Financial Management ACCT 702: Capital Budgeting & Lease Analysis

VerifiedAdded on 2023/06/12

|12

|2724

|132

Project

AI Summary

This project provides a comprehensive financial analysis of a machine purchase decision for two cupcake companies, Fluffy Cupcake Company (FCC) and Brownie Cake Company (BCC), under different financial scenarios. It begins by calculating the Free Cash Flow for the Firm (FCFF) and Net Present Value (NPV) to assess the financial viability of the purchase for both companies, considering scenarios with 100% equity and a mix of equity and debt. A sensitivity analysis is then performed to evaluate the impact of changes in key variables on the NPV. Finally, the project compares the purchase option with a lease alternative, determining the most financially beneficial option for both companies based on present value calculations. The analysis incorporates factors such as incremental cash revenues, operating expenses, depreciation, tax implications, and cost of capital to provide a thorough evaluation of the investment decision. Desklib offers this and many more solved assignments for students.

FINACIAL MANAGEMENT COURSE – ACCT 702_001 W 18

Name of the student

Name of the University

Name of the student

Name of the University

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Author Note

Table of Contents

Part A: Financial Viability for Fluffy Cupcake Company (FCC)......................................................................................................................................................................4

Part B: Financial Viability for Brownie Cake Company (BCC)........................................................................................................................................................................ 5

Part C: Sensitivity Analysis........................................................................................................................................................................................................................... 6

Part D: Purchase vs Lease Analysis............................................................................................................................................................................................................... 9

Bibliography............................................................................................................................................................................................................................................... 11

Part A: Financial Viability for Fluffy Cupcake Company (FCC)......................................................................................................................................................................4

Part B: Financial Viability for Brownie Cake Company (BCC)........................................................................................................................................................................ 5

Part C: Sensitivity Analysis........................................................................................................................................................................................................................... 6

Part D: Purchase vs Lease Analysis............................................................................................................................................................................................................... 9

Bibliography............................................................................................................................................................................................................................................... 11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

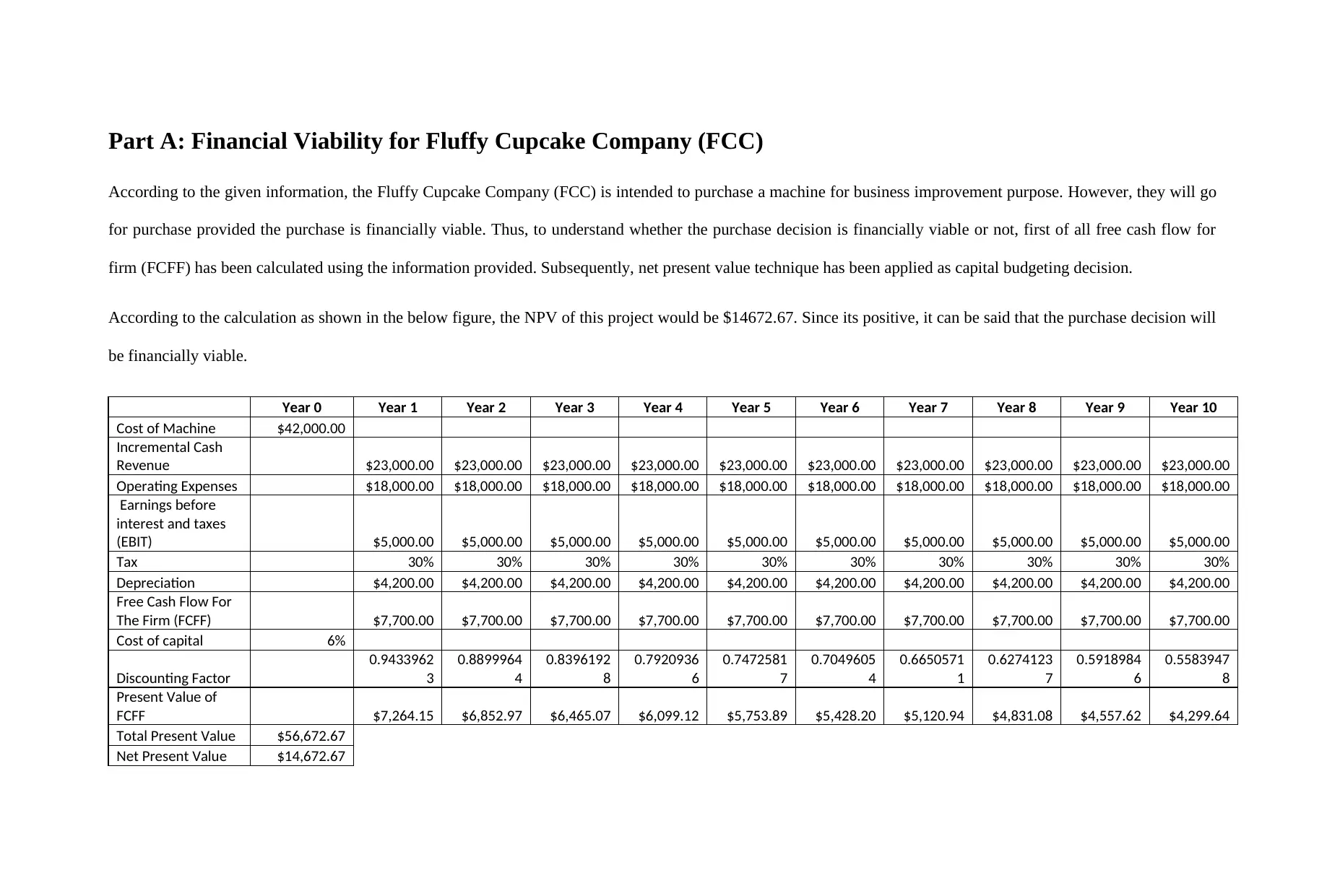

Part A: Financial Viability for Fluffy Cupcake Company (FCC)

According to the given information, the Fluffy Cupcake Company (FCC) is intended to purchase a machine for business improvement purpose. However, they will go

for purchase provided the purchase is financially viable. Thus, to understand whether the purchase decision is financially viable or not, first of all free cash flow for

firm (FCFF) has been calculated using the information provided. Subsequently, net present value technique has been applied as capital budgeting decision.

According to the calculation as shown in the below figure, the NPV of this project would be $14672.67. Since its positive, it can be said that the purchase decision will

be financially viable.

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Cost of Machine $42,000.00

Incremental Cash

Revenue $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00

Operating Expenses $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00

Earnings before

interest and taxes

(EBIT) $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00

Tax 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Depreciation $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00

Free Cash Flow For

The Firm (FCFF) $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00

Cost of capital 6%

Discounting Factor

0.9433962

3

0.8899964

4

0.8396192

8

0.7920936

6

0.7472581

7

0.7049605

4

0.6650571

1

0.6274123

7

0.5918984

6

0.5583947

8

Present Value of

FCFF $7,264.15 $6,852.97 $6,465.07 $6,099.12 $5,753.89 $5,428.20 $5,120.94 $4,831.08 $4,557.62 $4,299.64

Total Present Value $56,672.67

Net Present Value $14,672.67

According to the given information, the Fluffy Cupcake Company (FCC) is intended to purchase a machine for business improvement purpose. However, they will go

for purchase provided the purchase is financially viable. Thus, to understand whether the purchase decision is financially viable or not, first of all free cash flow for

firm (FCFF) has been calculated using the information provided. Subsequently, net present value technique has been applied as capital budgeting decision.

According to the calculation as shown in the below figure, the NPV of this project would be $14672.67. Since its positive, it can be said that the purchase decision will

be financially viable.

