Fraud Risk Assessment in Auditing

VerifiedAdded on 2020/03/01

|9

|2740

|51

AI Summary

This assignment explores the risks of fraud during the auditing process, particularly concerning the potential for management to inflate inventory values to depict higher profits. It examines how these fraudulent practices can influence the auditor's report and potentially lead to misstatements in a company's financial statements. The analysis highlights the auditor's responsibility to identify and mitigate these risks to ensure an accurate representation of the company's financial position.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

AUDIT & ASSURANCE

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit

Answer-1

There are several types of analytical processes that can be applied in order to make both financial

and non-financial decisions of the company. When it comes to the background information of

DIPL Ltd, the same processes can play a key role in ascertaining whether the data forming part

of its financial statements depict a true and fair view of its performance. In other words,

analytical processes can prove to be of immense benefit in identifying any material

misstatements prevalent in the financials of a company (Ghandar & Tsahuridu, 2013). Moreover,

making use of such analytical procedures can assist an auditor to perform the audit process with

more ease and effectiveness. There are many types of analytical processes that can be used in

this regard, and it depends upon an auditor to ascertain which process is more suitable for

performing the audit function.

In the given case of DIPL Ltd, the following analytical processes can be taken into account:

There may be a probability that the figures incorporated in the accounts of creditors and

debtors are not appropriately settled or collected by the officials of the company.

Therefore, it is important to verify the balances of the accounts of debtors and creditors

so that any inaccuracies, which are present, can be mitigated to the fullest. Besides, it

may happen that the company does not have any adequate information associated with

the same. Therefore, if the company is unaware of such a scenario, material misstatement

can incur, thereby affecting the decision-making on the part of auditors.

Another analytical process that can be implemented in the case of DIPL is by making a

comparison of the financial information of present year with that of the previous years.

Besides, such comparison of the current year can also be conducted with the forecasts for

future or with an industry engaged in the similar line of business (Guan et. al, 2008).

With the help of this comparison, the variations in patterns can be taken into account to

make relevant decisions for deciding the future course of action.

The relevance of using trend can be attributed to the fact that the alterations in accounts

can be taken into consideration for making effective decisions. Besides, the reason behind

such alterations can also be known and evaluated respectively. For instance, trend

analysis can be conducted by making a comparison of sales with that of previous years in

order to evaluate the increase or decrease in patterns. Hence, if there is a decrease in

2

Answer-1

There are several types of analytical processes that can be applied in order to make both financial

and non-financial decisions of the company. When it comes to the background information of

DIPL Ltd, the same processes can play a key role in ascertaining whether the data forming part

of its financial statements depict a true and fair view of its performance. In other words,

analytical processes can prove to be of immense benefit in identifying any material

misstatements prevalent in the financials of a company (Ghandar & Tsahuridu, 2013). Moreover,

making use of such analytical procedures can assist an auditor to perform the audit process with

more ease and effectiveness. There are many types of analytical processes that can be used in

this regard, and it depends upon an auditor to ascertain which process is more suitable for

performing the audit function.

In the given case of DIPL Ltd, the following analytical processes can be taken into account:

There may be a probability that the figures incorporated in the accounts of creditors and

debtors are not appropriately settled or collected by the officials of the company.

Therefore, it is important to verify the balances of the accounts of debtors and creditors

so that any inaccuracies, which are present, can be mitigated to the fullest. Besides, it

may happen that the company does not have any adequate information associated with

the same. Therefore, if the company is unaware of such a scenario, material misstatement

can incur, thereby affecting the decision-making on the part of auditors.

Another analytical process that can be implemented in the case of DIPL is by making a

comparison of the financial information of present year with that of the previous years.

Besides, such comparison of the current year can also be conducted with the forecasts for

future or with an industry engaged in the similar line of business (Guan et. al, 2008).

With the help of this comparison, the variations in patterns can be taken into account to

make relevant decisions for deciding the future course of action.

The relevance of using trend can be attributed to the fact that the alterations in accounts

can be taken into consideration for making effective decisions. Besides, the reason behind

such alterations can also be known and evaluated respectively. For instance, trend

analysis can be conducted by making a comparison of sales with that of previous years in

order to evaluate the increase or decrease in patterns. Hence, if there is a decrease in

2

Audit

sales, it is not a good sign for the company. Similarly, if there is an enhancement in sales

figures, it is a good indicator but the auditor must cautiously observe any significant

increase in amounts because it may either be influenced or occurred due to some error. It

is therefore vital that the auditor take relevant steps to verify the sales amount from the

authenticated documents. Furthermore, such comparison can also be conducted with

companies engaged in the similar line of businesses so that variations can again be

evaluated to identify management problems that persist owing to decline in patterns

(Cappelleto, 2010).

