HI6026 - Audit and Assurance

Added on 2020-03-01

9 Pages2740 Words51 Views

AUDIT & ASSURANCE

AuditAnswer-1There are several types of analytical processes that can be applied in order to make both financialand non-financial decisions of the company. When it comes to the background information of DIPL Ltd, the same processes can play a key role in ascertaining whether the data forming part of its financial statements depict a true and fair view of its performance. In other words, analytical processes can prove to be of immense benefit in identifying any material misstatements prevalent in the financials of a company (Ghandar & Tsahuridu, 2013). Moreover,making use of such analytical procedures can assist an auditor to perform the audit process with more ease and effectiveness. There are many types of analytical processes that can be used in this regard, and it depends upon an auditor to ascertain which process is more suitable for performing the audit function.In the given case of DIPL Ltd, the following analytical processes can be taken into account:There may be a probability that the figures incorporated in the accounts of creditors and debtors are not appropriately settled or collected by the officials of the company. Therefore, it is important to verify the balances of the accounts of debtors and creditors so that any inaccuracies, which are present, can be mitigated to the fullest. Besides, it may happen that the company does not have any adequate information associated with the same. Therefore, if the company is unaware of such a scenario, material misstatementcan incur, thereby affecting the decision-making on the part of auditors.Another analytical process that can be implemented in the case of DIPL is by making a comparison of the financial information of present year with that of the previous years. Besides, such comparison of the current year can also be conducted with the forecasts for future or with an industry engaged in the similar line of business (Guan et. al, 2008). With the help of this comparison, the variations in patterns can be taken into account to make relevant decisions for deciding the future course of action.The relevance of using trend can be attributed to the fact that the alterations in accounts can be taken into consideration for making effective decisions. Besides, the reason behindsuch alterations can also be known and evaluated respectively. For instance, trend analysis can be conducted by making a comparison of sales with that of previous years in order to evaluate the increase or decrease in patterns. Hence, if there is a decrease in 2

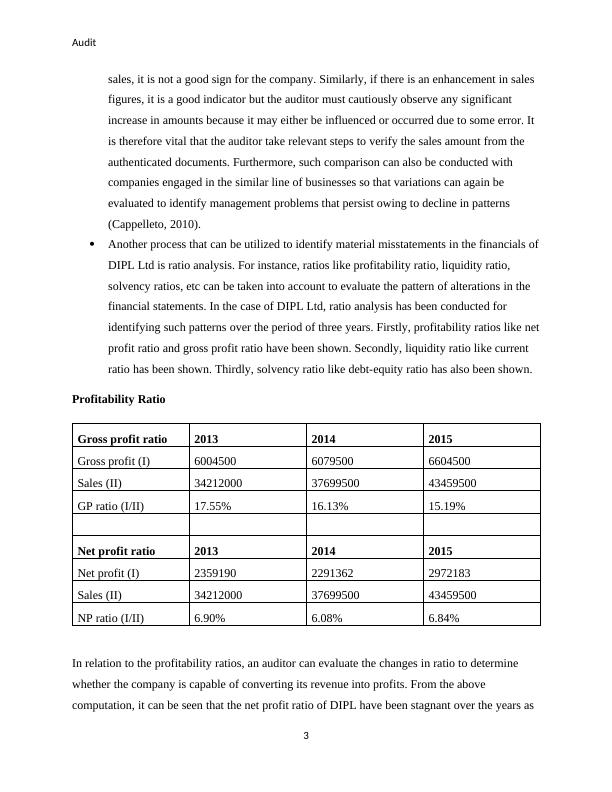

Auditsales, it is not a good sign for the company. Similarly, if there is an enhancement in sales figures, it is a good indicator but the auditor must cautiously observe any significant increase in amounts because it may either be influenced or occurred due to some error. It is therefore vital that the auditor take relevant steps to verify the sales amount from the authenticated documents. Furthermore, such comparison can also be conducted with companies engaged in the similar line of businesses so that variations can again be evaluated to identify management problems that persist owing to decline in patterns (Cappelleto, 2010).Another process that can be utilized to identify material misstatements in the financials ofDIPL Ltd is ratio analysis. For instance, ratios like profitability ratio, liquidity ratio, solvency ratios, etc can be taken into account to evaluate the pattern of alterations in the financial statements. In the case of DIPL Ltd, ratio analysis has been conducted for identifying such patterns over the period of three years. Firstly, profitability ratios like netprofit ratio and gross profit ratio have been shown. Secondly, liquidity ratio like current ratio has been shown. Thirdly, solvency ratio like debt-equity ratio has also been shown.Profitability RatioGross profit ratio201320142015Gross profit (I)600450060795006604500Sales (II)342120003769950043459500GP ratio (I/II)17.55%16.13%15.19%Net profit ratio201320142015Net profit (I)235919022913622972183Sales (II)342120003769950043459500NP ratio (I/II)6.90%6.08%6.84%In relation to the profitability ratios, an auditor can evaluate the changes in ratio to determine whether the company is capable of converting its revenue into profits. From the above computation, it can be seen that the net profit ratio of DIPL have been stagnant over the years as 3

End of preview

Want to access all the pages? Upload your documents or become a member.

Related Documents

HI6026 Audit, Assurance and Compliancelg...

|11

|2704

|27

Auditing and Assurance Services- Project Reportlg...

|10

|2670

|156

Audit, Assurance and Compliance | HI6026lg...

|9

|1848

|17

Assignment On Audit & Assurance- DIPL Ltdlg...

|9

|2061

|48

HI6026 - Audit, Assurance Compliancelg...

|9

|2492

|68

HI6026| The Audit, Assurance and Compliancelg...

|10

|2217

|43