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Cost of Machine $42,000.00

Incremental Cash

Revenue $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00 $23,000.00

Operating Expenses $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00 $18,000.00

Earnings before

interest and taxes

(EBIT) $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00 $5,000.00

Tax 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Depreciation $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00

Free Cash Flow For

The Firm (FCFF) $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00 $7,700.00

Cost of capital 6%

Discounting Factor

0.9433962

3

0.8899964

4

0.8396192

8

0.7920936

6

0.7472581

7

0.7049605

4

0.6650571

1

0.6274123

7

0.5918984

6

0.5583947

8

Present Value of

FCFF $7,264.15 $6,852.97 $6,465.07 $6,099.12 $5,753.89 $5,428.20 $5,120.94 $4,831.08 $4,557.62 $4,299.64

Total Present Value $56,672.67

Net Present Value $14,672.67

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

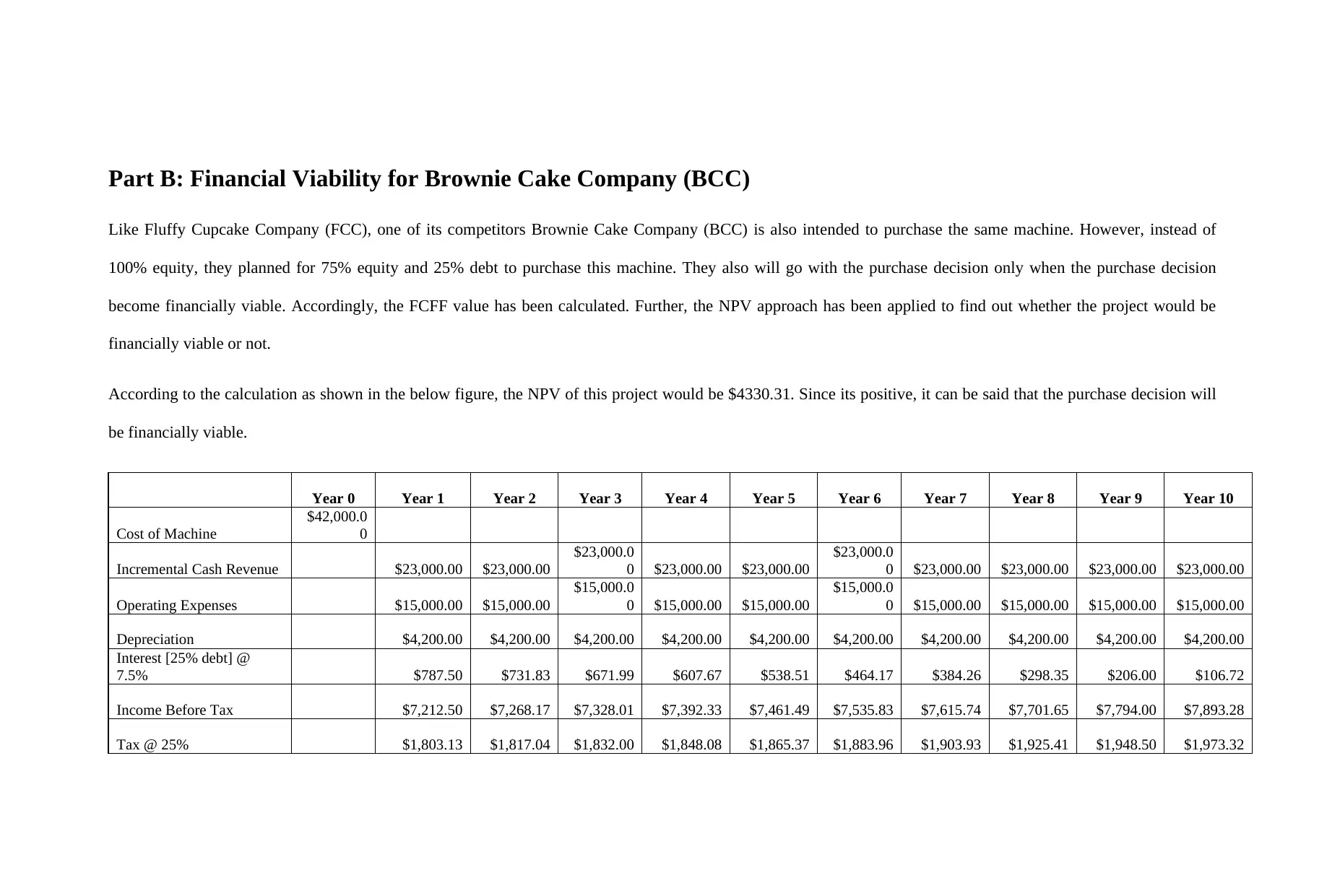

Part B: Financial Viability for Brownie Cake Company (BCC)

Like Fluffy Cupcake Company (FCC), one of its competitors Brownie Cake Company (BCC) is also intended to purchase the same machine. However, instead of

100% equity, they planned for 75% equity and 25% debt to purchase this machine. They also will go with the purchase decision only when the purchase decision

become financially viable. Accordingly, the FCFF value has been calculated. Further, the NPV approach has been applied to find out whether the project would be

financially viable or not.

According to the calculation as shown in the below figure, the NPV of this project would be $4330.31. Since its positive, it can be said that the purchase decision will

be financially viable.

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Cost of Machine

$42,000.0

0

Incremental Cash Revenue $23,000.00 $23,000.00

$23,000.0

0 $23,000.00 $23,000.00

$23,000.0

0 $23,000.00 $23,000.00 $23,000.00 $23,000.00

Operating Expenses $15,000.00 $15,000.00

$15,000.0

0 $15,000.00 $15,000.00

$15,000.0

0 $15,000.00 $15,000.00 $15,000.00 $15,000.00

Depreciation $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00

Interest [25% debt] @

7.5% $787.50 $731.83 $671.99 $607.67 $538.51 $464.17 $384.26 $298.35 $206.00 $106.72

Income Before Tax $7,212.50 $7,268.17 $7,328.01 $7,392.33 $7,461.49 $7,535.83 $7,615.74 $7,701.65 $7,794.00 $7,893.28

Tax @ 25% $1,803.13 $1,817.04 $1,832.00 $1,848.08 $1,865.37 $1,883.96 $1,903.93 $1,925.41 $1,948.50 $1,973.32

Like Fluffy Cupcake Company (FCC), one of its competitors Brownie Cake Company (BCC) is also intended to purchase the same machine. However, instead of

100% equity, they planned for 75% equity and 25% debt to purchase this machine. They also will go with the purchase decision only when the purchase decision

become financially viable. Accordingly, the FCFF value has been calculated. Further, the NPV approach has been applied to find out whether the project would be

financially viable or not.

According to the calculation as shown in the below figure, the NPV of this project would be $4330.31. Since its positive, it can be said that the purchase decision will

be financially viable.

Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Cost of Machine

$42,000.0

0

Incremental Cash Revenue $23,000.00 $23,000.00

$23,000.0

0 $23,000.00 $23,000.00

$23,000.0

0 $23,000.00 $23,000.00 $23,000.00 $23,000.00

Operating Expenses $15,000.00 $15,000.00

$15,000.0

0 $15,000.00 $15,000.00

$15,000.0

0 $15,000.00 $15,000.00 $15,000.00 $15,000.00

Depreciation $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00

Interest [25% debt] @

7.5% $787.50 $731.83 $671.99 $607.67 $538.51 $464.17 $384.26 $298.35 $206.00 $106.72

Income Before Tax $7,212.50 $7,268.17 $7,328.01 $7,392.33 $7,461.49 $7,535.83 $7,615.74 $7,701.65 $7,794.00 $7,893.28

Tax @ 25% $1,803.13 $1,817.04 $1,832.00 $1,848.08 $1,865.37 $1,883.96 $1,903.93 $1,925.41 $1,948.50 $1,973.32

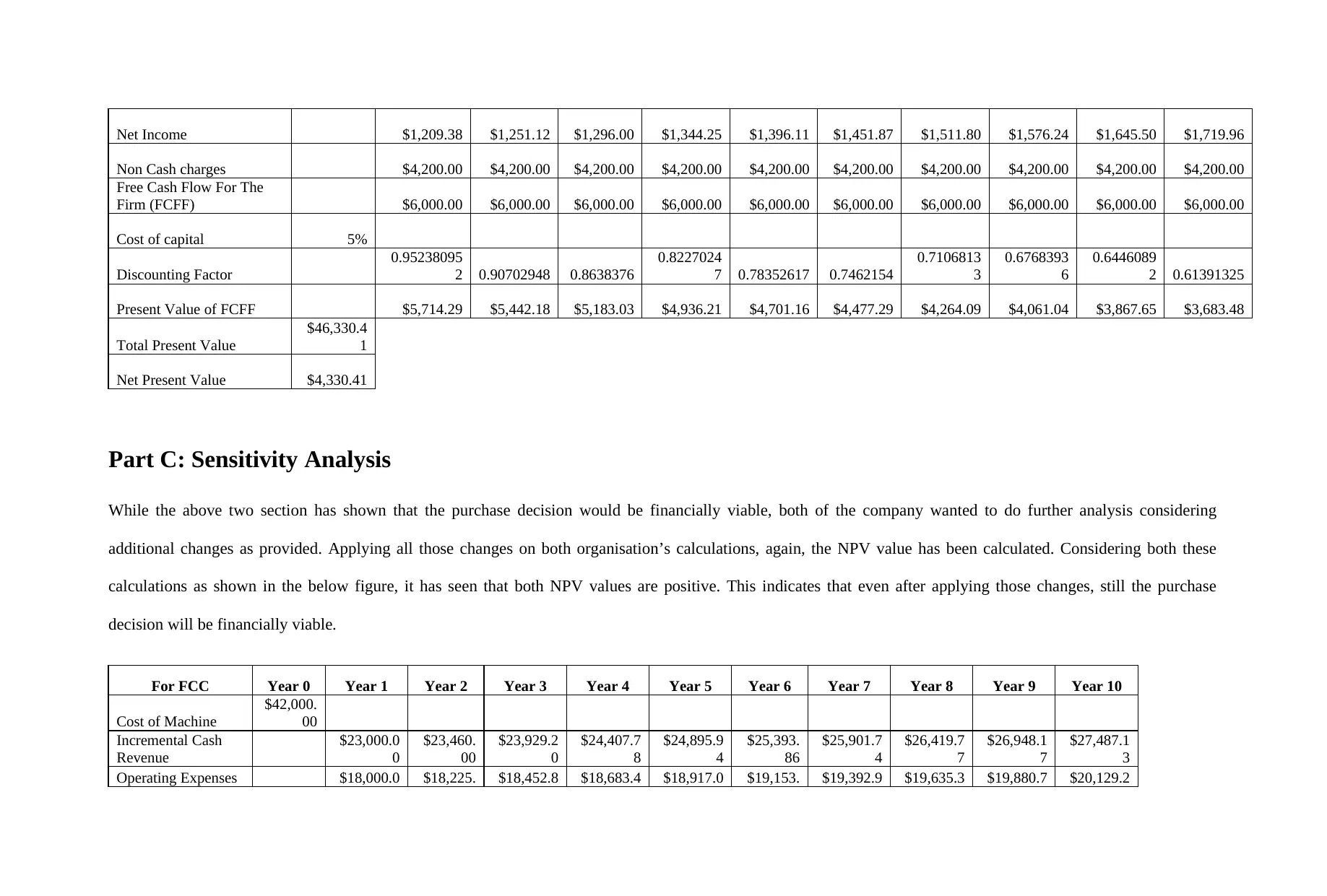

Net Income $1,209.38 $1,251.12 $1,296.00 $1,344.25 $1,396.11 $1,451.87 $1,511.80 $1,576.24 $1,645.50 $1,719.96

Non Cash charges $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00

Free Cash Flow For The

Firm (FCFF) $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00

Cost of capital 5%

Discounting Factor

0.95238095

2 0.90702948 0.8638376

0.8227024

7 0.78352617 0.7462154

0.7106813

3

0.6768393

6

0.6446089

2 0.61391325

Present Value of FCFF $5,714.29 $5,442.18 $5,183.03 $4,936.21 $4,701.16 $4,477.29 $4,264.09 $4,061.04 $3,867.65 $3,683.48