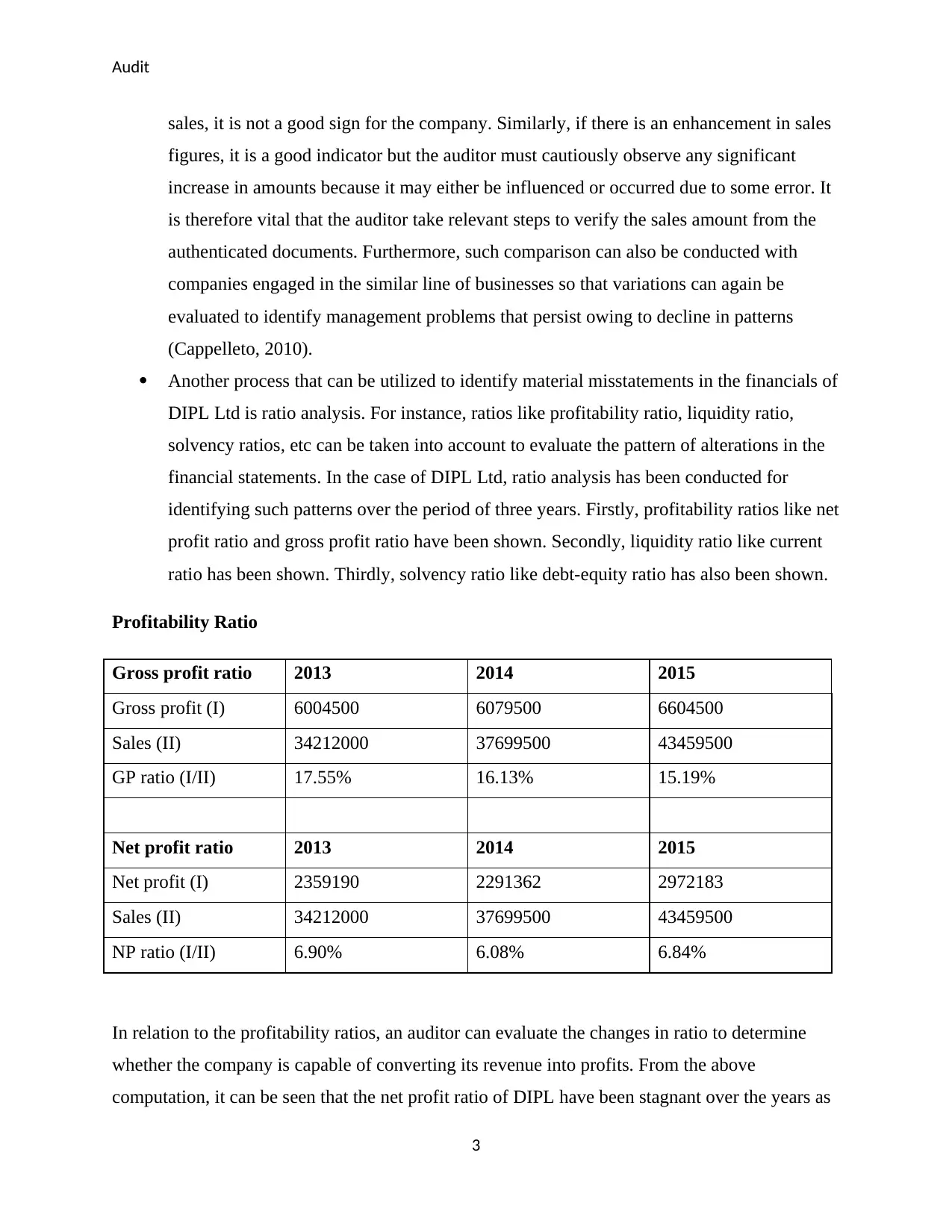

Another process that can be utilized to identify material misstatements in the financials of

DIPL Ltd is ratio analysis. For instance, ratios like profitability ratio, liquidity ratio,

solvency ratios, etc can be taken into account to evaluate the pattern of alterations in the

financial statements. In the case of DIPL Ltd, ratio analysis has been conducted for

identifying such patterns over the period of three years. Firstly, profitability ratios like net

profit ratio and gross profit ratio have been shown. Secondly, liquidity ratio like current

ratio has been shown. Thirdly, solvency ratio like debt-equity ratio has also been shown.

