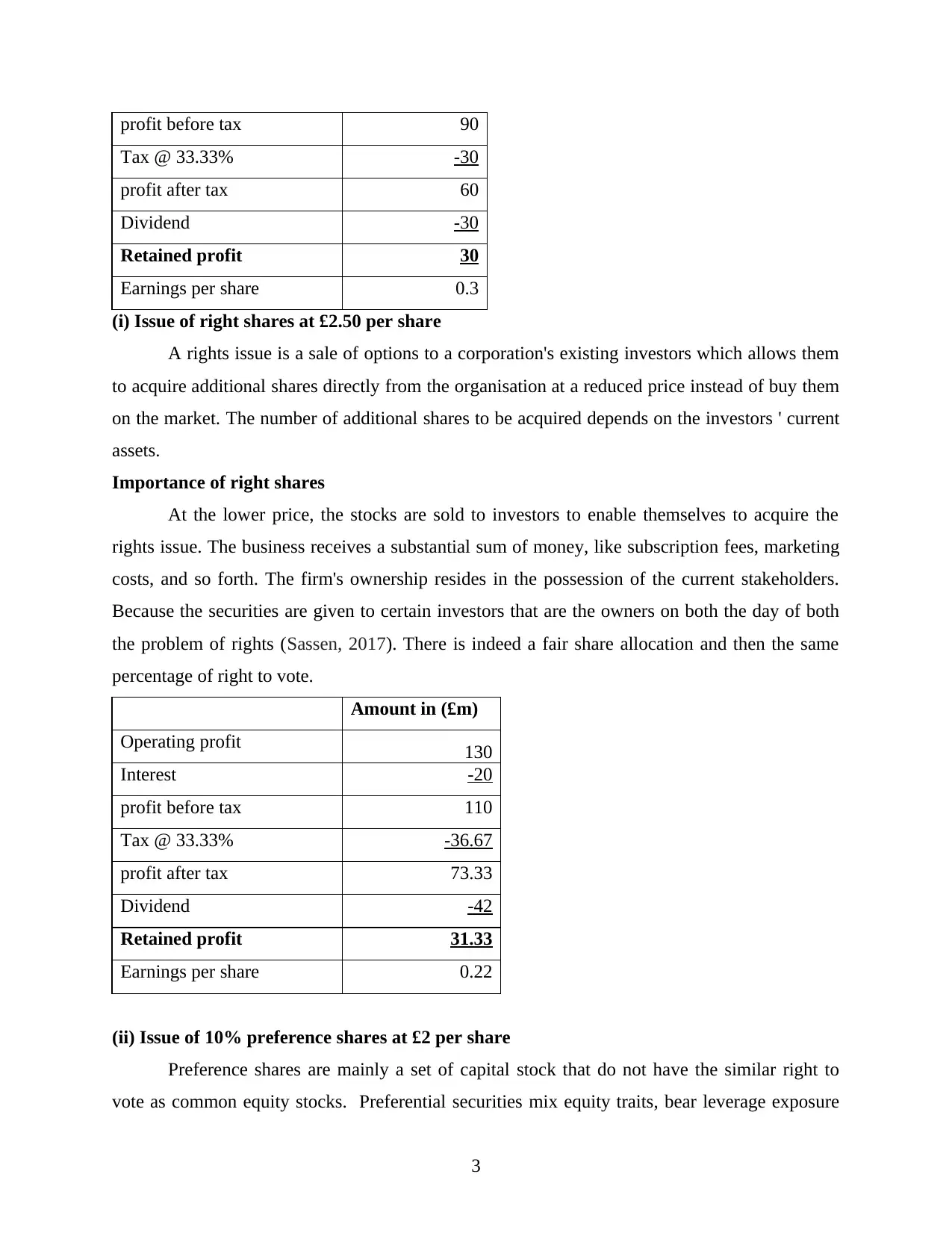

profit before tax 90

Tax @ 33.33% -30

profit after tax 60

Dividend -30

Retained profit 30

Earnings per share 0.3

(i) Issue of right shares at £2.50 per share

A rights issue is a sale of options to a corporation's existing investors which allows them

to acquire additional shares directly from the organisation at a reduced price instead of buy them

on the market. The number of additional shares to be acquired depends on the investors ' current

assets.

Importance of right shares

At the lower price, the stocks are sold to investors to enable themselves to acquire the

rights issue. The business receives a substantial sum of money, like subscription fees, marketing

costs, and so forth. The firm's ownership resides in the possession of the current stakeholders.

Because the securities are given to certain investors that are the owners on both the day of both

the problem of rights (Sassen, 2017). There is indeed a fair share allocation and then the same

percentage of right to vote.