Total Present Value

$46,330.4

1

Net Present Value $4,330.41

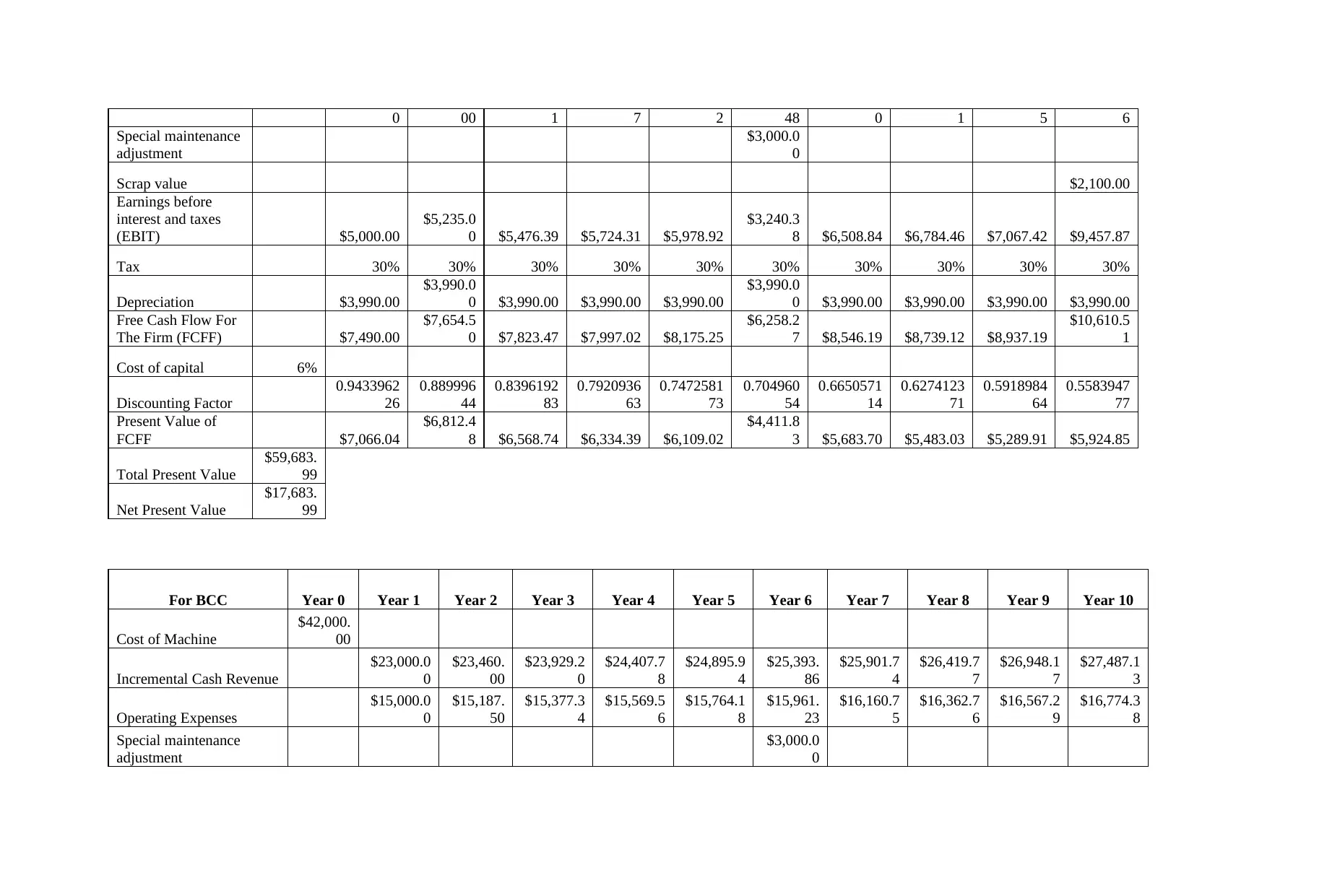

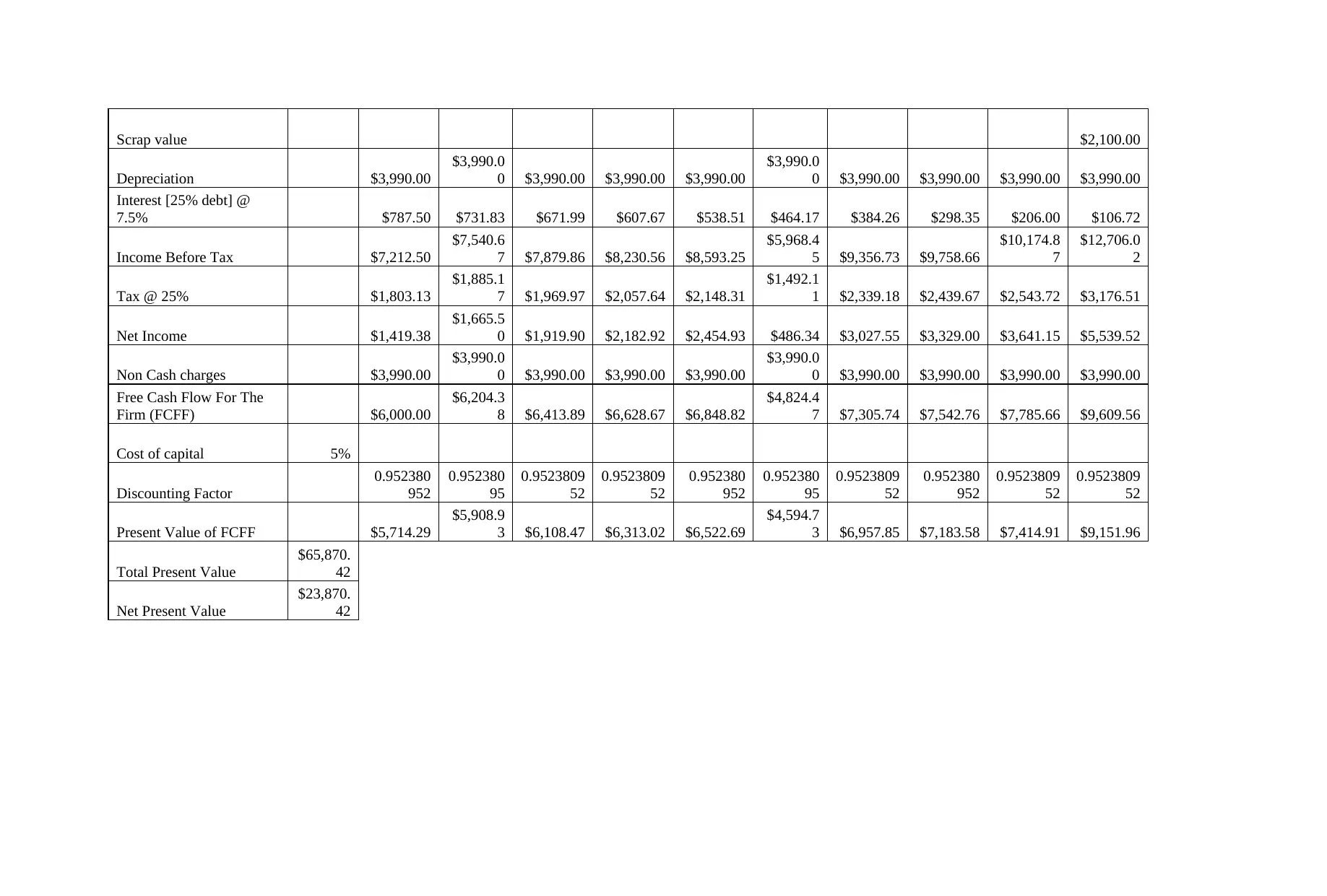

Part C: Sensitivity Analysis

While the above two section has shown that the purchase decision would be financially viable, both of the company wanted to do further analysis considering

additional changes as provided. Applying all those changes on both organisation’s calculations, again, the NPV value has been calculated. Considering both these

calculations as shown in the below figure, it has seen that both NPV values are positive. This indicates that even after applying those changes, still the purchase

decision will be financially viable.

For FCC Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Cost of Machine

$42,000.

00

Incremental Cash

Revenue

$23,000.0

0

$23,460.

00

$23,929.2

0

$24,407.7

8

$24,895.9

4

$25,393.

86

$25,901.7

4

$26,419.7

7

$26,948.1

7

$27,487.1

3

Operating Expenses $18,000.0 $18,225. $18,452.8 $18,683.4 $18,917.0 $19,153. $19,392.9 $19,635.3 $19,880.7 $20,129.2

Non Cash charges $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00 $4,200.00

Free Cash Flow For The

Firm (FCFF) $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00 $6,000.00

Cost of capital 5%

Discounting Factor

0.95238095

2 0.90702948 0.8638376

0.8227024

7 0.78352617 0.7462154

0.7106813

3

0.6768393

6

0.6446089

2 0.61391325

Present Value of FCFF $5,714.29 $5,442.18 $5,183.03 $4,936.21 $4,701.16 $4,477.29 $4,264.09 $4,061.04 $3,867.65 $3,683.48

Total Present Value

$46,330.4

1

Net Present Value $4,330.41

Part C: Sensitivity Analysis

While the above two section has shown that the purchase decision would be financially viable, both of the company wanted to do further analysis considering

additional changes as provided. Applying all those changes on both organisation’s calculations, again, the NPV value has been calculated. Considering both these

calculations as shown in the below figure, it has seen that both NPV values are positive. This indicates that even after applying those changes, still the purchase

decision will be financially viable.

For FCC Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Cost of Machine

$42,000.

00

Incremental Cash

Revenue

$23,000.0

0

$23,460.

00

$23,929.2

0

$24,407.7

8

$24,895.9

4

$25,393.

86

$25,901.7

4

$26,419.7

7

$26,948.1

7

$27,487.1

3

Operating Expenses $18,000.0 $18,225. $18,452.8 $18,683.4 $18,917.0 $19,153. $19,392.9 $19,635.3 $19,880.7 $20,129.2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

0 00 1 7 2 48 0 1 5 6

Special maintenance

adjustment

$3,000.0

0

Scrap value $2,100.00

Earnings before

interest and taxes

(EBIT) $5,000.00

$5,235.0

0 $5,476.39 $5,724.31 $5,978.92

$3,240.3

8 $6,508.84 $6,784.46 $7,067.42 $9,457.87

Tax 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Depreciation $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00 $3,990.00

Free Cash Flow For

The Firm (FCFF) $7,490.00

$7,654.5

0 $7,823.47 $7,997.02 $8,175.25

$6,258.2

7 $8,546.19 $8,739.12 $8,937.19

$10,610.5

1

Cost of capital 6%

Discounting Factor

0.9433962

26

0.889996

44

0.8396192

83

0.7920936

63

0.7472581

73

0.704960

54

0.6650571

14

0.6274123

71

0.5918984

64

0.5583947

77

Present Value of

FCFF $7,066.04

$6,812.4

8 $6,568.74 $6,334.39 $6,109.02

$4,411.8

3 $5,683.70 $5,483.03 $5,289.91 $5,924.85

Total Present Value

$59,683.