Profitability Ratio

Gross profit ratio 2013 2014 2015

Gross profit (I) 6004500 6079500 6604500

Sales (II) 34212000 37699500 43459500

GP ratio (I/II) 17.55% 16.13% 15.19%

Net profit ratio 2013 2014 2015

Net profit (I) 2359190 2291362 2972183

Sales (II) 34212000 37699500 43459500

NP ratio (I/II) 6.90% 6.08% 6.84%

In relation to the profitability ratios, an auditor can evaluate the changes in ratio to determine

whether the company is capable of converting its revenue into profits. From the above

computation, it can be seen that the net profit ratio of DIPL have been stagnant over the years as

3

sales, it is not a good sign for the company. Similarly, if there is an enhancement in sales

figures, it is a good indicator but the auditor must cautiously observe any significant

increase in amounts because it may either be influenced or occurred due to some error. It

is therefore vital that the auditor take relevant steps to verify the sales amount from the

authenticated documents. Furthermore, such comparison can also be conducted with

companies engaged in the similar line of businesses so that variations can again be

evaluated to identify management problems that persist owing to decline in patterns

(Cappelleto, 2010).

Another process that can be utilized to identify material misstatements in the financials of

DIPL Ltd is ratio analysis. For instance, ratios like profitability ratio, liquidity ratio,

solvency ratios, etc can be taken into account to evaluate the pattern of alterations in the

financial statements. In the case of DIPL Ltd, ratio analysis has been conducted for

identifying such patterns over the period of three years. Firstly, profitability ratios like net

profit ratio and gross profit ratio have been shown. Secondly, liquidity ratio like current

ratio has been shown. Thirdly, solvency ratio like debt-equity ratio has also been shown.

Profitability Ratio

Gross profit ratio 2013 2014 2015

Gross profit (I) 6004500 6079500 6604500

Sales (II) 34212000 37699500 43459500

GP ratio (I/II) 17.55% 16.13% 15.19%

Net profit ratio 2013 2014 2015

Net profit (I) 2359190 2291362 2972183

Sales (II) 34212000 37699500 43459500

NP ratio (I/II) 6.90% 6.08% 6.84%

In relation to the profitability ratios, an auditor can evaluate the changes in ratio to determine

whether the company is capable of converting its revenue into profits. From the above

computation, it can be seen that the net profit ratio of DIPL have been stagnant over the years as

3

Audit

it does not change significantly. This depicts that the company has been effective in this segment

(Guerard, 2013). However, the gross profit ratio has shown a declining trend over these years

that is not a good sign for the company in relation to profitability.