Amount in (£m)

Operating profit 130

Interest -20

profit before tax 110

Tax @ 33.33% -36.67

profit after tax 73.33

Dividend -42

Retained profit 31.33

Earnings per share 0.22

(ii) Issue of 10% preference shares at £2 per share

Preference shares are mainly a set of capital stock that do not have the similar right to

vote as common equity stocks. Preferential securities mix equity traits, bear leverage exposure

3

Tax @ 33.33% -30

profit after tax 60

Dividend -30

Retained profit 30

Earnings per share 0.3

(i) Issue of right shares at £2.50 per share

A rights issue is a sale of options to a corporation's existing investors which allows them

to acquire additional shares directly from the organisation at a reduced price instead of buy them

on the market. The number of additional shares to be acquired depends on the investors ' current

assets.

Importance of right shares

At the lower price, the stocks are sold to investors to enable themselves to acquire the

rights issue. The business receives a substantial sum of money, like subscription fees, marketing

costs, and so forth. The firm's ownership resides in the possession of the current stakeholders.

Because the securities are given to certain investors that are the owners on both the day of both

the problem of rights (Sassen, 2017). There is indeed a fair share allocation and then the same

percentage of right to vote.

Amount in (£m)

Operating profit 130

Interest -20

profit before tax 110

Tax @ 33.33% -36.67

profit after tax 73.33

Dividend -42

Retained profit 31.33

Earnings per share 0.22

(ii) Issue of 10% preference shares at £2 per share

Preference shares are mainly a set of capital stock that do not have the similar right to

vote as common equity stocks. Preferential securities mix equity traits, bear leverage exposure