99

Net Present Value

$17,683.

99

For BCC Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Cost of Machine

$42,000.

00

Incremental Cash Revenue

$23,000.0

0

$23,460.

00

$23,929.2

0

$24,407.7

8

$24,895.9

4

$25,393.

86

$25,901.7

4

$26,419.7

7

$26,948.1

7

$27,487.1

3

Operating Expenses

$15,000.0

0

$15,187.

50

$15,377.3

4

$15,569.5

6

$15,764.1

8

$15,961.

23

$16,160.7

5

$16,362.7

6

$16,567.2

9

$16,774.3

8

Special maintenance

adjustment

$3,000.0

0

Special maintenance

adjustment

$3,000.0

0

Scrap value $2,100.00

Earnings before

interest and taxes

(EBIT) $5,000.00

$5,235.0

0 $5,476.39 $5,724.31 $5,978.92

$3,240.3

8 $6,508.84 $6,784.46 $7,067.42 $9,457.87

Tax 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Depreciation $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00 $3,990.00

Free Cash Flow For

The Firm (FCFF) $7,490.00

$7,654.5

0 $7,823.47 $7,997.02 $8,175.25

$6,258.2

7 $8,546.19 $8,739.12 $8,937.19

$10,610.5

1

Cost of capital 6%

Discounting Factor

0.9433962

26

0.889996

44

0.8396192

83

0.7920936

63

0.7472581

73

0.704960

54

0.6650571

14

0.6274123

71

0.5918984

64

0.5583947

77

Present Value of

FCFF $7,066.04

$6,812.4

8 $6,568.74 $6,334.39 $6,109.02

$4,411.8

3 $5,683.70 $5,483.03 $5,289.91 $5,924.85

Total Present Value

$59,683.

99

Net Present Value

$17,683.

99

For BCC Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Cost of Machine

$42,000.

00

Incremental Cash Revenue

$23,000.0

0

$23,460.

00

$23,929.2

0

$24,407.7

8

$24,895.9

4

$25,393.

86

$25,901.7

4

$26,419.7

7

$26,948.1

7

$27,487.1

3

Operating Expenses

$15,000.0

0

$15,187.

50

$15,377.3

4

$15,569.5

6

$15,764.1

8

$15,961.

23

$16,160.7

5

$16,362.7

6

$16,567.2

9

$16,774.3

8

Special maintenance

adjustment

$3,000.0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Scrap value $2,100.00

Depreciation $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00 $3,990.00

Interest [25% debt] @

7.5% $787.50 $731.83 $671.99 $607.67 $538.51 $464.17 $384.26 $298.35 $206.00 $106.72

Income Before Tax $7,212.50

$7,540.6

7 $7,879.86 $8,230.56 $8,593.25

$5,968.4

5 $9,356.73 $9,758.66

$10,174.8

7

$12,706.0

2

Tax @ 25% $1,803.13

$1,885.1

7 $1,969.97 $2,057.64 $2,148.31

$1,492.1

1 $2,339.18 $2,439.67 $2,543.72 $3,176.51

Net Income $1,419.38

$1,665.5

0 $1,919.90 $2,182.92 $2,454.93 $486.34 $3,027.55 $3,329.00 $3,641.15 $5,539.52

Non Cash charges $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00 $3,990.00

Free Cash Flow For The

Firm (FCFF) $6,000.00

$6,204.3

8 $6,413.89 $6,628.67 $6,848.82

$4,824.4

7 $7,305.74 $7,542.76 $7,785.66 $9,609.56

Cost of capital 5%

Discounting Factor

0.952380

952

0.952380

95

0.9523809

52

0.9523809

52

0.952380

952

0.952380

95

0.9523809

52

0.952380

952

0.9523809

52

0.9523809

52

Present Value of FCFF $5,714.29

$5,908.9

3 $6,108.47 $6,313.02 $6,522.69

$4,594.7

3 $6,957.85 $7,183.58 $7,414.91 $9,151.96

Total Present Value

$65,870.

42

Net Present Value

$23,870.

42

Depreciation $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00 $3,990.00

Interest [25% debt] @

7.5% $787.50 $731.83 $671.99 $607.67 $538.51 $464.17 $384.26 $298.35 $206.00 $106.72

Income Before Tax $7,212.50

$7,540.6

7 $7,879.86 $8,230.56 $8,593.25

$5,968.4

5 $9,356.73 $9,758.66

$10,174.8

7

$12,706.0

2

Tax @ 25% $1,803.13

$1,885.1

7 $1,969.97 $2,057.64 $2,148.31

$1,492.1

1 $2,339.18 $2,439.67 $2,543.72 $3,176.51

Net Income $1,419.38

$1,665.5

0 $1,919.90 $2,182.92 $2,454.93 $486.34 $3,027.55 $3,329.00 $3,641.15 $5,539.52

Non Cash charges $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00

$3,990.0

0 $3,990.00 $3,990.00 $3,990.00 $3,990.00

Free Cash Flow For The

Firm (FCFF) $6,000.00

$6,204.3

8 $6,413.89 $6,628.67 $6,848.82

$4,824.4

7 $7,305.74 $7,542.76 $7,785.66 $9,609.56

Cost of capital 5%

Discounting Factor

0.952380

952

0.952380

95

0.9523809

52

0.9523809

52

0.952380

952

0.952380

95

0.9523809

52

0.952380

952

0.9523809

52

0.9523809

52

Present Value of FCFF $5,714.29

$5,908.9

3 $6,108.47 $6,313.02 $6,522.69

$4,594.7

3 $6,957.85 $7,183.58 $7,414.91 $9,151.96

Total Present Value

$65,870.

42

Net Present Value

$23,870.