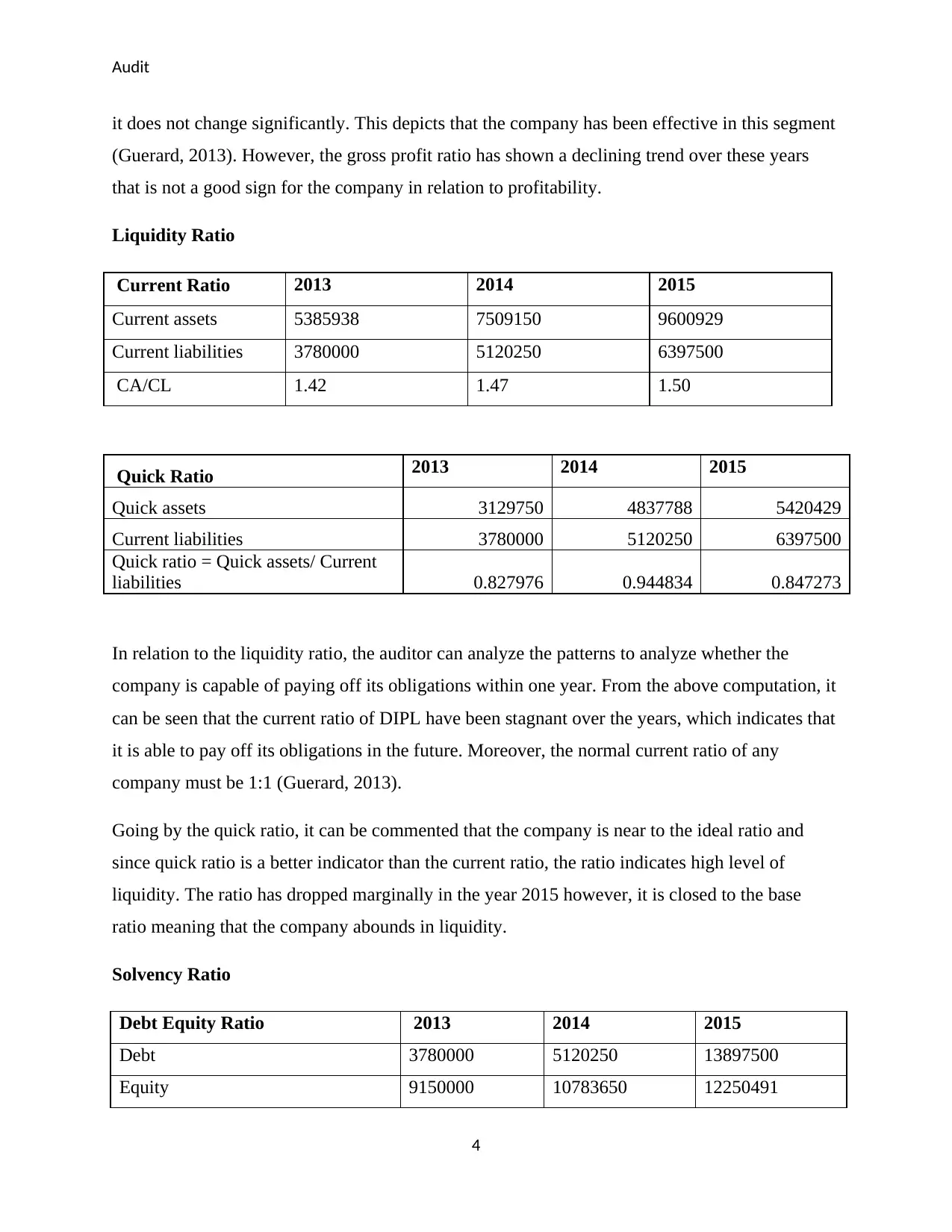

Liquidity Ratio

Current Ratio 2013 2014 2015

Current assets 5385938 7509150 9600929

Current liabilities 3780000 5120250 6397500

CA/CL 1.42 1.47 1.50

Quick Ratio 2013 2014 2015

Quick assets 3129750 4837788 5420429

Current liabilities 3780000 5120250 6397500

Quick ratio = Quick assets/ Current

liabilities 0.827976 0.944834 0.847273

In relation to the liquidity ratio, the auditor can analyze the patterns to analyze whether the

company is capable of paying off its obligations within one year. From the above computation, it

can be seen that the current ratio of DIPL have been stagnant over the years, which indicates that

it is able to pay off its obligations in the future. Moreover, the normal current ratio of any

company must be 1:1 (Guerard, 2013).

Going by the quick ratio, it can be commented that the company is near to the ideal ratio and

since quick ratio is a better indicator than the current ratio, the ratio indicates high level of

liquidity. The ratio has dropped marginally in the year 2015 however, it is closed to the base

ratio meaning that the company abounds in liquidity.