3

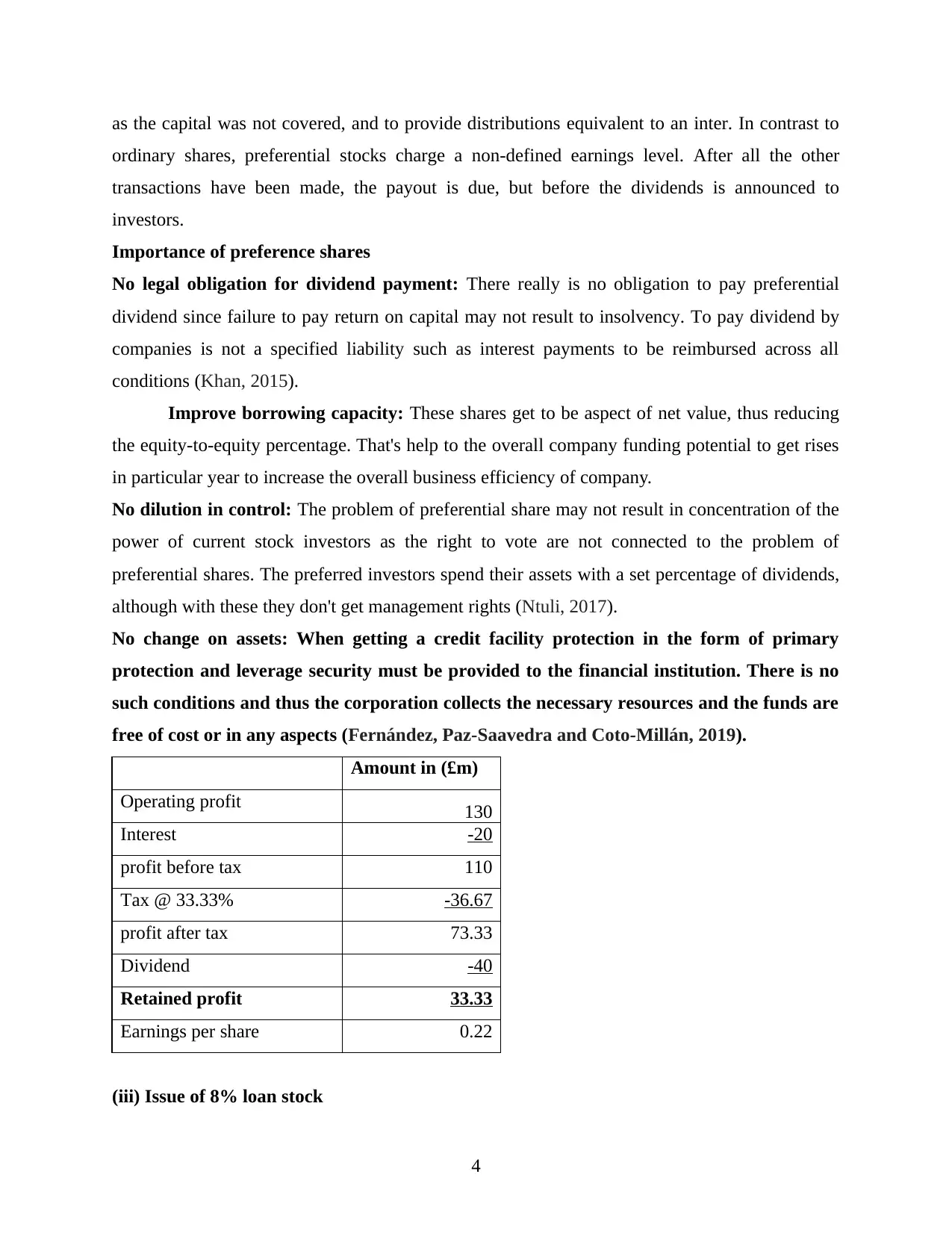

as the capital was not covered, and to provide distributions equivalent to an inter. In contrast to

ordinary shares, preferential stocks charge a non-defined earnings level. After all the other

transactions have been made, the payout is due, but before the dividends is announced to

investors.

Importance of preference shares

No legal obligation for dividend payment: There really is no obligation to pay preferential

dividend since failure to pay return on capital may not result to insolvency. To pay dividend by

companies is not a specified liability such as interest payments to be reimbursed across all

conditions (Khan, 2015).

Improve borrowing capacity: These shares get to be aspect of net value, thus reducing

the equity-to-equity percentage. That's help to the overall company funding potential to get rises

in particular year to increase the overall business efficiency of company.

No dilution in control: The problem of preferential share may not result in concentration of the

power of current stock investors as the right to vote are not connected to the problem of

preferential shares. The preferred investors spend their assets with a set percentage of dividends,

although with these they don't get management rights (Ntuli, 2017).

No change on assets: When getting a credit facility protection in the form of primary

protection and leverage security must be provided to the financial institution. There is no

such conditions and thus the corporation collects the necessary resources and the funds are

free of cost or in any aspects (Fernández, Paz-Saavedra and Coto-Millán, 2019).

Amount in (£m)

Operating profit 130

Interest -20

profit before tax 110

Tax @ 33.33% -36.67

profit after tax 73.33

Dividend -40

Retained profit 33.33

Earnings per share 0.22

(iii) Issue of 8% loan stock

4

ordinary shares, preferential stocks charge a non-defined earnings level. After all the other

transactions have been made, the payout is due, but before the dividends is announced to

investors.

Importance of preference shares

No legal obligation for dividend payment: There really is no obligation to pay preferential

dividend since failure to pay return on capital may not result to insolvency. To pay dividend by

companies is not a specified liability such as interest payments to be reimbursed across all

conditions (Khan, 2015).

Improve borrowing capacity: These shares get to be aspect of net value, thus reducing

the equity-to-equity percentage. That's help to the overall company funding potential to get rises

in particular year to increase the overall business efficiency of company.

No dilution in control: The problem of preferential share may not result in concentration of the

power of current stock investors as the right to vote are not connected to the problem of

preferential shares. The preferred investors spend their assets with a set percentage of dividends,

although with these they don't get management rights (Ntuli, 2017).

No change on assets: When getting a credit facility protection in the form of primary

protection and leverage security must be provided to the financial institution. There is no

such conditions and thus the corporation collects the necessary resources and the funds are

free of cost or in any aspects (Fernández, Paz-Saavedra and Coto-Millán, 2019).

Amount in (£m)