42

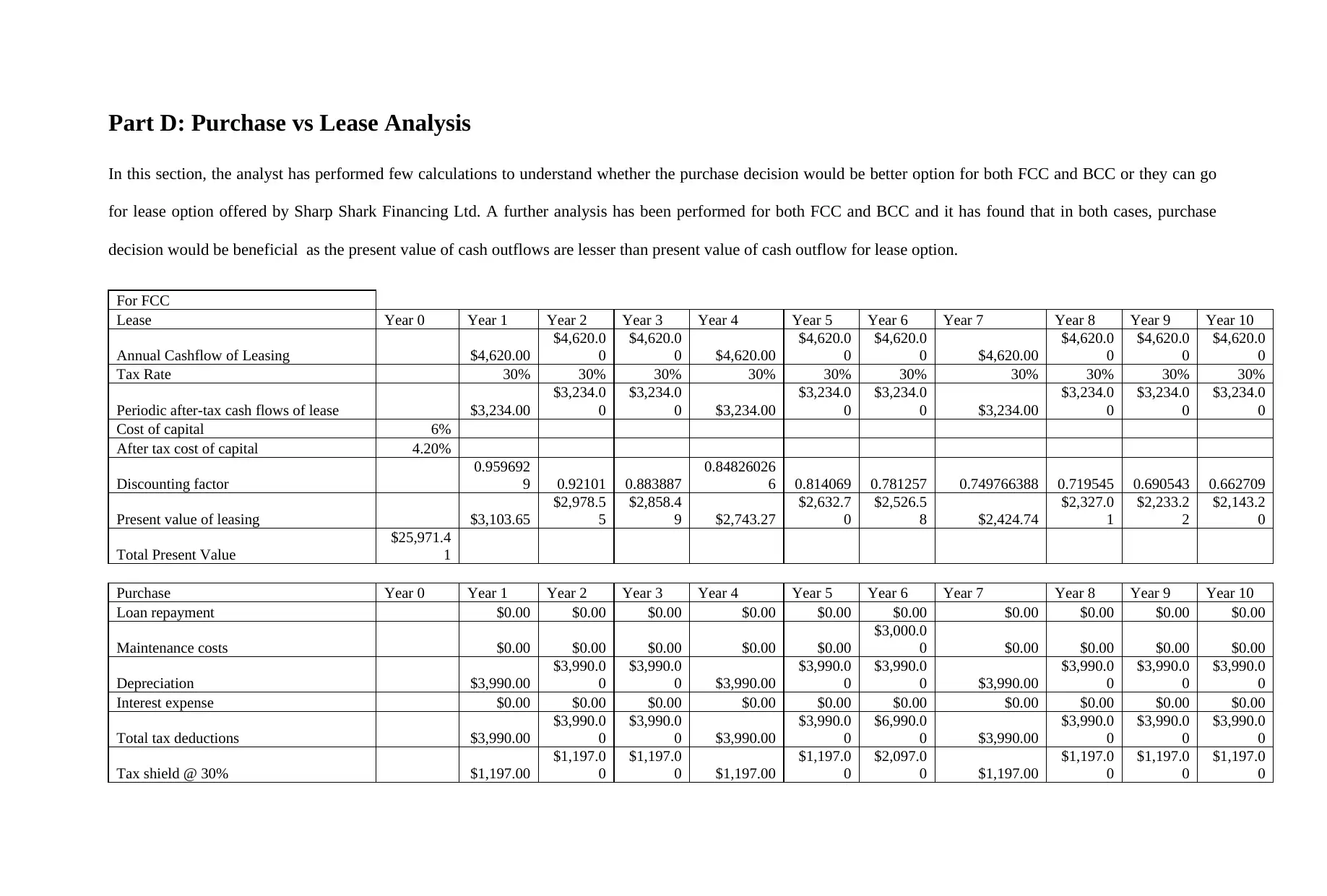

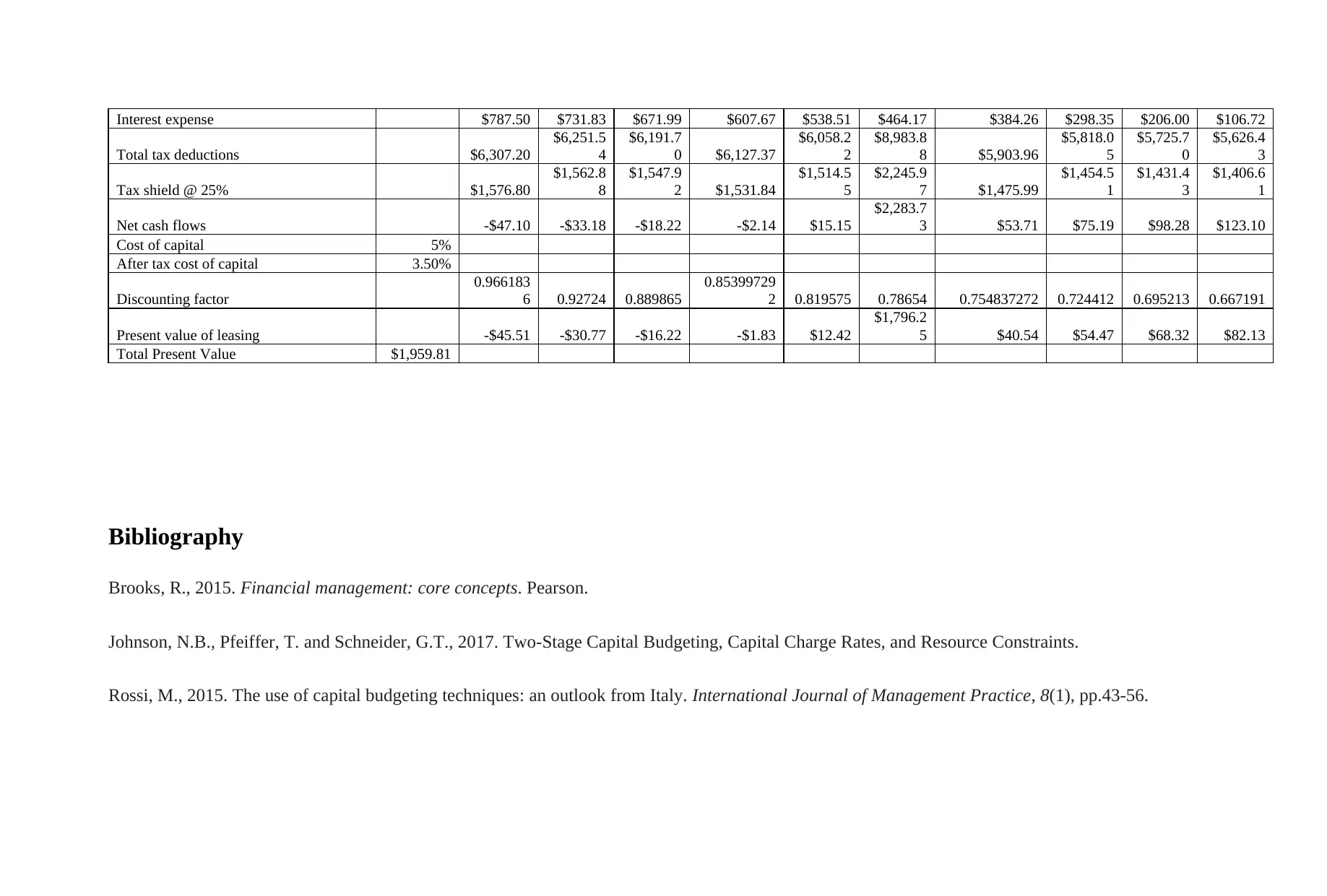

Part D: Purchase vs Lease Analysis

In this section, the analyst has performed few calculations to understand whether the purchase decision would be better option for both FCC and BCC or they can go

for lease option offered by Sharp Shark Financing Ltd. A further analysis has been performed for both FCC and BCC and it has found that in both cases, purchase

decision would be beneficial as the present value of cash outflows are lesser than present value of cash outflow for lease option.