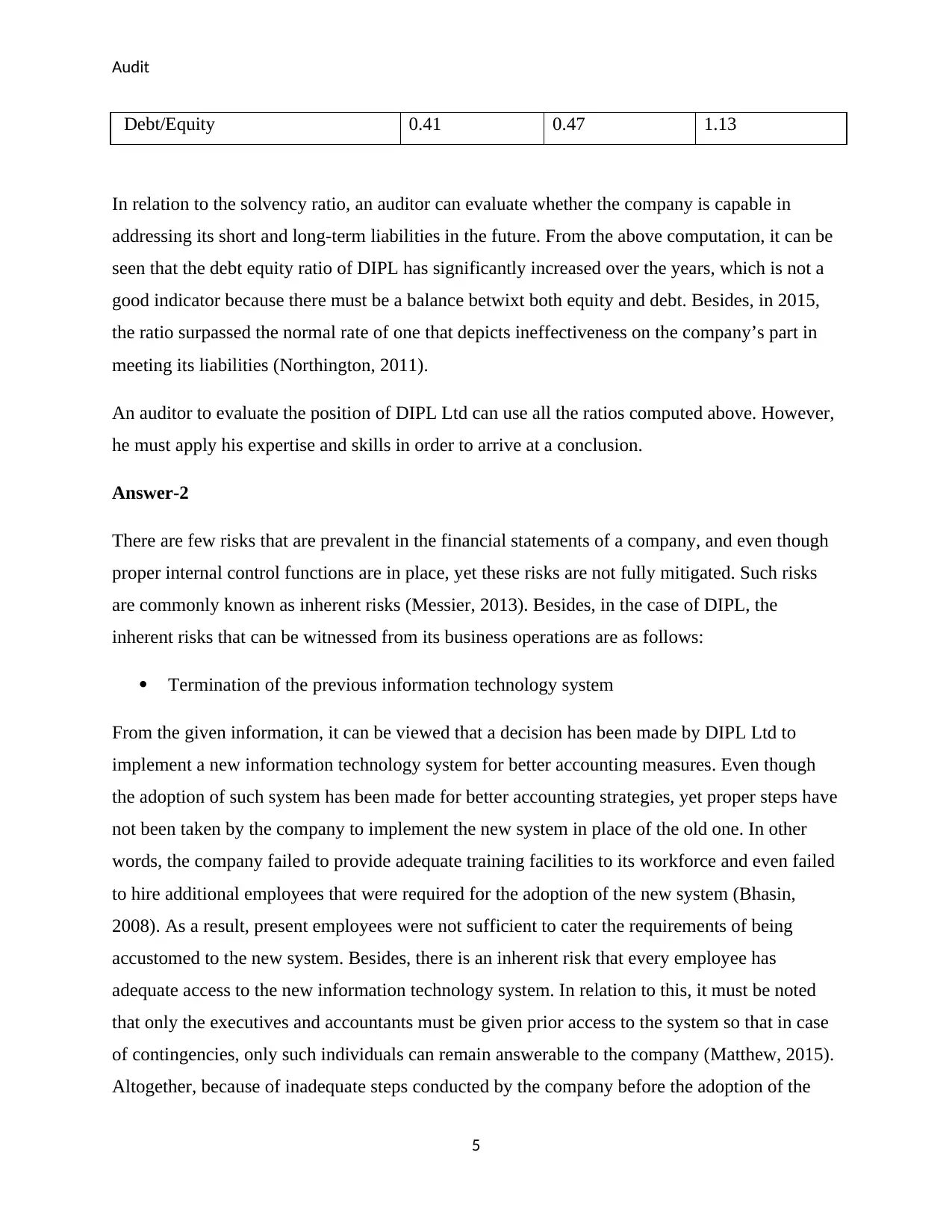

Solvency Ratio

Debt Equity Ratio 2013 2014 2015

Debt 3780000 5120250 13897500

Equity 9150000 10783650 12250491

4

it does not change significantly. This depicts that the company has been effective in this segment

(Guerard, 2013). However, the gross profit ratio has shown a declining trend over these years

that is not a good sign for the company in relation to profitability.

Liquidity Ratio

Current Ratio 2013 2014 2015

Current assets 5385938 7509150 9600929

Current liabilities 3780000 5120250 6397500

CA/CL 1.42 1.47 1.50

Quick Ratio 2013 2014 2015

Quick assets 3129750 4837788 5420429

Current liabilities 3780000 5120250 6397500

Quick ratio = Quick assets/ Current

liabilities 0.827976 0.944834 0.847273

In relation to the liquidity ratio, the auditor can analyze the patterns to analyze whether the

company is capable of paying off its obligations within one year. From the above computation, it

can be seen that the current ratio of DIPL have been stagnant over the years, which indicates that

it is able to pay off its obligations in the future. Moreover, the normal current ratio of any

company must be 1:1 (Guerard, 2013).

Going by the quick ratio, it can be commented that the company is near to the ideal ratio and

since quick ratio is a better indicator than the current ratio, the ratio indicates high level of

liquidity. The ratio has dropped marginally in the year 2015 however, it is closed to the base

ratio meaning that the company abounds in liquidity.

Solvency Ratio

Debt Equity Ratio 2013 2014 2015

Debt 3780000 5120250 13897500

Equity 9150000 10783650 12250491

4

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

Audit

Debt/Equity 0.41 0.47 1.13

In relation to the solvency ratio, an auditor can evaluate whether the company is capable in

addressing its short and long-term liabilities in the future. From the above computation, it can be

seen that the debt equity ratio of DIPL has significantly increased over the years, which is not a

good indicator because there must be a balance betwixt both equity and debt. Besides, in 2015,

the ratio surpassed the normal rate of one that depicts ineffectiveness on the company’s part in

meeting its liabilities (Northington, 2011).

An auditor to evaluate the position of DIPL Ltd can use all the ratios computed above. However,

he must apply his expertise and skills in order to arrive at a conclusion.