Operating profit 130

Interest -20

profit before tax 110

Tax @ 33.33% -36.67

profit after tax 73.33

Dividend -40

Retained profit 33.33

Earnings per share 0.22

(iii) Issue of 8% loan stock

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

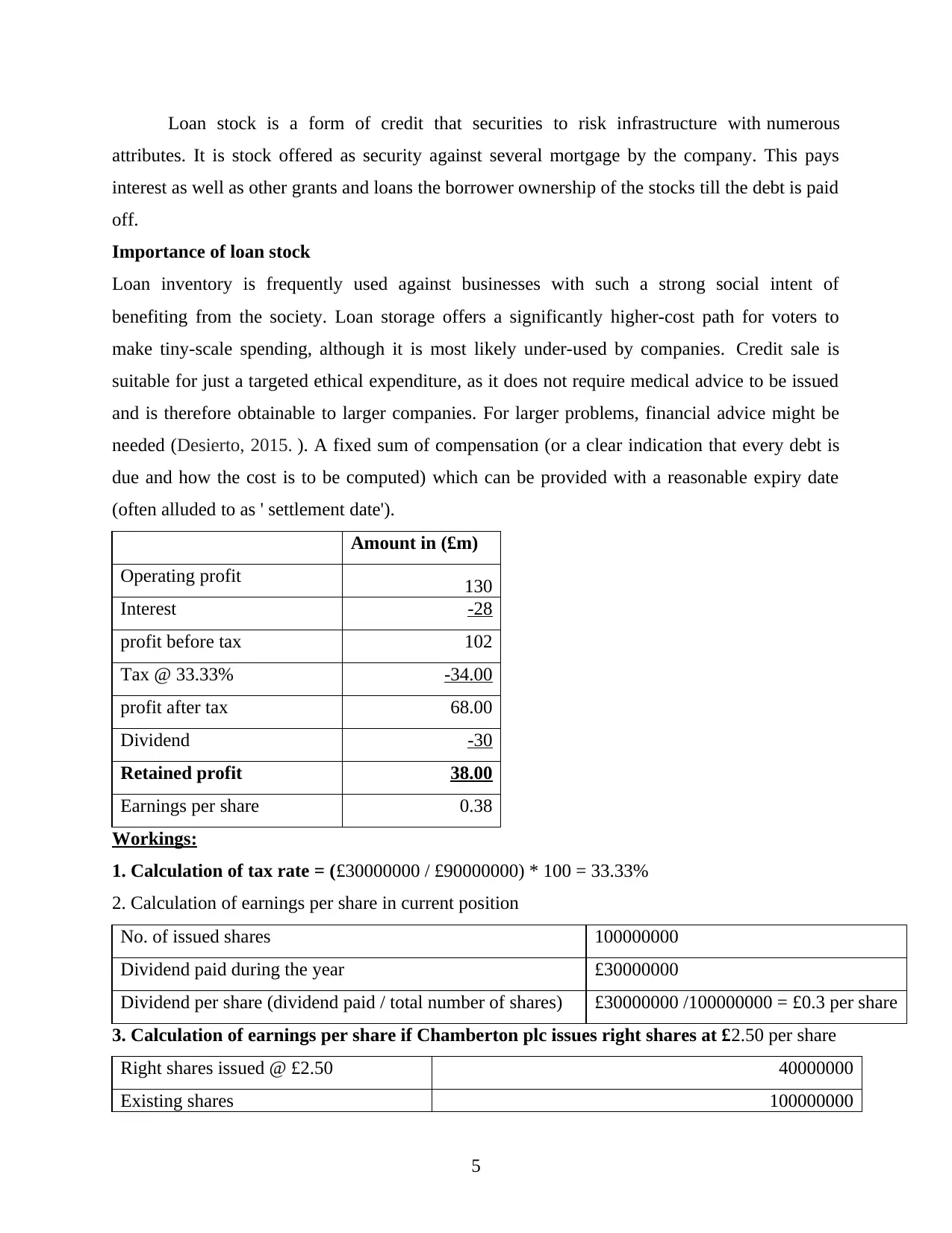

Loan stock is a form of credit that securities to risk infrastructure with numerous

attributes. It is stock offered as security against several mortgage by the company. This pays

interest as well as other grants and loans the borrower ownership of the stocks till the debt is paid

off.

Importance of loan stock

Loan inventory is frequently used against businesses with such a strong social intent of

benefiting from the society. Loan storage offers a significantly higher-cost path for voters to

make tiny-scale spending, although it is most likely under-used by companies. Credit sale is

suitable for just a targeted ethical expenditure, as it does not require medical advice to be issued

and is therefore obtainable to larger companies. For larger problems, financial advice might be

needed (Desierto, 2015. ). A fixed sum of compensation (or a clear indication that every debt is

due and how the cost is to be computed) which can be provided with a reasonable expiry date

(often alluded to as ' settlement date').

Amount in (£m)

Operating profit 130

Interest -28

profit before tax 102

Tax @ 33.33% -34.00

profit after tax 68.00

Dividend -30

Retained profit 38.00

Earnings per share 0.38

Workings:

1. Calculation of tax rate = (£30000000 / £90000000) * 100 = 33.33%

2. Calculation of earnings per share in current position

No. of issued shares 100000000

Dividend paid during the year £30000000

Dividend per share (dividend paid / total number of shares) £30000000 /100000000 = £0.3 per share

3. Calculation of earnings per share if Chamberton plc issues right shares at £2.50 per share

Right shares issued @ £2.50 40000000

Existing shares 100000000

5

attributes. It is stock offered as security against several mortgage by the company. This pays

interest as well as other grants and loans the borrower ownership of the stocks till the debt is paid

off.