For FCC

Lease Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Annual Cashflow of Leasing $4,620.00

$4,620.0

0

$4,620.0

0 $4,620.00

$4,620.0

0

$4,620.0

0 $4,620.00

$4,620.0

0

$4,620.0

0

$4,620.0

0

Tax Rate 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Periodic after-tax cash flows of lease $3,234.00

$3,234.0

0

$3,234.0

0 $3,234.00

$3,234.0

0

$3,234.0

0 $3,234.00

$3,234.0

0

$3,234.0

0

$3,234.0

0

Cost of capital 6%

After tax cost of capital 4.20%

Discounting factor

0.959692

9 0.92101 0.883887

0.84826026

6 0.814069 0.781257 0.749766388 0.719545 0.690543 0.662709

Present value of leasing $3,103.65

$2,978.5

5

$2,858.4

9 $2,743.27

$2,632.7

0

$2,526.5

8 $2,424.74

$2,327.0

1

$2,233.2

2

$2,143.2

0

Total Present Value

$25,971.4

1

Purchase Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Loan repayment $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00

Maintenance costs $0.00 $0.00 $0.00 $0.00 $0.00

$3,000.0

0 $0.00 $0.00 $0.00 $0.00

Depreciation $3,990.00

$3,990.0

0

$3,990.0

0 $3,990.00

$3,990.0

0

$3,990.0

0 $3,990.00

$3,990.0

0

$3,990.0

0

$3,990.0

0

Interest expense $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00

Total tax deductions $3,990.00

$3,990.0

0

$3,990.0

0 $3,990.00

$3,990.0

0

$6,990.0

0 $3,990.00

$3,990.0

0

$3,990.0

0

$3,990.0

0

Tax shield @ 30% $1,197.00

$1,197.0

0

$1,197.0

0 $1,197.00

$1,197.0

0

$2,097.0

0 $1,197.00

$1,197.0

0

$1,197.0

0

$1,197.0

0

In this section, the analyst has performed few calculations to understand whether the purchase decision would be better option for both FCC and BCC or they can go

for lease option offered by Sharp Shark Financing Ltd. A further analysis has been performed for both FCC and BCC and it has found that in both cases, purchase

decision would be beneficial as the present value of cash outflows are lesser than present value of cash outflow for lease option.

For FCC

Lease Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Annual Cashflow of Leasing $4,620.00

$4,620.0

0

$4,620.0

0 $4,620.00

$4,620.0

0

$4,620.0

0 $4,620.00

$4,620.0

0

$4,620.0

0

$4,620.0

0

Tax Rate 30% 30% 30% 30% 30% 30% 30% 30% 30% 30%

Periodic after-tax cash flows of lease $3,234.00

$3,234.0

0

$3,234.0

0 $3,234.00

$3,234.0

0

$3,234.0

0 $3,234.00

$3,234.0

0

$3,234.0

0

$3,234.0

0

Cost of capital 6%

After tax cost of capital 4.20%

Discounting factor

0.959692

9 0.92101 0.883887

0.84826026

6 0.814069 0.781257 0.749766388 0.719545 0.690543 0.662709

Present value of leasing $3,103.65

$2,978.5

5

$2,858.4

9 $2,743.27

$2,632.7

0

$2,526.5

8 $2,424.74

$2,327.0

1

$2,233.2

2

$2,143.2

0

Total Present Value

$25,971.4

1

Purchase Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Loan repayment $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00

Maintenance costs $0.00 $0.00 $0.00 $0.00 $0.00

$3,000.0

0 $0.00 $0.00 $0.00 $0.00

Depreciation $3,990.00

$3,990.0

0

$3,990.0

0 $3,990.00

$3,990.0

0

$3,990.0

0 $3,990.00

$3,990.0

0

$3,990.0

0

$3,990.0

0

Interest expense $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00 $0.00

Total tax deductions $3,990.00

$3,990.0

0

$3,990.0

0 $3,990.00

$3,990.0

0

$6,990.0

0 $3,990.00

$3,990.0

0

$3,990.0

0

$3,990.0

0

Tax shield @ 30% $1,197.00

$1,197.0

0

$1,197.0

0 $1,197.00

$1,197.0

0

$2,097.0

0 $1,197.00

$1,197.0

0

$1,197.0

0

$1,197.0

0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net cash flows

-

$1,197.00

-

$1,197.0

0

-

$1,197.0

0 -$1,197.00

-

$1,197.0

0 $903.00 -$1,197.00

-

$1,197.0

0

-

$1,197.0

0

-

$1,197.0

0

Cost of capital 6%

After tax cost of capital 4.20%

Discounting factor

0.959692

9 0.92101 0.883887

0.84826026

6 0.814069 0.781257 0.749766388 0.719545 0.690543 0.662709

Present value of leasing

-

$1,148.75

-

$1,102.4

5

-

$1,058.0

1 -$1,015.37 -$974.44 $705.47 -$897.47 -$861.30 -$826.58 -$793.26

Total Present Value -$7,972.16

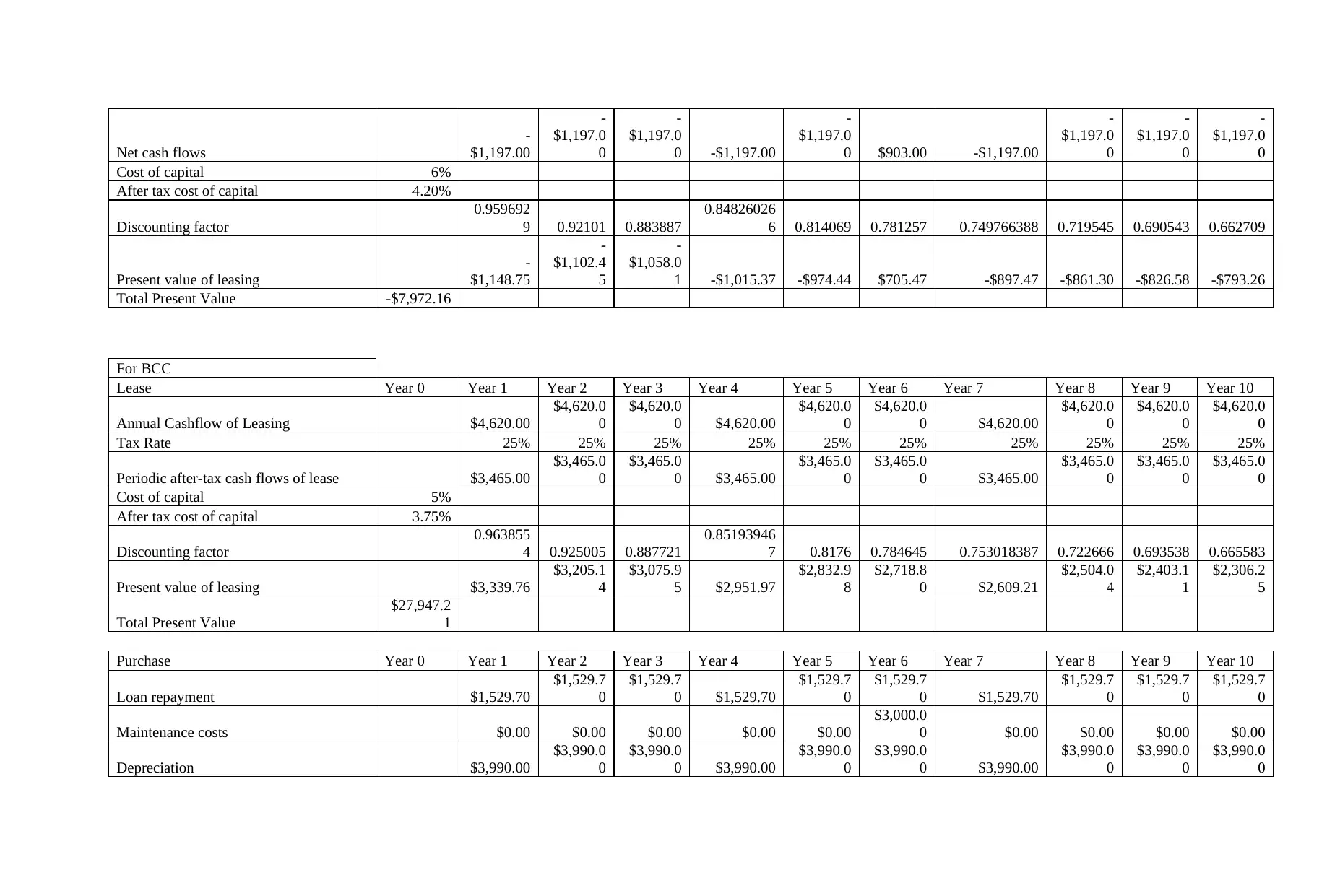

For BCC

Lease Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Annual Cashflow of Leasing $4,620.00