Answer-2

There are few risks that are prevalent in the financial statements of a company, and even though

proper internal control functions are in place, yet these risks are not fully mitigated. Such risks

are commonly known as inherent risks (Messier, 2013). Besides, in the case of DIPL, the

inherent risks that can be witnessed from its business operations are as follows:

Termination of the previous information technology system

From the given information, it can be viewed that a decision has been made by DIPL Ltd to

implement a new information technology system for better accounting measures. Even though

the adoption of such system has been made for better accounting strategies, yet proper steps have

not been taken by the company to implement the new system in place of the old one. In other

words, the company failed to provide adequate training facilities to its workforce and even failed

to hire additional employees that were required for the adoption of the new system (Bhasin,

2008). As a result, present employees were not sufficient to cater the requirements of being

accustomed to the new system. Besides, there is an inherent risk that every employee has

adequate access to the new information technology system. In relation to this, it must be noted

that only the executives and accountants must be given prior access to the system so that in case

of contingencies, only such individuals can remain answerable to the company (Matthew, 2015).

Altogether, because of inadequate steps conducted by the company before the adoption of the

5

Debt/Equity 0.41 0.47 1.13

In relation to the solvency ratio, an auditor can evaluate whether the company is capable in

addressing its short and long-term liabilities in the future. From the above computation, it can be

seen that the debt equity ratio of DIPL has significantly increased over the years, which is not a

good indicator because there must be a balance betwixt both equity and debt. Besides, in 2015,

the ratio surpassed the normal rate of one that depicts ineffectiveness on the company’s part in

meeting its liabilities (Northington, 2011).

An auditor to evaluate the position of DIPL Ltd can use all the ratios computed above. However,

he must apply his expertise and skills in order to arrive at a conclusion.

Answer-2

There are few risks that are prevalent in the financial statements of a company, and even though

proper internal control functions are in place, yet these risks are not fully mitigated. Such risks

are commonly known as inherent risks (Messier, 2013). Besides, in the case of DIPL, the

inherent risks that can be witnessed from its business operations are as follows:

Termination of the previous information technology system

From the given information, it can be viewed that a decision has been made by DIPL Ltd to

implement a new information technology system for better accounting measures. Even though

the adoption of such system has been made for better accounting strategies, yet proper steps have

not been taken by the company to implement the new system in place of the old one. In other

words, the company failed to provide adequate training facilities to its workforce and even failed

to hire additional employees that were required for the adoption of the new system (Bhasin,

2008). As a result, present employees were not sufficient to cater the requirements of being

accustomed to the new system. Besides, there is an inherent risk that every employee has

adequate access to the new information technology system. In relation to this, it must be noted

that only the executives and accountants must be given prior access to the system so that in case

of contingencies, only such individuals can remain answerable to the company (Matthew, 2015).

Altogether, because of inadequate steps conducted by the company before the adoption of the

5

Audit

new system, few accounting figures were not recorded in the new system, and that might have

affected the financial statements on a bad note (Cappelleto, 2010).

Appointment being done by person possessing financial interest

In relation to the available business information of DIPL Ltd, it can be viewed that the fresh

appointment of the Chief Executive Officer is not an effective one because he pursues a financial

interest with the company. The reason behind such financial interest can be attributed to the fact

that such CEO has been granted an opportunity wherein he will attain a ten percent share in the

profits of the company if a growth of more than ten percent revenues can be witnessed. The

inherent risk prevalent in this case is that the CEO is in a position wherein he will endeavor to

enhance the revenues of the company, and for such purpose, he might make use of fraudulent

ways to manipulate the accounts so that an enhancement in revenues can be witnessed (Hoffelder

2012). In addition to this, such CEO has taken steps to appoint an internal audit team for the

company who is under his control and may work under him to hide the manipulation being done

in the company financials. Therefore, this is also another inherent risk for DIPL Ltd that can play

a key role in altering the planning decisions. Nevertheless, in relation to this, if the CEO had not

appointed the internal audit team and instead, the Board would have undertaken such task, such

risk would not have incurred (Parker et. al, 2011).

Therefore, these two inherent risks pose a big threat to the effective functioning of the company,

and corrective actions must be immediately implemented so that such risks do not hamper the

entire business operations.

6

new system, few accounting figures were not recorded in the new system, and that might have

affected the financial statements on a bad note (Cappelleto, 2010).

Appointment being done by person possessing financial interest

In relation to the available business information of DIPL Ltd, it can be viewed that the fresh

appointment of the Chief Executive Officer is not an effective one because he pursues a financial

interest with the company. The reason behind such financial interest can be attributed to the fact

that such CEO has been granted an opportunity wherein he will attain a ten percent share in the

profits of the company if a growth of more than ten percent revenues can be witnessed. The

inherent risk prevalent in this case is that the CEO is in a position wherein he will endeavor to

enhance the revenues of the company, and for such purpose, he might make use of fraudulent

ways to manipulate the accounts so that an enhancement in revenues can be witnessed (Hoffelder

2012). In addition to this, such CEO has taken steps to appoint an internal audit team for the

company who is under his control and may work under him to hide the manipulation being done

in the company financials. Therefore, this is also another inherent risk for DIPL Ltd that can play

a key role in altering the planning decisions. Nevertheless, in relation to this, if the CEO had not

appointed the internal audit team and instead, the Board would have undertaken such task, such

risk would not have incurred (Parker et. al, 2011).