Importance of loan stock

Loan inventory is frequently used against businesses with such a strong social intent of

benefiting from the society. Loan storage offers a significantly higher-cost path for voters to

make tiny-scale spending, although it is most likely under-used by companies. Credit sale is

suitable for just a targeted ethical expenditure, as it does not require medical advice to be issued

and is therefore obtainable to larger companies. For larger problems, financial advice might be

needed (Desierto, 2015. ). A fixed sum of compensation (or a clear indication that every debt is

due and how the cost is to be computed) which can be provided with a reasonable expiry date

(often alluded to as ' settlement date').

Amount in (£m)

Operating profit 130

Interest -28

profit before tax 102

Tax @ 33.33% -34.00

profit after tax 68.00

Dividend -30

Retained profit 38.00

Earnings per share 0.38

Workings:

1. Calculation of tax rate = (£30000000 / £90000000) * 100 = 33.33%

2. Calculation of earnings per share in current position

No. of issued shares 100000000

Dividend paid during the year £30000000

Dividend per share (dividend paid / total number of shares) £30000000 /100000000 = £0.3 per share

3. Calculation of earnings per share if Chamberton plc issues right shares at £2.50 per share

Right shares issued @ £2.50 40000000

Existing shares 100000000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

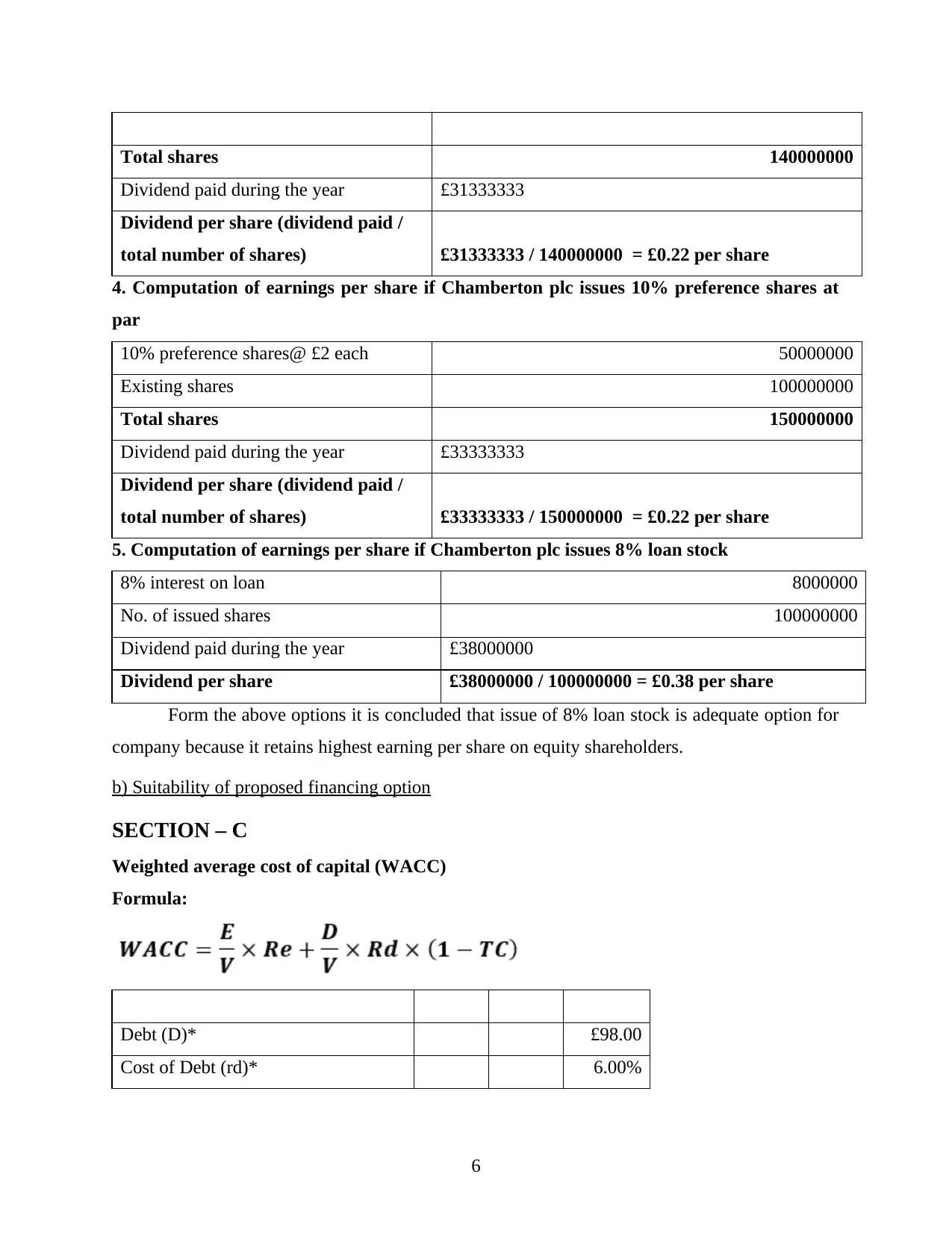

Total shares 140000000

Dividend paid during the year £31333333

Dividend per share (dividend paid /

total number of shares) £31333333 / 140000000 = £0.22 per share

4. Computation of earnings per share if Chamberton plc issues 10% preference shares at

par

10% preference shares@ £2 each 50000000

Existing shares 100000000

Total shares 150000000

Dividend paid during the year £33333333

Dividend per share (dividend paid /

total number of shares) £33333333 / 150000000 = £0.22 per share

5. Computation of earnings per share if Chamberton plc issues 8% loan stock

8% interest on loan 8000000

No. of issued shares 100000000

Dividend paid during the year £38000000

Dividend per share £38000000 / 100000000 = £0.38 per share

Form the above options it is concluded that issue of 8% loan stock is adequate option for

company because it retains highest earning per share on equity shareholders.

b) Suitability of proposed financing option

SECTION – C

Weighted average cost of capital (WACC)

Formula:

Debt (D)* £98.00

Cost of Debt (rd)* 6.00%

6

Dividend paid during the year £31333333

Dividend per share (dividend paid /

total number of shares) £31333333 / 140000000 = £0.22 per share

4. Computation of earnings per share if Chamberton plc issues 10% preference shares at

par

10% preference shares@ £2 each 50000000

Existing shares 100000000

Total shares 150000000

Dividend paid during the year £33333333

Dividend per share (dividend paid /

total number of shares) £33333333 / 150000000 = £0.22 per share

5. Computation of earnings per share if Chamberton plc issues 8% loan stock

8% interest on loan 8000000

No. of issued shares 100000000

Dividend paid during the year £38000000

Dividend per share £38000000 / 100000000 = £0.38 per share

Form the above options it is concluded that issue of 8% loan stock is adequate option for

company because it retains highest earning per share on equity shareholders.

b) Suitability of proposed financing option

SECTION – C

Weighted average cost of capital (WACC)

Formula:

Debt (D)* £98.00

Cost of Debt (rd)* 6.00%

6

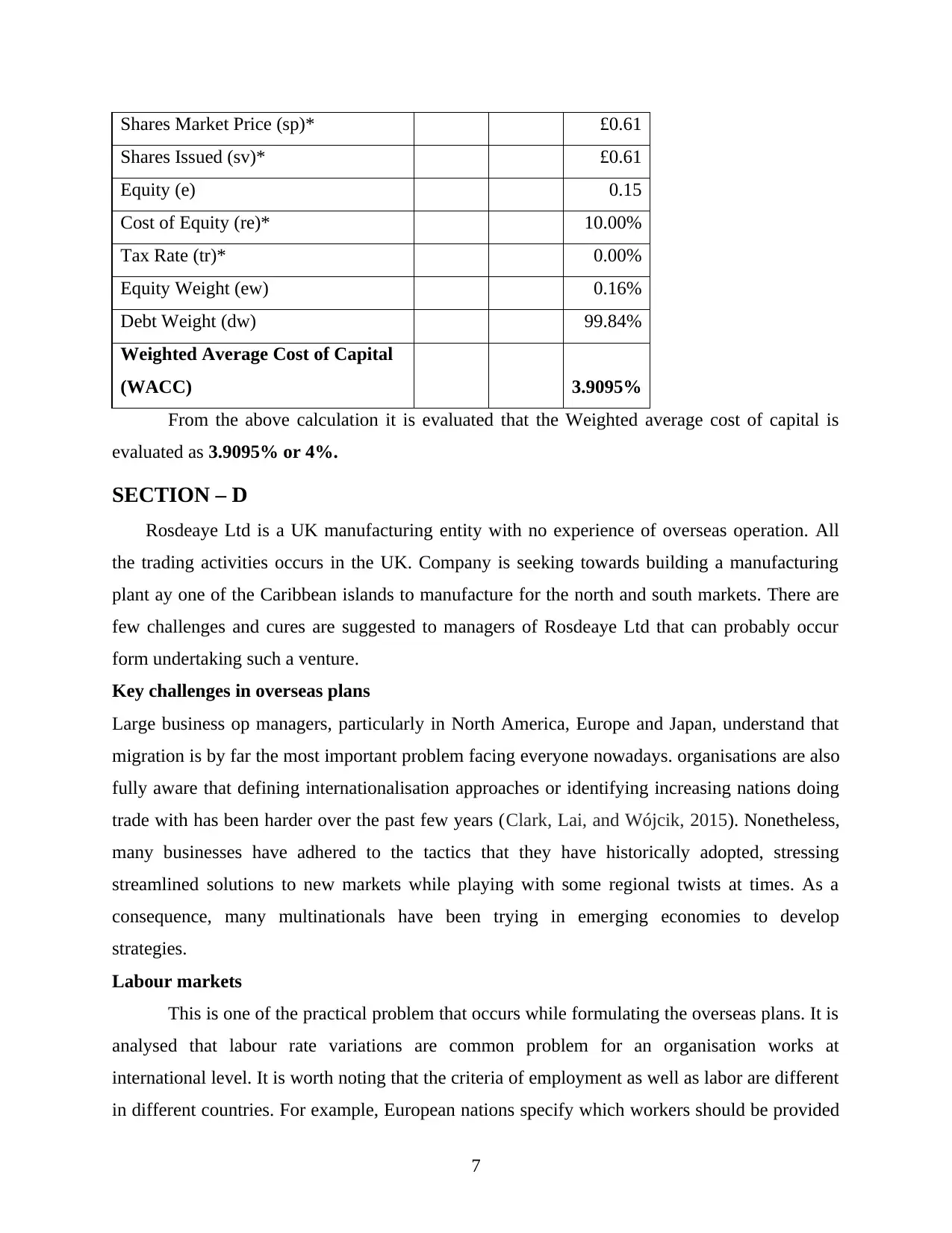

Shares Market Price (sp)* £0.61

Shares Issued (sv)* £0.61

Equity (e) 0.15

Cost of Equity (re)* 10.00%

Tax Rate (tr)* 0.00%

Equity Weight (ew) 0.16%

Debt Weight (dw) 99.84%

Weighted Average Cost of Capital

(WACC) 3.9095%

From the above calculation it is evaluated that the Weighted average cost of capital is

evaluated as 3.9095% or 4%.

SECTION – D

Rosdeaye Ltd is a UK manufacturing entity with no experience of overseas operation. All

the trading activities occurs in the UK. Company is seeking towards building a manufacturing

plant ay one of the Caribbean islands to manufacture for the north and south markets. There are

few challenges and cures are suggested to managers of Rosdeaye Ltd that can probably occur

form undertaking such a venture.

Key challenges in overseas plans

Large business op managers, particularly in North America, Europe and Japan, understand that

migration is by far the most important problem facing everyone nowadays. organisations are also

fully aware that defining internationalisation approaches or identifying increasing nations doing

trade with has been harder over the past few years (Clark, Lai, and Wójcik, 2015). Nonetheless,

many businesses have adhered to the tactics that they have historically adopted, stressing

streamlined solutions to new markets while playing with some regional twists at times. As a

consequence, many multinationals have been trying in emerging economies to develop

strategies.

Labour markets

This is one of the practical problem that occurs while formulating the overseas plans. It is

analysed that labour rate variations are common problem for an organisation works at

international level. It is worth noting that the criteria of employment as well as labor are different

in different countries. For example, European nations specify which workers should be provided

7