$4,620.0

0

$4,620.0

0 $4,620.00

$4,620.0

0

$4,620.0

0 $4,620.00

$4,620.0

0

$4,620.0

0

$4,620.0

0

Tax Rate 25% 25% 25% 25% 25% 25% 25% 25% 25% 25%

Periodic after-tax cash flows of lease $3,465.00

$3,465.0

0

$3,465.0

0 $3,465.00

$3,465.0

0

$3,465.0

0 $3,465.00

$3,465.0

0

$3,465.0

0

$3,465.0

0

Cost of capital 5%

After tax cost of capital 3.75%

Discounting factor

0.963855

4 0.925005 0.887721

0.85193946

7 0.8176 0.784645 0.753018387 0.722666 0.693538 0.665583

Present value of leasing $3,339.76

$3,205.1

4

$3,075.9

5 $2,951.97

$2,832.9

8

$2,718.8

0 $2,609.21

$2,504.0

4

$2,403.1

1

$2,306.2

5

Total Present Value

$27,947.2

1

Purchase Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Loan repayment $1,529.70

$1,529.7

0

$1,529.7

0 $1,529.70

$1,529.7

0

$1,529.7

0 $1,529.70

$1,529.7

0

$1,529.7

0

$1,529.7

0

Maintenance costs $0.00 $0.00 $0.00 $0.00 $0.00

$3,000.0

0 $0.00 $0.00 $0.00 $0.00

Depreciation $3,990.00

$3,990.0

0

$3,990.0

0 $3,990.00

$3,990.0

0

$3,990.0

0 $3,990.00

$3,990.0

0

$3,990.0

0

$3,990.0

0

-

$1,197.00

-

$1,197.0

0

-

$1,197.0

0 -$1,197.00

-

$1,197.0

0 $903.00 -$1,197.00

-

$1,197.0

0

-

$1,197.0

0

-

$1,197.0

0

Cost of capital 6%

After tax cost of capital 4.20%

Discounting factor

0.959692

9 0.92101 0.883887

0.84826026

6 0.814069 0.781257 0.749766388 0.719545 0.690543 0.662709

Present value of leasing

-

$1,148.75

-

$1,102.4

5

-

$1,058.0

1 -$1,015.37 -$974.44 $705.47 -$897.47 -$861.30 -$826.58 -$793.26

Total Present Value -$7,972.16

For BCC

Lease Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Annual Cashflow of Leasing $4,620.00

$4,620.0

0

$4,620.0

0 $4,620.00

$4,620.0

0

$4,620.0

0 $4,620.00

$4,620.0

0

$4,620.0

0

$4,620.0

0

Tax Rate 25% 25% 25% 25% 25% 25% 25% 25% 25% 25%

Periodic after-tax cash flows of lease $3,465.00

$3,465.0

0

$3,465.0

0 $3,465.00

$3,465.0

0

$3,465.0

0 $3,465.00

$3,465.0

0

$3,465.0

0

$3,465.0

0

Cost of capital 5%

After tax cost of capital 3.75%

Discounting factor

0.963855

4 0.925005 0.887721

0.85193946

7 0.8176 0.784645 0.753018387 0.722666 0.693538 0.665583

Present value of leasing $3,339.76

$3,205.1

4

$3,075.9

5 $2,951.97

$2,832.9

8

$2,718.8

0 $2,609.21

$2,504.0

4

$2,403.1

1

$2,306.2

5

Total Present Value

$27,947.2

1

Purchase Year 0 Year 1 Year 2 Year 3 Year 4 Year 5 Year 6 Year 7 Year 8 Year 9 Year 10

Loan repayment $1,529.70

$1,529.7

0

$1,529.7

0 $1,529.70

$1,529.7

0

$1,529.7

0 $1,529.70

$1,529.7

0

$1,529.7

0

$1,529.7

0

Maintenance costs $0.00 $0.00 $0.00 $0.00 $0.00

$3,000.0

0 $0.00 $0.00 $0.00 $0.00

Depreciation $3,990.00

$3,990.0

0

$3,990.0

0 $3,990.00

$3,990.0

0

$3,990.0

0 $3,990.00

$3,990.0

0

$3,990.0

0

$3,990.0

0

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interest expense $787.50 $731.83 $671.99 $607.67 $538.51 $464.17 $384.26 $298.35 $206.00 $106.72

Total tax deductions $6,307.20

$6,251.5

4

$6,191.7

0 $6,127.37

$6,058.2

2

$8,983.8

8 $5,903.96

$5,818.0

5

$5,725.7

0

$5,626.4

3

Tax shield @ 25% $1,576.80

$1,562.8

8

$1,547.9

2 $1,531.84

$1,514.5

5

$2,245.9

7 $1,475.99

$1,454.5

1

$1,431.4

3

$1,406.6

1

Net cash flows -$47.10 -$33.18 -$18.22 -$2.14 $15.15

$2,283.7

3 $53.71 $75.19 $98.28 $123.10

Cost of capital 5%

After tax cost of capital 3.50%

Discounting factor

0.966183

6 0.92724 0.889865

0.85399729

2 0.819575 0.78654 0.754837272 0.724412 0.695213 0.667191

Present value of leasing -$45.51 -$30.77 -$16.22 -$1.83 $12.42

$1,796.2

5 $40.54 $54.47 $68.32 $82.13

Total Present Value $1,959.81

Bibliography

Brooks, R., 2015. Financial management: core concepts. Pearson.

Johnson, N.B., Pfeiffer, T. and Schneider, G.T., 2017. Two-Stage Capital Budgeting, Capital Charge Rates, and Resource Constraints.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from Italy. International Journal of Management Practice, 8(1), pp.43-56.

Total tax deductions $6,307.20

$6,251.5

4

$6,191.7

0 $6,127.37

$6,058.2

2

$8,983.8

8 $5,903.96

$5,818.0

5

$5,725.7

0

$5,626.4

3

Tax shield @ 25% $1,576.80

$1,562.8

8

$1,547.9

2 $1,531.84

$1,514.5

5

$2,245.9

7 $1,475.99

$1,454.5

1

$1,431.4

3

$1,406.6

1

Net cash flows -$47.10 -$33.18 -$18.22 -$2.14 $15.15

$2,283.7

3 $53.71 $75.19 $98.28 $123.10

Cost of capital 5%

After tax cost of capital 3.50%

Discounting factor

0.966183

6 0.92724 0.889865

0.85399729

2 0.819575 0.78654 0.754837272 0.724412 0.695213 0.667191

Present value of leasing -$45.51 -$30.77 -$16.22 -$1.83 $12.42

$1,796.2

5 $40.54 $54.47 $68.32 $82.13

Total Present Value $1,959.81

Bibliography

Brooks, R., 2015. Financial management: core concepts. Pearson.

Johnson, N.B., Pfeiffer, T. and Schneider, G.T., 2017. Two-Stage Capital Budgeting, Capital Charge Rates, and Resource Constraints.

Rossi, M., 2015. The use of capital budgeting techniques: an outlook from Italy. International Journal of Management Practice, 8(1), pp.43-56.

Schlegel, D., Frank, F. and Britzelmaier, B., 2016. Investment decisions and capital budgeting practices in German manufacturing

companies. International Journal of Business and Globalisation, 16(1), pp.66-78.

companies. International Journal of Business and Globalisation, 16(1), pp.66-78.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.