Therefore, these two inherent risks pose a big threat to the effective functioning of the company,

and corrective actions must be immediately implemented so that such risks do not hamper the

entire business operations.

6

Audit

Answer-3(a)

There are two fraud risks that are prevalent in the financials of DIPL Ltd and that may affect its

smooth flow of operations.

After the adoption of the new system, it was visible that prior steps were not undertaken

by the company to terminate the previous system. As a result, many entries that were

conducted last year were not recorded in the new accounting system. However, this fraud

might have been done because of fraudulent intention of the managers or the accountants

so that the accounting figures could be manipulated and the accounts department could be

easily misled (Elder et. al, 2010). This mentioned fraud risk could also be witnessed in

the financial statement of DIPL Ltd since its cash balances have depicted a major fall in

the year 2015. Since no other reason behind the decline in cash can be witnessed; such

risk appropriately suits the scenario.

The second fraud risk that can be viewed in the financials of DIPL is the significant

increment in the level of inventories. The reason why this increment is aligned to a fraud

risk is that the level of sales was also immense over the years, which means that the

inventories must depict a declining figure but instead, it depicted an upwards trend that

raises dubiousness (Arens et. al, 2013). Therefore, it may be possible that the

management fraudulently enhanced its level of inventories in the financial statements so

that an increased amount of profits can also be shown.

Answer-3(b)

If the fraudulent practices mentioned above have been done either by the management or with

the permission of the management, not only the quality of audit but also the opinion of auditor

will be badly influenced. In relation to the first fraud risk, it may happen that the entries that

were not recorded in the new accounting system were of big amounts, thereby creating a big

complication for the auditor to detect the same (Arens et. al, 2013). This is because the auditor

might require some time to get accustomed to the new system and he may not find detection of

amounts from the old system. Thus, the audit report will be influenced due to such fraud. In

relation to the second fraud risk mentioned above, if the amounts of inventories had been

enhanced by the management in order to depict high profits in the income statement, it may

7

Answer-3(a)

There are two fraud risks that are prevalent in the financials of DIPL Ltd and that may affect its

smooth flow of operations.

After the adoption of the new system, it was visible that prior steps were not undertaken

by the company to terminate the previous system. As a result, many entries that were

conducted last year were not recorded in the new accounting system. However, this fraud

might have been done because of fraudulent intention of the managers or the accountants

so that the accounting figures could be manipulated and the accounts department could be

easily misled (Elder et. al, 2010). This mentioned fraud risk could also be witnessed in

the financial statement of DIPL Ltd since its cash balances have depicted a major fall in

the year 2015. Since no other reason behind the decline in cash can be witnessed; such

risk appropriately suits the scenario.

The second fraud risk that can be viewed in the financials of DIPL is the significant

increment in the level of inventories. The reason why this increment is aligned to a fraud

risk is that the level of sales was also immense over the years, which means that the

inventories must depict a declining figure but instead, it depicted an upwards trend that

raises dubiousness (Arens et. al, 2013). Therefore, it may be possible that the

management fraudulently enhanced its level of inventories in the financial statements so

that an increased amount of profits can also be shown.

Answer-3(b)

If the fraudulent practices mentioned above have been done either by the management or with

the permission of the management, not only the quality of audit but also the opinion of auditor

will be badly influenced. In relation to the first fraud risk, it may happen that the entries that

were not recorded in the new accounting system were of big amounts, thereby creating a big

complication for the auditor to detect the same (Arens et. al, 2013). This is because the auditor

might require some time to get accustomed to the new system and he may not find detection of

amounts from the old system. Thus, the audit report will be influenced due to such fraud. In

relation to the second fraud risk mentioned above, if the amounts of inventories had been

enhanced by the management in order to depict high profits in the income statement, it may

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit

result in inappropriateness because such figures of profits are hypothetical and not the real ones

(Heeler, 2009). Therefore, if the auditor does not take proper steps to identify the same, there

will be material misstatements in the financials of DIPL and as a result, he may prove incapable

in ascertaining the truthfulness and completeness of the company financials (Jubb, 2012).