Shares Issued (sv)* £0.61

Equity (e) 0.15

Cost of Equity (re)* 10.00%

Tax Rate (tr)* 0.00%

Equity Weight (ew) 0.16%

Debt Weight (dw) 99.84%

Weighted Average Cost of Capital

(WACC) 3.9095%

From the above calculation it is evaluated that the Weighted average cost of capital is

evaluated as 3.9095% or 4%.

SECTION – D

Rosdeaye Ltd is a UK manufacturing entity with no experience of overseas operation. All

the trading activities occurs in the UK. Company is seeking towards building a manufacturing

plant ay one of the Caribbean islands to manufacture for the north and south markets. There are

few challenges and cures are suggested to managers of Rosdeaye Ltd that can probably occur

form undertaking such a venture.

Key challenges in overseas plans

Large business op managers, particularly in North America, Europe and Japan, understand that

migration is by far the most important problem facing everyone nowadays. organisations are also

fully aware that defining internationalisation approaches or identifying increasing nations doing

trade with has been harder over the past few years (Clark, Lai, and Wójcik, 2015). Nonetheless,

many businesses have adhered to the tactics that they have historically adopted, stressing

streamlined solutions to new markets while playing with some regional twists at times. As a

consequence, many multinationals have been trying in emerging economies to develop

strategies.

Labour markets

This is one of the practical problem that occurs while formulating the overseas plans. It is

analysed that labour rate variations are common problem for an organisation works at

international level. It is worth noting that the criteria of employment as well as labor are different

in different countries. For example, European nations specify which workers should be provided

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

a minimal level of 14-week parental leave, when U.S. workers do not have such a necessity.