Thus, it is relevant to know that the auditor is under an obligation to take into consideration

every aspect of the financials so that the truthfulness can be ascertained. Moreover, if he does not

prove capable of detecting the risks, a true and fair view of the company’s performance cannot

be obtained.

8

result in inappropriateness because such figures of profits are hypothetical and not the real ones

(Heeler, 2009). Therefore, if the auditor does not take proper steps to identify the same, there

will be material misstatements in the financials of DIPL and as a result, he may prove incapable

in ascertaining the truthfulness and completeness of the company financials (Jubb, 2012).

Thus, it is relevant to know that the auditor is under an obligation to take into consideration

every aspect of the financials so that the truthfulness can be ascertained. Moreover, if he does not

prove capable of detecting the risks, a true and fair view of the company’s performance cannot

be obtained.

8

Audit

References

Arens, A. A, Best, P. J, Shailer, G. E. P & Loebbecke, J. K, 2013, Assurance Services and

Ethics in Australia, 9th ed, Australia: Pearson.

Bhasin, M. L 2008, ‘Corporate Governance and Role of the Forensic Accountant’, The

Chartered Secretary Journal, vol. 38, no. 10, pp. 1361-1368.

Cappelleto, G. 2010, Challenges Facing Accounting Education in Australia, AFAANZ,

Elder, J. R, Beasley S. M.& Arens A. A 2010, Auditing and Assurance Services, Person

Ghandar, A & Tsahuridu, E 2013, The Auditing Handbook 2013, Australia: Pearson.

Guan, L, Kaminski, K. A & Wetzel, T. S 2008, ‘Can Investors Detect Fraud Using Financial

Statements: An Exploratory Study’, Advances in Public Interest Accounting vol. 13, pp. 17-34.

Guerard, J 2013, Introduction to financial forecasting in investment analysis, New York, NY:

Springer, pp. 78-81

Heeler, D 2009, Audit Principles, Risk Assessment & Effective Reporting. Pearson Press

Hoffelder, K 2012, New Audit Standard Encourages More Talking, Harvard Press.

Jubb, C 2012, Auditing: A Business Risk Approach, Australia: Cengage

Matthew S. E 2015, ‘ Does Internal Audit Function Quality Deter Management Misconduct?’,

The Accounting Review, vol. 90, no. 2, pp. 495-527

Messier, F. W 2013, Auditing and Assurance Services - A systematic approach, 9th ed.

Australia: McGraw Hill.

Northington, S 2011, Finance, New York, NY: Ferguson's, pp. 52-55

Parker, L, Guthrie, J & Linacre, S 2011, The relationship between academic

accounting research and professional practice, Accounting , Auditing & Accountability

Journal, vol. 24, no. 1, pp. 5-14.

9

References

Arens, A. A, Best, P. J, Shailer, G. E. P & Loebbecke, J. K, 2013, Assurance Services and

Ethics in Australia, 9th ed, Australia: Pearson.

Bhasin, M. L 2008, ‘Corporate Governance and Role of the Forensic Accountant’, The

Chartered Secretary Journal, vol. 38, no. 10, pp. 1361-1368.

Cappelleto, G. 2010, Challenges Facing Accounting Education in Australia, AFAANZ,

Elder, J. R, Beasley S. M.& Arens A. A 2010, Auditing and Assurance Services, Person

Ghandar, A & Tsahuridu, E 2013, The Auditing Handbook 2013, Australia: Pearson.

Guan, L, Kaminski, K. A & Wetzel, T. S 2008, ‘Can Investors Detect Fraud Using Financial

Statements: An Exploratory Study’, Advances in Public Interest Accounting vol. 13, pp. 17-34.

Guerard, J 2013, Introduction to financial forecasting in investment analysis, New York, NY:

Springer, pp. 78-81

Heeler, D 2009, Audit Principles, Risk Assessment & Effective Reporting. Pearson Press

Hoffelder, K 2012, New Audit Standard Encourages More Talking, Harvard Press.

Jubb, C 2012, Auditing: A Business Risk Approach, Australia: Cengage

Matthew S. E 2015, ‘ Does Internal Audit Function Quality Deter Management Misconduct?’,

The Accounting Review, vol. 90, no. 2, pp. 495-527

Messier, F. W 2013, Auditing and Assurance Services - A systematic approach, 9th ed.

Australia: McGraw Hill.

Northington, S 2011, Finance, New York, NY: Ferguson's, pp. 52-55

Parker, L, Guthrie, J & Linacre, S 2011, The relationship between academic

accounting research and professional practice, Accounting , Auditing & Accountability

Journal, vol. 24, no. 1, pp. 5-14.

9

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.