Investments in knowledgeable and experienced multinational lawyer can be crucial with both the

intricacy involved in international exchange and employment rights.

Political risks

Surveillance and preparing international changes may reduce the political risks involved

of doing business overseas. Political uncertainty and volatility are an obvious risk for

international business. A risk assessment of the economic and political climate is important prior

to contemplating penetration into a new and uncertain area (Clark, Lai, and Wójcik, 2015).

Developed markets that can offer significant potential for international business expansion can

also face obstacles which are not posed by larger markets.

CONCLUSION

The above evaluation states the concept of financial strategies and policies. It is clearly

indicating that an effective financial strategies and policies leads organisation towards

sustainable success and helps in ascertain the requirements of successful business ideas. All the

four sections are critically analysed and presented with impacts and usefulness in organisational

context. Cash budgets, cost of capital and financial planning are categorised in this context. The

implications of overseas operations also categorised in the above context.

8

Investments in knowledgeable and experienced multinational lawyer can be crucial with both the

intricacy involved in international exchange and employment rights.

Political risks

Surveillance and preparing international changes may reduce the political risks involved

of doing business overseas. Political uncertainty and volatility are an obvious risk for

international business. A risk assessment of the economic and political climate is important prior

to contemplating penetration into a new and uncertain area (Clark, Lai, and Wójcik, 2015).

Developed markets that can offer significant potential for international business expansion can

also face obstacles which are not posed by larger markets.

CONCLUSION

The above evaluation states the concept of financial strategies and policies. It is clearly

indicating that an effective financial strategies and policies leads organisation towards

sustainable success and helps in ascertain the requirements of successful business ideas. All the

four sections are critically analysed and presented with impacts and usefulness in organisational

context. Cash budgets, cost of capital and financial planning are categorised in this context. The

implications of overseas operations also categorised in the above context.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals:

Vaubourg, A. G., 2016. Finance and international trade: A review of the literature. Revue

d'économie politique. 126(1). pp.57-87.

Steckel, J. C. and et. al., 2017. From climate finance toward sustainable development

finance. Wiley Interdisciplinary Reviews: Climate Change. 8(1). p.e437.

Sassen, S., 2017. Finance and business services in New York City: international linkages and

domestic effects. In Deindustrialization and Regional Economic Transformation(pp.

132-290). Routledge.

Ntuli, M. G., 2017. An evaluation of bank acquisition using an accounting based measure: a case

of Amalgamated Bank of South Africa and Barclays Bank Plc. Banks and Bank Systems.

12(1). p.160.

Khan, M. M., 2015. Sources of finance available for SME sector in Pakistan. International

Letters of Social and Humanistic Sciences. 47. pp.184-194.

Fernández, X. L., Paz-Saavedra, D. and Coto-Millán, P., 2019. THE IMPACT OF BREXIT ON

BANK EFFICIENCY: EVIDENCE FROM UK AND IRELAND. Finance Research

Letters. p.101338.

Desierto, D .A., 2015. Public policy in international economic law: the ICESCR in trade,

finance, and investment. Oxford University Press, USA.

Clark, G .L., Lai, K .P. and Wójcik, D., 2015. Editorial introduction to the special section:

Deconstructing offshore finance.

9

Books and Journals:

Vaubourg, A. G., 2016. Finance and international trade: A review of the literature. Revue

d'économie politique. 126(1). pp.57-87.

Steckel, J. C. and et. al., 2017. From climate finance toward sustainable development

finance. Wiley Interdisciplinary Reviews: Climate Change. 8(1). p.e437.

Sassen, S., 2017. Finance and business services in New York City: international linkages and

domestic effects. In Deindustrialization and Regional Economic Transformation(pp.

132-290). Routledge.

Ntuli, M. G., 2017. An evaluation of bank acquisition using an accounting based measure: a case

of Amalgamated Bank of South Africa and Barclays Bank Plc. Banks and Bank Systems.

12(1). p.160.

Khan, M. M., 2015. Sources of finance available for SME sector in Pakistan. International

Letters of Social and Humanistic Sciences. 47. pp.184-194.

Fernández, X. L., Paz-Saavedra, D. and Coto-Millán, P., 2019. THE IMPACT OF BREXIT ON

BANK EFFICIENCY: EVIDENCE FROM UK AND IRELAND. Finance Research

Letters. p.101338.

Desierto, D .A., 2015. Public policy in international economic law: the ICESCR in trade,

finance, and investment. Oxford University Press, USA.

Clark, G .L., Lai, K .P. and Wójcik, D., 2015. Editorial introduction to the special section:

Deconstructing offshore finance.

9

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2025 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.